Sample Category Title

Signs of a USDCAD Reversal

The Canadian dollar may be consolidating a corrective pullback from multi-year highs.

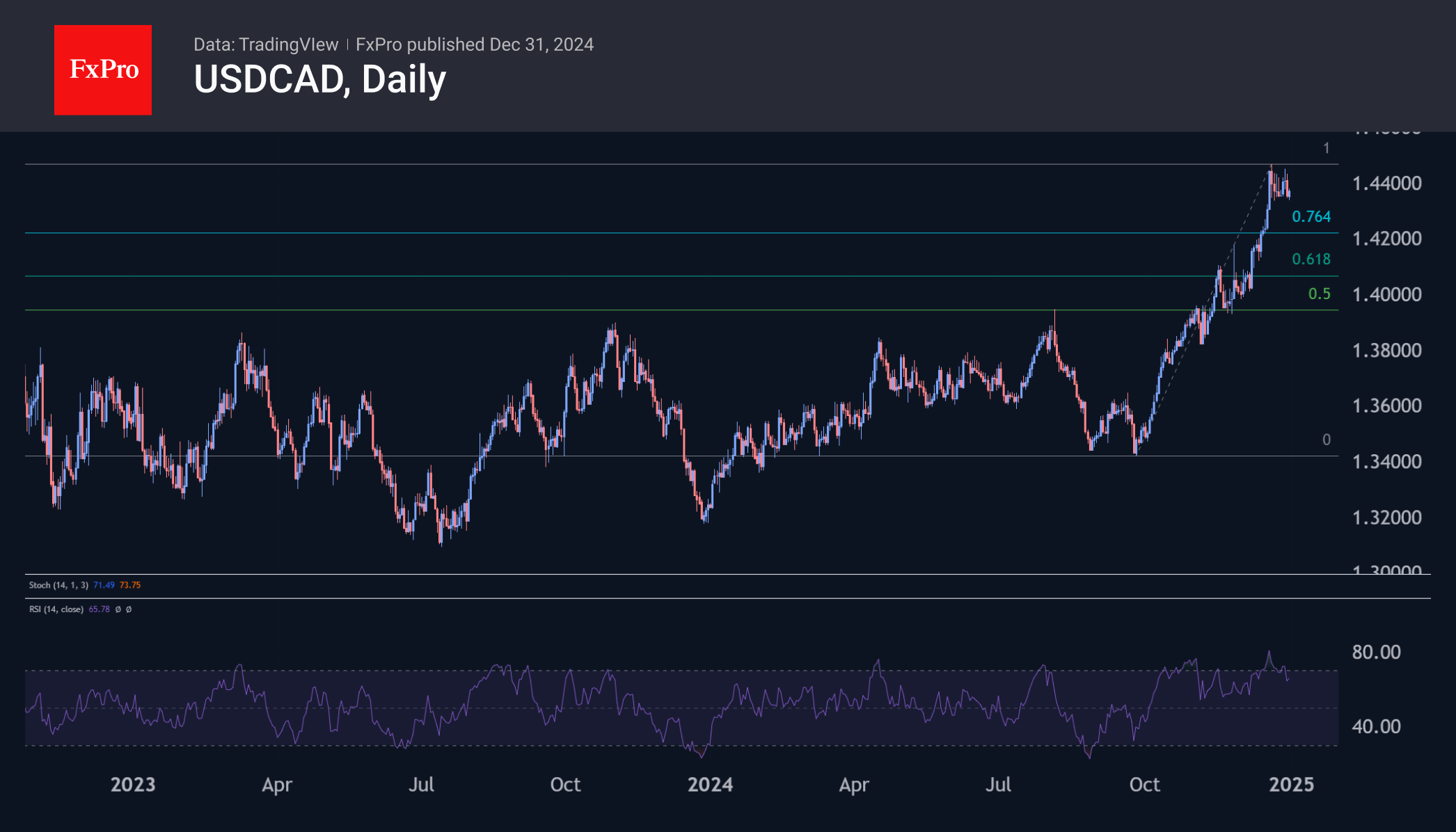

The USDCAD pair, which approached 1.45 in mid-December, is ending the year near 1.4350. The momentum of the last few days looks like a trend reversal, as there have been two unsuccessful attempts to storm the highs.

The upside momentum is losing strength after the extreme overbought conditions built up during the rally since September. The rally has been so extended that the RSI indicator on the weekly chart peaked at 75, only the third such episode in the last 10 years. In the previous two instances, the top was formed after oil.

This time, oil is smoothly forming a bottom, but it is already enough to stop the sell-off. Obviously, it is difficult for the market to push USDCAD higher without external support when the pair is already in multi-year extremes.

On the daily timeframe, USDCAD has reached overbought levels, with the RSI above 80, and the recent pullback indicates the start of a broad correction.

If we see a bottom in oil, this could attract buyers to the Canadian Dollar. The potential for a corrective pullback in USDCAD is around 2% from current levels to the 1.4080 area. The 50-day moving average and the upper boundary of the consolidation from the second half of November are now in place.

At the same time, history suggests that from such highs as we have seen in this pair, the chances of a long-term trend reversal, i.e. a return to the 1.34-1.38 area, are much higher.

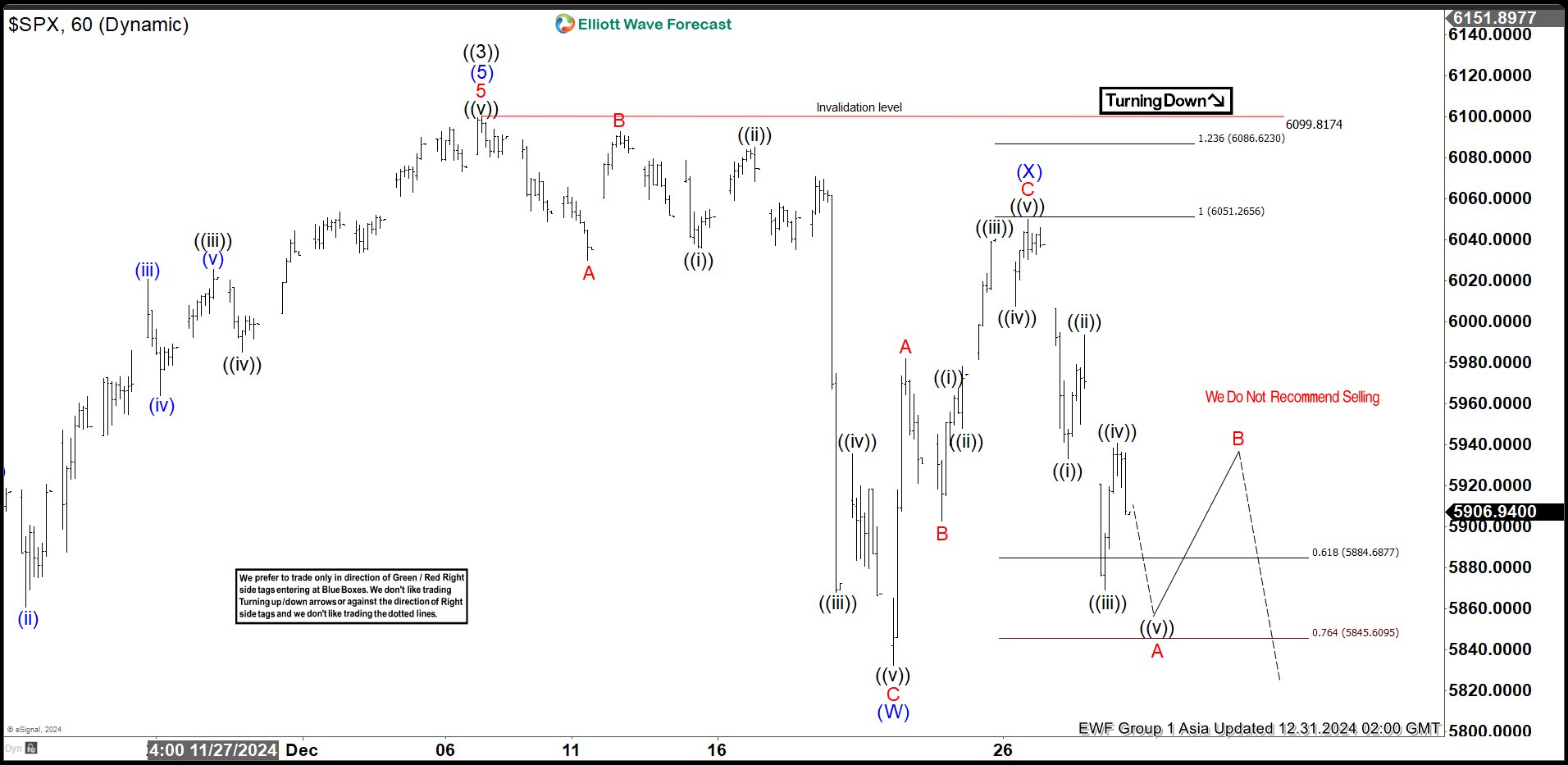

SPX : Elliott Wave Forecasting the Future Path

Hello traders ! In this technical article, we’re going to take a quick look at the Elliott Wave charts of the SPX index, published in the members area of the website. As our members know, SPX remains overall bullish, currently correcting the cycle from the August 5118.95 low. In this article, we will explain the forecast and the best way to trade SPX.

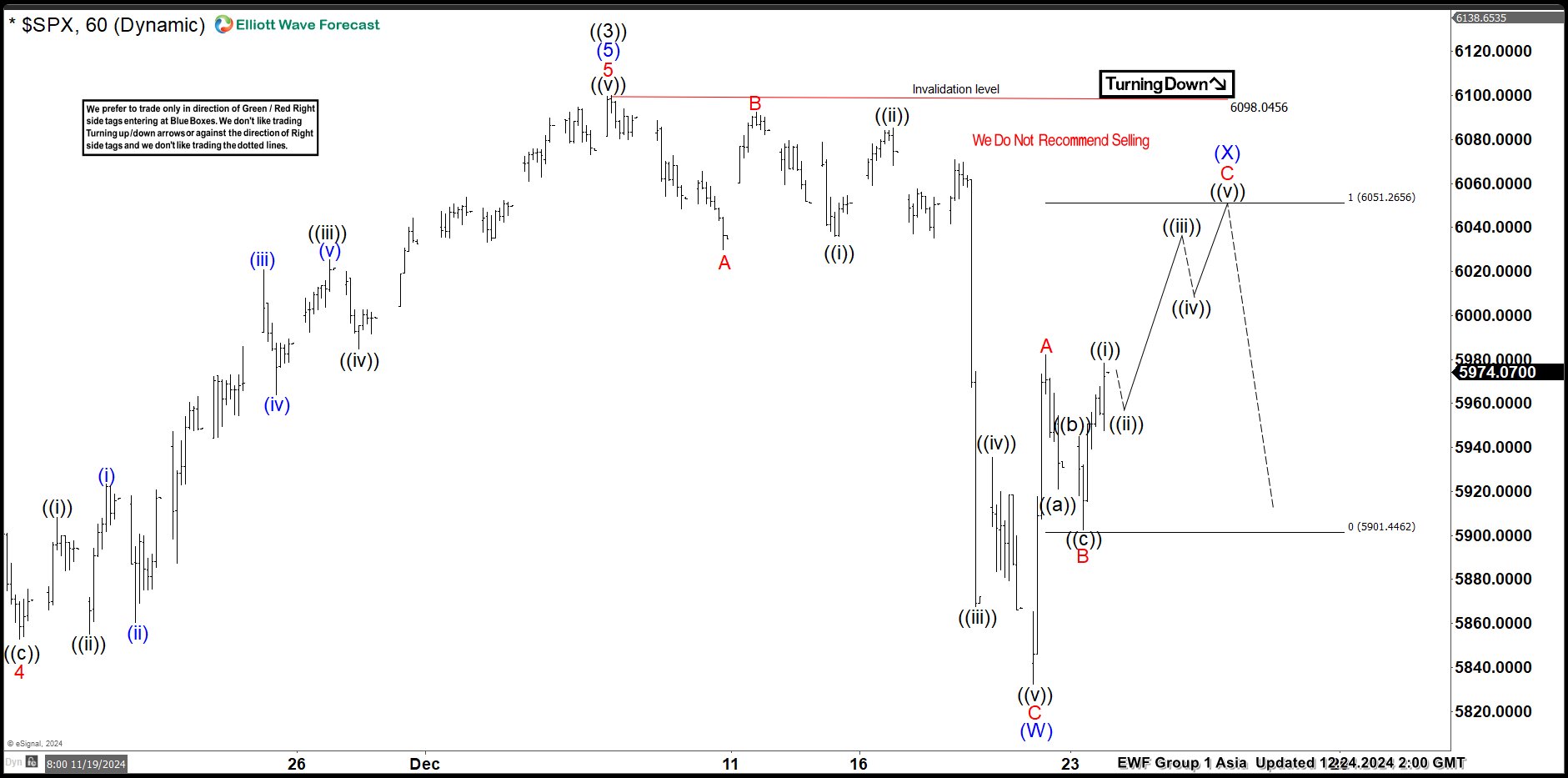

SPX H1 Update 12.24.2024

The index is bouncing against the 6098.045 high, and currently the recovery appears incomplete at the moment. We’ve seen a sharp rally from the lows, which looks impulsive. The current view suggests another leg up toward the 6051.2 area to complete a 3-wave bounce in the (X) blue recovery. From there, we could see another leg down in the (Y) blue wave to complete the 4-hour pullback against the August 5118.9 low. As our members know, we favor the long side in indices and do not recommend selling during any proposed pullbacks. If we see the proposed leg down, we will use it as a new buying opportunity.

SPX H1 Update 12.31.2024

SPX has completed the proposed leg up, forming a 3-wave recovery at the 6051 high. We consider the (X) recovery complete at that level. As long as the price remains below this high, we expect further weakness in the (Y) leg. A break of the (W) blue low at 5831.6 is needed to confirm the proposed scenario. We do not recommend selling against the main bullish trend and will view the (Y) leg as a new buying opportunity if the next extreme zone is reached.

Gold (XAU/USD) Price Analysis: Will Prices Continue to Soar in 2025?

- Gold prices on course to end 2024 with a 27% gain, the best yearly performance since 2010.

- 2025 outlook is positive due to geopolitical risks, central bank buying, and safe-haven demand.

- Trump administration policies present both risks and opportunities for gold prices.

- Technical analysis shows potential for further gains, but a deeper correction before reaching new highs is possible.

Gold prices slipped yesterday as a stronger US Dollar, anticipation of a hawkish Fed and thin liquidity all contributed. Uncertainties around tariffs and challenges in 2025 are keeping the precious metals appeal going for now and capping further losses.

Gold prices are on track to end the year with a remarkable 27% increase, marking their best yearly performance since 2010.

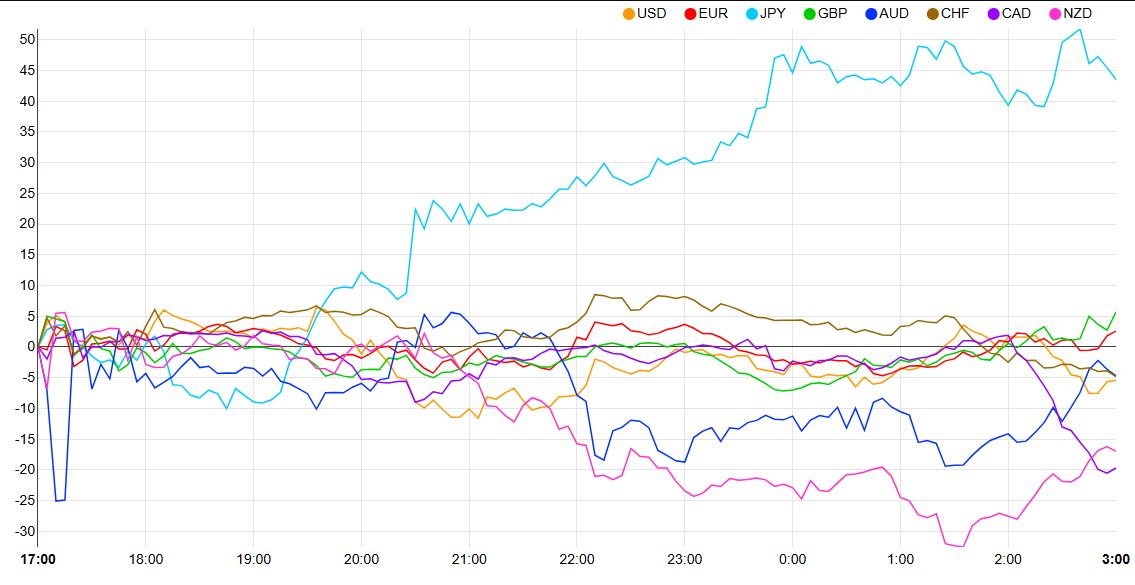

Currency Strength Chart: Strongest – Weakest – JPY, GBP, EUR, AUD, CHF, USD, NZD, CAD –

Source: FinancialJuice (click to enlarge)

2025 Outlook For Gold

Looking at the year ahead and 2025 and it will no doubt be interesting. Geopolitical risk remains a threat with the Middle East still on edge and the Russia-Ukraine situation no closer to a resolution. Just yesterday there were rumors that a proposal by the incoming Trump administration to delay Ukraine joining NATO by 10 years will not be accepted by the Kremlin.

Anyone with knowledge of the situation there will know that this will not change as the main reason for the conflict (at least from a Russian perspective) is Ukraine joining NATO. These developments are likely to keep some geopolitical risk premium in play and keep safe haven demand going.

Global Central Banks were one of the main drivers of the Gold price rise in 2024. This is expected to continue in 2025. The World Gold Council survey revealed in the second half of 2024 that Central Banks are likely to purchase more Gold in the next 12 months. This should further bolster demand for the precious metal.

When it comes to risks affecting Gold prices moving forward, it does get challenging. The reason for this is the incoming Trump administration is expected to do good things for the economy but some policies could lead to higher interest rates. This could weigh on Gold prices.

This is a double-edged sword however, in that the increased risk of uncertainty from Trump policy and concern around the impact of tariffs could actually bolster the demand for safe haven assets and thus Gold.

All in all analysts are largely pricing in further gains for the precious metal in 2025, personally I do see the potential for upside as well. However, I would not rule out a deeper correction before price does actually breach the current ATH resting around the 2790 handle.

The Week Ahead

Today could potentially be a slow day with the New Years holiday tomorrow. In such a case we could see a similar repeat to yesterday’s price action with a slow grind to the downside.

The holiday tomorrow will be followed by a return on Thursday January 2, 2025 which could bring about some volatility to markets as liquidity is expected to start returning to normal. Friday brings the last piece of high impact data from the US with the ISM Manufacturing PMI release.

The data is unlikely to change the overall narrative of the USD and thus any moves inspired by the data is likely to remain short-lived.

Technical Analysis Gold (XAU/USD)

Gold appeared poised for a move higher last week and it very much obliged. The precious metal ran into the first key area of resistance around the 2639 before falling to close the week around 2620.

The two-hour chart below shows the clear change in structure after topping out at 2639 on December 26. Since then, price has printed a series of lower highs and lower lows, breaching the 2600 psychological level briefly yesterday.

There is a descending trendline in play on the two-hour chart with a candle break and close above the trendline potentially leading to a retest of 2639.

A break below the $2600 handle may find support at the long-term ascending trendline which rests around the 2592-2596 range.

Gold (XAU/USD) Two-Hour (H4) Chart, December 31, 2024

Source: TradingView (click to enlarge)

Support

- 2600

- 2592

- 2575

Resistance

- 2620

- 2639

- 2650

WTI Oil Futures Hope for a Positive Start to 2025

- WTI oil futures gain positive momentum above short-term SMAs.

- Next challenge could occur within the $71.90-$72.50 area.

WTI oil futures are poised for a bullish start to the new year, having cemented the base around the $66.70 level, which successfully halted selling pressure for the fourth time in December. More recently, prices have climbed above both the 20-day and 50-day simple moving averages (SMAs), reinforcing the possibility that the recent rebound could gather further momentum.

The rising RSI and MACD endorse the positive scenario, but traders are unlikely to push the price higher unless they see a solid close above the nearby resistance of $71.90-$72.50. This level coincides with the 38.2% Fibonacci retracement of the July-September decline and the descending trendline from June. A breakout higher could initially pause near the 50% Fibonacci of $74.10 and then move toward the 200-day SMA and the long-term trendline from September 2023 both seen within the $75.20-$76.40 region. Beyond that, the next key level is October’s high of $77.68.

Should the bears pop up near the $72.00 number, the price may again seek shelter within the $69.00-$70.00 area. If selling interest persists, the spotlight will turn to the critical $66.70-$67.40 region, a break of which could cause an aggressive decline toward the 2024 low of $64.60 and the $64.00 level.

Summing up, WTI oil futures are poised for a new bullish cycle, with the confirmational signal likely coming above $71.90-$72.50.

What a Year It Has Been

Here we are, the last day and the last trading day of the year. It’s now been about two years that ChatGPT was launched and it’s been two years that the AI buzz pushed some US Big Tech companies to ... the sky, really. Nvidia, which has become the icon of the AI rally, gained almost 1000% since then, the Magnificent 7 nearly 100% since last November, and the S&P500 – where the market cap of the Big Tech stand for about a third of the total market cap – is set to close the year with a 25% advance, after a similar advance the year before. At the start of the year, the Big Tech rally was expected to broaden to the other sectors – which it did – but the broadening of the rally didn’t prevent the Magnificent 7 stocks to contribute to the much of the S&P500’s performance this year, the other sectors were mostly flat, the S&P500 equal-weight index played catch up with the normal-weighted, technology-heavy one, but investors gave in since the beginning of December, where we started seeing the Big Tech appetite take over. Apple for example – which remained on the backfoot with the AI progress and couldn’t do much on that platform yet, rallied 33% this year, and has fallen just 5 sessions since the beginning of the month – just five. Unfortunately, the last few days, even the tech appetite was weak. Santa didn’t show up – perhaps considering that we had enough gifts throughout the year - the S&P500 lost more than 1% for second session in a row, and Magnificent 7 was to blame. Together, they gave back 2% on Monday.

Of course, this week, the trading volumes are low, everyone – or almost everyone – is on holiday and the slightest moves in the market lead to exaggerated price action. But on the other hand, it’s also normal to start thinking that the AI rally will – one day – fizzle out, or at least we will see a sizeable correction given that the valuations went too high, and the expectations today have become very difficult to satisfy. But still, all those who called for a correction have so far happened to be wrong, and Wall Street analysts spent the year rising their price targets.

The consensus is that 2025 should be a good year, that the easing central bank policies and falling yields should help the US Big Tech rally to further broaden toward the non-tech pockets of the market, and beyond the US, with Europe seen as a good buy target for those betting that the European stocks will converge with their US peers – partly because their cyclical nature is favourable when global financial conditions ease, and partly because the valuation gap between the two

The Stoxx600 index did well between January and May this year, but then remained rangebound for the rest of the year with a marked selloff in summer. The European Central Bank (ECB) rate cuts certainly helped keeping the index in the upper Fibonacci range for a good part of the year, but it’s only a handful of companies that supported the gains. Among them, Siemens eked out the best performance of the year, the banks did well, but the luxury-stuff makers, the carmakers and heavy names like Nestle and Novo Nordisk have done poorly. You would say that it’s not very different in the US - that a few names shoulder the rally and the rest is sleeping. But in Europe, the overall growth and economic activity remains poor, which certainly pushes – and will continue to push – the ECB to be more aggressive with the rate cuts than the Federal Reserve (Fed).

And that positive divergence of the US economy was also noticeable in the valuation of the US dollar beyond the euro. The US dollar index is, in fact, having its best year since 2015. The dollar index is now consolidating gains at the highest levels in more than 2 years, and could continue to extend gains on the back of a gradually less dovish Fed outlook, based on the fact that the US economy did not weaken as much as it was expected to. On the contrary, the US GDP grew by more than 3% last quarter, versus 0.4% for the eurozone. The euro lost up to 6% against the greenback this year and up to 5% against sterling. The single currency has more room to weaken against both currencies. The pound on the other hand had a good year, but a bad selloff since September. But Cable is preparing to close the year just 1% lower against the dollar, while the USDJPY is behaving like its good, old self: the expectation that the Bank of Japan (BoJ) will normalize its policy gives hope to the bulls, but the BoJ remains short of expectations, then the yen gets sold, then the authorities step in to cool down the selloff by direct intervention and the BoJ helps by saying that they will tighten policy, and the cycle begins again.

In commodities, gold had a stellar year and could see more gains in case of a downside correction in global equity markets. While crude oil – which trades past the 100-DMA today for the first time since October – will likely close the week in the bearish consolidation zone, below the $72.85pb level, as the expectation of an average 1mbpd supply glut next year and China’s inability to reverse weakness will probably limit the upside potential.

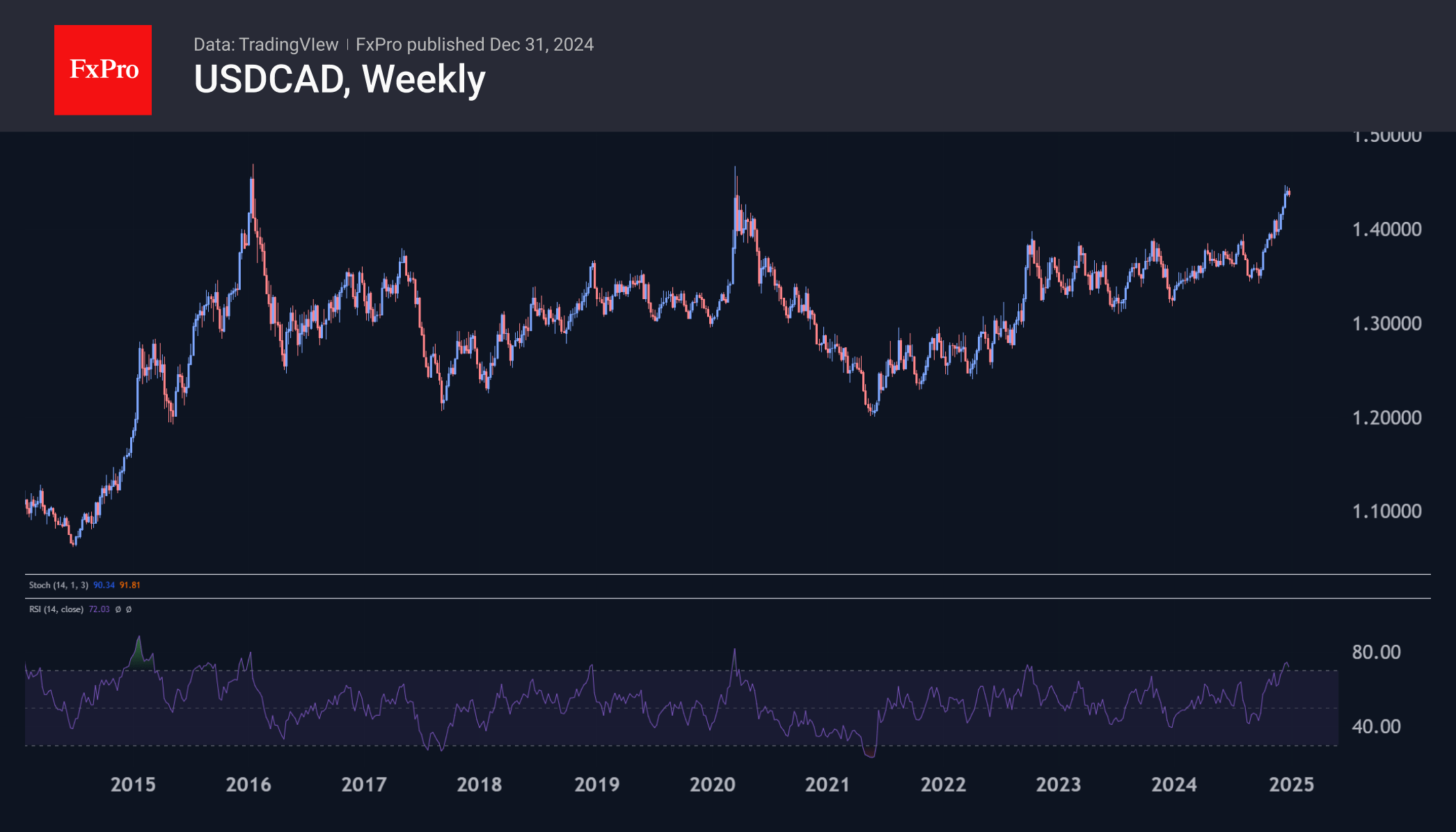

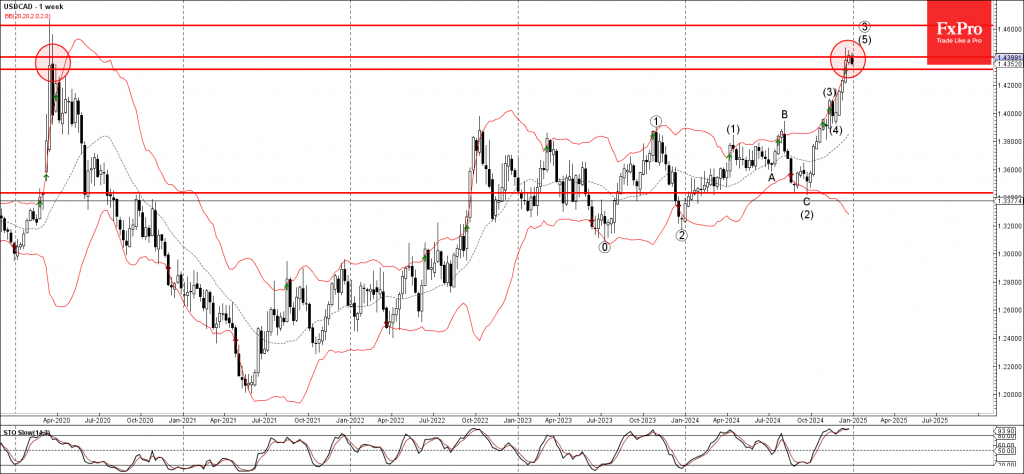

USDCAD Wave Analysis

- USDCAD reversed from resistance zone

- Likely to fall to support level 1.4400

USDCAD currency pair recently reversed down from the resistance zone surrounding the major long-term resistance level 1.4400 (which stopped the sharp uptrend at the start of 2020) intersecting with the upper weekly Bollinger Band.

The downward reversal from the resistance level 1.4400 stopped the previous medium-term impulse wave (5).

Given the strength of the support level 1.4400 and the overbought reading on the weekly Stochastic indicator, USDCAD currency pair can be expected to fall to the next support level 1.4315.

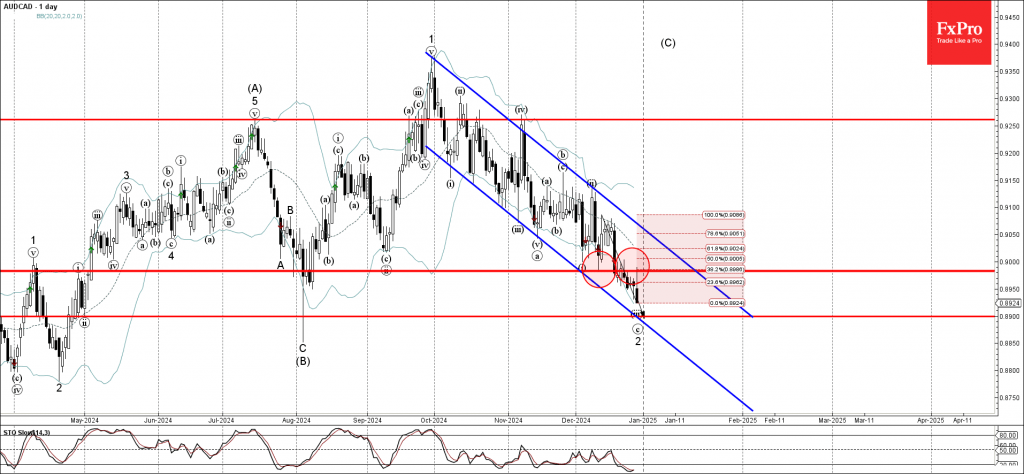

AUDCAD Wave Analysis

- AUDCAD reversed from resistance level 0.8980

- Likely to fall to support level 0.8900

AUDCAD currency pair recently reversed down from the key resistance level 0.8980 (former support from the start of December) intersecting with the 38.2% Fibonacci correction of the downward impulse from last month.

The downward reversal from the resistance level 0.8980 continues the active short-term impulse wave c of the ABC correction 2 from the end of September.

AUDCAD currency pair can be expected to fall to the next support level 0.8900 (former support from August and the target price for the completion of the active wave 2).