Sample Category Title

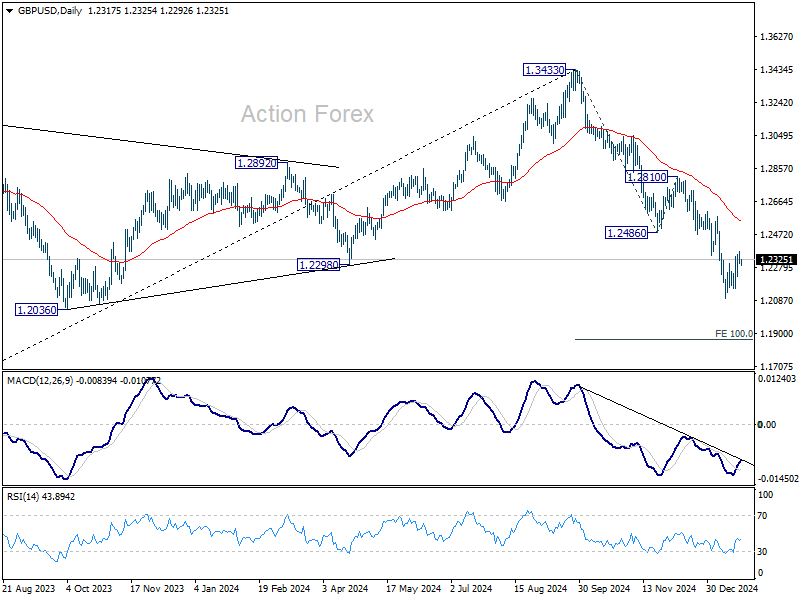

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2291; (P) 1.2333; (R1) 1.2359; More...

GBP/USD is still extending consolidation pattern from 1.2099 and intraday bias remains neutral. Further decline is expected with 1.2486 support turned resistance intact. On the downside, break of 1.2099 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

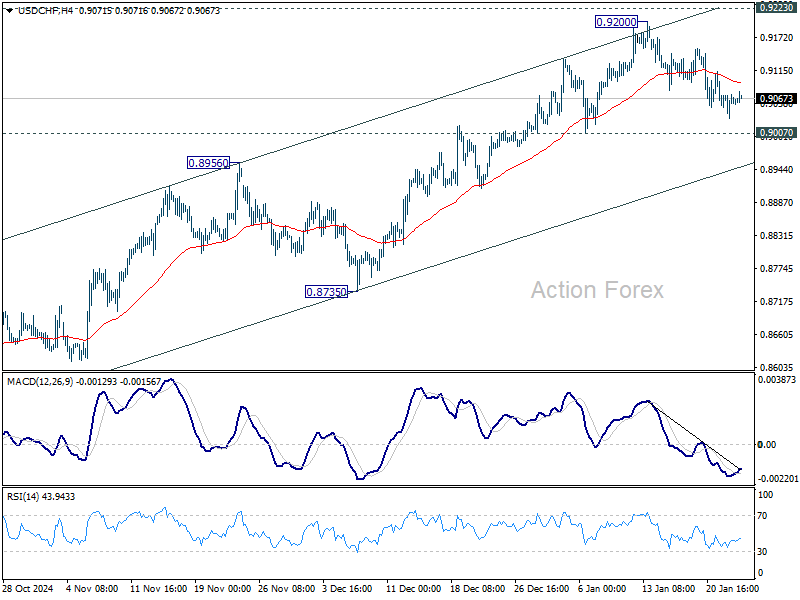

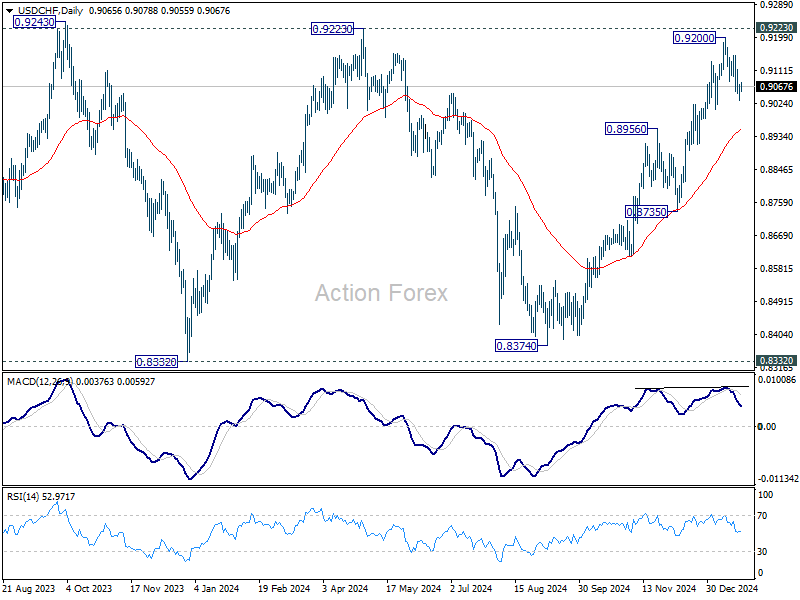

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9039; (P) 0.9062; (R1) 0.9090; More…

USD/CHF is still bounded in consolidation from 0.9200 and intraday bias stays neutral. Further rally is expected with 0.9007 support intact. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 0.8950).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

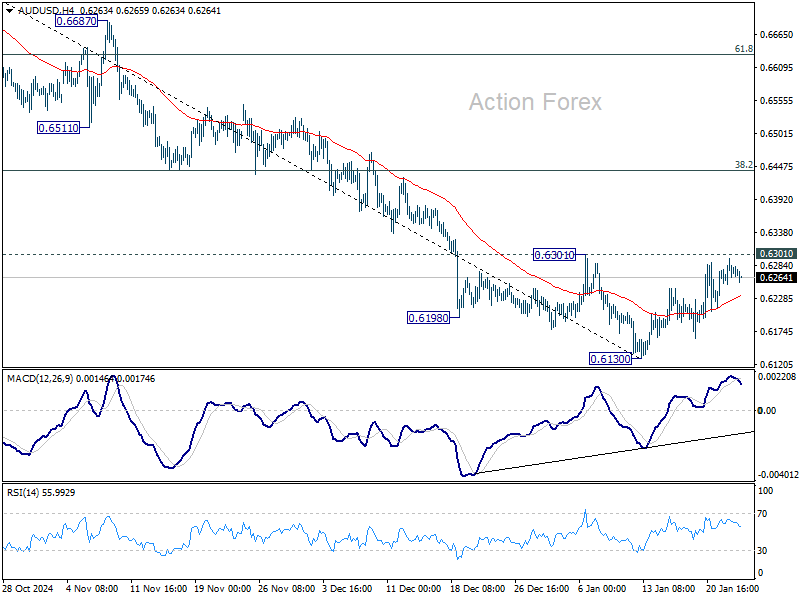

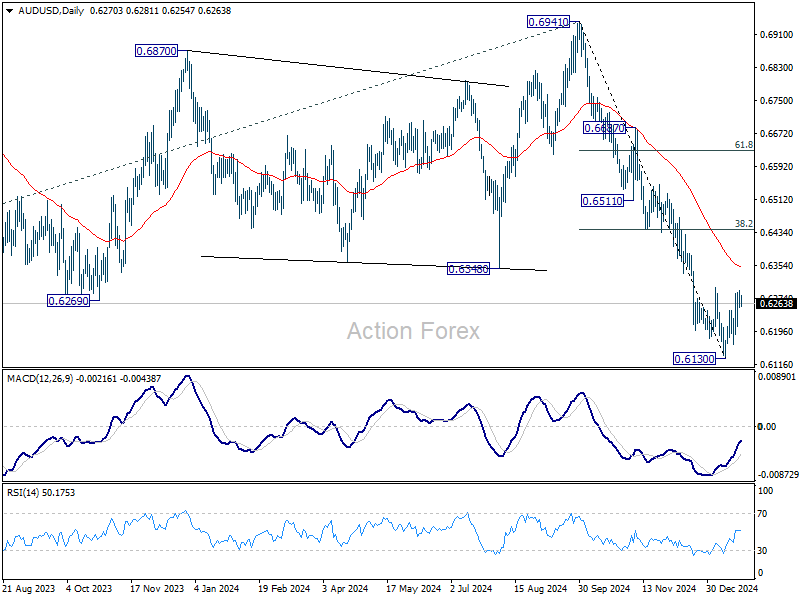

AUD/USD Daily Report

Daily Pivots: (S1) 0.6253; (P) 0.6274; (R1) 0.6296; More...

No change in AUD/USD's outlook and intraday bias remains neutral. Further decline is expected with 0.6301 resistance intact. Firm break of 0.6130 will resume the fall from 0.6941. However, sustained break of 0.6310 will turn bias back to the upside for stronger rebound to 55 D EMA (now at 0.6352), and possibly above.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

Dollar Range Trading Awaits Trump’s Directives

Following Donald Trump's inauguration, the dollar lost part of this month’s gains on Monday and adjusted to significant support levels. However, there is no clear development of a full-scale downward correction as yet. Most currency pairs remain within their previous sideways corridors, awaiting new directives from the newly inaugurated president.

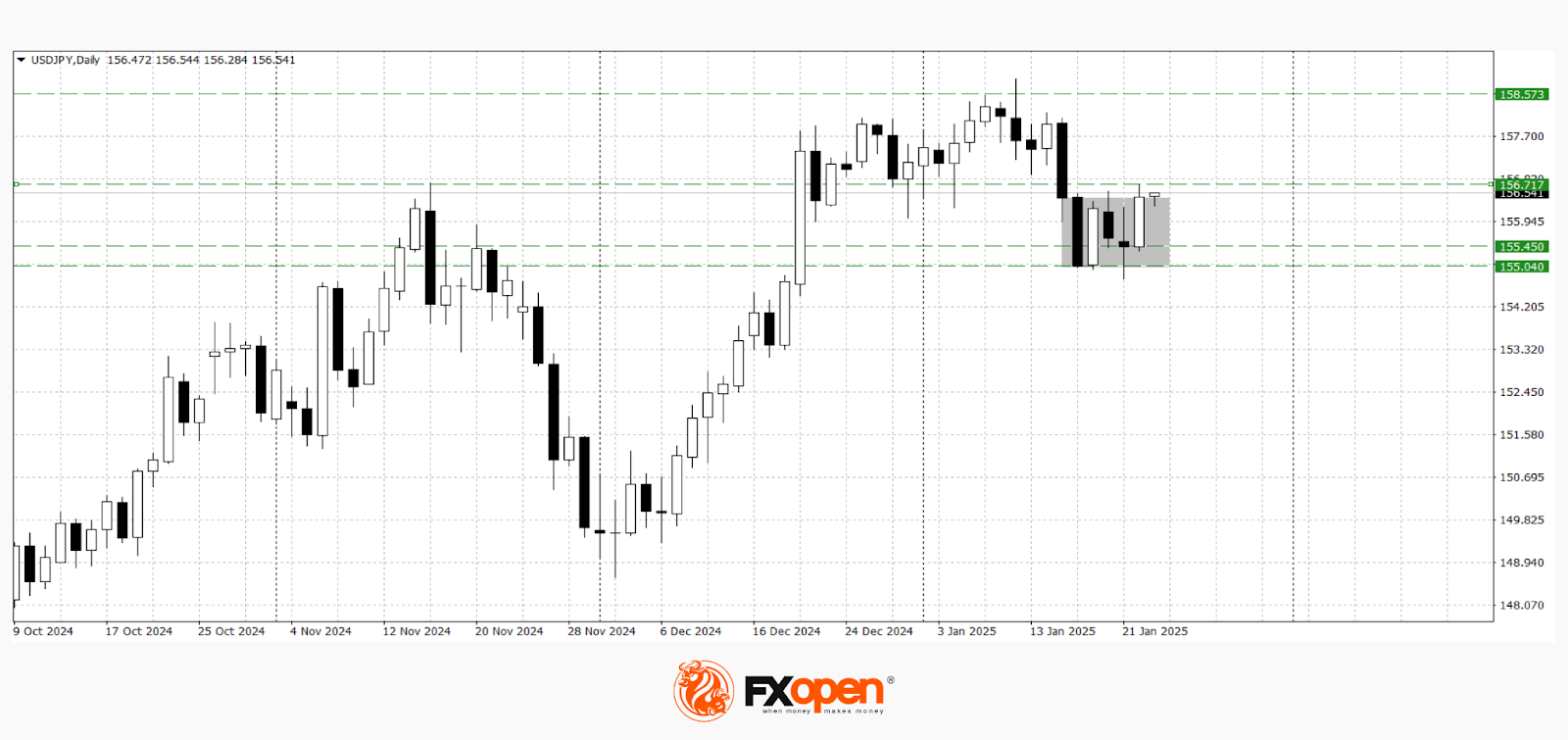

USD/JPY

The USD/JPY currency pair has once again tested the important range of 155.00–154.80. The inability of sellers to hold the price below 155.00 for two weeks could lead to another test of recent highs in the 157.00–157.80 zone.

Technical analysis of USD/JPY indicates a sideways movement of the pair. At present, the price is at the upper boundary of a five-day corridor. If it rebounds from the 156.70 level, a decline towards the 155.20–155.00 marks is possible.

A consolidation above 157.00 could result in an update of the year’s maximum at 158.90.

Key events influencing USD/JPY movements:

- Today at 16:30 (GMT+2): Initial Jobless Claims in the United States.

- Today at 19:00 (GMT+2): Speech by US President Donald Trump.

- Tomorrow at 05:30 (GMT+2): Bank of Japan’s Monetary Policy Report.

- Tomorrow at 06:00 (GMT+2): Bank of Japan Interest Rate Decision.

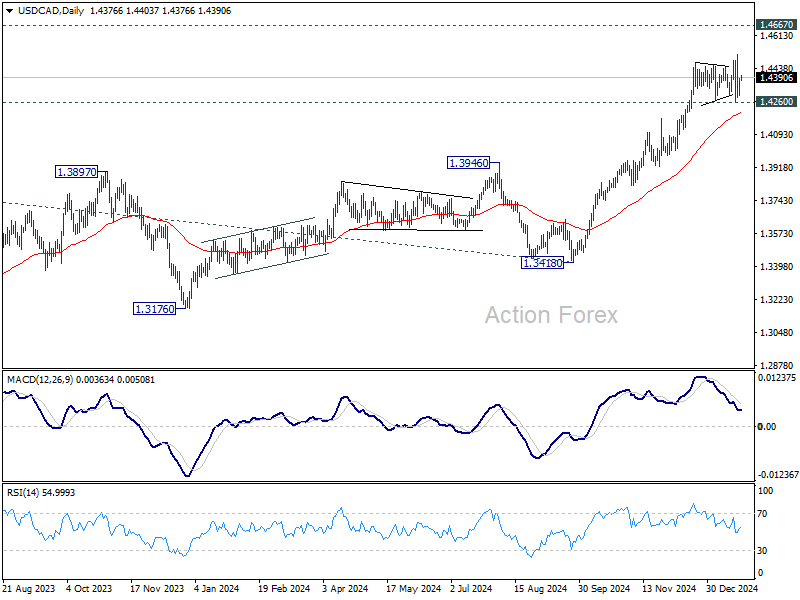

USD/CAD

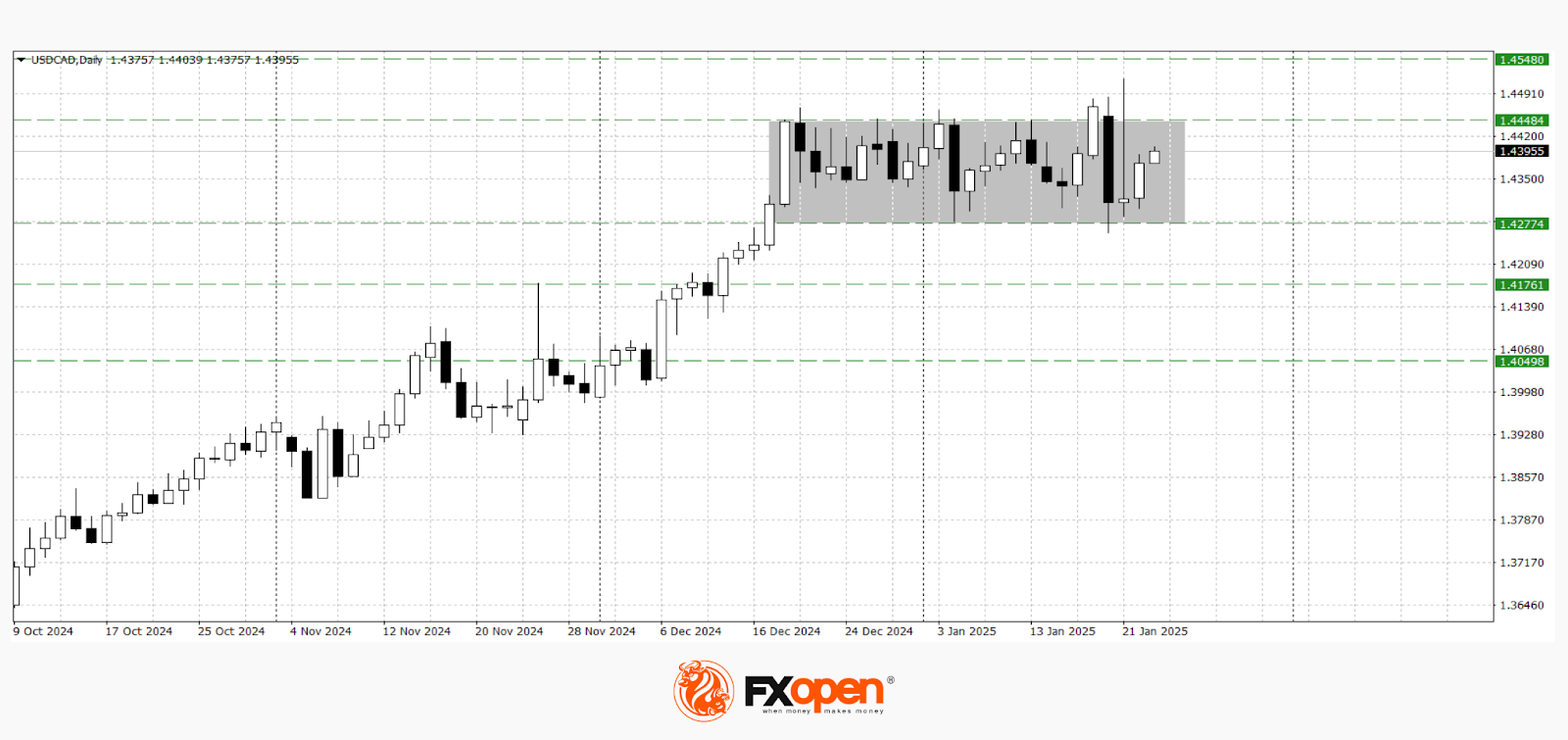

Range trading with false boundary breakouts is also observed in the USD/CAD pair. On Monday, the price updated its January low at 1.4280 but failed to develop a full-fledged downward correction and consolidate below this level. In the upcoming trading sessions, another approach to the 1.4420–1.4450 range is possible.

The nature of the price exit from the four-week range of 1.4300–1.4500 could provide more clues about the medium-term movement of USD/CAD.

Key events influencing USD/CAD pricing today:

- Today at 16:30 (GMT+2): Retail Sales Volume in Canada.

- Today at 16:30 (GMT+2): US Crude Oil Inventories.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

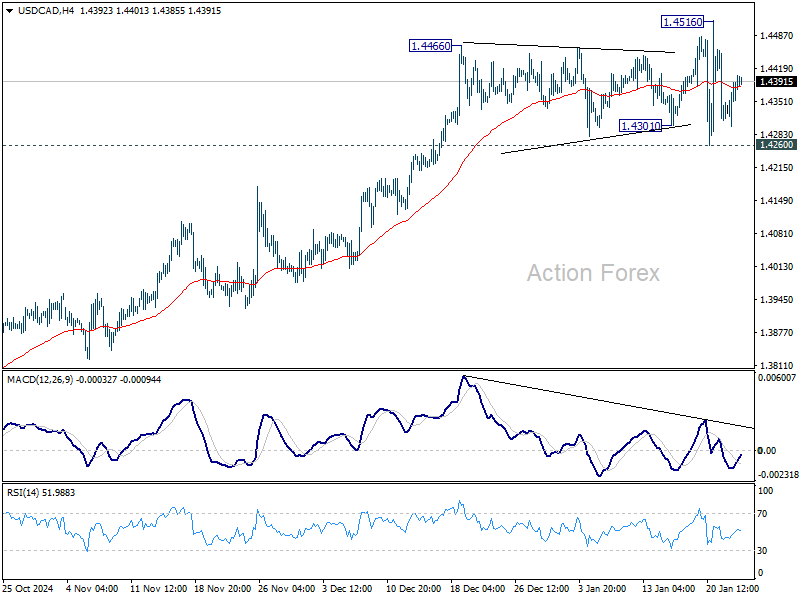

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4322; (P) 1.4357; (R1) 1.4412; More...

Range trading continues in USD/CAD and intraday bias remains neutral. Further rise is expected as long as 1.4260 support holds. Break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.4205) and below.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

Dollar Softness Continues as Forex Markets Tread Calm Waters

The forex markets remain unusually quiet today, with Dollar staying soft despite multiple attempts to rebound. The greenback has only managed meaningful gains against the weaker Yen and the struggling Canadian Dollar, while failing to build momentum against other major currencies. With little in the way of significant economic data on the calendar today, trading is expected to remain subdued. However, volatility could resurface, probably just temporarily, later in the week, with BoJ’s anticipated rate hike and key PMI releases from major economies slated for Friday.

Loonie, nonetheless, could see movement today, with retail sales data due. BoC is widely expected to cut rates by 25 bps at its upcoming meeting next Wednesday, a view supported by a Reuters survey where 25 out of 31 economists forecast such a move. Additionally, median expectations point to another 25 bps cut in March, followed by a further reduction later in the year, bringing the overnight rate to 2.50%.

For USD/CAD, however, the real driver for a decisive range breakout, beyond brief jitters, would lie in developments surrounding US-Canada trade relations. The market awaits details of tariffs expected to be announced on February 1, including their scope and which products will be affected.

So far this week, Yen has been the weakest performer, followed by Dollar and Loonie. At the other end of the spectrum, the Kiwi remains the strongest, while Euro and Aussie. Sterling and Swiss are still stuck in middle positions.

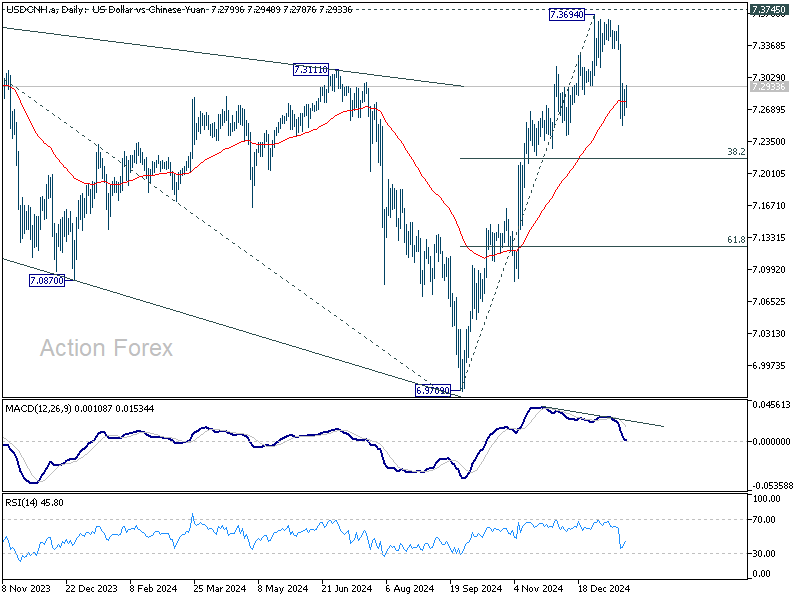

A key development this week has been the sharp decline in USD/CNH, which is viewed as a sign of a stabilizing risk sentiment toward global trade. Technically, a short term top should be formed at 7.3694, just ahead of 7.3745 key resistance (2022 high). More consolidative is expected in the near term with risk of deeper pull back. But downside should be contained by 38.2% retracement of 6.9709 to 7.3694 at 7.2172. Eventual upside break remains in favor.

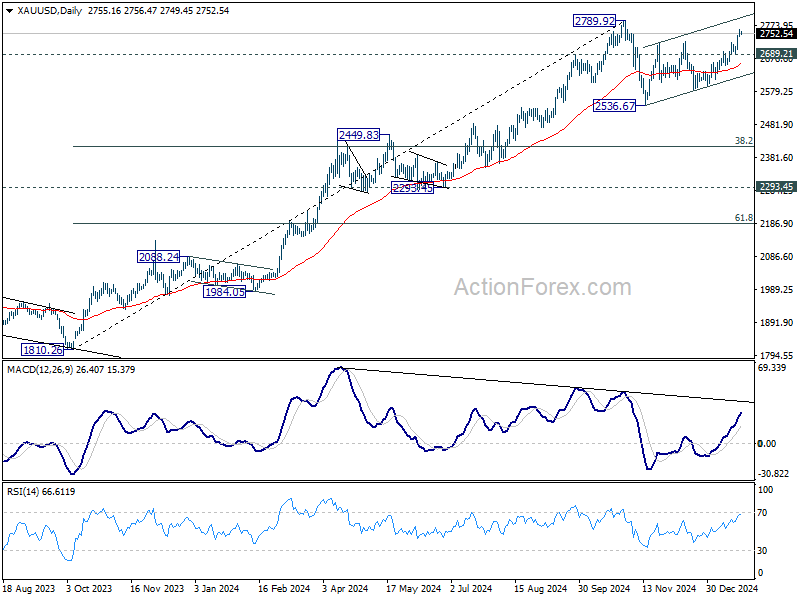

Gold surges on Dollar weakness, Silver lags

Gold prices surged past 2750 mark this week, supported largely by a weaker Dollar. The overall market sentiment is on a relatively calmer backdrop, with US President Donald Trump’s decision to delay tariff implementations contributed to easing trade-related fears. Additionally, geopolitical tensions receded as a ceasefire between Israel and Hamas took hold earlier in the week.

Hence, as whether Gold can break its record high of 2789 will depend largely on the depth of Dollar’s correction in the coming days.

Technically, Gold's rebound from 2536.67 is currently seen as the second leg of the corrective pattern from 2789.92 high. Strong resistance could be seen from this resistance to limit upside. Break of 2689.21 support will argue that the third leg of the pattern has started back towards 2536.67 support. Nevertheless, decisive break of 2789.92 will confirm up trend resumption.

Silver’s performance, by comparison, has been relatively subdued. Its recovery from 28.74 remains weak and corrective in nature. For now, as long as 32.30 resistance holds, fall from 34.84 is still in favor to resume at a later stage, to 26.44 cluster support zone.

Japan posts first trade surplus in six months

Japan recorded a trade surplus of JPY 130.9B in December, the first surplus in six months, driven by a 2.8% yoy rise in exports to JPY 9.91T. Imports also jumped, rising 1.8% yoy to JPY 9.8T.

However, exports to the two largest trading partners saw declines, with shipments to China falling by -3.0% yoy and to the US by 2.1% yoy.

On a month-on-month seasonally adjusted basis, exports rose 6.3% mom to JPY 9.44T. Imports increased 2.2% mom to JPY 9.47T, resulting in a seasonally adjusted trade deficit of JPY 33B.

For the entirety of 2024, Japan’s trade deficit narrowed significantly, shrinking by 44% from the previous year to JPY -5.33T. Exports reached a record high of JPY 107.09T, up 6.2%, bolstered by strong demand for vehicles and semiconductor-related products. Imports also rose by 1.8% to JPY 112.42T.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4322; (P) 1.4357; (R1) 1.4412; More...

Range trading continues in USD/CAD and intraday bias remains neutral. Further rise is expected as long as 1.4260 support holds. Break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.4205) and below.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

Gold surges on Dollar weakness, Silver lags

Gold prices surged past 2750 mark this week, supported largely by a weaker Dollar. The overall market sentiment is on a relatively calmer backdrop, with US President Donald Trump’s decision to delay tariff implementations contributed to easing trade-related fears. Additionally, geopolitical tensions receded as a ceasefire between Israel and Hamas took hold earlier in the week.

Hence, as whether Gold can break its record high of 2789 will depend largely on the depth of Dollar’s correction in the coming days.

Technically, Gold's rebound from 2536.67 is currently seen as the second leg of the corrective pattern from 2789.92 high. Strong resistance could be seen from this resistance to limit upside. Break of 2689.21 support will argue that the third leg of the pattern has started back towards 2536.67 support. Nevertheless, decisive break of 2789.92 will confirm up trend resumption.

Silver’s performance, by comparison, has been relatively subdued. Its recovery from 28.74 remains weak and corrective in nature. For now, as long as 32.30 resistance holds, fall from 34.84 is still in favor to resume at a later stage, to 26.44 cluster support zone.

Japan posts first trade surplus in six months

Japan recorded a trade surplus of JPY 130.9B in December, the first surplus in six months, driven by a 2.8% yoy rise in exports to JPY 9.91T. Imports also jumped, rising 1.8% yoy to JPY 9.8T.

However, exports to the two largest trading partners saw declines, with shipments to China falling by -3.0% yoy and to the US by 2.1% yoy.

On a month-on-month seasonally adjusted basis, exports rose 6.3% mom to JPY 9.44T. Imports increased 2.2% mom to JPY 9.47T, resulting in a seasonally adjusted trade deficit of JPY 33B.

For the entirety of 2024, Japan’s trade deficit narrowed significantly, shrinking by 44% from the previous year to JPY -5.33T. Exports reached a record high of JPY 107.09T, up 6.2%, bolstered by strong demand for vehicles and semiconductor-related products. Imports also rose by 1.8% to JPY 112.42T.

Tech Soap Opera

US equities were boosted by strong earnings and Trump’s AI push. Technology stocks led the rally, this time, and pushed Nasdaq 100 1.33% higher, the S&P500 hit a fresh intraday record high while gains in the Dow Jones were significantly lower. The index gained only 0.30% on Wednesday. Among the tech names, Netflix jumped around 10% on the back of strong earnings and traded at $999 a share – just short of the $1000 psychological mark. It’s probably a matter of time before Netflix claims the $1000 level provided that the company’s recent gains were driven by the strategic move to stream live events and has potential to fuel organic growth. Other than that, Nvidia, Oracle and OpenAI investor Microsoft – the names of the companies that are cited in the so-called Stargate project – gained. Nvidia extended gains by almost 4.5%, Microsoft gained more than 4% while Oracle jumped up to 10% but gave back a part of these gains to end the day with an almost 7% gain.

But Trump’s Best Buddy Elon Musk, probably irritated by the growing closeness between Donald Trump and OpenAI’s Sam Altman – his nemesis - wrote an X post saying that these companies don’t have the money to invest in Trump’s AI project. The post sparked concerns about Musk’s relationship with the White House, leading Tesla shares to drop 2%. The saga serves as a reminder that the next four years will be a constant watch of who’s aligned with whom, who’s feuding, who’s making waves, and who holds the power to steer things in their favor. I, for one, can’t wait."

Elsewhere, there was good from P&G’s latest quarterly report. The company revealed that its organic sales exceeded expectations. But what attracted investors’ attention is that the company’s Q4 sales growth came from higher volumes and not from price hikes, as the company didn’t raise the price of its products for the first time since 2019 according to Bloomberg. The latter gives an encouraging insight regarding the US inflation dynamics. Unfortunately, that doesn’t erase the risk of rising inflationary pressures on Donald Trump’s pro-growth policies, his tax cut and mass deportation plans and the tariffs – which are all potential inflation-boosters. Indeed, ‘US Republicans are in talks over raising the cap for state and local tax deductions’. And tax deductions are obviously bad for public finances. As such, the US 10-year yield is back to 4.60% after a decline to 4.53% earlier this week, while the US futures are slightly negative at the time of writing.

In Europe, the Stoxx 600 advanced to a fresh record high yesterday, on hope that the tariffs that the US would impose on Europe would be softer than the threats. So far, the Stoxx 600 gained around 4%, and outperformed the S&P500 – which posted around 3.60% since the beginning of the year. This is all very much in line with the expectation of convergence between the stocks of two continents due to the big valuation gap and on the expectation that the ECB will be more supportive of the economies than the Fed in the coming months.

In China, market sentiment is mixed. The relief over Donald Trump not announcing new tariffs on China during his inauguration didn’t last long. He said yesterday that he would impose 10% tariff on Chinese imports. Consequently, the Chinese equities were down yesterday and they are having hard time recovering on Chinese government’s freshly announced measures to boost sentiment. These measures include an increase to the amount of stocks that pension funds and insurers could buy, and encourages the listed firms to increase their share repurchases. Alas, the CSI 300 has erased most of its gains since this morning, and the shooting star pattern of today hints that sentiment remains bearish for Chinese equities.

In the FX, the US dollar rebounded yesterday on the back of higher US growth and potentially higher US inflation expectations. The EURUSD bounced lower after testing the 50-DMA. The European Central Bank (ECB) doves remain in charge of the market and cap the upside potential of the euro against the greenback. Across the Channel, Cable is also under pressure this morning as Rachel Reeves is being seriously challenged on her Budget in Davos. She said that she said that she was ‘absolutely relaxed’ about wealth creation. How lucky! The truth is investors are not as relaxed and they are losing confidence in Reeves’ growth-boosting plans. The sterling outlook remains negative, also backed by the expectation of two – and maybe more – rate cuts for this year.

Finally, crude oil is down for the sixth straight day on the back of Trump policy plans and a surprise 1 mio barrel build in US inventories last week. US crude is preparing to test a major support area, $75.20/75.40 range, that includes the 200-DMA and the major 38.2% Fibonacci retracement on the December to January rebound. A move below this zone will suggest a medium-term bearish reversal and hint at the possibility of deeper price pullback toward the $73.80 mark, the 50% retracement level.

Markets Eye Tariffs on the Horizon

In focus today

Markets remain closely focused on President Trump's actions during this first week of his presidency. He is expected to issue several executive orders building on his current momentum, leading to US news continuing to dominate the headlines as markets and world leaders alike are left navigating the implications.

In the euro area, we receive consumer confidence data for January, which will be very interesting. Following a continuous upward trend over the past two years, consumer confidence declined in both November and December. Since private consumption is anticipated to be the primary growth driver this year, consumer sentiment will be crucial for the economic outlook.

Norges Bank (NB) is highly expected to stay on hold at 4.5% today and signal that the first rate cut will most likely be delivered in March. December's core inflation likely relieves NB after November's spike, indicating continued disinflation. However, global rates, NOK, and oil prices suggest upside risk to December's rate path. NB is expected to remain vague on the outlook beyond March.

Overnight in Japan, we will receive both CPI and PMI data for December ahead of the Bank of Japan meeting early morning. Tokyo inflation data indicates price pressures have eased a bit in December. The economic recovery has been on track for a while and inflation close to target. We expect the BoJ will hike its policy rate by 25bp, which is also largely priced in by investors now.

Economic and market news

What happened yesterday

In the US, President Trump told Russian President Putin to reach a deal in Ukraine or be faced by increased sanctions from the US. This marks the first comment by the president on the war in Ukraine. Overnight Trump halted more than USD 300bn in US green infrastructure funding, while paving the way for a USD 500bn private-sector investment in AI infrastructure. He also disclosed that his administration was currently discussing a 10% tariff on China, as well as saying the EU will get tariffs due to a "troubling" trade surplus with the US.

Equities: Global equities rose yesterday, marking the seventh consecutive day of gains, with the MSCI World Index reaching a new all-time high. This is noteworthy given the widespread caution and predictions of volatility surrounding the inauguration of the US president, which have not materialised. Instead, there has been a steady increase, and those who reduced risk beforehand would have missed out on a 4% equity return, equivalent to half a year's average return in just seven days. This could serve as a reminder of not being too cautious about underweighting risk during periods when macroeconomic, microeconomic, and monetary policies are highly supportive, even when political issues dominate 90% of the media coverage.

In the US yesterday, the Dow was up by 0.3%, the S&P 500 by 0.6%, the Nasdaq by 1.3%, and the Russell 2000 was down by 0.6%. This morning presents a mixed picture in Asia. Earlier, Chinese stocks performed better following comments about increased public support for the equity markets, but this effect has since faded. US and European futures are slightly lower this morning.

FI: There was modest movement in global bond yields yesterday as 2Y and 10Y US Treasuries rose a few bp. In the European market there was also modest movement in bond yields. 2Y and 10Y German government bonds also just moved a few bp. Furthermore, the spread between the semi-core vs. Germany as well as periphery vs. Germany continue to tighten. Hence, the 10Y Italy vs. Germany spread is close to breaking through 100bp, while the 10Y French vs. German 10Y yield spread has stabilised and is slowly moving towards the 70bp-level. Finally, the Bund ASW-spread has also been rangebound at 0bp to -2bp.

FX: NOK rose and JPY lost ground yesterday ahead of monetary policy decisions from Norges Bank and Bank of Japan with the latter set to hike interest rates tomorrow. EUR/USD was steady yesterday just above 1.04.