Sample Category Title

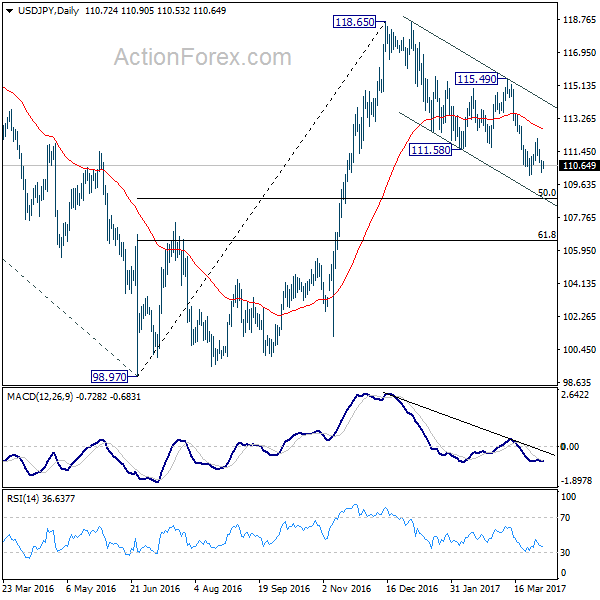

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.35; (P) 110.64; (R1) 111.02; More....

USD/JPY recovers mildly ahead of 110.10 support. But intraday bias stays on the downside for the moment. Break of 110.10 will resume the whole corrective decline from 118.65 and target 50% retracement of 98.97 to 118.65 at 108.81. On the upside, break of 112.19 resistance is needed to confirm near term reversal. Otherwise, outlook will stay mildly bearish in case of recovery.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

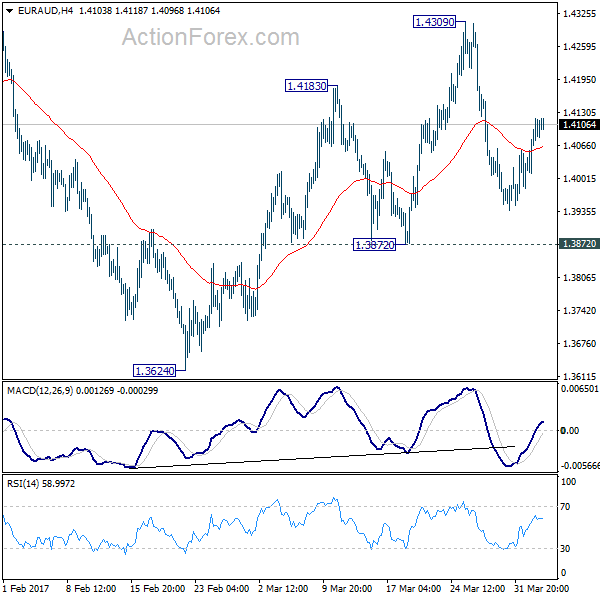

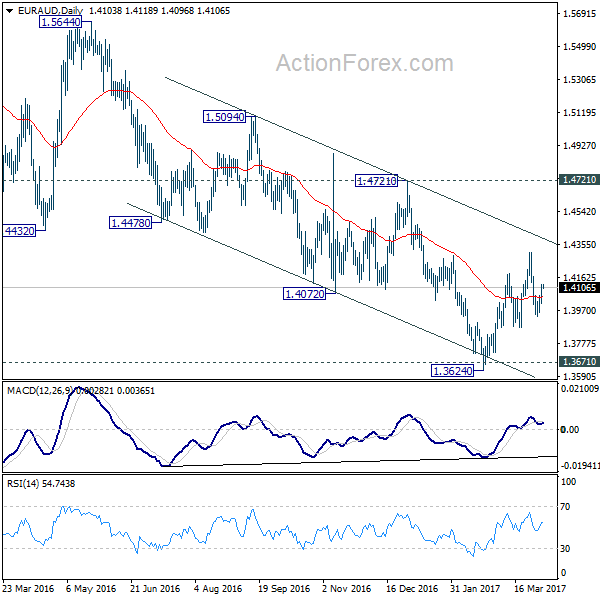

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4039; (P) 1.4080; (R1) 1.4149; More...

EUR/AUD remains bounded in range of 1.3872/4309 and intraday bias stays neutral. We're holding on to the view of trend reversal after defending key support level at 1.3671. Another rise is expected as long as 1.3872 minor support holds. Break of 1.4309 will extend the rebound from 1.3624 to 1.4721 key resistance level next. Break should confirm larger trend reversal. However, firm break of 1.3872 support will dampen our bullish view. In such case, intraday bias will be turned back to the downside for 1.3624 low instead.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

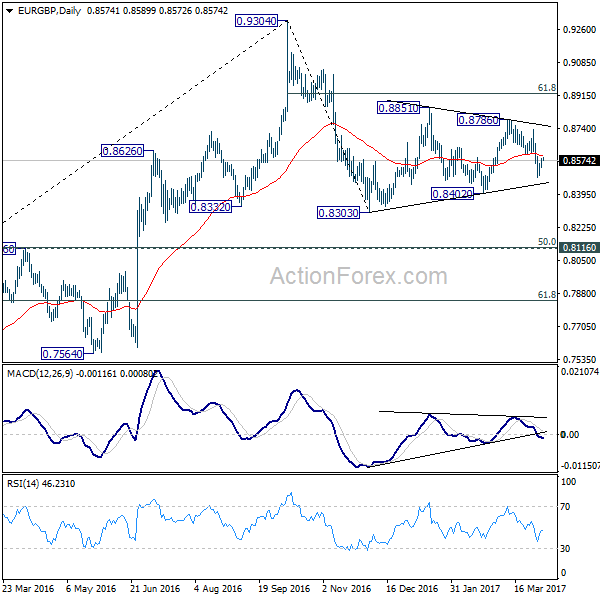

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8548; (P) 0.8568; (R1) 0.8598; More...

Intraday bias in EUR/GBP remains neutral for the moment for consolidation above 0.8430 temporary low. There is no change in the view that price actions from 0.8303 are a consolidation pattern. And, it's the second leg of the correction from 0.9304. Below 0.8430 will target 0.8402. Break of 0.8402 will resume the fall from 0.9304 to 0.8116/20 cluster support, where the correction should end. Above 0.8604 minor resistance will bring another recovery before fall from 0.9304 resumes.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is likely ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Break of 0.9304 will pave the way to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0676; (P) 1.0685; (R1) 1.0701; More...

A temporary low is in place at 1.0668 in EUR/CHF and intraday bias is turned neutral first. As long as 1.0734 resistance holds, deeper decline is expected in the cross. Below 1.0668 will target 1.0620/29 key support zone. Decisive break there will resume the larger fall from 1.1198. Nonetheless, break of 1.0734 will turn bias back to the upside for 1.0823 resistance instead.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Current development suggests that it's not completed yet. sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485. In any case, break of 1.0823 resistance is needed to be the first indication of reversal. Otherwise, deeper fall is still expected even in case of recovery.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 137.06; (P) 137.77; (R1) 138.46; More...

Intraday bias in GBP/JPY remains on the downside for the moment. The choppy decline from 144.77 is still in progress and should target medium term fibonacci level at 135.39. Overall, price action from 148.42 are seen as a consolidation pattern. We'll look for bottoming around 135.39. Meanwhile, break of 140.08 resistance is needed to indicate short term reversal. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern. Or, sustained break of 50% retracement of 122.36 to 148.42 at 135.39 will turn outlook bearish for a test on 122.36 low. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement of 195.86 to 122.36 at 167.78.

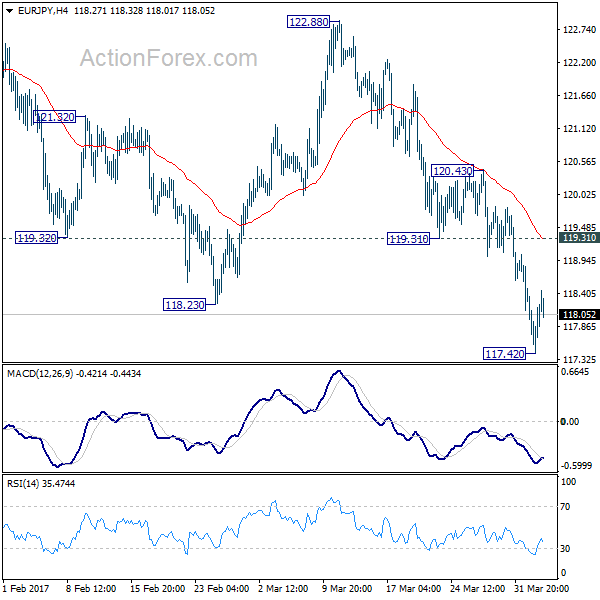

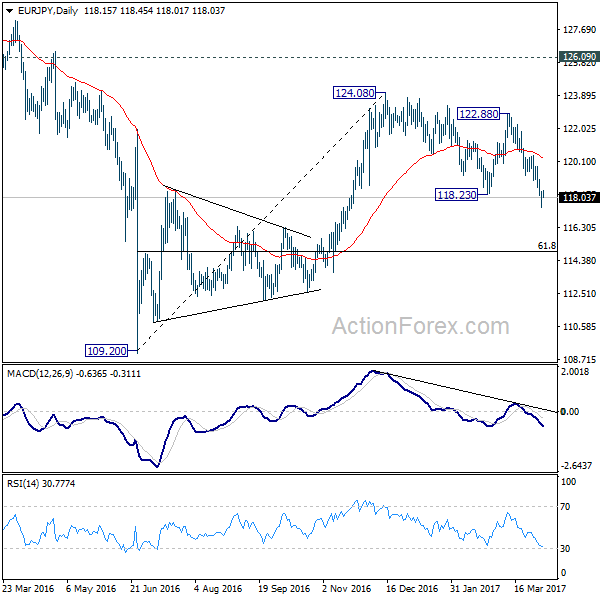

EUR/JPY Daily Outlook

Daily Pivots: (S1) 117.62; (P) 117.99; (R1) 118.55; More...

EUR/JPY recovered after forming a temporary low at 117.42 and intraday bias is turned neutral first. Some consolidations would be seen but upside should be limited by 119.31 support turned resistance and bring another decline. Current development suggests that medium term rise from 109.20 has completed at 124.08 already. Below 117.42 will target 61.8% retracement of 109.20 to 124.08 at 114.88 next. Nonetheless, sustained break of 119.31 will turn focus back to 120.43 resistance instead.

In the bigger picture, the firm break of 38.2% retracement of 109.20 to 124.08 at 118.39 indicates that medium term rise from 109.20 is completed at 124.08. That's well below 126.09 key support turned resistance. Also, EUR/JPY failed to sustain above 55 week EMA. Deeper decline would now be seen back to 109.20 low. Overall, the down trend from 149.76 (2014 high) is not completed yet. Break of 109.20 will resume such down trend towards 94.11 low. In any case, break of 126.09 is needed needed to confirm medium term reversal.

Euro Steady after French Election Debate, Markets Calm after Another North Korea Missile Test

The forex markets are pretty steady in Asian session today. Commodity currencies remain generally soft on mild risk aversion. Traders are cautious ahead of the meeting between US President Donald Trump and China President Xi Jinping. Yet, they are calm in spite of the news that North Korea fired another ballistic missile. Euro is also staying in range after French presidential election TV debate. Yen pares back some gains after treasury yields stabilized but more upside is still favored. In other markets, both gold and WTI crude oil extended recent rally but momentum is not too strong so far.

Le Pen targeted in chaotic TV debate

Eleven candidate joined the marathon French presidential election debate overnight. In a somewhat chaotic situation, far right candidate Marine Le Pen seemed to be the most targeted by the others. Front runner centrist Emmanuel Macron criticized that Le Pen's proposal of reverting to franc was a "reduction in French people's spending power". Conservative François Fillon criticized that Le Pen had no economic plan other than Frexit. Meanwhile, Socialist Benoit Hamon accused Le Pen of benefiting from Isis terrorists.

According to an Elabe poll, 25% said leftist Jean-Luc Melenchon was the most convincing performer in the debate. Fillon got 15% followed by Le Pen's 11%. An OpinionWay poll had Macron, Macron and Fillon tied at 18% and Le Pen at 11%.

North Korea fired another missile ahead of Trump-Xi meeting

It's reported the North Korea fired another ballistic missile into waters off its east coast into the sea of Japan. That came just before the summit between China President Xi Jinping and US President Donald Trump. The US department of state responded by said that "the United States has spoken enough about North Korea. We have no further comment".

North Korea is believed to be one of the top issues at the two-day meeting between Xi and Trump. And Trump has also said that China should use its "great influence" to resolve the issue of North Korea. And, Trump said that "if China is not going to solve North Korea, we will".

Richmond Fed president Lacker abruptly quit

Richmond Fed President Jeffery Lacker abruptly resigned yesterday as he disclosed confidential information to a Wall Street analyst of Medley Global Advisors back in 2012. Lacker said in a statement that he "crossed the line". He admitted that when the Medley analyst brought up confidential information, he "should have declined to comment and perhaps have ended the phone call". Early information regarding Fed's quantitative easing program was passed to the analysts and gave her clients an unfair advantage.

Lacker's lawyer said that the investigation was complete and there was no charge on Lacker. Fed's Office of Inspector General also said that investigation was now complete too.

On the data front...

UK BRC shop price index dropped -0.8%. UK PMI services will be a main focus in European session while Eurozone will release PMI services final. From US, ISM non-manufacturing composite and FOMC minutes will be released.

CAD/JPY heading to 80.18

CAD/JPY is one of the biggest losers for the week despite rise in oil price. WTI crude oil extended recent rally overnight and strength carries on in Asian session, hitting as high as 51.36. But that provides little support to the Loonie. Commodity currencies are generally lower this week ahead of the meeting between US Trump and China Xi, as well as non-farm payroll report from US. Yield and stocks stabilized but will face the first test of ADP employment today.

Technically, the fall from 88.90 is clearly corrective looking, especially in comparison to the rise from 74.80 to 88.90. But at this point, it's likely that such correction will go deeper to 61.8% retracement of 74.80 to 88.90 at 80.18. This will be the favored case as long as 84.19 near term resistance holds.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 117.62; (P) 117.99; (R1) 118.55; More...

EUR/JPY recovered after forming a temporary low at 117.42 and intraday bias is turned neutral first. Some consolidations would be seen but upside should be limited by 119.31 support turned resistance and bring another decline. Current development suggests that medium term rise from 109.20 has completed at 124.08 already. Below 117.42 will target 61.8% retracement of 109.20 to 124.08 at 114.88 next. Nonetheless, sustained break of 119.31 will turn focus back to 120.43 resistance instead.

In the bigger picture, the firm break of 38.2% retracement of 109.20 to 124.08 at 118.39 indicates that medium term rise from 109.20 is completed at 124.08. That's well below 126.09 key support turned resistance. Also, EUR/JPY failed to sustain above 55 week EMA. Deeper decline would now be seen back to 109.20 low. Overall, the down trend from 149.76 (2014 high) is not completed yet. Break of 109.20 will resume such down trend towards 94.11 low. In any case, break of 126.09 is needed needed to confirm medium term reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Mar | -0.80% | -1.00% | ||

| 7:45 | EUR | Italy Services PMI Mar | 54.3 | 54.1 | ||

| 7:50 | EUR | France Services PMI Mar F | 58.5 | 58.5 | ||

| 7:55 | EUR | Germany Services PMI Mar F | 55.6 | 55.6 | ||

| 8:00 | EUR | Eurozone Services PMI Mar F | 56.5 | 56.5 | ||

| 8:30 | GBP | Services PMI Mar | 53.5 | 53.3 | ||

| 12:15 | USD | ADP Employment Change Mar | 189K | 298K | ||

| 14:00 | USD | ISM Non-Manufacturing Composite Mar | 57 | 57.6 | ||

| 14:30 | USD | Crude Oil Inventories | 0.9M | |||

| 18:00 | USD | FOMC Meeting Minutes |

Market Morning Briefing: Fed And ECB Minutes Today

STOCKS

Almost all stocks look bullish for the medium term except Nikkei. Dax may consolidate in the near term before rising up sharply.

Dow (20689.24, +0.19%) is trying to rise above 20800 while above support near 20450. A failure to rise past 20800 could see a consolidative phase with some downside possibilities; else a break above 20800 is needed to take it to higher levels near 21200-21250.

Dax (12282.34, +0.21%) has played out exactly as expected. A rise to 12375 before falling off to 12220. Now while support at 12220 holds, it would try to rise back towards 12400 levels. The next 2-3 sessions could trade within 12400-12220 region.

Nikkei (18861.68, +0.27%) may test support near 18650 before again bouncing back to higher levels. Immediate resistance is seen near 19070 which if holds could keep the index in the 19070-18650 region for the next few sessions.

Shanghai (3257.64, +1.09%) opened with a gap up and could be headed towards 3275-3280 levels in the near term while support near 3200 holds.

Nifty (9237.85, +0.70%) had moved up quite a bit on Monday and could easily head towards our initial target of 9280 in the coming sessions. Momentum seems to be strongly bullish and a rise towards 9400-9500 levels in the longer term would not be a surprise if 9280 breaks in the initial testing.

COMMODITIES

As seen most of the times in the last few days, Gold (1253) and Silver (18.25) remained indifferent to the global cues and closed below their respective resistances levels of 1263 and 18.50, indicating a complete absence of directional clarity. . We have been expecting 1237 for gold and 17.90 for silver to hold for some time and gradual buying at lower levels can’t be ruled as buyers are taking every dip as a further opportunity for buying.

Copper (2.64) is trading within a range of 2.57-2.70. Only above 2.70, higher resistances of 2.80 can come into consideration. In the medium term 2.55-57 are going to be a strong support now but a close below that could open up 2.55 and 2.49 levels respectively.

Both Brent (52.83) and WTI(51.21) have found support and trading within the range of 52.09-53.45 and 50.30-51.7, though the possibility of a decline towards supports can’t be ruled out. We have US crude oil inventory data at 8.00 pm IST and the U.S. data forecast is -0.1M, decrease in weekly inventory. But a lower than expected decrease or an increase in inventory could open up 50 levels for Brent and 48.25 for WTI respectively.

FOREX

Absolutely no movement in Dollar this week so far but some volatility can be expected after the Fed and ECB minutes release today. Rupee may see some adjustment to the existing positions before the RBI meet tomorrow.

Dollar Index (100.50) has been trading in the narrowest range seen in a long time and this thin range of 100.35-70 may be resolved soon, probably to the higher side. Similar inertial is seen in Euro (1.0676) too, where the risk of further decline to 1.0580 levels remain still open.

Dollar-Yen (110.74) has broken the support of 110.90-75 and the chances of the upside being capped to 112.00-20 for the week are much higher now with the bears staying in control and immediate support coming near 110.10-109.90.

Pound (1.2440) is in a gradual contracting phase inside our range of 1.2350-1.2600 which may continue for the rest of the week.

Aussie (0.7567) has registered the weekly low so far at 0.7541, marginally higher from our target/support of 0.7530 and now may bounce towards 0.7650-80 in the coming days if 0.7530-00 holds.

The closing above the immediate resistance of 65.00 has opened up 65.20 for Dollar Rupee (65.02) but the chances of the resistance 65.20 holding and pushing Dollar Rupee down once again remain strong at the moment. Even in the best case scenario, the upside may be limited to 65.50-60 in the near term with the downside still open.

INTEREST RATES

The US-Japan 10YR (2.28%) has broken below the support near 2.3% which may now act as an immediate resistance for the coming sessions. In case the yield spread remains below 2.3%, it could possibly come down towards 2.25-2.20% in the near term. That could possibly indicate a fall in Dollar-yen in the next 2-3 sessions.

The US yields have risen slightly. The 5YR (1.88%), 10yr (2.35%) and the 30Yr (2.99%) are up 2-3bps and could rise some more in the near term.

The UK-US 10YR (-1.30%) is headed downwards and if it moves down further towards -1.33%, Pound could extend some more losses in the near term.

The German-US 10YR (-2.10%) is trading just above support levels and could bounce from there. Also watch out for a bounce in Euro in the coming sessions.

Elliott Wave View: EURJPY Correction In progress

Short term Elliott Wave view in EURJPY suggests that cycle from 3/12 peak (122.89) is unfolding as a double three Elliott wave structure where Minor wave W ended at 119.28 and Minor wave X ended at 120.45. Minor wave Y is in progress and the internal is unfolding also as a double three Elliott wave structure where Minute wave ((w)) ended at 117.38 and wave ((x)) bounce is in progress to correct cycle from 3/28 peak (120.445) towards 118.9 – 119.72 area before pair turns lower. As pair is showing a 5 swing bearish sequence from 3/12 peak as well as from 12/14/2016 peak, more downside is expected in the pair. We don’t like buying the proposed bounce and expect sellers to appear at the above area once wave ((x)) bounce is complete in 3, 7, or 11 swing provided that pivot at 3/28 high stays intact in the first degree.

EURJPY 1 Hour Elliott Wave Chart

US ADP Payrolls Report And FOMC Minutes To Guide Markets

The USD is higher against most major pairs as investors are reducing their appetite for risk and flock to safe havens. The JPY is the only of the majors to gain against the dollar on Tuesday's trading session ahead of the release of the first US employment report of the week and the much awaited minutes from the Fed policy meeting in March.

ADP payrolls report will be published at 8:15 am EDT (12:15 pm GMT). The number of jobs added to employers excluding the government and farming industry is forecasted at 191,000. A slowdown of more than 100,000 form last month's giant gain of 298,000, but still a healthy trend for US employment.

The US Institute for Supply Management (ISM) will pots its non-manufacturing index at 10:00 am EDT (2:00 pm GMT). The ISM non-manufacturing index is expected to come in slightly slower than last month at 57.1. The US crude inventories will be released at 10:30 am EDT (2:30 pm GMT). Oil prices have climbed in anticipation of a drawdown in US inventories last week.

The minutes from the March Federal Open Market Committee (FOMC) meeting will be published at 2:00 pm EDT (6:00 pm GMT). Analysts and investors will be looking through the notes looking for more insight into the Fed's balance sheet and their plan to wind it down going forward. The US central bank wants to avoid another 'taper tantrum' like in 2013 so it will carefully pick what gets communicated to markets.

The EUR/USD gained 0.101 in the last 24 hours. The single currency is trading at 1.0661 as the USD gained against most major pairs after risk aversion has gripped the market and made some currencies a safer haven than others. The main topic on the global agenda is the meeting between the Chinese President and US President Donald Trump. Trade and currency manipulation could be part of the discussions, although the market expects a more amicable meeting.

European data will be scarce this week offering little support for the EUR. Last week German confidence was steady at 112.3 and this week PMIs were almost unchanged except a drop in Spanish manufacturing being offset by a gain in Italian data. Retail sales in the EU came in higher than the forecast at 0.7 percent but given the political risk due to the upcoming French elections the EUR will continue to be under pressure as investors look for safe havens.

The USD/MXN gained 0.736 in the Tuesday trading session. The pair is trading at 18.6803 as the peso fell alongside LatAm currencies. The USD gained as risk aversion gripped investors ahead of the China-US meeting in Florida and the employment data in the US to be released on Friday. US economic cada has been mixed with manufacturing slowing down as data released on Monday showed (54.2 vs 55.1 forecasted)but the trade balance deficit shrinking more than expected on Tuesday (–43.6B vs –46.0B forecasted).

The private payroll report from the ADP will mark the start of employment releases in the US with a forecasted 191,000 jobs added to the economy. The NFP at the end of the week is anticipated to bring another addition of 150,000 jobs to the economy as a whole, which could boost the USD higher specially if there is anxiety about the China-US meeting and the aftermath of the terrorist attacks in Russia.

Mexico will release its consumer confidence data on Wednesday at 9:00 am EDT and is expected to improve upon last month's drop as the main negative factor was the Trump administration policies that could impact the Mexican economy. The tone towards Mexico has softened while at the same time other trade deals have been explored to offset the possible scenario of a hard breakup of Nafta, although in the past weeks that scenario has lost traction given the comments from the Trump administration. Timing wise the first round of $20 billion forex hedges set by the Mexican central bank will expire tomorrow.

The price of energy rose 1.078 percent during the Tuesday trading session. West Texas is trading at $50.45 as the market is expecting a drawdown in US inventories to be released tomorrow at 10:30 am EDT by the Energy Information Administration (EIA). US production is a higher concern than global supply as even the end of disruptions in Libya has not impacted crude on the downside.

Oil has managed to remain stable thanks to the efforts of the Organization of the Petroleum Exporting Countries (OPEC) and some non-OPEC members who agreed to limit production seeking to bring crude from the lows seen in 2016. The strategy so far has worked, but oil producers not part of the deal, like the US, have started to ramp up production which is offsetting the boost from the OPEC deal. The production cut agreement is for six months and there have been some signs that some members would be willing to extend if it means price stability given the high compliance seen by the nations that are taking part in the deal.

Market events to watch this week:

Wednesday, April 5

4:30am GBP Services PMI

8:15am USD ADP Non-Farm Employment Change

10:00am USD ISM Non-Manufacturing PMI

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Meeting Minutes

Thursday, April 6

7:30 am EUR ECB Meeting Minutes

8:30am USD Unemployment Claims

Friday, April 7

4:30am GBP Manufacturing Production m/m

8:30am CAD Employment Change

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

*All times EDT