Sample Category Title

Could the “Trump trade” Now Become the “Trump Disappointment”?

Is the Trump honeymoon over? That is the question being asked today after the breaking news late last week and what has dominated attention over the weekend with this being that President Trump was defeated in his quest at replacing Obamacare. The result of the Trump healthcare bill was not in line with market expectations, but more importantly it has made the markets begin to get nervous about what other possible hurdles Trump could potentially face when it comes to implementing other aspects of his campaign agenda.

Truth be told Obamacare was ripped apart from its infancy around the same time it was introduced seven years ago, yet it seems to still be more popular than whatever President Trump and his team proposed to replace it with. If Trump is going to face such opposition with the House of Representatives as he has with healthcare when other proposals are presented, it does make you wonder what could happen when he attempts to push through his proposals on tax reforms and other promises he made during his political campaign.

Investors have certainly priced in huge premiums into the financial markets following the night Trump was declared victorious in the US election based on his campaign promises, but actions speak louder than words and this could be a turning point and investors will need to monitor how the markets react as trading continues to get underway for the new week.

Where does this leave President Trump? Under the spotlight to provide the necessary clarity on his tax reforms plans. Trump has already signalled that he is set to move onto the next phase of his Presidential plan, which is cutting taxes and this is the key contributor to the heavy rally throughout the financial markets. Tax reforms and fiscal stimulus promises also represents a key reason why heavy gains were priced into the markets as investors thought Trump could be good for the US economy, but few people would have thought replacing the unpopular Obamacare would become this complicated and it's unlikely passing tax reforms and other aspects of fiscal stimulus that will increase national debt will be plain sailing.

Dollar slides down the charts

The Dollar has opened the new trading week slipping lower against the overwhelming majority of its trading partners following the doubts settling in that President Trump could face further obstacles when it comes to implementing other aspects of his campaign promises. Risk aversion is somewhat the name of the game taking place, with Gold climbing back towards a three-month high last seen in late February above $1250 and the Japanese Yen once again acting as a trader's best friend in times of market uncertainty. Emerging market currencies are also gaining from the weakness in the US Dollar, and these will be contenders to regain the most ground if the USD does enter a slump with it being well-known that these markets were seen as the most vulnerable to Trump's presidential agenda.

Currencies like the Malaysian Ringgit, Korean Won, Indian Rupee and Chinese Yuan are just some of the many that could benefit from USD buyers taking a spell on the sidelines. The USD Index has closed below the psychological 100 level that was previously viewed as a critical benchmark, meaning this could make technical traders think twice before purchasing the USD on the pullback like they have done in recent months.

Gold gains but Oil resumes its slump

Gold is as you would expect one of the main beneficiaries from the USD weakness, and traders will now be monitoring whether any additional moves towards risk-off from investors and further losses in the equity markets provide the platform for the value of the precious metal to continue its recovery that it has experienced over the first quarter of 2017.

While Gold is one of the commodities that is enjoying consistent buying momentum, Oil is most certainly not and has resumed its weakness into the new trading week despite reports circulating over the weekend that major Oil producing nations will consider extending their recent cuts in production.

GBPUSD and EURUSD benefit from short squeeze

Both the GBPUSD and EURUSD have climbed significantly higher as the markets welcome the new trading week, with the Pound up 1% and the Euro around 0.85 % at the time of writing.

This week represents the week where UK Prime Minister Theresa May is widely expected to invoke the long-awaited Article 50, which in simple terms essentially means delivering a letter to her counterparts in Europe saying I want a divorce. While short options on the Pound are around record levels with the ongoing uncertainty expected with Brexit negotiations, traders need to be careful how they position themselves because further short squeezes on the USD can all of a sudden lead to additional bounces higher on the Pound.

Where does the Eurodollar go from here? It's already climbed to a 2017 high this morning above 1.0895 and above a four-month high, but if it wasn't for the impending political risks in Europe I would personally say that the Euro is the most oversold currency in the developed markets. Ambitious investors who believe the Dollar is set to weaken further could possibly be targeting 1.10.

USD Hits Lowest Level Since November on Trump’s Healthcare Failure

The dollar index slumped to a 4-and-a-half-month low of 98.85 this morning during the European session, US equities also fell, as markets have lost confidence in Trump's administration to fulfil his promises.

Trump's first bill proposal since taking office, to repeal Obamacare and replace it with the American Health Care Act, failed on Friday March 24. This is his second failure following the refugee and immigration travel ban. Not surprisingly President Trump blamed the Democrats for the failure.

On one hand, none of Democrats were willing to support the new healthcare bill. On the other hand, the defections within the Republican party were more than the limit of 22. Even Trump had tried to convince his peers on Friday, clearly his warnings and efforts were not effective.

The failure has put an issue on the spot: compared to the Democratic Party's unity, there seems to be lots of disagreements within the Republican party, and the leadership of Trump and the House Speaker Paul Ryan face severe challenges. The hurdles that Trump's administration will likely face seem to be more than expected.

President Trump now focuses on his next bill proposal: tax reform, which is a more controversial issue. He promised to cut the corporate tax to 15% during the election. His plan is to make up the reduction of government's tax income by the decrease of healthcare spending – not an easy task following last week's failure of the healthcare bill. It is likely the administration will face the same hurdle (Democratic disfavour and Republican disagreements) on the tax reform proposal. Thus, it will be difficult for Trump to keep his promise to reform taxes.

If the tax bill fails to pass the Republican voters' disappointment might be greatly lifted and the party will likely lose some seats in the 2018 election. USD and US equities still face downward pressure on Trump's tax plan uncertainty.

UK Prime Minister, Theresa May, will trigger Article 50 of the Lisbon treaty on Wednesday March 29, starting the 2-year Brexit negotiation process with the EU.

Theresa May will formally notify the EU Council President, Donald Tusk. Tusk is expected to present draft Brexit guidelines to the European Union's 27 member states within 48 hours of the UK triggering Article 50. The member states are expected to hold a Brexit summit within 4-6 weeks. Theresa May's letter, and Donald Tusk's response, will likely give markets more clues about the potential difficulties of the upcoming Brexit procedure.

GBP/USD reached 1.2579 the highest the pair has attained since February 9 mainly because of the weakening of USD. The Scottish parliament will vote on whether to hold a second Scottish independence referendum on Tuesday March 28, which is only one day ahead the triggering of the Brexit process. If the result is to hold a referendum, the proposal will be delivered to the UK parliament for voting. In this situation, it will pose more political uncertainties on the UK's economic prospects and GBP.

UK Q4 GDP final reading will be released this Friday with better-than-expected readings likely providing some support to GBP.

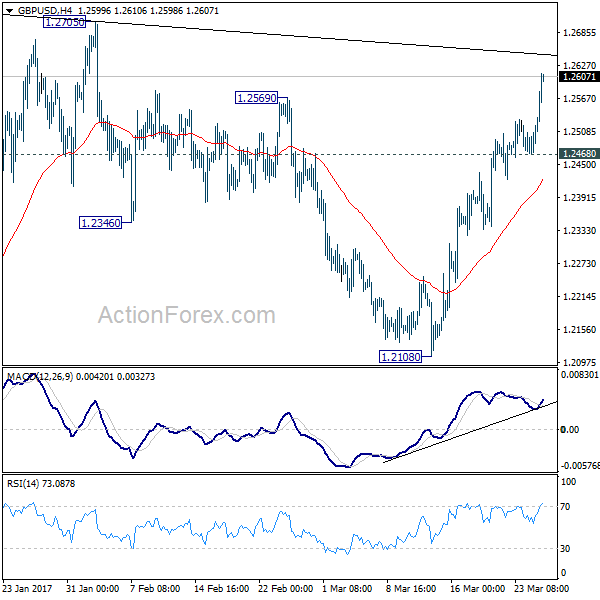

GBP/USD Bulls Test 1.2600 Ahead of Brexit Triggering

This morning GBP/USD reached 1.2597, the highest the pair has attained since February 2, helped by the slump of USD caused by Trump's healthcare bill failure.

GBP/USD has been trading above the downside uptrend line support since mid-March. The significant psychological resistance level at 1.2500 was broken today during early Asian session.

The bulls are currently testing the next significant psychological resistance level at 1.2600.

At present, the price still trades along the upper band of the Bollinger Band indicator, suggesting the trend remains bullish.

The resistance level is at 1.2600, followed by 1.2630 and 1.2650.

The support line is at 1.2550, followed by 1.2530 and 1.2500.

There are two upcoming risk events this week, which will likely have some impact on GBP.

UK Prime Minister, Theresa May, will trigger Article 50 of the Lisbon treaty on Wednesday March 29, starting the 2-year Brexit negotiation process with the EU. Theresa May will formally notify the EU Council President, Donald Tusk. Tusk is expected to present draft Brexit guidelines to the European Union's 27 member states within 48 hours of the UK triggering Article 50.

Theresa May's letter, and Donald Tusk's response, will likely give markets more clues about the potential difficulties of the upcoming Brexit procedure.

The Scottish parliament will vote on whether to hold a second Scottish independence referendum on Tuesday March 28, which is only one day ahead the triggering of the Brexit process. If the result is to hold a referendum, the proposal will be delivered to the UK parliament for voting. In this situation, it will pose more political uncertainties on the UK's economic prospects and GBP.

UK Q4 GDP final reading will be released this Friday with better-than-expected readings likely providing some support to GBP.

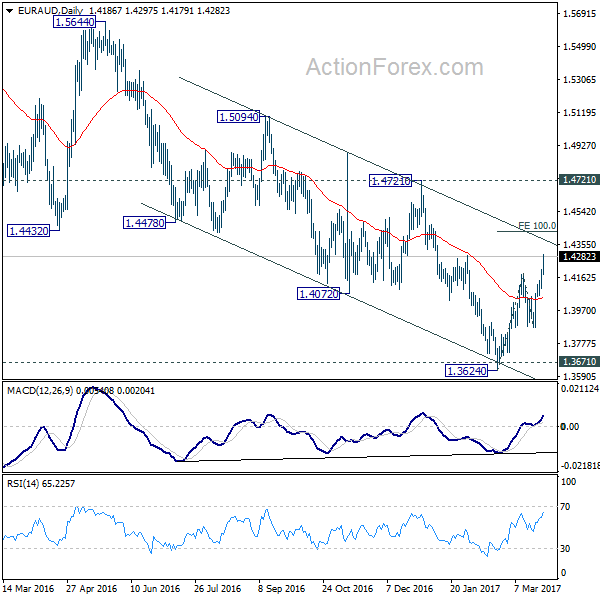

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.4101; (P) 1.4154; (R1) 1.4211; More...

EUR/AUD rises to as high as 1.4297 so far today. Intraday bias remains on the upside. Current rise should target 100% projection of 1.3624 to 1.4183 from 1.3872 at 1.4431 next. Decisive break there will indicate upside acceleration and target 1.4721 key resistance. On the downside, below 1.4148 minor support will turn bias neutral and bring consolidations first before staging another rally.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn focus back to 1.1602 long term bottom.

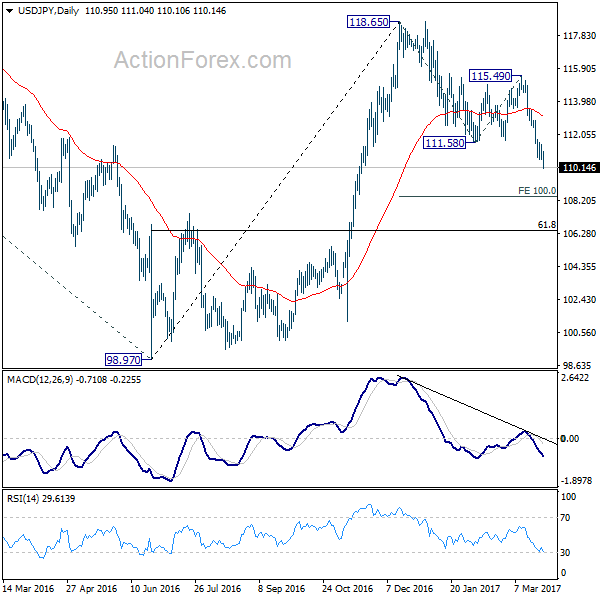

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.79; (P) 111.14; (R1) 111.65; More...

USD/JPY's fall continues today and reaches as low as 110.10 so far. Intraday bias remains on the downside and the fall from 118.65 would target 100% projection of 118.65 to 111.58 from 115.49 at 108.42 and possibly below. On the upside, break of 111.57 resistance is needed to indicate short term bottoming. Otherwise, near term outlook stays mildly bearish in case of recovery.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. sustained trading below 55 week EMA (now at 111.11) will indicates that such consolidation is not completed. And another fall would be seen back to 98.97 as the third leg. In that case, downside would be contained by 61.8% retracement of 75.56 to 125.95 at 94.77 to complete the correction. On the upside, above 115.49 will extend the rise from 98.97 to retest 125.85 first. Overall, up trend from 75.56 is expected to resume after the consolidation from 125.85 completes.

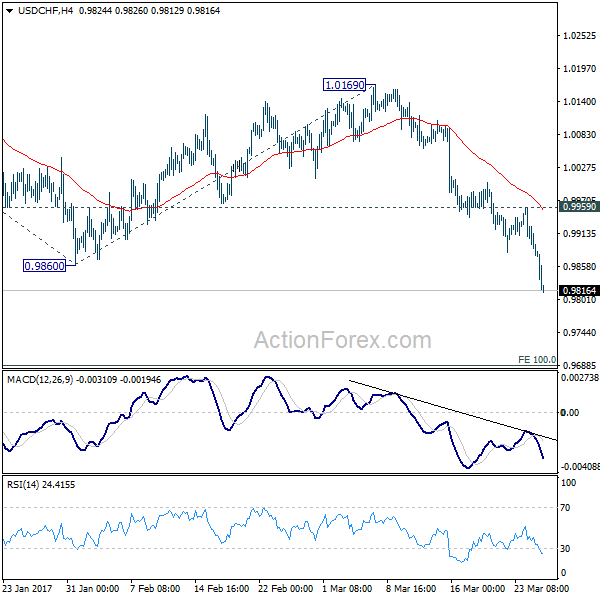

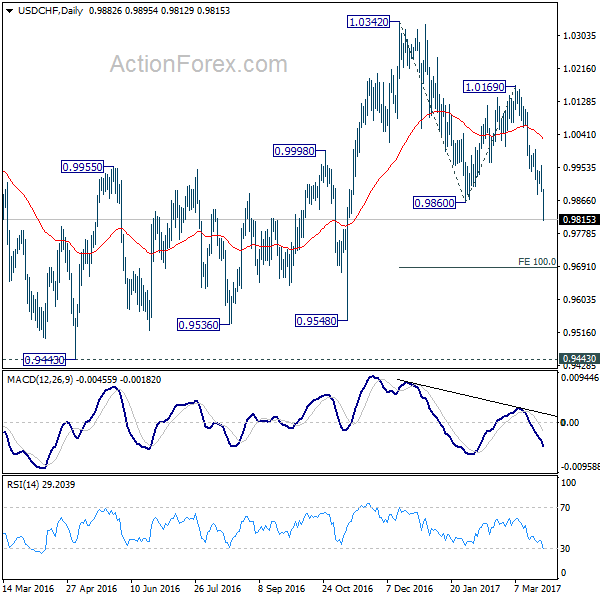

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9881; (P) 0.9920; (R1) 0.9952; More.....

USD/CHF's decline accelerates to as low as 0.9812 so far. Intraday bias remains on the downside. Whole decline from 1.0342 would target 100% projection of 1.0342 to 0.9860 from 1.0169 at 0.9687 and possibly below. On the upside, break of 0.9959 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of deeper fall, we'd expect strong support from 0.9443/9548 support zone.

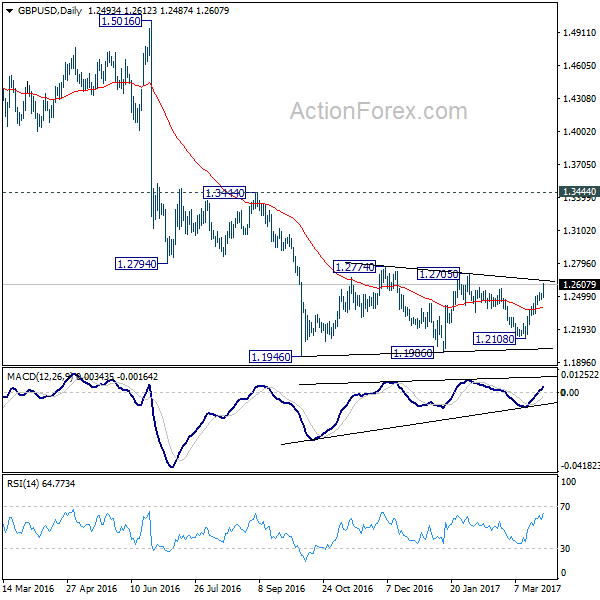

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2453; (P) 1.2487; (R1) 1.2506; More...

GBP/USD's rally accelerates through 1.2569 resistance today and hit as high as 1.2612 so far. Intraday bias remains on the upside for 1.2705/74 resistance zone. Such rise is seen as part of the consolidation pattern from 1.1946. We'd expect upside to be limited by 1.2705/2774 to bring down trend resumption eventually. On the downside, below 1.2422 minor support will turn bias back to the downside for 1.2108 support first. Though, sustained break of 1.2774 will extend the rise towards 1.3444 key resistance level.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

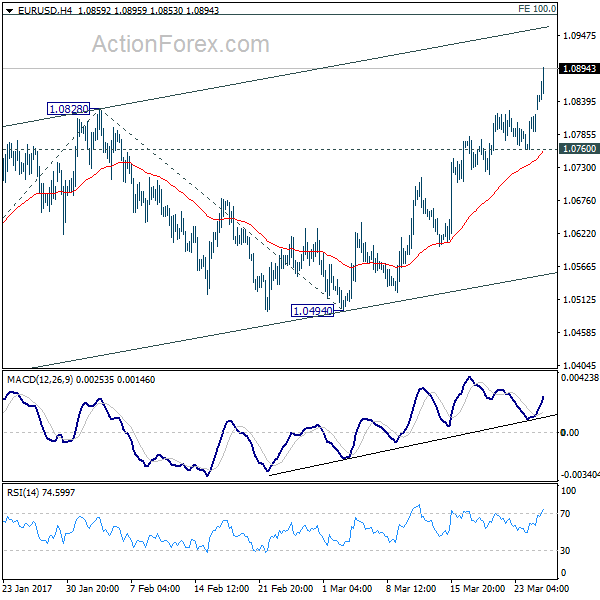

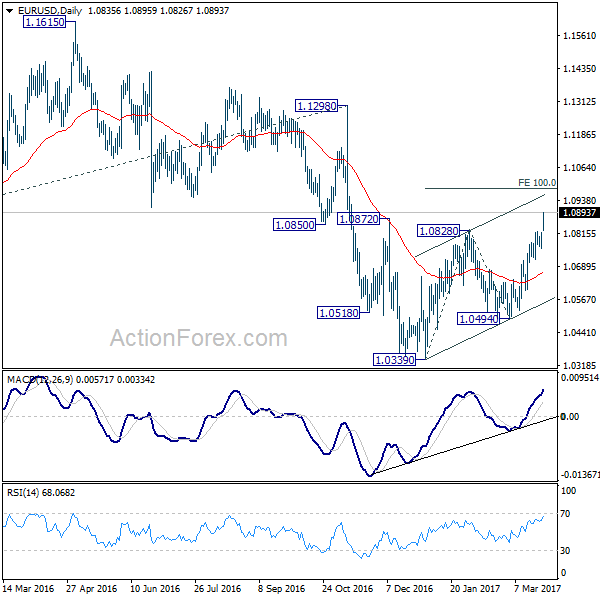

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0764; (P) 1.0791 (R1) 1.0823; More.....

EUR/USD's rally accelerates to as high as 1.0895 so far and intraday bias remains on the upside. Current rise is expected to target 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. At this point, we're still treating rise from 1.0339 as a correction. Hence, we'd expect strong resistance from 1.0983 to limit upside and bring near term reversal. On the downside, break of 1.0760 support will turn bias back to the downside for 1.0494 support. However, firm break of 1.0983 will dampen our view and put focus on 1.1298 key resistance.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Dollar Decline Accelerates as Reverse Trump Trade Intensifies

Dollar's decline accelerates as markets seem to have made up their mind regarding US president Donald Trump's health care act failure. The dollar index is losing -0.7% at the time of writing, diving through 99.23 near term support and hits as low as 98.90 so far. Risk aversion dominates the markets as investors seriously question Trump's ability to push through his policies. Nikkei closed down -1.44% at 18985.59. FTSE, DAX and CAC are trading down -0.8%, -0.95% and -0.45% respectively. US futures point to another three-digit fall in DJIA at open. In the currency markets, Yen and European majors are generally higher with Sterling leading the way. Commodity currencies are broadly under pressured.

Labour demands May's Brexit plan to meet six tests

In UK, Prime Minister Theresa May is going to meet Scotland First Minister Nicola Sturgeon later today. In a speech in Scotland, May said that she would never allow UK to become "looser or weaker" because of Brexit. And she emphasized that when all four nations "works together with determination, we are an unstoppable force." May is expected to discuss with Sturgeon on the topic of another Scottish independence referendum.

May will trigger Article 50 for Brexit negotiation on Wednesday. Ahead of that Labour Party's Keir Starmer demanded May's Brexit plan to meet "six tests" to get the party's support. The tests include "fair migration system for UK business and communities", "retaining strong collaborative relationship with EU", "protecting national security and tackling cross-border crime", "delivering for all nations and regions of the UK", "protecting workers' rights and employment protections", and "ensuring same benefits currently enjoyed within single market.

German Ifo hit near six year high

Germany Ifo business climate rose to 112.3 in March, up from 111.0 and beat expectation of 111.1. That's also the highest reading in nearly six years since July 2011. Current assessment gauge rose to 119.3, up from 118.4 and beat expectation of 118.3. Expectations gauge rose to 105.7, up from 104.0 and beat expectation of 104.3. Ifo president Clemens Fuest noted that "the upwards trend in assessments of the current business situation continues unabated." And, "the business outlook for companies also improved again this month. Also "the upswing in the German economy is gaining impetus." Meanwhile, Ifo economist Klaus Wohlrabe also said that "the political uncertainties don't affect the German economy."

Also from Eurozone, M3 money supply rose 4.7% yoy in February, below expectation of 4.9% yoy.

BoJ opinions: monetary policy based on Japan, not overseas

In Japan, BoJ released summary of opinions from the March 15/16 policy meeting. The document noted that "some market participants argue that the Bank needs to change the monetary policy in response to the rise in the long-term yields overseas." But, majority believed that "monetary policy in Japan should be decided based on Japan's economic activity and prices". Therefore, "it will be a considerable length of time before the Bank will need to change its monetary policy." At the meeting, BoJ held interest rate unchanged at -0.1%. And under the Yield Curve Control framework, BoJ target to guide 10 year yield at around 0%. The annual target of asset purchase was held at JPY 80T.

Also from Japan, corporate serve price index rose 0.8% yoy versus expectation of 0.5% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0764; (P) 1.0791 (R1) 1.0823; More.....

EUR/USD's rally accelerates to as high as 1.0895 so far and intraday bias remains on the upside. Current rise is expected to target 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. At this point, we're still treating rise from 1.0339 as a correction. Hence, we'd expect strong resistance from 1.0983 to limit upside and bring near term reversal. On the downside, break of 1.0760 support will turn bias back to the downside for 1.0494 support. However, firm break of 1.0983 will dampen our view and put focus on 1.1298 key resistance.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions at March 15-16 Meeting | ||||

| 23:50 | JPY | Corporate Service Price Y/Y Feb | 0.80% | 0.50% | 0.50% | |

| 8:00 | EUR | Eurozone M3 Y/Y Feb | 4.70% | 4.90% | 4.90% | |

| 8:00 | EUR | German IFO - Business Climate Mar | 112.3 | 111.1 | 111 | |

| 8:00 | EUR | German IFO - Expectations Mar | 105.7 | 104.3 | 104 | |

| 8:00 | EUR | German IFO - Current Assessment Mar | 119.3 | 118.3 | 118.4 |

Dow Fell Further after Holding in Directionless Mode

Dow fell further on Monday after holding in directionless mode during past three days and hit fresh nearly six-weeks low at 20386, where rising 55SMA offered temporary to renewed bears.

Extended wave C, on which the price is currently riding, hit levels below its FE 161.8% (20400), seeing scope for further extension towards next Fibonacci expansion levels at 20344 (176.4%), possibly towards double Fibo support at 20260 zone (FE200% / Fibo 61.8% of 19713/21160 rally).

Session high at 20526 (also 22 Mar low, reinforced by falling 4-hr 10SMA) marks solid barrier.

Res: 20471; 20526; 20558; 20664

Sup: 20400; 20386; 20266; 20225