Sample Category Title

Dollar Resilience Basically Remained in Place

Markets

The correction in US yields that started on (marginally) softer than expected US CPI data and comments from Fed Waller finally met first support on Friday as markets returned their focus to the new Trump era. Solid US housing and production data helped build this floor. US yields in a bear flattening move added between 5.3 bps (2-y) and 0.2 bps (30-y). EMU/German yields intraday also showed signs of bottoming but still closed the day in red (German 2-y -0.1 bp, 30-y -2.0 bps). Still, the yields’ move didn’t change the constructive bias on global equity markets. US indices closed the session up to 1.5% higher (Nasdaq). Europe this time slightly underperformed the US (EuroStoxx50 +0.81%), but the index still firmly confirmed the break above the cycle top. Last week’s setback in the USD on lower US yields and the broader risk-on mostly remained modest and this dollar resilience basically remained in place at the end of last week. At 109.35, DYX still closed the week within striking distance of the correction top (110 area) reached on Monday. EUR/USD extended the short-term consolidation pattern (close 1.0273), but in this process last week failed to challenge any significant resistance level, suggesting that underlying USD strength/euro weakness still remained in place. UK and sterling trailed as weaker-than-expected retail sales confirmed a mediocre narrative on the economy as the government tries to convince the country and markets on the viability of its economic/budgetary policy. EUR/GBP (0.8442) closed the week near the 0.845 resistance area.

Asian equity markets mostly open in positive territory. Regional investors apparently take comfort from the headlines on a what was said to have been a good conversation between Donald Trump and Chinese leader Xi Jinping. ECB Board member Isabel Schnabel in an interview with Finanztip this weekend indicated that for now she sees no major risk that could prevent the bank from reaching the 2.0% target, allowing it to continue its easing cycle. However, after steep rate cuts executed of late, she said that the point is coming closer for the bank to evaluate whether and to what extent the ECB can cut rates further.

Today’s calendar in Europe is empty and US markets are closed in observance of Martin Luther King day. All eyes evidently will be on Washington as Donald Trump will be sworn in as the 47th president of the US. The president is expected to announce an avalanche of executive orders in the first hours/days after taking office, with sweeping measures to be announced on migration, tariffs, deregulation and American energy policy amongst others. The wide scope of potential surprises makes a consistent market reaction not evident, but the focus likely will be on the pace and nature of the first import tariffs. Visibility on longer-term market impact/reaction function stays low, but we assume that even ‘disruptive’ Trump measures won’t be disruptive for the Trump trade in a first instance. (US) yields might to look for a bottom after last week’s correction. The 4.20% area serves as a first support area for the US 2-y yield. The 1.0400/1.0450 area remains strong resistance for the EUR/USD cross rate.

News & Views

Average asking prices for newly listed UK homes rose by 1.7% M/M in January to be 1.8% higher compared with the same period last year. The nominal average price of £366 189 is only £9k below the peak hit in May of last year. Other signs of momentum come from increases in agreed sales (+11% Y/Y), the number of buyers contacting agents about properties (+9% Y/Y) and the number of new properties coming to the market (+11% Y/Y). Property website Rightmove, who conducted the survey, said that current drive could rapidly peter out should hopes on BoE rate cuts not materialize as they are key in reducing mortgage rates. April’s expiry of a lower rate of property purchase tax on less expensive homes is seen as currently boosting demand but equally represents a risk from Q2 onwards for momentum to be sustained.

The German conservative opposition block CDU/CSU polled a first time below 30% since April in the run-up to February 23 parliamentary elections. They maintained their lead over the far-right AfD though which also dropped a point to 21%. Support for social Democrats of Chancellor Scholz (16%) and greens (13%) was unchanged with relative gains going to smaller parties. With centre-left and centre-right all refusing a tie-up with AfD, election night will decide on whether CDU/CSU-leader Merz will be able to set-up his preferred two-way coalition or whether he’ll have to explore the three-way alliance.

GBP/USD Under Pressure, USD/CAD Powers Higher

GBP/USD started a fresh decline below the 1.2320 zone. USD/CAD is rising and might aim for more gains above the 1.4500 resistance.

Important Takeaways for GBP/USD and USD/CAD Analysis Today

- The British Pound started another decline from the 1.2320 resistance zone.

- There is a short-term bearish trend line forming with resistance at 1.2205 on the hourly chart of GBP/USD at FXOpen.

- USD/CAD is showing positive signs above the 1.4400 support zone.

- There is a key bullish trend line forming with support at 1.4420 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair struggled to continue higher above the 1.2320 resistance zone. The British Pound started a fresh decline and traded below the 1.2270 support zone against the US Dollar, as discussed in the previous analysis.

The pair even traded below 1.2250 and the 50-hour simple moving average. Finally, the bulls appeared near the 1.2100 level. The recent swing low was formed at 1.2160 and the pair is now consolidating losses.

Immediate resistance on the upside is near a short-term bearish trend line at 1.2205. The first major resistance is near the 1.2230 zone and the 50% Fib retracement level of the downward move from the 1.2305 swing high to the 1.2160 low.

The main hurdle sits at 1.2270 and the 76.4% Fib retracement level of the downward move from the 1.2305 swing high to the 1.2160 low. A close above the 1.2270 resistance might spark a steady upward move.

The next major resistance is near the 1.2305 zone. Any more gains could lead the pair toward the 1.2320 resistance in the near term.

Initial support on the GBP/USD chart sits at 1.2160. The next major support sits at 1.2140, below which there is a risk of another sharp decline. In the stated case, the pair could drop toward 1.2100.

USD/CAD Technical Analysis

On the hourly chart of USD/CAD at FXOpen, the pair formed a strong support base above the 1.4300 level. The US Dollar started a fresh increase above the 1.4345 resistance against the Canadian Dollar.

The bulls pushed the pair above the 1.4380 and 1.4400 levels. The pair cleared the 50-hour simple moving average and climbed above 1.4450. A high was formed at 1.4485 and the pair recently corrected some gains.

There was a move toward the 23.6% Fib retracement level of the upward move from the 1.4302 swing low to the 1.4485 high. Initial support is near the 1.4420 level.

There is also a key bullish trend line forming with support at 1.4420. The next major support is near the 1.4395 level or the 50% Fib retracement level of the upward move from the 1.4302 swing low to the 1.4485 high.

The main support sits near the 1.4345 zone on the same USD/CAD chart. A downside break below the 1.4345 level could push the pair further lower. The next major support is near the 1.4300 support zone, below which the pair might visit 1.4250.

If there is another increase, the pair might face resistance near the 1.4485 level. A clear upside break above 1.4485 could start another steady increase. The next major resistance is the 1.4540 level.

A close above the 1.4540 level might send the pair toward the 1.4580 level. Any more gains could open the doors for a test of the 1.4620 level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Trump and Coin

After a few weeks of hesitation around the beginning of the new year, the equity bulls finally returned to the market last week on the back of a set of slower-than-expected inflation figures from both the US and the UK, and a set of stronger-than-expected US big bank results. The global bond yields retreated in the developed world from a peak reached earlier last week and let the equities take a breather. The US equity indices posted their best weekly performance since the US post-election rally of last year, and the non-tech sectors performed better than their tech peers. Both Nasdaq and the S&P500 closed the week above the downtrending channel top building since mid-December, while the Dow Jones recovered half of losses that it had accumulated after hitting a record high back in December 5th and outperformed its US peers. The more cyclical Stoxx 600 stocks gained around 2.40% – a bit less than their US peers, while the FTSE 100 rallied more than 3% to an ATH level.

In the FX, the US Dollar retreated on the back of soft CPI and softening Federal Reserve (Fed) expectations, leading to a slow down of the selloff in the EURUSD and Cable. The euro is trying to hang on to the 1.03 level this morning, while Cable is drilling past the 1.22 at the time of writing. The USDJPY, on the other hand, starts the week in favour of the Japanese yen as the Bank of Japan (BoJ) is expected to announce a rate hike this Friday – with hope that their action won’t send a shockwave across the global financial markets as it had been the case in summer 2023, and on hope that Trump’s policies won’t have a dramatic impact on the Japanese fundamentals.

The Trump and coin

Today, Donald Trump will be sworn in and officially move into the White House. A good part of Trump trade has already happened – the small and mid-caps rallied, energy and financials outperformed and cryptocurrencies touched the sky. Therefore, the first week under Trump may not bring a lot of surprises... (but it may as well!) The WSJ writes that Donald Trump has already prepared 100 – yes 100 – executive orders to take swift action after today’s inauguration, including an order to make crypto a policy priority and giving insiders of the crypto market a good voice within his administration.

Trump launched a cryptocurrency of his own on the Solana blockchain and the coin gained up to 600% in three days reaching a $15bn capitalization before easing – a little bit – also sending Solana to a fresh record high.

But beyond that optimism, Trump policies are expected to be a double-edged sword. His pro-growth policies and deregulation are expected to benefit to the US economy but his tariff policies will certainly lead inflation higher and soften the Fed doves’ hands for easing policy. In addition, exploding debt levels will likely further push the borrowing costs higher.

Optimism in Asia

The week kicks off on a positive note in Asia. Tiktok is back and running in the US after a short blackout during the weekend. Donald Trump wants to extend the deadline for the company to find US partners to continue running the popular social media platform in the US. And Trump optimism goes beyond that. He and Xi Jinping held ‘a very good’ phone call to ‘make the world more peaceful and safe’. The Chinese CSI 300 is up this Monday although the People’s Bank of China (PBoC) kept its lending rates unchanged for the third straight month to contain the downside pressure on the yuan, the 10-year yield is trying to push higher...

Earnings

This week, big names including Netflix, P&G and American Express will go to the earnings confessional. The S&P500 companies are expected to print an almost 12% earnings growth in Q4. Pulling the Magnificent 7 out of the equation, the S&P500’s earnings growth is expected to be around 4%. Strong earnings and prospects of further rate cuts – though slower – could give support to equity valuations.

Oil rally slows near $80pb

Crude oil’s 20% rally since December 10th sees strong resistance above the $80pb level and the six-week ceasefire deal in Gaza helps easing the price of a barrel this Monday. But geopolitical risks prevail with Trump aiming to go after Russian oil giants, Iran and Venezuela. The IEA not expects a lower output surplus this year and the latter should give support to oil prices. Minor support is seen near the $77.30pb level – the minor 23.6% Fibonacci retracement on the latest rebound, and the major support stands near the $75.30/40pb region that shelters the major 38.2% retracement and the 200-DMA.

Trump’s Inauguration Day

In focus today

The main focus of the week is Donald Trump's 2nd Inauguration which takes place today at 18:00 CET. He will be officially sworn in as the President of the US and markets will closely follow his first executive orders and remarks to the public in the evening with special focus on possible tariff announcements and cuts to regulation.

Otherwise, the week ahead will be relatively quiet on the data front, with the exception of Friday when flash PMIs for both the euro area and the US are released. Financial markets have been particularly attentive to this indicator as focus has shifted to growth following the continued lower inflation momentum movements observed recently in especially the euro Area.

Economic and market news

What happened overnight

In the US, President Trump reiterated his pledge to initiate the largest deportation effort in US history on day one, aiming to remove millions of immigrants and implement stricter immigration limits.

What happened over the weekend

In the euro area, final HICP data came in at expected levels with 0.4% m/m and 2.4% y/y for December on Friday. In the details, momentum continued lower for the eighth consecutive month, now standing at 3.5% in the 3m/3m SAAR measure. The easing momentum will cause the yearly inflation rate to also decline significantly this year, which was acknowledged by the ECB at the December meeting. Hence, underlying inflation clearly continued to give green light for further rate cuts by the ECB.

In the US, industrial production for December overshot expectations at 0.9% (cons: 0.3%, prior: -0.1%) and data for November was revised up to 0.2% from -0.1%. The increase was supported by a rise in factory output, suggesting that manufacturing is stabilizing after two years of weakness.

In China, USD/CNH dropped from 7.355 to below 7.34 following Trump writing on Truth Social that he had a very good call with Xi Jinping. The message by Trump eased concerns over a trade war, saying he expects they will solve many problems together. Read more in China Flash - GDP surprises upwards but housing stabilisation more important, 17 January.

In the Middle East, a ceasefire deal took effect between Isreal and Hamas following 15 months of war between the two. The ceasefire was postponed by three hours due to a holdup in the release of three Israeli hostages. The deal acts as the first of three potential phases set to follow further negotiations in the weeks ahead. With the second phase including a complete withdrawal of Israeli troops from Gaza and the third phase including Gaza's reconstruction.

Equities: Global equities rose on Friday and for the week, following what we consider an almost full complement of support for equities last week. We saw a soft US inflation print, which sent yields lower, generally strong demand data, a very strong start to the earnings season, and finally, geopolitical improvement with the ceasefire in Gaza. Therefore, in our opinion, it should not be surprising to see global equities up by 2.5% last week, led by cyclical stocks, bringing the MSCI back to just 1% shy of its all-time high. In the US on Friday, the Dow rose by 0.8%, the S&P 500 by 1.0%, the Nasdaq by 1.5%, and the Russell 2000 by 0.4%. This morning, most Asian markets are in the green, led by Chinese shares in Hong Kong, while South Korean equities are underperforming. US and European futures are fluctuating around Friday's close.

FI: The bond market recovered modestly last week on the back soft US inflation data and comments from Federal Reserve's Waller. However, the 10Y US treasury yield has risen some 100bp since September, and with the inauguration of Trump today sentiment can change quickly.

FX: USD rose against the rest of the G10 on Friday ahead of President Trump's inauguration today. NOK in particular was under pressure, but JPY, CAD and GBP also felt the heat. EUR/USD traded around the 1.03 level and EUR/NOK rose firmly above 11.70.

What Next: Trump 2.0 and BoJ Hike

On Monday, January 20th, U.S. markets are closed for Martin Luther King Day celebrations, which will affect the trading hours of exchange-traded instruments such as U.S. stocks, indices and futures. Trump’s inauguration is scheduled for the same day, which may affect trading dynamics in the currency market and global stock markets.

On Tuesday, the dynamics of the Canadian dollar can be affected by the report on consumer inflation. Since August, this indicator has fallen to the 2% target for the Bank of Canada, allowing it to reduce the rate to support the economy. But the big question now is whether the 7% inflation rate spurred the Loonie’s collapse over the last quarter. A CPI acceleration could support the Canadian dollar on a reassessment of the outlook.

The Bank of Japan may raise its key rate Friday morning, marking the third increase in nearly a year. This very Japanese-style leisurely phase of policy normalisation is likely to continue, guided by the Rising Sun’s long-term government bond yields flying to all-time highs. The tightening of the policy could provide fundamental support to the Japanese yen.

Also, on Friday, the preliminary estimates of PMI indices for European countries will be released. These are often very influential indicators that can visibly affect the dynamics of the euro, especially for Germany.

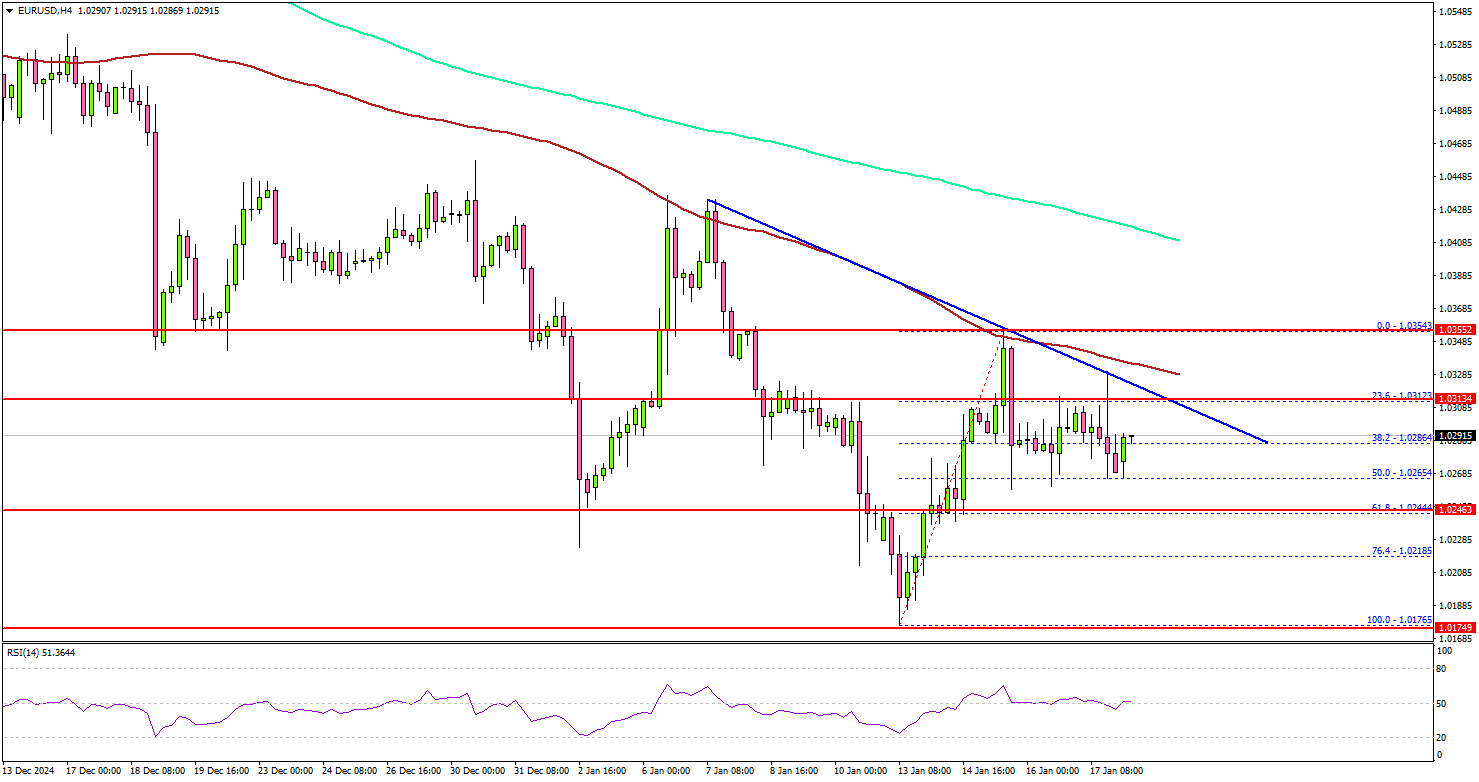

EUR/USD Faces Uphill Battle: Will Bulls Regain Momentum?

Key Highlights

- EUR/USD started a consolidation phase below the 1.0350 resistance.

- A major bearish trend line is forming with resistance at 1.0315 on the 4-hour chart.

- GBP/USD is consolidation losses below the 1.0320 resistance.

- Crude oil prices rallies toward $80.00 before it corrected some gains.

EUR/USD Technical Analysis

The Euro remained in a bearish zone below 1.0350 against the US Dollar. EUR/USD even extended losses and traded below the 1.0220 support.

Looking at the 4-hour chart, the pair traded as low as 1.0176 and is currently consolidating losses. There was a close below the 1.0350 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

It seems to be facing resistance near the 1.0300 and 1.0315 levels. The next major resistance is near the 1.0350 level. A close above the 1.0350 level could set the tone for another increase. In the stated case, the pair could rise toward the 1.0420 resistance. The main hurdle could be 1.0450.

On the downside, immediate support sits near the 1.0265 level. The next key support sits near the 1.0245 level. Any more losses could send the pair toward the 1.0200 level.

Looking at GBP/USD, the pair started a short-term recovery wave, but the bears are active near the 1.2280 resistance zone.

Upcoming Economic Events:

- Euro Zone Construction Output for Nov 2024 (YoY) – Forecast +1.1%, versus +1.0% previous.

Dollar Index (DXY) Elliott Wave Calling The path

In this technical article we’re going to take a quick look at the Elliott Wave charts of Dollar Index (DXY) published in members area of the website. As our members are aware, the DXY is currently showing impulsive bullish sequences in the cycle from the September low. As a result, we are leaning towards the long side at this stage.

Recently, the Dollar Index has completed a 3-wave pullback, with buyers stepping in precisely at the equal legs zone. In this article, we will dive deeper into the Elliott Wave forecast and explain the reasoning behind our outlook.

DXY H1 London Update 01.15.2025

The current view suggests that the Dollar is forming a ((iv)) black pullback as Elliott Wave Zig-Zag Pattern. The structure of the correction remains incomplete, indicating more short-term weakness. We expect to see another leg down towards the equal legs zone between 108.900 and 108.373 (the potential buyers’ zone).

Once the extreme zone is reached, we anticipate that potential buyers will step in, which could lead to a further rally towards new highs, or at least a three-wave bounce.

DXY H1 London Update 01.17.2025

DXY H1 London Update 01.17.2025

The US Dollar extended lower towards the buying area as expected. Price reached the extreme zone at 108.900 – 108.373. DXY found buyers and rallied from the Equal Legs zone, completing the pullback at 108.62.

The 108.62 low is key for the view. While above this level, we expect further strength towards new highs. A break below it would prolong the correction.

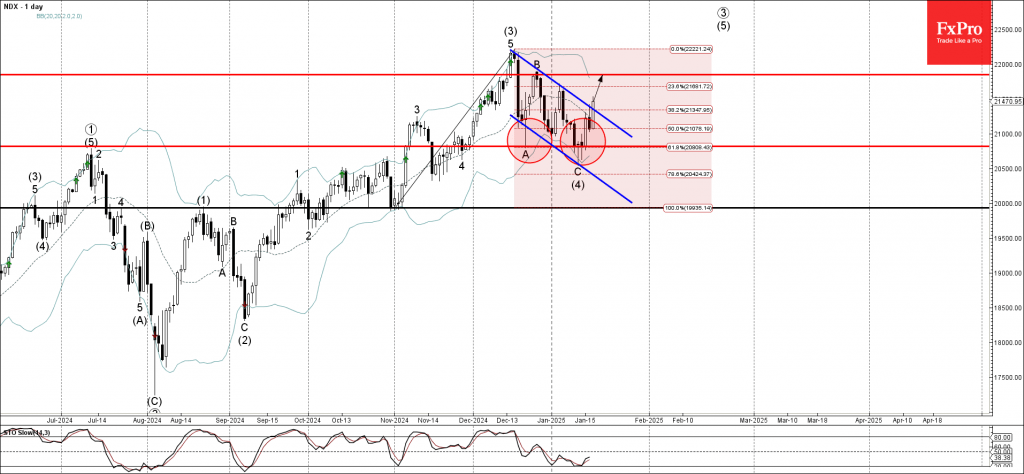

Nasdaq-100 Wave Analysis

- Nasdaq-100 broke daily down channel

- Likely to rise to resistance level 21850.00

Nasdaq-100 index rising inside the intermediate impulse wave (5), which started earlier from the support zone located between the key support level 20820.00 (former low of wave A from December) and the support trendline of the daily down channel from December (which encloses earlier ABC wave (4)).

The index just broke the aforementioned down channel which should accelerate the active impulse wave (5).

Given the strong daily uptrend, Nasdaq-100 index can be expected to rise to the next resistance level 21850.00, top of the previous B-wave.

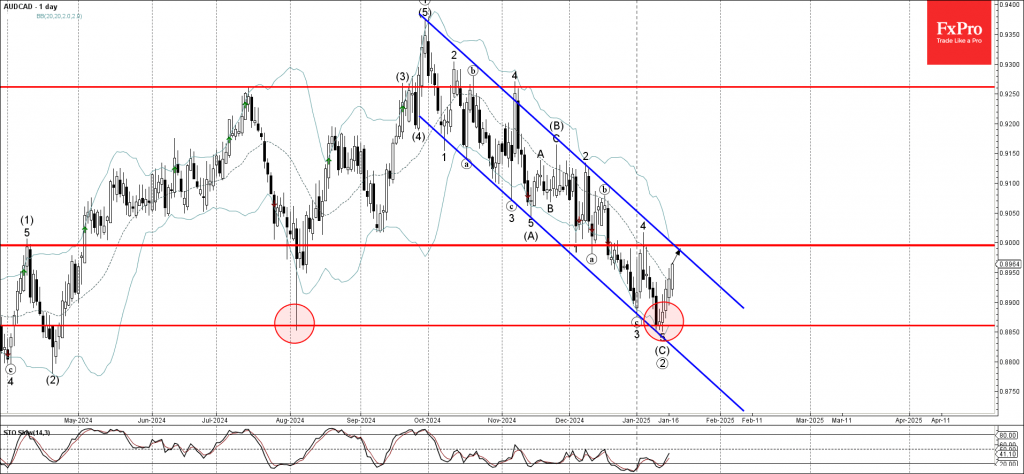

AUDCAD Wave Analysis

- AUDCAD reversed from support zone

- Likely to rise to resistance level 0.9000

AUDCAD currency pair continues to rise inside the minor impulse wave 1, which started earlier from the support zone located between the key support level 0.8860 (former multi month low from April) and the lower daily Bollinger Band.

The active impulse wave 1 belongs to the higher order impulse waves (1) and 1, which started from the same support area.

AUDCAD currency pair can be expected to rise to the next resistance level 0.9000, former strong support from December coinciding with the daily down channel from September.