Sample Category Title

Canada: Retail Sales flat in November, But Likely to Remain a Key Driver of Real Consumption in Q4

Retail sales were flat month-over-month (m/m) in November, right in line with the Statistics Canada’s advance estimate.

In real terms, however, sales declined by 0.4% m/m.

Sales at motor vehicle and parts dealers were up by 2.0% m/m, building on October's strong gains of 2.4% m/m. Ex-autos, sales were down 0.7% m/m, falling short of the consensus expectation of 0.1% m/m growth.

Receipts at gas stations and fuel vendors rose by 0.7% m/m in nominal terms and by 0.8% m/m in real terms, reflecting softer prices.

Excluding both auto sales and gas station receipts, core retail sales fell by 1.0% m/m in November, following a downwardly revised flat reading in October (previously reported as +0.2% m/m).

- The decline was driven by food and beverage retailers (-1.6% m/m), building material & garden supply dealers (-2.1% m/m), and general merchandise stores (-1.0% m/m).

- Gains at miscellaneous store retailers (+0.7% m/m) and furniture and home furnishings stores (+0.2% m/m) were not enough to offset declines.

E-commerce sales declined by 1.2% m/m after two consecutive months of growth.

Statistics Canada’s advance estimate for December suggests that sales were up 1.6%.

Key Implications

Apart from strength in auto sales, this was a softer-than-expected report. Flat goods inflation in November weighed on nominal sales, but even after accounting for price effects, real sales contracted in November.

Despite this, we upgraded our real consumption forecast to 3% in Q4 2024 as a strong flash estimate for December points to a rebound in activity. A parallel report on food services and drinking places suggests that services spending was robust. Moreover, shoppers could have been holding back their purchases in November until the expected GST tax in December (a sizeable decline in beer& wine stores provide good evidence of that). We estimate that the holiday provided a substantial 8.6% discount on affected items, which suggests that real activity was even stronger than reported in the flash estimate.

Yen Stabilizes in Weak Position as BoJ Rate Hike Awaited

While Yen remains the worst performer of the week so far, it has stabilized as the markets await the highly anticipated BoJ rate hike in the upcoming Asian session. Expectations for this rate move were well set by comments from BoJ Governor Kazuo Ueda last week. Risks from US political developments—specifically tariff policies under President Donald Trump—have now been set aside too, clearing the way for BoJ to proceed with its monetary normalization. Policy rate should be raised by 25bps to 0.50%.

The question now centers on how BoJ will portray Japan’s economic outlook and its policy path for the year. With signs of resurgent inflationary pressures, it’s unlikely that Ueda will strike a dovish tone. In fact, Japan’s upcoming CPI datad ue tomorrow too—expected to show core inflation rising for a second month to 3% in December—will support that view.

Ueda's comments in the post meeting press conference could be cautiously optimic. On the one hand, he would reiterate international uncertainties, and refrain from committing to a specific timeline for policy normalization. But the view towards domestic wage development could be upbeat. Inflation forecasts could also be raised in the new quarterly economic outlook report. Both would be seen as hawkish, albeit mildly. Currently, markets are seeing the chances of another hike in the middle of the year, and probably one more by the year-end to bring interest rate to a more neutral setting at 1.00%.

USD/JPY would be logically a pair to pay attention to. Price actions from 158.86 are seen as developing in to a corrective pattern for sure. While initial support was seen above 55 D EMA (now at 154.67) to slow the pull back, a hawkish BoJ hike tomorrow could push USD/JPY lower towards 38.2% retracement of 139.57 to 158.86 at 151.49.

Conversely, a robust rebound—even if BoJ sounds hawkish—might suggest that the correction from 158.86 is already done, and the rally from 139.57 could be ready to resume.

Overall for the week so far, the rankings in the performance ladder didn't chance much as trading has been rather subdued after volatility on Monday. Kiwi is currently the strongest, followed by Euro and then Aussie. Yen is the worst, followed by Dollar and then Loonie. Sterling and Swiss Franc are stuck in the middle.

Canada’s retail sales stagnate in Nov as core sales down -1% mom

Canada’s retail sales were flat in November, falling short of the expected 0.2% mom increase. The data revealed mixed performance across sectors, with declines in six out of nine subsectors.

Sales at food and beverage retailers dropped by -1.6% mom, driving much of the weakness in the report. However, gains in motor vehicle and parts dealers (+2.0% mom) and gasoline stations and fuel vendors (+0.7% mom) helped offset the broader declines, preventing an outright contraction in overall retail activity.

Core retail sales, which exclude the more volatile categories of motor vehicles and gasoline, declined by a notable -1.0% mom.

US initial jobless claims rises to 223k, above exp 220k

US initial jobless claims rose 6k to 223k in the week ending January 18, above expectation of 220k. Four-week moving of initial claims rose 750 to 213.5k.

Continuing claims rose 46k to 1899 in the week ending January 11, highest since November 13, 2021. Four-week moving average of continuing claims rose 500 to 1866k.

Japan posts first trade surplus in six months

Japan recorded a trade surplus of JPY 130.9B in December, the first surplus in six months, driven by a 2.8% yoy rise in exports to JPY 9.91T. Imports also jumped, rising 1.8% yoy to JPY 9.8T.

However, exports to the two largest trading partners saw declines, with shipments to China falling by -3.0% yoy and to the US by 2.1% yoy.

On a month-on-month seasonally adjusted basis, exports rose 6.3% mom to JPY 9.44T. Imports increased 2.2% mom to JPY 9.47T, resulting in a seasonally adjusted trade deficit of JPY 33B.

For the entirety of 2024, Japan’s trade deficit narrowed significantly, shrinking by 44% from the previous year to JPY -5.33T. Exports reached a record high of JPY 107.09T, up 6.2%, bolstered by strong demand for vehicles and semiconductor-related products. Imports also rose by 1.8% to JPY 112.42T.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0368; (P) 1.0401; (R1) 1.0461; More...

Intraday bias in EUR/USD remains neutral for the moment. On the upside, firm break of 1.0435 resistance will extend the rebound from 1.0176 to 38.2% retracement of 1.1213 to 1.0176 at 1.0572. Rejection by 1.0435 will keep the correction from 1.0176 relatively short. Firm break of 1.0176 will resume whole fall from 1.1213.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0368; (P) 1.0401; (R1) 1.0461; More...

Intraday bias in EUR/USD remains neutral for the moment. On the upside, firm break of 1.0435 resistance will extend the rebound from 1.0176 to 38.2% retracement of 1.1213 to 1.0176 at 1.0572. Rejection by 1.0435 will keep the correction from 1.0176 relatively short. Firm break of 1.0176 will resume whole fall from 1.1213.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

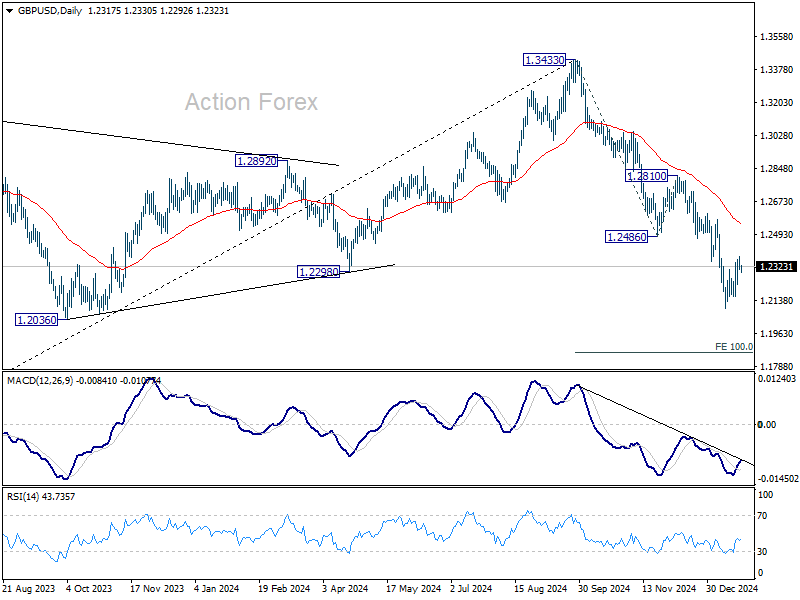

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2291; (P) 1.2333; (R1) 1.2359; More...

Intraday bias in GBP/USD remains neutral as consolidation pattern from 1.2099 is still extending. Further decline is expected with 1.2486 support turned resistance intact. On the downside, break of 1.2099 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

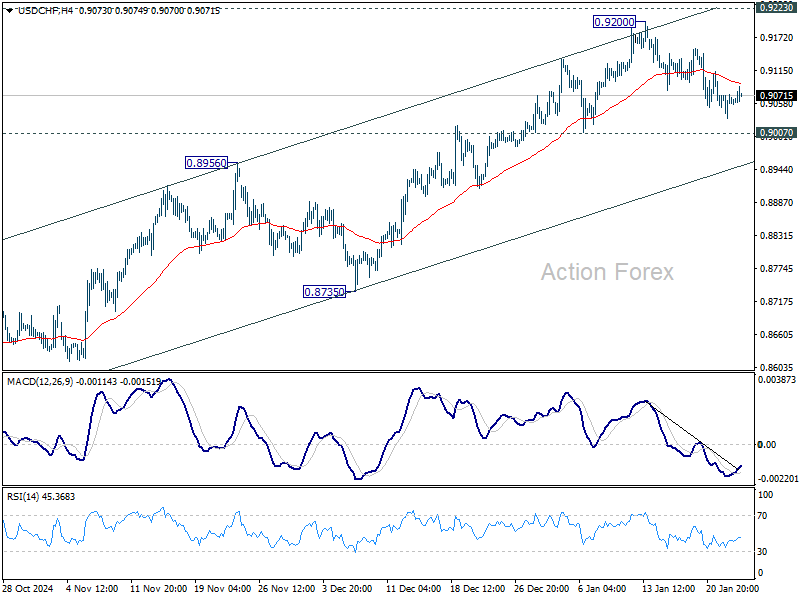

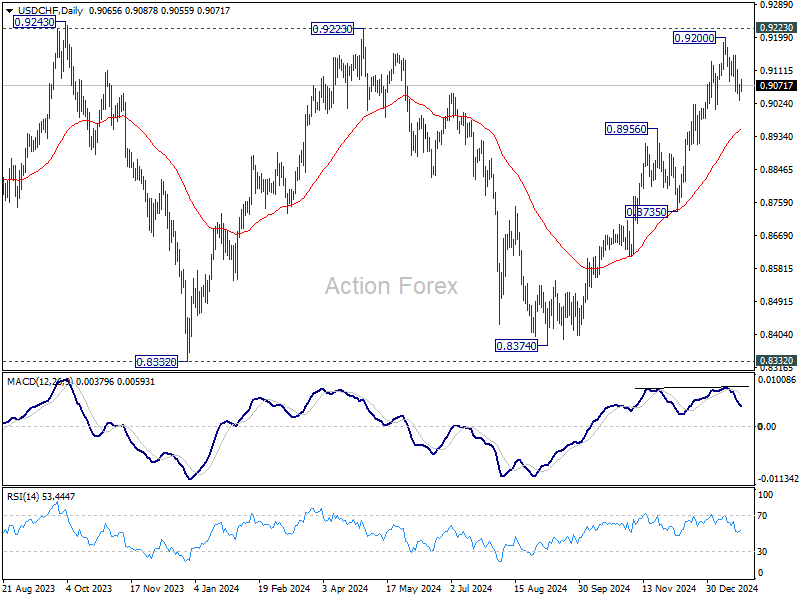

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9039; (P) 0.9062; (R1) 0.9090; More…

Intraday bias in USD/CHF stays neutral as consolidations continue below 0.9200. Further rally is expected with 0.9007 support intact. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 0.8950).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

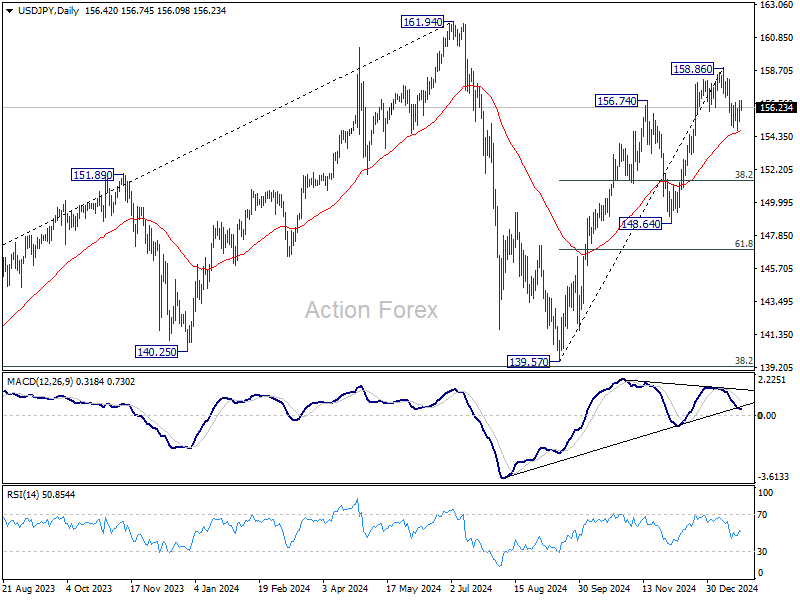

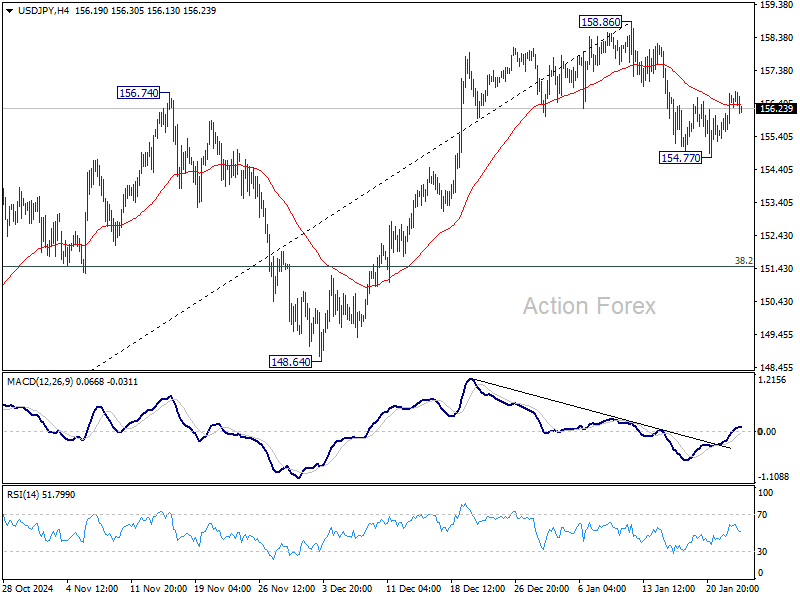

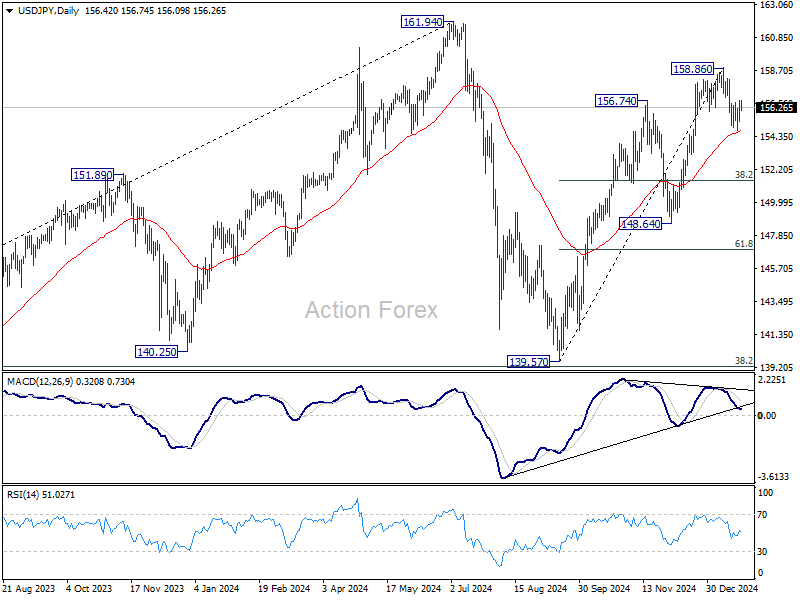

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.68; (P) 156.20; (R1) 157.04; More...

Intraday bias in USD/JPY stays neutral for the moment, and some more sideway trading might be seen. On the downside, sustained trading below 55 D EMA (now at 154.73) will extend the correction from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49 next. However, firm break of 158.86 will resume the whole rally from 139.67 to retest 161.94 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Canada’s retail sales stagnate in Nov as core sales down -1% mom

Canada’s retail sales were flat in November, falling short of the expected 0.2% mom increase. The data revealed mixed performance across sectors, with declines in six out of nine subsectors.

Sales at food and beverage retailers dropped by -1.6% mom, driving much of the weakness in the report. However, gains in motor vehicle and parts dealers (+2.0% mom) and gasoline stations and fuel vendors (+0.7% mom) helped offset the broader declines, preventing an outright contraction in overall retail activity.

Core retail sales, which exclude the more volatile categories of motor vehicles and gasoline, declined by a notable -1.0% mom.

US initial jobless claims rises to 223k, above exp 220k

US initial jobless claims rose 6k to 223k in the week ending January 18, above expectation of 220k. Four-week moving of initial claims rose 750 to 213.5k.

Continuing claims rose 46k to 1899 in the week ending January 11, highest since November 13, 2021. Four-week moving average of continuing claims rose 500 to 1866k.

Canadian Dollar Steady Ahead of Retail Sales

The Canadian dollar is showing limited movement on Thursday. In the European session, USD/CAD is trading at 1.4396, up 0.13% on the day. The Canadian dollar started the week with sharp gains of over 1% but has since given up about half of those gains.

Canada’s retail sales expected to have declined in November

Canada’s retail sales are projected to have decelerated in November and that could be bad news for the Canadian dollar. Retail sales are expected to have eased to 0.2% m/m, down from 0.6% in October. Consumer spending has shown some robustness, with four straight months of strong gains, in response to interest rate cuts from the Bank of Canada. A major test for retail sales will be the November and December reports, which reflects consumer spending during the critical Christmas season.

The central bank has been aggressive in its easing cycle, chopping borrowing costs by 175 basis points since June 2024, including a 50-bp cut at the December meeting. The cash rate of 3.25% is much lower than the Federal Reserve’s rate of 4.25%-4.5% and the BoC will have to tread carefully. The Fed has sounded more hawkish lately and is not expected to cut more than one or two times due to the strong US economy. If the BoC is more aggressive than the Fed in lowering rates, it would widen the US/Canada rate differential and put further downward pressure on the weak Canadian dollar.

Another headache for the BoC is the Trump factor. The new US President has threatened to levy 25% tariffs on Canada as early as February 1. Ever the deal maker, Trump may be leveraging this threat to wring concession from Ottawa. Still, Trump’s tariff threat has to be taken seriously as such a move would damage the weak Canadian economy, which is very dependent on the US.

USD/CAD Technical

- USD/CAD is putting pressure on resistance at 1.4412. Above, there is resistance line in 1.4447

- 1.4357 and 1.4322 are the next support levels

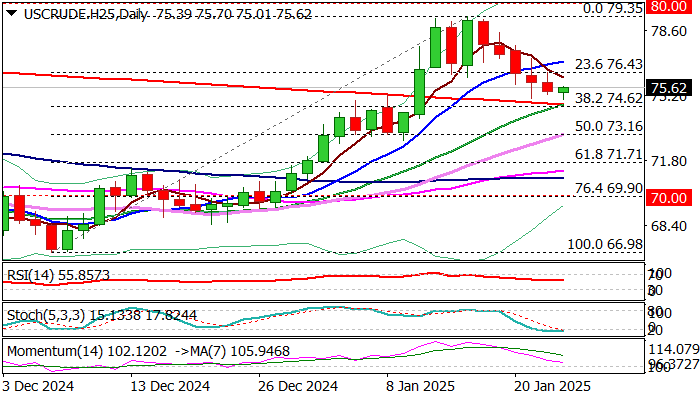

WTI Oil: Daily Studies Signal Possible End of Recent Drop

WTI Oil remains at the back foot on Thursday, but moving at the lower pace, compared to a steep fall in past few sessions when oil price was down around four dollars.

Key drivers of oil price were signals of increased US oil production on new policies of Trump’s administration and calmer geopolitical situation in the Middle East.

Global oil demand could be also dampened by trade tariffs, which might be imposed on a number of countries, potentially to the EU that would send additional shockwaves through the market.

Unexpected rise of US crude stocks (API report) added to negative near term outlook.

While fundamentals remain weak, technical picture is slightly brighter.

Daily studies remain positive overall, as MA’s are in bullish configuration, momentum is still positive and the price is facing strong supports at $74.70 zone (Fibo 38.2% retracement of $66.98/$79.35 / converged 20/200DMA about to form golden cross), with today’s action being so far shaped in daily Doji and suggesting that near-term bears off $79.35 peak, might be losing traction.

However, these initial signals will require confirmation on extension through initial trigger at $76.00 zone (base of thick 4-hr cloud) then $76.43 (broken Fibo 23.6%) and finally lift above 10DMA ($76.98) to generate reversal signal.

Otherwise, limited upticks would signal that bears might be consolidating for fresh push lower, but sustained break through 200DMA will be needed to signal bearish continuation.

Res: 76.09; 76.43; 76.98; 77.18.

Sup: 75.01; 74.76; 74.62; 74.02.