Sample Category Title

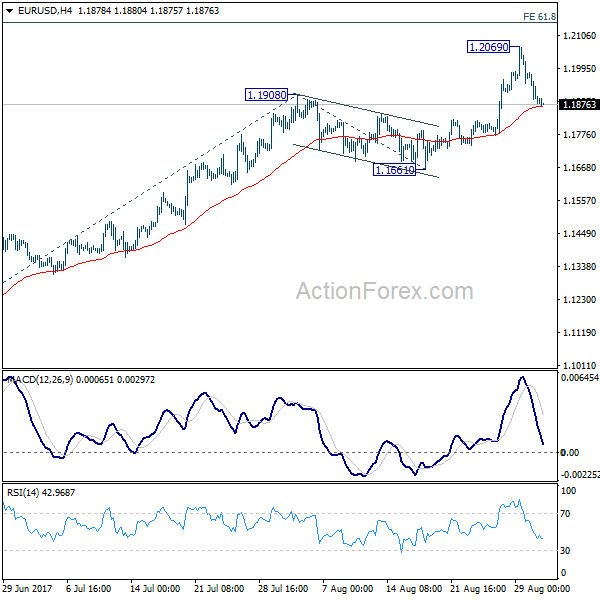

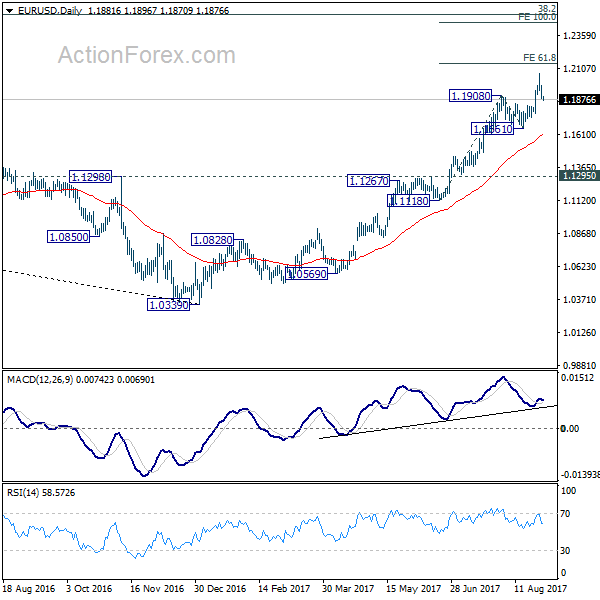

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1847; (P) 1.1915 (R1) 1.1950; More...

Intraday bias in EUR/USD remains neutral as the corrective pattern from 1.2069 is unfolding. While deeper fall cannot be ruled out, downside should be contained well above 1.1661 support to bring rise resumption. Above 1.2069 will extend the whole rally from 1.0339 to 61.8% projection of 1.1118 to 1.1908 from 1.1661 at 1.2149 first. Break there will target 100% projection at 1.2451 next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. For now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

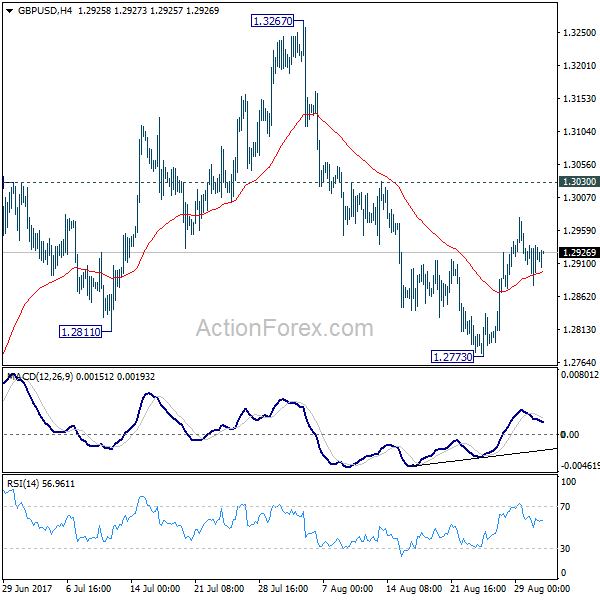

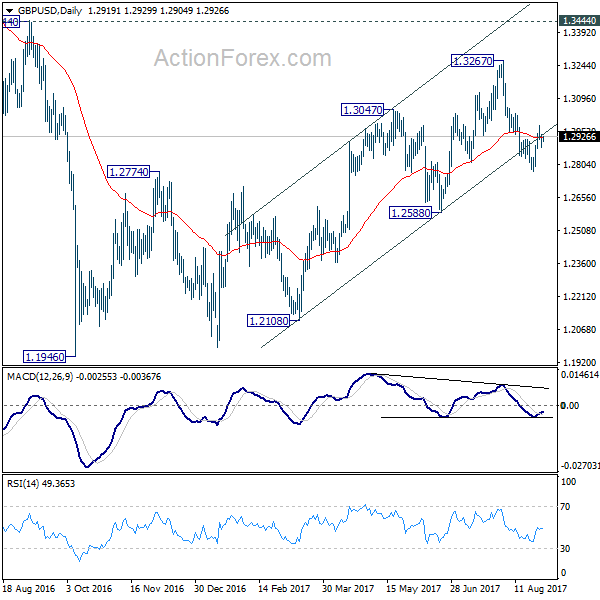

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2888; (P) 1.2912; (R1) 1.2947; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.2773 is unfolding. We're favoring the case that correction from 1.1946 is completed at 1.3267. Below 1.2773 will target 1.2588 key near term support first. Decisive break of 1.2588 will confirm our view and target a test on 1.1946 low. Though, break of 1.3030 will dampen this bearish view and turn bias back to the upside for retesting 1.3267.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

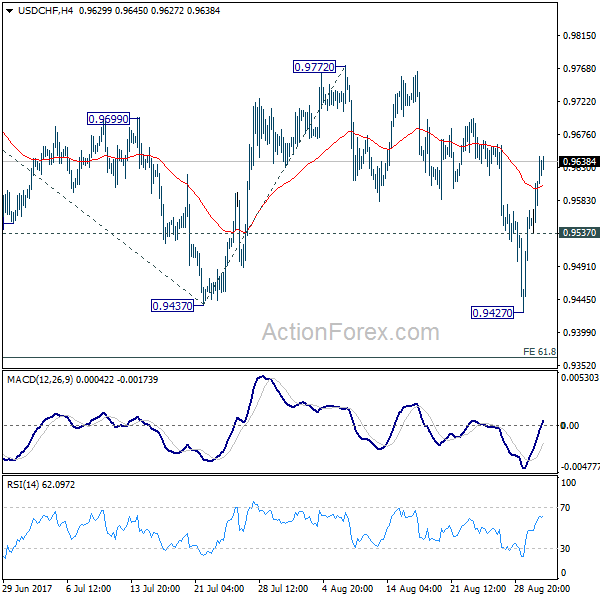

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9567; (P) 0.9606; (R1) 0.9674; More....

USD/CHF's rebound from 0.9427 is still in progress and further rise might be seen. The consolidation could extend longer considering that the pair is close to 0.9443 key support. Nonetheless, break of 0.9772 resistance is needed to confirm near term reversal. Otherwise, outlook stays bearish for another decline. Below 0.9537 minor support will turn bias back to the downside for retesting 0.9427 first. Break of 0.9427 will target 61.8% projection of 1.0099 to 0.9437 to 0.9772 at 0.9363.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.69; (P) 110.06; (R1) 110.59; More...

Intraday bias in USD/JPY stays neutral as it's bounded in range of 108.26/110.94. With 110.94 resistance intact, near term outlook stays mildly bearish and deeper decline is expected. Firm break of 108.12 support will resume the whole corrective decline from 118.65. In that case, USD/JPY will target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, considering bullish convergence condition in 4 hour MACD, break of 110.94 will indicate near term reversal and bring stronger rebound back towards 114.49 resistance.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Dollar Maintaining Data Inspired Gains, Yen Broadly Lower as Risk Aversion Eased

Dollar is trading firm is Asian session today and maintains overnight gains inspired by positive ADP and GDP data. That was accompanied mild strength in stocks, with DOW closed up 0.12%. 10 year yield also edged higher by gaining 0.007 to 2.143. Dollar index dived to as low as 91.62 yesterday but seems to be getting strong support fro 91.91/3 key level and rebounded. The key will lie in tomorrow's non-farm payroll report. As risk aversion eased, Yen is trading in red against all other major currencies for the week, except Canadian Dollar. Gold also pares back much of this week's gain and is back pressing 1300, after hitting as high as 1331.9 earlier in the week. The Loonie is weighed down by weakness in oil price which sees WTI dips to as low as 45.58.

Trump laid the onus on Congress for tax reform

US President Donald Trump finally made his first major speech on tax reform yesterday. Trump highlighted a few key targets including simpler tax codes, lowering tax burden on US businesses and cutting rates, cutting tax rates for the middles and bring back overseas parked cash. He painted the picture that lowering business tax rates will boost job growth and wages. However, there was practically no details on the plan. Additionally, there was no counter arguments to claims that his proposal would eventually help the wealthy the most. Instead, Trump laid the onus on Congress and said he's "fully committed to working with Congress to get this job done" and "I don't want to be disappointed by Congress".

EU Verhofstadt: Brexit transition can only be status quo

Guy Verhofstadt, European Parliament's Brexit coordinator, said that the negotiation won't have sufficient progress by October "if it goes very slow, as is the case at the moment". And he criticized that "if only one party around the table is putting a position and the other party is not responding then it is difficult to start a negotiation." At the same time, he also pointed out that "the more and more time we lose in the coming months, the more and more it is clear that the transition period can only be the prolongation of the existing situation, of the status quo."

UK Brexit Secretary David Davis called for being "flexible and imaginative" to resolve the negotiation deadlocks. But EU chief negotiator Michel Barnier expressed his frustrations on the topic. Barnier said that "to be flexible you need two points, our point and their point," and "we need to know their position and then I can be flexible." And Barnier insisted that the guidelines on the talks were designed for "serious and constructive negotiations" and urged "clear UK positions on all issues".

The third round of negotiation will conclude today. It seems there is still quite some distance to achieve significant progress for EU to give green lights to start the talks on trade agreements in October.

BoJ Masai: Economy is gaining momentum for 2% inflation

BoJ board member Takako Masai said that there is still "some distance" to achieve the 2% inflation target. However, she believed that "momentum towards achieving the target is strengthening." Steady rise in household income and tightening job markets will eventually boost domestic demand and push inflation up to target. BoJ has repeatedly pushed back the timing for hitting the 2% inflation target. And now, the central bank projected it will be achieved by March 2020. Masai said that the delay was "unfortunate" and emphasized that it's important to "pursue policy to lay the groundwork for achieving 2 percent inflation."

ANZ business confidence points to broad based economic expansion

New Zealand ANZ business confidence dropped to 18.3 in August, down from 19.4. That is, a net 18.3% of firms surveyed expect general business condition to improve over the coming year. ANZ bank chief economist Cameron Bagrie said that theses are "healthy readings for confidence, activity expectation, investment and employment across all sectors and regions". And, there is a broad-based economic expansion in operation".

RBNZ governor Graeme Wheeler said yesterday that "a lower New Zealand dollar is needed to increase tradables inflation and help deliver more balanced growth." And, "the appreciation in the exchange rate has been a headwind for the tradables sector and, by reducing already weak tradables inflation, made it more difficult to reach the Bank's inflation goals."

On the data front

China official PMI manufacturing rose to 51.7 in August, up from 51.4 and beat expectation of 51.3. Official PMI non-manufacturing dropped to 53.4, down from 54.5. Japan industrial production dropped -0.8% mom in July, versus expectation of -0.3% mom. Australia private capital expenditure rose 0.8% in Q2. New Zealand ANZ business confidence dropped to 18.3 in August, down from 19.4. UK Gfk consumer confidence rose to -10 in August.

Eurozone CPI is the key focus in European session. Eurozone will also release unemployment rate. Germany will release retail sales and unemployment. Later in the day, Canada will release GDP. US will release jobless claims, personal income and spending, Chicago PMI, pending home sales.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.69; (P) 110.06; (R1) 110.59; More...

Intraday bias in USD/JPY stays neutral as it's bounded in range of 108.26/110.94. With 110.94 resistance intact, near term outlook stays mildly bearish and deeper decline is expected. Firm break of 108.12 support will resume the whole corrective decline from 118.65. In that case, USD/JPY will target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, considering bullish convergence condition in 4 hour MACD, break of 110.94 will indicate near term reversal and bring stronger rebound back towards 114.49 resistance.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Aug | -10 | -13 | -12 | |

| 23:50 | JPY | Industrial Production M/M Jul P | -0.80% | -0.30% | 2.20% | |

| 1:00 | NZD | ANZ Business Confidence Aug | 18.3 | 19.4 | ||

| 1:00 | AUD | HIA New Home Sales M/M Jul | -6.90% | |||

| 1:00 | CNY | Manufacturing PMI Aug | 51.7 | 51.3 | 51.4 | |

| 1:00 | CNY | Non-manufacturing PMI Aug | 53.4 | 54.5 | ||

| 1:30 | AUD | Private Capital Expenditure Q2 | 0.80% | 0.20% | 0.30% | 0.90% |

| 5:00 | JPY | Housing Starts Y/Y Jul | -0.30% | 1.70% | ||

| 6:00 | EUR | German Retail Sales M/M Jul | -0.60% | 1.10% | ||

| 7:55 | EUR | German Unemployment Change Aug | -6K | -9K | ||

| 7:55 | EUR | German Unemployment Rate Aug | 5.70% | 5.70% | ||

| 9:00 | EUR | Eurozone Unemployment Rate Jul | 9.10% | 9.10% | ||

| 9:00 | EUR | Eurozone CPI Estimate Y/Y Aug | 1.40% | 1.30% | ||

| 9:00 | EUR | Eurozone CPI - Core Y/Y Aug A | 1.20% | 1.20% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Aug | -37.60% | |||

| 12:30 | CAD | GDP M/M Jun | 0.10% | 0.60% | ||

| 12:30 | USD | Initial Jobless Claims (AUG 26) | 237K | 234K | ||

| 12:30 | USD | Personal Income Jul | 0.30% | 0.00% | ||

| 12:30 | USD | Personal Spending Jul | 0.40% | 0.10% | ||

| 12:30 | USD | PCE Deflator M/M Jul | 0.10% | 0.00% | ||

| 12:30 | USD | PCE Deflator Y/Y Jul | 1.40% | 1.40% | ||

| 12:30 | USD | PCE Core M/M Jul | 0.10% | 0.10% | ||

| 12:30 | USD | PCE Core Y/Y Jul | 1.40% | 1.50% | ||

| 13:45 | USD | Chicago PMI Aug | 59.2 | 58.9 | ||

| 14:00 | USD | Pending Home Sales M/M Jul | 0.50% | 1.50% | ||

| 14:30 | USD | Natural Gas Storage | 43B |

Market Morning Briefing: Further Rise To 110.50 Has Been Seen In Dollar-Yen

STOCKS

Almost all major stocks are trading higher today except Shanghai.

Dow (21892.43, +0.12%) has moved up to test immediate resistance near 21950. We wait to see if the index faces any rejection from here which could push it back towards 21750. Else a break above 21950 could indicate an extension on the upside for the near term.

Dax (12002.47, +0.47%) bounced back slightly but does not look very strong just now. Downside possibility remains open towards 11900-11800 while below 12300.

Sharp recovery on the Dollar Index and Dollar Yen has aided to a pull back in Nikkei too. Nikkei (19647.97, +0.72%) has clearly bounced back above 19600 and could now head towards 19700-19800 levels in the coming sessions.

Shanghai (3347.55, -0.48%) has shown first signs of rejection from 3375 levels and could come off towards 3275 in the near term before again bouncing back. Near term looks bearish.

Nifty (9884.40, +0.90%) held below 9925 yesterday too and could trade within 9800-9950 region in the near term as mentioned in our earlier editions. Sideways consolidation within the mentioned range is possible for at least another 3-4 sessions.

COMMODITIES

Although Gold (1307) had responded to its highly overbought condition and moved lower in line with our expectation, but there will be no change in the immediate trading range of 1280-1350, with a pivot at 1300 levels. We will remain bullish on gold while it is trading above 1280 regions. There was no such movement in Silver (17.32) yesterday, but it could also move lower towards 16.90 levels to gather fresh buying momentum.

Copper (3.08) is trading within the narrow range of 3.00-3.12. Only above 3.12, higher resistances of 3.26 can come into consideration. The only concern in the short term overbought condition which may drag the price towards 3.00 levels. But we will remain bullish on copper while it is trading above 2.88 levels in the medium term time frame.

10th consecutive weeks of fall (-5.4M B) in U.S oil inventory but there was hardly any refection on the price action. Brent (50.65) moved lower towards its channel support of 49.83 along with WTI (45.93), which is still trading within the midterm bearish channel. Thus We will remain neutral on Brent and WTI, while they are trading below 52.80 and 49 levels on a weekly closing basis.

FOREX

Strong recovery in the Dollar Index (93.00) from the low of 91.62 seen on Tuesday, just above 91.39, the 50% retracement of the earlier rise from 78.91 (May 2014) to 103.82 (Jan 2017). If the momentum of the current bounce continues, we may see 93.40 and 94.00-94.30 on the upside, but we also note trend Resistance at 93.25.

Higher than expected US Q2 GDP preliminary data yesterday (+3.00% against expectation of +2.7%) has helped the Dollar recover and induced further profit-taking in the Euro (1.1877). We have to see whether the near-term Support at 1.18 (mentioned yesterday) holds or not. If not, then a further dip to 1.1750 can be seen.

Further rise to 110.50 has been seen in Dollar-Yen (110.52) yesterday, in line with reading. Immediate Resistance seen at 110.65 now and then series of Resistances available up to 111.35. So, maybe we may see a bit of a corrective dip towards 110.10-109.90. Note that the Resistance at 132.00-25 is holding well enough on Euro-Yen (131.28) and can trigger an intra-day dip to 130.80-60 before a fresh rise towards 132.25-50.

Despite the bounce from 1.2773 to 1.2978 this week, the Pound (1.2911) is not displaying much strength. Given the recovery in the Dollar now, it may range between 1.2825-2925 for a few days while trying to figure out longer term direction.

The 200-week MA at 0.80 on the Aussie (0.7909) mentioned yesterday has held well and pushed the Aussie down. We need to see if the mentioned Support at 0.79 holds and propels the Aussie higher towards 0.81. Failure to bounce from 0.7900, or max 0.7865, would be a blow to the currently preferred bullish possibility.

Small recovery in Dollar-Yuan (USDCNY = 6.5962) as well. Dollar-Rupee trades 64.04/07 on the NDF and is expected to continue to move sideways between 63.90-64.10 in the near term.

INTEREST RATES

The German-US 2 Yr Spread (-2.10%) has dropped but the German-US 10Yr Spread (-1.77%) is hovering around between -1.79-1.75 regions. yesterday, Euro had moved lower, seems to be responding more to the German-US 2Yr Spread in short term time frame. If the German-US 2Yr Spread could manage to rebound from its support at -2.09-10 levels then it could possible pull up the Euro too.

The benchmark US 10Yr yield has rebound from 2.09 levels due to the positive GDP figures and expected to remain stable at current levels of 2.14 for the rest of the week. But there are rooms for further downside towards 1.97 if the US 10Yr will close below 2.09% on a daily closing basis.

Muted price action has been seen in the Japanese 5Yr JGB (-0.14%) and the 30Yr JGB (+0.83%) as they are hovering around their respective supports, suggesting a possible bounce in near term time frame.

UK 5Yr and 30Yr Gilt Yields find support at 0.42 and 1.56 levels and moved up (5Yr 0.44% and 30Yr 1.59%) but the 10Yr is still trading at 1.00 regions with no sign of recovery.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a bearish momentum yesterday bottomed at 1.1880. The bearish pin bar on daily chart I showed you yesterday gave us a valid bearish signal. The bias is bearish in nearest term testing 1.1800 – 1.1770 region. Immediate resistance is seen around 1.1950. A clear break above that area could lead price to neutral zone in nearest term testing 1.2000. Overall I remain bullish but need a clear break above 1.2070 to end the current bearish correction phase and reactivate my bullish mode targeting 1.2175 or higher.

GBPUSD

The GBPUSD had another indecisive movement yesterday. There are no changes in my technical outlook. The bias remains neutral in nearest term. Price has been moving sideways between 1.2980 – 1.2870 range area since Monday and we need a clear break from that range area to see clearer direction. A clear break and daily close below 1.2870 would expose 1.2775/00 region. On the other hand, a clear break and daily close above 1.2980 would expose 1.3050 – 1.3100 region or higher. Overall I remain neutral.

USDJPY

The USDJPY had a bullish momentum yesterday, broke above 109.85 resistance and hit 110.54 earlier today in Asian session. The bullish pin bar on daily chart I showed you yesterday gave us a valid bullish signal. The bias is bullish in nearest term testing 111.00 region, which located around the daily EMA 200. Immediate support is seen around 109.85. A clear break back below that area could lead price to neutral zone in nearest term as direction would become unclear. Overall I am neutral in this pair.

USDCHF

The USDCHF had a bullish momentum yesterday topped at 0.9645. The bullish pin bar I showed you yesterday gave us a valid bullish signal. The bias remains bullish in nearest term testing 0.9700 – 0.9765 area. Immediate support is seen around 0.9580. A clear break and daily close back below that area could lead price to neutral zone in nearest term as direction would become unclear testing 0.9525 area but key support remains at 0.9450 region.

USD Thunders Back To Life

USD thunders back to life

The USD thundered back to life augmented by startlingly positive US GDP and labour market data. Also, investors were quick to put the recent North Korean flair up in the rear view mirror as haven assets lost their endearment and US equity markets rebounded.

Risk off flows are becoming an increasingly ephemeral event and are proving to be excellent opportunities for strapping on risk. The latest round of risk aversion was over in a heartbeat as investors continue to bank on amiable central bank policy as opposed to a militaristic escalation in North Korea

Also, the lack of fire and fury from President Trump and a more calculated While House response was viewed far more market friendly and quickly eased investor angst. All in all the markets regained their composure quickly.

Hurricane Harvey continues to leave a nasty footprint devastating Southeast Texas, and the Louisiana coastal communities while weighing negatively on crude demand from the heart of the U.S. petroleum refining industry. So while gasoline premium rises, WTI prices continue to fall as there are few venues available to pick up the processing slack.

But as significantly for currency traders, Harvey’s fallout has inspired a whole new level of debate regarding the debt ceiling showdown as to how the US government will meet federal assistance needs among the debt ceiling debate. But logic should dictate that to not approve a debt ceiling extension would prove to be political suicide for those in opposition given the humanitarian element of this recent natural disaster.

Euro

The ECB will certainly take some consolation the Euro assent reversed as an unexpectedly boisterous US GDP data has lit a fire under the USD dollar overnight. Also, the US ADP report had tongues wagging +237k (vs the +185k expected) – not surprisingly sending analysts scurrying to rethink their NFP headline. But the chance of an uptick in the wage growth component of NFP is what has traders buying the buck in the wake of back to back strong employment reading from both Tuesday’s surging US consumer confidence and last nights stellar ADP.

Japanese Yen

Dollar yen continues to move higher as the risk recovery had begun late in the US trading session on Tuesday rolled on overnight as Wall Street extended gains while haven assets were sold off. However not to completely sugar coat recent events, traders remain dispassionate with the UN resolution on North Korea but with risk rebounding and robust US economic data leading the charge, the current move higher could have some more room to play out.

Australian Dollar

The Australian dollar retreated, giving up earlier gains against the greenback after building approvals fell less than expected in July as the resurgent Greenback takes centre stage after a forecast-beating US GDP print. However with risk sentiment surging the Aussie is unlikely to run too far south from current base levels

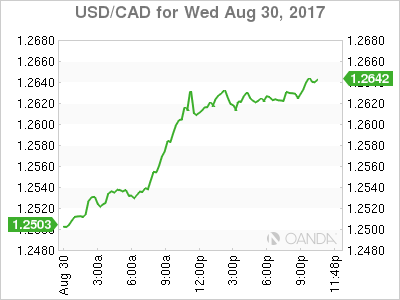

USD/CAD Canadian Dollar Lower After US GDP Improvement And Tax Reform Talk

The Canadian dollar depreciated on Wednesday after the private payroll processor ADP posted a 237,000 monthly job gains in the US. The positive news for the US dollar would keep coming in with an improvement on the quarterly GDP estimate now at 3.0 percent after the first forecast of 2.6 percent delivered last month. President Donald Trump made a big push for tax reform earlier today in Missouri but was short on details while putting the onus on making the reform a reality on congress. Tax reform was one of the early supporters of the dollar rally after the November US presidential election results, but it now faces a different political landscape than when Trump first announced it.

A rise in imports to Canada drop the current account deficit higher in the second quarter but it did so at a lower pace than forecasted and the first quarter data was also revised to show a lower deficit than originally reported. Tomorrow's release of monthly GDP will be the highlight on the CAD economic calendar with Canadian production expected to have slowed down to 0.1 percent.

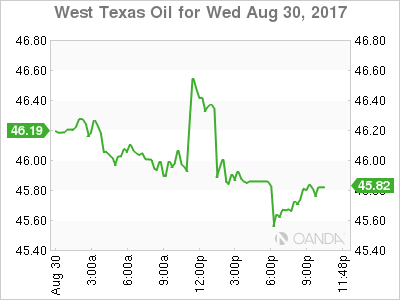

US refineries continue to shut operations in the aftermath of Hurricane Harvey. The storm has taken offline almost 24 percent of refiners with a week or more until they can restart work. West Texas Intermediate is down as there is a supply glut of crude while gasoline prices have risen. Hurricane Harvey ended up closing more refineries than Katrina, which mostly affected platforms reducing the supply of crude. With a world awash in crude it is easier to replace than the capacity for refining those into distillates which explains the sudden rise of gasoline prices. Even the bigger than expected drawdown in last week's US crude inventory data did little to push prices higher.

The USD/CAD gained 0.794 percent on Wednesday. The currency pair is trading at 1.2621 near daily highs after a strong ADP private payrolls report has raised expectations of a strong U.S. non farm payrolls (NFP) on Friday. The two employment reports don't have a strong correlation as the NFP report is a more complete look at the jobs component. With the market's confidence in a third rate hike by the U.S. Federal Reserve this year slowing evaporating a strong showing in wage growth could boost the USD.

The main indicator release this week for CAD traders will be the monthly GDP data due on Thursday, August 31 at 8:30 am EDT. The Canadian GDP is expected to have slowed down after a strong first half of the year.

NAFTA negotiations will start on Friday with sources pointing out that Mexico has already started to work out a plan B if US President Donald Trump does indeed withdraw from the trade agreement. Canada has been active pushing trade talks with the United Kingdom, Europe and China but they are far from being active in time to be a reliable backup option to a world without NAFTA.

The price of West Texas Intermediate fell 0.845 percent in the last 24 hours. WTI is trading at 45.86 after Hurricane Harvey continues to reduce refinery capacity in Texas. Close to a quarter of refineries are now shut down due to flooding with a week or more before they can reopen.

US weekly inventories did little to stop the drop in crude prices. The Energy Information Administration (EIA) published today a 5.4 million drawdown that eclipsed the 1.9 million barrels that were forecasted. The report data comes just days before Hurricane Harvey hit, as it still shows 96.6 percent refining utilization, which has been the stat that has come down more after the storm.

Market events to watch this week:

Thursday, August 31

8:30 am CAD GDP m/m

8:30 am USD Unemployment Claims

9:45 pm CNY Caixin Manufacturing PMI

Friday, September 1

4:30 am GBP Manufacturing PMI

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

10:00 am USD ISM Manufacturing PMI

USD Extends Bounce On Data

Tentative signs of a turnaround turned into something more concrete Wednesday as the US dollar rally continued on strong data. The USD was the top performer while the Swiss franc lagged. USDX finally regains its 200-week MA, a triple bottom beckons, USD jobs around the corner and a potential Draghi jawboning is less than 10 days away. Seems like the perfect USD play. Ashraf's special-edition Premium video on how to play the USD stabilisation.

We wrote yesterday about the positive signs in the US dollar but worried that it hadn't come with any upper-tier data. That changed Wednesday on strong growth and jobs numbers. Q2 GDP was revised to 3.0% from 2.7% on strong corporate profits and consumer spending. The ADP employment report hit a 5-month high at 237K compared to 185K expected.

On the political front, speculation also mounted that relief funding from Hurricane Harvey will make it easier to raise the debt ceiling, at least for a short time. Trump also focused on corporate tax cuts in a speech in Missouri.

The moves in the dollar were substantial. After rising as high as 1.2070 a day ago, EUR/USD sank to 1.1881 and finished on the lows. The commodity currencies were also hit hard late in the day as AUD/USD fell a full cent from the highs in an outside reversal. USD/CAD was one of the reversals we highlighted yesterday and that pair posted its best day in four weeks, climbing 120 pips.

The loonie will stay in focus in the day ahead with Canada delivering the first report on Q2 GDP. Expectations are for a sparking 3.7% reading but the risks are to the downside after soft current account numbers Wednesday.

A full slate of data is up beforehand including the China official PMIs, Australian private sector credit, speeches from the BOJ's Masai and RBA's Harris. That's followed by German retail sales, French CPI, Eurozone CPI, a speech from the BoE's Sanders, the US PCE report and the Chicago PMI among others.

It's safe to say that the summer lull is over.