Sample Category Title

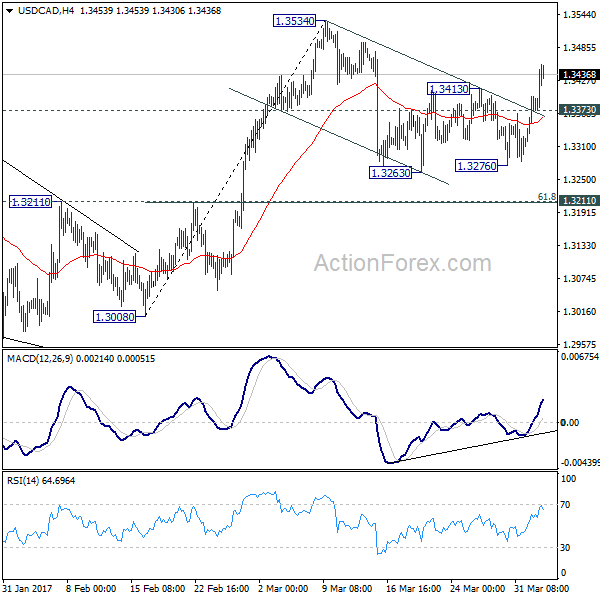

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3314; (P) 1.3356; (R1) 1.3425; More....

USD/CAD's strong rally today and break of 1.3413 resistance indicates that corrective fall from 1.3534 has completed already. Intraday bias is turned back to the upside for retesting 1.3534 first. Break will extend whole rise from 1.2698 to 1.3598 resistance. Overall, medium term rebound form 1.2460 is still expected to extend through 1.3598. On the downside, below 1.3373 minor support will turn bias back to the downside and could extend the correction from 1.3534 with another fall. But we'd expect strong support from 1.3211 cluster level (61.8% retracement of 1.3008 to 1.3534 at 1.3209) to contain downside and bring rebound.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 will argue that the third leg has already started and should at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

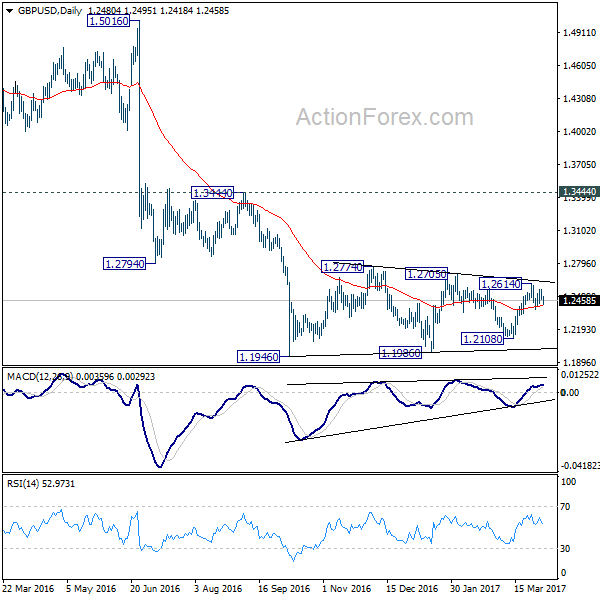

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2448; (P) 1.2501; (R1) 1.2538; More...

Intraday bias in GBP/USD remains neutral as it's staying in range of 1.2376/2614. Overall, price actions from 1.1946 are viewed as a consolidation pattern pattern. On the downside, break of 1.2376 will turn bias to the downside for 1.2108 support. Decisive break there will be an early sign of larger down trend resumption. On the upside, break of 1.2614 will extend the rise from 1.2108. But upside should be limited by 1.2705/2774 resistance zone to bring larger down trend resumption eventually.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

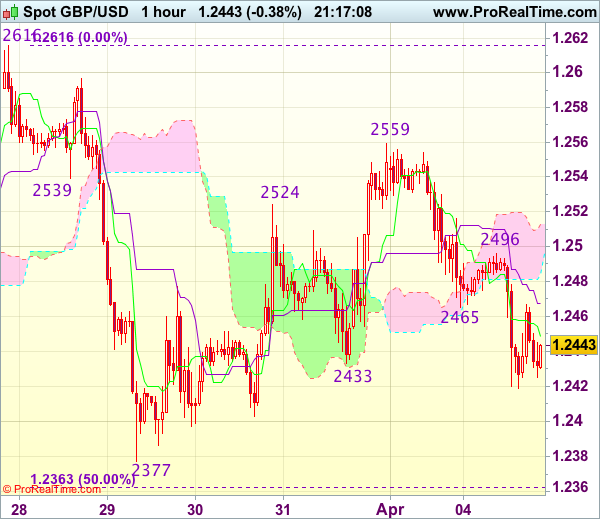

Trade Idea Update: GBP/USD – Hold short entered at 1.2465

GBP/USD - 1.2460

Original strategy :

Sold at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

New strategy :

Hold short entered at 1.2465, Target: 1.2365, Stop: 1.2500

Position : - Short at 1.2465

Target : - 1.2365

Stop : - 1.2500

Although cable has rebounded after finding support at 1.2419 and minor consolidation above this level would be seen, reckon the Kijun-Sen (now at 1.2475) would limit upside and bring another decline later, below said support at 1.2419 would extend weakness to 1.2400, break there would add credence to our view that the rebound from 1.2377 has ended at 1.2559, bring further fall towards support at 1.2377. Looking ahead, only a drop below 1.2377 would confirm the fall from 1.2616 is still in progress for subsequent decline towards key support at 1.2335.

In view of this, we are holding on to our short position entered at 1.2465 but one should exit on such decline. Only break of said resistance at 1.2496 would abort and suggest an intra-day low is formed instead, risk a stronger rebound to 1.2525-30.

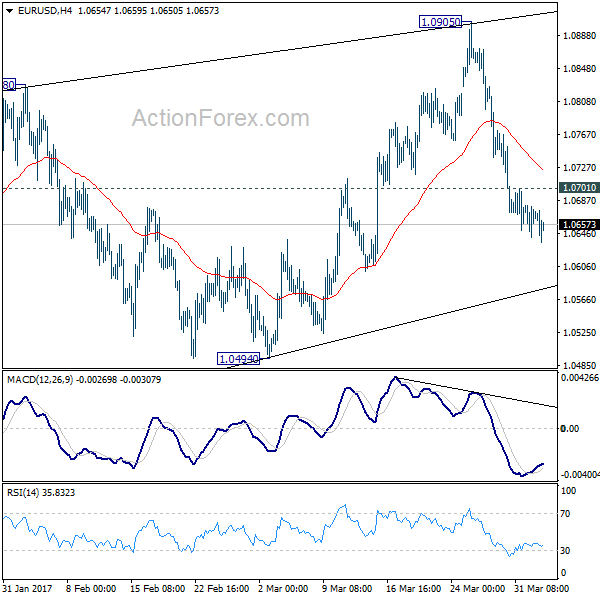

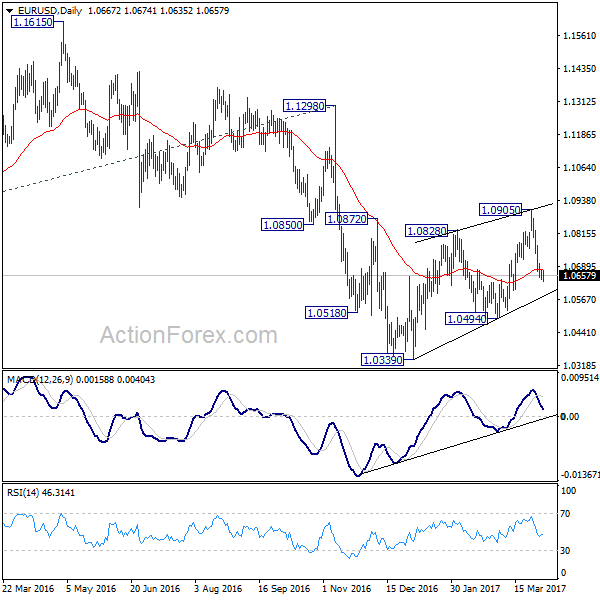

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0647; (P) 1.0664 (R1) 1.0686; More....

Intraday bias in EUR/USD remains on the downside for 1.0494 support despite diminishing downside momentum. Our view is unchanged that corrective rise from 1.0339 is completed at 1.0905. And more importantly, larger down trend is probably resuming. Break of 1.0494 should confirm this bearish case and target 1.0339 low. Further break of 1.0339 will target parity next. On the upside, above 1.0701 will bring consolidations first before staging another decline.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

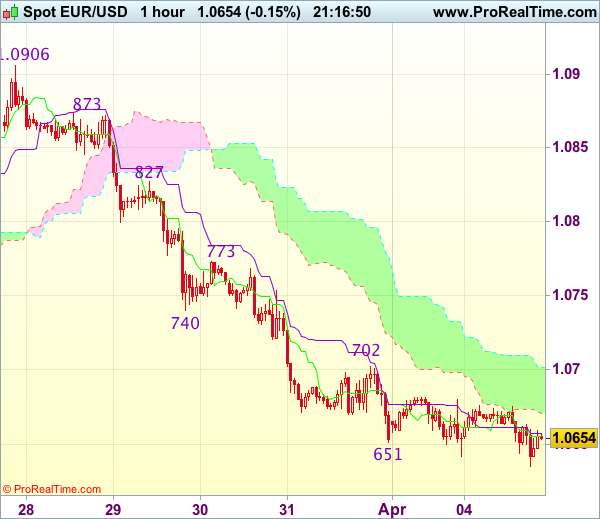

Trade Idea Update: EUR/USD – Sell at 1.0730

EUR/USD - 1.0659

Original strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0730, Target: 1.0610, Stop: 1.0765

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after falling to 1.0642 yesterday, adding credence to our bearish view that the decline from 1.0906 top is still in progress and bearishness remains for this fall to extend further weakness to 1.0620-25, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first, otherwise, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0730-40 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

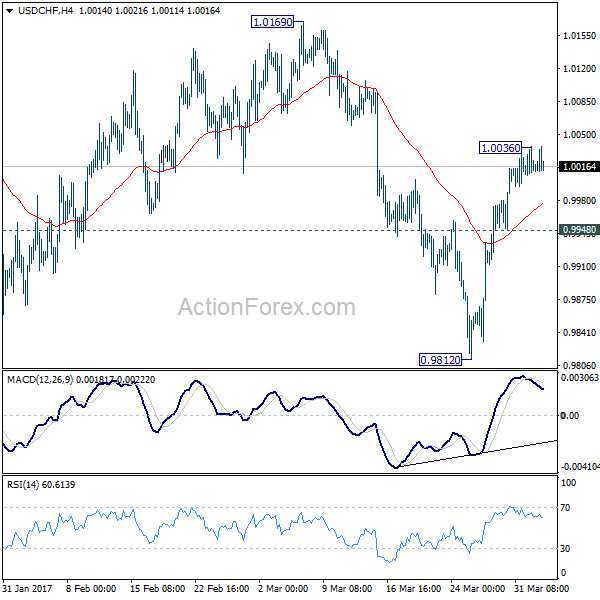

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0002; (P) 1.0019; (R1) 1.0032; More.....

A temporary top is in place at USD/CHF with 4 hours MACD crossed below signal line. Intraday bias is turned neutral for some consolidations. Overall, we're holding on to the view that corrective decline fall from 1.0342 should have finished with three waves down to 0.9812 already. Break of 1.0036 will turn bias to the upside for 1.0169 resistance. Break there will confirm this bullish case and target a test on 1.0342 high. On the downside, however, below 0.9948 minor support will turn bias back to the downside for 0.9812 instead.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

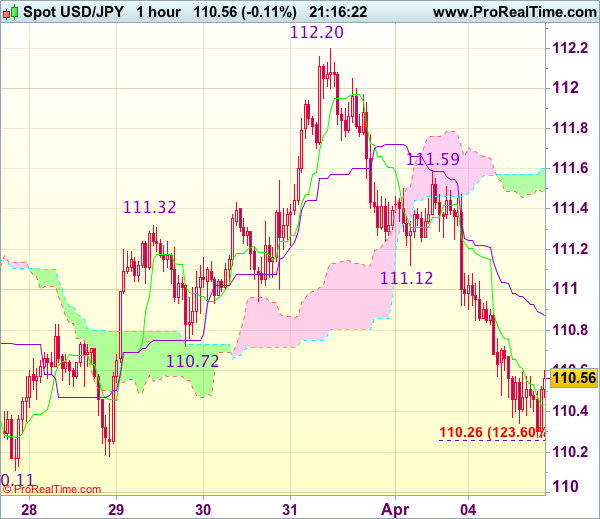

Trade Idea Update: USD/JPY – Sell at 110.95

USD/JPY - 110.57

Original strategy :

Sell at 110.95, Target: 109.95, Stop: 111.30

Position : -

Target : -

Stop : -

New strategy :

Sell at 110.95, Target: 109.95, Stop: 111.30

Position : -

Target : -

Stop : -

As the greenback has dropped again after meeting renewed selling interest at 111.59 yesterday, adding credence to our view that top ha been formed at 112.20 and bearishness remains for the selloff from there to extend weakness to 110.11 support, however, break there is needed to retain downside bias and confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) which is likely to hold on first testing.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 110.90-95 should limit upside. Above previous support at 111.12 (now resistance) would defer but only break of resistance at 111.59 would abort and signal the fall from 112.20 has ended instead.

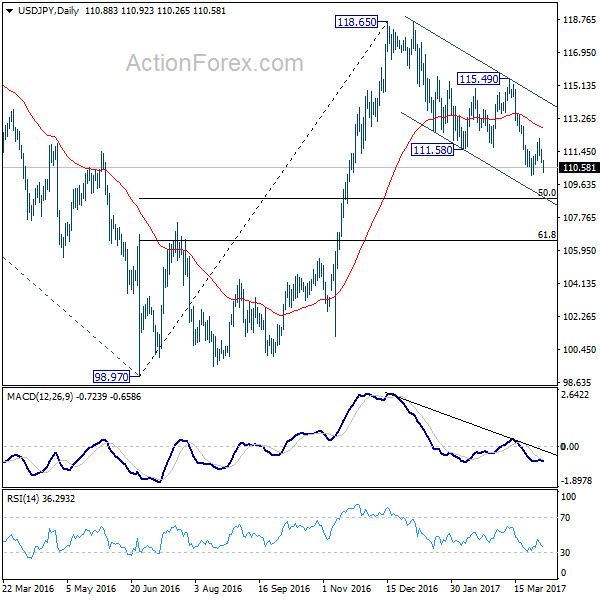

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.64; (P) 111.11; (R1) 111.37; More....

Intraday bias in USD/JPY remains on the downside for the moment. As noted before, corrective fall from 118.65 is still in progress and is possibly resuming. Break of 110.10 will confirm this bearish case and target 50% retracement of 98.97 to 118.65 at 108.81. On the upside, break of 112.19 resistance is needed to confirm near term reversal. Otherwise, outlook will stay mildly bearish in case of recovery.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

Japanese Yen Remains Strong head of Donald Trump-Xi JinPing Summit

Japanese Yen remains the strongest major currency for the week on risk aversion. On the one hand, sentiments were weighed down by terrorist attack in Russia. On the other hand, markets are getting cautious ahead of the summit between US president Donald Trump and China President Xi Jinping. Dollar follows Yen as the second strongest one but it's losing some momentum against Euro. Commodity currencies are generally lower today with Aussie leading the way down on the perceived dovish RBA statement. In other markets, Gold seems to benefit from risk aversion and jumped to 1263.7 but lost momentum quickly. WTI crude oil is struggling around 55 day EMA around 50.67.

Trump and Xi to meeting later this week

US trade deficit narrowed to USD -43.6b in February, better than expectation of USD -46.0b. Exports rose 0.2% to USD 192.9b while imports dropped -1.8% to 236.4b. Trade with China contributed to nearly 70% of the deficit. US president Donald Trump and China president Xi Jinping will meet later this week. Trade relationship and issues on North Korea will be the focuses in the talk between the leaders.

Some economists anticipated that the result of the meeting will set the tone for US-China relationship for the next few years. While it's generally believed both leaders wouldn't want to spoil the meeting, nothing solid could be achieved other than some minor economic concessions from China. Also released in US session, Canada trade balance came in at CAD -1.0b deficit in February.

Brexit committee urged assessment on "no deal"

In UK, Prime Minister Theresa has warned that "no deal is better than a bad deal" for Brexit. A report by a cross-party MPs' Brexit committee criticized that such claim is "unsubstantiated" before an economic assessment of "no deal" is completed. In addition, the report urged that the parliament must have a vote before Brexit without a deal.

UK construction PMI dropped 0.3 to 52.2 in March, below expectation of 52.5. Markit noted that "March data revealed a slowdown in growth across the UK construction sector, led by a weaker rise in residential building activity." Also, that provides an indication that the cooling UK housing market has started to act as a drag on the construction sector."

Released from Eurozone, retail sales rose 0.7% mom in February.

Aussie lower after RBA

Australian dollar's decline accelerates today after RBA left cash rate unchanged at 1.50% as widely expected. RBA sounded more concerned on employment as it noted that "some indicators of conditions in the labour market have softened recently." On the other hand, the central bank continued to struggle between soaring property prices and subdued inflation. We expect RBA to leave its monetary stance unchanged throughout the year. More in RBA Torn Between High Housing Prices And Subdued Inflation.

Also from Australia, trade surplus widened to AUD 3.57b in February. Meanwhile, Japan monetary base rose 20.3% yoy in March.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.64; (P) 111.11; (R1) 111.37; More....

Intraday bias in USD/JPY remains on the downside for the moment. As noted before, corrective fall from 118.65 is still in progress and is possibly resuming. Break of 110.10 will confirm this bearish case and target 50% retracement of 98.97 to 118.65 at 108.81. On the upside, break of 112.19 resistance is needed to confirm near term reversal. Otherwise, outlook will stay mildly bearish in case of recovery.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Mar | 20.30% | 23.20% | 21.40% | |

| 1:30 | AUD | Trade Balance (AUD) Feb | 3.57B | 1.75B | 1.30B | 1.50B |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 8:30 | GBP | Construction PMI Mar | 52.2 | 52.5 | 52.5 | |

| 9:00 | EUR | Eurozone Retail Sales M/M Feb | 0.70% | 0.50% | -0.10% | 0.10% |

| 12:30 | CAD | International Merchandise Trade (CAD) Feb | -1.0B | 0.7B | 0.8B | -0.4B |

| 12:30 | USD | Trade Balance Feb | -43.6B | -46.0B | -48.5B | -48.2B |

| 14:00 | USD | Factory Orders Feb | 0.90% | 1.20% |

Japanese Yen Improves, BoJ Core CPI Misses Estimate

The Japanese yen has edged higher on Tuesday, continuing the upward trend which marked the Monday session. Early in the North American session, USD/JPY is trading at 110.40. On the release front, BoJ Core CPI edged lower to 0.1 percent. In the US, the trade deficit narrowed to $43.6 billion, better than the forecast of $46.0 billion. On Wednesday, all eyes will be on the Federal Reserve, which will publish the minutes of its March policy meeting. As well, the US will release ADP Employment Change and ISM Non-Manufacturing PMI.

Japan's economy has shown improvement in recent months, buoyed by stronger exports. At the same time, domestic consumption remains soft and inflation levels remain well below the BoJ's target of 2.0% percent. The BoJ's preferred inflation indicator, BoJ Core CPI, remains weak and dipped to 0.1 percent. With such low inflation levels, the Bank of Japan is unlikely to tighten monetary policy anytime soon.

The US economy has looked sharp in 2017, and the markets are expecting strong data for the first quarter. The CB consumer confidence report soared to 125.6 in March, and strong consumer confidence levels should translate into increased consumer spending, a key component of economic growth. GDP for the fourth quarter was revised to 2.1%, up from 1.9% in the previous GDP report. With the economy headed in the right direction, the discussions around the monetary policy tables are not whether the Fed will raise rates, but will it press the rate trigger two or three more times in 2017. The markets will be paying close attention to the minutes of the March meeting, when the Fed raised rates by a quarter-point, to a range of 0.75%-1.00%. Any hints about the timing of the next hike, as well as the tone of the minutes are factors which could move the currency markets on Wednesday. The markets considered the rate statement overly cautious, and this sentiment sent the US dollar broadly lower. If the reaction to the minutes is one of disappointment, the dollar could again head downwards.