Sample Category Title

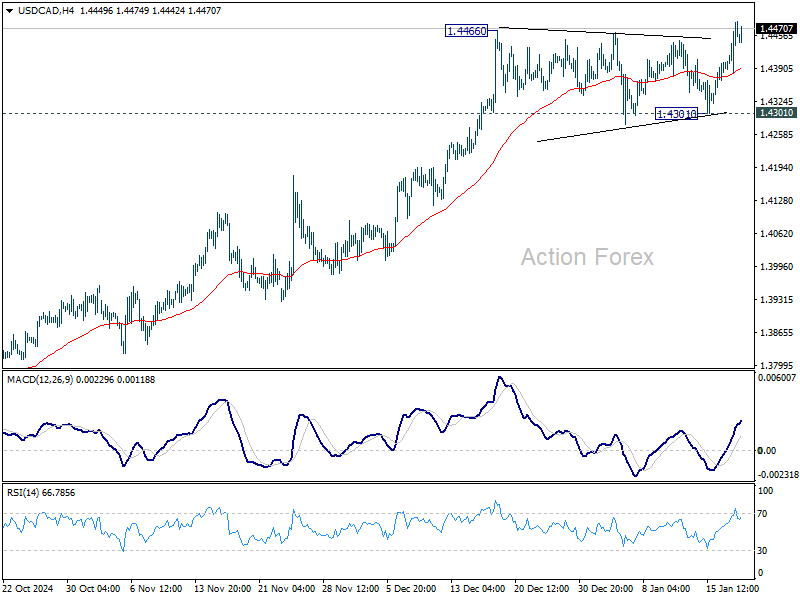

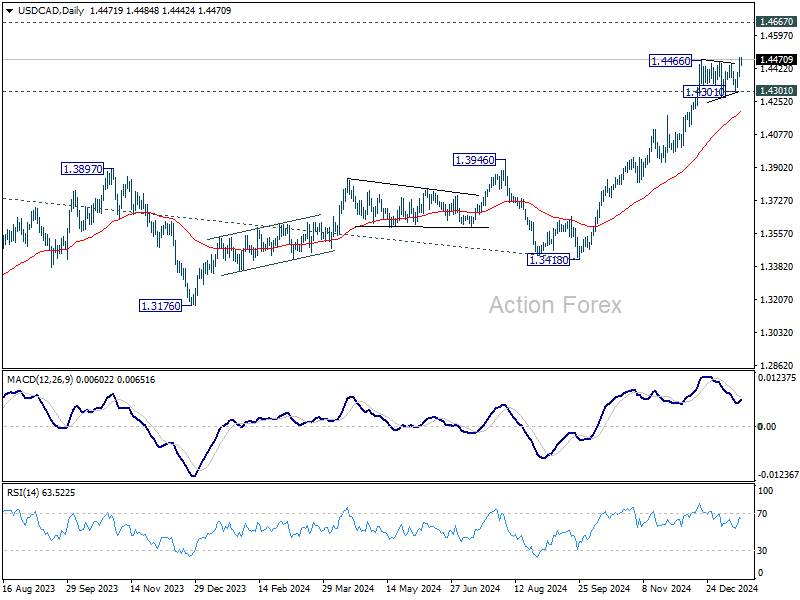

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4406; (P) 1.4446; (R1) 1.4520; More...

Intraday bias in USD/CAD remains on the upside for the moment. Current up trend should target 1.4667/89 long term resistance zone. For now, outlook will stay bullish as long as 1.4302 support holds, in case of retreat.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

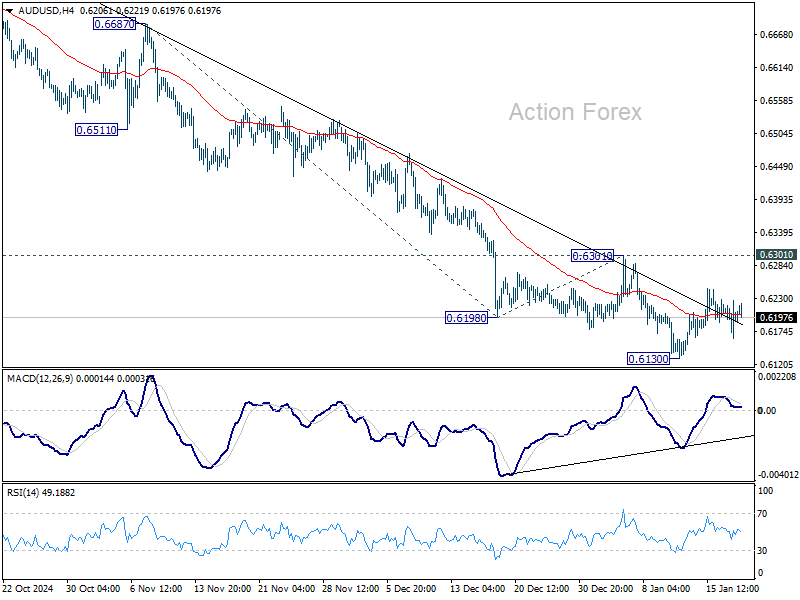

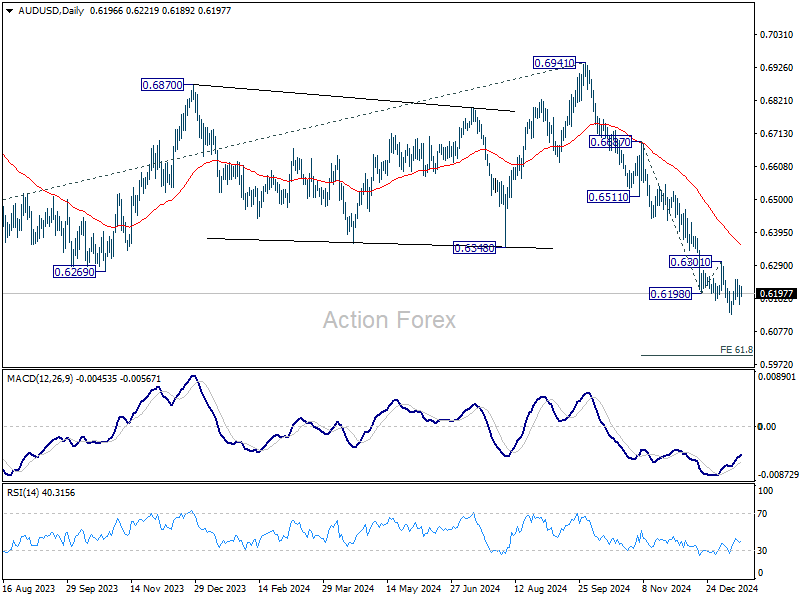

AUD/USD Daily Report

Daily Pivots: (S1) 0.6163; (P) 0.6195; (R1) 0.6226; More...

Intraday bias in AUD/USD remains neutral as consolidations continue above 0.6130 support. Outlook will remain bearish as long as 0.6301 resistance holds. Break of 0.6130 will resume the fall from 0.6941 and target 61.8% projection of 0.6687 to 0.6198 from 0.6301 at 0.5999. However, considering bullish convergence condition in 4H MACD, break of 0.6310 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

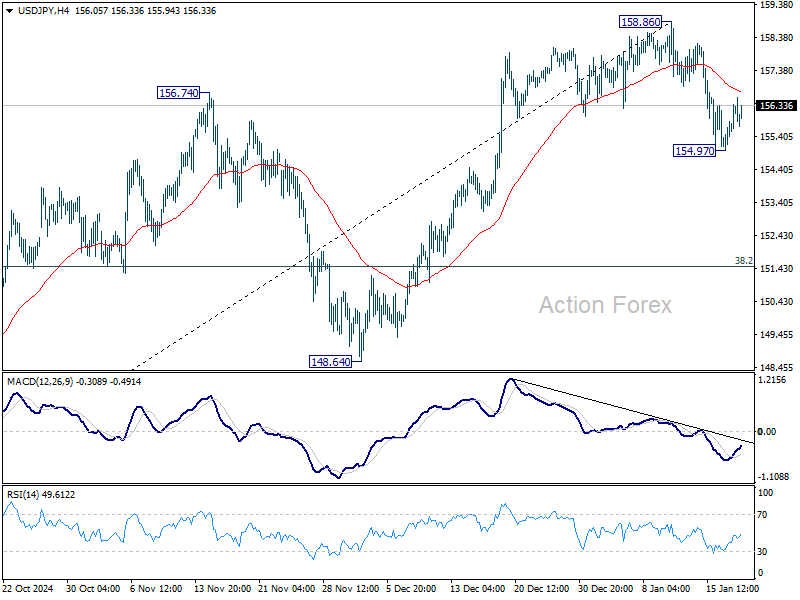

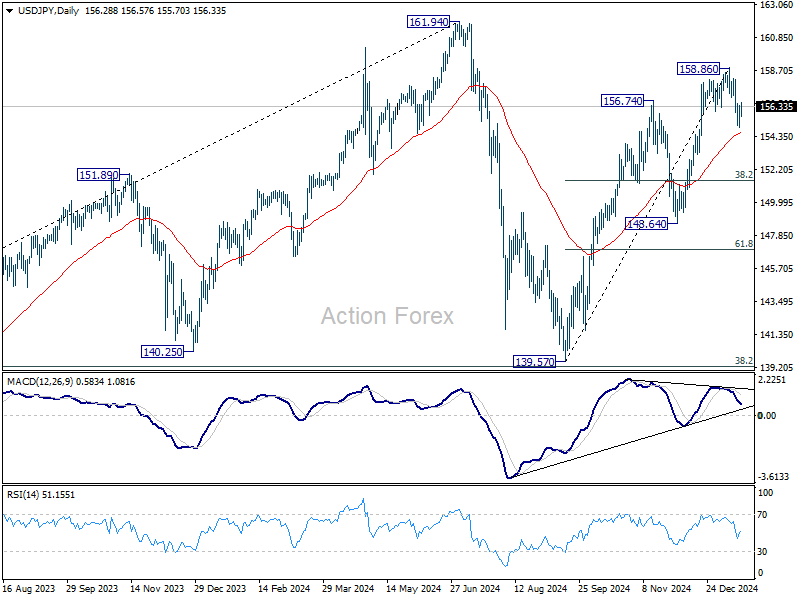

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.39; (P) 155.88; (R1) 156.79; More...

Intraday bias in USD/JPY remains neutral, and risk will stay on the downside as long as 158.86 short term top holds. On the downside, below 154.97 will target 55 D EMA (now at 154.59). Sustained break there will target 38.2% retracement of 139.57 to 158.86 at 151.49 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

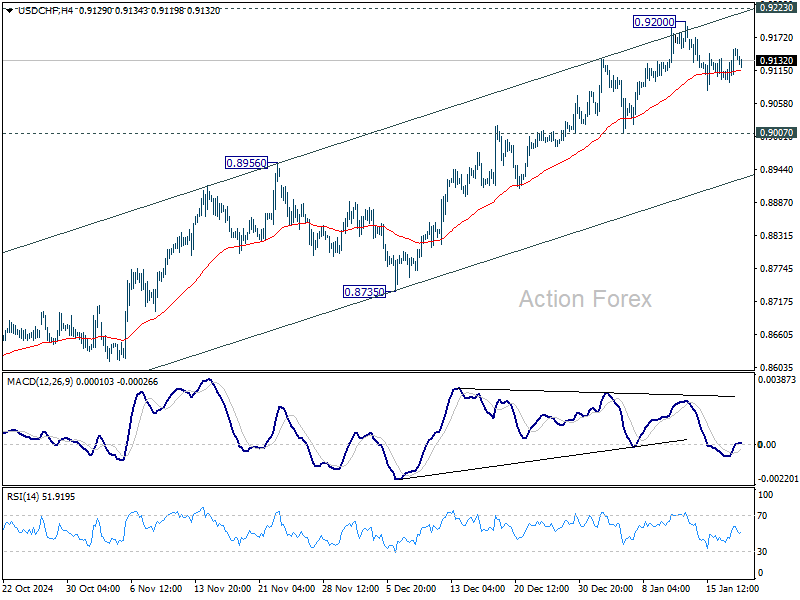

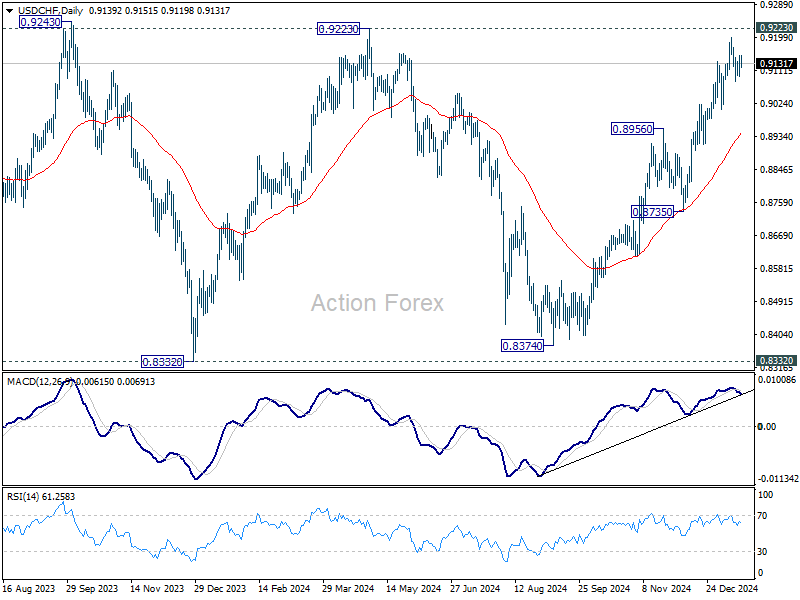

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9111; (P) 0.9133; (R1) 0.9171; More…

Range trading continues in USD/CHF below 0.9200 and intraday bias remains neutral. More consolidations could be seen but outlook will stay bullish as long as 0.9007 support holds. On the upside, decisive break of 0.9223 will carry larger bullish implications. However, break of 0.9007 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 0.8944).

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

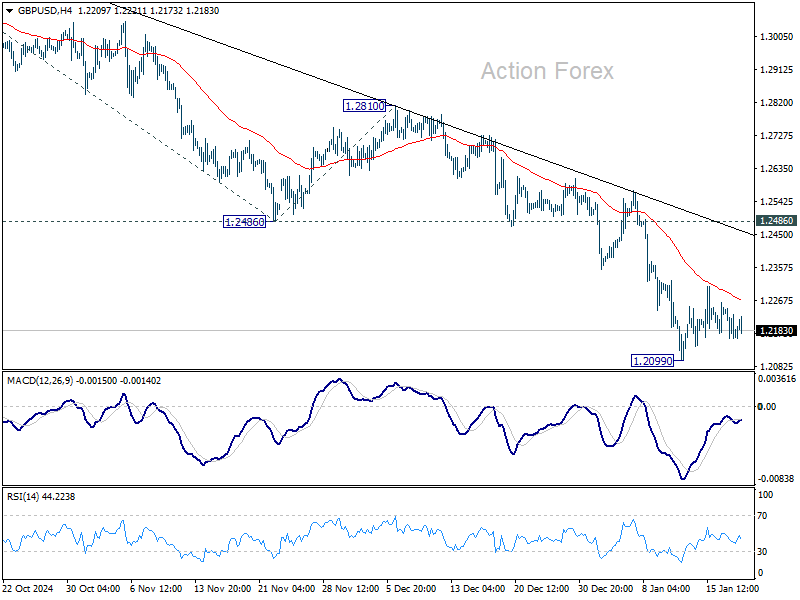

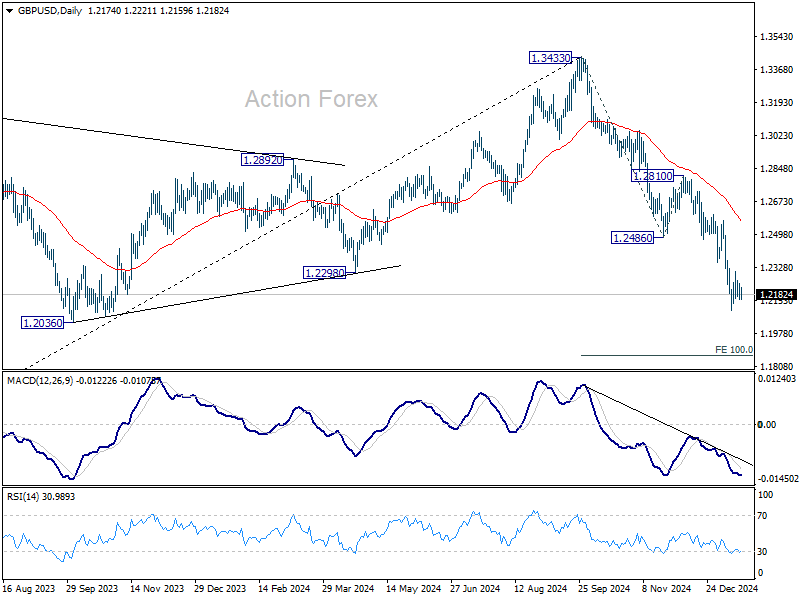

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2137; (P) 1.2193; (R1) 1.2226; More...

Intraday bias in GBP/USD remains neutral as range trading continues above 1.2099. More consolidations would be seen and stronger recovery cannot be ruled out. But outlook will remain bearish as long as 1.2486 support turned resistance holds. On the downside, break of 1.2099 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.

XAU/USD Analysis: Gold Prices Poised for a New Trend

Although today is a public holiday in the US (Martin Luther King Jr. Day), financial markets are unlikely to remain calm, as traders and investors will be closely watching the inaugural speech of Donald Trump, the 47th President-elect, scheduled for 20:00 GMT+3.

Trump's speech could impact gold prices in USD, particularly if it addresses:

→ Monetary policy: With current Federal Reserve rates trending lower, non-yielding assets like gold may become more attractive.

→ International trade: If Trump’s remarks on tariffs are particularly bold, gold’s status as a “safe haven” asset could boost its appeal.

→ The dollar's value: Policies aimed at strengthening the USD and reducing national debt may influence gold prices inversely.

Technical analysis of the XAU/USD chart shows that gold prices are trading within a narrowing triangle:

→ The lower boundary is supported by the ascending channel that began in March 2024.

→ Resistance sits at $2,720 per ounce. Although this level served as support in October, bulls have struggled to break it since December (as indicated by the arrow).

While bullish sentiment dominates the gold market (evident from the orange trend lines relevant for January), Trump’s speech could trigger volatility spikes. These fluctuations may shift the current sentiment balance and spark the formation of a new trend for XAU/USD.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

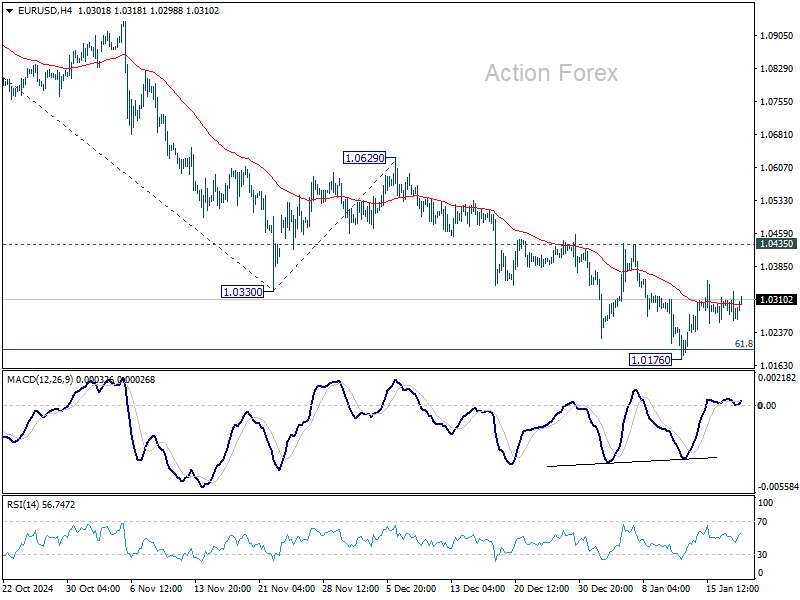

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0247; (P) 1.0289; (R1) 1.0313; More...

EUR/USD recovers mildly today but stays in the middle of near term range above 1.0176. Intraday bias stays neutral and outlook remains bearish with 1.0435 resistance intact. On the downside, break of 1.0176 will resume the fall from 1.1213 and target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. However, firm break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

Greenback Eases Ahead of Trump’s Executive Actions, Bitcoin Takes Leads and Hits New Record

Dollar is trading slightly lower today as markets await Donald Trump’s inauguration as the 47th US President. Attention is focused on his inaugural speech, expected to confirm his policy priorities. However, the real market-moving event is likely to be the series of executive actions Trump has promised to enact immediately.

Over 200 directives are anticipated, including legally binding executive orders and proclamations, with particular interest in measures affecting tariffs and deregulations in sectors like energy and cryptocurrencies.

One key area of focus is Trump’s potential tariff policies, which would surely reshape US trade relationships with allies and adversaries and impact global market. Deregulation efforts, spanning traditional energy sectors to the fast-growing cryptocurrency industry, are also expected to influence investor sentiment.

Meanwhile, Bitcoin has reached a new all-time high, reflecting the renewed bullish sentiment in cryptocurrencies. Technically, next near term target is 61.8% projection of 49008 to 108368 from 89127 at 125812. Outlook will stay bullish as long as 89127 support holds, even in case of pull back.

While Trump’s inauguration and executive actions are dominating headlines, global markets are also preparing for several other key events. BoJ is widely expected to raise its policy rate. UK employment data will provide insight into the labor market's response to the Autumn Budget. Inflation data from Canada and New Zealand will help shape monetary policy projections of BoC and RBNZ. PMI data from major economies will round out the week’s events.

ECB's Holzmann: January rate cut not as certain with elevated inflation risks

Austrian ECB Governing Council member Robert Holzmann expressed skepticism over a potential rate cut at ECB's upcoming January meeting. In an interview with Politico, Holzmann stated, “A cut is not a foregone conclusion for me at all,” emphasizing his commitment to approaching the discussion with an "open mind."

Holzmann highlighted that ECB decisions are fundamentally data-driven and noted that inflation remained “well above” 2% in December, with January figures expected to reflect similar levels. He cautioned that "cutting interest rates when inflation rises faster than anticipated, even temporarily, risks hurting credibility."

As a known policy hawk, Holzmann also revealed increased doubts about inflation settling around ECB’s 2% target by the end of the year. He cited unexpected developments since the December decision, including faster-than-expected depletion of gas reserves due to colder weather, the effective closure of the Ukraine gas transit, and the risks of persistently high energy prices.

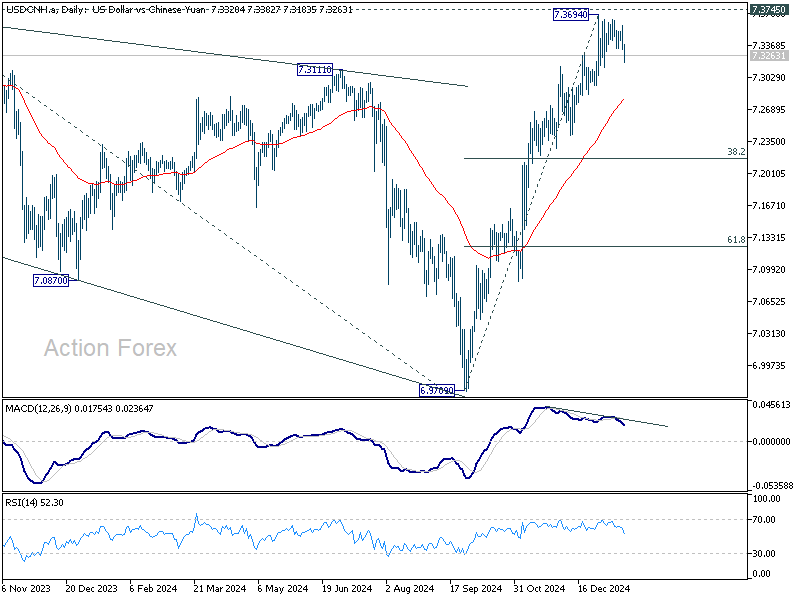

China maintains LPR as offshore Yuan recovers ahead of key support

China’s central bank maintained its benchmark lending rates unchanged on Monday. The one-year loan prime rate was steady at 3.1%, while the over-five-year LPR, which influences mortgage rates, remained at 3.6%.

The offshore Yuan strengthened notably against the Dollar, continuing to draw support from a a key long-term level. This comes despite market speculation that China might allow Yuan to weaken further to counteract the economic effects of new tariffs introduced under Donald Trump’s presidency.

A weaker currency would bolster export competitiveness by making Chinese goods more affordable internationally. However, Beijing faces a dilemma: while a controlled depreciation could help exporters, an uncontrolled fall could lead to heightened volatility in domestic financial markets and reduced investor confidence.

Acknowledging these risks, PBOC Governor Pan Gongsheng reaffirmed the central bank’s commitment to exchange rate stability last week, stating, “We will resolutely prevent the risk of the exchange rate overshooting, ensuring that the Yuan exchange rate remains generally stable at a reasonable, balanced level.”

Technically, a short term top should be confirmed at 7.3694 in USD/CNH with today's dip. But it's early to call for bearish reversal as long as 55 D EMA (now at 7.2797) hits. Further rally remains in favor through 7.3745 (202 high) to resume the long term up trend.

Nevertheless, firm break of 55 D EMA should bring deeper pull back to 38.2% retracement of 6.9709 to 7.3694 at 7.2172, which is close to 55 W EMA (now at 7.2097) even just as a correction to rise from 6.9709.

From BoJ to inflation data and PMIs, global markets have more to focus on than Trump

While the inauguration of Donald Trump dominates the headlines in US markets, global investors are turning their attention to a week packed with pivotal high-impact economic events that would provide crucial clues about the monetary policy paths of key economies.

BoJ’s upcoming meeting is a top priority for global markets. After repeated signals from Governor Kazuo Ueda and other top officials, markets should be well-prepared for a 25bps rate hike, raising the policy rate to 0.50%. However, beyond the rate decision, the focus will shift to BoJ's updated economic projections and policy guidance.

While Ueda is expected to remain cautious about committing to a specific timeline for normalization, he may strike a more optimistic tone regarding wage growth, based on reports from branch managers. Additionally, BoJ could raise inflation forecasts in its quarterly outlook, both of which would add hawkish tones to the meeting.

In the UK, attention is squarely on employment data, which will shed light on the labor market’s response to the government’s Autumn Budget. The markets are already pricing in over 75 basis points of BoE rate cuts in 2025. Meanwhile, IMF is projecting an even deeper 100bps reduction. The strength of the labor market will play a pivotal role in determining the scale of monetary easing this year, making this release a key driver for Sterling sentiment.

Inflation data from Canada and New Zealand also hold significant importance. In Canada, BoC has indicated that the pace of rate reductions will slow, but uncertainty remains over the timing of pauses. A Reuters poll suggests an 80% chance of a 25bps cut on January 29, following December’s larger 50-bps move. CPI data will either reinforce or challenge this expectation.

Meanwhile, New Zealand’s Q4 inflation report is expected to show further easing in price pressures, consistent with RBNZ’s forecasts. If the trend persists, RBNZ could deliver another 50bs rate cut at its February meeting

Other data to watch this week include Germany’s ZEW Economic Sentiment Index and PMI reports from several major economies. These releases will provide additional context on global economic momentum and inform central bank decisions in the months ahead.

Here are some highlights for the week:

- Monday: Japan machine orders, tertiary industry index; Germany PPI; Swiss PPI; BoC business outlook survey.

- Tuesday: New Zealand BNZ services; UK employment; Germany ZEW economic sentiment; Canada CPI.

- Wednesday: New Zealand CPI; UK public sector net borrowing: Canada IPPI and RMPI.

- Thursday: Japan trade balance; Canada retail sales; US jobless claims.

- Friday: Australia PMIs; Japan CPI, PMIs, BoJ rate decision; Eurozone PMIs; UK PMIs; Canada new housing price index; US PMIs, US existing sales.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0247; (P) 1.0289; (R1) 1.0313; More...

EUR/USD recovers mildly today but stays in the middle of near term range above 1.0176. Intraday bias stays neutral and outlook remains bearish with 1.0435 resistance intact. On the downside, break of 1.0176 will resume the fall from 1.1213 and target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. However, firm break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.

ECB’s Holzmann: January rate cut not as certain with elevated inflation risks

Austrian ECB Governing Council member Robert Holzmann expressed skepticism over a potential rate cut at ECB's upcoming January meeting. In an interview with Politico, Holzmann stated, “A cut is not a foregone conclusion for me at all,” emphasizing his commitment to approaching the discussion with an "open mind."

Holzmann highlighted that ECB decisions are fundamentally data-driven and noted that inflation remained “well above” 2% in December, with January figures expected to reflect similar levels. He cautioned that "cutting interest rates when inflation rises faster than anticipated, even temporarily, risks hurting credibility."

As a known policy hawk, Holzmann also revealed increased doubts about inflation settling around ECB’s 2% target by the end of the year. He cited unexpected developments since the December decision, including faster-than-expected depletion of gas reserves due to colder weather, the effective closure of the Ukraine gas transit, and the risks of persistently high energy prices.

China maintains LPR as offshore Yuan recovers ahead of key support

China’s central bank maintained its benchmark lending rates unchanged on Monday. The one-year loan prime rate was steady at 3.1%, while the over-five-year LPR, which influences mortgage rates, remained at 3.6%.

The offshore Yuan strengthened notably against the Dollar, continuing to draw support from a a key long-term level. This comes despite market speculation that China might allow Yuan to weaken further to counteract the economic effects of new tariffs introduced under Donald Trump’s presidency.

A weaker currency would bolster export competitiveness by making Chinese goods more affordable internationally. However, Beijing faces a dilemma: while a controlled depreciation could help exporters, an uncontrolled fall could lead to heightened volatility in domestic financial markets and reduced investor confidence.

Acknowledging these risks, PBOC Governor Pan Gongsheng reaffirmed the central bank’s commitment to exchange rate stability last week, stating, “We will resolutely prevent the risk of the exchange rate overshooting, ensuring that the Yuan exchange rate remains generally stable at a reasonable, balanced level.”

Technically, a short term top should be confirmed at 7.3694 in USD/CNH with today's dip. But it's early to call for bearish reversal as long as 55 D EMA (now at 7.2797) hits. Further rally remains in favor through 7.3745 (202 high) to resume the long term up trend.

Nevertheless, firm break of 55 D EMA should bring deeper pull back to 38.2% retracement of 6.9709 to 7.3694 at 7.2172, which is close to 55 W EMA (now at 7.2097) even just as a correction to rise from 6.9709.