Sample Category Title

Sunset Market Commentary

Markets

Markets today ‘enjoyed’ some final calm before the expected storm. US markets are closed for Martin Luther King Day, given investors an additional day to reassess their strategy before Donald Trump later takes office as president of the US. Already at its first working day, he is expected to kickstart a policy U-turn with a barrage of sweeping executive orders on everything ranging from migration and boarder control, over US energy production and broad deregulation. Trump also was expected to announce multiple layers of trade tariffs. However, the Wall Street Journal today reported that Trump in a first step is planning to issue a broad Memorandum that directs federal agencies to study US trade policies and evaluate trade relationships with its neighbors and China. However, the action is said to stop short of already imposing new tariffs. This at least supported risk sentiment on European markets intraday. Already for quite some time, the expected US measures were some kind of a black box as investors were obliged to guess the potential impact on growth and inflation inside and outside the US. A high degree of unpredictability will probably remain the watermark of Trump policy, but of over the next 24 hours investors will get a first insight on the degree of disruptiveness of the new policy for actors inside and outside the US. Up until new, the ‘preamble Trump trade’ mostly consisted of higher US yields, a stronger dollar and US equities outperforming most of their ‘friends’/‘allies’. Even as quite some ‘Trumpism’ should already be discounted it would be a surprise for the first flood of voluntary Trump measures to already profoundly reverse the trends of higher (US) yields and a stronger dollar. Looking at the strong performance of European equity markets today and over the previous week, investors apparently consider(ed) a WSJ like scenario were tariffs on trade with Europe won’t be overly disruptive and/or that already quite some negative news is discounted from now.

Returning to day-to-day price action in Europe, the EuroStoxx 50 index (+0.6%) is trading at the highest level since September 2000! After having jumped to level north of $82 p/b last week, Brent oil today drops back below $80. As one of its first measures, US president Trump is rumoured to possibly declare an Energy Emergency in order to facilitate the production and export of US fossil energy and to take measures to decrease domestic US energy costs. EMU interest rate markets show yield changes of 1-2 bps max across the curve. Dollar moves initially also were limited but the US currency fell off a cliff after the WSJ headlines. DXY dropped about 1.0% to trade near 108.25. EUR/USD jumped from the 1.0315 area to 1.042.

News & Views

Slovakia kicked of this year’s debt issuance with a regular auction. Four bonds were on offer, raising a combined €812mn instead of the targeted €600mn with total demand almost reaching €2bn. The country has an estimated gross issuance need of €12bn this year. Debt agency Ardal intends to raise half of that amount via syndicated deals and half via auctions like today. Three new bonds will be launched in one of those processes: a 4-yr, a 12-yr and a 15-yr(+) one. Today’s auction was overshadowed by political developments over the weekend. Smer party member and deputy speaker Gasper suggested that Slovakia could in the future consider leaving the EU and NATO though that would be an extreme solution. Slovak PM Fico indirectly backed his opinion by saying that the country should prepare for any possible EU-crisis. PM Fico holds together a very fragile and narrow coalition government with snap elections before the autumn of 2027 not ruled out.

Several members of the Polish central bank hit the wires today, softening last week’s hawkish (solo?) by NBP President Glapinski. The chairman suggested unaltered policy rates over 2025. While today’s comments of NBP Tyrowicz, Wnorowski and Kotecki all suggest that it will be premature in March, despite updated growth and inflation forecasts, to put a policy rate cut on the table, they all leave more maneuvering room for the rest of the year. Energy regulations will obviously be key – without subsidy extension they’ll push inflation higher again in Q4 2025 - with NBP Kotecki also referring to the presidential ballot mid-May and early-June. Leading candidate of the ruling party of PM Tusk has criticized the hawkish Glapinski (confidant of previous PiS-government) turn as being politically motivated. The Polish presidency is more than a ceremonial function with current PiS-president Duda hampering the political decision making process. The Polish zloty holds strong, continuing the test of EUR/PLN 4.25 support.

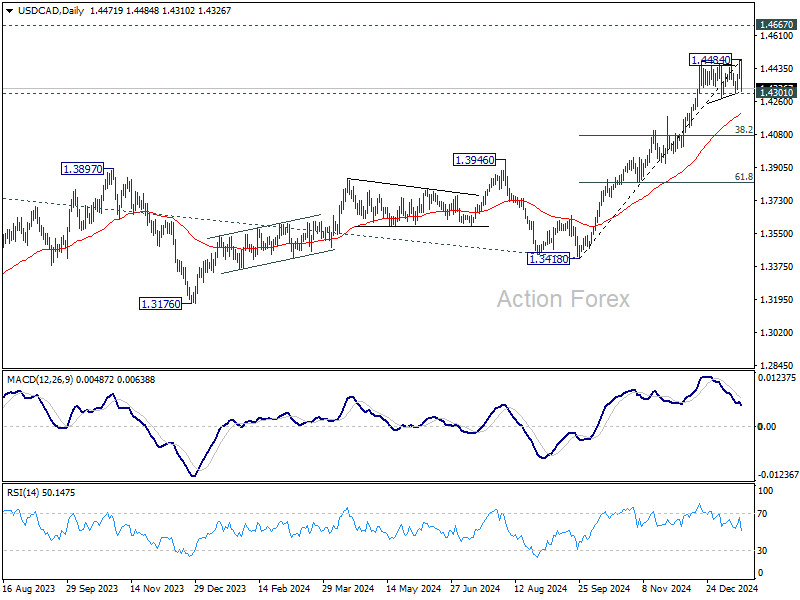

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4406; (P) 1.4446; (R1) 1.4520; More...

USD/CAD's steep decline today and break of 1.4301 support indicates short term topping at 1.4484, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside. Fall from 1.4484 is seen as a correction to rally from 1.3418, and should target 55 D EMA (now at 1.4193) or even further to 38.2% retracement of 1.3418 to 1.4484 at 1.4077. For now, near term risk will stay on the downside as long as 1.4484 holds, in case of recovery.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

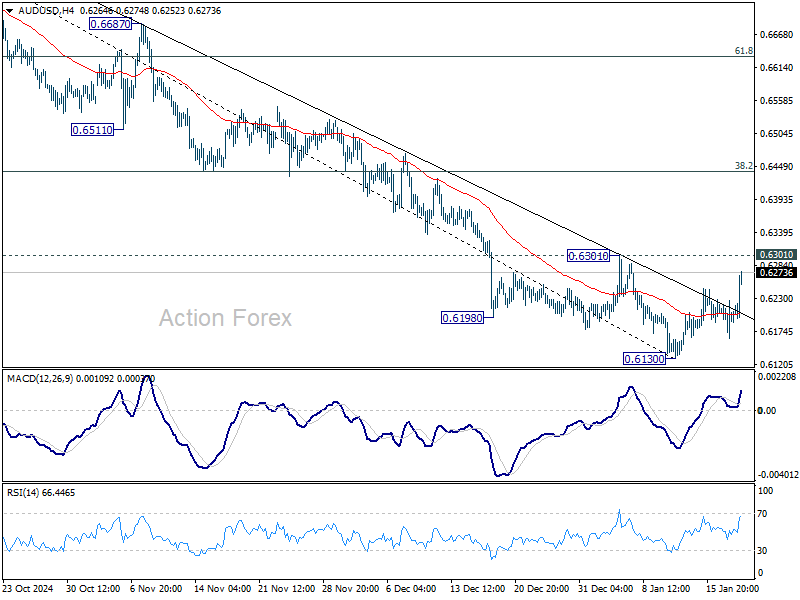

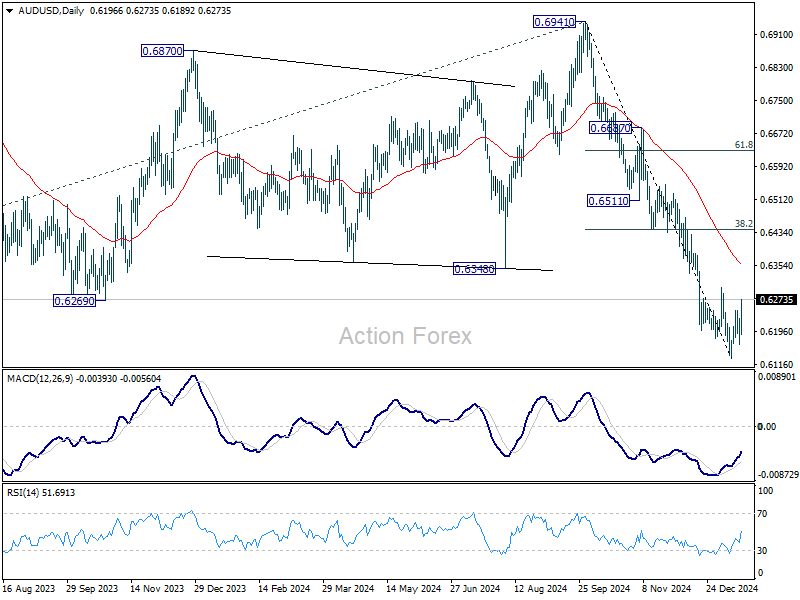

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6163; (P) 0.6195; (R1) 0.6226; More...

AUD/USD's rebound from 0.6130 extends higher today, but upside is still limited below 0.6301 resistance. Intraday bias remains neutral for the moment, and more consolidations could be seen. Outlook will remain bearish as long as 0.6301 resistance holds. Break of 0.6130 will resume the fall from 0.6941. However, considering bullish convergence condition in 4H MACD, break of 0.6310 will indicate short term bottoming, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 0.6360).

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

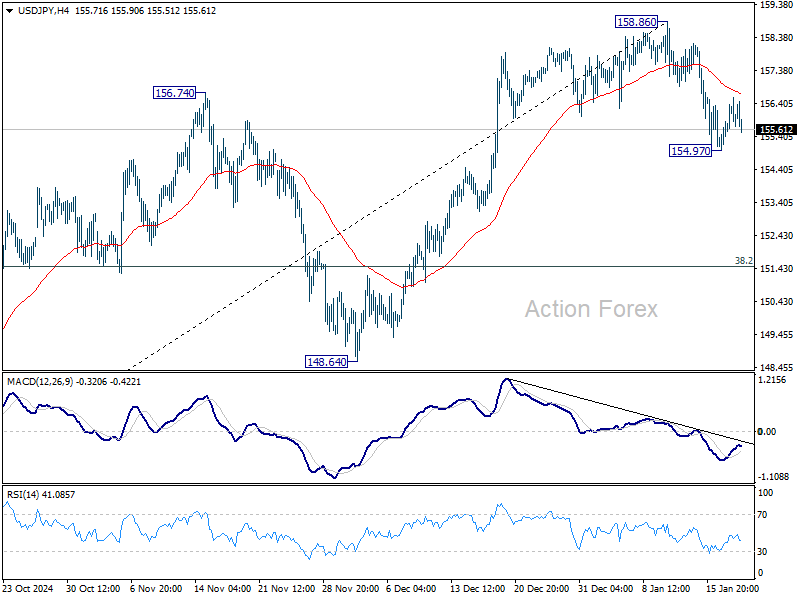

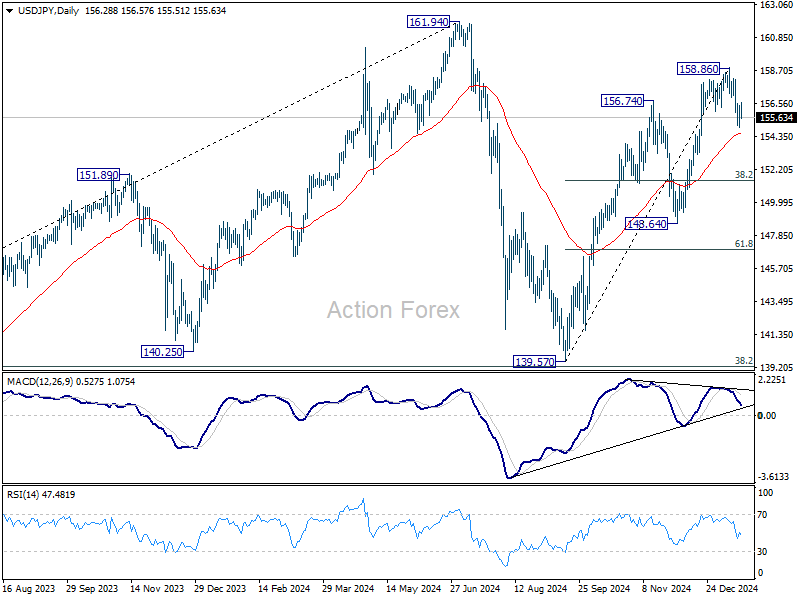

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.39; (P) 155.88; (R1) 156.79; More...

Outlook in USD/JPY is unchanged and intraday bias remains neutral. Risk will stay on the downside as long as 158.86 short term top holds. On the downside, below 154.97 will target 55 D EMA (now at 154.59). Sustained break there will target 38.2% retracement of 139.57 to 158.86 at 151.49 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

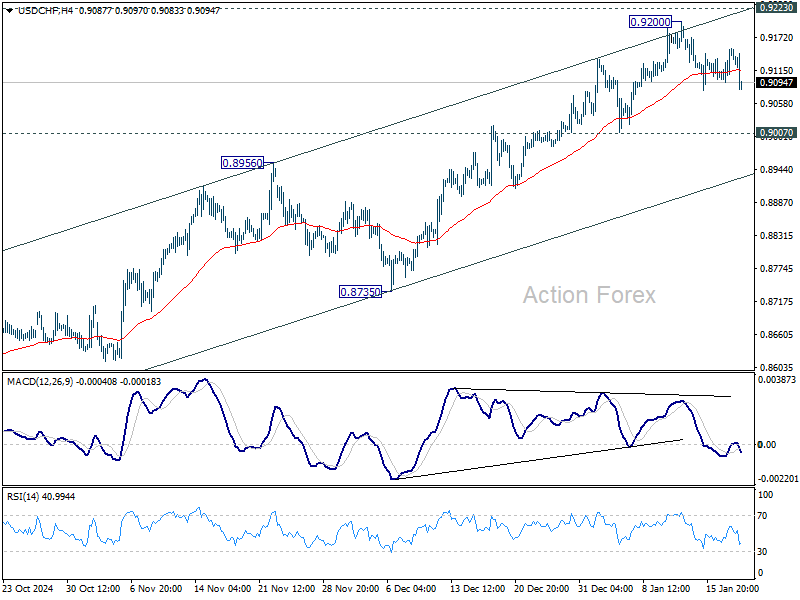

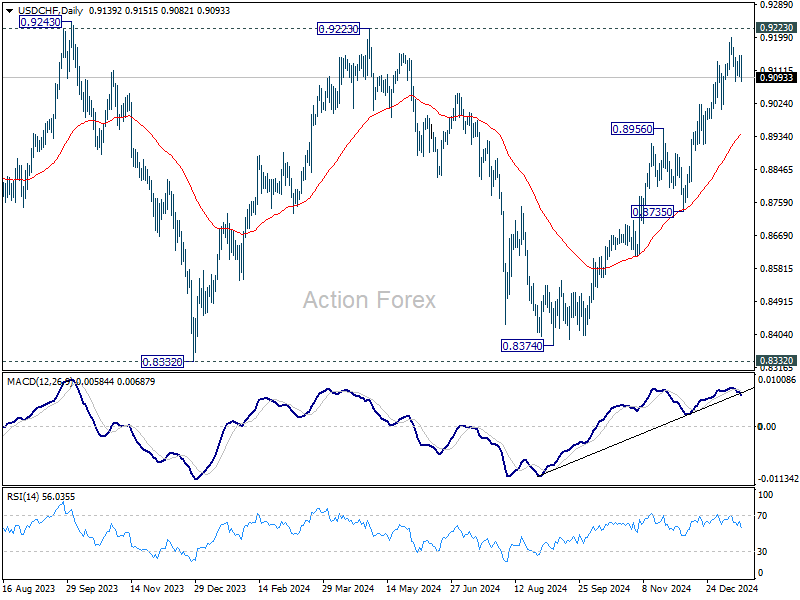

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9111; (P) 0.9133; (R1) 0.9171; More…

USD/CHF dips notably today but outlook is unchanged. Intraday bias stays neutral, and more consolidations could be seen. Outlook will stay bullish as long as 0.9007 support holds. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 0.8944).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

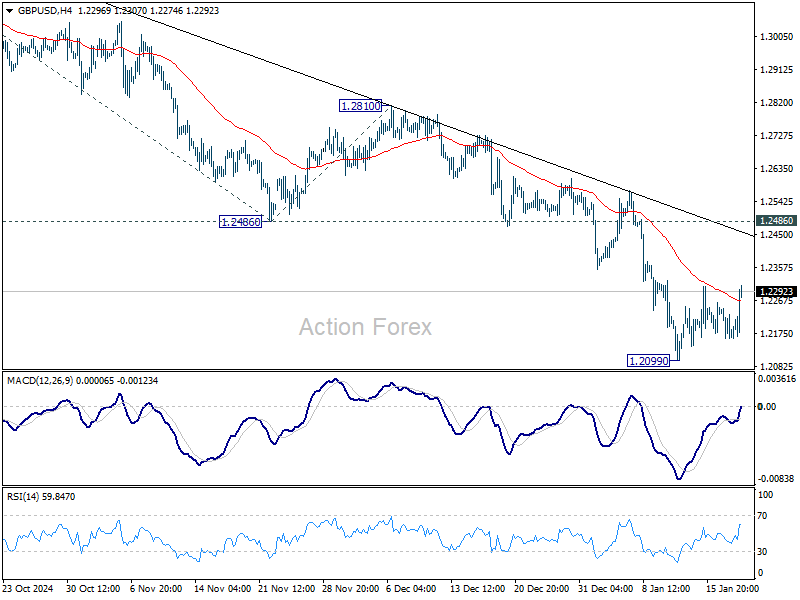

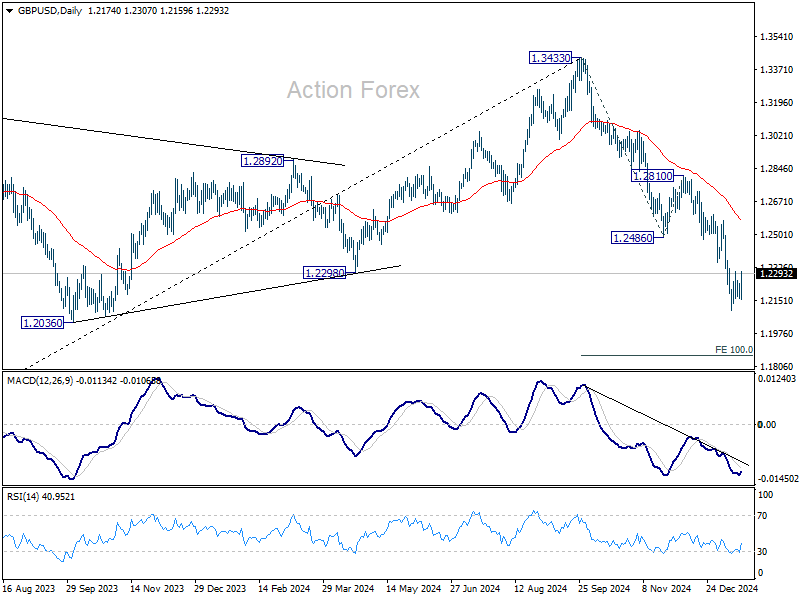

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2137; (P) 1.2193; (R1) 1.2226; More...

GBP/USD recovered today but stays well below 1.2486 support turned resistance. Intraday bias remains neutral and outlook is unchanged. More consolidations would be seen and stronger recovery cannot be ruled out. But outlook will remain bearish as long as 1.2486 support turned resistance holds. On the downside, break of 1.2099 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

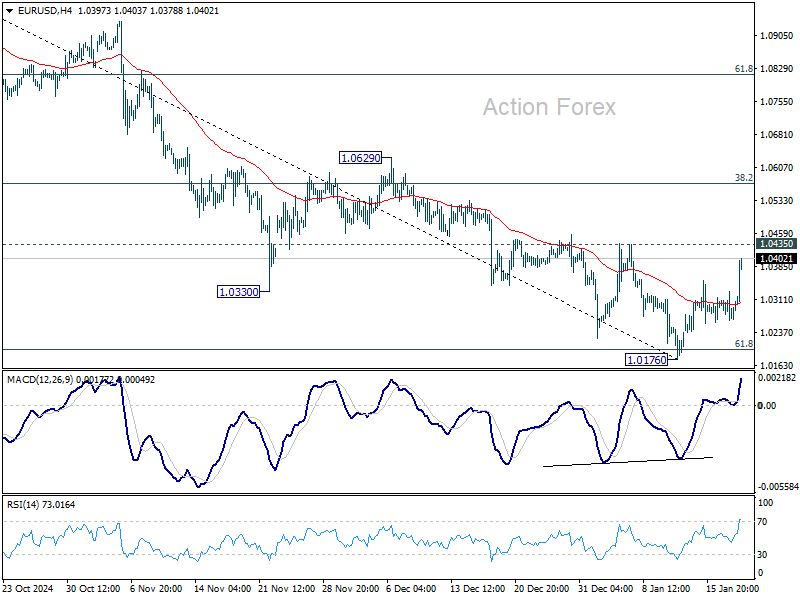

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0247; (P) 1.0289; (R1) 1.0313; More...

EUR/USD is still capped below 1.0435 resistance despite extending rebound from 1.0176. Intraday bias remains neutral and outlook stay bearish. Firm break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound to 38.2% retracement of 1.1213 to 1.0176 at 1.0572 first.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

Dollar Weakened by Reports Trump Is Holding Off on New Tariffs

Dollar weakened broadly in early US session as reports from The Wall Street Journal indicated that Donald Trump, during his inauguration, will only outline his trade vision but avoid imposing new tariffs for now. While this temporarily calms market fears of immediate disruptions, the situation remains dynamic, and unexpected developments could trigger sharp reversals, especially if the WSJ report proves inaccurate.

According to the report, Trump plans to issue a memorandum directing federal agencies to study trade policies and assess trade relationships with key partners, including China, Canada, and Mexico. The memorandum is expected to focus on addressing persistent trade deficits and investigating unfair trade and currency practices.

Specific directives include examining China’s compliance with the 2020 trade deal and reviewing the US-Mexico-Canada Agreement, which is up for re-evaluation in 2026. These steps suggest Trump is prioritizing groundwork over immediate action, but the spotlight remains on the possibility of future tariffs.

Technically, immediate focus is now on 1.4301 support in USD/CAD's with today's sharp reversal. Firm break there would at least bring deeper pull back to 55 D EMA (now at 1.4194). There is prospect of even deeper fall to 38.2% retracement of 1.3418 to 1.4484 at 1.4077 should CPI and retail sales data from Canadian Dollar later in the week are Loonie supportive. Or, at least, Canadian Dollar could have a breather until Trump's tariffs are really imposed.

In Europe, at the time of writing, FTSE is extending its record run and rises 0.12%. DAX is down -0.03% while CAC is up 0.02%. UK 10-year yield is up 0.041 at 4.701. Germany 10-year yield is up 0.016 at 2.548. Earlier in Asia, Nikkei rose 1.17%. Hong Kong HSI rose 1.75%. China Shanghai SSE rose 0.08%. Singapore Strait TImes fell -0.07%. Japan 10-year JGB yield fell -0.010 to 1.197.

ECB's Holzmann: January rate cut not as certain with elevated inflation risks

Austrian ECB Governing Council member Robert Holzmann expressed skepticism over a potential rate cut at ECB's upcoming January meeting. In an interview with Politico, Holzmann stated, “A cut is not a foregone conclusion for me at all,” emphasizing his commitment to approaching the discussion with an "open mind."

Holzmann highlighted that ECB decisions are fundamentally data-driven and noted that inflation remained “well above” 2% in December, with January figures expected to reflect similar levels. He cautioned that "cutting interest rates when inflation rises faster than anticipated, even temporarily, risks hurting credibility."

As a known policy hawk, Holzmann also revealed increased doubts about inflation settling around ECB’s 2% target by the end of the year. He cited unexpected developments since the December decision, including faster-than-expected depletion of gas reserves due to colder weather, the effective closure of the Ukraine gas transit, and the risks of persistently high energy prices.

China maintains LPR as offshore Yuan recovers ahead of key support

China’s central bank maintained its benchmark lending rates unchanged on Monday. The one-year loan prime rate was steady at 3.1%, while the over-five-year LPR, which influences mortgage rates, remained at 3.6%.

The offshore Yuan strengthened notably against the Dollar, continuing to draw support from a a key long-term level. This comes despite market speculation that China might allow Yuan to weaken further to counteract the economic effects of new tariffs introduced under Donald Trump’s presidency.

A weaker currency would bolster export competitiveness by making Chinese goods more affordable internationally. However, Beijing faces a dilemma: while a controlled depreciation could help exporters, an uncontrolled fall could lead to heightened volatility in domestic financial markets and reduced investor confidence.

Acknowledging these risks, PBOC Governor Pan Gongsheng reaffirmed the central bank’s commitment to exchange rate stability last week, stating, “We will resolutely prevent the risk of the exchange rate overshooting, ensuring that the Yuan exchange rate remains generally stable at a reasonable, balanced level.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0247; (P) 1.0289; (R1) 1.0313; More...

EUR/USD is still capped below 1.0435 resistance despite extending rebound from 1.0176. Intraday bias remains neutral and outlook stay bearish. Firm break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound to 38.2% retracement of 1.1213 to 1.0176 at 1.0572 first.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

Gold (XAU/USD) Price Steady On Inauguration Day, Calm Before the Storm?

- Gold prices found stability above $2700/oz after an initial drop.

- Historically, gold prices saw an initial two-day rally followed by a decline after Trump’s 2017 inauguration, driven by safe-haven demand and uncertainty.

- Technically, gold appears to be in a “wait and see” mode, with a bounce off the 2700 handle suggesting potential upside.

- Markets will be keeping an eye on the proposed tariffs and policy changes under the new.

Gold prices dropped following the market open yesterday but has since found some stability above the $2700/oz handle. Markets had expected a bout of volatility which I still believe will begin tomorrow and potentially later in the day.

The US holiday however, does mean that low levels of liquidity will be present during the US session and could mean any significant moves may materialize from tomorrow onward.

Golds Reaction to Trump 2.0

Historic data is always worth paying attention to even though at times they do not always pan out. Based on Trump’s first term, how did the price of gold fare after the inauguration?

Well, in 2017, January 20 when Trump was inaugurated Gold prices rose for an initial two-day rally before falling over 2.75% over the next three-days. At the time a lot of the rise in Gold was possibly down to safe haven demand as uncertainties about a Trump Presidency were rife.

This time around however, Trump does enjoy the support of the majority of Republicans which should allay fears within the US. However, Global Markets will be on edge in the coming days as they wait to see what plans Trump looks to implement when it comes to tariffs, border control and cryptocurrency.

This could lead to some wild price swings in the day ahead and thus warrants keeping a close eye on.

The return of Trump and proposed tariff hikes has lent strength to the US Dollar over the past 2 months. However, this is a double edged sword as high tariffs is likely to lead to a drop in gold prices at least temporarily while the uncertainty could keep haven demand active.

Is Gold about to enter a new phase of ‘consolidation’? We will soon find out.

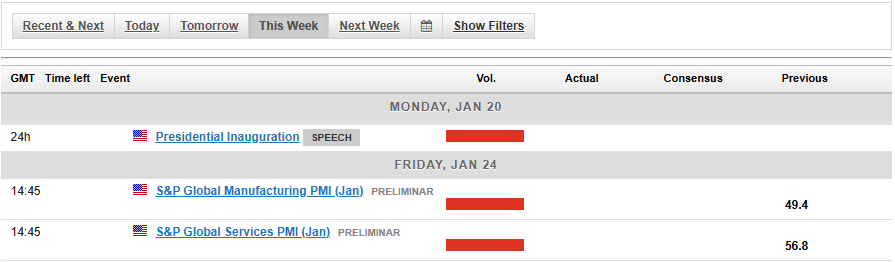

The Week Ahead

The inauguration and first few days in office for President Trump do promise a lot and thus could overshadow data releases this week. The US does not have a lot of data scheduled for the week ahead with the S&P manufacturing and services PMI data due out on Friday.

In the interim i would suggest paying close attention to tariff chatter and the like as this could have material implications across a variety of markets and instruments.

Technical Analysis Gold (XAU/USD)

Gold appears to be in a wait and see mode at present.

Looking at the daily timeframe below and a bounce off the 2700 handle does bode well for bullish continuation.

That coupled with the overall trend leaves me to believe that we could be in for more upside in the days ahead.

Gold (XAU/USD) Daily Chart, January 29, 2025

Source: TradingView (click to enlarge)

Dropping down to a H1 chart and as you can see below, price is currently in no man’s land.

The H1 however, does appear to have changed structure and now also hints at further potential upside.

However a H1 candle close above the 2716 handle could help facilitate further upside and maybe even retest of the 2024 highs.

Gold (XAU/USD) One-Hour H1 Chart, January 20, 2025

Source: TradingView (click to enlarge)

Support

- 2700

- 2690

- 2673

Resistance

- 2716

- 2724

- 2739

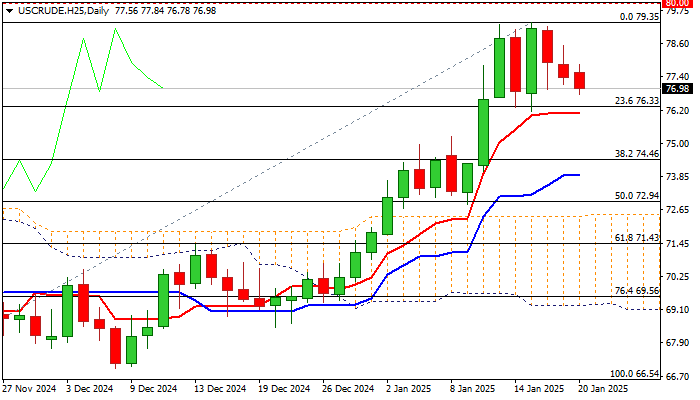

WTI Oil Price Eases from New Highs as Market Awaits Fresh Signals

WTI oil price eased further in early Monday trading, after last week’s multiple upside rejections at the base of daily Ichimoku cloud ($79.00) left a weekly bull-trap, prompting traders for a partial profit-taking.

All eyes are on inauguration of the US President Donald Trump and a number an executive orders he promised to sign in his first 24 hours in the White House.

Markets also speculate that Trump may relax some of energy related sanctions against Russia, in attempts to start moving the war in Ukraine towards the end.

Larger bulls faced headwinds from barriers at $80 zone (50% retracement of $95.00/$65.26 / 200WMA) as well as a ceasefire Gaza, which capped the latest rally.

Overall technical picture remains bullish, and is boosted by better than expected recent economic data from China, world’s top oil importer, which brightened demand outlook in coming months.

The recent formation of 10/200DMA golden cross was supportive, however fading bullish momentum suggests that there will be more room for deeper correction before broader bulls regain traction.

Initial supports lay at $76.33/10 (Fibo 23.6% of $66.54/$79.35 / daily Tenkan-sen), followed by 200DMA ($74.90) and Fibo 38.2% ($74.46) where deeper dips should find firm ground and mark a healthy correction.

At the upside, the latest top ($79.35) and $80 zone mark pivotal barriers, violation of which to expose targets at $83.64 (Fibo 61.8% of $95.00/$65.26) and $84.50 (June 30 lower top).

Res: 78.53; 79.00; 79.35; 80.00.

Sup: 76.33; 76.10; 74.90; 74.46.