Sample Category Title

WTI Oil – Increased Demand on Holiday Season Lifts the Price Further

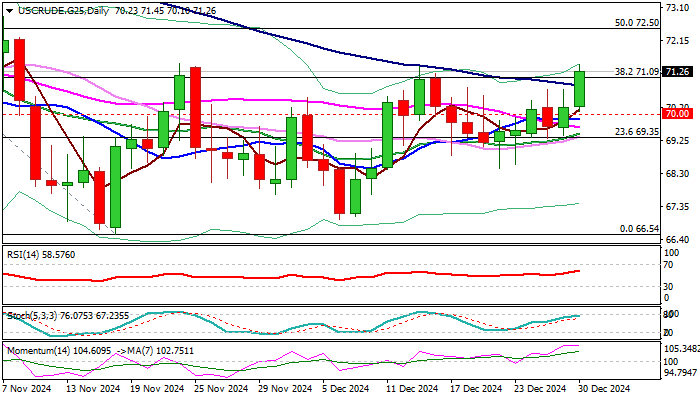

WTI oil price advanced around 1.3% in holiday-thinned trading on Monday, underpinned by increased fuel demand on holiday season that was reflected on stronger than expected drop in crude inventories.

Near-term picture is turning positive on improving daily technical studies (positive momentum / daily Tenkan/Kijun-sen in bullish setup) and signals attack at key barriers at $71.39/48 (peaks of recent range) after bulls broke above 100DMA ($70.84) and $71.09 (Fibo 38.2% of $78.45 / $66.54).

Sustained break of $71.39/48 to generate fresh bullish signal and open way for further gains, with targets at $72.50 and $72.85 (50% retracement / Nov 7 high) to come in focus.

However, larger picture is still negative, as oil price was down around 0.8% in 2024, with minimum impact from key factors – supply / demand and geopolitics.

Markets await releases of economic data from China (Tuesday) and the US (Friday) for fresh signals from two largest economies and oil consumers.

Focus will be also on anticipated action from new US administration after Donald Trump returns to the White House on Jan 20.

Res: 71.48; 72.00; 72.50; 72.85

Sup: 71.09; 70.84; 70.00; 69.64

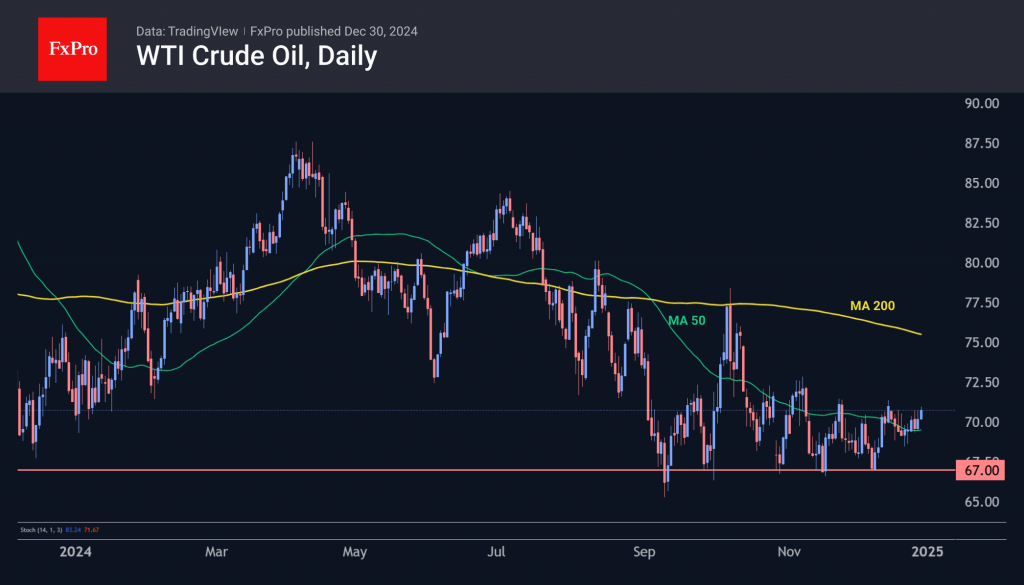

Oil: Forming the Bottom

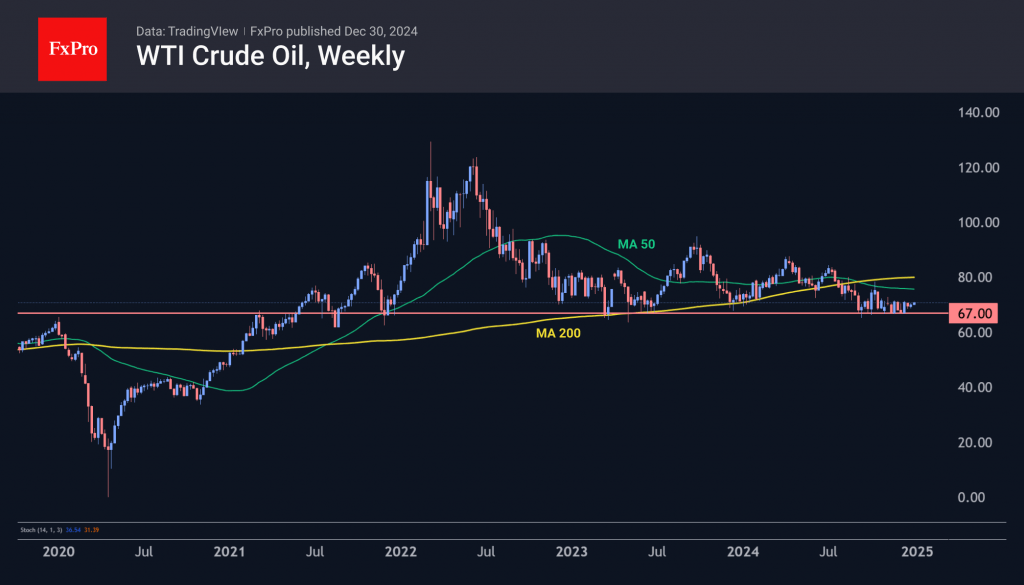

Energy is expected to regain the attention of market speculators next year due to both technical and fundamental factors.

WTI has repeatedly rallied on attempts to break below $67, which has been a turning point on dips since early 2023. A break below the 50- and 200-week moving averages was a bearish signal, but it has not fully materialised. Continued support leads us to consider the bottoming scenario followed by a global reversal.

Technically, oil could rally relatively easily to the $75 level, where it will begin to struggle with its 50-week and 200-day moving averages.

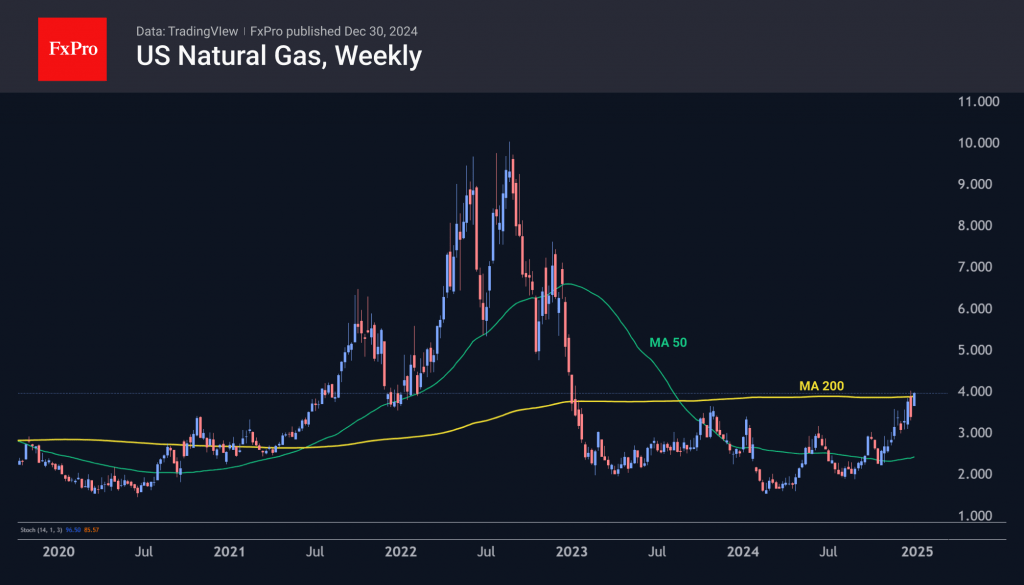

Natural gas, the closest substitute for oil, has rallied almost 90% from its early August lows and is approaching the highs of the past two years thanks to increased demand for US LNG amid Russian energy sanctions. Fears of a cold winter in Europe are also pushing gas higher, which is bullish for oil.

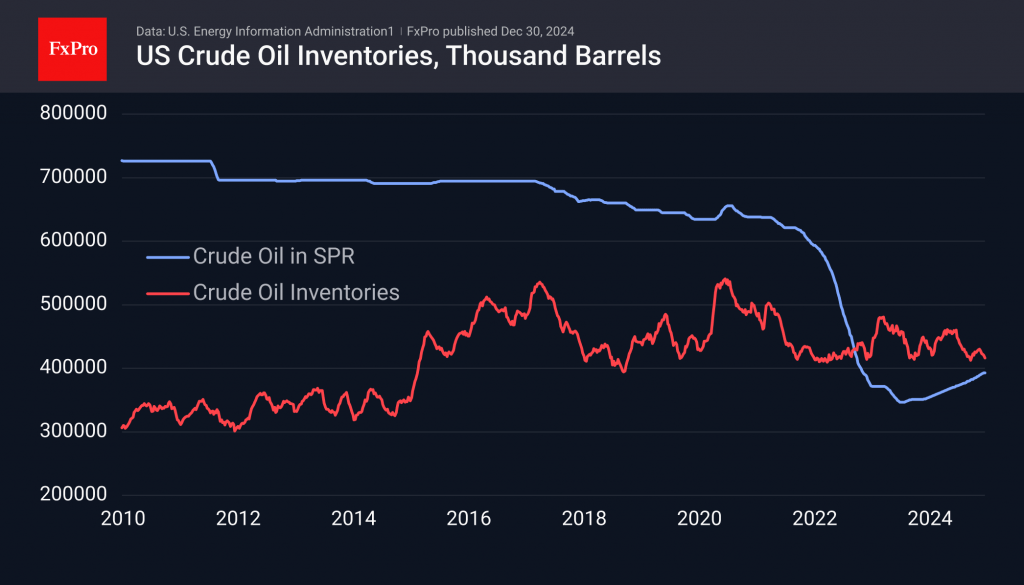

In industry news, we note the five-week decline in US commercial crude oil inventories. Stocks are now 4.5% lower than a year ago and remain near the lower end of the range over the past decade. The picture is complemented by a series of six-week declines in gas inventories, which have moved from the upper end of the range to the middle of the range.

An important factor is the dominance of the Republicans in US politics, among whom the oil industry lobby is strong. The agenda of US energy exports around the world and declining support for alternative energy sources should favour oil.

If our expectations are realised, oil could push off the bottom and start to rise. The easiest part of the rise is seen to be to the $75 level. If the rally continues, the next target will be the $80-86 area. The prospect of an end to the Russia-Ukraine conflict, however elusive, creates moderate downside risks. However, if this or China’s stimulus measures boost global growth, this will have a positive impact on the oil price, taking it to $100 within two years.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0404; (P) 1.0424; (R1) 1.0443; More...

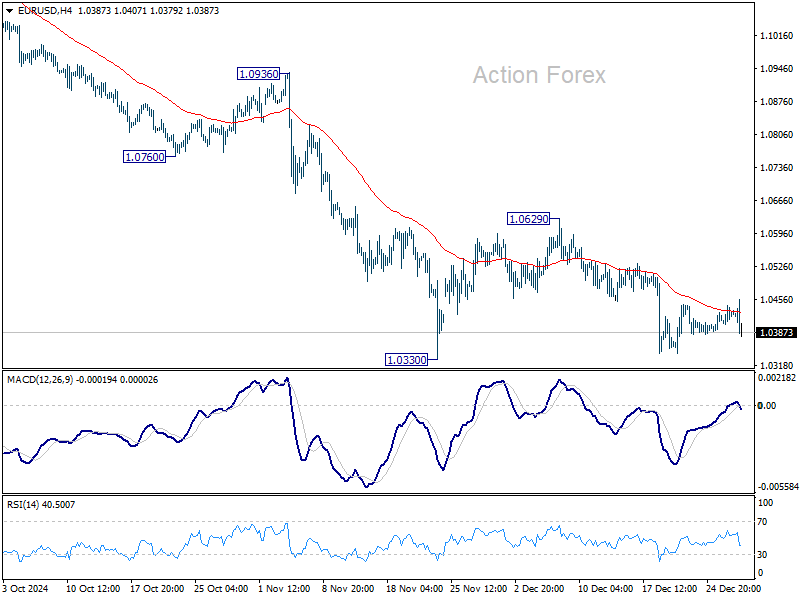

EUR/USD is still bounded in range trading and intraday bias stays neutral at this point. Stronger recovery cannot be ruled out, but outlook will remain bearish as long as 1.0629 resistance holds. Firm break of 1.0330 will confirm resumption of whole decline from 1.1213. Sustained trading below 1.0404 fibonacci level will carry larger bearish implications.

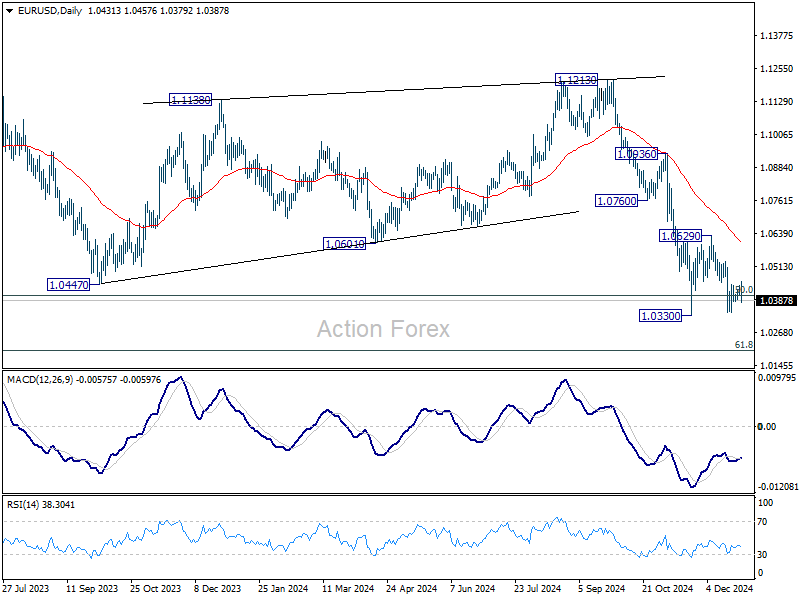

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

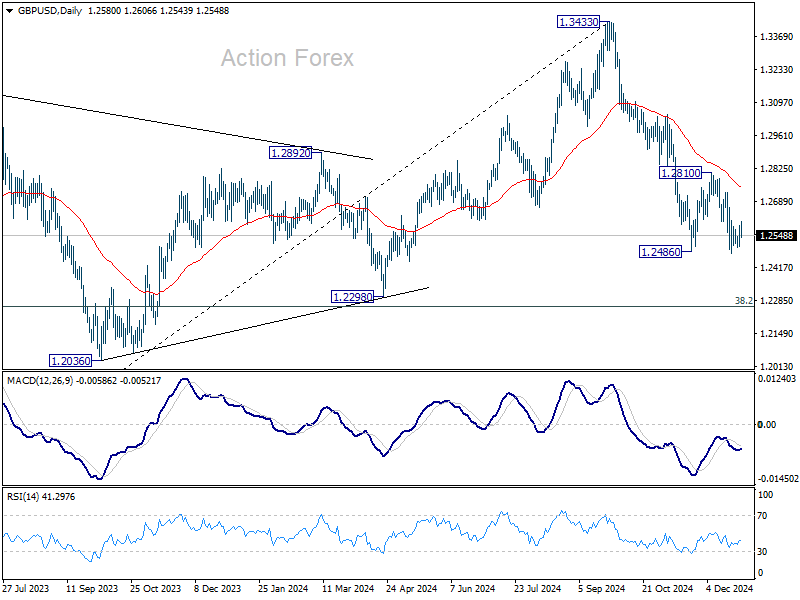

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2526; (P) 1.2559; (R1) 1.2614; More...

Range trading continues in GBP/USD and intraday bias stays neutral. While another recovery cannot be ruled out, outlook will stay bearish as long as 1.2810 resistance holds. On the downside, break of 1.2474 will resume the fall from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

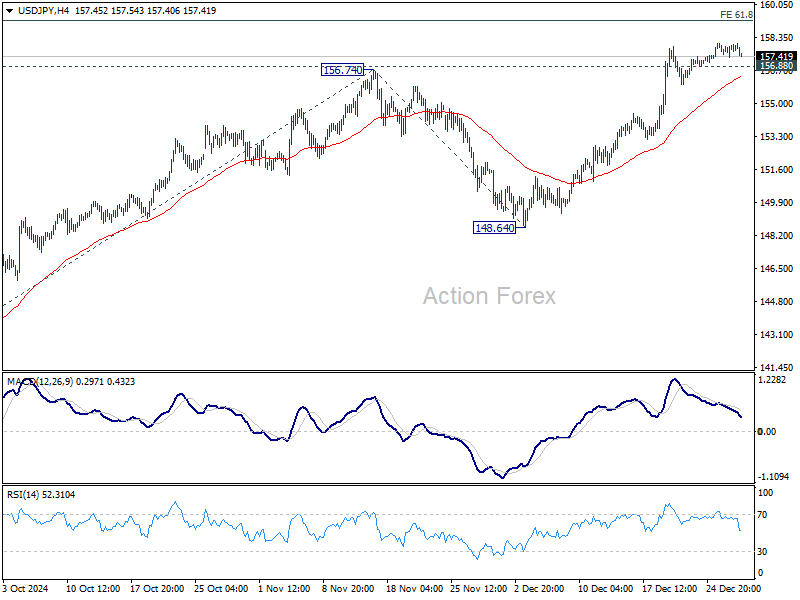

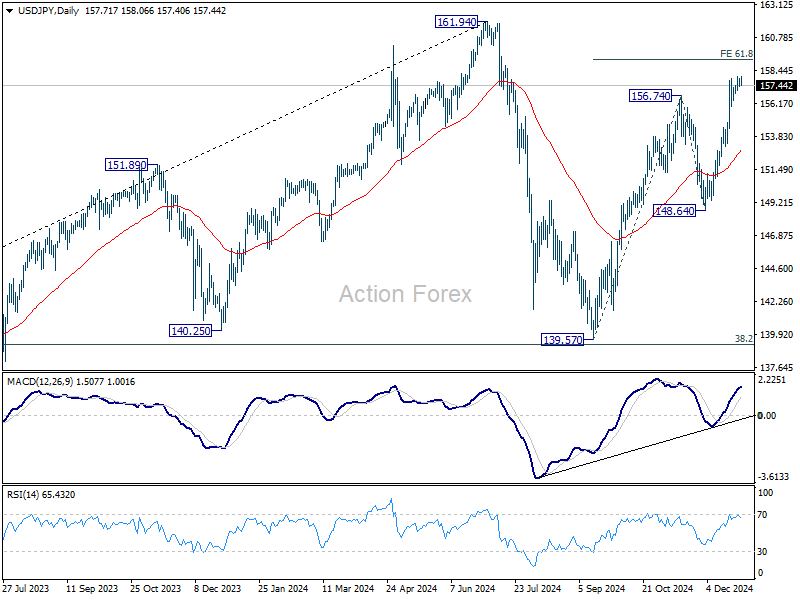

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.49; (P) 157.74; (R1) 158.14; More...

No change in USD/JPY's outlook and intraday bias stays mildly on the upside despite weak momentum. Current rise from 139.57 is still in progress for 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. Firm break there will pave the way back to 161.94 high. On the downside, though, below 156.88 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

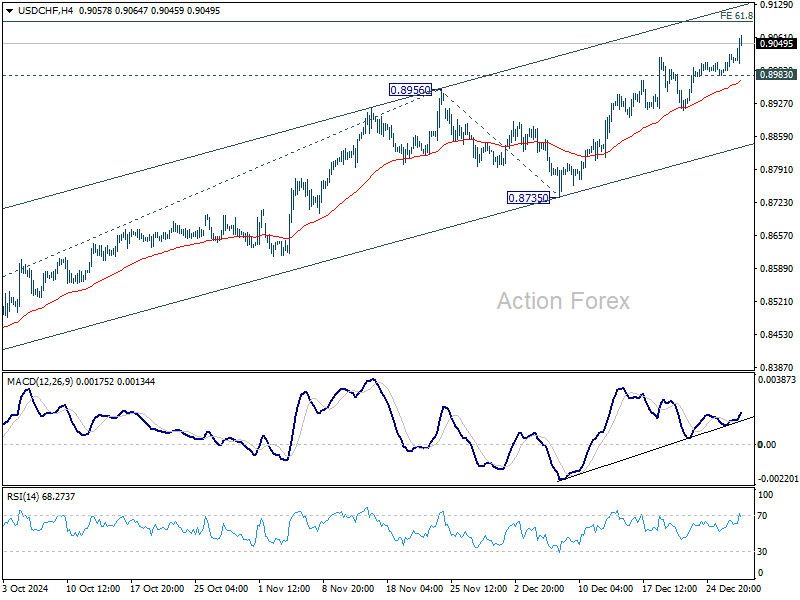

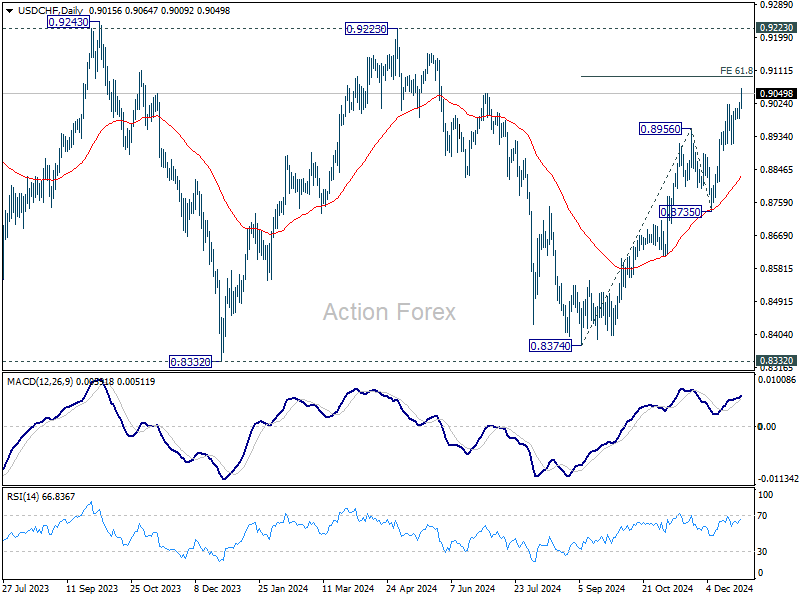

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8995; (P) 0.9011; (R1) 0.9038; More…

USD/CHF's rally continues today and intraday bias stays on the upside. Rise from 0.8374 is in progress for 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095. On the downside, below 0.8983 minor support will turn bias neutral and bring consolidations again first.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

European Majors Dip in Holiday Calm, China’s PMIs Next

The forex markets remain subdued as traders maintain a cautious stance ahead of the New Year. European major are notably weaker, with Swiss Franc leading the declines. Euro is also under pressure, while Sterling has shown resilience, managing to avoid sharper losses.

Meanwhile, Yen has staged a modest recovery, supported by easing US and European benchmark yields, which have tempered earlier selloffs. Commodity currencies, including Australian Dollar, are firming slightly as they digest steep losses accumulated over December. Dollar is trading sideways, reflecting an overall lack of momentum as the markets consolidate in thin year-end trading.

Looking ahead, attention is on China’s NBS PMIs, scheduled for release during the upcoming Asian session. Expectations point to slight expansions in both the manufacturing and non-manufacturing sectors for December, which could provide insights into the state of China’s recovery efforts.

Adding to the focus, President Xi Jinping is set to deliver his New Year’s address later in the week. Markets will be keen to parse his remarks for any reaffirmation of commitments to revive China’s struggling economy.

China’s authorities have already pledged to issue CNY 3 trillion in special treasury bonds in 2025 to boost fiscal stimulus, although further details are unlikely until March’s National People’s Congress. Analysts remain cautious about the effectiveness of these measures, particularly given structural challenges such as sluggish household consumption and a soft real estate market.

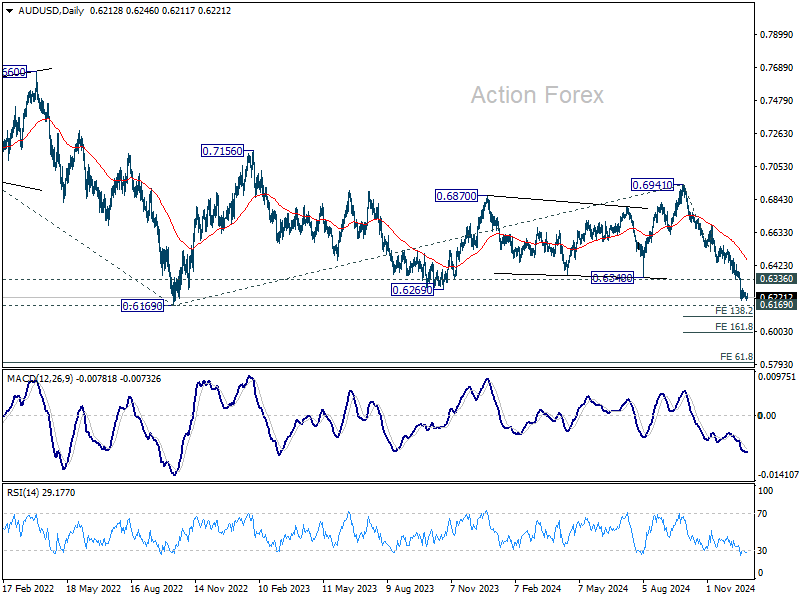

Aussie would be particularly sensitive to developments in China. While downside surprises in tomorrow’s Chinese PMI data could reignite selling pressure in AUD/USD, 0.6169 (2022 low) could continue to act as a critical support level. Yet any recovery might be capped below 0.6336 support turned resistance. The next big move would hinge on both the development surrounding China's outlook in 2025, as well as whether RBA would start easing sooner in February.

In Europe, at the time of writing, FTSE is down -0.51%. DAX is down -0.38%. CAC is down -0.41%. UK 10-year yield is down -0.024 at 4.616. Germany 10-year yield is down -0.021 at 2.377. Earlier in Asia, Nikkei fell -0.96%. Hong Kong HSI fell -0.24%. China Shanghai SSE rose 0.21%. Singapore rose 0.64%. Japan 10-year JGB yield fell -0.0106 to 1.094.

Swiss KOF falls below average, signals dampened outlook

Swiss KOF Economic Barometer fell to 99.5 in December, down from 102.9 in November and below market expectations of 101.1. This decline brings the indicator slightly below its medium-term average, signaling a "dampened" outlook for the Swiss economy .

KOF Economic Institute attributed the drop to weaker performance across multiple sectors. In particular, indicators for manufacturing, other services, the hospitality industry, foreign demand, and private consumption showed significant declines, collectively driving the overall decrease.

Japan's PMI manufacturing finalized at 49.6, nears stabilization and cost pressures persist

Japan's Manufacturing PMI for December was finalized at 49.6, an improvement from November's 49.0, indicating a gradual move toward stabilization in the sector.

According to Usamah Bhatti of S&P Global Market Intelligence, the data "painted a picture of a near-stabilization" in manufacturing conditions as declines in both production and new orders softened.

Encouraged by these improvements, firms increased hiring, partly to address existing labor shortages and in anticipation of future demand recovery.

However, price pressures remained elevated, with input costs rising at their fastest pace since August due to higher raw material and labor costs, compounded by Yen’s weakness. To manage these cost burdens, manufacturers passed on higher prices to clients, resulting in the strongest output charge increases in five months.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8995; (P) 0.9011; (R1) 0.9038; More…

USD/CHF's rally continues today and intraday bias stays on the upside. Rise from 0.8374 is in progress for 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095. On the downside, below 0.8983 minor support will turn bias neutral and bring consolidations again first.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

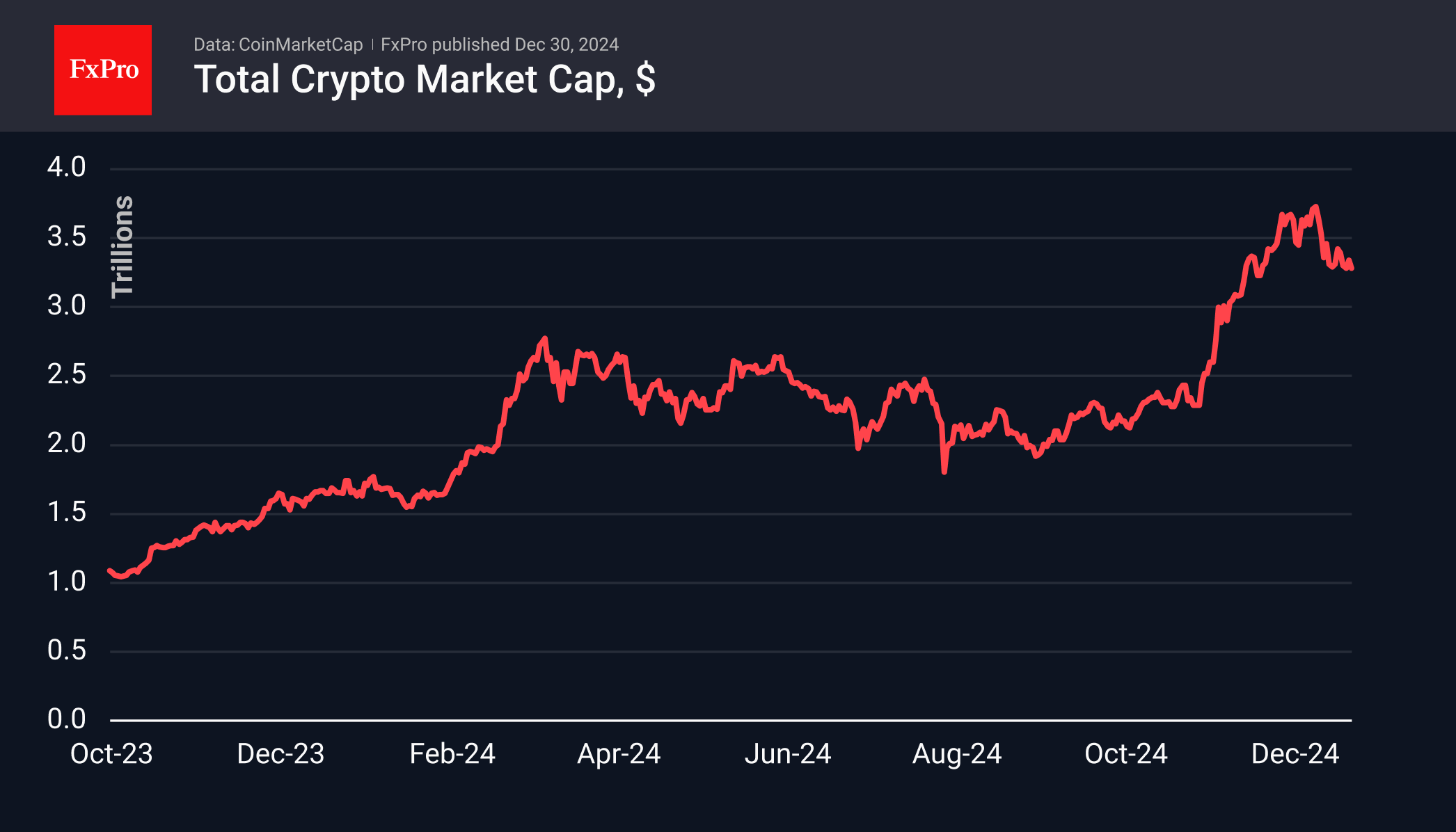

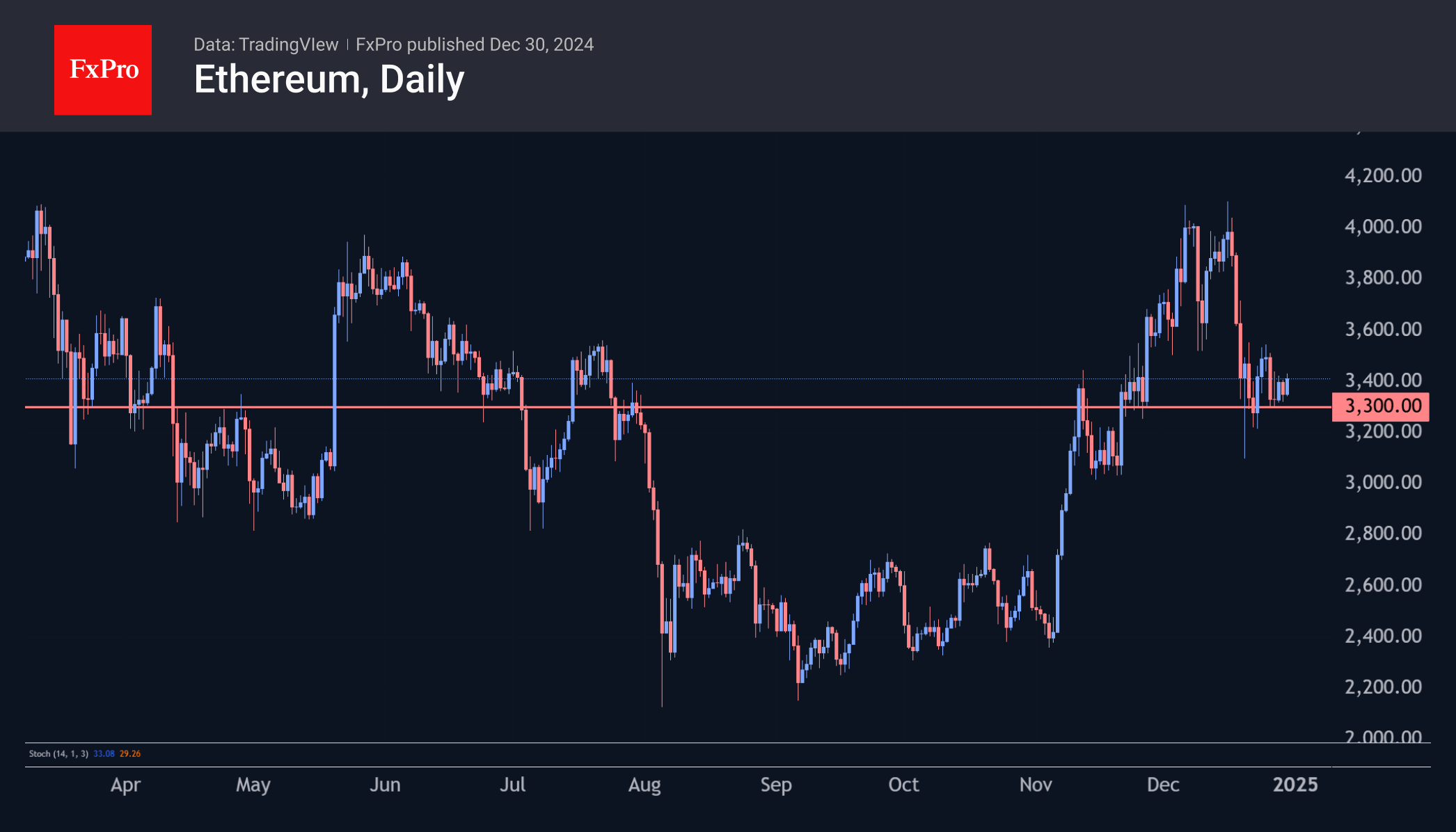

Crypto Market Teeters on the Brink of Correction

Market Picture

The cryptocurrency market has lost 1.4% in the last 24 hours, falling to $3.29 trillion. Over the past 10 days, the market has mostly stayed in the $3.3-3.4 trillion range, pulling back to late November levels where positions were also shaken out. Here is the classic 61.8% retracement level from the early November rally to the mid-December high.

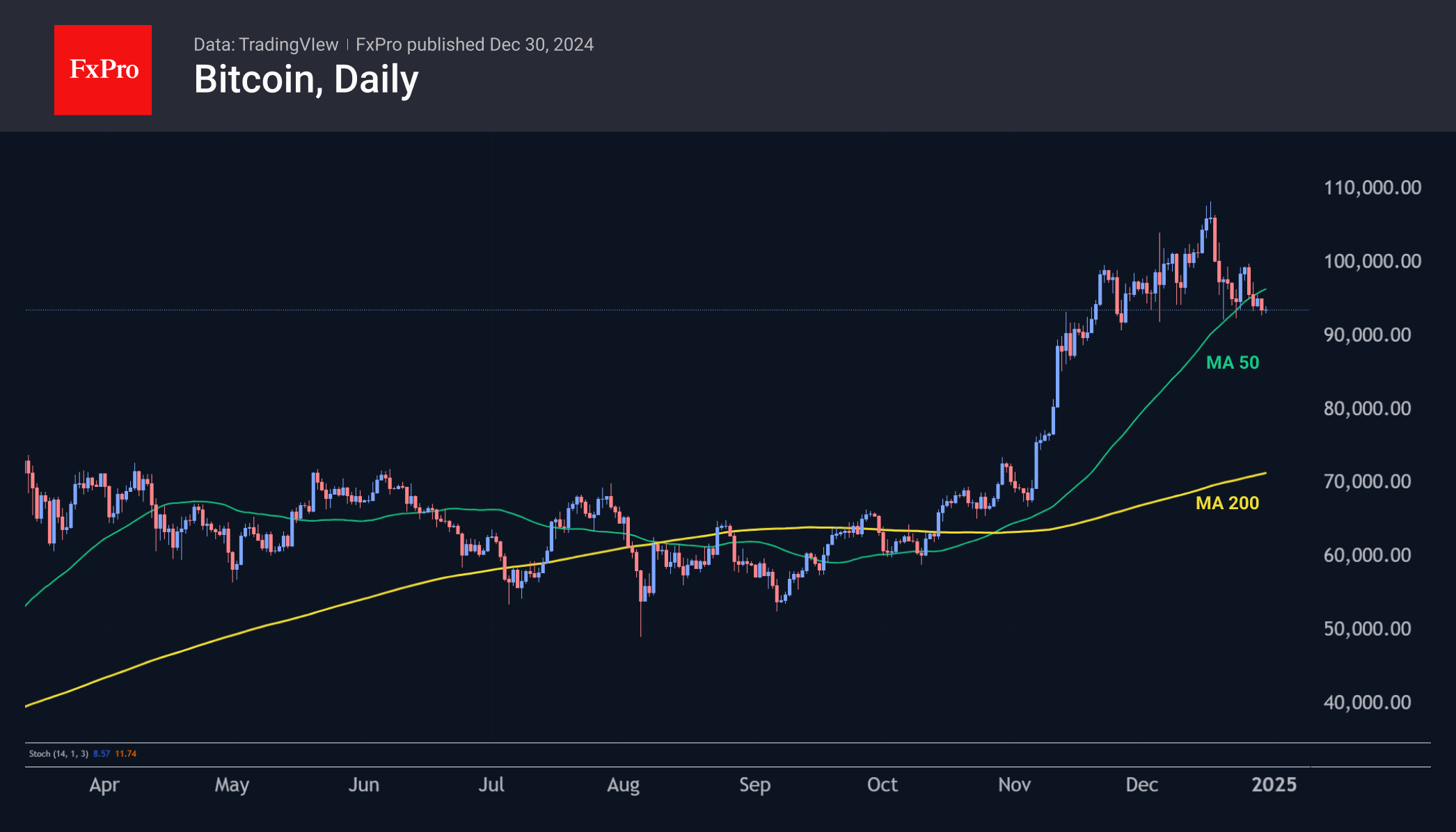

The price of Bitcoin pulled back to $93.5k, falling below the 50-day moving average after Christmas. Like the rest of the crypto market, bitcoin has returned to the 61.8% level. Bitcoin is on the verge of a technical pullback, and a failure below $93k would signal a break in the short-term trend, which could lead to a deeper decline that could erase all the gains made in November-December.

Among the top coins, Ethereum managed to swim against the tide, adding 0.6% for the day. The coin has been attracting buyers on the decline towards $3300 in recent days, forming an uptrend.

News Background

Net outflows in the BTC ETF for the week totalled $387.5 million, the highest since early September. The positive weekly trend was broken after three weeks of inflows. Cumulative inflows since the launch of bitcoin ETFs in January fell to $35.66 billion (-1.1% for the week).

Net inflows into ETH ETFs rose to $349.2 million for the week. The positive weekly trend continued for the fifth consecutive week. Cumulative net inflows from ETF launches in July rose to $2.68 billion (+15% for the week).

Strive Asset Management has filed to launch a bond ETF for bitcoin strategy companies such as MicroStrategy. The firm was founded by Vivek Ramaswamy, who will be working with Elon Musk at DOGE under the Trump administration.

CryptoQuant CEO Ki Young Ju said that the bearish trend in the bitcoin market has not yet formed, and the price is far from its peak. In his opinion, BTC will soon rise by more than 30%.

Bitcoin selling pressure and increased volatility may intensify in the coming days, believes a CryptoQuant contributor nicknamed IT Tech. He noted an increase in bitcoin reserves of centralised exchanges – by about 20,000 BTC in recent days.

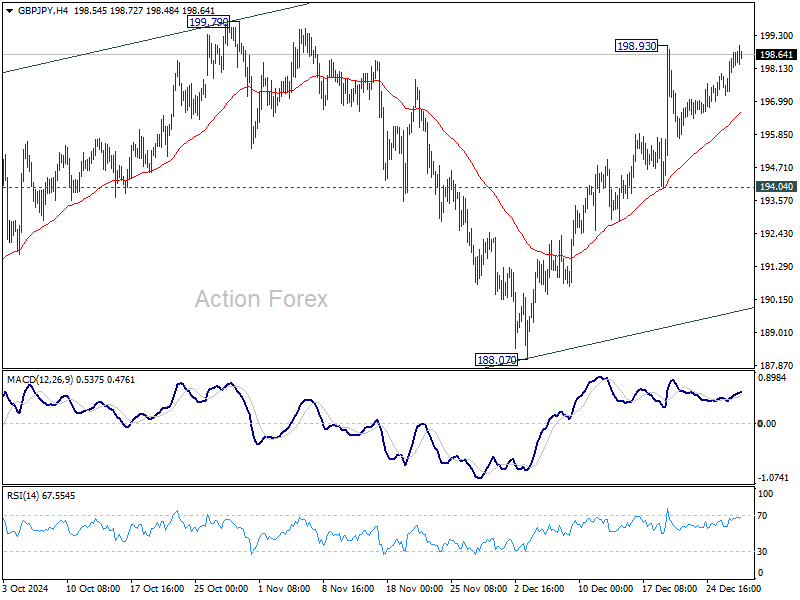

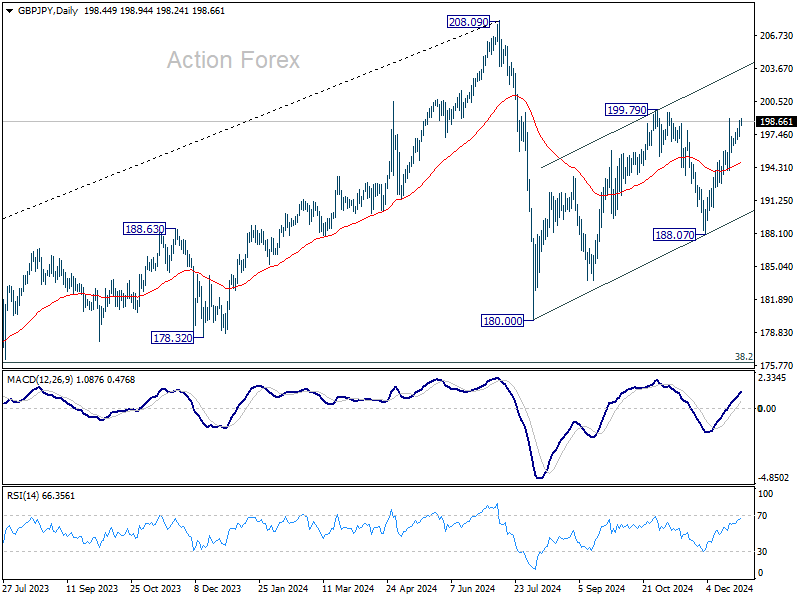

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.60; (P) 198.16; (R1) 199.10; More...

Intraday bias in GBP/JPY remains neutral and outlook is unchanged. As noted before, corrective pattern from 180.00 is extending with another rising leg. Further rise is expected as long as 194.04 support holds. On the upside, above 1999.79 will will target channel resistance (now at 203.63).

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

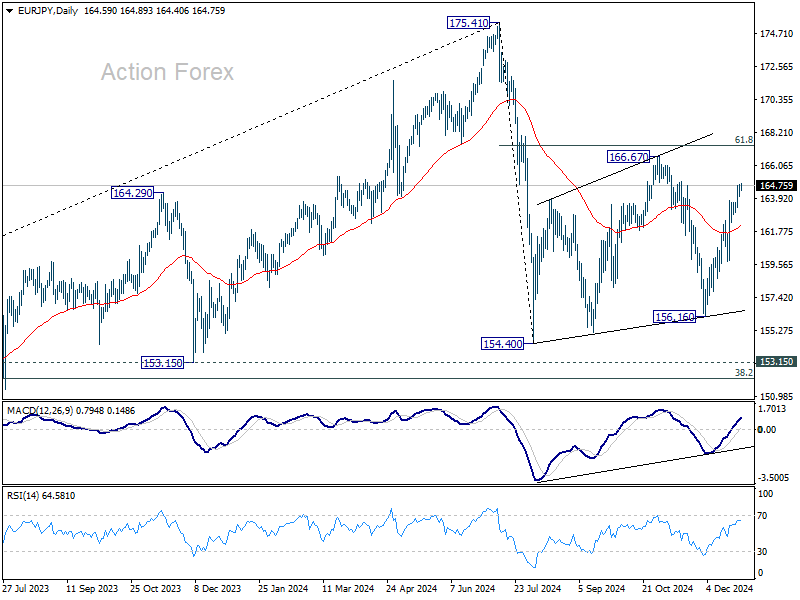

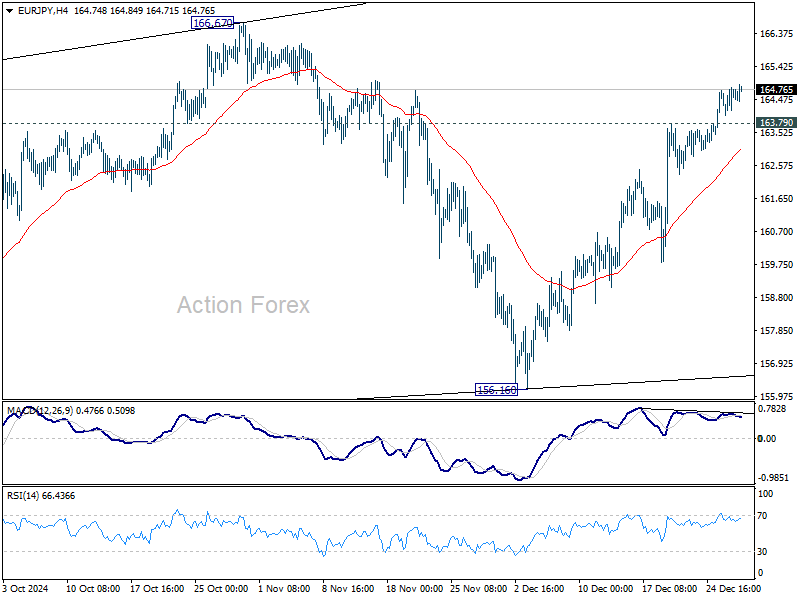

EUR/JPY Daily Outlook

Daily Pivots: (S1) 164.14; (P) 164.49; (R1) 164.94; More...

EUR/JPY's rally from 156.16 is still in progress and intraday bias stays on the upside. Corrective pattern from 154.04 is extending with another rising leg. Further rise should be seen to 166.67 resistance next. On the downside, below 163.79 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.