Sample Category Title

Global Markets Are Fairly Quiet This Morning

Market movers today

This morning markets will digest the results of the German election yesterday.

The fourth round of Brexit negot iat ions begins today. Theresa May's speech in Florence on Friday did not reveal much news after the leaks on Thursday evening.

In Germany, the Ifo business confidence for September is expected to show a further increase and add to the upbeat picture of the euro area witnessed in the PMI data last week.

The Fed's Vice-Chairman Bill Dudley (voter, dove) is set to speak but the theme is workforce development , so it is not clear if he will touch on monetary policy. The Fed's Evans is due to speak tonight on the economy and monetary policy. The ECB speeches from Mario Draghi, Yves Mersch and Benoît Coeuré are also due today.

Later this week, focus will turn to euro inflation and Chinese PMI. In Scandi, the most interesting releases will be Swedish NIER business confidence and Norwegian unemployment.

Selected market news

Global markets are fairly quiet this morning. US yields are trading close to Friday levels and the S&P 500 equity future is around the S&P500 closing level on Friday. Chinese stocks have taken a small hit as developers are under pressure from new housing restrictions in eight cities in a move to cool the housing market further.

Angela Merkel secured her fourth term in office as her Conservat ives (CDU/CSU) remained the largest party with 33.0% in yest erday's elect ion, followed by the Social Democrats (SPD) at 20.5%. However, both parties registered significant losses in their vote shares to the benefit of the euro-scept ic AfD party, which will become the first right -wing nat ionalist party to enter the Bundestag since the 1950s with a vote share of 12.6%. The outcome now leaves only two viable coalition possibilities that can obtain a majority: Another grand coalition of CDU/CSU and SPD or a ‘Jamaica' coalit ion of CDU, FDP and the Greens. However, as the SPD leadership currently rules out another grand coalit ion under Merkel because of its disappoint ing elect ion result , a Jamaica coalition seems increasingly likely, in our view. Wit h t he ‘illegal' Cat alonian referendum this weekend and an Italian general elect ion looming, where the Five Star Movement stands to be a serious competitor for the premier minister posit ion, European political woes might well become a market driver once again.

On Friday, the ECB's Vítor Constâncio played down the effect of the euro appreciation saying it might have a smaller effect on inflat ion than usual, based on recent ECB research. He also referred to a slight steepening of the Philips curve recently, saying t his gives ‘some hope that the future closing of the output gap will allow us to gradually reach our inflation target '.

Japan PMI manufacturing for September rose to 52.6 from 52.2 and continues to signal robust manufacturing growth in line with most other regions. It adds to the picture of st ill strong global growth in H2. Japan 's Prime Minister Shinzo Abe is expected to announce snap elections on Monday to take advantage of improved ratings.

Daily Technical Analysis: EUR/USD, GBP/USD Build Key Sideways Correction And Chart Patterns

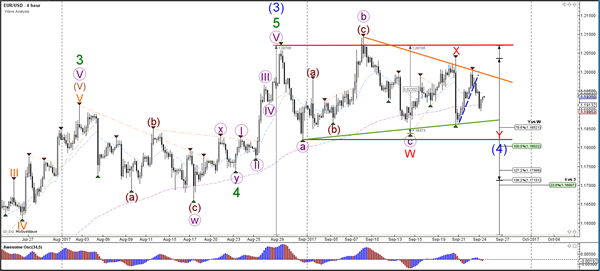

Currency pair EUR/USD

The EUR/USD is moving sideways as price stays in between support (green) and resistance (red) trend lines. The overall trend however is up and a bearish break could stop at the Fibonacci support levels of wave 4 (blue). A bullish breakout could indicate that the WXY (red) correction is finished.

The EUR/USD is in a triangle chart pattern which is indicated by the trend lines. Price is in a wave C (purple) of wave Y (red) unless price manages to break above resistance (red). In that case, the wave C is most likely completed at the most recent bottom.

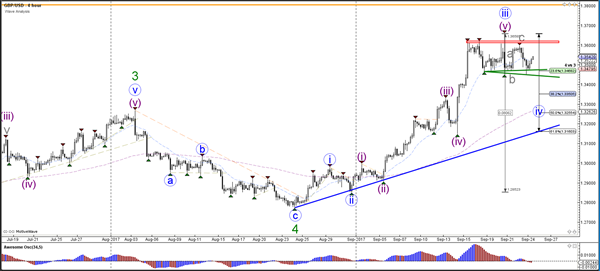

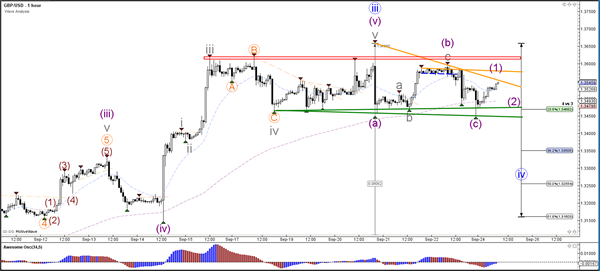

Currency pair GBP/USD

The GBP/USD is also in a sideways range (red/green lines) within a larger uptrend. A break below support could see price challenge the 38.2% Fibonacci level of wave 4 vs 3. A break above resistance could see price continue with the trend.

The GBP/USD needs to breakout below support (green) or above resistance (red/orange) otherwise the sideways range remains valid.

Currency pair USD/JPY

The USD/JPY is testing a support trend line (green) of the uptrend channel.

The USD/JPY needs to break above resistance (orange) before an uptrend continuation is likely. A break below support (blue) could confirm an ABC (blue) correction.

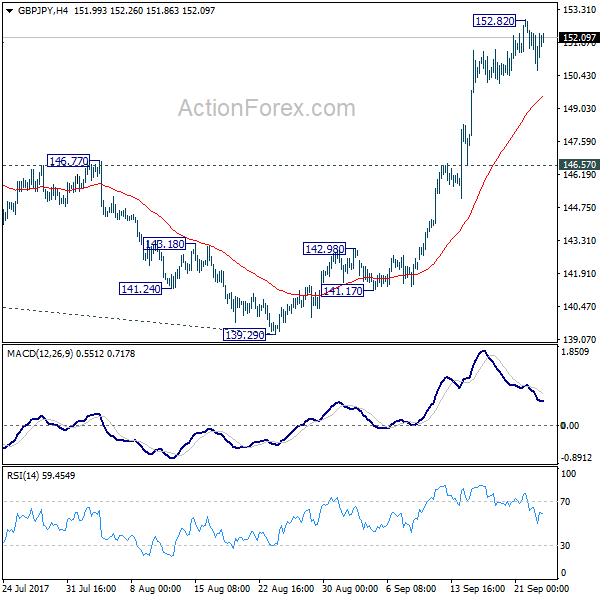

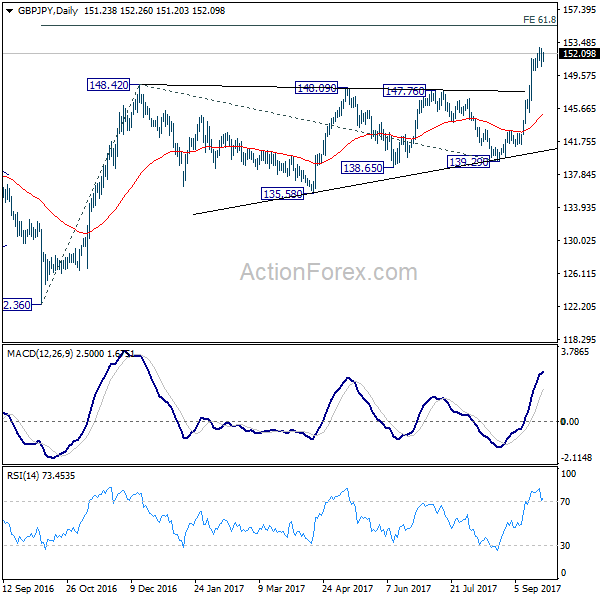

GBP/JPY Daily Outlook

Daily Pivots: (S1) 150.18; (P) 151.48; (R1) 152.32; More

Intraday bias in GBP/JPY remains neutral for consolidation below 152.82. Downside of retreat should be contained above 146.57 support to bring another rally. Above 152.82 will target 61.8% projection of 122.36 to 148.42 from 139.29 at 155.39 next.

In the bigger picture, medium term rebound from 122.36 is in progress. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. For now, the bullish scenario is preferred as long as 139.29 support holds.

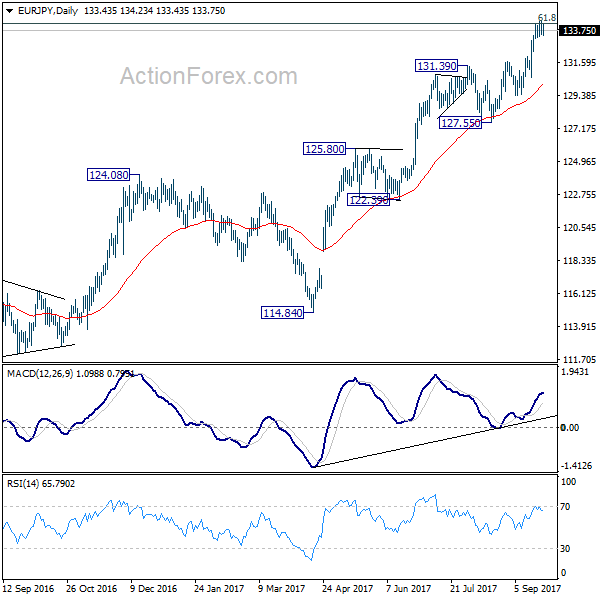

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.68; (P) 134.03; (R1) 134.66; More...

Intraday bias in EUR/JPY remains neutral for the moment. More consolidations could be seen. But outlook remain bullish as long as 131.69 resistance turned support holds. Sustained break of 134.20 fibonacci level will target 141.04 resistance next.

In the bigger picture, current rise from 109.03 is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. On the downside, break of 127.55 support is needed to be the first signal of medium term reversal. Otherwise, outlook will remain bullish.

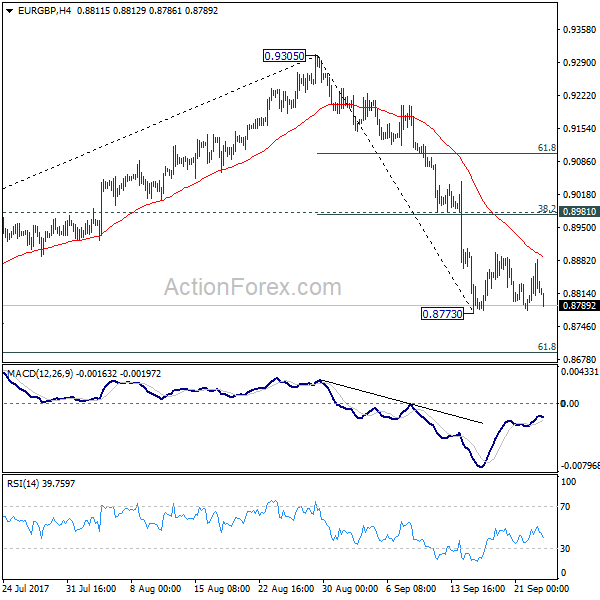

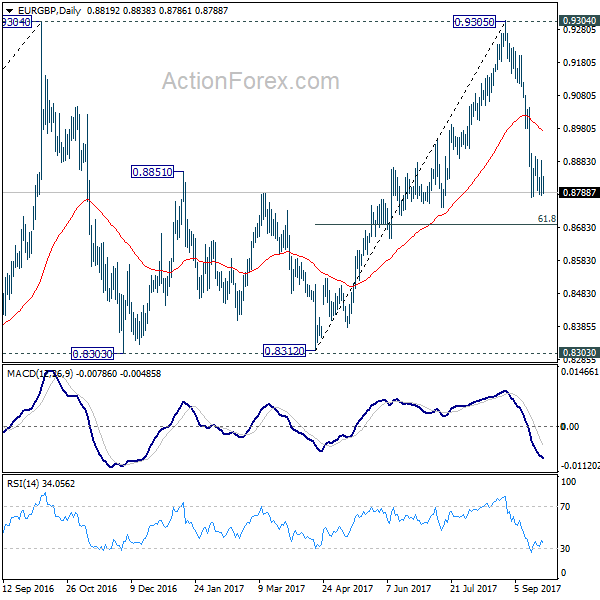

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8796; (P) 0.8839; (R1) 0.8892; More

EUR/GBP is staying above 0.8773 low and intraday bias remains neutral for the moment. More consolidations could be seen. But near term outlook stays bearish as long as 0.8981 cluster resistance holds (38.2% retracement of 0.9305 to 0.8773 at 0.8976). Fall from 0.9305 is seen as the third leg of consolidation pattern from 0.9304. Below 0.8773 will target 61.8% retracement of 0.8312 to 0.9305 at 0.8691 and below. We'll look for bottoming signal again at it approaches 0.8303 support.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's still in progress with fall from 0.9305 as the third leg. Break of 0.8303 could be seen. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

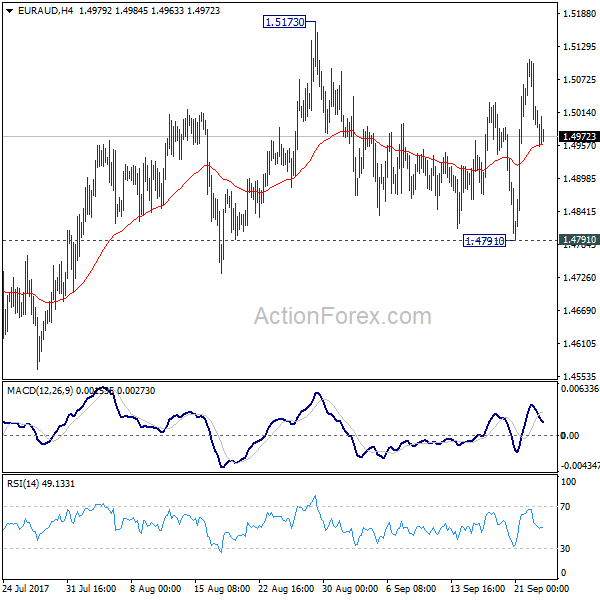

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4952; (P) 1.5030; (R1) 1.5071; More....

Intraday bias in EUR/AUD remains neutral for consolidation inside range of 1.4791/5173. On the upside, break of 1.5173/5226 resistance zone will finally resume larger rise from 1.3624. On the downside, break of 1.4791 support will turn bias to the downside and extend the fall from 1.5173 to retest 1.4421 support.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. The corrective structure of the price actions from 1.5226 is affirming this view. Above 1.5226 will target a test on 1.6587 key resistance. However, break of 1.4421 support will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

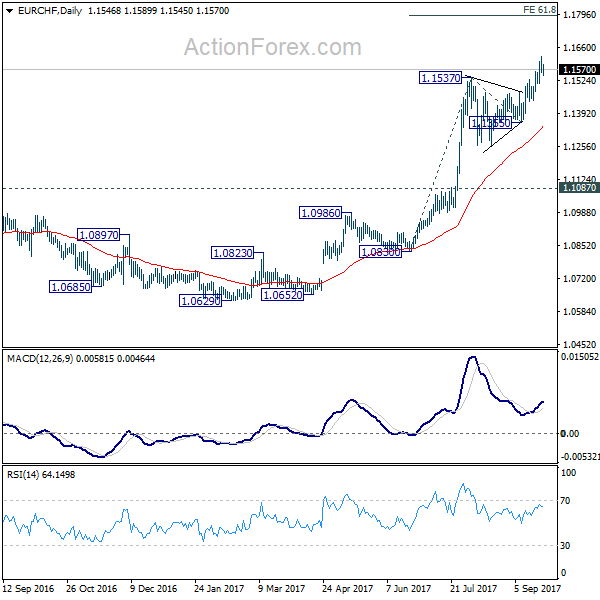

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1548; (P) 1.1586; (R1) 1.1612; More... .

With 1.1511 minor support intact, further rise is expected in EUR/CHF. Current rally would target 61.8% projection of 1.0830 to 1.1537 from 1.1355 at 1.1792 next. On the downside, below 1.1511 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1198 resistance turned support holds.

New Zealand General Election: Economics Clouded By Politics

While the final result would be formally announced on October 7 (due to the complex arithmetic of the mixed-member proportion system), the available information confirmed that the centre-right National Party remains the biggest party but would again be shy of being a majority government. Worse still, it would also be challenging for Nationals to form a minority government with consent of smaller parities. While many believe that the most likely result would be a Nationals+ NZ First coalition, it is not yet a done deal as it is still possible for NZ First form a coalition government with centre-left Labors and left-wing Greens. With plenty of uncertainties remains and the populist NZ First likely be a kingmaker in this term, New Zealand dollar got hit, losing over -1% against US dollar and Australian dollar.

Election Results

Securing 46% of votes, the National Party is projected to have won 58 seats, marking two seats lower than the 2014-term and three seats short of majority. The Labor Party won 45 seats, surging from 32 in the last term. The third biggest party comes the right-wing, populist NZ First Party. Although the seats it won has dropped to 9, from 11 previously. Greens got 7 seats, just half of what it got in 2014. While ACT managed to keep its one seat, other small parties, including Maori and United Front, failed to return the parliament this time. The number of parties in the parliament falls to 5 from 7 previously.

Back in 2014, Nationals formed a minority government by entering confidence and supply agreements with the centrist United Future, the neoliberal ACT Party, and the indigenous rights-based Māori Party. This combination had existed since Nationals took office in 2008. A re-run of it would be difficult as Maori and United Front are kicked out of the parliament this time, while Labors, Greens and NZ First would prefer to be the oppositions, if not forming a government.

Most Likely Coalition

For now, it is widely anticipated that Nationals would form a coalition with NZ First. As we discussed last week, NZ First is closer to Nationals on social policies but closer to Labors on economic policies. NZ First’s “New Zealand First” stance has led to its proposals to limit foreign investments, revise current FTA deals and sharply cut the numbers of immigrants to around 10K per year, etc. Meanwhile, NZ First proposes the most vigorous reform, amongst other parties, of the Reserve Bank Act. Of course, not all of its proposals would be accepted in a Nationals + NZ First coalition. Given the heightened uncertainty with NZ First on board and the NZD-negative nature of NZ First’s electoral platform, kiwi’s outlook to this combination is skewed to negative.

Uncertainties Remain

Yet, this combination is yet to be a done deal. NZ First had history of working with both Nationals and Labors. As such, a Labors+ Greens +NZ First coalition cannot be ruled out. We believe this trio poses more negatives to New Zealand dollar than the nationals + NZ First coalition. Both Labors and NZ First favor lowering the number of net immigration, although the target numbers of reduction diff. Cutting net immigration is prone to lower GDP growth in coming years. Meanwhile, all three parties propose to reform RBNZ and the proposed changes should likely delay the rate hike schedule. The actual impact on kiwi depends on the priority of the policy implantation, and to what extents these policies are to be implemented.

Aussie Dollar Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.44% against the USD and closed at 0.7962 on Friday.

LME Copper prices declined 0.04% or $2.5/MT to $6405.0/MT. Aluminium prices declined 0.8% or $17.0/MT to $2137.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7956, with the AUD trading 0.08% lower against the USD from Friday's close.

The pair is expected to find support at 0.7917, and a fall through could take it to the next support level of 0.7879. The pair is expected to find its first resistance at 0.7990, and a rise through could take it to the next resistance level of 0.8025.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Manufacturing Sector Activity At A Nearly 7-Year High In September, Services Sector Growth Soared To A 4-Month High...

For the 24 hours to 23:00 GMT, the EUR slightly rose against the USD and closed at 1.1944 on Friday, after the latest data suggested that economic recovery across the Euro-zone retained its momentum at the end of the third quarter.

Data indicated that the Euro-zone's flash Markit manufacturing PMI surprisingly advanced to a level of 58.2 in September, expanding at its quickest pace since February 2011. Market participants had envisaged the PMI to drop to a level of 57.2, after recording a level of 57.4 in the previous month.

Additionally, the region's preliminary Markit services PMI jumped to a level of 55.6 in September, notching a four-month high level and beating market consensus for an advance to a level of 54.8. In the previous month, the PMI had registered a reading of 54.7.

Separately, activity in Germany's manufacturing sector unexpectedly surged to a more than six-year high level of 60.6 in September, confounding market expectations for a drop to a level of 59.0. In the previous month, the PMI had registered a reading of 59.3. Moreover, the nation's services sector growth accelerated to a six-month high level of 55.6 in September, while markets were anticipating it to climb to a level of 53.7. In the previous month, the PMI had registered a reading of 53.5.

The greenback nursed losses against a basket of major currencies on Friday, on the heels of simmering tensions on the Korean peninsula, after North Korea stated that it might test a hydrogen bomb in the Pacific Ocean in response to the US President, Donald Trump's warning to destroy the isolated nation.

The preliminary Markit manufacturing PMI in the US rose to a level of 53.0 in September, meeting market expectations and hitting a two-month high level. The PMI had recorded a level of 52.8 in the prior month.

On the other hand, the nation's flash Markit services PMI declined to a two-month low level of 55.1 in September, worse than market expectations for a fall to a level of 55.8 and following a reading of 56.0 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.1931, with the EUR trading 0.11% lower against the USD from Friday's close, after the German Chancellor, Angela Merkel, won a fourth term but was left struggling to form a governing coalition.

The pair is expected to find support at 1.1895, and a fall through could take it to the next support level of 1.1860. The pair is expected to find its first resistance at 1.1985, and a rise through could take it to the next resistance level of 1.2040.

Moving ahead, investors will look forward to Germany's Ifo expectations and business climate indices, both for September, slated to release in a few hours. Additionally, ECB Chief, Mario Draghi's speech, due later today, will be assessed by traders.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.