Sample Category Title

CAC Shrugs off Solid French Industrial Production, Draghi Speech Next

The CAC is unchanged in the Wednesday session, as the index is trading at 5,395.50.On the release front, French data was better than expected. Industrial production posted a gain of 2.0%, above the estimate of 1.2%. France's trade deficit improved to EUR -5.4 billion, better than the forecast of EUR -5.9 billion. The markets are keeping a close eye on ECB President Mario Draghi, who will speak about monetary policy in the Dutch House of Representatives. On Thursday, the US releases PPI, an important inflation indicator.

The eurozone has posted stronger numbers in the first quarter, and this has included industrial better production and manufacturing numbers in France and Germany. In France, industrial production jumped 2.0% in March, ending a streak of three consecutive declines. The Markit France Manufacturing PMI rose to 55.1 in April, its highest level since 2011. German industrial production in March declined 0.4%, but this was just a blip, as industrial production in the first quarter posted a respectable gain of 1.6%. German Factory Orders came in at 1.0%, above the forecast of 0.7%. An improvement in global economic conditions has boosted the demand for Eurozone exports, notably cars and machinery. A weak euro has made European exports more attractive and helped boost the manufacturing sector. The German economy will get a report card on Friday, with the release of Preliminary GDP for the first quarter. The markets are predicting a gain of 0.6%. A better than expected GDP report could shake the DAX out of its slumber and push the index to higher levels.

Donald Trump unconventional style has caused consternation and uneasiness in the markets, but his latest move could turn into a political earthquake. Trump abruptly fired FBI director James Comey on Tuesday, stunning the political establishment in Washington. Comey, who has been conducting an investigation into possible collusion between Trump and Russia during the presidential campaign, clearly has been a thorn in Trump's side. The White House has claimed that it fired Comey over his handling of an email scandal involving Hillary Clinton, but the move has been roundly condemned by the Democrats, and some key Republicans have also voiced opposition as well. The political firestorm could heat up further, with calls in Congress to appoint a special prosecutor into Trump's connections with Russia. Has Trump gone one step to far? The dollar has already recorded some losses since the firing, and this latest controversy could cause some jitters among investors and send the stock markets downwards.

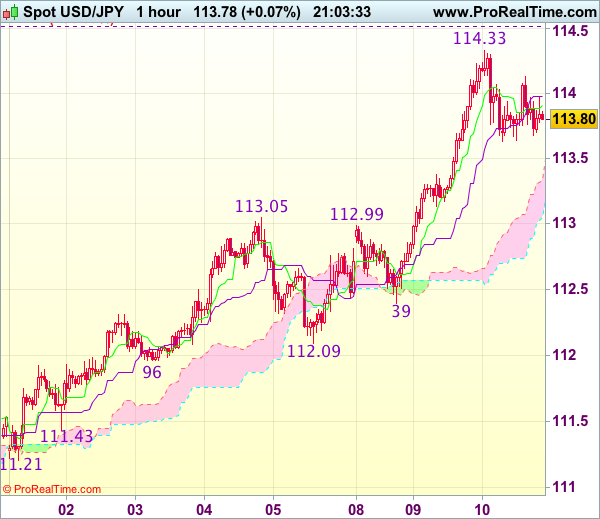

Trade Idea Update: USD/JPY – Buy at 113.25

USD/JPY - 113.82

Original strategy :

Buy at 113.35, Target: 114.45, Stop: 113.00

Position : -

Target : -

Stop : -

New strategy :

Buy at 113.25, Target: 114.45, Stop: 112.90

Position : -

Target : -

Stop : -

Dollar’s retreat after rising to 114.33 suggests consolidation below this level would be seen and pullback to 113.50 cannot be ruled out, however, reckon 113.30-35 would limit downside and bring another rise later, above said resistance at 114.33 would extend recent upmove to 114.50-55 (100% projection of 108.13-111.78 measuring from 110.87), however, near term overbought condition should limit upside to 114.75-80 and price should falter below 115.00, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as 113.25-35 should contain downside. Only below previous resistance at 113.05 would defer and suggest top is formed, bring correction of recent upmove to 112.70-80 but reckon support at 112.39 would remain intact.

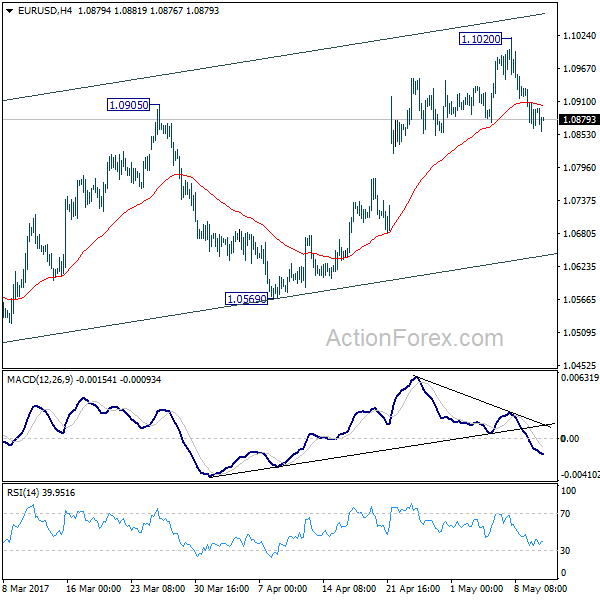

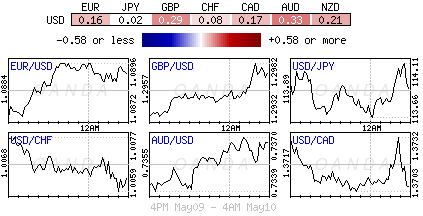

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0846; (P) 1.0890 (R1) 1.0916; More....

Intraday bias in EUR/USD remains mildly on the downside for the moment. A short term top is in place at 1.1020 on bearish divergence condition in 4 hour MACD. Deeper decline would be seen back to 55 day EMA (now at 1.0757) first. As noted before, rise from 1.0339 is seen as a corrective move. Break of 55 day EMA will affirm the case that such correction is completed and bring deeper decline to 1.0569 for confirmation. Above 1.1020 will extend such corrective rise instead.

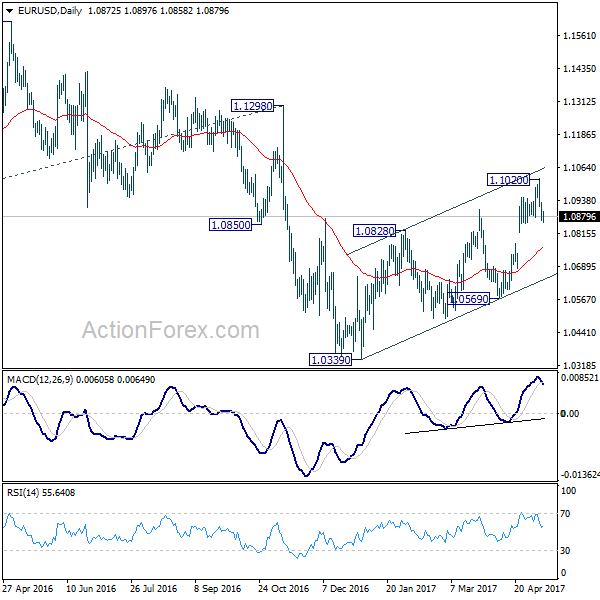

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate long term reversal.

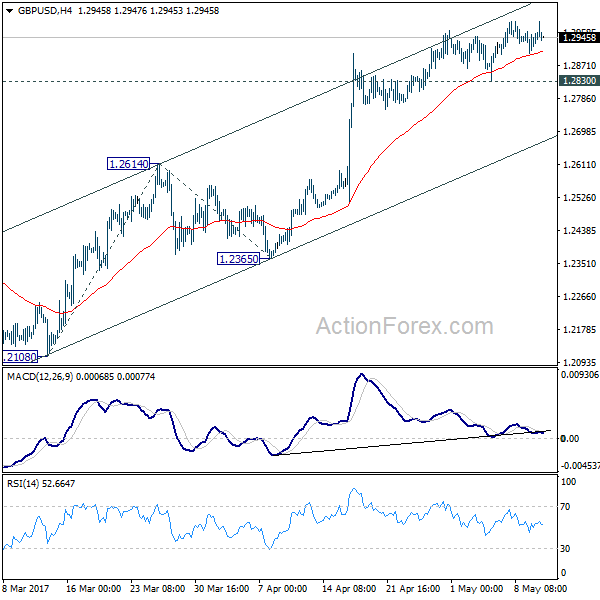

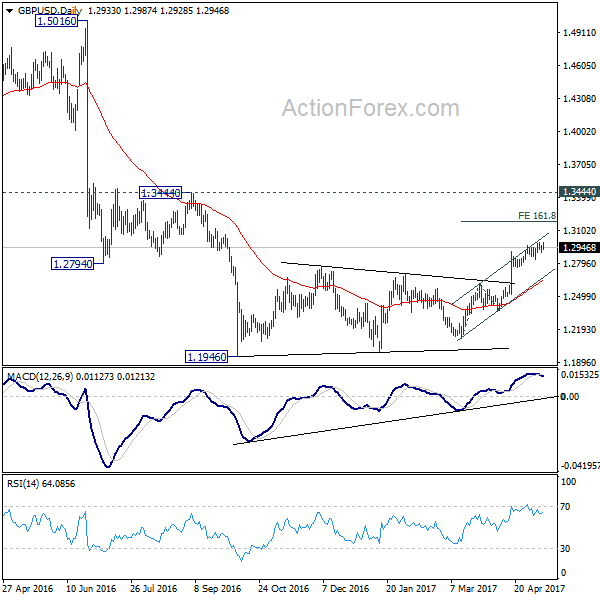

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2904; (P) 1.2932; (R1) 1.2962; More...

No change in GBP/USD's outlook for the moment. With 1.2830 minor support intact, further rise is still in favor. Current rise could target 161.8% projection of 1.2108 to 1.2614 from 1.2365 at 1.3184. At this point, price actions from 1.1946 are still interpreted as a correction pattern. Therefore, we'd expect strong resistance below 1.3444 to bring larger down trend resumption. On the downside, break of 1.2830 support will indicate short term topping. In such case, intraday bias will be turned back to the downside for 1.2614 support.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

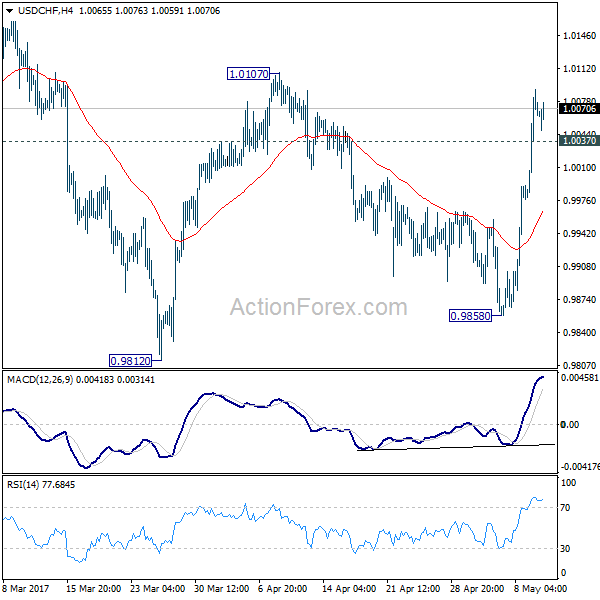

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0000; (P) 1.0045; (R1) 1.0118; More.....

Intraday bias in USD/CHF remains on the upside for 1.0107 resistance. Current development revived the case that correction from 1.0342 is already completed at 0.9812. Break of 1.0107 will bring a retest on 1.0342 high. On the downside, below 1.0037 minor support will turn bias neutral and bring consolidation first before staging another rise.

In the bigger picture, we're still maintaining that firm break of 1.0342 key resistance is needed to confirm underlying bullish momentum in the pair. However, the corrective nature of the fall from 1.0342 is starting to give the medium term outlook a bullish favor. Hence, in stead of looking for topping signal around 1.0342, we'd now pay closer attention to upside acceleration as USD/CHF approaches this level again.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.30; (P) 113.82; (R1) 114.50; More...

USD/JPY is losing some upside momentum as seen in 4 hour MACD. But with 113.04 minor support, intraday bias remains on the upside for the moment, for 115.49 resistance next. Outlook remains unchanged that correction from 118.65 has completed with three waves down to 108.12. Break of 115.49 will resume larger rally from 98.97 to 125.85 high. On the downside, below 113.04 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Dollar Rally Slows on Concern Trump’s Firing of FBI Comey Would Delay Tax Reforms

Dollar rally lost some momentum as markets are concerned that US President Donald Trump's firing of FBI Director James Comey could delay his tax reform. In a controversial move, Trump abruptly fired Comey who oversaw an FBI investigation into Trump's tie with Russia during last year's election campaign. Trump's tax reform was originally targeted at approval by the Congress by August. It was already delayed after the healthcare act failure. Markets are concerned that there will be more distraction to Trump ahead and further slow down the progress on tax reforms.

Also there are concerns that Trump's move would further reduce the support from fellow Republicans. Some prominent ones like Senator Jeff Flake said he cannot find any rationale for doing so. Armed Services Chairman John McCain said the removal of Comey confirmed the "need and urgency" for a special congressional investigation on Russia's interference in the election. A former chief White House ethics lawyer to George W Bush also criticized the case as an "abuse of power".

ECB Study: High labor market slack caps wage growth

According to a ECB study, wage growth has been unexpectedly weak and unemployment in higher than what the official data suggest. The adjusted labor market slack is around 15%, well above the official 9.5% unemployment rate. The study noted that "in France and Italy, broader measures of labour market slack have continued to increase throughout the recovery, while in Spain and in the other euro area economies, they have recorded some recent declines, but remain well above pre-crisis estimates." And, "the level of the broader indicator of labour underutilisation is still high, and this is likely to continue to contain wage dynamics."

BoJ might release calculations on impact of stimulus exit

BoJ Governor Haruhiko Kuroda said today that BoJ might release the details of the study of stimulus withdrawal and the impact on its balance sheet. And he emphasized that "it is very important to explain in easy-to-understand terms how monetary policy could affect the BOJ's financial health". Regarding monetary policies, Kuroda said that he's "not thinking about changing the policy mix right now". And "the amount of our bond purchases may vary depending on financial market conditions at the time. But this has no implications for monetary policy going forward." Regarding the economy, Kuroda said that "while global economic growth is gaining momentum, various uncertainties remain".

In the summary of opinions of BoJ meeting, board members believed that current massive policy accommodations are warranted because of downside risks from overseas. Nonetheless, as export and production outlook improved, it was appropriate to raise economic assessment.

China CPI accelerated

China's headline CPI accelerated to 1.2% yoy in April, up from 0.9% a month ago, as mainly driven by the recovery of food disinflation. Food price contracted -3.5% yoy, following a -4.4% drop in March. Non-food inflation rose to 2.4% yoy in April from 2.3% a month ago. Core inflation (excluding food and energy) improved to 2.1% yoy from 2% in March. Such level should be in line with the government's target. PPI moderated to 6.4% in April from 7.6% in March. The deceleration came in more than expectations. A key contributor to the slowdown was commodity prices which slowed further in April as low base effects dissipated. Global prices also pulled back after the strong rally earlier in the year. More in China's PPI Inflation Fell Further From High Level.

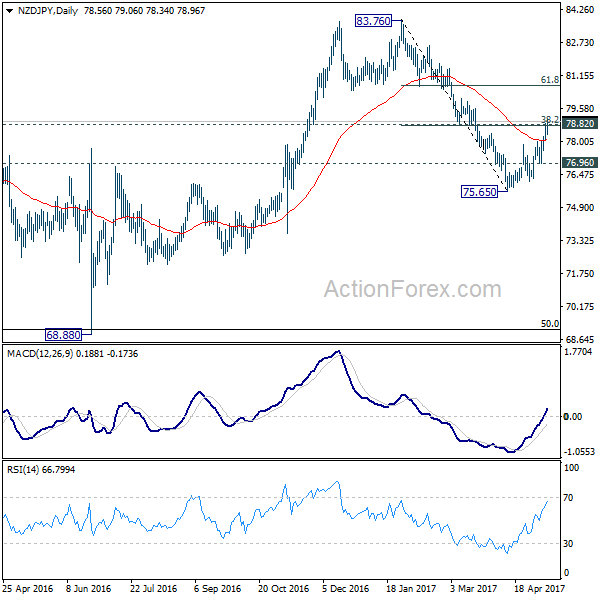

Kiwi extends rally ahead of RBNZ

RBNZ rate decision will be a focus in the upcoming Asian session. The central bank is widely expected to keep interest rate unchanged at 1.75%. New Zealand Dollar strengthens broadly this week as markets are expecting an upbeat statement by RBNZ after recent economic data. In particular, headline inflation already jumped to 2.2% yoy. And, some economists expected inflation to stay above 2% level through 2017 and 2018. Opinions are divided on when RBNZ would hike, ranging from Q1 in 2018 to Q4 in 2018.

NZD/JPY's rally extended to as high as 79.06 this week. Upside acceleration and break of 78.82 cluster resistance (38.2% retracement 83.76 to 75.65 at 78.74 suggests that fall fro 83.76 is completed at 75.65. It's early to say whether rise from 75.65 is resuming medium term rebound from 68.88, or a part of the consolidation pattern from 83.76. In both case, NZD/JPY should now target 61.8% retracement at 80.66 next.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.30; (P) 113.82; (R1) 114.50; More...

USD/JPY is losing some upside momentum as seen in 4 hour MACD. But with 113.04 minor support, intraday bias remains on the upside for the moment, for 115.49 resistance next. Outlook remains unchanged that correction from 118.65 has completed with three waves down to 108.12. Break of 115.49 will resume larger rally from 98.97 to 125.85 high. On the downside, below 113.04 minor support will turn bias neutral and bring consolidations before staging another rally.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. It's uncertain whether it's completed yet. But in case of another fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77 to bring rebound. Meanwhile, break of 115.49 resistance will extend the rise from 98.97 to retest 125.85. Overall, rise from 75.56 is still expected to resume later after the correction from 125.85 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions at April 26-27 Meeting | ||||

| 1:30 | CNY | CPI Y/Y Apr | 1.20% | 1.10% | 0.90% | |

| 1:30 | CNY | PPI Y/Y Apr | 6.40% | 6.70% | 7.60% | |

| 5:00 | JPY | Leading Index Mar P | 105.5 | 105.5 | 104.8 | |

| 12:30 | USD | Import Price Index M/M Apr | 0.50% | 0.20% | -0.20% | |

| 14:30 | USD | Crude Oil Inventories | -0.9M | |||

| 18:00 | USD | Monthly Budget Statement Apr | -176.2B | |||

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |

EURUSD: Bearish, Declines Further

EURUSD: With the pair extending its downside pressure on Tuesday, further weakness is likely in the days ahead. Resistance comes in at 1.0900 level with a cut through here opening the door for more upside towards the 1.0950 level. Further up, resistance lies at the 1.1000 level where a break will expose the 1.1050 level. Conversely, support lies at the 1.0800 level where a violation will aim at the 1.0750 level. A break of here will aim at the 1.0700 level. Its daily RSI is bearish and pointing lower suggesting further weakness. All in all, EURUSD faces further bear threats.

Pick Your Poison: What is the Market Focusing On?

Wednesday May 10: Five things the markets are talking about

There are a number of moving parts that are currently keeping capital markets on their toes - China, ECB, Fed, N. Korea, Trump and OPEC.

Investors have been extra focused on China after a selloff erased at least -$500B from the value of stocks and bonds since mid-April, amid policy makers' moves to crack down on leverage. Data overnight showed that prices slowed more than expected (see below).

When is the ECB going to start rate normalization? They have to get their timing correct. Today's ECB unemployment figures support the case for ongoing stimulus. A broader measure of regional unemployment shows that around +15% of eurozone workers are "unemployed or underemployed," which suggests wages and inflation are unlikely to pick up for some time. A June Fed hike is almost fully priced in.

North Korea says it's going ahead with its sixth nuclear test, who is pulling the strings?

President Trump fires FBI Director Comey, citing his handling of the investigation into Hillary Clinton's email server - what's the impact on the FBI probe into possible ties between the Trump campaign and Russia?

OPEC still does not have a consensus to maintain last November's production cuts into H2, 2017. But, is it coming soon?

1. Global bourses see mixed results

Overnight, Asian stocks resumed a rally as Hong Kong shares jumped to a two-year high, while European shares are mixed and U.S futures see red as President Trump fired FBI Director James Comey.

In Hong Kong, the Hang Seng rose +0.5%, to its highest level since July 2015. The Hang Seng China Enterprises Index jumped +0.9%, rallying for a third consecutive day, while the Shanghai Composite Index retreated -0.9% to its lowest level since October.

In Japan, the broader Topix index increased +0.2% and the Nikkei 225 rose +0.3%. Gains were limited by yen's rally overnight on tentative 'risk aversion' trading (¥113.83).

In South Korea, the Kospi slid -1% after surging +2.3% on Monday, the most since September 2015.

In Europe, indices are trading mixed this morning with notable weakness in the Swiss SMI and out-performance in the FTSE on energy prices. Corporate earnings look set to dominate the Eurostoxx 600.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx50 -0.3% at 3640, FTSE +0.1% at 7347, DAX -0.1% at 12742, CAC-40 -0.2% at 5388, IBEX-35 -0.6% at 10985, FTSE MIB -0.4% at 21398, SMI -0.8% at 9047, S&P 500 Futures -0.2%

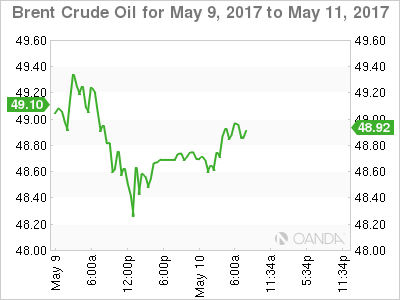

2. Crude oil prices find support on potential cut extension, gold higher

Ahead of the U.S open, oil prices are on the rise on rumoured reports that Saudi Arabia would cut supplies to the region. Prices are also supported by a larger than expected fall in yesterday's API crude inventories last week, down -5.8m barrels compared with market expectations for a -1.8m barrels decline.

Brent futures are up +19c, or +0.4%, at +$48.92 a barrel - they fell -1.2% yesterday. U.S West Texas Intermediate (WTI) crude is up +23c, or +0.5%, at +$46.11 a barrel.

Note: WTI also fell -1.2% Tuesday, and the closing price for both contracts was the second lowest since Nov. 29, the day before OPEC agreed to cut production during H1, 2017.

There are reports this morning that State-owned Saudi Aramco will reduce oil supplies to Asian customers by about -7m barrels in June, as part of OPEC's agreement to reduce production.

Capping price gains is higher crude output from the U.S, particularly shale producers.

Note: U.S crude production is expected to rise by more than previously expected in 2017 to +9.31m bpd from +8.87m bpd in 2016.

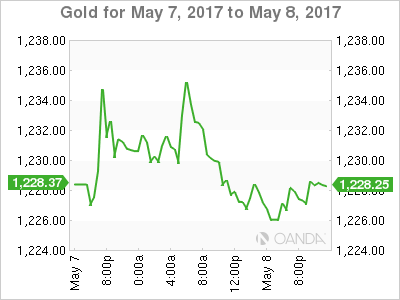

Gold (+0.2% at +$1,223.30 an ounce) has edged off the previous day's two-month low this morning as U.S President Trump's abrupt firing of FBI chief James Comey hit equities, but expectations of further Fed rate hike is likely to limit gains by the metal.

3. Global yields little changed, focus on Central Banks

With Euro go-political risk abating somewhat since the weekend, dealers and investors are returning to fundamentals and central bank monetary policy for guidance.

The markets main focus is on the Fed and the ECB. The current odds for a Fed hike next month are +83%, however, for Draghi, the question is not about rate hikes, but about reducing stimulus.

Central banks may be best placed to understand other central banks, and if so, the ECB is not expected to be winding down its stimulus programs anytime soon. According to today's minutes from its April policy meeting, Sweden's Riksbank expects the "ECB to continue to pursue a very expansionary monetary policy in the foreseeable future." And it's for this reason why the Riksbank is prepared to extend its own bond-buying program to the end of 2017.

Yields on eurozone government bonds are declining slightly in early Wednesday trading, but a major drop seems unlikely due to supply of new debt this week. Not only are sovereigns, including Germany, in the market to place new debt, but so to are agencies. German 10-year Bunds yields have fallen -1 bps to +0.43%.

Elsewhere, the yield on 10-year Treasury notes fell -1 bps to +2.39%, while Australian 10-year yields dropped -3 bps to +2.66%.

Note: The Bank of England (BoE) publishes its interest-rate decision and quarterly Inflation Report Thursday.

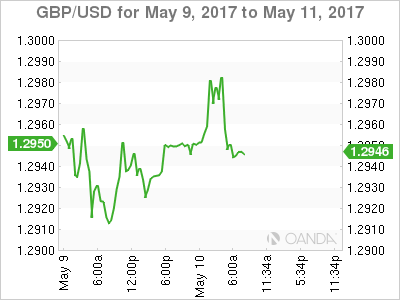

4. Sterling hovers atop key resistance, a break could trigger more gains

Ahead of the U.S open, the pound trades up +0.37% at £1.2983 outright, hovering just below the psychological £1.30 handle, a level not traded in eight-months.

Of late, sterling has been benefitting as "weaker short-positions" are been forced to close out. Ahead of the BoE rate announcement and inflation quarterly report tomorrow, do not be surprised to see more positions unwind ahead of time.

Any hints from Governor Carney that they are considering raising rates would be sterling positive. More market stop-loss orders could be executed when £1.3000 is finally breached with momentum.

Elsewhere, the FX markets saw little volatility in the session. A slightly softer USD was attributed to President Trump's firing of his FBI director, the yen (¥113.83) found some support, while the EUR continues to hover just under the psychological €1.09 area (€1.0873).

5. China CPI rises to 3-month highs while PPI growth slows

China inflation data has also propped up sentiment, with Consumer Price Index rising to three-month highs and beat market expectations on a month-over-month (+0.1% vs. -0.3% prior) and year-over-year basis (+1.2% vs. +1.1%e).

Note: The main driver of the pick-up was an increase food price inflation, which rose from -4.4% y/y to -3.5% on the back of pick-ups in fruit and vegetable price inflation. Non-food inflation also edged up from 2.3% y/y to 2.4%, but this was largely due to a seasonal increase in tourism cost inflation.

China's Producer Price Index (+6.4% vs. +6.7%e) was positive for the eight consecutive month, but the rate of increase was smallest in four-months as the recent free-fall in metal prices is also reflected in the results.

Note: The driver was a drop in industrial commodity prices, with factory gate prices declining most among steel and oil producers.

GBP-AUD Likely to See Some Volatility in the Next Few Days

- Surpise Sterling success and a slip in Australian Dollar - interesting times ahead?

- GBP-AUD likely to see some volatility in the next few days

- Australia unlikely to make further interest rate cuts

Theresa May calling the snap election helped boost the Pound and with the Conservative Party ahead by 22 points in the polls, that's certainly supporting Sterling. The uncertainty of a general election will usually weaken a currency, but the unanimous nature of the polls suggesting a sizeable Tory majority and the repercussions for a stronger hand in the Brexit negotiations have benefitted the Pound. This week we have "Super Thursday" – so called because a large number of economic indicators for the UK are released on the same day:

- We'll hear from the Bank of England (BoE), who will vote on interest rates; in the last meeting, one member of the Monetary Policy Committee (MPC) voted for an interest rate hike, which boosted the Pound. If there's a change to the voting, and we more in favour of an interest rate increase, that will add strength to the Pound. On the other hand, if 9-0 committee members vote in favour of no change of interest rates, then expect the Pound to drop a little.

- The quarterly inflation report will also be released; this will be market moving and may well see the BoE downgrade growth forecasts for the UK for 2017 (currently forecast at 2.0%), which would weaken the Pound.

- Also featuring on "Super Thursday" will be UK manufacturing and industrial production data and trade balance figures. The forecasts are good, so that may counterbalance any Sterling weakness.

GBP-AUD likely to see some volatility in the next few days

With all this key economic data and potential for market movement, it may be worth converting a portion of GBP into AUD beforehand, just in case GBP falls back and signals a short term top on GBP-AUD.

Technically, GBP-AUD had been trading in the 1.5920 to 1.7170 range since October 2016, and so when the breakout happened last April, it was a decisive break. Currently, the Sterling-Australian Dollar exchange rate is heading up towards the next level of resistance at 1.7800 but this week's slew of UK data may see the Pound stumble. On the daily and weekly charts, this currency pair is looking a bit overstretched, so it is possible that this rally could be exhausted. With this in mind, consider reducing your risk and/or trading a portion of your funds.

Australia unlikely to make further interest rate cuts

Over in Australia, the Reserve Bank of Australia (RBA) has left interest rates on hold at 1.5% in recent months and their policy statement remains neutral – it's unlikely that they'll cut interest rates any further. We anticipate that the next move could be higher but that may be sometime in 2018. What has triggered the fall in the Australian Dollar over the last two months is the drop in commodity prices, particularly iron ore – Australia's largest export – and copper, which has meant the Australian Dollar is one of the worst performers of the year, thus far. Building approvals and retail sales data both came in below expectations, which added to the downward pressure on the AUD; but with the GBP-AUD currency pair looking overstretched and with traders focusing on the UK's Super Thursday, the currency pair will likely tread water over the next couple of days.

Guidance for exchanging GBP-AUD

Hedging your bets is always a sensible strategy, particularly when there are warning signs that GBP-AUD may be topping out. You can take advantage of the current exchange rates by converting a portion of your funds on either a spot contract or fixing the rate for a later delivery on a forward contract with the view to converting more if and when GBP-AUD breaks through the next level of resistance at 1.7800.