Sample Category Title

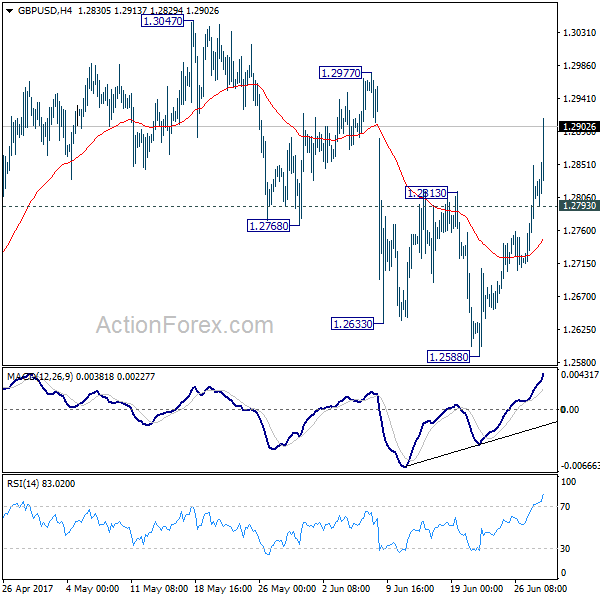

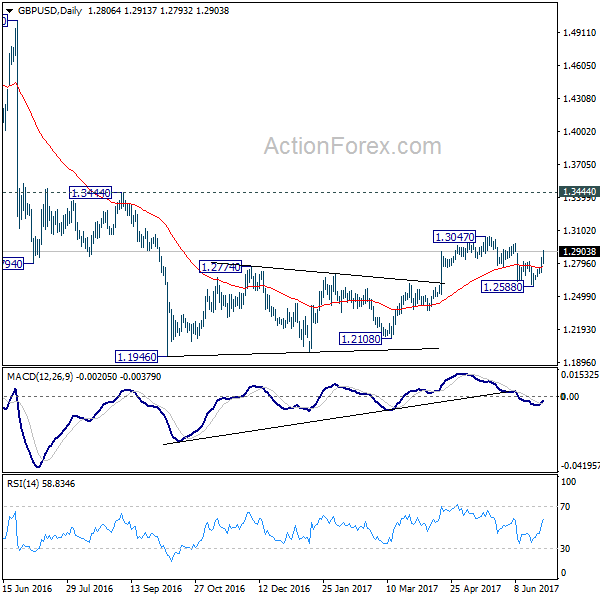

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2731; (P) 1.2796; (R1) 1.2876; More...

GBP/USD's rally accelerates to as high as 1.2911 so far today and intraday bias remains on the upside. Pull back from 1.3047 should have completed at 1.2588 already. Rise from there should now target 1.2977 resistance first. Break there will likely extend the larger rise through 1.3047 resistance. On the downside, below 1.2793 minor support will turn bias neutral first and bring retreat.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. Pull back from 1.3047 has completed after failing to sustain below 1.2614 resistance turned support. It argues that the corrective pattern from 1.1946 is still in progress for another high above 1.3047. But still, outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes.

Trade Idea Update: EUR/USD – Buy at 1.1280

EUR/USD - 1.1335

Original strategy :

Buy at 1.1280, Target: 1.1395, Stop: 1.1245

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1280, Target: 1.1395, Stop: 1.1245

Position : -

Target : -

Stop : -

The single currency has retreated after rising to 1.1389, suggesting consolidation below this level would be seen and pullback to 1.1280-85 (50% Fibonacci retracement of 1.1172-1.1389) cannot be ruled out, however, reckon 1.1255 (61.8% Fibonacci retracement) would hold and bring another rise later, above said resistance at 1.1389 would extend recent upmove 1.1400-05 (61.8% projection of 1.0839-1.1296 measuring from 1.1119), then towards 1.1430 but overbought condition should prevent sharp move beyond 1.1450-60 and price should falter below 1.1500.

In view of this, would not chase this rise here and would be prudent to buy euro on pullback as 1.1280-85 should limit downside. Below 1.1245-50 would defer and risk test of previous resistance at 1.1220 but break there is needed to confirm top is formed instead, bring correction towards 1.1180-85 later.

Trade Idea Update: USD/JPY – Buy at 111.80

USD/JPY - 112.16

Original strategy :

Buy at 111.80, Target: 112.80, Stop: 111.45

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.80, Target: 112.80, Stop: 111.45

Position : -

Target : -

Stop : -

The greenback has maintained a firm undertone after this week’s rally on active cross-selling in yen, adding credence to our bullishness and signal the rise from 108.82 low is still in progress, hence further gain to 112.75–80 (61.8% projection of 108.82-111.79 measuring from 110.95) would be seen, however, loss of momentum should limit upside and price should falter below 113.00-10 today, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback but at a higher level as 111.80 should limit downside. Below minor support at 111.46 would defer and suggest top is possibly formed, risk weakness to 111.10-15, break there would confirm, then test of support at 110.95 would follow.

CAC Ticks Lower, Investors Look for Cues

The CAC index is showing little movement in the Wednesday session. Currently, the index is down 0.07% and is trading at 5264.00. ECB President Mario Draghi will address the ECB Forum of Central Bankers. Will Draghi perform an encore and push the euro even higher? On Thursday, the US will publish Final GDP.

The markets continue to keep an eye on Sintra, Portugal, which is hosting the ECB Forum. On Tuesday, Mario Draghi was upbeat about economic conditions in the eurozone, and the euro responded with sharp gains, although the CAC lost ground. Draghi acknowledged that economic indicators continued to point to a broadening recovery in the eurozone, but pointed to inflation as the barrier to tightening policy. Draghi defended the bank's loose accommodative policy, saying that it had pushed inflation higher, but stimulus was needed until inflation becomes "durable and self-sustaining".

The election of Emmanuel Macron as president has revived morale in the country, as the young and charismatic Macron appears determined to bring major changes to France. This sense of optimism was underscored by the latest INSEE consumer confidence report, which jumped to 108 points in the June report, up from 103 in May. This marked the highest level since 2007. Although consumers are in a good mood, this optimism has so far not translated into stronger consumer spending, but nevertheless is another sign that the French economy is improving. INSEE has revised upwards its estimate for France's GDP for the first quarter to 0.5%, up from 0.4% earlier in June.

Investors are anxiously awaiting a key report card for the US economy, with the release of Final GDP on Thursday. Preliminary GDP, which was released in May, came in at 1.2%, and this is the same estimate for the upcoming GDP report. Recent economic data has been softer than expected, notably construction and manufacturing reports. US durable goods releases were weak in May. Core Durable Goods broke a streak of two straight declines, but the weak gain of 0.1% missed expectations. Durable Goods declined 1.1%, its sharpest decline since June 2016. The slowdown in orders of business equipment could weigh on second quarter growth. Last week, it was the turn of construction numbers to disappoint, as Housing Starts and Building Permits both missed expectations. Consumer spending has also been softer than expected, and if Final GDP falls short of the modest estimate of 1.2%, the dollar could respond with losses.

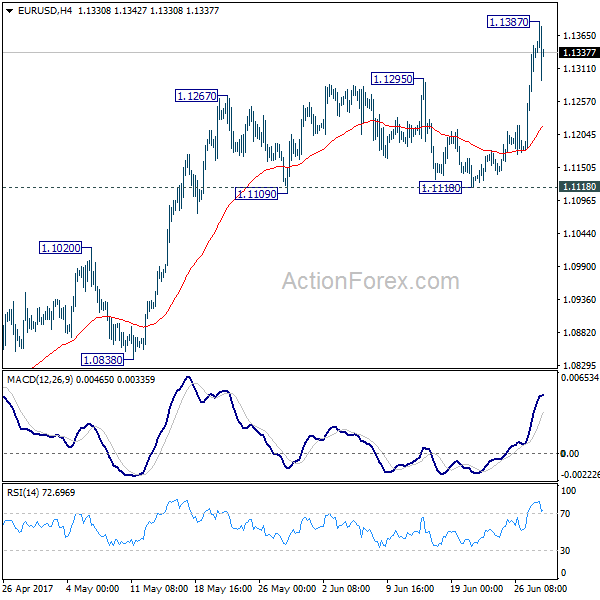

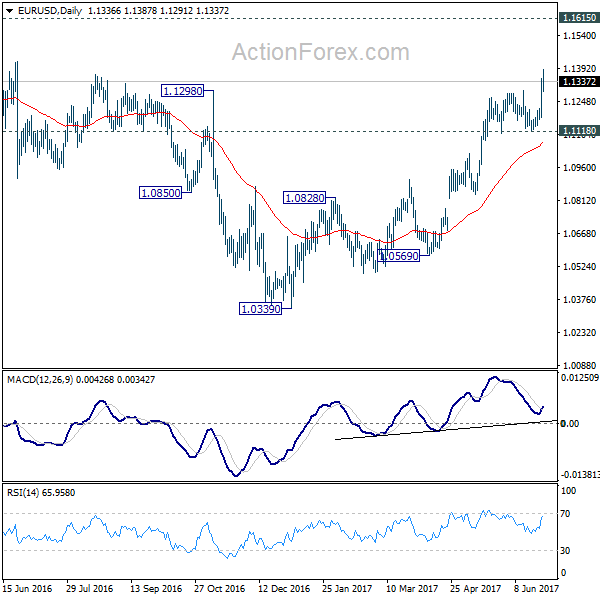

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1227; (P) 1.1288 (R1) 1.1398; More....

EUR/USD surges to as high as 1.1387 today but retreats sharply since then. A temporary top should be in place and intraday bias is turned neutral for consolidation first. Downside of retreat is expected to be contained well above 1.1118 support to bring rally resumption. Above 1.1387 will extend the larger rally to 1.1615 resistance next. However, break of 1.1118 will now confirm short term topping and bring deeper pull back.

In the bigger picture, the break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition is seen in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Euro Retreats Sharply on Talk that Markets Misinterpreted ECB Draghi and Overreacted

Quick update: Sterling jumps sharply after BoE governor Mark Carney's comments. He said that "these are some of the issues that the MPC will debate in the coming months," Carney said. "Some removal of monetary stimulus is likely to become necessary if the trade-off facing the MPC continues to lessen and the policy decision accordingly becomes more conventional."

Euro retreats sharply on report that markets has overreacted to ECB President Draghi's comment yesterday. Bloomberg quoted unnamed source saying that Draghi's comments were intended to strike a balance between recognizing Eurozone's strength while maintaining that policy accommodation is still needed. In particular, the reactions were hyper sensitive to Draghi's comment that "the threat of deflation is gone and reflationary forces are at play". EUR/USD hits as high as 1.1387 earlier today but is now back at 1.1330 after breaching 1.13 handle briefly. EUR/GBP also breached 0.8851/8865 key resistance zone earlier today but is back at 0.8830. Meanwhile, the development also triggered recovery in USD/CHF to as high as 0.9646.

Technically, Euro would likely turn into consolidation first before traders make up their mind on what to believe in. As long as 1.1118 support holds, EUR/USD stays bullish for further rally. As long as 124.64 support holds, EUR/JPY also stays bullish. And, as long as 0.8718 support holds, EUR/GBP also remains bullish in near term.

ECB Vice Constancio: Slack is bigger than they judge

ECB Vice President Vitor Constancio questioned whether the central bank's measures of the slack of the economy is correct. He pointed out that "domestic factors of inflation starting with wage and cost developments and then also price decisions are not responding the way we would expect in view of our more common estimates of this slack." He said that unemployment in Eurozone is at 9.3% according to "normal international standard" of measurement. However, it would be 18% if ECB uses the broader concept as in US. Hence, the slack is "bigger" than ECB could judge some time ago.

BoE Cunliffe wants more time before hiking

BoE Deputy Governor Jon Cunliffe said he would prefer more time to see how things evolve before raising interest rate. He pointed to slowing consumer spending as households' real incomes were squeezed by higher inflation. While some of the effect would be offset by growth in business investment and exports, he "wanted to see how that plays out". Meanwhile, looking at domestic inflation pressure, Cunliffe said the data "gives us a bit of time to see how this evolves". While inflation above target is "not a comfortable place" for any MPC member, it's important to see how much was generated domestically, comparing to the consequence of Sterling's depreciation. He highlighted slow wage growth as averages earnings rose just 1.7% in the three months to April, lowest since January 2015.

IMF lowered US growth forecast

Yesterday, IMF lowered US growth forecast in 2017 to 2.1%, down from April projection of 2.3%. For 2018, growth projection was also lowered to 2.1%, down from 2.5%. IMF director of the Western Hemisphere Department Alejandro Werner said that given the uncertainty of US President Donald Trump's policies, "we have removed the assumed fiscal stimulus from our forecast". Also, IMF noted that even with an "ideal constellation of pro-growth policies, the potential growth dividend is likely to be less than that projected in the budget and will take longer to materialize." That is, IMF is not convinced that Trump's policy, even if implemented, could bring 3% growth in US by 2020.

On the data front

US wholesale inventories rose 0.3% in May versus expectation of 0.2%. Trade deficit narrowed slightly to USD -66.0b in May. Eurozone M3 money supply rose 5.0% yoy in May. Swiss UBS consumption indicator rose to 1.39 in May. German import price index dropped -1.0% mom in May.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1227; (P) 1.1288 (R1) 1.1398; More....

EUR/USD surges to as high as 1.1387 today but retreats sharply since then. A temporary top should be in place and intraday bias is turned neutral for consolidation first. Downside of retreat is expected to be contained well above 1.1118 support to bring rally resumption. Above 1.1387 will extend the larger rally to 1.1615 resistance next. However, break of 1.1118 will now confirm short term topping and bring deeper pull back.

In the bigger picture, the break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition is seen in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | EUR | German Import Price Index M/M May | -1.00% | -0.60% | -0.10% | |

| 06:00 | CHF | UBS Consumption Indicator May | 1.39 | 1.48 | 1.34 | |

| 08:00 | EUR | Eurozone M3 Y/Y May | 5.00% | 5.00% | 4.90% | |

| 12:30 | USD | Advance Goods Trade Balance May | -66.0B | -66.2B | -67.1B | -67.0B |

| 12:30 | USD | Wholesale Inventories May P | 0.30% | 0.20% | -0.50% | -0.40% |

| 14:00 | USD | Pending Home Sales M/M May | 0.80% | -1.30% | ||

| 14:30 | USD | Crude Oil Inventories | -2.5M |

The Dollar Sinks While Euro Rallies

The last remnants of the once phenomenal Trump rally were thoroughly crushed on Tuesday after the International Monetary Fund (IMF) trimmed its growth forecast for the US economy amid uncertainty over White House policies. Although US President Donald Trump has, on multiple occasions, stated that he will 'make America great again' the IMF seems unconvinced as it cut growth forecast for the US economy to 2.1% in 2017 and 2018, against April's projections of 2.3% in 2017 and 2.5% in 2018. With the world's largest economy struggling to hit Trump's 3% GDP target as it confronts issues ranging from an ageing population to low productivity, sentiment is likely to take a hit with the Dollar finding itself under renewed selling pressure.

Bearing in mind that the IMF's growth projection for the US economy was revised due to flailing assumptions of Donald Trump moving forward with market shaking pro-growth policies, this is a big deal and it will be interesting to see how Fed policymakers react.

Dollar bullish investors who were in desperate need of inspiration to support the Greenback were left empty handed on Tuesday evening after Yellen maintained a safe distance from monetary policy at an event in London. Although she reiterated that 'it will be appropriate to raise interest rates very gradually,' this was old news with nothing fresh brought to the table.

An interesting statement on Yellen's part was how the banking reforms have currently made the financial system safe, with the next type of crisis that rattled the global markets in 2008 'hopefully not in our lifetimes.' While the comment continues to echo her overall optimism over the US and global economy, Dollar bears were unfazed with the Dollar Index sinking towards 96.20 as of writing.

GBPUSD pops above 1.2775

Sterling bulls were gifted an unexpected lifeline on Tuesday in the form of Nicola Surgeon putting the Scottish independence referendum bill on hold. With the delay of the proposed referendum reducing some political risk at home, the Pound was given room breath. A weak Dollar played a role in the GBPUSD's rebound as prices sprung towards 1.2850. While short-term technical bulls may have won the battle this week, the war still rages on with Brexit woes likely to limit gains in the medium to longer term.

Euro bulls were unstoppable during Tuesday's trading session following the firmly hawkish comments from European Central Bank President Mario Draghi which boosted confidence over the health of the European Economy. With 'deflationary forces being replaced by reflationary ones,' speculation has mounted over the central bank potentially tapering QE in the future. Although the central bank president still highlighted that the inflation dynamics remain muted, there is optimism that the current factors hindering inflation are transitory and as such the Euro found further support. A vulnerable US Dollar complimented the EURUSD's upside with prices bursting above 1.1300. Technical traders could exploit the decisive break above 1.1300 to target 1.1450.

WTI Crude edges above $44

The fundamental reason why oil has remained depressed for such a prolonged period lies in the high global crude inventories. As long as the oversupply woes remain a dominant theme, the bearish sentiment towards oil should ensure sellers maintain control. Although WTI Crude edged higher during Wednesday's trading session, this technical bounce may provide a platform for bears to install renewed rounds of selling. This remains a critical period for the oil markets especially when factoring in how the extended periods of low prices and US Shales resurgence could cause OPEC's output cut deal to fall apart. A technical bounce on oil may be on the cards with traders observing how prices react to the daily 20 SMA which is coincidentally at $45.

Commodity spotlight – Gold

Gold bulls were unrestrained during Wednesday's trading session with prices clipping $1252 as the combination of Dollar weakness and risk aversion boosted the metal's safe-haven allure. The sharp losses observed at the start of the week have almost been clawed back with bulls eyeing $1260. With the ongoing uncertainty of Brexit, political risk in Washington and jitters from depressed oil accelerating the flight to safety, Gold is likely to remain supported moving forward. Technical traders will be paying attention to how the metal behaves above $1250. A daily close above $1250 could encourage a further incline towards $1260

GBPUSD – Remains Bullish, Eyes Further Upside Pressure

GBPUSD - The pair continues to face upside pressure following its higher close on Tuesday. Support lies at the 1.2750 level where a break will turn attention to the 1.2700 level. Further down, support lies at the 1.2650 level. Below here will set the stage for more weakness towards the 1.2600 level. Conversely, resistance stands at the 1.2850 levels with a turn above here allowing more strength to build up towards the 1.2900 level. Further out, resistance resides at the 1.2950 level followed by the 1.3000 level. Its daily RSI is bullish and pointing higher suggesting further strength. On the whole, GBPUSD continues to face upside threats.

Optimistic Draghi Propels The Euro Higher

The euro skyrocketed yesterday, following some optimistic comments from the ECB chief Mario Draghi. He noted that deflationary forces in the euro area have been replaced by reflationary ones, and that the factors weighing on the path of inflation are mainly temporary factors that typically the Bank can look through. He added that signs now point to a strengthening and broadening recovery in the euro area, while the bloc's economic growth is above trend.

Even though none of these signals is particularly new, his hawkish tone may have come as a surprise to investors who expected yet another cautious speech, following the one on Monday. What's more, these remarks are in line with our view that the ECB is likely to continue to shift towards a more sanguine tone at its upcoming gatherings. Indeed, the Bank has removed some dovish aspects from its forward guidance in both the March and the June meetings. Assuming that Eurozone's economic data remain solid, we could see this process continue at the September meeting, or even earlier, perhaps in July. Something like that could keep the euro under buying interest. Having said that, much of the currency's near-term direction may also depend on the bloc's preliminary CPI prints for June, due out Friday.

EUR/USD surged on Tuesday following ECB President Draghi's remarks. The pair emerged above 1.1220 (S2) on the comments and later in the day, it managed to overcome the key resistance (now turned into support) hurdle of 1.1300 (S1). In our view, the break above 1.1300 (S1) signals the upside exit of the sideways range that contained the price action since the 19th of May, between that barrier and the support zone of 1.1120. As such, we consider the short-term outlook to have turned back positive. We expect the bulls to challenge the 1.1370 (R1) resistance soon, where a decisive break could set the stage for more upside extensions, perhaps towards our next resistance of 1.1430 (R2). Nevertheless, given that the rally appears overextended, we would stay mindful that a corrective setback may be on the cards, perhaps to test the 1.1300 (S1) obstacle as a support this time.

EUR/GBP also rallied on Draghi's speech. The pair emerged above the 0.8820 (S1) hurdle and during the early European morning appears ready to challenge the 0.8870 (R1) resistance, marked by the peak of the 12th of June. Bearing in mind that the rate continues to trade above the uptrend line drawn from the low of the 10th of May, we consider the short-term outlook to be positive. A decisive move above 0.8870 (R1) would confirm a forthcoming higher high and perhaps open the way for our next resistance of 0.8945 (R2).

Today's highlights:

The only economic indicators we get are the UK's nationwide house price index for June, and later in the day, US pending home sales for May.

The absence of major economic indicators does not imply a quiet day though, as we have a plethora of speakers on the agenda. The main event will probably be a panel discussion at the ECB forum on Central Banking, featuring ECB President Mario Draghi, BoE Governor Mark Carney, BoJ Governor Haruhiko Kuroda and BoC Governor Stephen Poloz. Even though the discussion may be academic overall and thus may not have a significant market impact, we will still listen closely, considering the importance of all these speakers. ECB Vice President Vitor Constancio, as well as Executive Board members Sabine Lautenschlager and Yves Mersch, will also deliver remarks.

EUR/USD

Support: 1.1300 (S1), 1.1220 (S2), 1.1170 (S3)

Resistance: 1.1370 (R1), 1.1430 (R2), 1.1485 (R3)

EUR/GBP

Support: 0.8820 (S1), 0.8775 (S2), 0.8715 (S3)

Resistance: 0.8870 (R1), 0.8945 (R2), 0.9000 (R3)

DAX Lower, Investors Await German CPI

The DAX index has lost ground in the Wednesday session, continuing the downward trend which marked the Tuesday session. Currently, the index is at 12,605.50, down 0.56%. On the release front, ECB President Mario Draghi will speak again before the ECB Forum of Central Bankers. On Thursday, Germany releases Preliminary CPI and the US will publish Final GDP and unemployment claims.

The markets continue to keep an eye on Sintra, Portugal, which is hosting the ECB Forum. On Tuesday, Mario Dragihi's was upbeat about economic conditions in the eurozone, and the euro responded with sharp gains, although the CAC lost ground. Draghi acknowledged that economic indicators continued to point to a broadening recovery in the eurozone, but pointed to inflation as the barrier to tightening policy. Draghi defended the bank's loose accommodative policy, saying that it had pushed inflation higher, but stimulus was needed until inflation becomes “durable and self-sustaining”. Germany is not happy with the ECB's current monetary policy, as it feels that tighter policy is more appropriate for the strong German economy. For his part, Draghi has no intentions of altering current policy until inflation moves closer to the ECB's target of 2 percent, and he has been consistent in this message.

The German economy continues to perform well, as the labor market is strong, exports are up and consumer demand is solid. Still, Germany has not been immune to low inflation levels, which have hampered economies in Europe, Japan and North America (The UK is one notable exception). German CPI, the primary gauge of consumer inflation, has not posted a gain since March, and the estimate for the June report stands at a flat 0.0%. The strong economy and the ECB's loose monetary policy, inflation remains stubbornly low. One key factor in this is falling oil prices, which have also pushed energy stocks lower, and this has weighed on the CAC. Mario Draghi has sounded more optimistic about inflation levels, but at the same time has underscored that the ECB has no plans to remove stimulus until inflation levels in the eurozone are closer to the ECB's target of 2 percent. Some analysts have projected that the ECB will not raise interest rates before 2019.