Sample Category Title

Canadian GDP Up in October, But Momentum Faded in November

The Bottom Line:

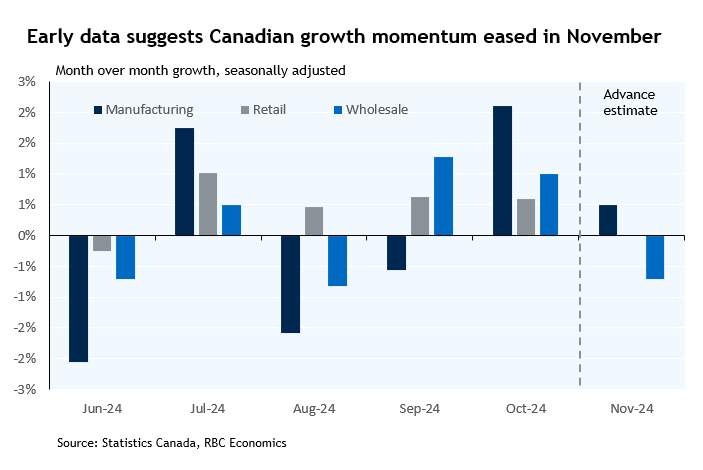

Today's GDP report shows Canadian economic growth accelerated in October from September; however, the early estimate points to a contraction (-0.1%) in November, consistent with preliminary reports showing softer wholesale sales, declining manufacturing volumes, and flat retail sales.

The Bank of Canada's December messaging pointed to a more gradual approach on rate cuts going forward than the 50 bp reductions in each of October and December, but we continue to expect that interest rate cuts down to a net stimulative 2% overnight rate (below the BoC's estimated neutral range of 2.25% to 3.25%) will be warranted to allow economic growth to strengthen and prevent inflation from falling significantly below the central bank’s 2% target.

The Details:

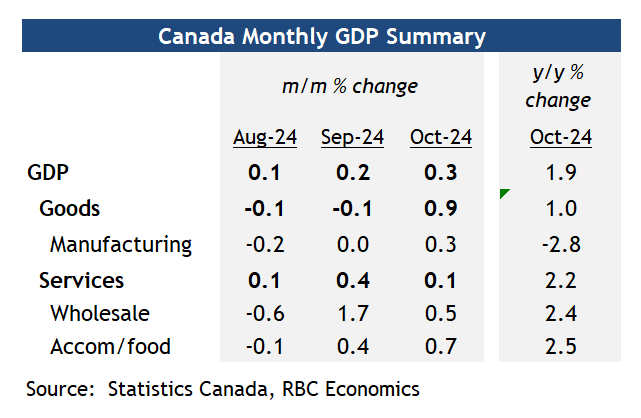

Canadian GDP expanded 0.3% in October following a revised 0.2% increase in September (upgraded from an initial reading of 0.08% to 0.24%). October's growth exceeded Statistics Canada's preliminary estimate of 0.1%.

The advance estimate pointed to a 0.1% contraction in November. These preliminary figures are typically subject to significant revision, but the pullback in November is consistent with softer looking wholesale and manufacturing sale advance estimates for the month, and a pullback in consumer spending in our own tracking of card transactions.

At current trajectory, Q4 GDP growth appears to be tracking closer to, but still slightly below, the Bank of Canada's 2% forecast.

The goods-producing sector registered its strongest performance since January 2023, expanding 0.9% in October. This growth was primarily driven by the mining, quarrying, and oil and gas extraction sector, which surged 2.4%.

Other goods sectors also showed improvement. Mining support activities rose 1.3% in October, partially reversing declines from the previous two months. Manufacturing output increased 0.3%, breaking a four-month streak of weak readings. StatsCan reported that non-durable manufacturing posted particularly strong growth (+1.2%), boosted by petroleum refineries resuming operations following scheduled maintenance.

Growth in the services sector moderated to 0.1% from September's 0.4% pace. While retail trade output remained flat, wholesale trade advanced 0.5%. The real estate sector maintained its strong momentum (+6.3%), supported by robust home resale activity during the month.

Canada’s Economy Beats Growth Expectations in October, Pullback Expected in November

Canadian economic growth jumped 0.3% month-on-month (m/m) in October, ahead of Statistics Canada's advanced guidance and consensus expectations. Early estimates from Statistics Canada point to a slight pullback in November GDP (-0.1% m/m).

October's reading was broad-based, with output expanding in 12 of 20 industries. The goods sector grew by a hefty 0.8% m/m, while the services sector added a modest assist of 0.1% m/m to October's GDP growth.

On a weighted basis, the mining/oil & gas sector posted the biggest tailwind for October activity, gaining 2.4% m/m, with oil & gas extraction (+3.1% m/m) accounted for most of the gain. Elsewhere, the manufacturing sector advanced for a second consecutive month (0.3% m/m), while construction grew by 0.4% m/m.

On the services side, the real estate sector saw its biggest monthly gain so far in 2024, up by 0.5% m/m on the back of a rise in national home sales. Wholesale trade (0.5% m/m) and the transportation sector (0.2% m/m) also recorded gains despite coinciding with the Canada Post strike.

The advanced reading of a slight pullback in growth in November is due in part to a moderation in the oil and gas sector as well as finance and insurance.

Key Implications

Solid October GDP growth combined with upward revisions to the month prior put Canada's economic activity on decent footing to end the year. Early tracking for fourth-quarter GDP suggests trend-like growth (~1.7%), an uptick relative to Q3's more meager gain of just 1%.

The Bank of Canada has cut interest rates by 100 basis points (bps) over their last two meetings. Today's data should assuage fears of excessive downside to Canadian growth in the near-term, which should see the Bank move back to a more measured 25 bps cut at their next policy meeting in January. Looking ahead, more cuts are on the way, with the focus now shifting back to upcoming labour market updates.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0365; (P) 1.0407; (R1) 1.0470; More....

EUR/USD is staying in consolidation above 1.0330 and intraday bias stays neutral for the moment. While stronger recovery cannot be ruled out, outlook will remain bearish as long as 1.0629 resistance holds. Firm break of 1.0330 will confirm decline resumption and target 61.8% projection of 1.0936 to 10330 from 1.0629 at 1.0254, and then 100% projection at 1.0023.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

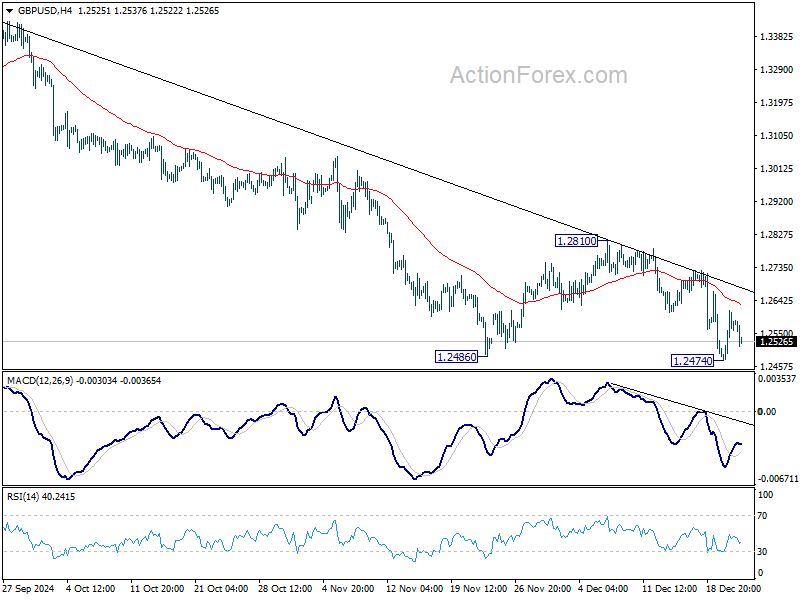

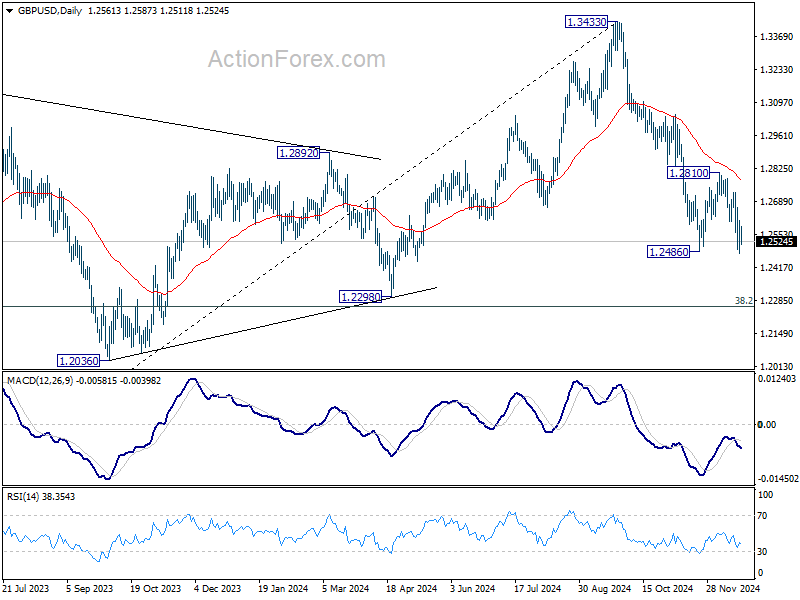

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2491; (P) 1.2553; (R1) 1.2630; More...

GBP/USD is staying in consolidations above 1.2474 temporary low and intraday bias remains neutral. Outlook will stay bearish as long as 1.2810 resistance holds. On the downside, break of 1.2474 will resume the fall from 1.3433 to 1.2298 cluster support zone.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

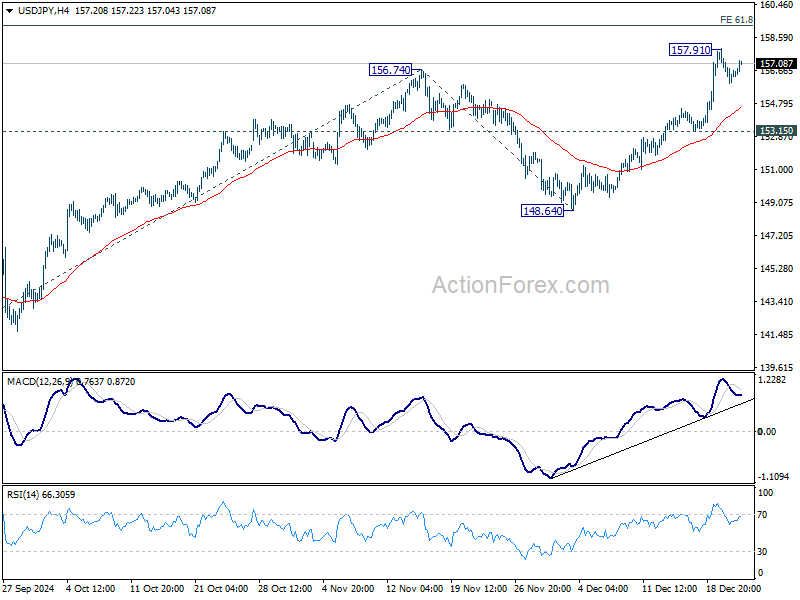

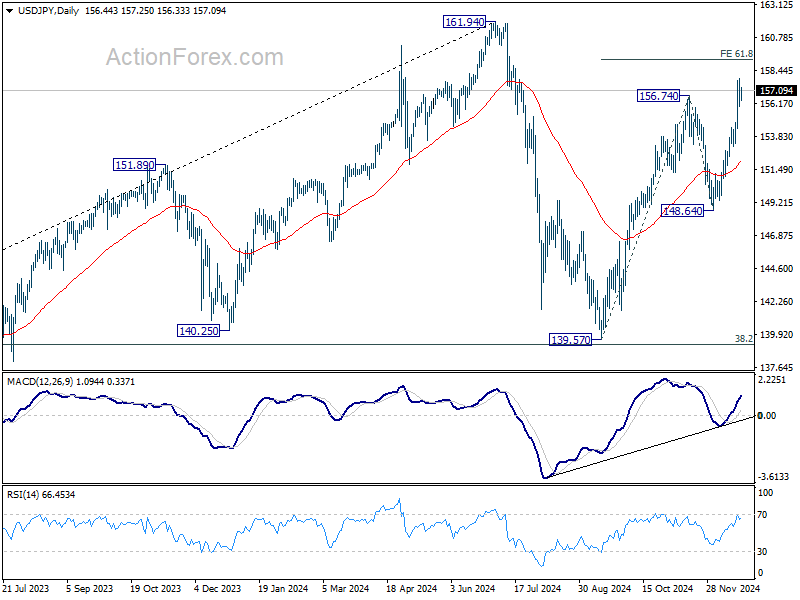

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.64; (P) 156.78; (R1) 157.61; More...

USD/JPY is staying in consolidation below 157.91 temporary top and intraday bias stays neutral. Deeper pull back cannot be ruled out, but outlook will stay bullish as long as 153.15 support holds. On the upside, break of 157.91 will resume the rally from 139.57 to 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

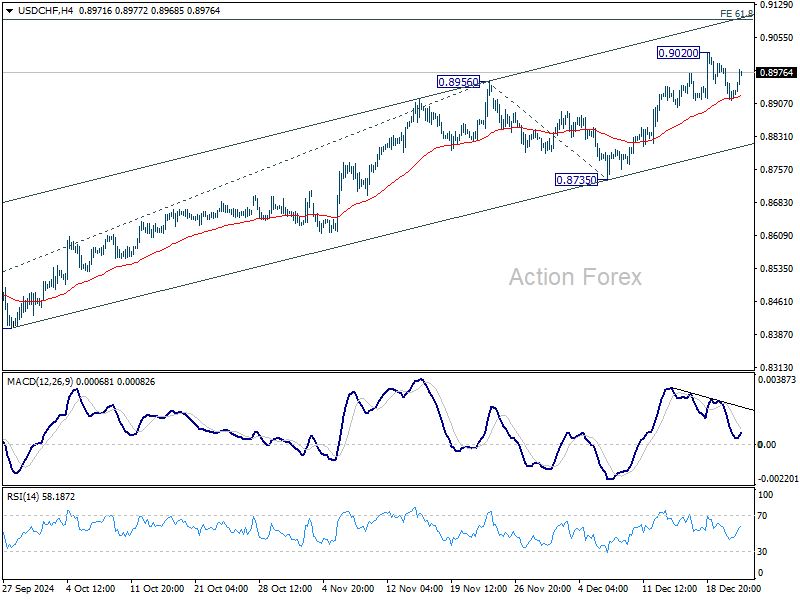

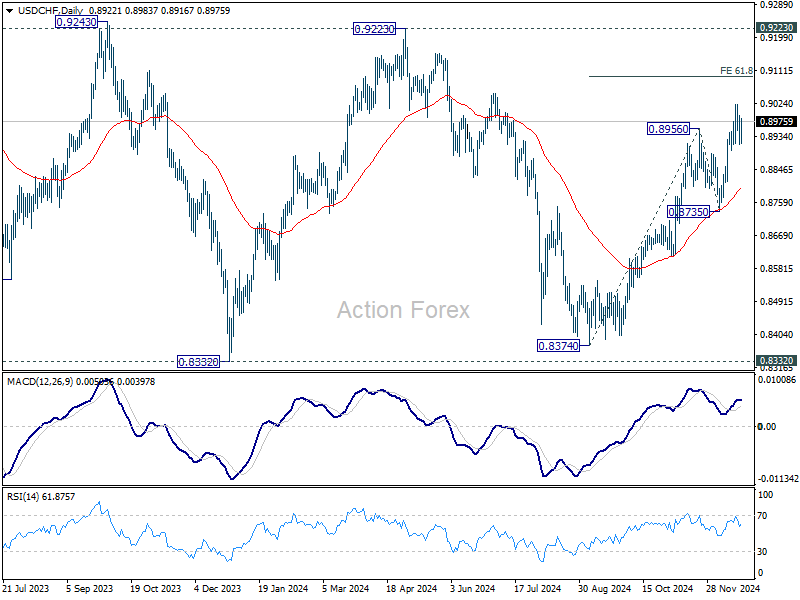

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8898; (P) 0.8946; (R1) 0.8979; More…

USD/CHF bounces after drawing support from 55 4H EMA, but stays below 0.9020 temporary top. Intraday bias remains neutral at this point. While deeper pull back might be seen, downside should be contained above 0.8735 support to bring another rally. Above 0.9020 will resume the rise from 0.8374 and target 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

Dollar Firm Despite Durable Order Miss, Aussie Awaits RBA Minutes

Dollar edged higher in subdued holiday trading, maintaining its recent strength but staying within a narrow range below last week’s highs against major currencies. Markets largely brushed aside the disappointing US durable goods orders data, as the series is known for its volatility. Moreover, traders are prioritizing labor market and consumption trends, which Fed views as more significant for its policy decisions for the moment.

Canadian Dollar Showed little reaction to the better-than-expected October GDP growth, as concerns about sustained economic strength linger. November’s advance estimate pointed to a contraction, reinforcing the overall sluggish outlook. BoC has shifted into a measured phase of easing, where further rate cuts are evaluated on a meeting-by-meeting basis. While policymakers have signaled a slower pace of reductions in 2025, uncertainty remains around the overall depth and timing of further easing, keeping CAD on the defensive.

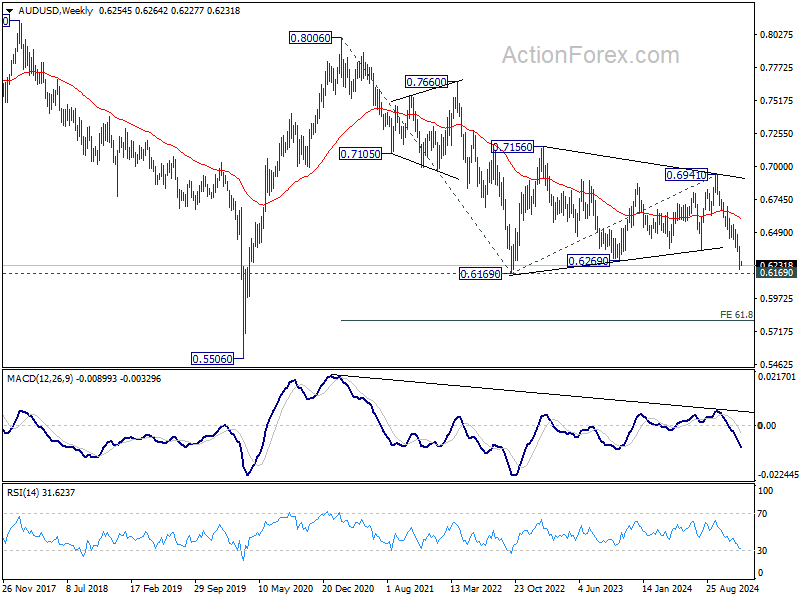

Looking ahead to the Asian session, RBA's December meeting minutes will be a focal point. RBA’s latest dovish shift has raised speculation that policymakers are moving closer to rate cuts, though recent data suggests that easing is not yet imminent. Traders will scrutinize the minutes for details on the board’s reasoning for the pivot and the conditions that could prompt the first cut.

Technically, AUD/USD is quickly approaching 0.6169 key support after last week's downside acceleration. For now, given the light economic calendar at this year period, it's unlikely for the pair to break through this support yet. Indeed, less dovish that expected RBA minutes might help AUD/USD for a bounce. Yet, the medium term down trend is expected at a later stage, probably in later January after Australia's Q4 CPI is published. Any bounce in the near term could be viewed as selling possibilities.

In Europe, at the time of writing, FTSE is up 0.12%. DAX is down -0.14%. CAC is down -0.07%. UK 10-year yield is up 0.034 at 4.543. Germany 10-year yield is up 0.025 at 2.312. Earlier in Asia, Nikkei rose 1.19%. Hong Kong HSI rose 0.82%. China Shanghai SSE fell -0.50%. Singapore Strait Times rose 0.87%. Japan 10-year JGB yield rose 0.0136 to 1.069.

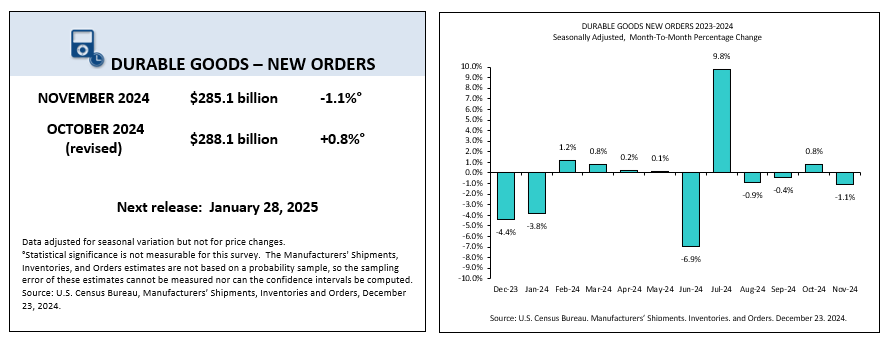

US durable goods orders slump -1.1% mom, transportation sector leads decline

US durable goods orders dropped -1.1% mom in November to USD 285.1B, significantly missing market expectations of a -0.3% mom decline. This also marks the third decline in the last four months.

Excluding transportation, orders edged down -0.1% mom to USD 189.6B, while orders excluding defense fell -0.3% mom to USD 267.4B. The transportation equipment category, which has also fallen in three of the past four months, accounted for the largest share of the decline, with a -2.9% mom drop to USD 95.5B.

Canada’s GDP beats Oct expectations, but Nov decline looms

Canada’s GDP rose 0.3% mom in October, surpassing expectations of 0.2% mom, with 12 out of 20 sectors contributing to the growth.

This marked a rebound for the goods-producing industries, which expanded by 0.9% mom after four months of contraction, driven primarily by mining, quarrying, and oil and gas extraction.

The services-producing industries edged up by 0.1% mom, supported by growth in real estate and rental and leasing, which saw its fifth consecutive month of expansion.

However, preliminary data for November suggests a -0.1% mom contraction in real GDP, with declines in mining, quarrying, and oil and gas extraction, as well as transportation, warehousing, and finance and insurance. These losses were partly offset by gains in accommodation and food services and continued strength in real estate and rental and leasing.

ECB’s Lagarde: Inflation target within reach, services inflation still stubborn

In an interview with the Financial Times, ECB President Christine Lagarde expressed optimism about nearing the inflation target.

She remarked that ECB is "very close" to declaring that inflation has been "sustainably" brought back to its 2% medium-term target.

The latest inflation reading of 2.2% reflects the success of ECB’s restrictive monetary policy. However, she highlighted persistent concerns in the services sector, where inflation remains high at 3.9%, describing it as "not budging much" despite showing slight signs of decline.

On the topic of US tariff threats, Lagarde emphasized the economic risks of retaliatory trade measures, stating, "Retaliation was a bad approach." She warned that tit-for-tat trade conflicts could harm the global economy.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8898; (P) 0.8946; (R1) 0.8979; More…

USD/CHF bounces after drawing support from 55 4H EMA, but stays below 0.9020 temporary top. Intraday bias remains neutral at this point. While deeper pull back might be seen, downside should be contained above 0.8735 support to bring another rally. Above 0.9020 will resume the rise from 0.8374 and target 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

Dollar: Slowing Momentum, Same Direction

Stock market sentiment is moving out of the extreme fear zone it plunged into last week, and the dollar has paused its strengthening. Friday’s CPI report came in slightly weaker than average forecasts, reducing the fear of future Fed monetary policy.

Traders probably assumed that the Fed had better information about recent inflationary trends, which caused the sell-off in US equities to accelerate and expand. However, Friday’s data eased the pressure, allowing the indices (except for Russell2000) to begin to recoup losses. The dollar index took a step back, returning below 108, while EURUSD bounced above 1.04 and GBPUSD above 1.25.

One can understand the change in tone from Fed members, as the Personal Consumption Price Index accelerated to 2.4% y/y against 2.3% in October and a low of 2.1% in September. The Fed’s preferred inflation gauge showed gains of 2.8% y/y in November and October. That, too, is an acceleration from June’s 2.6%, the lowest in this cycle. On the other hand, it is lower than the 2.9% y/y anticipated.

Favourable vibes were reinforced by the University of Michigan report, which showed inflation expected in a year at 2.8% vs. the first estimate of 2.9% and the same expectations but accelerating from 2.6% previously.

Friday’s data triggered short-term profit-taking in dollar long positions. The effect is unlikely to be long-lasting, affecting the intensity of the current trend but not the direction. Inflation remains above target, accelerating instead of slowing. US economic activity is currently better than many peers, keeping the balance in favour of higher interest rates compared to other G10 currencies.

Simply put, fundamentals continue to point to the potential for a stronger dollar, bringing it closer to parity with the euro in the next couple of weeks and into the 0.95 area by the end of Q1 2025. The dollar index would then return to the 2022 highs, entering the 112-115 territory.

US durable goods orders slump -1.1% mom, transportation sector leads decline

US durable goods orders dropped -1.1% mom in November to USD 285.1B, significantly missing market expectations of a -0.3% mom decline. This also marks the third decline in the last four months.

Excluding transportation, orders edged down -0.1% mom to USD 189.6B, while orders excluding defense fell -0.3% mom to USD 267.4B. The transportation equipment category, which has also fallen in three of the past four months, accounted for the largest share of the decline, with a -2.9% mom drop to USD 95.5B.

Canada’s GDP beats Oct expectations, but Nov decline looms

Canada’s GDP rose 0.3% mom in October, surpassing expectations of 0.2% mom, with 12 out of 20 sectors contributing to the growth.

This marked a rebound for the goods-producing industries, which expanded by 0.9% mom after four months of contraction, driven primarily by mining, quarrying, and oil and gas extraction.

The services-producing industries edged up by 0.1% mom, supported by growth in real estate and rental and leasing, which saw its fifth consecutive month of expansion.

However, preliminary data for November suggests a -0.1% mom contraction in real GDP, with declines in mining, quarrying, and oil and gas extraction, as well as transportation, warehousing, and finance and insurance. These losses were partly offset by gains in accommodation and food services and continued strength in real estate and rental and leasing.