Sample Category Title

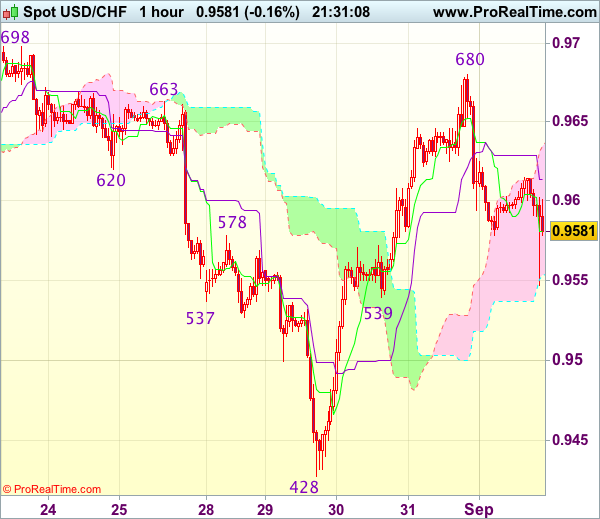

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 0.9610

Original strategy :

Buy at 0.9540, Target: 0.9640, Stop: 0.9505

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback only slipped to as low as 0.9547 in US morning before finding renewed buying interest (missed our long entry at 0.9540), this anticipated rebound signals an intra-day low has been formed there and consolidation with upside bias is seen for gain to 0.9640-50, however, break there is needed to signal the pullback from yesterday’s high of 0.9680 has ended, bring retest of this level, break there would confirm the rise from 0.9428 low has resumed and extend headway to 0.9698-99 resistance first.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent retreat. Below 0.9575-80 would risk another test of 0.9547 and possibly support at 0.9539, however, only break there would shift risk to downside and signal the rise form 0.9428 has ended, then weakness towards 0.9500 would follow.

U.S. Job Growth Slower But Still Strong in August

Highlights:

- Payroll employment rose a smaller-than-expected 156k in August with 41k worth of downward revisions to June and July gains combined.

- The unemployment rate ticked up to 4.4% from the cycle-low 4.3% in July but is still down half a percent from a year ago.

- The annual increase in average hourly earnings was 2.5% for a fifth straight month.

Our Take:

The 156k increase in jobs in August was smaller-than-expected — and more-so when including 41k worth of downward revisions to the two prior monthly estimates. Looking through monthly volatility, year-over-year employment growth hit its lowest level since mid-2013 in August. Employment growth has long been expected to slow, though, as slack in labour markets is absorbed. By most estimates, even the recent pace would be sufficient to further tighten labour markets over time. The unemployment rate did tick higher in August but to a 4.4% rate that is still below the Fed's estimate of its long-run 'full-employment' level. The rate is still down half a point from a year ago and twice that when including sources of 'hidden unemployment' like discouraged workers.

More concerning to fed officials than slower job growth is likely to be the stalling out of wage growth year-to-date in 2017. Despite ostensibly tighter labour markets, wage growth has been stuck at 2.5% over the last 5 months, similar to the 2.6% average increase last year. The lack of further acceleration in wages coupled with a lack of inflation pressures continues to provide the fed with flexibility around the pace of monetary policy tightening despite what historically would look like relatively tight labour markets.

US Jobs Report: More Bad News For Fed Hawks

Is Another Rate Hike This Year Still Warranted?

If Federal Reserve policy makers were already starting to question the need for another rate hike this year - and the pace thereafter - then this week's data won't have made them feel any more comfortable.

Thursday's weak inflation data - continuing this year's trend of cooling price pressures - was today made all the worse by a poor August jobs report across the board with unemployment rising, job creation falling well short of expectations and earnings showing no improvement. Anyone hoping for a signal this month that the Fed is on track for another rate hike this year may well be disappointed.

The downward revision to July's NFP number was the icing on the cake. It's worth noting that while the numbers are disappointing, the labor market is still performing very well, but when inflation data is lacking, the Fed is relying on the employment data to justify more rate hikes.

While the dollar came under significant pressure after the release - as traders moved to increasingly price out a December hike - the move was quickly reversed against the euro. Just as Mario Draghi and his colleagues at the ECB were watching in disbelief as EURUSD headed back towards 1.20 and looked like easing past it, "ECB sources" came to the rescue and the move was quickly reversed.

In what appears to be far more than a coincidence, ECB source reportedly claimed that the QE plan won't be fully ready until December. This may be the sceptic in me but it would seem the central bank is paying far too much attention to its fx rate and may now even be planning its tapering announcement around it, or at least using it as a tool to hold back the currency.

The pound managed to hold onto its gains against the dollar which supports the view that the reversal was driven by the ECB source comments, as opposed to the usual volatility that can follow such releases.

Either way, the jobs report will be seen as a blow to Fed chances of another rate hike this year, as well as to Donald Trump who I'm sure would have loved nothing more than a reason to post something positive on Twitter. I feel this month's report may not make the Twitter cut.

Gold Hits 10-Month High as US Employment Numbers Disappoint

Gold has posted gains in the Friday session, continuing the upward movement we saw on Thursday. In the North American session, gold is trading at $1323.74, up 0.18% on the day. On the release front, US job numbers were unexpectedly soft. Nonfarm payrolls slowed to 156 thousand, well below the estimate of 180 thousand. Wage growth also disappointed, as Average Hourly Earnings posted a small gain of 0.1%, shy of the estimate of 0.2%.

Gold prices have enjoyed a strong week, gaining 1.9% this week. The metal showed some strong gains earlier on Friday, as the metal touched a daily high of $1329.05, its highest level since November 2016. These gains were triggered by the disappointing nonfarm payrolls and wage growth reports for August, both of which missed their estimates. Although the US labor market remains tight, investors are fretting about the lack of wage growth, which has contributed to the low inflation which continues to hamper the US economy. The Federal Reserve will also be dismayed by negligible wage growth, as a December rate hike is very much in doubt due to inflation levels which stubbornly remain well below the Fed's inflation target of 2.0%. Currently, the likelihood of a December rate hike stands at just 36%.

Gold is traditionally considered a safe-haven asset, and often benefits when investors get jittery and lose their risk appetite. Such was the case this week, as renewed tensions between the US and North Korea early in the week propelled the metal above the symbolic $1300 level. On Tuesday, North Korea fired a missile over Japanese territory, drawing sharp condemnations from Japan and the US, with President Trump declaring that "all options remain on the table". Although, tensions have since eased somewhat, if North Korea decides to fire another missile towards Japan or the US military base on Guam, gold prices will likely move higher. As well, as the markets digest the disappointing job numbers, we could see risk appetite continue to wane early next week, which could extend the current gold rally.

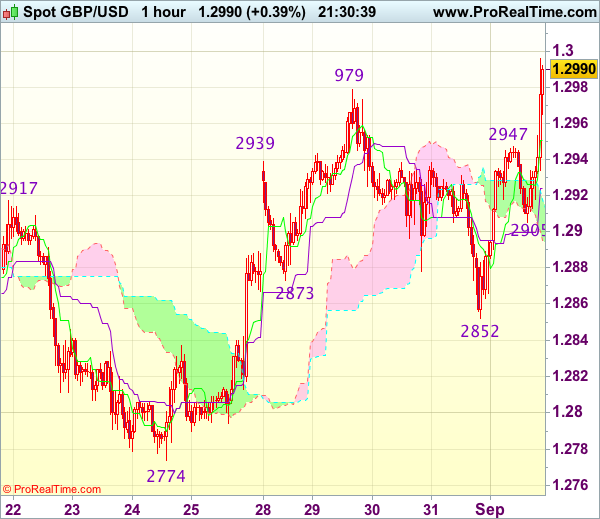

Trade Idea Update: GBP/USD – Target met and stand aside

GBP/USD - 1.2965

Original strategy :

Bought at 1.2855, met target at 1.2955

Position : - Long at 1.2855

Target : - 1.2955

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has rallied after finding renewed buying interest at 1.2905 today, justifying our bullishness and our long position entered at 1.2855 met upside target at 1.2955 (with 100 points profit), the breach of indicated resistance at 1.2979 adds credence to our view that early rise from 1.2774 has resumed, hence mild upside bias remains for this move to extend gain towards 1.3000 which is likely to hold on first testing and price should falter below previous resistance at 1.3032.

As we have taken profit on our long position entered at 1.2855, would not chase this rise here and would be prudent to stand aside for now. Below 1.2930-35 would risk test of said support at 1.2905 but only break there would signal top is formed instead, bring subsequent fall to 1.2875-80 and later towards said support at 1.2852.

Weak Wage Growth Unlikely to Dissuade the Fed from Normalizing Balance Sheet, But Rate Hikes Unlikely Until Inflation Firms...

Non-farm payrolls increased by 156k in August, well below the 180k expected by the street. Revisions to the previous two months' of payrolls subtracted 41k positions, with June and July hiring reduced to 210k and 189k, respectively. As a result, the three-month moving average of job growth slowed from 195k to 185k.

Private payrolls rose by 165k, just 8k below consensus expectations. Private-services hiring was once again led by business services (+40k), health care & education (+25k), other services (+16k) and finance (+10k). Goods hiring was robust, with manufacturing (+36k), construction (+28k) and mining & logging (+6k) all adding jobs. Government hiring (-9k) was weak, as all branches of government shed jobs.

The unemployment rate ticked up by 0.1 percentage points to 4.4% as the labor force increased by 77k while the ranks of the unemployed swelled by double that (151k). The participation rate was largely unchanged, at 62.9. Despite the tick-up in the headline unemployment rate, broader measures of labor underutilization were unchanged.

Average hourly earnings rose by 0.1% during the month, at half the pace that was expected, with downward revision to the past month. As a result, the year-over-year wage metric held steady at 2.5% in August.

Average weekly hours declined by 0.1 to 34.4.

Key Implications

It is not easy to find cheery news in the August employment report. The headline print disappointed expectations, contrary to the strong ADP print mid-week. Alongside the large downward revisions to prior months', trend payroll growth slowed from 195k prior to the report to just 185k given the new data. Lastly, the diffusion index – which measures the breadth of the gains across industries – pulled back a bit to 63.8.

Still, while not cheery, the report was not all doom and gloom. The pace of job creation still remained well above what is considered slack absorbing pace of around 100k per month. Moreover, most of the sectors that added jobs were the well-paying ones, while the ones readings were typically in industries that had strong hiring in the prior months. Importantly, the goods producing sectors, which often are a better indicator of underlying momentum roared on the month.

This report was not at all impacted by Hurricane Harvey, but we expect there may be an impact in next months' reports should the disruptions extend to mid-month. For more information about the impact of Hurricane Harvey click here.

Perhaps the most disappointing element of the report of the wage data, with the headline missing expectations and sizeable downward revisions to prior months. This is the element that the Fed is looking for as far as potential inflationary pressures, with the softness suggesting more patience as far as tightening of monetary policy. Ultimately, we don't expect the data to dissuade the Fed from beginning sheet normalization in the coming weeks, but any hikes are unlikely to take place until inflation and wages firm up. This is indeed what we're expecting, with the Fed still likely to hike at its December meeting, once the data flow becomes more constructive.

NFP Report: the Results

Any hopes that the Dollar could continue its rebound with an encouraging US jobs report, appears to have been thrown out the window, following a "hat-trick" of losses in the recently released jobs report for August. The number of jobs created in August, earnings and the unemployment rate, all fell short of expectations. The negative news doesn't conclude there; the figures for number of jobs created in both June and July, were also revised lower.

The headline figures coming out the Non-Farm Payroll report do not look encouraging for those investors who were looking to purchase the Dollar, at what could be argued as oversold levels - after the Dollar Index touched its lowest level since January 2015 earlier this week. I still feel that in terms of price action, the Dollar is oversold. However the employment sector has been one of the star performers for the US economy over the past two years and this news does not look encouraging for the jobs sector.

It's possible that this report could just be a one-off, but the headline news may encourage sellers re-entering the market to short the Dollar.

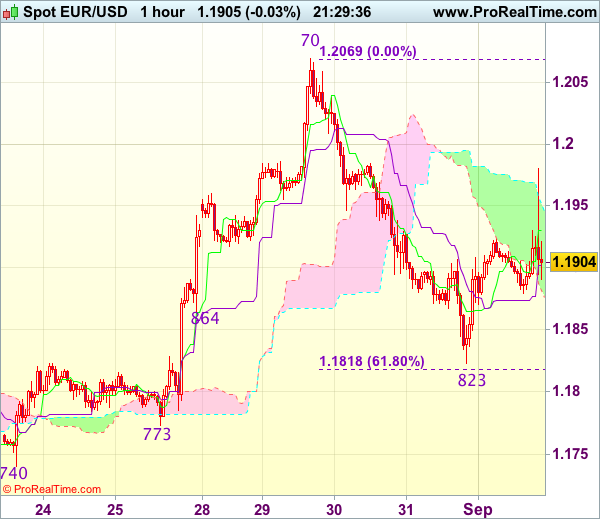

Trade Idea Update: EUR/USD – Hold short entered at 1.1975

EUR/USD - 1.1890

Original strategy :

Sold at 1.1975, Target: 1.1850, Stop: 1.2010

Position : - Short at 1.1975

Target : - 1.1850

Stop : - 1.2010

New strategy :

Had short entered at 1.1975, Target: 1.1875, Stop: 1.1945

Position : - Short at 1.1975

Target : - 1.1875

Stop : - 1.1945

Although the single currency staged a brief bounce to 1.1980 in NY morning after NFP, as renewed selling interest emerged there and euro has dropped again, retaining our bearishness or weakness to 1.1850, however, break of yesterday’s low at 1.1823 is needed to signal the fall from 1.2070 top has resumed and extend decline to 1.1815-18 (61.8% Fibonacci retracement of 1.1662-1.2070) but downside should be limited to 1.1790-00 and support at 1.1773 should remain intact.

In view of this, we are holding on to our short position entered at 1.1975. Above said resistance at 1.1980 would abort and signal the fall from 1.2070 has ended at 1.1823 yesterday, bring further gain to 1.2000 and possibly towards 1.2025-30 but still reckon upside would be limited to 1.2050 and price should falter below said this week’s high at 1.2070, bring another retreat later.

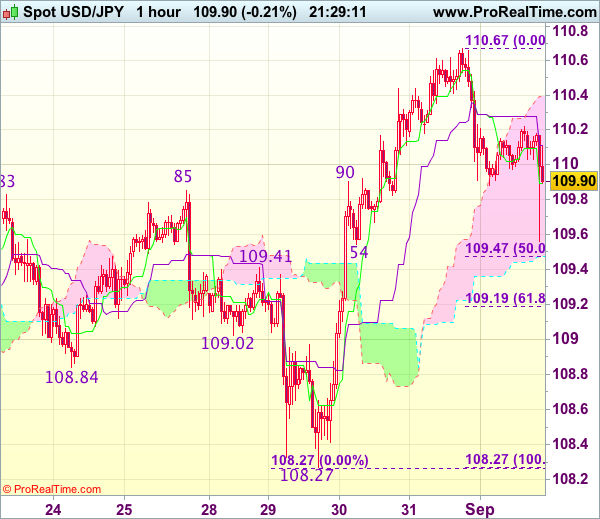

Trade Idea Update: USD/JPY – Exit long entered at 109.55

USD/JPY - 109.99

Original strategy :

Bought at 109.55, Target: 110.80, Stop: 109.20

Position : - Long at 109.55

Target : - 110.80

Stop : - 109.20

New strategy :

Exit long entered at 109.55,

Position : - Long at 109.55

Target : -

Stop : -

Although the greenback slipped in US morning on US NFP data, below 109.41-47 (previous resistance and 50% Fibonacci retracement of 108.27-110.67) is needed to signal top has indeed been formed at 110.67 yesterday, bring further fall to 109.15-20 (61.8% Fibonacci retracement) and possibly towards 108.95-00, however, reckon 108.55-60 would remain intact.

In view of this, would be prudent to exit long entered at 109.55 and stand aside for now. Above 110.20-25 would revive bullishness and signal an intra-day low is formed, bring further gain to 110.40, then retest of 110.67.

U.S Non-farm Payrolls Disappoint – Risk off, Dollar Down

- US Labor - Aug Nonfarm Payrolls +156K; Consensus +179K

- US Aug Unemployment Rate 4.4%; Consensus 4.3%

- US Aug Average Hourly Earnings +0.11%, or +$0.03 to $26.39; Over Year +2.5%

- US Aug Private Sector Payrolls +165K and Government Payrolls -9K

- US Aug Average Workweek -0.1 Hour to 34.4 Hours

- US Aug Labor-Force Participation Rate 62.9%

- US Jul Payrolls Revised to +189K; Jun Revised to +210K

- US Jul Unemployment Unrevised at 4.3%

August non-farm payrolls rose by a seasonally adjusted +156k m/m - the unemployment rate rose to +4.4% from +4.3%, though the level remains atop of historical lows.

For the Fed, wages maintained a modest growth rate.

Note: The data does not reflect any disruptions caused by Hurricane Harvey and related flooding in Texas.

Average hourly earnings for private-sector workers increased +3c last month to +$26.39 an hour. From a year earlier, wages rose +2.5%, consistent with their growth pace for most of this year.

The labor-force participation rate held steady at +62.9% in August.

Net result - the Fed will find it tough to sell another rate hike in 2017.

USD under pressure across the board (€1.1946, £1.2935, ¥109.70). U.S 10-year yields fall -2 bps to an intraday low for 2017 at +2.10% and gold prices rally +0.8% to +$1,1324.