Sample Category Title

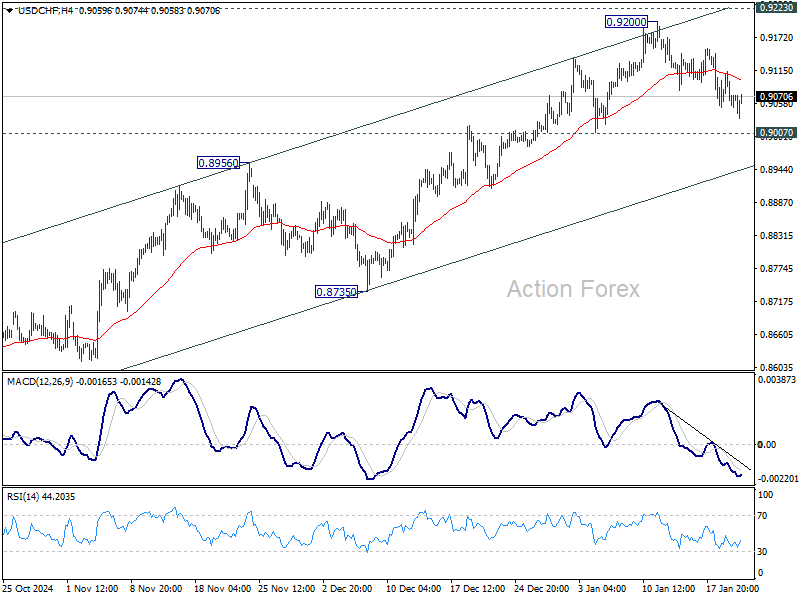

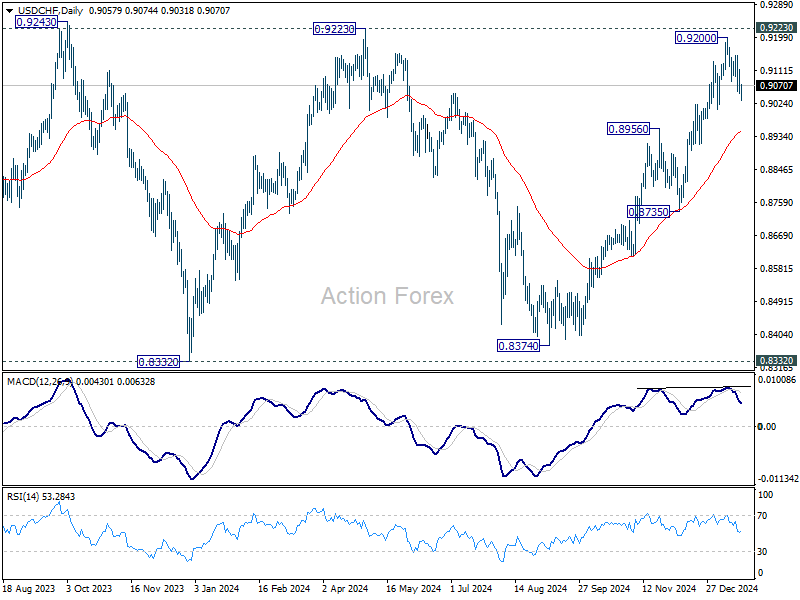

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9032; (P) 0.9077; (R1) 0.9102; More…

Intraday bias in USD/CHF stays neutral for now, as the pair is in mild recovery. Price actions from 0.9200 are seen as a near term corrective pattern only. Further rally is expected with 0.9007 support intact. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 0.8950).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

Dollar Recovery Capped by Stocks Rally, S&P 500 Ready for New Record

Despite being pressured in the past few days, Dollar remains relatively resilient, refusing to drop despite renewed selling pressure earlier today. US President Donald Trump’s tariff rhetoric is having a diminishing effect on markets, as traders shift their attention back to fundamental and intermarket dynamics. The first significant market reaction to tariffs is likely to come only after actual implementation, with the initial measures on Canada, Mexico, and China anticipated on February 1.

A key intermarket factor aiding Dollar’s stability is recovery in US Treasury yields, which is providing some support. However, upside momentum of the greenback is clearly capped by strong risk-on sentiment in equity markets. In particular, S&P 500, currently hovering just inch below its all-time high of 6099.97, is showing robust upward momentum. Decisive break above this level would confirm the resumption of the index’s long term up trend, with upper channel resistance (now at around 6380) as next target.

For the week so far, Japanese Yen is the weakest performer as markets look past BoJ’s expected rate hike on Friday. Dollar follows as the second worst performer, trailed Loonie. In contrast, Kiwi is still leading gains, despite expectations of another 50bps RBNZ rate cut after inflation data. Euro is supported by ECB officials’ reassurances of gradual easing, making it the second-best performer. Aussie Australian Dollar comes in third strongest, with Sterling and Swiss Franc positioned in the middle of the pack.

ECB's Lagarde highlights regular, gradual rate cuts as policy diverges from Fed

ECB President Christine Lagarde emphasized the central bank’s commitment to a “regular, gradual path” of monetary easing, citing progress in disinflation across the Eurozone.

Speaking to CNBC, Lagarde reiterated that the pace of rate cuts will depend on incoming data. Meanwhile, she described the neutral rate — where monetary policy neither stimulates nor restricts the economy — as between 1.75% and 2.25%.

Lagarde also acknowledged the divergence in monetary policy paths between ECB and Fed. She attributed this gap to differing economic circumstances, noting that the two central banks “did not reduce rates at the same pace.” Markets, she said, are pricing in “vastly different monetary policy moves” over the next few months, reflecting these fundamental differences.

On external risks, Lagarde played down concerns about inflation being exported to Europe from the US, suggesting that any reigniting of U.S. inflation would primarily impact the U.S. economy. She added, “We are not overly concerned by the export of inflation to Europe.” However, she acknowledged potential spillover effects through the exchange rate, which “may have consequences.”

SNB's Schlegel: Negative rates remain a tool, despite being unpopular

SNB Chair Martin Schlegel said today at the World Economic Forum in Davos that with the policy rate currently at 0.50%, "we still have some room" for adjustments. But he ruled out any firm commitment on future rate moves.

While negative rates remain an unpopular tool in Switzerland, Schlegel noted that the SNB would reintroduce them if deemed necessary to stabilize monetary conditions.

Looking ahead to the SNB’s next policy meeting in March, Schlegel indicated that the central bank will evaluate whether further rate adjustments are warranted.

"At the moment monetary conditions are appropriate. We decide from quarter to quarter and then we will see," he said, refraining from estimating the likelihood of rates turning negative again.

Schlegel also addressed risks stemming from global uncertainties, particularly the tariff hikes proposed by Trump administration. While he downplayed the direct impact of such measures on Swiss inflation, he acknowledged that heightened global risks could bolster the safe-haven appeal of the Swiss Franc.

"Whenever there is a crisis, investors tend to buy the Swiss Franc," Schlegel said, highlighting the currency’s role in monetary conditions alongside interest rates.

New Zealand CPI unchanged at 2.2% yoy, non-tradeable pressures persist

New Zealand’s CPI rose 0.5% qoq in Q4 2024, in line with expectations, as tradeable inflation increased 0.3% qoq and non-tradeable inflation rose 0.7% qoq. Annually, CPI was unchanged at 2.2% yoy, slightly exceeding the anticipated 2.1% yoy. This marks the second consecutive quarter that inflation has stayed within RBNZ's target range of 1% to 3%.

The data highlights diverging trends within inflation components. Non-tradeable inflation, which reflects domestic demand and supply conditions and excludes foreign competition, stood at 4.5% yoy, highlighting persistent internal price pressures. Tradeable inflation, influenced by global factors, recorded a -1.1% yoy decline.

Rent prices were the largest contributor to the annual CPI increase, rising 4.2% and accounting for nearly 20% of the overall 2.2% gain. Lower petrol prices, down -9.2% yoy, offset some of the upward momentum, with CPI excluding petrol increasing 2.7% yoy.

Australia's Westpac Leading Index falls to 0.25%, signals gradual growth pickup

Westpac Leading Index for Australia dipped slightly in December, moving from 0.33% to 0.25%. Westpac noted that while the growth signal remains modest, it reflects a marked improvement from the consistently negative and below-trend readings observed over the past two years. This uptick hints at a gradual lift in economic momentum through the first half of 2025.

Westpac forecasts GDP growth to improve steadily over the course of 2025, projecting a year-end expansion of 2.2%—a notable recovery from the weak 0.8% growth recorded in the year to September 2024. However, the bank noted that while this represents progress, it remains below the economy’s long-term potential.

Westpac highlighted that recent improvements in the Leading Index coincide with mixed signals on broader economy. A key concern for RBA is the labor market, where the "rebalancing" stalled in H2 2024.

"A further slowdown in underlying measures of inflation could still see the Bank ease in February or April but we suspect the RBA will need to be more comfortable about some of these risks before it is prepared to begin easing," Westpac noted.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9032; (P) 0.9077; (R1) 0.9102; More…

Intraday bias in USD/CHF stays neutral for now, as the pair is in mild recovery. Price actions from 0.9200 are seen as a near term corrective pattern only. Further rally is expected with 0.9007 support intact. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will turn bias back to the downside for deeper pull back to 55 D EMA (now at 0.8950).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

Sunset Market Commentary

Markets

Stock markets took central stage today. Netflix record-breaking earnings and US president Trump’s massive AI infrastructure project (“Stargate”, planning to spend $100bn on Big Tech infrastructure projects, with the figure rising to $500bn (!) over the next four years) gave European and US equity indices even more momentum. The likes of the German Dax, French CAC 40 and EuroStoxx 50 gain around 1%. US benchmarks open up to 0.50% higher with the tech-heavy Nasdaq outperforming (+1%). It overshadowed the looming 10% tariff threat from US President Trump against China which in the end is of course less than the earlier 60% warning. Simultaneously there is some early hope that the Russian conflict in Ukraine might finally be drawing to an end, which starts showing in CE space. Positive risk sentiment marginally supported the euro. EUR/USD set an intraday high around 1.0450 from a start above 1.04, but is currently back at 1.0425. EUR/GBP took a fresh aim at 0.8448/63 resistance on soaring budget deficit data (£129.9bn for the first nine months of the fiscal year, £4.1bn above forecast), but a break didn’t occur. EMU and UK PMI confidence data on Friday offer another possibility. In absence of eco data, there was also some fuzz about Spain’s record-breaking syndicated 10-yr benchmark deal. They received a record €143bn in orders, allowing them to sell €15bn at 5 bps over the Spanish curve compared with guidance in the +8 bps area. There was plenty of ECB rhetoric on the sidelines of the World Economic Forum in Davos but they don’t move the needle in the central bank’s compass nor in market thinking on future policy. Generally speaking, we think that there is a very broad consensus to keep with 25 bps rate cuts at the January and March meetings. Depending on the nature of the ECB speaker (dove-centrist-hawk), the cutting cycle cut might even stretch until April or June. It’s also clear that there’s very little appetite at the moment to take the policy rate even lower. EMU money markets discount a cumulative 75 bps rate cuts in H1 of this year with a final 25 bps move somewhere during H2 2025. Daily changes on European and US curve are limited to 1 bp.

News & Views

Polish industrial production was down 8% m/m in December. Such a steep drop by year’s end is not unusual but even taking into account seasonal effects, IP was 1.1% lower on the month. Production over the whole of 2024 was 0.6% lower (SA) compared to the same month in 2023. With the December data out, Polish industrial production is back to square one with output basically flat already since mid-2022. The disappointing results also lowered KBC Economics’ GDP nowcast to slightly below 3% for 2024. Polish wage growth (4% m/m, 9.8% y/y) also missed the bar for December but remains quick enough to offset <5% inflation. Such rapid real wage growth is expected to promote private consumption to the main economic growth driver going forward. Employment fell by 0.1% at the end of the year, lowering the y/y-reading from -0.5% to -0.6% - the lowest since March 2021. PPI numbers, finally, came in at 0.2% m/m and -2.6% y/y, also marginally below analysts’ estimates. The Polish zloty couldn’t care less about the weakish data set though. It is instead eyeing a hawkish central bank that’s been sticking to a higher-for-longer narrative for quite some time now. With the help of a constructive risk environment PLN pushes beyond tough resistance around EUR/PLN 4.25 and currently even beyond the December PLN high of 4.23.

Speaking in Davos, Swiss National Bank president Schlegel defended the use of FX interventions saying they have worked in the past and added that policymakers would use it as a tool again if needed. He shrugged off the possibility of being labeled a currency manipulator by the Trump administration anew, which is what they did during Trump’s first term over the SNB’s previous large-scale interventions. But Schlegel also said that they are not considering a new cap on the franc for the time being. The SNB president noted their primary tool remains the policy rate and repeated they won’t shy away from going back subzero if circumstances require so. The Swiss policy rate currently stands at 0.5% after a large 50 bps cut mid-December. The Swiss franc trades unchanged against the euro around EUR/CHF 0.945. This compares to the 0.9206 briefly seen end of November, which was the strongest CHF level on record – barring the huge volatility spike higher in the wake of the SNB releasing the CHF cap in early 2015.

EUR/USD Technical Outlook: Is EUR/USD Poised for Potential 800-pip Rally?

- EUR/USD has seen a recent rally driven by market reactions to the incoming Trump administration.

- A divergence exists between technical analysis, suggesting further upside potential, and fundamental factors, pointing towards potential weakness due to policy divergence between the ECB and FED.

- Key support levels for EUR/USD are 1.0425, 1.0350, and 1.0293, while resistance levels are 1.0500, 1.0600, and 1.0700.

EUR/USD Fundamental Backdrop

EUR/USD has been on an offensive since Monday but does appear to be running out of steam. There are both technical and fundamental factors currently to consider and this makes EUR/USD an even more intriguing prospect to analyze.

The obvious factor behind the moves this week has been the incoming US administration under Donald Trump as markets continue to grapple with the prospect of tariffs and its impact on the US Dollar. Just yesterday President Trump vowed duties on European imports without giving much detail adding to market uncertainty.

However, there is also a growing belief that policy divergence may be even more severe under a Trump Presidency especially if the tariff threat becomes a reality. ECB policymaker Villeroy has attempted to downplay this by saying that a decoupling between the ECB and FED on rate is not an issue.

However, if this gap widens EUR/USD risks dropping below parity as sluggish growth and a host of problems continue to plague Europe’s largest economies. According to LSEG data, markets are currently pricing in around 95 bps of cuts from the ECB through December 2025, while pricing in around 39 bps for the Federal Reserve over the same period.

If this gap continues to widen, the Euro may lose significant ground to the Greenback which could affect every consumer and ratchet up pressure on the ECB.

Technical Vs Fundamental Outlook – Growing Divergence

There has always been a school of thought that the Technical and Fundamental pictures when looking at any instrument kind of complement each other. Off late however, EUR/USD has seen this case put to the test as the movement of EUR/USD this week is at odds with the overarching fundamentals discussed above.

The move unfolding in EUR/USD has been touted a s potential deeper retracement following the protracted selloff that began at the back-end of September. However, looking at the technicals, both price action and chart patterns are hinting at the start of a big move to the upside.

Technical Analysis on EUR/USD

EUR/USD Daily Chart, January 22, 2025

Source: TradingView.com (click to enlarge)

Looking at EUR/USD daily chart above and as you can see EUR/USD appears to have bottomed out on January 13 before beginning its impressive move higher.

The move was sparked by President Trump on Monday where EUR/USD rose around 120 pips or 1.45%. What intrigues most about the pair is where price currently rests. Price is testing the long-term descending trendline with a daily candle close above likely to encourage bulls and thus stimulate more buying pressure.

EUR/USD Four-Hour (H4) Chart, January 22, 2025

Source: TradingView.com (click to enlarge)

Dropping down to a four-hour chart, we have already had a candle close above the trendline, a retest and continuation with a fresh high on the H4 chart printed this morning.

All of this bodes well for further upside despite the fundamental picture as mentioned.

If EUR/USD is able to sustain its bullish advance, immediate resistance rests at the 1.0500 handle before the 1.0600 and 1.0700 levels come into focus.

A rejection here, or failure to kick on could leave EUR/USD vulnerable to retest key support at 1.0425 before the 1.0350 and 1.0293 handles come into focus.

Support

- 1.0425

- 1.0350

- 1.0293

Resistance

- 1.0500

- 1.0600

- 1.0700

NZ Inflation Unchanged, NZ Dollar Under Pressure

The New Zealand dollar dropped as much as 0.5% earlier today but has recovered. In the European session, NZD/USD is trading at 0.5684, up 0.10% on the day.

New Zealand inflation unchanged at 2.2%

New Zealand CPI, released quarterly, was unchanged in the fourth quarter at 2.2% y/y. This was slightly above the market estimate of 2.1% but marked the lowest inflation rate since March 2021. Transportation prices fell but food and housing prices rose at a faster pace than in the third quarter. On a quarterly basis, CPI ticked lower to 0.5%, down from 0.6% in Q3 and below the market estimate of 0.5%.

The inflation report didn’t show much change in CPI and the Reserve Bank of New Zealand remains on course to deliver a jumbo half-point cut at its meeting on Feb. 19. The markets have fully priced in a rate cut at that meeting, with a 66% probability of a half-point cut and a 33% likelihood of a quarter-point cut.

The RBNZ last met in November and slashed rates by a half-point at that time. The central bank has been aggressive in its easing cycle but the cash rate remains high at 4.25%. The RBNZ is expected to deliver a series of rate cuts in order to boost the weak economy, provided that inflation does not rebound higher.

There are no tier-events out of the US today. On Thursday, the US releases unemployment claims and President Trump will address the World Economic Forum. Trump’s comments on Monday, his first day in office, sent the US dollar sharply lower against the major currencies after he announced that he was delaying his trade tariffs until at least Feb. 1.

NZD/USD Technical

- NZD/USD tested support at 0.5662 earlier. Below, there is support at 0.5634

- There is resistance at 0.5706 and 0.5734

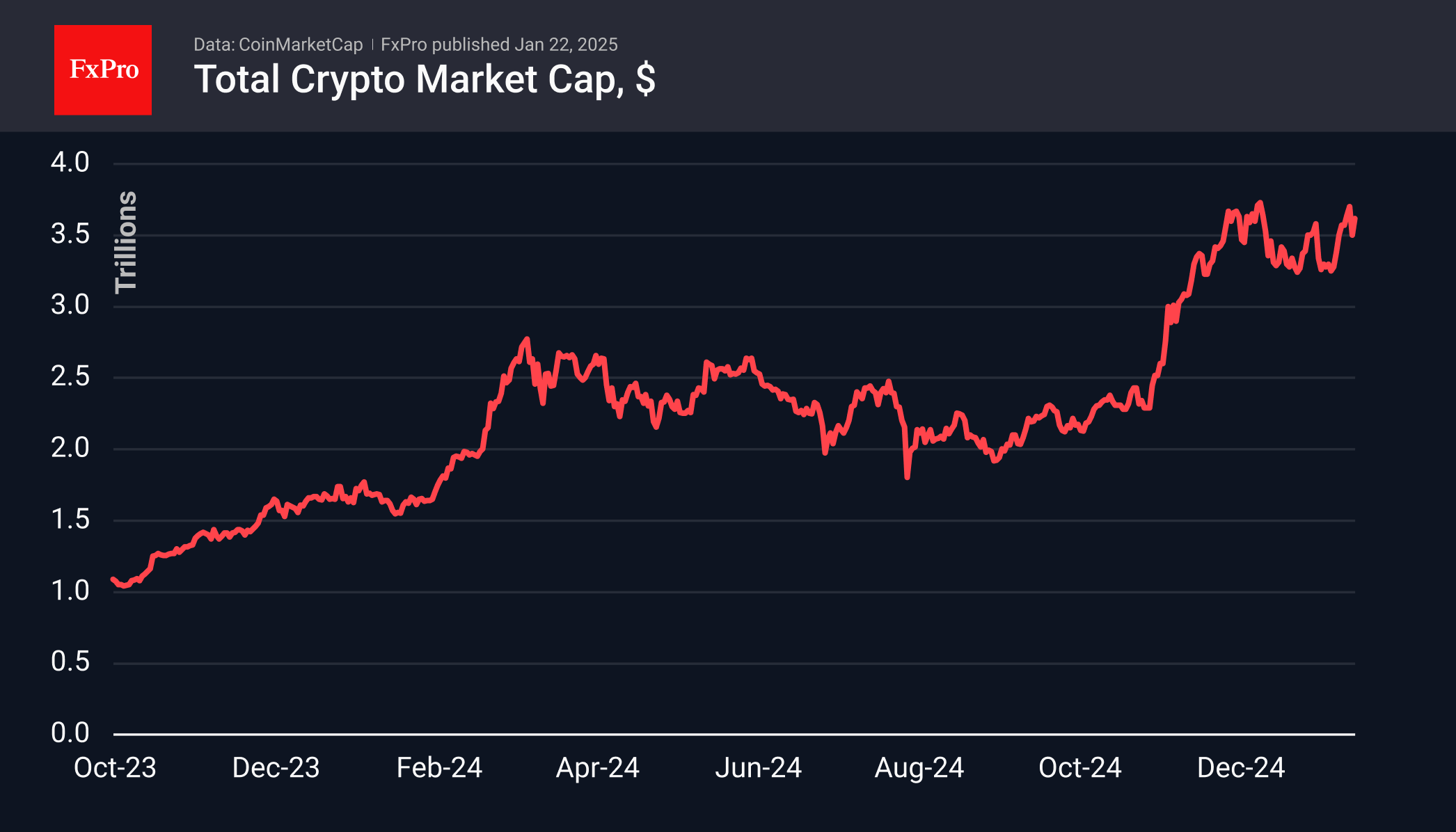

The Plateau of Crypto

Market picture

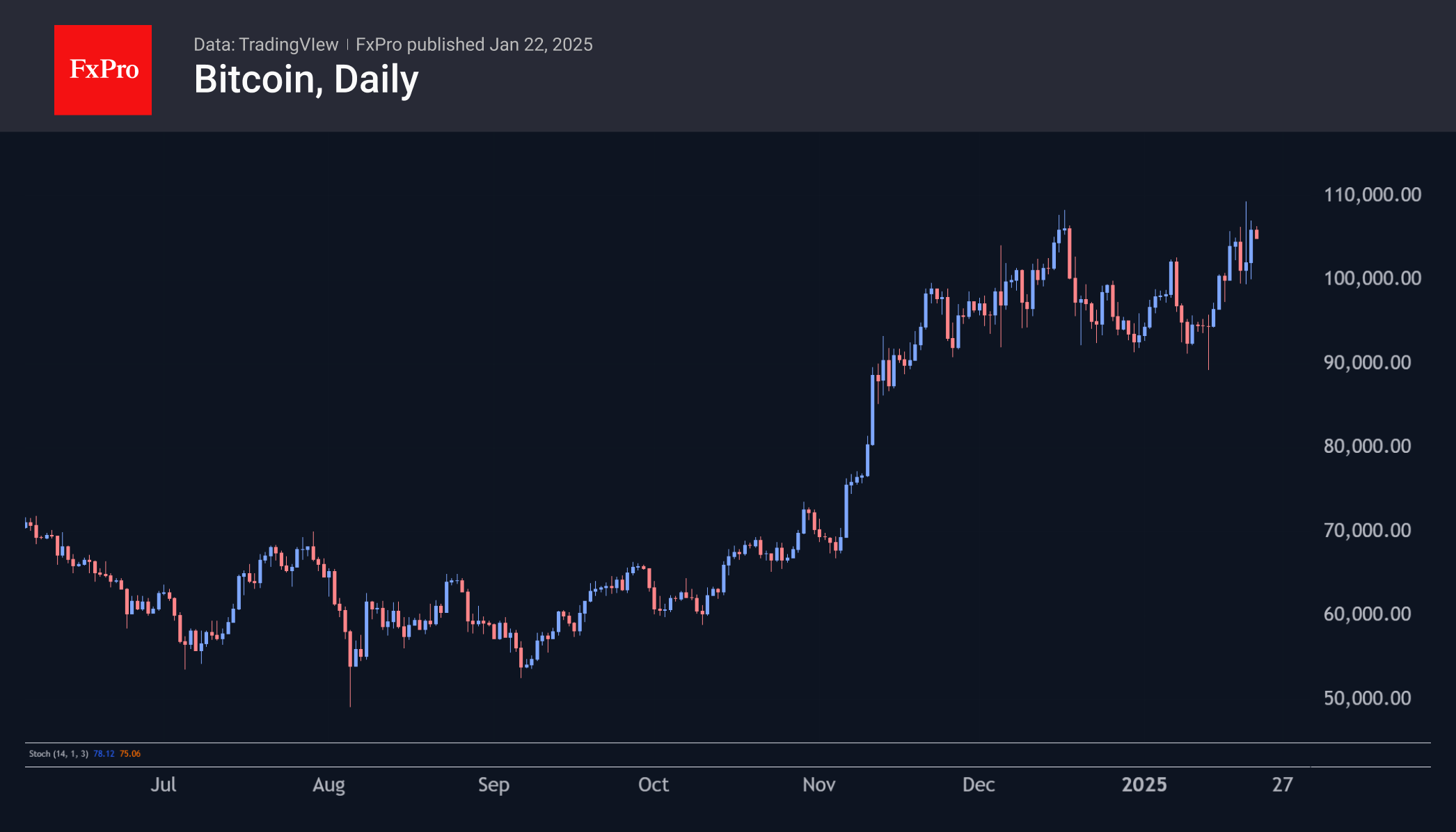

The cryptocurrency market rose 3.5% in the last 24 hours, recovering to $3.63 trillion, having peaked in the last five days. The market’s rapid recovery is indicative of continued interest in risk assets. Despite the day’s rise in altcoins, they remain well below their recent highs, accentuating the performance of Bitcoin, which is close to its all-time highs.

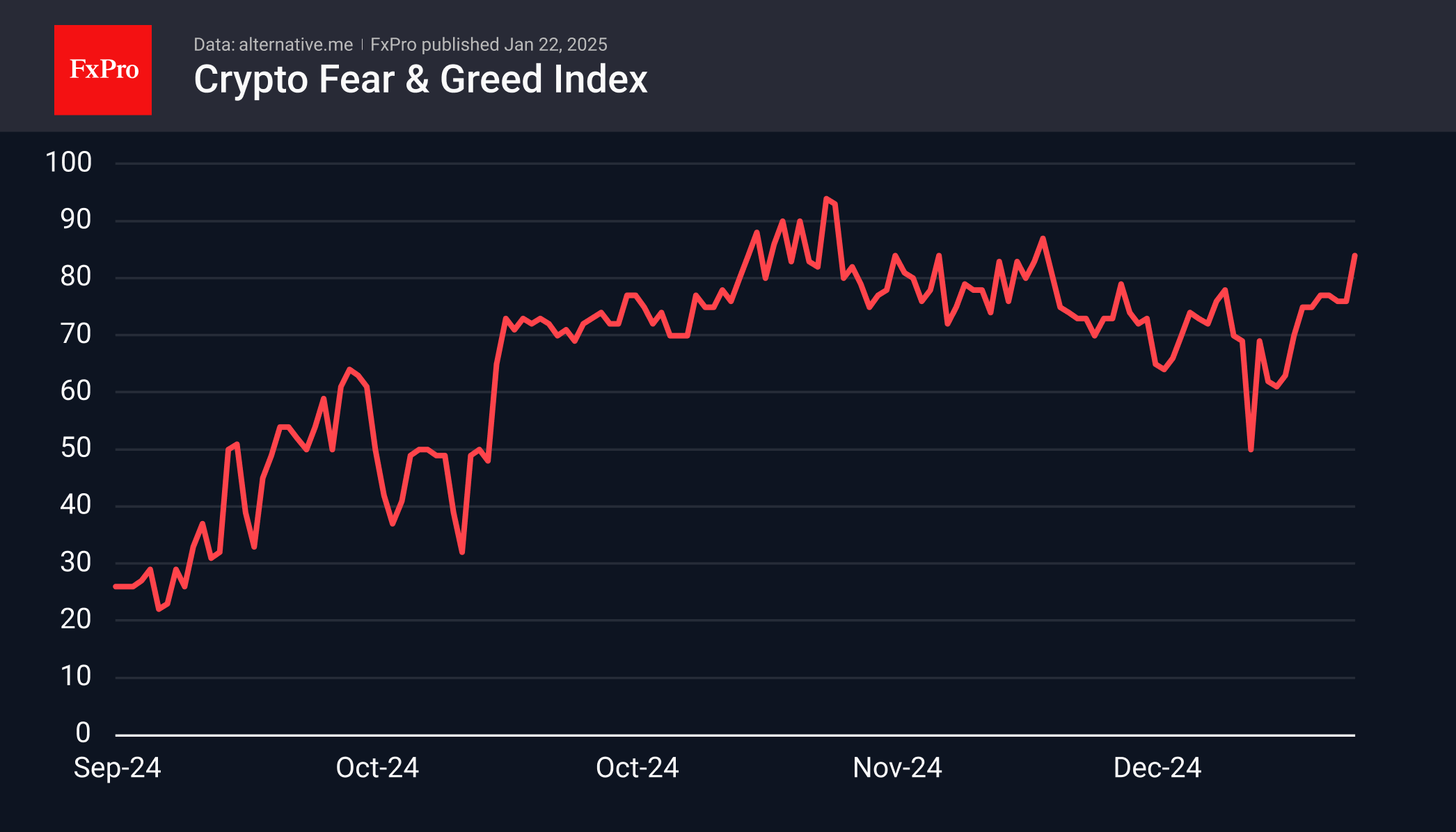

The Cryptocurrency Market Sentiment Index increased by 8 to 84 (extreme greed), the highest in the last five weeks. In mid-December, a similar level of sentiment led to a five-day sell-off.

Bitcoin traded near the $105K mark. It was quickly bought back on Tuesday when it fell to $101K, but when it reached the $107K level early Wednesday afternoon, the market shifted to sellers. Clearly, optimism is high in the market, but an additional factor is needed for new momentum.

News background

News background

The Block recorded an increase in the number of enquiries on the topic of Bitcoin, interpreting this as a leading indicator of stronger retail investment inflows. The number of mentions of Bitcoin in X last week doubled from the previous week to 495 thousand. On Google Trends, the number of ‘how to buy cryptocurrency’ queries reached an all-time high.

Dogecoin showed significant growth after the US government’s Department of Government Efficiency (DOGE) published the Dogecoin meme cryptocurrency logo on its official website.

Last week, MicroStrategy acquired an additional 11,000 BTC through the sale of ~$1.1bn worth of shares at an average price of around $101,191 per coin. The company holds 461,000 BTC on its balance sheet, acquired for a combined $29.3bn at an average price of $63,610.

On 21 January, Telegram and the TON Foundation announced an exclusive agreement requiring embedded Web3 applications to use the TON network exclusively. Existing wallet protocols for third-party networks will be prohibited, except for applications with cross-chain functionality.

SNB’s Schlegel: Negative rates remain a tool, despite being unpopular

SNB Chair Martin Schlegel said today at the World Economic Forum in Davos that with the policy rate currently at 0.50%, "we still have some room" for adjustments. But he ruled out any firm commitment on future rate moves.

While negative rates remain an unpopular tool in Switzerland, Schlegel noted that the SNB would reintroduce them if deemed necessary to stabilize monetary conditions.

Looking ahead to the SNB’s next policy meeting in March, Schlegel indicated that the central bank will evaluate whether further rate adjustments are warranted.

"At the moment monetary conditions are appropriate. We decide from quarter to quarter and then we will see," he said, refraining from estimating the likelihood of rates turning negative again.

Schlegel also addressed risks stemming from global uncertainties, particularly the tariff hikes proposed by Trump administration. While he downplayed the direct impact of such measures on Swiss inflation, he acknowledged that heightened global risks could bolster the safe-haven appeal of the Swiss Franc.

"Whenever there is a crisis, investors tend to buy the Swiss Franc," Schlegel said, highlighting the currency’s role in monetary conditions alongside interest rates.

ECB’s Lagarde highlights regular, gradual rate cuts as policy diverges from Fed

ECB President Christine Lagarde emphasized the central bank’s commitment to a “regular, gradual path” of monetary easing, citing progress in disinflation across the Eurozone.

Speaking to CNBC, Lagarde reiterated that the pace of rate cuts will depend on incoming data. Meanwhile, she described the neutral rate — where monetary policy neither stimulates nor restricts the economy — as between 1.75% and 2.25%.

Lagarde also acknowledged the divergence in monetary policy paths between ECB and Fed. She attributed this gap to differing economic circumstances, noting that the two central banks “did not reduce rates at the same pace.” Markets, she said, are pricing in “vastly different monetary policy moves” over the next few months, reflecting these fundamental differences.

On external risks, Lagarde played down concerns about inflation being exported to Europe from the US, suggesting that any reigniting of U.S. inflation would primarily impact the U.S. economy. She added, “We are not overly concerned by the export of inflation to Europe.” However, she acknowledged potential spillover effects through the exchange rate, which “may have consequences.”

Gold Rises Further on Uncertainties over US Trade Policies, Weaker Dollar

Gold price hit new multi-week high early Wednesday, in extension of Tuesday’s 1.4% advance, with near-term action being well supported by strong safe haven demand on fresh uncertainties over Trump’s trade policies that weakened dollar and wide expectations that the Fed will keep interest rates on hold in the policy meeting next week.

Bull leg above $2700 level extends into third consecutive day, as Tuesday’s close above pivotal barriers at $2721/26 (former double top) and $2730 (Fibo 76.4% of $2790/$2536) generated strong bullish signal.

Bulls eye new record high ($2790, hit in Oct 2024) and psychological $2800 barrier, but will likely consolidate before final attack.

Overbought conditions on daily chart and south-turning 14-d momentum signal that bulls already started to face headwinds.

Dips should ideally find support at $2730/20 zone (former pivotal barriers) to mark a healthy correction and offer better levels to re-enter bullish market, however, larger picture is expected to remain biased higher if deeper dips stay above $2700 zone.

Res: 2762; 2774; 2790; 2800.

Sup: 2741; 2730; 2721; 2700.

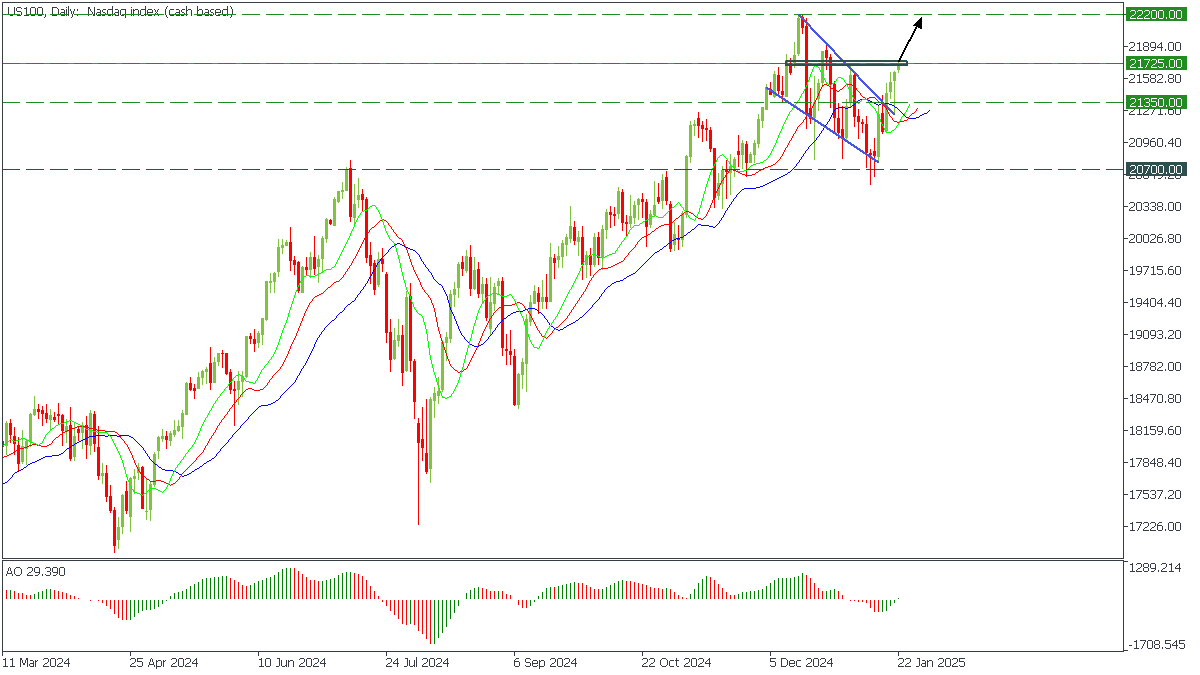

US100: Way to ATH

US100, Daily

US100 broke the upper trendline of the descending channel after a short-term decline. Lips crossed the jaw on the Alligator, and AO indicates rising bullish sentiment.

- In this case, we can consider buying US100 on the break of 21725 resistance with a target up to 22200;