Sample Category Title

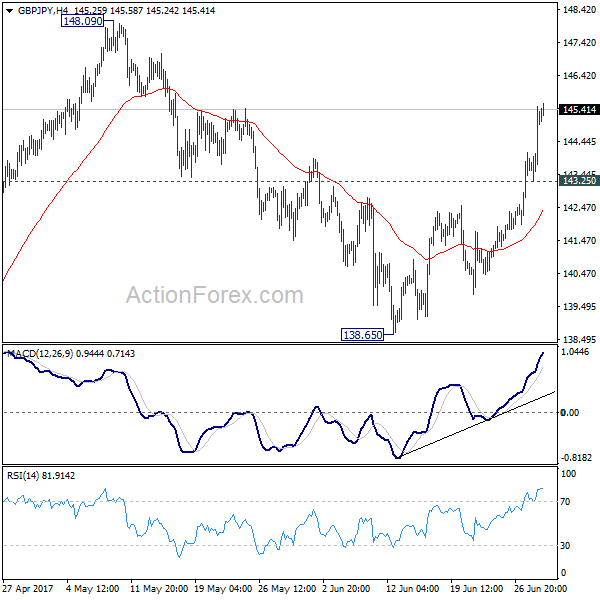

GBP/JPY Daily Outlook

Daily Pivots: (S1) 143.77; (P) 144.64; (R1) 146.03; More....

GBP/JPY reaches as high as 145.58 so far as rise from 138.65 extends. Intraday bias remains on the upside for 148.09/42 resistance zone. Decisive break there will resume whole rebound from 122.36 for key fibonacci level at 150.43. On the downside, below 143.256 minor support will turn bias neutral and bring retreat before staging another rally.

In the bigger picture, price actions from 148.42 are viewed as a consolidative pattern. And medium term rally from 122.36 is expected to resume later. Decisive break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications and pave the way to 61.8% retracement at 167.78. In case of another fall, we'd bee looking for strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside.

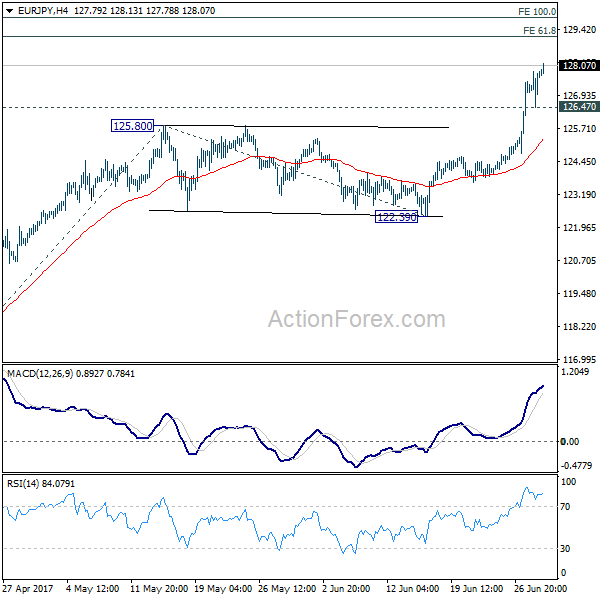

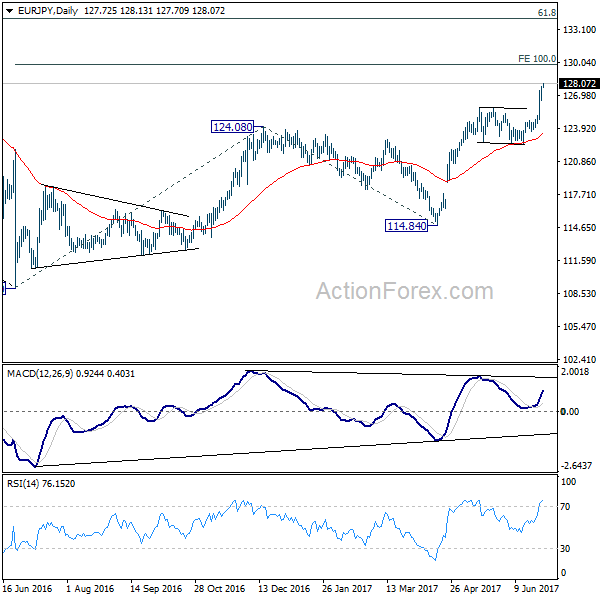

EUR/JPY Daily Outlook

Daily Pivots: (S1) 126.88; (P) 127.37; (R1) 128.27; More...

EUR/JPY's rally resumed after brief retreat and hits as high as 128.13 so far. Intraday bias is back on the upside. Current rise from 114.84 is expected to target 61.8% projection of 114.84 to 125.80 from 122.39 at 129.16 first next. That's also close to medium term projection level at 129.89. On the downside, below 126.47 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 should target 100% projection of 109.03 to 124.08 from 114.84 at 129.89 first. Break there will pave the way to 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will now remain bullish as long as 122.39 support holds.

British Pound and Canadian Dollar Soar on Rate Hike Expectations, Euro Rally Resumes after Jitters

Sterling and Canadian Dollar jumped sharply overnight as comments from BoE Governor Mark Carney and BoC Governor Poloz hinted at rate hikes ahead. Canadian Dollar is additional supported by the rebound in oil price, which sees WTI breaching 45 handle. Euro suffered some jitters on report that markets misjudged ECB President Mario Draghi's hawkish comments. But traders quickly turned to the bigger picture that ECB is, nonetheless, in a transition phase into stimulus removal. Euro remains the strongest major currency for the week, followed by Sterling and Canadian Dollar. On the other hand, the Japanese Yen is trading as the weakest as BoJ is expected to maintain stimulus. Dollar follows as markets are in doubt whether Fed will hike again in September.

BoE Carney: To debate rate hike in the coming months

BoE Governor Mark Carney said that "some removal of monetary stimulus is likely to become necessary if the trade-off facing the MPC continues to lessen and the policy decision accordingly becomes more conventional". And, as "spare capacity erodes", the "tolerance for above-target inflation falls". Carney said that the MPC will debate some of the issues "in the coming months". That's sharp turn from his own comments that "now it's not the time yet" for rate hike last week. And Carney is now more in-line with chief economist Andy Haldane that who noted that it would be "prudent" to begin removing accommodations "into the second half of the year".

Markets pricing in July hike after BoC Poloz comments

BoC Governor Stephen Poloz said that the rate cuts back in 2015 "have done their job" to counter the impact of falling oil price on the economy. And, the central bank is "approaching a new interest rate decision". He noted that for the decision "we need to be at least considering that whole situation now that the excess capacity is being used up steadily." He pointed out that regarding recovery momentum "the US obviously was way out in front. Canada some distance, perhaps as much as two years behind, given the oil shock. And then a little bit behind of course Europe." Markets took Poloz's comments as a signal that a rate hike in July 12 meeting is something that policymakers will consider. And, financial markets are pricing in over 50% chance for that.

Misjudged or not, ECB still on course to stimulus removal

Euro's rally started early this week on ECB President Mario Draghi's comment that "the threat of deflation is gone and reflationary forces are at play". There were then report yesterday saying that markets have misjudged. And, Draghi merely wanted to strike a balance between recognizing Eurozone's strength while maintaining that policy accommodation is still needed. But after all, the messages were still the same as what we pointed out before. Firstly, Draghi isn't concerned with the slowdown in inflation and judged that as "on the whole temporary". He is also optimistic on the outlook that "all the signs now point to a strengthening and broadening recovery in the euro area". So ECB is still on course to scale back monetary stimulus ahead. And September is still the time to debate and decide what to do after the current EUR 60b asset purchase program ends in December.

Markets doubtful on September Fed hike

On the other hand, news for US haven't been positive this week. In particular, markets are getting more impatient and doubtful on US President Donald Trump's ability to push through his economic agenda. Senate's delay of the healthcare vote was another sign of loss of political influence. IMF lowered US growth forecast after removing the "assumed fiscal stimulus" is another sign that analysts are giving up. Fed fund futures are pricing in less than 20% chance of a rate hike in September. It will now very much depend on the Q2 data to come out in July.

On the data front

Japan retail sales rose 2.0% yoy in May. New Zealand ANZ business confidence rose to 24.8 in June. Germany will release Gfk consumer confidence and CPI in European session. Eurozone confidence indicators will also be featured. UK will release mortgage approvals. From US, Q1 GDP final will be released with jobless claims.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 126.88; (P) 127.37; (R1) 128.27; More...

EUR/JPY's rally resumed after brief retreat and hits as high as 128.13 so far. Intraday bias is back on the upside. Current rise from 114.84 is expected to target 61.8% projection of 114.84 to 125.80 from 122.39 at 129.16 first next. That's also close to medium term projection level at 129.89. On the downside, below 126.47 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, the break of 126.09 support turned resistance should have confirmed completion of down trend form 149.76 (2014 high), at 109.03 (2016 low). Current rise from 109.03 should target 100% projection of 109.03 to 124.08 from 114.84 at 129.89 first. Break there will pave the way to 61.8% retracement of 149.76 to 109.03 at 134.20 and above. Medium term outlook will now remain bullish as long as 122.39 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y May | 2.00% | 2.80% | 3.20% | |

| 1:00 | NZD | ANZ Business Confidence Jun | 24.8 | 14.9 | ||

| 6:00 | EUR | German GfK Consumer Confidence Jul | 10.4 | 10.4 | ||

| 8:30 | GBP | Mortgage Approvals May | 64K | 65K | ||

| 9:00 | EUR | Eurozone Business Climate Indicator Jun | 0.93 | 0.9 | ||

| 9:00 | EUR | Eurozone Economic Confidence Jun | 109.5 | 109.2 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Jun | 2.8 | 2.8 | ||

| 9:00 | EUR | Eurozone Services Confidence Jun | 12.8 | 13 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Jun F | -1.3 | -1.3 | ||

| 12:00 | EUR | German CPI M/M Jun P | 0.00% | -0.20% | ||

| 12:00 | EUR | German CPI Y/Y Jun P | 1.40% | 1.50% | ||

| 12:30 | USD | GDP (Annualized) Q1 T | 1.20% | 1.20% | ||

| 12:30 | USD | GDP Price Index Q1 T | 2.20% | 2.20% | ||

| 12:30 | USD | Initial Jobless Claims (JUN 24) | 240K | 241K | ||

| 14:30 | USD | Natural Gas Storage | 61B |

Elliott Wave View: EURJPY Update 6.29.2017

Short term EURJPY Elliott Wave view suggests the decline to 122.35 on 6/15 low ended Intermediate wave (X). Rally from there is unfolding as an impulse Elliott Wave structure with extension where Minute wave ((i)) ended at 124.46 and Minute wave ((ii)) ended at 123.62. Minute wave ((iii)) ended at 127.84 and Minute wave ((iv)) at 126.46. Up from there pair has broken above the wave ((iii)) peak suggesting the next leg higher in Minute wave ((v)) has started already and after a short term pullback in Minutte wave (ii) pair should see more upside. We don’t like selling the pair.

EURJPY 1 Hour Elliott Wave Chart

Market Morning Briefing: Pound Has Surged To A 4-Week High

STOCKS

Dow (21454.61, +0.68%) bounced back from interim support near 21310 but it would be important to see if the index manages to break above 21500-21550 levels. A confirmed break on the upside, if seen could initiate fresh bullishness for the medium term.

Dax (12647.27, -0.19%) is trading higher today after testing levels just above 12500 yesterday. There is some scope of testing 12400 on the downside before bouncing back towards 12800 and higher.

Shanghai (3180.43, +0.23%) could come off towards 3150 while resistance near 3200 holds. Near term dip is possible within an overall gradual uptrend.

Nikkei (20238.85, +0.54%) is headed towards 21000, a crucial medium term resistance which could produce some corrective dip back to 19000 in the coming sessions.

There is scope for Nifty (9491.25, -0.21%) to test levels near 9400-9380 in the coming sessions before a fresh bounce could take place. For now, the corrective phase may continue for some more sessions.

COMMODITIES

Gold (1252) and Silver (16.87) are going nowhere as they keep trading in the narrow range of 1233-1262 and 16.30-17.10 respectively, which may continue for the rest of the week. A break of the respective resistances could be resulted in gradual buying for the target of 1280 and 17.50.

Copper (2.68) moved higher in line with our expectation and trading within a range of 2.66-78. The scrip is overbought thus upside could be limited but in the medium term 2.55-57 are going to be a strong support and we will remain bullish while it is trading above those levels.

Brent (47.57) and WTI (45.01) closed higher and trading as per our recommended levels. We will remain bullish in extreme short term time frame while Brent and WTI are trading above 46 and 43 levels. We might see 49 (Brent) and 47(WTI) within this rally. But in the medium term, sellers will take every bounce as a further opportunity of selling while Brent and WTI are trading below 56 and 53 levels.

FOREX

Clear indications of rate hikes coming from all the central banks from the European to North American continent and worries over the relative economic performance of US are pushing Dollar down and strengthening the majors.

Dollar Index (95.85) continues to register fresh lows as it approaches the support zone of 95.40-00. The trend remains down as long as it trades below 97.00 but keep an eye on Euro (1.1403) which has reached the major supply zone of 1.1400-1.1500. This supply zone has been rejecting all the upmoves in the last 2 years, demanding absolute caution at the current levels. 1.1550 is the highest possible level seen for now before a major bout of profit booking emerges.

Dollar-Yen (112.29) has tested 112.50 as expected and may rise further towards 113.00 if the support of 112.00 holds for the next couple of sessions.

Pound (1.2950) has surged to a 4-week high on the back of the BOE governor Carney signaling the possibility of rate hikes coming sooner than expected. It remains to be seen if the resistance zone of 1.3000-50 can contain the current rally as a successful break above this resistance may unfold further rally to 1.33-34 but the chances of the resistane holding for a few sessions before a breakout can’t be negated at this point.

Aussie (0.7655) is getting closer to the major resistance zone of 0.7700-0.7800 which is expected to hold for the next few days and push the currency back.

Dollar-Rupee (64.55) was almost ranged in the 13paisa region of 64.50-64.63 yesterday and is expected to trade sideways in the near term within 64.40-64.60. As long as the interim resistance of 64.63 holds, we could see a fall back towards 64.40 in the next couple of sessions.

INTEREST RATES

The US 10YR (2.2261%) trading higher and looks bullish in the near term. If it does not manage to break above 2.25/26% in the near term, we could see a fall back to 2.20% in the coming sessions.

The German 10Yr (0.368%) is also rising and could head towards 0.38% in the next few sessions. Greece 10Yr (5.497%) and the Italian 10YR (2.032%) are also rising respectively and looks bullish for the near to medium term.

The Japanese yields too seem to be on a rising track and could head higher in the near term. The 10Yr (0.066%) is trading higher and may test 0.070% soon.

EUR/JPY And EUR/USD Buying Opportunity After ECB Warns That The Market Misjudged Draghi’s Speech

We spoke yesterday about EUR/JPY blowing through double top resistance and price action in the aftermath suggesting huge bullish momentum.

The key quote that I wanted to extract from that post is the following:

'…and if Draghi doesn't backtrack, then any short term pullbacks could be seen as juicy buy signals.'

Well funnily enough, it turns out that the ECB backtracking on Draghi's behalf actually gave traders that juicy buy signal that we were waiting for across the Euro focused forex pairs. Have a look at some of the headlines that caused the spike down:

Now take a look at both the EUR/JPY and EUR/USD levels that I'm referring to on the charts below. The daily charts show the higher time frame resistance level that Draghi's speech saw price break out of. Then if you truly did believe in the bullish momentum behind the Euro, the intraday charts show simple areas of interest as the perfect pullback zones to buy into:

EUR/JPY Daily:

EUR/JPY 15 Minute:

EUR/USD Daily:

EUR/USD 15 Minute:

ECB Refine Message But Markets Focus on Tightening

Senior ECB officials tried to play down Draghi's hawkish speech, yet the break higher of yields, Euro and GBP crosses suggests traders expect tightening of some sort over the coming months.

It's not often a Central Bank directly tells markets how a speech or statement was meant to be deciphered. This now leaves the question as to whether Draghi was merely testing the waters and was not happy with yesterday's reaction on the Euro as it was bid aggressively higher. Overall data from Europe is strong, continues to outperform the US, China and Japan and likely supportive of sustained growth and inflation. The only ingredient lacking for a tightening is a central bank committed to doing it.

Despite the correction, it wasn't enough to stop the Euro hurtling higher and the Greenback extending losses. He US Dollar Index is within a cats-whisker from the low seen moments before Trump's election speech. The Republicans inability to get the healthcare bill through before 4th July adds another reason to sell the Greenback, and the 95.88 low of election day can be seen as confirmation that Trump's reflationary policies are indeed deemed as dead.

95.885 marks the election day low and momentum which has led us so close to it suggests it wants to break to the downside sooner than later. Unless it can form a basing pattern of some sort then 95.07 is likely the next stop.

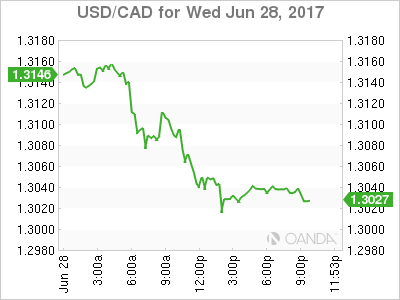

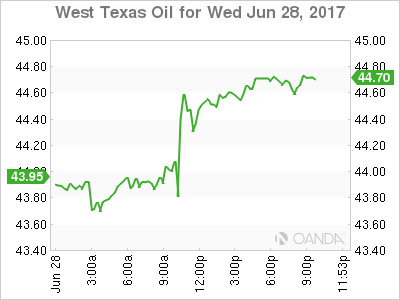

Stronger oil prices only added to the downside momentum on USDCAD, which came close to testing 1.30. This is its most bearish session in 3 months and lowest level since Feb - momentum only points down from here as the Greenback is clearly unloved and oil prices still have room to bounce further.

The prior swing high is all the way up at 1.3345, so the bearish trend is under no immediate pressure to be tested. After coming close to, yet failing to break 1.30 then there is potential for stability over the Asia session whilst oil trading also goes quiet. Yet momentum here is also pointing firmly lower. At -1.19% open to open, it went beyond a -1 standard deviation day - an area it spends 75% of trading days within. On a weekly basis, the cross in on track for a 2nd consecutive -2 standard deviation week.

We believe mean reversion is at play with oil prices and further upside could see it travel towards $47. The rally has already made it to the 20-day MA, after reverting from the lower bollinger band. The DPO (detrended price oscillator) provided a bullish divergence after price retraced from both lower bollinger bands. We are using a 20 and 20 day bollinger band to help filter out more meaningful reversal, and the 40-day MA is currently at $47. Upon prior occasions, we have seen price reverse higher from the 20 and 40 day bollinger bands, it has travelled beyond the 20 and 40-day MA. The weaker Greenback us also helping oil prices move higher and technically, we see further upside potential on WTI.

Central Banks Take Center Stage

Central Banks take Center Stage.

The market continues focusing on central bank commentary, especially in the wake of Tuesday’s speech by Mario Draghi that whipped currency markets into a frenzy. While it’s been a year of political shockers as the whirling half year comes to a close, politics, that was thought to be the main driver in the global currency market in 2017, more or less remains the sideshow as Global Central Banks once again assert dominance and take centre stage.

Signs of G-10 policy convergence abound leaving the USD prone and off balance as traders mull which central bank is the next hawkish surprise. Coupled with soft to average US economic data of late, this weaker dollar trend could have much further to run.

Central Bank headlines continued to provide much of the currency fodder overnight as both BoE and ECB were trying their best to outdo one another on the highlight reel.But perhaps it was the Bank of Canada that stole the show after both BoC Governor Poloz’s and Deputy Governor Patterson offered little ambiguity by confirming BoC hawkish policy shift.

The British Pound-Carney Carnage

BoE Carney policy flip-flop, saw the Pound powering higher to 1.2970 overnight.This abrupt policy shift saw chaotic price action leaving a swath of carnage in its wake.The markets have been trading GBP from the short side given the recent election results, and all the negativity surrounding Brexit. The markets punched through the 1.2950 level in the blink of an eye and the voracity of the 2nd “ flash rally” in as many days, has the hallmarks of nasty short covering acquiescence as GBP interest rate sensitivity comes to the fore and all but dampening the negativity from the UK political scene.

The Euro – The Rollercoaster

ECB sensitivity to risk was evident when Draghi’s hawkish lean sent European equity and bond markets topsy-turvy.

ECB headlines emerged overnight suggesting the market misinterpreted Draghi’s intentions set pandemonium in motion on G-10 desks in early NY trade. With dealers in a state heightened central bank headline sensitivity, they were quick to drive the Euro lower in aggressive selling, but the headline head fake blowout move below 1.1300 was quickly retracted, and the EURUSD powered ahead. The ECB is in the transition from floating the taper trial balloon and are now preparing the markets for the eventual end of ultra-loose money policies.Traders are focusing on the broader picture as Global Central Bankers are singing a much different tune these days. Draghi for his part made a conscious effort, using Sintra as a platform, to send a clear and unambiguous message to the market, discounting this type of guidance would be folly.

Australian Dollar -Ascending Asset

The Australian dollar moved to a three-month high powered on by broader USD weakness and rising commodity prices. The weaker US dollar is being driven by G-10 central bank policy convergence, and as traders take note of Ex RBA members John Edwards suggestions the RBA could be the next central bank hawkish surprise as inflation near in on the RBA baseline

But the fundamentals continue to paint a temperate USD landscape. The Fed is one-sidedly focused on inflation, and the lack of inflation expectations globally is keeping repricing of additional tightening from the Fed low, despite the hawkish rhetoric.

The Canadian Dollar- The Market Darling

Dealing desks were ablaze with chatter through all timezone regarding Bank of Canada Governor Poloz’s hawkish interview yesterday in early Asia. The Canadian dollar continued to power towards the psychological 1.3000 level after Deputy Governor Patterson stayed the course confirming the BoC unmistakable hawkish policy shift.

EM Asia FX

Given the stable renminbi complex and light positioning in Asia FX, the landscape appears poised for further strengthening of Asian currencies. Even if the Fed does move towards a more aggressive path of interest rate normalisation, the improving global growth narrative should support exporters in the region. While a shift is afoot towards global central bank hawkishness, the impact from ECB and BOE rate hikes tend to be less impactful for EM than a hawkish Fed as these moves will weaken the DXY broad-based and should support the underlying EM Asia currencies

This view is evident this morning as inflows are roaring back as the Kospi hits record highs.

WTI

In oil, Department of Energy crude inventories rose by just 117k. While still a disappointment from consensus calls of -2.16mn, it’s less than the +0.8mn build signalled by API. WTI dipped below $44.00 on an initial read of the data but bounced back to life.

USD/CAD Canadian Dollar Higher After BoC Signals Rate Hike

The Canadian dollar hit a four month high versus the US dollar on Wednesday after comments from Bank of Canada (BoC) Governor Stephen Poloz made it clear the central bank is considering an interest rate hike. Canadian monetary policy makers have issued hawkish statements since June 11. The market has gone from not pricing a rate move in 2017, to a 70 percent chance of a rate hike in July. The Loonie has surged as the BoC is joining a chorus of central banks that have changed the tune of their rhetoric following the lead of the U.S. Federal Reserve who has already hiked twice in 2017 with a possible another rate raise before the end of the year and a reduction of the massive balance sheet also in the works.

The BoC did not engage in a quantitive easing program although it did consider all options including negative rates but after the proactive rate cuts of 2015 the Federal government launched a fiscal stimulus program. At this time the central bank and the government are saying their actions are paying off. Concerns for rising household debt levels have prompted rating agencies to downgrade Canadian banks for their exposure to an overpriced real estate market. The central bank is now in a position to gradually start tightening. The fact that there is no QE to taper or negative rates to undo before the effects of the first rate hike puts the BoC ahead of the pack of policy makes around the globe.

Earlier today another BoC Deputy Governor Lynn Patterson added to the comments made by her peer Carolyn Wilkins and Governor Poloz by saying that the negative impact of the oil shock of 2014 is not longer dragging the economy down.

The USD/CAD lost 0.942 percent in the last 24 hours. The currency pair is trading at 1.3032 after hawkish comments from the BoC Governor have put a rate hike on the table in the near future. The market is now speculating about a July 12 meeting policy decision, although it might be too early after the BoC changed its tune from neutral to hawk in June.

The US healthcare reform has proven too controversial and has depleted the political capital of the Trump administration. This means that the pro-growth policies promised just after the elections are unlikely to be brought forth this year. The market had already priced in infrastructure spending and tax reform back in December. Right now economic fundamentals and the Federal Reserve are keeping the USD afloat. The failure to launch of relevant policies and the Russia probe are in headlines constantly. The Fed and mixed economic results have offset some of the negative pressure.

Energy prices gained 1.148 percent on Wednesday. The price of West Texas Intermediate is trading at $44.59 after the release of the US weekly crude inventories saw a small rise of 118,000 barrels instead of the forecasted drawdown of 2.5 million barrels. Oil production was down week over week as the storm in the Gulf of Mexico has affected supply in the US. The API report came in with higher buildups so the energy traders were already pessimistic by the time the Energy Information Administration (EIA) report showed a lower buildup in crude and a surprise drawdown in gasoline stocks.

US oil rigs have increased in number this year at the same time the Organization of the Petroleum Exporting Countries (OPEC) has agreed to extend the production oil cut agreement in a move that aims to stabilize oil prices going forward. OPEC members will meet with other major producers in Russia to discuss the next steps to boost energy prices.

Market events to watch this week:

Thursday, June 29

8:30 am USD Final GDP q/q

8:30 am USD Unemployment Claims

Friday, June 30

4:30 am GBP Current Account

8:30 am CAD GDP m/m

Gold Edges Higher, Markets Nervously Eye US GDP

Gold has edged higher on Wednesday. In the North American session, spot gold is trading at $1249.56 per ounce. In economic news, Pending Home Sales disappointed with a decline 0.8%, well short of the forecast of +0.9%. On Thursday, the US releases Final GDP and unemployment claims.

Investors are casting a nervous glance towards Thursday, as the US releases Final GDP for the first quarter. Preliminary GDP, which was released in May, came in at 1.2%, and this is the same estimate for the upcoming GDP report. Recent economic data has been softer than expected, notably construction and manufacturing reports. US durable goods releases were weak in May. Core Durable Goods broke a streak of two straight declines, but the weak gain of 0.1% missed expectations. Durable Goods declined 1.1%, its sharpest decline since June 2016. The slowdown in orders of business equipment could weigh on second quarter growth. Last week, it was the turn of construction numbers to disappoint, as Housing Starts and Building Permits both missed expectations. Consumer spending has also been softer than expected, and if Final GDP falls short of the modest estimate of 1.2%, the dollar could respond with losses.

This week, the markets are focused on the picturesque city of Sintra, Portugal. Sintra is hosting the ECB Forum, as central bankers have stepped in as market-movers this week. On Tuesday, the euro posted strong gains after ECB President Mario Carney sounded upbeat about the eurozone economy and shrugged off concerns about low inflation. On Wednesday, it was BoE Governor Mark Carney's turn in the limelight, as his comments have sent the pound higher. Carney said that the BoE would have to consider removing monetary stimulus, and the markets jumped on his comments as a possible sign that he was not adamantly opposed to rate hikes in the near future. BoE policymakers have waged a public debate about rate policy, with Carney stating last week that he was opposed to hikes, only to be contradicted by MPC member Ande Haldane, who said he had been close to voting in favor of a rate hike at the June rate meeting. The vote at the meeting was 5-3 in favor of maintaining rates, surprising the markets, which had predicted a 7-1 vote to keep rates at current levels. Although there are renewed fears that Brexit will take a toll on the British economy, inflation is running close to 3%, well above the BoE's target of 2 percent. A rate increase would help lower inflation, but Carney, who has voiced concerns about Brexit's negative ramifications since the vote last June, has been solidly against a rate increase. The comments from Draghi and Carney could improve investors' risk appetite, which in turn could send gold prices to lower levels.