Sample Category Title

USD/JPY Hovers Above Support Ahead of French Election

Monday April 17, USD/JPY hit the lowest level of 108.12 since November 15, as a result of the strengthening of the yen on markets' safe haven demand.

However, the bearish attempt was held above the 108.00 support line since Monday.

On the 4-hourly chart, the 10-SMA crossed over the 20-SMA from below on Wednesday, the bulls have broken the downtrend line resistance, indicating the bearish momentum has been waning.

The daily Stochastic Oscillator reading is around 30, suggesting a rebound.

The resistance level is at 109.30, followed by 109.70 and 110.00.

The support line is at 108.65, followed by 108.30 and 108.00.

Keep an eye on the US Treasury Secretary Mnuchin's speech at 18:15 BST today, it will likely affect USD crosses.

Most importantly, be aware that the first round of the French presidential election will be held this Sunday April 23.

The recent polls showed a tightening race between the top four candidates: Macron, Le Pen, Fillion and Jean-Luc Melenchon. The difference of votes between the 4 candidates is less than 3% which poses more uncertainty to the election.

The consensus is that the Centrist Macron and the far-right wing Le Pen would likely get into the second round, then Macron would likely win the final vote.

However, be aware that if the result of the first-round surprises the markets, especially if the far-right wing Le Pen's share of vote sees a large increase, it will likely push safe havens further up. In this situation, USD/JPY will likely fall and test supports again.

CAC Moves Higher as Macron Takes Lead in French Election Countdown

The CAC 40 has improved on Thursday and is currently trading at 5043.00. It's a quiet day on the release front, with no major events on the schedule. Eurozone Consumer Confidence is expected to remain unchanged at -5 points. Friday will be busier, as France and Eurozone publish PMIs from the services and manufacturing sectors. The markets are expecting these indicators to point to expansion.

It's the final countdown before the French election, with the first round of voting slated for April 23. This election is one of the tightest in decades, with the four front-runners clustered within a few percentage points. Given the closeness and unpredictability of the election, it's no surprise that final opinion polls before the vote are moving markets. European stock markets have gained ground on Thursday following a Harris Interactive opinion poll, which shows centrist Emmanuel Macron gaining ground, with 25% of the vote. Far-right candidate Marine Le Pen follows with 22%. Next are Republican candidate Francois Fillon and left-wing candidate Jean-Luc Melenchon, both tied at 19%. Le Pen and Melenchon are running on an anti-EU platform, so the markets are cheering for Macron and Fillion. We can expect more volatility as we near Election Day, and French banks will be manned throughout Sunday night in order to respond quickly to developments in the currency markets as the votes are counted.

Eurozone consumer inflation has been gaining strength in recent months, but softened in March. Final CPI slipped to 1.5%, compared to 2.0% a month earlier. The index climbed to 2.0% in February, which is the ECB's inflation target. This had led to speculation that the ECB might have to consider tightening its monetary policy, either by lowering interest rates or tapering its asset-purchase program (QE). The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank will have to reconsider that date or taper the program if growth and inflation numbers in the Eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with the upcoming election in France and a September election in Germany.

What's next for Janet Yellen & Co.? The Federal Reserve has sent out broad hints that it plans to raise rates gradually in 2017, but the timing and number of moves in store remains uncertain. The Fed has broadly hinted that it plans two more rate hikes this year, but there have been calls from some Fed policymakers for three more hikes. However, soft retail sales and CPI numbers in March are likely to make the Fed more dovish, and on Tuesday, the Atlanta and New York Federal Reserve lowered their outlook for US economic growth for the first quarter. The Fed can point to a labor market that is close to capacity as well as strong consumer confidence, but surprisingly, this has not translated into stronger consumer spending, a key driver of economic growth. The odds of a June hike have slipped to 46% according to the CME Group, down sharply from 65% in early April.

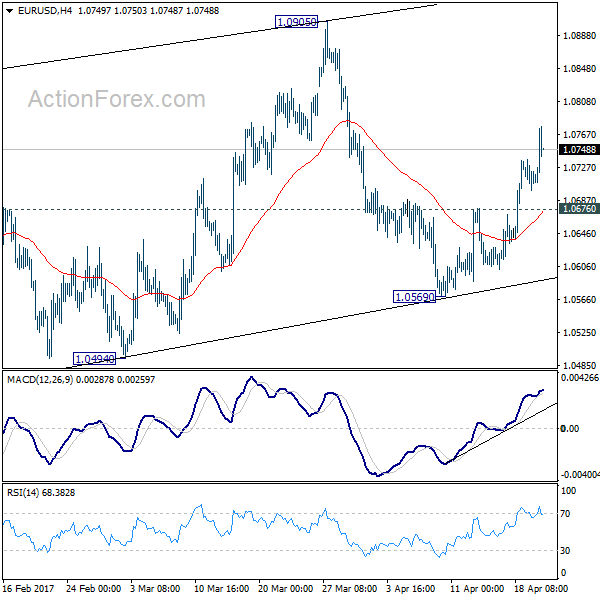

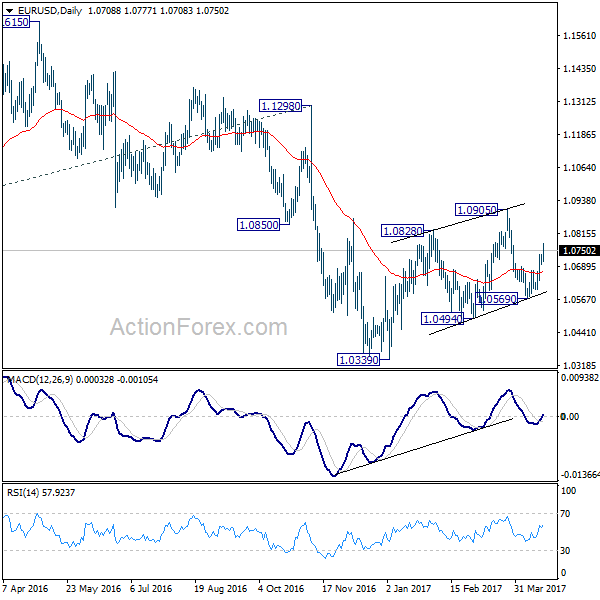

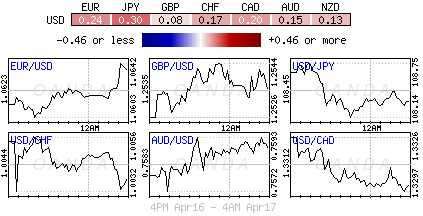

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0694; (P) 1.0715 (R1) 1.0732; More....

EUR/USD's rise from 1.0569 continues today and reaches as high as 1.0777 so far. Intraday bias remains on the upside for 1.0905 resistance and above. Nonetheless, choppy rise from 1.0339 is still seen as a correction. Hence, we'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0676 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Dollar Under Pressure Against Euro and Swiss Franc, Yen Soft

Dollar trades mixed in early US session with notable weakness against Euro and Swiss Franc. The forex markets are relatively steady elsewhere, with Aussie and Loonie trading to recover while yen extends its pull back. US initial jobless claims rose 10k to 244k in the week ended April 15, slightly above expectation of 241k. Continuing claims dropped -49k to 1.98m in the week ended April 8, lowest since April 2000. Philly Fed survey dropped to 22.0 in April, down from 32.8, below expectation of 25.6. In other markets, US futures point to a mildly higher open and stocks could pare back some of yesterday's steep loss. Gold is hovering around 1280 while crude oil is heading to test 50 psychological level.

Fed's Beige Book: Modest to moderate expansion in all districts

Released yesterday, Fed's latest Beige Book indicated that economic activity increased in each of the twelve Federal Reserve Districts between mid-February and the end of March. The the pace of expansion was "equally split between modest and moderate". On the labor market situation, the report noted that it "remained tight, and employers in most Districts had more difficulty filling low-skilled positions, although labor demand was stronger for higher skilled workers". It added that "modest wage increases broadened" with "bigger increases for workers with skills that are in short supply". A larger number of firms noted "higher turnover rates and more difficulty retaining workers". Yet, the wage pressure remained modest and has not yet significantly passed to selling prices. As the report suggested, "input prices generally increased at a modest rate and outpaced gains in selling prices, which rose only slightly".

UK PM May got parliament backing for snap election

UK Prime Minster Theresa May won backing from the parliament for the snap election on June 8. The bill was passed with overwhelming 522 to 13 votes. The Parliament will now formally be dissolved on May 3. May said that she won't be doing TV debates as she believes in "campaigns where politicians actually go out and about and meet with voters. And she wants the election to focus on Brexit and gives her "the strongest possible hand" for negotiation with EU. She also noted that the election is "a choice between strong and stable leadership under the Conservatives or weak and unstable coalition of chaos led by Jeremy Corbyn."

ECB officials sound cautious on stimulus exit

ECB governing council member Benoit Coeure said yesterday that policy makers are "very, very serious about the forward guidance". Coeure referred to the communicates that ECB will keep buying assets "until December or later if necessary, that rates will remain low". Coeure sees no reason to change the sequence. Another governing council member Francois Villeroy de Galhau said that the "current monetary policy stance remains fully appropriate based on current information." ECB chief economist Peter Praet said that "risks are still tilted to the downside" in the medium term. Released from Eurozone, German PPI rose 0.0%, 3.1% yoy in March.

Australia business confidence unchanged

Australia NAB quarterly business confidence was unchanged at 6 in Q1. NAB chief economist Alan Oster noted that employment expectations hit multi-year highs in short and medium term. And the set of data "points to a tighter labour market than the ABS unemployment rate is currently suggesting." Also, capex plans reached highest level since 2011. Thus, with lack of inflation pressure, RBA would stand pat for an "extended period".

New Zealand CPI jumped

New Zealand CPI rose 1.0% qoq in Q1, up from prior quarter's 0.4% qoq, and beat expectation of 0.8% qoq. Kiwi jumped briefly on talk that RBNZ is falling behind the curve. And the central bank could be forced to raise interest rates. Overnight index swaps are pricing in 80% chance of a rate hike within the coming 12 months.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0694; (P) 1.0715 (R1) 1.0732; More....

EUR/USD's rise from 1.0569 continues today and reaches as high as 1.0777 so far. Intraday bias remains on the upside for 1.0905 resistance and above. Nonetheless, choppy rise from 1.0339 is still seen as a correction. Hence, we'll pay attention to topping signal above 1.0905 again, as we'd expect larger down trend to resume later. On the downside, break of 1.0676 minor support will turn intraday bias back to the downside for 1.0569 instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 1.00% | 0.80% | 0.40% | |

| 23:50 | JPY | Trade Balance (JPY) Mar | 0.17T | 0.61T | 0.68T | 0.61T |

| 01:30 | AUD | NAB Business Confidence Q1 | 6 | 5 | 6 | |

| 06:00 | EUR | German PPI M/M Mar | 0.00% | 0.20% | 0.20% | |

| 06:00 | EUR | German PPI Y/Y Mar | 3.10% | 3.10% | ||

| 12:30 | USD | Initial Jobless Claims (APR 15) | 244K | 241K | 234K | |

| 12:30 | USD | Philly Fed Manufacturing Index Apr | 22 | 25.6 | 32.8 | |

| 14:00 | EUR | Eurozone Consumer Confidence Apr A | -5 | -5 | ||

| 14:00 | USD | Leading Indicators Mar | 0.20% | 0.60% | ||

| 14:30 | USD | Natural Gas Storage | 10B |

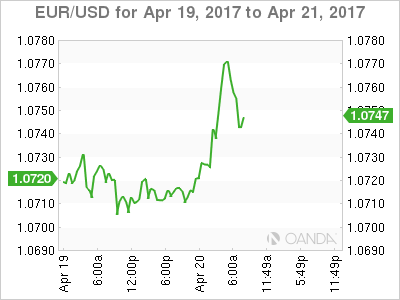

It is all about the Euro

The Euro was elevated to levels not seen since March 2017 at 1.0777 during Thursday's trading session, as participants discarded short positions ahead of the first round of the French Presidential elections this weekend. Although the Euro has continued to display resilience against pre-election jitters, investors should be under no illusion that this has to do with a change of sentiment. With political uncertainty still a recurrent theme in Europe, the incredible rebound that the Euro has staged may be utilized by longer-term bears to send prices lower.

The latest opinion poll figures that indicate a fierce competition will be taking place between the four candidates in this first round have simply added to anxieties, as speculators ponder over which of them will be seizing the title of President. Although Centrist Emmanuel Macron has been labeled as the favorite to become the next French President, it must be kept in mind that millions of French voters remain undecided, fueling concerns of a potential election shocker. The threat of Marine Le Pen winning the election remains live, and the risks associated with such a victory may ensure further downside pressures on the Euro.

From a technical standpoint, the EURUSD is challenging the 1.0750 level on the daily charts. A solid daily close above this level could open a path towards the next level of interest at 1.0820. If bulls fail to maintain control above 1.0750, then the Euro could edge back down towards 1.0685.

Dollar remains on the back foot

A flurry of disappointing U.S economic data and rising concerns over Trump's ability to push through with the phenomenal tax cuts he promised during his election campaign has left the Greenback vulnerable to steep losses. With the Trump rally displaying signs of exhaustion, speculations over the Federal Reserve raising U.S interest rates in June has taken a hit, with probability falling to 46.6%. Investors remain on edge over the heated tensions between the U.S and North Korea, which may have complimented to the downside. From a technical standpoint, the Dollar Index remains pressured on the daily charts, with a break below 99.50 opening a path towards 99.00.

French Fears has Asset Classes on Edge

Thursday April 20: Five things the markets are talking about

Current price action suggests that investors continue to pare back 'risk-on' market positions ahead of this weekend's first round of the French Presidential election.

Geopolitical worry over North Korea, a faltering U.S economy and a snap U.K election are also consuming investor's mindsets.

A race too close to call - every French poll for the past month has shown the independent Macron and the National Front's Le Pen taking the top two-spots. Macron is then expected to easily win the May 7 runoff by a +25% margin.

However, both front-runners have been steadily slipping over the past fortnight, and Republican Francois Fillon and Communist-backed Jean-Luc Melenchon are now within striking distance.

Nevertheless, Millions of French voters remain undecided, making this the least predictable vote in France in decades.

1. Stocks stick to tight ranges

Global stocks eked out small gains overnight as investors resisted risky bets ahead of the first round of the French presidential election.

In Japan, the broader Topix index added +0.1%, bringing its weekly gain to +0.9%, while the Nikkei 225 share average ended -0.01% lower.

In Hong Kong, the Hang Seng advanced +0.7%, while down-under the Aussie S&P/ASX 200 Index climbed +0.3%, while South Korea's Kospi index was up +0.5%.

In China, the Shanghai Composite was little changed, after four days of losses brought it to the lowest level since early February.

In Europe, equity indices are trading generally higher as market participants continue to focus on the upcoming French presidential elections. Banking stocks are supporting the Eurostoxx, while energy, commodity and mining stocks are trading lower on the FTSE 100.

U.S stocks are set to open in the black (+0.3%).

Indices: Stoxx50 +0.5% at 3,440, FTSE -0.1% at 7,105, DAX +0.2% at 12,034, CAC-40 +0.9% at 5,048, IBEX-35 +0.9% at 10,461, FTSE MIB +0.4% at 19,907, SMI +0.4% at 8,564, S&P 500 Futures +0.3%

2. Oil prices claw back losses, but oversupply still weighs, gold higher

Oil prices have regained some ground overnight after yesterday's steep losses, as Kuwait said it expected an OPEC-led effort to cut supplies would be extended into H2.

Brent crude futures are at +$53.34 per barrel, up +41c, or +0.77% from last nights close. U.S. West Texas Intermediate (WTI) crude futures are up +32c, or +0.63%, to +$50.76 a barrel.

Also supporting prices was yesterday's data from the EIA, which showed a reduction in commercial U.S crude stocks, which fell by -1m barrels last week to +532.34m barrels.

Note: Crude prices fell -3.5% Wednesday after the EIA reported surging gasoline inventories as well as another rise in U.S crude oil production to +9.25m bpd, up almost +10% in 12-months.

Compliance between OPEC and Non-OPEC members on agreed upon production cuts was over +90% in March.

Gold prices are holding firm (unchanged at +$1,278.74 per ounce) ahead of the U.S open after falling as much as -1% yesterday, with tensions surrounding North Korea and the upcoming French presidential election driving safe-haven demand.

Yesterday, the yellow metals drop was its worst one-day fall in four-weeks.

3. Global yield curves remain flatter

The U.S 10-year Treasury yield has tumbled about -40 bps from its 2017 peak in March. Despite the plunge in yields, bond bears still expect U.S yields to back up towards that +3% handle by Q4. They don't believe that the current patch of 'softer' U.S data is weak enough to throw the Fed off its game plan to normalize rates.

However, one risk for that higher yield call is for both far right and far left candidates in the French Presidential election to enter into the second round.

If the market gets its baseline scenario - Le Pen vs. Macron - in the second round on May 7, Le Pen is unlikely to significantly increase her support beyond her base, and voters of the moderate left and right are expected to merge around Macron. This scenario should be a plus for the EUR (€1.1000'ish) and have Bund yields unwinding the past months risk premium rather quickly.

The yield on U.S 10's has slid -1 bps to +2.20% after a +5 bps advance Wednesday. Most other eurozone bond yields are little changed on the day.

4.'Big' dollar remains under pressure

The USD remains soft against the G10 FX pairs that started with last Friday's soft retail sales and CPI data from the U.S.

The EUR has rallied +0.5% to a three-week high atop of €1.0777, shrugging off political uncertainty before this weekend's first-round French presidential elections. Election risk seems to be more evident in Scandinavian and central European currencies. The EUR is also being supported by the markets doubts about the global reflation trade.

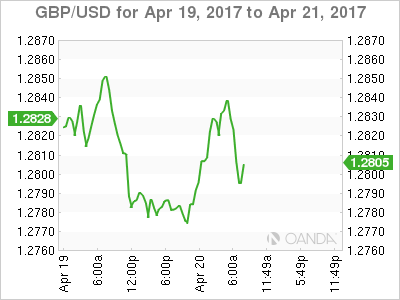

GBP (£1.2836) remains supported by the view that early elections in the U.K diminishes prospects of a messy exit from the E.U - however, someone needs to tell that to the European side!

Elsewhere, the NZD (NZ$0.7036) is firmer after data overnight showed that New Zealand Q1 CPI annual reading remained within the target range for the second consecutive month and the highest level since Q3 2011.

5. German March PPI unchanged on month, +3.1% on year

Data this morning showed that German producer prices remained unchanged last month, while the annual rate stabilized at February's level.

As expected, factory gate prices rose +3.1% in March y/y., while the annual rate matched the strongest annual rise in over five-years.

Note: Following the pattern of previous months, energy prices (+4.5% y/y) continue to have the biggest impact on the overall index.

Ex-energy prices, producer prices rose +0.3% on the month and increased by +2.6% on the year.

Sterling Reacts Positively as Polls Put Conservatives ahead

- UK election to go ahead on June 8th

- Sterling reacts positively as polls put Conservatives ahead

- US Unemployment Claims later this afternoon

Yesterday was once again dominated by the political scene, with the Election Bill surpassing the two thirds needed in the commons by a considerable margin of 522 - 13 votes. This officially means the election will go ahead on June 8th and campaigning can start. The bookmakers are seeing it as a Conservative landslide with labour in such disarray under Jeremy Corbyn, despite him putting on a brave face. Sterling has reacted positively as polls put the Conservatives ahead, as a potential landslide win is perceived to help the UK's Brexit negotiation stance, mainly because Prime Minister, Theresa May, will be able to control the more Eurosceptic fringe of the Conservative party. The odds of a "softer" Brexit and an easier path through the Commons have increased. The Pound did strengthen throughout the day, although came off the highs before the close.

Last night, we also had the release of the Beige Book in the United States, which is monitored closely, as it summarises current economic conditions and is only released eight times a year. The key points were that the economy grew at a modest to moderate pace and wages are looking more positive, which is being viewed as an optimistic sign for another Federal Reserve rate hike this year.

Looking to today, as the political landscape unfolds, the main news will be Bank of England Governor, Mark Carney, speaking in Washington at around 10:30 GMT. Carney will be speaking at the Institute of International Finance event and this will be watched closely for any monetary and political speak, especially with what has gone on over the last few days. We also get US Unemployment Claims data at 13:30 GMT, which will be closely watched by the market.

Badly explained film plots

The Shining: A family's first Airbnb experience goes very wrong

The Chronicles of Narnia: Kid comes out of the closet

The Lord of the Rings: Group spends nine hours returning jewellery

DAX Pushes Above 12,000 As Macron Takes Lead In French Opinion Poll

The DAX has posted gains in the Thursday session, climbing above the symbolic 12,000 level. Currently, the DAX is trading at 12,015.50. On the release front, there are no major events in the eurozone. German PPI dipped to 0.0%, short of the estimate of 0.2%. On Friday, Germany and the Eurozone release services and manufacturing PMIs, which are expected to indicate expansion.

Market focus is fixed on the French presidential election, with the first round of voting slated for April 23. This election is one of the tightest in decades, with the four front-runners clustered within a few percentage points. Given the closeness and unpredictability of the election, it's no surprise that final opinion polls before the vote are moving markets. A Harris Interactive opinion poll published on Thursday showed centrist Emmanuel Macron gaining ground, with 25% of the vote. Far-right candidate Marine Le Pen follows with 22%. Next are Republican candidate Francois Fillon and left-wing candidate Jean-Luc Melenchon, both tied at 19%. Le Pen and Melenchon want to hold a referendum on French membership in the EU, so the markets are clearly more comfortable with Macron and Fillion, and this latest poll has boosted the stock markets. We can expect more volatility as we near Election Day, and French banks will be staffed throughout Sunday night in order to respond quickly to developments in the currency markets after the election results.

Eurozone consumer inflation softened in March, but matched the forecast. Final CPI slipped to 1.5%, compared to 2.0% a month earlier. The indicator has been steadily rising, and climbed to 2.0% in February, which is the ECB's inflation target. This had led to speculation that the ECB might have to consider tightening its monetary policy, either by lowering interest rates or tapering its asset-purchase program (QE). The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank could opt to bring up that date or taper QE if growth and inflation numbers in the Eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with upcoming elections in France and Germany.

Eurozone consumer inflation has been gaining strength in recent months, but softened in March. Final CPI slipped to 1.5%, compared to 2.0% a month earlier. The index climbed to 2.0% in February, which is the ECB's inflation target. This had led to speculation that the ECB might have to consider tightening its monetary policy, either by lowering interest rates or tapering its asset-purchase program (QE). The ECB's asset-purchase program is scheduled to remain in place until December, although the central bank could opt to bring up that date or taper the program if growth and inflation numbers in the Eurozone are unexpectedly strong. There are also political considerations at play, as the ECB is reluctant to make any significant monetary moves with upcoming elections in France and Germany.

The Federal Reserve has sent out broad hints that it plans to raise rates gradually in 2017, but the timing and number of moves in store remains uncertain. The Fed has broadly hinted that it plans two more rate hikes this year, but there have been calls from some Fed policymakers for three more hikes. However, soft retail sales and CPI numbers in March are likely to make the Fed more dovish, and on Tuesday, the Atlanta and New York Federal Reserve lowered their outlook for US economic growth for the first quarter. The Fed can point to a labor market that is close to capacity as well as strong consumer confidence, but surprisingly, this has not translated into stronger consumer spending, a key driver of economic growth. The odds of a June hike have slipped to 46% according to the CME Group, down sharply from 65% in early April.

Daily Technical Analysis: USD/CAD Bullish Marubozu On Daily Timeframe

The USD/CAD has formed a bullish marubozu (strong momentum candle) on daily timeframe (see the mini daily chart) which marks an uptrend. Retracement towards POC might start at the break of trendline (red). If the price gets to POC (38.2, ATR low, D L4, EMA89) the POC zone should spike the price further up towards D H3 at 1.3513 and D H4/ATR High at 1.3540. Only above 1.3545 we could see 1.3600.

D L3 - Daily Camarilla Pivot (Daily Interim Support)

D H3 - Daily Camarilla Pivot (Daily Interim Resistance)

D H4 - Daily Camarilla Pivot (Strong Daily Resistance)

D L4 - Daily Camarilla Pivot (Very Strong Daily Support)

D L5 - Daily Camarilla Pivot (Strongest Daily Support)

W H5 - Weekly H4 Camarilla (Strongest Weekly Resistance)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Technical Outlook: US Oil – Risk Of Fresh Attempts At $50.00 Support After Correction

US oil holding within narrow daily cloud (spanned between ($50.74 and $51.15) following bounce from Wednesday’s spike low at $ 50.06.

Strong bearish acceleration on Wednesday extended pullback from $50.74 (12 Apr recovery high) and probed below important support at $50.41 (daily Kijun-sen line) and approached psychological $50.00 level. Fall was accelerated by lower than expected draw in oil inventories which showed 1 million barrels draw in the week ending 12 Apr, compared to 1.5 million barrels draw forecast.

In addition, increased production of US shale oil continues to undermine attempts of OPEC to stabilize and boost oil prices by reducing production.

Wednesday’s long bearish daily candle weighs on markets, as oil price was firmly in red for past three days, with weakening daily studies supporting negative scenario.

Corrective bounce is seen limited and should ideally remain under broken 55SMA at $51.55, with extended upticks to be capped by broken 100SMA / daily Tenkan-sen at $51.85/90, ahead of fresh leg lower.

Key supports at $50.00 and $49.62 (Fibo 61.8% of $47.07/$53.74 rally) remain in near-term focus, with sustain break lower to confirm an end of recovery phase from $47.07 and expose next strong support at $48.96 (200SMA).

Res: 51.32, 51.55, 51.90, 52.34

Sup: 50.87, 50.00, 49.62, 48.96