Sample Category Title

The Weekly Bottom Line: Feeling The Impact Of Harvey

U.S. Highlights

- Substantial positive revisions to Q2 US GDP indicated stronger momentum going into the third quarter than previously thought, with Hurricane Harvey expected to shave 0.1-0.4 ppts. off growth in Q3.

- Inflation continued to be stubbornly elusive in July but we still expect a hike by the Fed in December, given that inflation will likely strengthen in the coming months.

- Global economies continue to strengthen alongside the US, with China's Caixin manufacturing PMI expanding to its highest level in six months in August, led by strong foreign demand for goods.

Canadian Highlights

- Hurricane Harvey is impacting Canada via higher gasoline prices and lower crude oil prices. On average, prices at the pump have jumped by 10 cents per litre this week, while the WTI-WCS spread widened by 20% to $11.75.

- Real GDP grew by 4.5% in the second quarter, marking the best 4-quarter performance since 2006. Growth of 0.3% in June provides a strong handoff for Q3.

- The CFIB Business Barometer fell for a third consecutive month in August, suggesting that the robust pace of growth is unlikely to last.

U.S. - Inflation Remains Elusive in Q3

It was a busy week for data this week in the US, with investors looking for clues on how the economy is performing and whether it warrants further tightening. Substantial positive revisions to Q2 US GDP indicated stronger momentum going into the third quarter than previously thought, with Q2 growth revised up to a robust 3.0% annualized. However, Hurricane Harvey, which made landfall in Southeast Texas last week, looks to be a transitory obstruction for the economy in Q3. The storm is expected to shave 0.1-0.4 ppts. off growth but a similar acceleration in Q4 should leave the second half of the year unchanged on balance. Harvey will also necessitate the passage of a disaster assistance package by the federal government. On that note, until further details surrounding policy and tax reform materialize, investors will remain fixated on economic data.

Evidence to support the Fed's tightening path was mixed as the week progressed. July's personal income & spending report highlighted the pivotal role of the consumer in the economic recovery, with strength in real spending apparent. But the missing piece of the puzzle continues to be inflation, which has been stubbornly elusive during this recovery. And this was compounded by Friday's jobs report that indicated relatively subdued wage growth -a trend that does not bode well for the inflation outlook (Chart 1). We still expect a hike by the Fed in December, but expect that inflation will materialize in the coming months. Manufacturing activity displayed pronounced strength in hiring in August while the positive ISM reading for the month prefaces continued strength in the sector going forward (Chart 2). As such, investor confidence in the American economy remains intact, which alongside weaker inflation has supported US equities.

Asian economies have also shown increased momentum lately. Case in point, China's Caixin manufacturing PMI expanded to its highest level in six months in August, led by strong demand for exports. That's a welcome development given concerns regarding the economy's slowing growth this year and the role that government debt has had in stimulating growth. Other Asian economies echoed this constructive tone, leading the MSCI Asia Pacific Index to a level just shy of a decade high.

European equities also reaped the benefits of improving economic data. Despite August's strong inflation reading in the Eurozone, the ECB is expected to leave its policy stance unchanged at next week's meeting. The committee's monetary policy path is complicated by the differing rates of recovery within the Eurozone. Germany and Northern Europe have displayed strong growth, while Southern economies including Greece and Italy are still grappling with slow employment growth and an elevated euro that is proving to be a barrier to export growth.

With a relatively quiet data release schedule for next week, investors will turn their attention to the array of speeches being made by FOMC members. Of central importance will be their views on the soft inflation and wage prints in recent data. Ultimately, we do not expect these developments to dissuade the Fed from beginning balance sheet normalization in the coming weeks, but some improvement on the inflation front is likely to be needed before another rate hike by the Fed.

Canada - Feeling The Impact Of Harvey

This week started off with Hurricane Harvey in the spotlight, as it barreled across Southeast Texas and Louisiana causing massive flooding and destruction in the area. While far removed from the devastation, Canada was not left unscathed by the tropical storm. Harvey has wreaked havoc on the energy industry - shutting in roughly a tenth of production and a third of all U.S. oil refining capacity - with the outages affecting the Canadian economy. The most visible impact has been on gasoline prices, which have risen on average by about 10 cents per litre since Monday, reaching the highest level seen in two years. The increase has been even more pronounced in some Canadian cities. Canada imports some refined products from the U.S., and the market is tightly integrated, suggesting no relief for drivers over the near-term. In fact, further increases expected over the weekend could push pump prices up to a 3-year high. It is too early to tell how long the flooding in Texas will persist, or how long refineries will be shut down. But, it is safe to believe that drivers will be facing elevated pump prices for several weeks.

Another impact has been on the Canadian oil sands, which have seen a drop in demand from the Gulf coast refineries. This has weighed on the price they receive for their heavy oil. The spread between Western Canadian Select - the benchmark for heavy oil - and WTI (which fell as expectations for lower refinery demand outweighed the oil production shutdowns) widened by 25% to $11.75 this week, marking the largest discount since March. Moreover, U.S. supplies of oil sands diluent (which is used to dilute bitumen so it can flow through pipelines) has been curtailed given a pipeline shutdown. Roughly a third of diluent used by oil sands producers comes from south of the border. While demand for Canadian oil may be weak in the near term, it will likely rebound once refining resumes.

On a brighter note, the highlight of the week for the Canadian economy was yet another stellar GDP report. Although backward looking, it showed that the economy expanded by a whopping 4.5% in the second quarter, marking the fourth straight quarter of robust growth. In fact, this is Canada's best four-quarter performance since 2006. What's more, economic activity grew by a solid 0.3% in June, providing a strong handoff for the third quarter.

That said, a repeat performance of the first half of the year is unlikely going forward. The small business barometer showed that optimism among businesses fell in August for a third consecutive month. This is typically a leading indicator, with these recent declines and weakness in forward looking indicators pointing to a deceleration in economic activity. Indeed, early tracking does suggest that economic growth will slow in the third quarter. However, it is expected to remain at an above-trend pace near 3%, which could push the economy into excess territory. Following the GDP report, odds of a rate hike in September edged up. However, given that there has been no communication from the Bank of Canada since its last meeting, we would be surprised to see a move next week. We do expect the rate hiking cycle to continue though, with a 25 basis point hike in October, followed by two more in 2018.

Canada: Upcoming Key Economic Releases

Canadian International Trade - July

Release Date: September 6, 2017

Previous Result: -$3.60bn

TD Forecast: -$3.30bn

Consensus: -$3.35bn

The goods trade deficit is forecast to narrow modestly to $3.3bn in July on a combination of weaker import and export activity. CAD appreciation should act as a driving force behind the pullback on both sides of the ledger after the loonie soared by roughly 4.5% during the month, though there are also a few one off events which could make for a noisy report. Gold bullion imports surged by 40% m/m in June and a full correction should single handedly shave $400m from the deficit. The stronger Canadian dollar should feed through to softer trade activity where FX passthrough is most prominent, namely agriculture and other unrefined resources, of which Canada is a net exporter. Motor vehicle exports should come under pressure in light of declining US demand, a pullback in Canadian production and downward pricing pressures. Imports however should remain well supported by a resilient Canadian consumer.

Canadian Employment - August

Release Date: September 8, 2017

Previous Result: 10.9k, unemployment rate: 6.3%

TD Forecast: 10k, unemployment rate: 6.3%

Consensus: 15k, unemployment rate: 6.3%

The Canadian economy is forecast to add 10k jobs in August, little changed from the prior month but subdued in comparison to the lofty pace in Q2. Job growth should skew towards public and private employees, which would coincide with a pullback in self-employment after a strong two months. Last month's 35k gain in full time employment was in line with the six-month trend and while we could see some moderation from these levels, there is no catalyst to suggest an outright correction. The unemployment rate should hold steady at 6.3%, a record low for the current cycle, though the risks lean a 6.4% print should last month's pullback in labour force participation correct. Wage growth, currently sitting at a subdued 1.2% y/y, should a modest pickup on the heels of the tightening in labour market conditions and muted base-effects from last August.

Dollar Mixed After Jobs Miss Ahead of BoC and ECB

Mixed economic data and political turmoil has hurt USD

The US dollar is mixed against majors after staging a comeback late in the week. The USD regained some ground even though the biggest indicator in the market the U.S. non farm payrolls (NFP) report disappointed by adding less than the expected number of jobs (156,000 versus 180,000) but the data point that had more significance was the low pace of growth of wages at 0.1 percent. A third rate hike for US interest rates could be pushed back to next year if inflation does not pick up convincing the Federal Reserve.

The Canadian dollar was of the biggest movers against the USD. Canadian GDP for the second quarter destroyed expectations with a 4.5 percent quarterly growth when a slight slowdown was expected. The strength of the economy has put a second rate hike to the Canadian benchmark rate firmly on the table. The Bank of Canada (BoC) will be publishing a rate statement on Wednesday, September 6 at 10:00 am EDT.

The EUR kept losing ground as the week passed with reports of the council not having a final decision on its plans for tapering quantitive easing. The lack of communication has allowed the USD to appreciate versus the single currency ahead of its September monetary policy meeting. The European Central Bank (ECB) will publish its benchmark rate on Thursday, September 7 at 7:45 am EDT. ECB President Mario Draghi will offer a press conference at 8:30 am EDT. There is a sense of urgency as the ECB Governing council will hold its first formal talk on the subject leaving just two meetings before the end of the year.

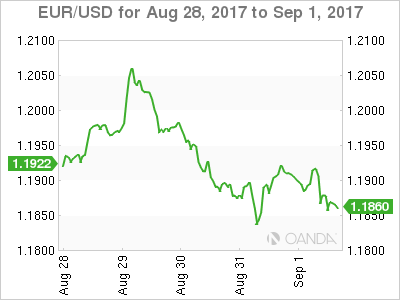

The EUR/USD dropped 0.154 percent in the last five days. The single currency is trading at 1.1868 near weekly lows after the USD managed to recover from losses earlier in the week when the pair touched 1.20 only to start sliding downward as positive US data was released. The U.S. non farm payrolls (NFP) was the most anticipated indicator this week and it disappointed with a headline jobs miss and soft wage growth in the United States.

The Trump administration has used hardball tactics ahead of the second round of NAFTA renegotiations that are taking place in Mexico City. Although the treaty itself leaves the door open for any member to exit the deal by giving six months notice, there are winners and losers of the deal in all three countries. American businesses would be hurt by a sudden end to the agreement, although their gain came from the job losses suffered in America that propelled Mr. Trump into the White House. American companies are hard at work lobbying for the deal to be reshaped for the modern world, but instead are getting anxious at Trump's tweets threatening to end NAFTA. The three nations have signed non-disclosure agreements on the negotiations leaving the market to speculate on the talks as they happen.

The comments from European Central Bank (ECB) President Mario Draghi were thought to be one of the most awaited during the Jackson Hole summit in late August, but failed to bring any light into what the next steps would be for the central bank. With their September monetary policy meeting close at hand, some communication around the timeline of the tapering of quantitive easing. Little word could mean no plans to launch the tapering program in September, leaving it up once again for a December monetary policy with a major decision like in previous years. The ECB will post its rate statement on Thursday, September 7 at 7:45 am EDT and will be followed by a press conference with Mr. Draghi at 8:30 am EDT.

Gold rose 2.44 percent this week. The yellow metal is trading at $1,323.70. The commodity was the biggest winner of a soft August employment report. The lack of a strong wage growth component is putting into question the U.S. Federal Reserve's plans for a third rate hike in 2017 and helping gold reach higher. The metal had its second best month in August only after January. The threat of North Korea as well as the turmoil in Washington and the impact of Hurricane Harvey had the dollar under pressure from geopolitical events. Macro indicators offered little help with Jackson Hole comments offering no support of the USD and although the ADP jobs report and an improvement on second quarter GDP were offset by the miss of the NFP report.

US Oil prices dropped 1.054 percent this week. The price of West Texas Intermediate is trading at $47.04 after the impact of Hurricane Harvey has caused a glut of crude oil, while limiting the capacity to refine it into gasoline making the price of the distillate soar. The Department of Energy has released 4.5 million barrels of the US strategic reserve destined to be refined in Louisiana to try to keep prices stable until refineries in Texas can reopen.

US oil interests are also under threat as the NAFTA trade talks take place in Mexico City. The treaty has allowed US producers to sell refined products back to Canada and Mexico, but could end up being caught in a tariff war if Trump decides to walk off the negotiating table.

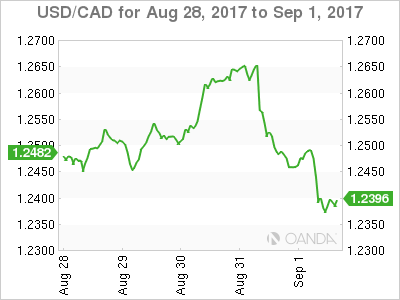

The USD/CAD fell 0.712 percent in the last five days. The currency pair is trading at 1.2384 near weekly lows. The Canadian dollar took advantage of the ills that affect the USD and combined with strong economic indicators appreciated during the week.

The Canadian economy surprised to the upside with a 4.5 percent GDP growth in the second quarter being expectations of a 3.7 percent increase. This makes Canada the best performing country in the G7 and has put a rate hike before the end of the year firmly on the table. The Bank of Canada (BoC) is set to deliver its rate statement on September 6, which could be too early with market analyst favouring the October monetary policy meeting which could give the central bank enough time to see what its American and European counterparts will be launching in September. Bond markets are pricing in a 37.8 percent probability of a rate hike in September, up from yesterday's 20.9 percent. The October rate hike has a 86.8 percent chance according to fixed income prices.

The Bank of Canada (BoC) will release its rate statement on Wednesday, September 6 at 10:00 am EDT. The better than expected second quarter GDP has increased the probability of a rate hike in September, but the majority of analysts still view October as a more likely scenario. The Canadian benchmark rate sits at 0.75 percent and still 25 basis points below where the rate was in early 2015 before the BoC made two proactive rate cuts.

Market events to watch this week:

Monday, September 4

- 4:30 am GBP Construction PMI

Tuesday, September 5

- 12:30 am AUD Cash Rate

- 12:30 am AUD RBA Rate Statement

- 4:30 am GBP Services PMI

- 9:30 pm AUD GDP q/q

Wednesday, September 6

- 8:30 am CAD Trade Balance

- 10:00 am CAD BOC Rate Statement

- 10:00 am CAD Overnight Rate

- 10:00 am USD ISM Non-Manufacturing PMI

- 9:30 pm AUD Retail Sales m/m

- 9:30 pm AUD Trade Balance

Thursday, September 7

- 7:45 am EUR Minimum Bid Rate

- 8:30 am EUR ECB Press Conference

- 8:30 am USD Unemployment Claims

- 11:00 am USD Crude Oil Inventories

- Tentative CNY Trade Balance

Friday, September 8

- 4:30 am GBP Manufacturing Production m/m

- 8:30 am CAD Employment Change

*All times EDT

Take the ISM with a Grain of Salt

The 58.8 reading for ISM signals the fastest pace of manufacturing growth in six years. The factory sector is undoubtedly on an upswing, but August can be a head-fake. Watch for inventories to boost growth in H2.

After Lame Jobs Report, ISM Does Not Disappoint

After the dud employment report earlier this morning, the latest print for the ISM manufacturing index offers a little more excitement. Manufacturing activity in August rose to its highest level (58.8) since 2011, according to the Institute for Supply Management.

Most months, the ISM release becomes available prior to the almighty jobs report, but when the stars align such that the first Friday of the month happens to fall on the 1st, the jobs number hits the wire an hour and a half before the ISM. That can matter because the employment component of the ISM can offer clues about the direction and magnitude of hiring. In this case, advance knowledge might not have helped.

The consensus overshot the extent of job growth for August, but expectations might have been even greater if we had advance knowledge that the ISM would shoot higher and the employment component would soar to a six-year high of 59.9.

Admittedly, manufacturing jobs have gone 10 months without a decline and the 36,000 increase reported in August was the biggest monthly increase in four years. So, maybe this ISM report is not such a red herring after all.

Remember What Kipling Said about Triumph and Disaster

Before we get too far ahead of ourselves celebrating the great manufacturing renaissance, it bears noting that the August print for ISM last year was an aberration and this may be as well. August has proven to be a difficult month for seasonal adjustment at the Labor Department and perhaps the ISM has had similar issues. Last year in August the ISM suddenly and unexpectedly fell below 50, signaling contraction, but a month later the ISM jumped to 51.7 and has not returned to contraction territory since.

Tell Me an Inventory Story

As we wrote in a recent special report, "Inventories: The Tail That Wages the Dog in Q3?", after an uncharacteristically calm stretch, inventory dynamics may play a big role in the third quarter. There are some clues in today's ISM about the current state of inventory dynamics. In fact the two largest overall moves in the month were in the inventories component, which jumped 5.5 points, signaling the fastest pace of stockpiling in seven years and customer inventories, which dropped 8.0 points to 41.0 which suggests customer inventories are too low—the lowest in fact that we've seen in six years. The takeaway in our view is that there is a bulge getting ready to work its way through the supply chain and as that plays out we expect inventories to be additive to topline GDP growth in the second half of 2017. Of course, Hurricane Harvey will introduce an additional degree of variability which we will be monitoring.

Weekly Market Outlook: ECB, BoC, RBA, and Riksbank Policy Meetings, Key Data in Focus

Next week's market movers

- The main event will probably be the ECB policy gathering. Market focus may be on whether the Bank will remove more dovish aspects from its forward guidance.

- In Canada, the BoC is expected to remain on hold. Expectations for another rate hike this year remain elevated, and investors may look for a confirmation on that front.

- The RBA and the Riksbank are both likely to stand pat as well.

- We also get key economic data from Australia, the UK, the US, Canada, and China.

On Monday, the UK construction PMI for August will be in focus and subsequently on Tuesday, we will get the services index for the same month. We expect market participants to focus primarily on the services print, as services account for the vast majority of the UK economy. The index is expected to have slid somewhat, but given that the manufacturing PMI unexpectedly rose on Friday, we see the case for a rebound here as well. Having said that though, we don't expect something like that to revive speculation with regards to a BoE rate hike this year. At the time of writing, the UK Overnight Index Swaps (OIS) suggest that the probability for a hike by year-end is 23%. Even though that appears low at first glance, we believe that it is in fact overly optimistic. Even if the August PMIs suggest that the economy has gained some momentum, back in June, Governor Carney made it clear that any near-term hike would likely depend on a pickup in wages and business investment. Therefore, officials are likely to wait for improvements in those two fronts before start looking at the hike button.

On Tuesday, during the Asian day, the RBA will announce its policy decision. At its latest gathering, the Bank refrained from acting, as was widely expected, while the statement accompanying the decision showed once again that officials are content with the strong employment growth. However, they were still concerned regarding subdued wage growth, a view that was confirmed a couple of weeks later after data showed that wages rose at the same lackluster pace as in Q1 on a yoy basis. The continued softness in wages makes us conclude that the RBA is highly unlikely to act at this meeting, or the next few ones, and suggests that it won't even try to shift its stance to more hawkish anytime soon.

As for the Aussie, an important point in the latest statement was officials' discomfort with regards to its appreciation. A few days later Governor Lowe added more fuel to the fire by reminding investors that direct FX intervention is always on the table if needed. Nevertheless, the minutes of the latest gathering revealed that policymakers were less concerned with regards to the Aussie's strength than what was initially interpreted. Therefore, given that we don't expect any changes in policy, nor the Bank's language, we will dig into the statement for any hints that clear up the picture around the Aussie's strength.

On Wednesday, the central bank torch will be passed to BoC. The last time Bank officials gathered to decide on monetary policy, they judged it right to raise the benchmark interest rate by 25bps, in line with market expectations. The tone of the statement accompanying the decision was on the hawkish side, with the Bank dismissing the until-then soft inflation as being temporary. Most importantly, policymakers kept the prospect of further near-term hikes on the table. Since then, data showed that even though headline inflation slowed in June, it rebounded in July to fractionally below the Bank's forecast of inflation averaging at around 1.3% in Q3.

Although another rate hike this year is more-than-fully priced in, according to Canada's Overnight Index Swaps, we don't expect a rate increase to come at this gathering. We believe that policymakers may prefer to wait for August's and September's CPI prints before they arrive to safe conclusions that inflation is progressing in line with their forecasts. We expect them however to maintain their hawkish bias. Indeed, the economy's output gap continues to narrow at a steady pace and is expected to close entirely by the turn of the year, which implies that inflationary pressures are likely to pick up afterwards.

As for the economic data on Wednesday, Australia's GDP print for Q2 will be in focus. Without a forecast available, we see the case for the nation's growth rate to have accelerated following a mere +0.3% qoq in Q1. Even though iron ore prices tumbled somewhat in Q2, the labor market continued to tighten and perhaps most importantly, retail sales were exceptionally strong.

In the US, the ISM non-manufacturing PMI for August is due out and the forecast is for the index to have risen somewhat after declining significantly in July. Something like that could be encouraging news for FOMC policymakers, and would likely be another piece of data entering the basket of those supporting the case for another rate hike this year. That said, as we have noted countless times, the main determinant of whether another hike will indeed materialize this year may be US inflation data. According to the Fed funds futures, following the disappointing US employment data for August, market pricing currently suggests only a 26% probability for such action.

On Thursday, market participants will turn their eyes to the highly-anticipated ECB policy gathering. Given that no change in policy is expected, market focus may be on whether the Bank will remove more dovish aspects from its forward guidance. Specifically, whether it will remove from its statement the easing bias that QE can be expanded both in terms of size and/or duration if needed. However, a week ahead of the gathering, Reuters and Bloomberg reports, citing sources familiar with ECB discussion, poured cold water on such expectations.

The Reuters report noted that sources said that "rapid gains by the euro against the dollar are worrying a growing number of policymakers". They also noted that this raises the chance that asset purchases will be phased out only slowly and that the ECB is highly unlikely to take any decision at this meeting. The Bloomberg report also noted that the governing council has no appetite to rush into a decision when it meets on Thursday, and added that policymakers may not be ready to finalize their decision until December.

These developments suggest that in case the Bank maintains its QE easing bias, the market may react little as it has already responded to the aforementioned reports. The surprise would be a removal of that bias.

Another key point of interest may be any comments regarding the rapid pace of the euro's appreciation. Although the aforementioned sources said that the ECB is getting more concerned with regards to the euro's appreciation, Governing Council member Ewald Nowotny noted on Friday that the Bank shouldn't "overdramatize" the euro rise and that exit from policy can't be about stepping on the brake.

As for our view, while we may not get any changes or hints at this gathering, we still believe that the QE-exit may begin by the turn of the year. The minutes of the July meeting revealed some concerns regarding the risk of the exchange rate overshooting in the future, but officials also noted that the recent appreciation could be seen as reflecting changes in the fundamentals of Eurozone. Therefore, as long as Draghi continues to remind us that financial conditions remain accommodative, we don't expect a reversal in the common currency's uptrend. Even if the Bank seizes the opportunity to express some further worries about the euro's strength, we expect something like that to only trigger a correction lower. The risk to that view is any signals that the currency's appreciation has started weighing on inflation, or any hints that financial conditions in general have started to tighten due to that.

A few hours ahead of the ECB, the Riksbank will announce its own interest rate decision. At the latest policy gathering, the world's oldest central bank disappointed investors looking for a removal of its interest rate easing bias, as the Norges Bank and ECB had done a few days earlier. Although the Riksbank noted that the likelihood for further easing is lower than previously, it still kept the option on the table. Ever since, inflation has risen at a pace much faster than the Riksbank anticipated in its latest forecasts, and now lies above the 2% target. In July, the nation's CPI rate rose to 2.2% and the CPIF surged to 2.4%, while the Riksbank anticipated these rates to average 1.6% and 1.8% respectively in 2017. This upbeat development, and the fact that economic growth in Q2 was much stronger than expected, make us believe that the Bank could proceed with removing its interest rate bias at this policy gathering.

The key risk to our view relates to the strength of the SEK. Even in the minutes of the latest meeting, policymakers reiterated that for inflation to stabilize around the target, the krona must not appreciate too rapidly. However, the krona gained further against both the dollar and the euro since then. Granted, the dollar has been weak overall, so there's no surprise there. However, the fact that it also gained against the almighty euro suggests that buying interest around the SEK is strong, which could make the Riksbank hesitant to remove dovish aspects of its forward guidance.

Finally on Friday, during the Asian morning, China will release its trade balance data for August.

In Canada, employment data for August are coming out, though no forecast is available yet. Neither the Markit nor the Ivey PMIs for the month have been released by the time of writing, so we do not have any major gauges of how the labor market fared in August. In any event, we believe that the Loonie's short-term direction may be decided primarily by the outcome of the BoC policy meeting earlier on Wednesday.

Weekly Market Outlook: Tensions Are Mounting Ahead Of ECB And Fed Meetings

- ECB: Let The Games Begin - Peter Rosenstreich

- Tensions Are Mounting Ahead Of ECB And Fed Meetings - Arn

- ud Masset

- Hurricane Harvey Impacts Crude Oil Prices - Yann Quelenn

- German Leaders

FX Market - ECB: Let the games begin

At this week's European Central Bank policy meeting we expect the Draghi will signal a step-away from emergency measure by removal of easing bias and deceleration in pace of asset purchases. Yet, details are not expected until next meeting at the end of October. In addition, the ECB president could emphasize new forward guidance on rates to lessen signaling effect of the actual change. To cushion the blow and avoid excessive Euro appreciation, Draghi will attempt to hide the clear meaning and stress that reduction is not tightening. This feat likely be accomplished by puzzling "Greenspan-like" language, stressing flexibility and eventually extending the asset program by six months, (slowing monthly pace of purchased to €30bn). Just enough information to place the seed of doubt in euro bulls mind.

The rational for removing emergence measure via the reduction of bond purchase is simple. The European economy has recovered strongly. According to members, European growth "was increasingly selfsustaining and hence had become less dependent on the current degree of monetary policy accommodation". This also supports our thinking that the ECB growth projections will be revised higher. However, inflations path remains subdued as even Augusts uptick was item specific and not broad-based. There is increasing discussion that reduction is less economic decision and more market structure driven choice. Should the ECB continue its €60bn monthly purchases, holding of German sovereign debt would reach its self-imposed limited to by a maximum of 33% of issuers bonds. Shortly after bond holding limits will be breached with other core EU nations. The ECB could adjust the limit, however ruling by the European Court of Justice and the German Constitutional Court indicated the purchase program is legal only if they refrain from monetary financing. Draghi in May indicated awareness of Treaty rules and had no intentions of challenging.

Friday ECB Nowotny stated that Euro moves shouldn't be "overdramatized" and chance QE plan not fully ready until Dec. Already member are taking down expectations. Draghi careful comments in a speech in Sintra, generated volatility as yields and euro reacted significantly. The ECB will proceed cautiously with the removal of monetary stimulus, maintaining flexibility and controlling any excessive appreciation in Euro.

Economies - Tensions Are Mounting Ahead Of ECB And Fed Meetings

The week started fairly well for the greenback as investors reduced their short positions ahead of a full week of economic data. The first batch of data was quite encouraging with ADP employment change rising to 237k versus 185k expected and the second print on the second quarter GDP being revised to 3%q/q (annualised) from 2.6% initially estimated. The dollar index reversed the trend as it climbed back towards the 93 threshold. However, things started to deteriorate slightly on Thursday amid a mixed personal income and spending reports and flat inflation readings.

Indeed, personal spending and income came in roughly in line with expectations, though the former printed slightly lower, suggesting that personal consumption should continue to improve in the third quarter. Moreover, June's personal spending was revised to the upside from a flat reading to +0.2%m/m. However, investors should remain cautious regarding the outlook as Hurricane Harvey will surely weigh on those measures in the coming months.

On the inflation front, the Fed's favourite gauge matched expectation with the core personal consumption expenditure printing at 1.4%y/y in July, down from 1.5% in the previous month. This lacklustre inflation reading is of bad omen for the Fed monetary policy normalization process. However, the economy has recently gather momentum and it should translate into a pick-up in consumer prices at some point. It will just take time.

Expectations were quite high for the jobs report. NFPs were expected to trail ADPs with median forecast standing at 180k while wages were anticipated to have expanded 2.6%y/y in August. Nevertheless, it was a big miss as all those gauge missed market's expectations. The US economy created only 156k non-farm jobs, while average hourly earnings grew 2.5%y/y. Finally, the unemployment rate ticked-up to 4.4%. On a more positive note, we remain cautious regarding August data in general as it has proved to be subject to significant statistical distortions. One therefore has to take those figures with a grain of salt. The market's reaction was harsh with the dollar tumbling 0.50% against most of its G10 peers. Yet this negative USD sentiment didn't last long as ISM manufacturing came in above expectations, printing at 58.8 versus 56.5 median forecast.

It was a bumpy week in the FX market as investors become nervous ahead of this week ECB meeting and next week Fed meeting. Traders are and will remain highly sensitive to economic data until September 20th. This going to be a busy week as many central bank will update their police stance. The RBA (Australia), BoC (Canada), BCB (Brasil), Riksbank (Sweden) and finally the ECB are expected. Be ready for a potentially bumpy week.

Economics - Hurricane Harvey Impacts Crude Oil Prices

The US Energy Department has released earlier last week inventories data which shows a decline of 5.932 million barrels during the week ending August 25. It is the ninth consecutive weeks of decline and crude oil had lost 1% and was now challenging its 6-week low before bouncing back.

Oil fundamentals are challenged by the tropical storm Harvey which is ravaging Houston and some US refineries out there are now closed temporarily. Yet, markets were clearly not fearing any potential shortages within the short-term as crude oil is most of the time very easy to replace. Any shortage longer than a week or ten day are usually driving crude oil prices higher. It now seems that some refineries will stay closed for at least two weeks and crude oil prices jumped 10%. This natural disaster has a significant impact on prices. Upside risks should likely persist within the next few weeks.

Other fundamentals are not very enthusiastic for the US refining industry. The trend in the rig count is bearish due to sustainable low prices. Numbers of rigs declined to 940 from a week earlier. Yet it is still up from last year. Now markets will start pricing in the next OPEC meeting late November. We do not consider that any production cut will be applied. The market share war between OPEC members and the US will continue and the US are likely to keep suffering.

Anyway, we keep on believing that upside pressures on oil are ahead of us. In particular, at the moment, there is a seasonal effect that should soon be back. In September the demand for crude oil normally increases as the summer season is over and overproducing oil is not a viable longterm project. Today's low crude oil prices are definitely preparing tomorrow high prices.

Themes Trading - German Leaders

German companies remains the most valued in Europe. High-end manufacturing and solid governance continually make German equities a quality investment. German stocks are likely to experience volatility ahead of the federal election on 24 September, yet the expected outcome should provide the needed stability, therefore the longer-term outlook remains bright. Germany is the largest economy and a dominant political force in Europe, often steering policy decisions towards its own selfinterest. ECB overnight rate is expected to remain negative for another 12 months, but tightening monetary policy is approaching. Investors will look towards Germany's fast growing companies for a higher rate of return. Worries over the effect of a stronger euro on Germany's export-driven economy has weighed on the DAX bullish momentum. Yet despite the higher euro, European companies have revised their 2Q earnings higher by an average of 1%, the financial and automobile sectors being the strongest. An improving global trading environment, world-class brands and lagging valuation will keep investors interested in German corporate stocks. This Theme was built using the top German large and midcap companies.

Week Ahead – Markets Look to ECB Meeting for Euro and Tapering Guidance; RBA and BoC also Meet

Monetary policy will dominate the coming week as the central banks of Australia, Canada, the Eurozone and Sweden hold their scheduled policy meetings. Data wise, the focus will be on trade and industrial output indicators, with a number of countries reporting, including Germany, France and the United Kingdom. However, it will be a slow start to the week with both US and Canadian markets closed on Monday for Labour Day.

Important week for aussie with GDP and RBA meeting

The Australian dollar has been consolidating after reaching a two-year high against the greenback in late July. Next week's risk events could provide investors some much-needed direction. Business inventories data due on Monday for the second quarter will be watched closely as it should be indicative of Wednesday's GDP data. The Australian economy is expected to have picked up speed in the second quarter. After growing by just 0.3% quarter-on-quarter in the first three months of the year, GDP growth is forecast to improve to 0.8% in the second quarter.

The Reserve Bank of Australia will likely have advance knowledge of the GDP data when it meets on Tuesday to set interest rate policy. RBA Governor Philip Lowe had said back in August "I think that they are reasonable assumptions, that the next move will be up, rather than down, but it will not be for some time". His comments reinforced expectations that the RBA will keep rates at the record low of 1.5% for a considerable period of time and no deviation from the neutral stance is expected next week. However, the Bank's wordings on the strength of the economy and the exchange rate in its statement will nevertheless be carefully scrutinized.

Also to watch out of Australia next week will be July retail sales and trade figures on Thursday, and housing finance data on Friday.

Bank of Canada rate rise on the horizon after strong GDP

Canada's economy grew by an unexpectedly robust annualized rate of 4.5% in the second quarter, fuelling expectations that the Bank of Canada may raise rates as early as the September meeting on Wednesday. Prior to the GDP figures, October was seen as the favourite after the BoC signalled that a second rate increase was likely following its surprise hike in July. The strong growth figures have raised the odds of a September move to around a third and it's now looking almost certain that the overnight rate target will go up to 1.00% by October. The Canadian dollar's rally against the US dollar has stalled over the past month as a second rate hike has already been priced in. The loonie could therefore prove sensitive to any shift in the Bank's tone next week.

Important data releases will also attract attention, starting with July trade figures on Wednesday, the Ivey PMI on Thursday and the August employment report on Friday.

Quieter week for the US

South of the border, the US calendar will take a backseat with major data being limited to the ISM non-manufacturing PMI. The closely watched indicator is forecast to increase to 55.3 from 53.9 in August when released on Wednesday. Other US data will include factory orders on Tuesday, and trade figures and IHS Markit's final services PMI on Wednesday.

Chinese trade and inflation data eyed

Following the release of better-than-expected manufacturing PMIs in China this week, there is growing confidence that China's economy will slow only marginally in the second half of 2017. Exports from China have recovered strongly this year despite a gradual appreciation of the yuan, signalling a strengthening global demand. The latest trade numbers out on Friday should show if this trend continued in August. Producer and consumer price data will follow on Saturday. Rising producer prices is seen as a positive development not just for China's economy but also for the global economy as it can boost profitability for local companies as well as export inflation to the rest of the word. After surging to 7.8% in February, producer prices eased to 5.5% in May and have been stuck there ever since. Another fall in August could worry investors.

UK industrial output and PMIs in focus

The stalemate in the Brexit negotiations has been weighing on the pound this week but UK data due in the next seven days may provide some much needed distraction for traders. First up will be the IHS Markit/CIPS construction PMI on Monday, which will be followed by the services PMI on Tuesday. The construction PMI is forecast at 51.8 in August, while the services PMI is expected at 53.5, both down on the month. Although this week's manufacturing PMI beat expectations, a similar upside surprise is less likely for the services PMI given the weakening picture for consumer spending.

On Friday, attention will shift to trade and industrial output. Industrial production is expected to rise by 0.1% month-on-month and 0.4% year-on-year in July. Output in the manufacturing sub-sector is forecast to expand by 0.3% m/m and 1.7% y/y. The figures are not impressive when considering the significant depreciation of sterling after the Brexit vote. The pound's Effective Exchange Rate Index has recently come close to reaching last October's 7½-year low, but so far, UK exports have received only a modest boost, leaving the country's current account position highly exposed at a time of uncertainty. July trade numbers out on Friday should show whether there's been any improvement on this front.

All eyes on Draghi as ECB tapering discussions loom

A decision on winding down its massive asset purchases has been a long time coming for the European Central Bank, but investors will probably have to wait till October for any announcement on the decision, with discussions on the topic only set to start at the September 6-7 policy meeting. ECB officials have been signalling that any scaling back of the stimulus program will be very gradual and that scenario is looking increasingly likely given the euro's recent sharp rally. Sources close to the ECB told Reuters this week that "the exchange rate has become a bigger issue" for ECB policymakers, adding to speculation that ECB chief, Mario Draghi, will use his press conference next Thursday to verbally intervene to stem the euro's rise.

The single currency may find it difficult to repeat this week's 2½-year high of above $1.20 in the run up to the ECB meeting, but Eurozone data should give traders something other than the ECB to talk about. The Eurozone sentix reading for September is due on Monday, along with the July producer prices for the region. July retail sales and the final services and composite PMIs for August are out on Tuesday, and the third revision to Eurozone GDP for the second quarter is due on Thursday (though no revision is expected). Also of interest will be German and French industrial output and trade data on Thursday and Friday.

The ECB will not be the only central bank in Europe holding a meeting as Sweden's Riksbank will announce its decision a few hours before the ECB. The Riksbank was criticised this week by one of Sweden's largest banks, SEB, for its continued dovish policy stance, which has failed to keep a lid on the krona's gains. The Swedish krona has appreciated around 12% against the dollar in the year to date and is flat against the euro. Markets see the Riksbank's ultra-loose policy as unsustainable given above 2% inflation (July) and 4% GDP growth (Q2). Although no change in the repo rate is expected on Thursday, currently at -0.50%, the bank may signal the end to its easing bias.

NFP Disappoints But Dollar Finds Support on Manufacturing PMI; Euro Down as ECB Constancio and Nowotny Remain Cautious

The dollar went downhill during the mid-European trading hours as the widely expected and Fed's closely watched indicators, nonfarm payrolls and earnings, came in worse than expected in August but managed to recover on upbeat manufacturing PMI readings. The euro hit lower while the dollar was rebounding but did not show significant reaction to the less hawkish remarks made from ECB officials on Friday.

While analysts expected nonfarm payrolls to increase by 180,000 in August, the actual number popped up far below expectations at 156,000, while July's mark was downwardly revised to 189,000 from 209,000 estimated initially. Although the figure underperformed previous months' prints, it was more than the 75,000 to 100,000 jobs needed for the workforce to keep expanding.

The unemployment rate rose marginally by 0.1 percentage points to 4.4%, missing the forecast of 4.3%, while the participation rate stood flat at 62.9%, pointing that the economy still operates under full employment conditions.

Regarding labour payments, average hourly earnings dropped surprisingly by 0.2 percentage points to 0.1% m/m, while forecasts supported a growth of 0.2%. However, on a yearly basis earnings continued rising by 2.5% for a fifth consecutive month.

Despite labour data weakening, the US manufacturing activity improved surprisingly in the aforementioned month according to the ISM manufacturing PMI readings published few hours later. The index climbed by 2.5 percentage points to 58.8, exceeding the projections of 56.5. The Markit equivalent gauge went up as well from 52.5 to 52.8.

The dollar index sank by 0.75% to an intra-day low of 92.05 in the wake of the labour data, but the evidence on the manufacturing PMI helped the greenback to reverse losses and move up to 92.72.

Dollar/yen hit a low of 109.55 before it rises to 110.74.

The euro gained on US labour data, advancing to $1.1978. However, it fell to $1.1872 following the dollar's rebound.

Besides that, currency markets were indifferent to less hawkish comments made today by the ECB vice president Vitor Constancio and the ECB governing council's member Ewald Nowotny, just a few days before the central bank kicks off its next monetary policy meeting on Thursday in Frankfurt. Constancio, during his speech at the Forum Villa d' Este, said that rising inflation might be a difficult manner than it was earlier thought to be. Additionally, he said that weak global "reflationary pressures" are mainly restricting inflation and employment to reach targets. However, he added that the monetary union is now more resilient to shocks. Nowotny, speaking to reporters today, argued that the markets should not over-interpret the euro's 13% rise against the dollar this year. Moreover, he said that a careful examination should be conducted before the ECB limits its asset purchases which amount to 2.3 trillion euros.

Meanwhile, data out of the region showed that manufacturing activity in the euro area remained robust in August, with the sector's PMI increasing by 0.8 points to a six-year high of 57.4, as expected. The figure for Germany, the largest European economy, strengthened from a five-month low of 58.1 to 59.3. Yet, it fell slightly short of expectations which were for the indicator to rise to 59.4.

Cable surged to a two-week high of 1.2994 before it sank to 1.2953. Manufacturing PMI out of the UK gave also some support to the pound earlier in the session, reaching the highest level in three years. The index improved by 1.3 points to 56.9, above the 55.0 expected.

Turning to commodities, oil prices pared losses made in the Asian session as tropical Hurricane Harvey forced major energy refineries to shut down, spreading fears of fuel shortages during the weekend and Labor Day holiday that follows. According to Reuters estimates, the refineries shutdown has impacted about 4.4 billion barrels per day of output. WTI crude futures (October) rose to $47.15 per barrel while Brent climbed to $52.87.

Gold gained some ground in the middle of the European session, rising to $1321.84 per ounce.

Australia & New Zealand Weekly: How Our Views Contrast With the RBA

Week beginning 4 September 2017

- RBA on hold - how our views contrast with the RBA.

- RBA policy announcement, speeches RBA Governor and Deputy Governor.

- Australia: GDP and partials, current account, retail, trade balance, housing finance.

- NZ: building work.

- China: CPI, PPI.

- Eur: ECB policy decision, final GDP, retail sales.

- US: Labor day, factory orders, numerous Fed speeches.

- Key economic & financial forecasts.

Information contained in this report was current as at 1 September 2017.

RBA on hold - how our views contrast with the RBA

The Reserve Bank Board next meets on September 5. The Board is certain to keep rates on hold. It is interesting to recall the key aspects of the Governor's Statement following the last meeting on August 2:

- The RBA expects growth to be "around 3%" - in fact updated forecasts released three days later showed the Bank had retained its May forecasts of 3.25% in 2018 and 3.5% in 2019 (comfortably above trend of 2.75%).

- A pick-up in non-mining investment and wages growth is expected for 2018 and 2019.

- The Bank expects the unemployment rate to decline a little over the next couple of years.

- The higher exchange rate, and any further appreciation, is expected to contribute to reduced price pressures and a slower pick-up in activity. Note that despite those comments, there was no change in the Bank's growth forecasts between May (AUD at USD 0.74) and August (AUD at USD 0.79). The AUD has remained in the USD 0.79-0.80 range since the last meeting.

- Growth in housing debt has been outpacing the slow growth in household incomes (an indirect reference to concerns around house prices).

The key themes around growth; investment; wages and inflation contrast with our own views.

This week, Westpac sponsored the 'Breakfast with the Economists' series with events in Sydney (1000 guests) and Melbourne (400 guests) featuring Paul Sheard (Chief Economist for Standard and Poor's); myself; and several other economists in panel sessions.

I set out my opening remarks below:

Westpac expects the Australian economy to slow down in 2018 - to around a 2.5% growth rate in both 2018 and 2019, down from 2.8-3.0% in 2017.

This contrasts with 'official' forecasts from the RBA for 3.25% growth in 2018 (0.5% above trend) and 3.5% in 2019.

So where do we differ from the 'official' view?

Firstly, we expect the residential construction cycle will turn down from the second half of 2017 - high rise building approvals (around 50% of dwellings currently under construction) are already down 40% from their peak while detached approvals have only just started to recover from a soft patch this year.

Looking further out, it appears clear to us that the stresses around foreign investors and developers will further exacerbate the high rise construction cycle.

These investors and developers have been squeezed by tightening direct controls in China; higher state based stamp duties for foreign investors and other Government charges at both federal and state level; and reduced access to domestic funding.

Fortunately, there will be some offset to the housing construction downturn from stronger non-residential investment in offices and social building while state infrastructure investment, particularly in NSW, will also be a positive.

The second drag on growth should come from slower consumer related activity - wages growth is set to remain flat; spending associated with residential construction will slow; the wealth/ confidence effects resulting from rising house prices will dissipate; and heightened risk aversion will weigh on the consumer.

House price inflation will largely disappear over the course of 2018 as stretched affordability combines with tightening financial conditions (expect ongoing scrutiny from regulators with further 'macro prudential' policy tightening likely); and large increases in supply which will weigh on high rise markets, especially in Brisbane and Melbourne.

The unexpected recent strength in the AUD is already boosting services imports as more Australians look overseas for their holidays. The surge in foreign student enrolments in recent years may also ease.

Business investment is unlikely to lift much. A cautious consumer is one challenge. There is also likely to be intensifying political uncertainty which will see businesses quite reluctant to take risks in 2018 and 2019 until the next election is settled.

The job growth 'catch-up' we are currently seeing in Australia is also likely to reverse next year. The big job drivers in the economy - housing; consumer related spending; and services exports - will all be slowing.

We expect the unemployment rate, which is likely to settle around 5.5% in 2017, to move back towards 6% in 2018.

World growth and trade have surprised to the upside in 2017. Again, next year is likely to be a different story as China further tightens credit conditions and its economic growth slows from 6.7% in 2017 to 6.2% in 2018.

As President Xi consolidates his power at the upcoming National Congress (five of the seven Politburo Standing Committee members are expected to retire) he should cautiously resume a reform agenda. However, he is likely to continue to 'tread lightly' given no particular tight deadline. China's debt issues are over-hyped by many global investors. Although corporate debt is around 170% of GDP, much of it is between Government banks and State owned Enterprise (i.e. government to government). Rebalancing this debt is a challenge for fiscal policy, but the cost is highly unlikely to be borne broadly by the private sector (either corporate or household).

The spillover effect of a slowing China will be sufficient to slow growth in our trading partners despite the US maintaining an above trend 2% pace in 2018.

That growth scenario will have clear implications for markets. The Reserve Bank will remain on hold next year, despite confident market pricing for the normalisation process to begin.

On the other hand, as financial conditions in the US have eased, and the FED becomes more flexible with its inflation target, the FED is likely to continue along its tightening path with three more hikes expected by end 2018.

At that point, the Australian cash rate (1.50%) will have fallen below the Federal funds rate (1.875%) and that unusual inversion will weigh on the AUD.

Confidence in the US dollar is also likely to be partially restored as the political turmoil seen this year eases and the administration surprises with tax reform; infrastructure investment; and a more liberal attitude to regulation across a range of industries.

As with last year, our forecasts are significantly out of line with market views but, as with last year, we are confident that markets will eventually move in the direction of these expectations.

Bill Evans, Chief Economist

Data wrap

Aus Jul dwelling approvals

- Dwelling approvals dipped 1.7% in July, the pull-back from June's 11.7% jump much milder than expected (market forecast was -5%, Westpac -4%). Approvals are down 13.9% vs their high a year ago but over recent months have shown signs of stabilisation for high rise and firming across non high rise segments.

- The detail showed a flat month for private detached house approvals, the segment holding in a firm uptrend. Private unit approvals declined 6.7% but were coming off a 21% jump in June, the July read still 13% above the May level. The more granular detail points to a further small rise in high rise approvals (about 4%) which had been a big driver of the June gain (up about 15%mth). 'Low rise' or medium density dwelling approvals showed a more material reversal (down about 9% vs a 22% rise in June).

- Combined, non high rise approvals look to have pulled back about 3% from an 8.7% gain in June. This is broadly consistent with construction-related finance approvals which have shown a clear firming in recent months.

- By state, the lift in high rise approvals through June-July centred on NSW with this segment down across other states on a combined basis for the month. While volatility makes it hard to be definitive and its unclear whether the June-July lift in NSW will sustain, the broad picture across the major states still looks to be of high rise approvals levelling out after a sharp fall late last year and in early 2017.

- The state breakdown of non high rise approvals is more constructive with a clear firming trend in Vic, a more uneven pick up in NSW and Qld and stabilisation in WA.

- The value of renovation approvals declined 5.3% in July but was coming off a solid gain through May-June with a firm uptrend still intact (running at +1.8%mth, +5.1%yr).

- The value of non residential building approvals rose 2.4% in July but was also coming off a sold run in previous months with trend growth now a robust 3.1%mth, 14%yr. The lift is being driven by a surge in private sector office approvals which hit a new post-GFC monthly high in July. Recent gains in this segment have ben spread across both NSW and Vic.

- While a high-rise driven slowdown in dwelling activity remains assured near term, there are two key questions heading into 2018: 1) whether high rise takes another leg lower; and 2) whether the upturn apparent in non high rise segments in recent months continues. The risks to the first question look stacked to the downside particularly in the wake of the recent moves by Chinese authorities to curtail offshore investment by Chinese businesses. The second question remains more open - our prior is that a slowdown in the wider housing market and weak buyer sentiment will eventually see the recent rally fade. However, there are some positives relating to state government approval policies and perhaps some buyer and developer preference for lower density projects.

Aus Q2 construction work

- Construction work, having trended lower in recent years, associated with the deflating of the mining investment boom, spiked in the June quarter.

- In the June quarter 2017, construction work jumped 9.3%, a rise of $4.4bn, or 1.1% of GDP. That was well in excess of expectations (market median 1.0% and Westpac 1.0%).

- In the commentary associated with the release, the statistician was silent on this issue.

- We suspect that the spike is entirely due to the importation of a floating LNG platform, Prelude, which set sail for WA from a South Korean shipyard on June 28. The survey reports that private infrastructure work jumped 32.2% in the quarter, +$4.0bn and that construction work in WA leapt 55.6%, $4.1bn.

- This should have no net impact on GDP, with the rise in investment offset by a rise in imports.

- We had expected the ABS to amortise the value of the platform, spreading it over the time that it was constructed. This would see a relatively smooth rise in investment and in imports. This has been the approach in recent years and avoids these spikes - the approach taken back in the 1990s by the ABS.

- We are mindful that the import data, as reported in the monthly trade release, did not show a spike in June - hence our surprise today. We are now inclined to expect the ABS to revise the import data with the release of the Balance of Payments on Tuesday September 5, a day ahead of the National Accounts.

- In other detail, the standout is the upswing in public works, which is a notable growth engine as governments commit to new projects, particularly in transport. Public construction work grew by a further 4.7% in the quarter. Growth has been sustained at a brisk double digit pace, with the annual pace currently of 13.7% matching the 13.6% of a year ago.

- Private new home building activity may already be at a peak. Activity fell by 2.7% in Q1, revised up from -4.6%, with work disrupted by wet weather and flooding in NSW and Qld. In Q2, work declined by a further 0.8%. Over the past year, activity declined by 4%, with falls in this period reported for Victory, Qld and WA.

- Private renovation work managed a partial rebound, up 2.6%, after a 5.7% decline in Q1, to be 0.8% below a year ago.

- Private commercial building work consolidated in the quarter, inching 0.2% lower to be 1% below the level of a year ago. Going forward, work is set to advance, as indicated by the lift in approvals, with strength concentrated in Victoria and NSW, the two states experiencing above average population growth.

Aus Q2 private capex

- The latest ABS survey of private business CAPEX provided an update on actual spending for the June quarter 2017 and the 3rd estimate of plans for 2017/18, as well as the 7th and actual estimate of capex for 2016/17. The survey was conducted during July and August.

- The mining investment downturn has dominated total capex spending in recent years, a well as shaping the outlook. Recently, spending has consolidated has the mining downturn wanes and as spending by the non-mining sectors moves modestly higher.

- In the June quarter, total capex spending increased by 0.8%, exceeding expectations (mkt median 0.2% and Westpac -0.8%).

- The 0.8% gain follows a 0.9% rise in the March quarter and a decline of only 1.1% in the final quarter of 2017. Over the past year, capex declined by 3.0%, moderating from a 17% fall over the previous year.

- Capex by industry for Q2 was: services, +2.8%qtr, +3.7%yr; manufacturing, +1.4%qtr, +6.8%yr; and mining, -2.8%qtr, -15.2%yr.

- Equipment spending advanced by 2.7% in the quarter, exceeding expectations (Westpac f/c +0.6%). A lift in spending was reported across each of the three broad industry groups.

- Building & structures edged lower, -0.6%, again above expectations (Westpac f/c -1.8%). A further decline for the mining sector was largely offset by a modest rise across nonmining.

- Capex plans for 2017/18 have been upgraded, centred on services and commercial building.

- Estimate 3 for 2017/18 is $101.8bn, -3.6% vs Est 3 a year ago, a decline of $3.8bn. This is an improvement on the -6.4% for Est 2 on Est 2 reported three months earlier.

- Mining is the source of weakness for 2017/18, at -22%, -$9.2bn (unchanged from three months ago). Services was upgraded to +10% from +6%, so too manufacturing, to -2.6% from -12.4%.

- Calculations based on average realisation ratios (RRs) describe a similar picture. Est 3 implies a 3% fall in 2017/18, upgraded from -9% three months ago. By industry, results from average RR calculations are: mining -24%; services +9.5% vs +1.5% 3 months ago; and manufacturing -5%.

- Note, the capex survey has its limitations. The survey provides only partial coverage of total business investment, thereby overweighting the mining sector. Preliminary estimates (particularly Est 1 and Est 2) of capex plans are, by their nature, an inaccurate guide to the ultimate outcome - the extent of the error varies by asset, by industry and from year to year.

Aus Jul private credit

- Credit grew by 0.5% in July, matching the average for the June quarter and a step-up from the relatively soft 0.3% March quarter average as business emerges from a soft spot.

- Annual total credit growth is 5.3% currently, moderating from 6.0% a year earlier. Housing credit growth is 6.6%, unchanged from a year ago. Business credit grew by 4.2% over the past year, slowing from 6.3% a year earlier, reflecting some loss of appetite from both borrowers and lenders.

- Housing credit growth is likely to slow in response to the recent tightening of lending standards and out of cycle interest rate rises by commercial banks. As well, the boost from RBA rate cuts in May and August 2016 has faded. That said, more generous state government first home buyer initiatives, in effect from July, will provide a partial offset.

- There is tentative evidence that housing credit is beginning to slow. In July, housing credit expanded by 0.48%. This represents a step-down from a 0.55% average pace in the March quarter. It follows outcomes of 0.51% in April, a surprise 0.56% rise in May (most likely noise), and a 0.50% for June.

- On a quarterly basis, the tentative slowdown in housing credit is evident. The recent quarterly growth profile is: 6.1% annualised in Q2 2016; lifting to 6.4% in Q3; 6.6% in Q4; and 6.8% in 2017 Q1; then moderating to 6.5% in Q2; and printing at 5.9% annualised for the month of July 2017.

- The total value of housing finance having edged lower earlier this year appeared to have stabilised in June. While some month to month volatility is likely, we expect an emerging downtrend to be evident over coming months.

- As to investor housing credit, this grew by 0.41%mth in June and July, the softest monthly results since May 2016 - partly due to switching to the owner-occupier market. Annual growth for investors is 7.4% currently, while the 3 month annualised pace is 5.4%. For the owner-occupier segment, 3 month annualised credit growth has lifted to 6.9%, up from 5.5% at the start of the year.

- Turning to business, lending was volatile around a weaker trend over the past year or so. There was the dampening impact from heightened uncertainty around the July 2016 Federal election. This was followed by a burst of lending late in 2016 around infrastructure privatisation, contributing to a 1.1% jump in business credit in the month of December.

- In the business segment, over this period, there was an underlying loss of appetite from some borrowers (including deleveraging by the mining sector) and from some lenders (partly to reduce exposure to selected industries and to larger companies).

- More recently: the business mood has improved, mirroring global trends; commercial finance, while still volatile and not at a strong level, is off earlier lows; and business credit has advanced. Business credit increased by 0.5% in July, following gains of 0.4%, 0.3% and 0.8% for the three months April through to June.

- Business investment in the real economy by the non-mining sectors is advancing, but growth is currently relatively subdued, pointing to only modest growth in business credit.

New Zealand: Week ahead & Data Wrap

New Zealand is wrestling with a large and growing shortage of houses, with the shortfall centred squarely on Auckland. However, strong headwinds in the construction sector mean that building levels are likely to rise only gradually. This will challenge the strength of GDP growth over the coming year, and reinforces the case for the OCR staying on hold for an extended period.

Pressures in the Auckland housing market have continued to grow ...

Back in 2009, we highlighted the emerging pressures in the Auckland housing market, and forecast that this would result in a strong pick up in construction activity. Eight years on, that's exactly what we have seen. Residential construction has risen rapidly in recent years. That includes a sizeable lift in home building in Auckland.

But despite the lift in home building, pressures in the Auckland market haven't gone away. In fact, they've gotten worse. Auckland's population has risen by much more than expected, and home building has not kept pace. This has seen housing market tightness in Auckland rising to acute levels, reflected in a sharp increase in the average number of people per dwelling.

Looking ahead, Auckland's population is set to continue growing at a rapid pace, with around 290,000 more people expected to settle in the region over the coming decade. Coming on top of the existing tightness in the Auckland housing market, this signals the need for a significant number of new homes in the region.

... however growing headwinds mean that residential construction is set to increase only gradually …

Despite the growing need for new building in Auckland, headwinds in the construction sector mean that we're expecting only subdued growth in residential construction over the coming year. And recent developments indicate that growth in construction could be even softer than we're assuming.

Several factors are providing a brake on residential construction. First is that developers are encountering increasing difficulties accessing finance. This is particularly important in Auckland, given the greater prevalence of medium to high-density housing developments, for which finance can be a significant hurdle.

At the same time, capacity in the construction sector has become stretched following strong increases in building activity over the past few years. This has resulted in building costs rising at a rapid pace, with the cost of building a new home in Auckland up around 40% over the past five years alone.

Importantly, this rise in building costs has come at the same time as the housing market in Auckland has been softening. Existing homes prices in Auckland are down 4% since the start of this year, and sales are at their lowest level since 2011. Many developers will be nervous about building into a slowing market.

These headwinds have sapped the momentum in Auckland's construction sector, which showed through very clearly in this week's July dwelling consent numbers. Consent issuance in Auckland has fallen 8% over the past three months (though that does include a pullback in the volatile multiples consent category). Looking at the longer-term trend, annual dwelling consent numbers have essentially flatlined at just over 10,000 since the start of this year. And the most recent figures actually point to some softening in building activity over the coming months. Importantly, dwelling consents numbers have plateaued at levels that are still well short of what's needed to keep up with population growth. Consequently, it's likely that tightness in the Auckland housing market will get worse before it gets better.

… reinforcing the case for the OCR remaining low for an extended period

Our forecasts for subdued residential construction are a key point of difference between us and the Reserve Bank. The RBNZ's August policy assessment factored in continued strong increases in residential construction over the next few years. However, such increases look doubtful, especially with the slowdown in Auckland coming on top of the continued gradual wind-down of reconstruction work in Canterbury.

This subdued outlook for residential construction has important implications for economic conditions more generally. Construction activity was a key contributor to increases in GDP and employment in recent years, with spillovers to a number of associated industries. But with the momentum in the construction sector now waning, it's likely that we'll see more moderate GDP growth over the coming year. This will make it even harder for the RBNZ to generate the pick-up in domestic inflation that they have long pursued.

With the headwinds for growth increasing and a sustained pick-up in domestic inflation remaining elusive, the case for Official Cash Rate hikes in the near term looks thin. We expect that the OCR will remain on hold until late 2019. This is in contrast to financial markets pricing, which is consistent with OCR hikes from around September of next year.

Data previews

Aus Q2 profits

Sep 4, Last: 6.0%, WBC f/c: -4.0%

Mkt f/c: -4.0%, Range: -9.0% to 6.0%

- In the year to March 2017, company profits surged, jumping 40%, including a 6% rise in the quarter. The key was the rebound in commodities, up from the lows of late 2015, early 2016. Mining profits (36% of the total) more than doubled, +113%, over the period, while profits ex-mining rose 17%.

- However, in the June quarter, commodity prices stumbled and hence profits dipped. We anticipate the Business Indicators survey will report profits declined by 4%.

- Mining profits came off their highs in the quarter, with a potential double digit fall, a forecast -11.5%, associated with an 8% decline in global commodity prices.

- Non-mining profits were potentially constrained to only a small rise, a forecast +0.5%. Expanding sales were a plus in Q2 but margins remained under pressure, with a lack of pricing power at a time of rising costs.

Aus Q2 inventories

Sep 4, Last: 1.2%, WBC f/c: 0.2%

Mkt f/c: 0.3%, Range: -0.7% to 1.0%

- Inventories were a likely swing factor over the first half of 2017, centred on mining.

- In Q1, inventories rose 1.2%, +$1.8bn, the largest rise since March 2012, and added 0.4ppts to quarterly growth. There was a $1.0bn build-up on mining inventories as some rail links to the ports were closed due to flooding.

- In Q2, we expect total inventories to increase by only 0.2%, subtracting 0.4ppts from growth. The headline figure is constrained by a likely drawing down of mining inventories as rail links re-opened.

- Total inventories ex mining and ex manufacturing (where there is a structural decline) are forecast to rise by a strong 1.5% in Q2, matching the outcome for Q1. Firms across the non-mining economy are expanding inventories to meet rising sales.

Aus Q2 current account, AUDbn

Sep 5, Last: -3.1, WBC f/c: -9.0

Mkt f/c: -7.4, Range: -9.5 to -1.0

- Australia's current account deficit narrowed to only $3.3bn in Q1, 0.7% of GDP. That was the smallest deficit as a share of the economy since the end of 1979. The trade surplus was 2.1% of GDP, the largest since mid-1973.

- In Q2, the current account widened to a forecast $9.0bn as the trade position deteriorated on a dip in export prices as commodity prices eased.

- The trade balance was $3.3bn in Q2, a $5.9bn deterioration on Q1 (or, after revisions, a deterioration of $4.0bn). Export earnings declined by around 3%, dented by lower prices, while the import bill increased by around 2%. The terms of trade declined by an estimated 5%.

- The net income deficit is expected to hold around the Q1 level of $12.35bn, which represented a $5bn deterioration on six months earlier, as foreign investors in the mining sector enjoyed stronger returns.

Aus Q2 net exports, ppts cont'n

Sep 5, Last: -0.7, WBC f/c: 0.10

Mkt f/c: -0.05, Range: -0.60 to 0.10

- Net exports, like inventories, were a swing factor over the first half of 2017 - but moving in the opposite direction.

- In Q1, net exports subtracted a hefty 0.7ppts from growth as exports fell by 1.6% and imports increased by 1.6%, to meet rising demand. The key surprise was that resource exports slumped 4.6%, subtracting 2.5ppts of total exports, hit by bad weather and mechanical disruptions.

- In Q2, net exports are expected to be broadly neutral, at +0.1ppt.

- Export volumes rose an estimated 2.2%, with gains in iron ore, LNG, services and manufacturing outweighing a fall in coal. Coal shipments are set to rebound in Q3 with a return to more normal conditions.

- Import volumes advanced a further 1.9% we estimate, with broad based strength (excluding gold).

Aus Q2 public demand

Sep 5, Last: 0.5%, WBC f/c: 1.3%

- Public demand grew by an above trend pace in 2015 and 2016, 4.6% and 4.1%, respectively. This followed four years of weakness.

- An upswing in public investment is underway, lifting from recent lows, as governments commit to additional projects now that earlier fiscal pressures at the state level have receded.

- In Q1, public demand surprised to the down side, with a gain of only 0.5%, constrained by a dip in investment.

- In Q2, the upswing in public investment resumed. Overall public demand is expected to increase by 1.3% in the quarter, adding 0.3ppts to growth.

Aus RBA policy decision

Sep 5, Last: 1.50%, WBC f/c: 1.50%

Mkt f/c: 1.50%, Range: 1.50% to 1.50%

- The RBA is certain to leave rates unchanged again at its September meeting. The Bank has left the cash rate unchanged since August last year.

- Over the past year, economic growth has been patchy, core inflation is below the target band, there is significant slack in the labour market and wages growth is at historic lows.