Sample Category Title

Trade Idea Update: USD/CHF – Buy at 0.9950

USD/CHF - 1.0027

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

As the greenback has continued trading with a firm undertone after last week’s rally above 1.0003 resistance, suggesting recent rise from last week’s low at 0.9813 is still in progress and bullishness remains for this move to extend gain to previous support at 1.0060 (now resistance), however, loss of upward momentum should prevent sharp move beyond resistance at 1.0109, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as said support at 0.9948 should limit downside. Below 0.9931 (50% Fibonacci retracement of 0.9831-1.0031) would abort and signal top is formed instead, bring correction to 0.9905-10 (61.8% Fibonacci retracement) but reckon previous resistance at 0.9869 would hold from here.

Trade Idea Update: GBP/USD – Hold short entered at 1.2465

GBP/USD - 1.2481

Original strategy :

Sold at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

New strategy :

Hold short entered at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

As cable has rebounded again after holding above support at 1.2419, suggesting further consolidation above this level would be seen, however, as long as indicated resistance at 1.2496 holds, mild downside bias remains for another fall, below said support at 1.2419 would bring test of 1.2400 but break there i needed to add credence to our view that the rebound from 1.2377 has ended at 1.2559, bring further fall towards support at 1.2377. Looking ahead, only a drop below 1.2377 would confirm the fall from 1.2616 is still in progress for subsequent decline towards key support at 1.2335.

In view of this, we are holding on to our short position entered at 1.2465 but one should exit on such decline. Only break of said resistance at 1.2496 would abort and suggest an intra-day low is formed instead, risk a stronger rebound to 1.2525-30.

FOMC Minutes And ADP Employment In Focus, Oil Prices Rise

News and Events:

US Dollar subject to downside risk heading into FOMC minutes

Most currency pairs have been trading sideways so far this week as investors remained reluctant to choose sides between Dollar bears or bulls. Obviously against this backdrop of uncertainties, the Japanese Yen took the best of the situation and extended gains as it returned below the 111 threshold. Investors will however slowly get out of the rut as a few pieces of key economic data are due for release before Friday, as well as the minutes of the March FOMC meeting.

The ADP job report is due for release at GMT 12:15 today. The market is expecting a much lower reading compared to February, when the pace of hiring exploded and printed at 298k versus 187k median forecast. For March, the market is expecting a reading closer to 185k. On our side, we believe that there is a substantial chance that February's reading will be revised downwards. Over the last few months, the Federal Reserve has been slowly shifting its communication, putting less emphasis on the headline unemployment rate and the pace of job creation, but rather stressing developments in the underemployment rate and core inflation.

Today's job report, just as Friday's NFPs, will therefore have little impact on the course of the USD. On the other hand, March's FOMC minutes that are due for release at GMT 18:00 could matter. Especially in the event of a dovish surprise which would eventually weigh on the greenback. The risk is definitely a downwards shift for the USD as we head into the minutes.

French Elections: Mélenchon risk to single currency is underestimated

The second debate of the French Presidential Election was broadcast yesterday, during which the 11 candidates had the chance to expose their views on many different topics. Emmanuel Macron was widely expected to win and he was hardly attacked by the other candidates. No candidate performed badly and so it was very hard to find a winner.

In the markets, we can see the CAC 40 is improving more slowly than the Euro Stoxx 50. We try to measure investors' fear and we believe banks' stocks price are a good proxy for that. It is clear that their volatility is increasing.

Currency-wise, we do not see the single currency improving should Macron or Francois Fillon get elected. There is also a growing risk for the single currency as we believe Jean-Luc Mélenchon's chance of winning is underestimated. His performances in the debates are always one of the most accomplished, if not the best. And his “Plan B” is that in the case of negotiation failure, he would not hesitate to ask for a Frexit referendum. So we now assume that Euro downside risks are not anymore only due to Marine Le Pen.

Oil-linked FX gets a boost

Oil prices rallied to a one-month high as expectations increased ahead of today's EIA inventories reports. There are clear signs that U.S inventories have fallen from record high levels. WTI crude today has reached $51.50 in early European trading on tightening supplies speculation. Improving US consumer health has seen a deeper draw on gasoline stockpiles. Gasoline supplies fell 3.7 million barrels while distillates stockpiles dropped 2.5 million barrels last week. In addition, potential supply disruptions in Libya and an unscheduled production outage in the North Sea provide further support for higher crude prices.

Crude bullish sentiment has given oil-linked FX a boost. Global storage inventories have been a overhang to higher prices. As glut is substantially reduced, crude prices can move higher. Mexican Peso (MXN) and Ruble (RUB) have led the gainers on the Emerging Markets side. Oil and gas stocks were the second best sector in equities. We are constructive on the complete crude trade since global economic conditions (improvement in trade and manufacturing) are driving additional crude demand. OPEC capped production limits by 1.2 million barrels and any extension (unlikely to end in May) might have seemed trivial at the time. However, with global fundamentals strengthening and heading to the summer driving season every barrel counts.

Today's Key Issues (time in GMT):

- Bank of Russia Governor Speaks at Moscow Exchange Forum

- RUB / 07:00Mar Standard Bank South Africa PMI, last 50,5 ZAR / 07:15

- Mar Markit Spain Services PMI, exp 57,4, last 57,7 EUR / 07:15

- Mar Markit Spain Composite PMI, exp 57, last 57 EUR / 07:15

- Feb Industrial Production MoM, exp 0,10%, last 2,00%, rev 3,30% SEK / 07:30

- Feb Industrial Production NSA YoY, exp 1,80%, last 1,30%, rev 4,30% SEK / 07:30

- Feb Industrial Orders MoM, last -2,60%, rev -3,30% SEK / 07:30

- Feb Industrial Orders NSA YoY, last 0,00%, rev 0,50% SEK / 07:30

- Feb Service Production MoM SA, exp -1,00%, last 1,10%, rev 0,90% SEK / 07:30

- Feb Service Production YoY WDA, last 7,70%, rev 6,80% SEK / 07:30

- RBA's Heath Bloomberg Panel Participation AUD / 07:30

- Mar Markit/ADACI Italy Services PMI, exp 54,3, last 54,1 EUR / 07:45

- Mar Markit/ADACI Italy Composite PMI, exp 54,9, last 54,8 EUR / 07:45

- Mar F Markit France Services PMI, exp 58,5, last 58,5 EUR / 07:50

- Mar F Markit France Composite PMI, exp 57,6, last 57,6 EUR / 07:50

- Mar F Markit Germany Services PMI, exp 55,6, last 55,6 EUR / 07:55

- Mar F Markit/BME Germany Composite PMI, exp 57, last 57 EUR / 07:55

- Mar F Markit Eurozone Services PMI, exp 56,5, last 56,5 EUR / 08:00

- Mar F Markit Eurozone Composite PMI, exp 56,7, last 56,7 EUR / 08:00

- Mar New Car Registrations YoY, last -0,30% GBP / 08:00

- Spain Reserves EUR / 08:00

- Istat Releases the Monthly Economic Note EUR / 08:00

- Mar Markit/CIPS UK Services PMI, exp 53,4, last 53,3 GBP / 08:30

- Mar Markit/CIPS UK Composite PMI, exp 53,8, last 53,8 GBP / 08:30

- Mar Official Reserves Changes, last $360m GBP / 08:30

- 4Q Unit Labor Costs YoY, exp 2,00%, last 2,30%, rev 2,50% GBP / 08:30

- Mar SACCI Business Confidence, last 95,5 ZAR / 09:30

- mars.31 MBA Mortgage Applications, last -0,80% USD / 11:00

- Mar Markit Brazil PMI Composite, last 46,6 BRL / 12:00

- Mar Markit Brazil PMI Services, last 46,4 BRL / 12:00

- Mar ADP Employment Change, exp 185k, last 298k USD / 12:15

- BOE Policy Maker Gertjan Vlieghe Speaks in London GBP / 12:30

- Apr 3 CPI WoW, last 0,00% RUB / 13:00Apr 3 CPI Weekly YTD, last 1,00% RUB / 13:00

- Mar F Markit US Services PMI, exp 53,1, last 52,9 USD / 13:45

- Mar F Markit US Composite PMI, last 53,2 USD / 13:45

- Mar ISM Non-Manf. Composite, exp 57, last 57,6 USD / 14:00

- mars.31 DOE U.S. Crude Oil Inventories, exp -150k, last 867k USD / 14:30

- mars.31 DOE Cushing OK Crude Inventory, exp 125k, last -220k USD / 14:30

- Mar Commodity Price Index YoY, last -9,91% BRL / 15:30

- Mar Commodity Price Index MoM, last -2,37% BRL / 15:30

- Currency Flows Weekly BRL / 15:30

- mars.15 FOMC Meeting Minutes USD / 18:00

- Mar CPI YTD, exp 1,00%, last 0,80% RUB / 22:00

- Mar CPI MoM, exp 0,20%, last 0,20% RUB / 22:00

- Mar CPI YoY, exp 4,30%, last 4,60% RUB / 22:00

- Mar CPI Core MoM, exp 0,20%, last 0,20% RUB / 22:00

- Mar CPI Core YoY, exp 4,60%, last 5,00%, rev 5,00% RUB / 22:00

- 1Q Consumer Confidence Index, last -18 RUB / 22:00

The Risk Today:

EUR/USD is getting lower despite ongoing consolidation. The pair is heading lower since the pair failed to hold above former resistance given at 1.0874 (08/12/2017 high). Hourly support can be found at 1.0643 (03/04/2017 low). Stronger support can be found at 1.0493 (22/02/2017 low). The short-term technical structure indicates further weakness.. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD's bullish pressures have faded abruptly. Hourly resistance is located at 1.2615 (27/03/2017 high) while hourly support can be found at 1.2324 (03/17/2017 low). Expected to show continued strengthening towards resistance at 1.2775 (06/12/2016 high) if support area around 1.24 stands. The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

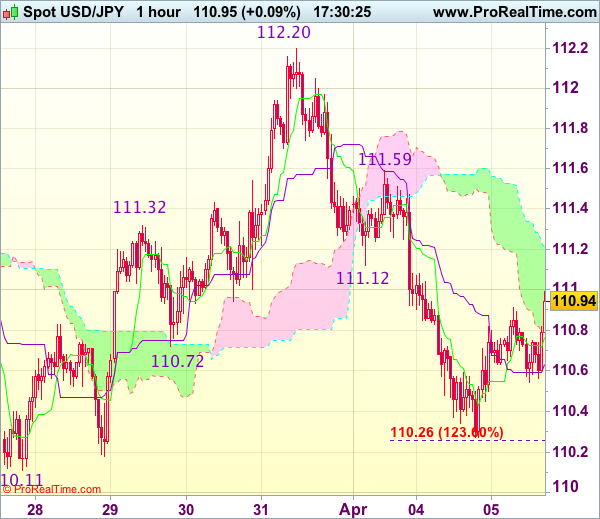

USD/JPY's bearish pressures are fading. Hourly resistance is given at 112.20 (31/03/2017 high). Stronger resistance can be located at 113.57 (16/03/2017 high) while support is given at 110.11 (27/03/2017 low). We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

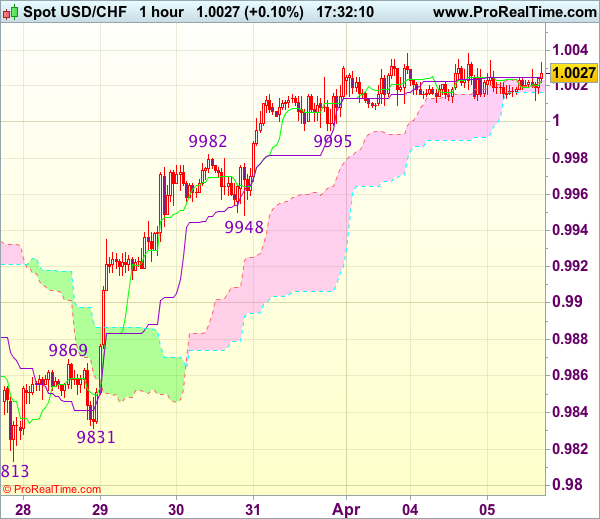

USD/CHF is strengthening. Hourly support is given at 0.9814 (27/03/2017 low). Key resistance can be found at a distance at 1.0344 (15/12/2016 high). Expected to show further consolidating. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3121 | 1.0652 | 118.66 |

| 1.0954 | 1.2775 | 1.0344 | 115.62 |

| 1.0906 | 1.2706 | 1.0171 | 112.20 |

| 1.0669 | 1.2504 | 1.0024 | 110.80 |

| 1.0494 | 1.2377 | 0.9814 | 108.50 |

| 1.0341 | 1.2110 | 0.9550 | 106.04 |

| 1.0000 | 1.1986 | 0.9444 | 101.20 |

Trade Idea Update: EUR/USD – Sell at 1.0730

EUR/USD - 1.0668

Original strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

As the single currency has recovered after falling to 1.0635 yesterday, suggesting minor consolidation above this level would be seen and corrective bounce to 1.0702 cannot be ruled out, however, reckon 1.0730-40 would limit upside and bring another decline, below said support at 1.0635 would add credence to our bearish view that the decline from 1.0906 top is still in progress and extend further weakness to 1.0620, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0730-40 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

Trade Idea Update: USD/JPY – Sell at 111.55

USD/JPY - 110.93

Original strategy :

Sell at 111.10, Target: 110.00, Stop: 111.45

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.55, Target: 110.35, Stop: 111.90

Position : -

Target : -

Stop : -

As the greenback has rebounded again in European morning, suggesting near term upside risk remains for the rebound from 110.27 (yesterday’s low) to bring retracement of the decline from 112.20, hence further gain to previous support at 111.12 cannot be ruled out, however, resistance at 111.59 would cap upside and bring another decline later, below 110.50-55 would suggest the rebound from 110.27 has ended, bring retest of this level, break there would extend the fall from 112.20 to last week’s low at 110.11. Looking ahead, break there is needed to retain downside bias and confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) which is likely to hold on first testing.

In view of this, would not chase this fall here and would be prudent to sell dollar on further subsequent recovery as 111.59 resistance should limit upside. Above 111.80 would shift risk to upside and signal the fall from 112.20 has ended, bring subsequent rise to 112.00-05 first.

French Election Monitor No.1: Emmanuel Macron Remains Favourite After 2nd TV Debate

Yesterday, the second TV debate of all 11 presidential candidates took place, which again saw Emmanuel Macron as one of the candidates with the most convincing performance (21% of viewers) after Jean-Luc Mélenchon (25%). On the other hand, Marine Le Pen was rated only the fourth most convincing candidate (11%), according to a snap poll by Elabe conducted right after the debate. In the same poll, Macron was also seen as the candidate with the best programme by 23% of viewers. A third and final debate is scheduled for 20 April but it is currently unclear if it will take place, as some candidates have complained that it is being held too close to the first round on 23 April.

The impact of these debates should not be underestimated, and we are likely to see polling for Macron and Mélenchon move up after their convincing performance yesterday. Macron's support surged after the first TV debate, when he was seen as the most convincing candidate and similarly for Melénchon, who due to his performance has now overtaken the Socialist candidate Benoît Hamon in the polls (see Chart 1). For now, it still seems to come down to a second round run-off on 7 May between Le Pen and Macron, where the latter is projected to win at around 61% and the margin of winning for Macron has also stayed relatively stable since the beginning of the year (see Chart 2).

However, the overall electorate is still not too determined in their voting intentions, as only 62% express certainty in their choice of candidate. Hence, the election outcome remains unpredictable and will to a large extent also depend on the participation rate. Traditionally, participation for presidential elections has been relatively high at around 80%. However, recent polls have suggested that voter turnout might be lower this time, only around 66-76%, due to widespread dissatisfaction with the political class. Should this be the case, it would be likely to boost Le Pen's chances of winning, as her supporters remain the most certain of their vote at 81%, compared to only 63% for Macron supporters (see Chart 3). For the short-term market implications of a Le Pen win, see Le Pen – What If? Implications for Euro and Nordic markets, 13 February 2017

UK Construction Growth Slows Slightly In March

'UK construction firms experienced a growth slowdown in March, with the loss of momentum centred on housebuilding.' - Tim Moore, IHS Markit

The Purchasing Manager's Index for the British construction sector slipped slightly last month, falling behind analysts' expectations. IHS Markit reported on Tuesday its UK Construction PMI came in at 52.2, while analysts held expectations for an unchanged reading of 52.5. According to IHS Markit's report, this drop reflected a slowdown in residential building activity, which offset a revival in both commercial and civil engineering sectors. The data showed a minor change in new business growth, due to consumers' budget constraints that also slowed hiring and created less demand for raw materials. In addition, companies reported weaker demand for subcontractors' services and noted that inflationary pressures continued to build in because of expensive imports and rising commodity prices. Nevertheless, construction companies maintained a positive outlook for short-term growth prospects, referring to lower anxiety associated with Brexit and satisfactory macroeconomic data. Stronger consumer confidence also contributed to firms' optimism, which reached a fifteen-month high. In particular, almost half of the respondents claimed their business activity would likely improve, while 9% of the surveyed expressed strong pessimism on growth .

Canada Posts Trade Deficit For First Time Since October In February

'The Bank of Canada has highlighted we've been here before, where things have looked good at the start of the year if only to melt away in the second half. They've noted they're not going to make policy decisions on a short stretch of data.' - Nick Exarhos, CIBC Capital Markets

Canada's balance of trade turned negative for the first time since October 2016 in February, surprising markets and raising concerns about the overall health of the economy. Canada posted a trade deficit of C$972 million ($724) in February, following the preceding month's downwardly revised surplus of C$421, Statistics Canada reported on Tuesday. Total exports' value dropped 2.4%, the largest decline since March 2016. Yesterday's data called to question Canada's stronger than expected economic figures released in March. Thus, analysts started to doubt whether the Canadian economy managed to hit 2.5% growth in the Q1 of 2017 as predicted by the Bank of Canada. Moreover, following the release, analysts suggested that the Central bank would leave its monetary policy on hold at its April meeting next week, keeping the key interest rate at a record low of 0.50%. The data showed exports in the farm, fishing and food products sector fell 10.6%, whereas shipments of aircraft and transportation equipment dropped 15.2%. The largest declines were registered in shipments of aircrafts and canola, which contributes $26.7B to the Canadian economy each year. Exports to Canada's southern neighbour, the United States, decreased 1.2%, while shipments to other countries plunged 5.9%.

New Zealand Dairy Product Prices Rise 1.6% At Latest Global Dairy Trade Auction

'Buyers will be aware that New Zealand dairy farmers are having a strong finish to the production season which means there is extra milk powder coming on line, so in this environment it is very positive to see whole milk powder prices creeping back up.' - Susan Kilsby, AgriHQ

Dairy product prices rose for the second time in a row at the Global Dairy Trade auction on Tuesday amid growing market optimism. The GDT Price Index climbed 1.6% to $3,005 after advancing 1.7% at the preceding auction. Some 22,642 tonnes of dairy products was sold, compared to 22,498 tonnes sold at the previous auction. The whole milk powder price rose 2.4% to $2,924 per tonne, while the rennet casein price surged 6.9% to $6,260 per tonne. Prices for anhydrous milk fat advanced 2.5% to $5,936 per tonne, whereas the lactose price climbed 2.2% to $927 per tonne. In the meantime, prices for butter milk powder plunged 12.2% to $1,588 per tonne, while prices for cheddar fell 4.4% to $3,288 per tonne. The butter price decreased 1.6% to $4,751 per tonne, whereas the skim milk powder price declined 0.8% to $1,913 per tonne. According to analysts, the second straight increase in the GDT Price Index is encouraging, as it is common for prices to dip during the spring season. However, the latest auction results suggest that skim milk powder markets are under pressure due to large inventories in Europe, but analysts expect to see further demand growth in China and other Asian countries. The NZD/USD pair surged shortly after the release, rising above the 70.00 level.

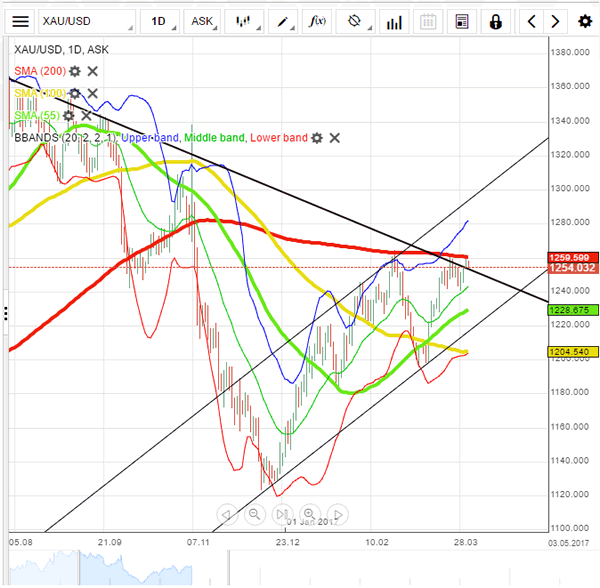

XAUUSD: Fluctuates Above 1,250 Mark

'The markets are waiting for the conference between the most important leaders in the world.' – Jiang Shu, Shandong Gold Group (based on Reuters)

Pair's Outlook

On Wednesday morning the yellow metal's price remained almost unchanged at the 1,255 mark. However, various clues were indicating that the bullion's price was about to decline down to the 1,250 mark, where a cluster of support was located at. The main reason for that hypothesis was the fact that the 200-day SMA was providing resistance at the 1,256.45 level, and gold clearly could not pass it. It is highly possible that the bullion's price will decline down to the combined support of the weekly PP and the 50.00% Fibonacci retracement level, respectively, at 1,249.67 and 1,248.96 during the day's trading session.

Traders' Sentiment

Traders have become slightly bearish on the metal, as 52% of open positions are short on Wednesday. Meanwhile, 63% of trader set up orders are to buy.