Sample Category Title

EUR/GBP POC Zone Might Reject the Price

As Article 50 has been enacted today, we saw EURGBP dropping prior to official announcement. At this point the EUR is dropping vs GBP but it might change soon. 0.8590-0.8605 (W L4, D L5, historical buyers) is the zone to look for longs. Bullish reversal candlestick pattern with a possible MACD divergence could be a trigger for a move to 0.8700 where D L3 might be retested. Have in mind that ATR has already been overshot so reversal move is more likely to happen.

USDCHF: Extends Bull Pressure, Eyes 1.0000 Zone

USDCHF: The pair looks to extend its upside pressure leaving of bull pressure. On the downside, support lies at the 0.9950 level. A turn below here will open the door for more weakness towards the 0.9900 level and then the 0.9850 level. On the upside, resistance resides at the 1.0000 level where a break will clear the way for more strength to occur towards the 1.0050 level. Further out, resistance comes in at the 1.0100 level. Its daily RSI is bullish and pointing higher suggesting further strength. All in all, USDCHF faces further price strength.

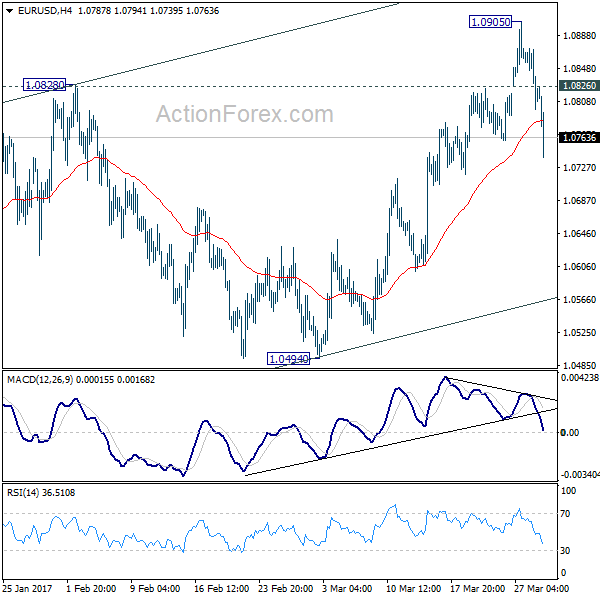

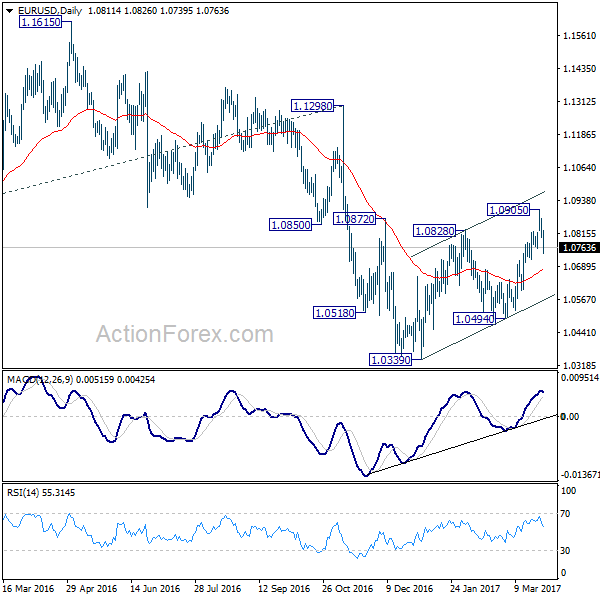

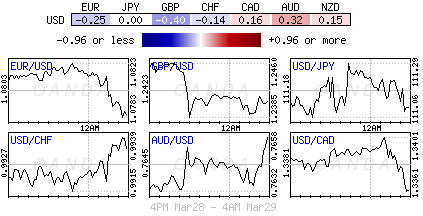

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0784; (P) 1.0828 (R1) 1.0858; More.....

EUR/USD's sharp fall and break of 1.0760 support today argues that rise from 1.0494 has completed at 1.0905 already. Meanwhile, the rise from 1.0339, a corrective move, is possibly finished too. Intraday bias is back on the downside for 55 day EMA (now at 1.0677) first. Sustained break there will affirm this view and target 1.0494 resistance for confirmation. On the upside, above 1.0826 minor resistance will indicate that the corrective rise from 1.0339 is still in progress. Intraday bias would then be flipped back to the upside for 1.0905 and above.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Euro Dives as Markets Over-interpreted ECB Message; Brexit Request Formally Submitted

Euro drops sharply today, taking over Sterling as the weakest major currency for the week. The selloff in the common currency is triggered by reports that the markets have over-interpreted ECB's message in the March meeting. Back than, there was a slight change in the language in the guidance. Markets took that as a sign that ECB is moving closer to stimulus exit. However, Reuters quoted unnamed source saying that policy makers merely wanted to communicate reduced tail risk. There were also talks that ECB could just lift interest rate back from negative to zero first. But another unnamed source described that as "communication nightmare" since markets would automatically price in a few hikes after rate is back to zero. Ad that would push the entire curve sharply higher. Meanwhile, another unnamed source was quoted that policy makers are not too worried about inflation as it has peaked for now with oil price down 10% from recent high.

More on ECB: No ECB Rate Hike or Tapering Until 2018

UK formally submitted Brexit request

UK has finally submitted a formal request for exiting European Union today, triggering the Article 50 of the Lisbon Treaty. EU President Donald Tusk has confirmed receiving the request and tweeted that "after nine months, the UK has delivered". UK Prime Minster Theresa May said that "this is a historic moment from which there can be no turning back". But she emphasized to forge "a deep and special partnership" with EU. And she told the Parliament that "there should be no reason why we should not agree a new and special agreement between the UK and EU that works for all."

The Brexit request is widely expected and May has already announced the schedule. The question now is what comes next. It's generally expected that EU leaders will take a tough stance in the negotiation considering the rise in euroskeptism, nationalism and populism in Europe in general. There are three main topics for negations including immigration, trade relationship and the cost of the "divorce".

Scottish Parliament backs another independence referendum

At the same time the UK is now facing resurgence of Scottish independence risk. The Scottish Parliament approved a plan to request another independence referendum with 69-59 vote yesterday. And that could take place just before UK completes the Brexit process even though the timing was rejected by UK PM May. The British government's Scottish secretary David Mundell said that the government "won't be entering into any negotiation at all until the Brexit process is complete." That should refer to first half of 2019. But Scotland's First Minister Nicola Sturgeon argued that by Autumn 2018, the details of Brexit agreement should be known.

Fed Fischer: Two more hikes seems about right

Fed Vice Chair Stanley Fischer sounded hawkish in his interview by CNBC yesterday. He said that two more rate hikes "seems about right" for this year. He noted that it is "the sensible thing to do" to watch and wait White House's fiscal policies which jumping the gun on the results. US President Donald Trump's failure on health care act changed Fischer's "internal calculus" but the the overall economic outlook. Separately, Fed Governor Jerome Powell said Fed is "getting closer" to achieving maximum employment. Inflation is "still a bit short, but not terribly short" of target. He reiterated that "it's appropriate if we stay on this path for us to gradually raise interest rates."

BoC Poloz: Costs of protectionism are steep

In Canada, BoC Governor Stephen Poloz emphasized yesterday that the "correlation between economic progress and openness" is "striking". And, "when trade barriers are falling, when people are coming to our shores and when investment is rising, Canadians prosper." In response to the current protectionist approach of US Trump, Poloz warned that "protectionism does not promote growth and its costs are steep." Regarding immigration, Poloz said that Canada would have to rely entirely on immigration in less than 30 years to maintain population growth. And, "take away the force of international migration since Confederation, and Canada would be around 10 million people, not 36 million as we are today."

On the data front...

UK mortgage approvals dropped to 68.3k in February, M4 money supply dropped -0.3% mom. German import price rose 0.7% mom in February versus expectation of 0.4% mom. Swiss UBS consumption indicator rose to 1.5 in February. Japan retail sales rose 0.1% yoy in February, below expectation of 0.7% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0784; (P) 1.0828 (R1) 1.0858; More.....

EUR/USD's sharp fall and break of 1.0760 support today argues that rise from 1.0494 has completed at 1.0905 already. Meanwhile, the rise from 1.0339, a corrective move, is possibly finished too. Intraday bias is back on the downside for 55 day EMA (now at 1.0677) first. Sustained break there will affirm this view and target 1.0494 resistance for confirmation. On the upside, above 1.0826 minor resistance will indicate that the corrective rise from 1.0339 is still in progress. Intraday bias would then be flipped back to the upside for 1.0905 and above.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Feb | 0.10% | 0.70% | 1.00% | |

| 6:00 | EUR | German Import Price Index M/M Feb | 0.70% | 0.40% | 0.90% | |

| 6:00 | CHF | UBS Consumption Indicator Feb | 1.5 | 1.43 | ||

| 8:30 | GBP | Mortgage Approvals Feb | 68.3k | 69.5k | 69.9k | 69.1k |

| 8:30 | GBP | M4 Money Supply M/M Feb | -0.30% | 0.50% | 0.90% | |

| 14:00 | USD | Pending Home Sales M/M Feb | 2.00% | -2.80% | ||

| 14:30 | USD | Crude Oil Inventories | 5.0M |

Sterling Erratic as EU Receives Brexit Notice

Sterling displayed explosive levels of volatility during Wednesday's trading session with prices violently swinging between losses and gains as anxiety heightened after Brexit was formally triggered. With investors on edge as Britain officially embarks on an irreversible quest to leaving the European Union, Sterling may be instore for further punishment in the longer term as uncertainty dents buying sentiment. Although Sterling has traded higher following the official triggering of Article 50, it must be kept in mind that hard Brexit fears remain rife with the EU's demand for a £50 billion Brexit bill already adding to the horrible cocktail of potential complications in the early stages of the negotiations.

While most have suggested that Brexit has already been priced in, markets may be in for a rude awakening in the future, especially if Sterling finds itself exposed to further downside shocks amid the rising uncertainty. There is a strong likelihood of the Brexit developments dictating where Sterling trades in the medium to longer term with economic fundamentals almost becoming secondary. With the Brexit fears clearly bone-deep, Sterling weakness may become a recurrent theme moving forward with upside gains limited.

From a technical standpoint, the GBPUSD has staged a modest rebound from the 1.2400 support and such has nothing to do with a change in the bearish sentiment. While Sterling could edge higher in the shorter term as participants reposition, bears may exploit the technical bounce to install fresh rounds of selling. If bears manage to drag prices back below 1.2400 then a decline towards 1.2300 and potentially lower could become a possibility.

Dollar Index eyes 100.00

Dollar bulls were on the offense on Tuesday with the Greenback bouncing from 4-month lows after Federal Reserve officials suggested more rate hikes to come this year. The upside momentum was complimented by the impressive consumer confidence in March which soared to its highest level in more than 16 years. The fact that investors remain cautiously optimism over Donald Trump's pro-growth economic policies despite the recent setbacks could offer some support to the Dollar. While the improving sentiment towards the U.S economy may translate to further upside on the Dollar in the longer term, the lingering uncertainty over Donald Trump could still be enough to limit gains in the short term. From a technical standpoint, the Dollar Index is still pressured on the daily charts but a break and daily close above 100.00 could be the first steps for bulls to reclaim back some control.

Commodity spotlight - WTI Crude

Oil markets received a slight boost on Tuesday with WTI Crude edging higher towards $48.80 after supply distributions in Libya and speculations of OPEC extending the output cut enticed bulls to install light rounds of buying. Regardless of the recent upside, oil prices remain gripped by the oversupply woes with the rapidly diminishing optimism over the effectiveness of OPEC's supply cut limiting upside gains. While speculations may mount over the cartel extending the output cut deal in an effort to stabilize the saturated oil markets, the resurgence of U.S shale may simply counteract the cartel's efforts. A build in the pending crude oil inventories report this evening could expose oil markets to downside risks as the oversupply concerns haunt investor attraction further. From a technical standpoint, WTI Crude remains pressured on the daily charts with bears in firm control below $50. The current technical bounce could create a foundation for sellers to send WTI Crude back towards $48 and potentially lower.

GBP/USD Holds Above Significant Support Post Scottish Referendum Shock

Tuesday evening, March 28, the Scottish parliament has voted by 69 to 59, in favour of holding a second independence referendum. GBP/USD has slumped more than 220 points since Tuesday, from a psychological level at 1.2600, to a 1-week low of 1.2376, breaking the support level at 1.2500.

This morning, the bulls have recovered the significant support level at 1.2400, as a correction after a slump, also because the level provides a stronger support. The bearish momentum has been waning; we will likely see a rebound here.

The 4-hourly Stochastic Oscillator reading is below 30, suggesting a rebound.

However, Theresa May, will trigger Article 50 of the Lisbon treaty today, March 29, starting the 2-year Brexit negotiation process with the EU.

It is still uncertain whether Brexit would be hard or soft, and what kind of final deal would be made. Be aware that downward pressure is still on GBP and GBP crosses with any negative news over Brexit process.

The resistance level is at 1.2460, followed by 1.2475 and 1.2500.

The support line is at 1.2420, followed by 1.2400 and 1.2380.

Trigger Article 50 and Be Done With It

Wednesday March 29: Five things the markets are talking about

U.K PM Theresa May has written a letter that will be delivered by hand to E.U Council President Donald Tusk at around 07:30 EST – only when notification is received in Brussels will Article 50 finally be triggered.

Yesterday, U.K Brexit Minister David Davis stated that he was not targeting a "no-deal" Brexit, but insisted that the government has a "huge contingency plan" for the U.K leaving the E.U without a deal, and that the country would abide by its obligations when settling outstanding liabilities with the E.U.

The triggering of Article 50 is expected to spark long-term volatility for the pound. Current sentiment remains firmly 'bearish' towards sterling moving forward, and the potential resurgence of hard-Brexit fears could ensure price weakness would become a recurring theme.

It will likely take a couple of months for negotiations to start in earnest, with the E.U's 27 other members needing to agree formally how they will approach the talks. Further delaying matters, both sides will need to see the outcome of German elections in September.

Note: GBP has slid more than -1% (£1.2420) within the past 24-hours ahead of today's move by PM May.

Now that Scottish lawmakers voted 69-59 in favour of an "independence referendum" yesterday, sets Edinburgh on a collision course with the U.K government. Messy or what?

Let the gamesmanships "formally" begin!

1. Global stocks get a U.S confidence boost

Stocks in Europe and Asia climbed for a second day amid rising optimism over the strength of the U.S economy and are on course for their fifth consecutive month of gains.

Down-under overnight, Australia's ASX 200 Index and New Zealand's NZX 50 both added at least +0.9%. Singapore's Straits Times Index gained +0.8% and Jakarta's benchmark jumped +0.7%, while Hong Kong's Hang Seng was little changed.

In Japan, the Nikkei (+0.1%) share average produced small gains in choppy trade, but any advances were limited as ex-dividend share price adjustments pressured the market and offset positive U.S sentiment. The broader Topix shed -0.2% – more than three-quarters of its member companies traded ex-dividend.

In Europe, equity indices are trading higher as official Brexit negotiations are scheduled to begin. Banking stocks are leading the gains in the Eurostoxx, while energy, commodity and mining stocks are trading notably higher in the FTSE 100.

U.S stocks are set to open in the black (+0.1%).

Indices: Stoxx50 +0.3% at 3,475, FTSE flat at 7,343, DAX +0.5% at 12,210, CAC-40 +0.3% at 5,061, IBEX-35 flat at 10,384, FTSE MIB flat at 20,327, SMI +0.2% at 8,615, S&P 500 Futures +0.1%

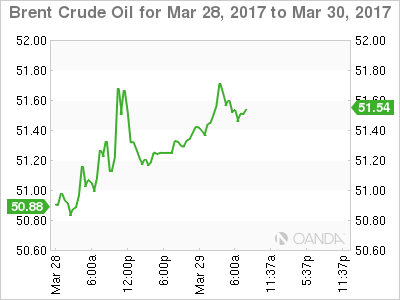

2. Oil rises on Libyan supply disruptions, gold lower

Crude oil prices have extended their gains from yesterday's close, lifted by supply disruptions in Libya and on market expectations that an OPEC-led output reduction will be extended into H2.

Brent crude futures have rallied +29c, or +0.6% to +$51.62 per barrel from Tuesday's close. West Texas Intermediate (WTI) crude futures are up +34c, or +0.7%, at +$48.71 a barrel.

Note: Armed protesters, reducing output by -252k bpd, have blocked oil production from the western Libyan fields of Sharara and Wafa.

Despite OPEC and non-OPEC members agreeing to cut production by almost -1.8m bpd during H1 in order to rein in a global fuel supply overhang and prop up prices, U.S shale oil drillers continue to ramp up their output and exports.

And reason why the market continues to expect another build on weekly crude inventories when EIA release their figures at 10:30 am EST this morning (+1.2m e).

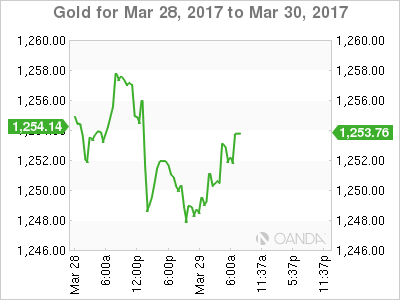

Ahead of the U.S open, gold has slid -0.1% ($1,250.19), paring its Q1 gain to +9%. Some investors believe the 'yellow' metal may be in the early stages of a new "bull" run, and is poised to rally to levels last seen four-years ago as rising inflation and negative real interest rates combine to boost demand.

3. Global yield curves have the confidence to back up

U.S Treasury yields backed up yesterday after consumer confidence (125.6 vs. 113 e) hit its highest level in 17-years and while the Richmond Fed manufacturing data posted a big beat (22 vs. 17).

Yields on U.S 10-year notes are little changed at +2.41%, after yesterday's advance of +4 bps.

In the U.K, the "official" triggering of Article 50 could still generate further market jitters in fixed income if there is any evidence of disagreements about 'how to negotiate' before negotiations even begin.

Note: U.K 10-year gilt yields (+1.19%) dropped right after the U.K. gave notice of triggering Article 50, even though PM May was expected to do so by the end of Q1.

While on mainland Europe, a strengthening eurozone economy and higher inflation expectations are the main cause for rising yields. German 10-year bunds have backed up +2bps to +0.38%.

Note: On the day after the Brexit vote (June 24, 2016), German 10's saw the yield drop to a low of -0.17%.

4. Dollar pulls away from multi month lows

The 'mighty' dollar is a tad firmer overnight; pulling away from its four and half month lows as impressive U.S economic strength has kept the door ajar for continued 'gradual' rate hikes by the Fed. A number of Fed officials (Powell, Kaplan and George) this week have reiterated their views for steady pace in 'normalization.' For now, rate differentials remain the dollars biggest supporter, especially as other central banks (BoC and SNB) have hinted that it was too premature to consider tightening at this time.

GBP/USD (£1.2420) remains under pressure as the Brexit process is set in motion. The pair was off -0.5% in early trading. The trick now is to figure out if the market has already priced a 'hard Brexit'?

Ahead of the U.S open, EUR/USD is trading atop of its O/N lows at €1.0791, USD/JPY is at ¥111.00.

Elsewhere, Thailand's CB kept their overnight benchmark (+1.5%) rates steady. Officials noted that the THB currency strength ($34.38) was not good for the economy. Investors should expect THB to face higher short-term volatility.

5. German import prices rise

On a light day on the economic front, data this morning showed that German import prices increased at the fastest pace in nearly six-years last month.

Import prices climbed by +7.4% year-on-year in the month, the highest rise since April 2011, when prices surged +7.6%.

At the same time, export prices climbed +2.5%, faster than January's +1.8% increase.

On Monday, German Ifo Business Climate in March, rose to 112.3 points and marked its highest level since July 2011 and supports high optimism in the business sector, despite rumblings of protectionism from the U.S and the uncertainty in Europe over the imminent Brexit negotiations.

Note: The German economy has enjoyed a robust Q1. Later this week, Germany releases key consumer and employment numbers, including CPI, retail sales and unemployment claims.

DAX Steady As German Import Prices Beats Estimate

The DAX Index has ticked lower in the Wednesday session, as the DAX trades at 12,194.25. On the release front, it's another light day. The sole eurozone event is German Import Prices, which gained 0.7%. This beat the estimate of 0.4%. On Thursday, Germany releases Preliminary CPI and the US publishes Final GDP.

The DAX has moved higher this week, bolstered by a sparkling reading from German Ifo Business Climate in March. The indicator climbed to 112.3 points, its highest level since July 2011. The excellent release underscores high optimism in the business sector, despite rumblings of protectionism from the US and the uncertainty in Europe over the imminent Brexit negotiations. Stronger global demand has led to increased German exports, notably cars and machinery. Germany's GDP expanded 1.6% in 2016, its highest rate since 2012. The economy has enjoyed a robust first quarter, and this has helped boost growth in the eurozone. Later this week, Germany releases key consumer and employment numbers, including CPI, retail sales and unemployment claims. Any unexpected readings could have a strong impact on the movement of EUR/USD.

President Donald Trump was on the wrong end of the rough-and tumble politics in Washington, as his bill to replace the Affordable Care Act was pulled before it even went to a vote. This was a humiliating setback for Trump, given that the Republicans enjoying a majority in Congress. The bruising defeat has sent the US dollar sharply lower and market jitters higher. Trump's administration has stumbled out of the starting gate, and after more than two months in office, he has yet to provide any details over even an outline of economic policy. The inquiry into the Trump administration's links with Russia is gathering steam, and is another cause for concern for nervous investors. Trump has said he will now focus on tax reform, but he has his work cut out, trying to convince a skeptical Congress and general public that he can deliver the goods and push his tax legislation through Congress.

Sterling Slips ahead of Article 50 Trigger

US consumer confidence rose significantly in March. At 125.6, it is the highest level since December 2000 and well above any forecasts. Add to that the annual rise in house prices of 5.7% – also above expectation – and there is every reason to see US Dollar strength. That strength may also come from the triggering of Article 50 by the UK.

Sir Tim Barrow, Britain's permanent representative to the European Union, will deliver the letter notifying Donald Tusk, the president of the European Council, that Britain is to leave the EU in two years. Let the negotiations begin! Sterling had been rising ahead of this event, but slipped overnight as it dawned on traders that the big day had arrived. The confirmation of the event could well return some strength in the Pound but uncertainty is still a nerve racking experience for investors, so volatile trading conditions are kind of inevitable over the next 48 hours.

If you have a currency requirement, placing an automated order trying to target rates above or below the current market level is an eminently sensible thing to do at a time when volatility is so widely expected.

I should mention that we will get UK mortgage lending data this morning and that is expected to be positive, but it'll be lost in the melee of traders setting themselves up to take advantage of or protect against today's announcement.

Sadly, that is about all of the tier one data we expect today. We will get a couple of speeches from Federal Reserve members in the US and a speech from a member of the European Central Bank, but these are unlikely to be market moving. By way of contrast, Thursday offers a swathe of data from across the globe – and that will be influential as we approach the end of the month, the quarter and the financial year in many corporates.

Thought for the day

You'll never know how many people you dislike until you have to choose your baby's name.

European Market Update: Brexit Divorce Process Set To Begin

Brexit divorce process set to begin

Notes/Observations

Brexit process begins and formally sets off two years of negotiations

European confidence data mixed (France in-line, Sweden misses, Italy beats)

Overnight:

Asia:

BOJ's Sato: Labor market reforms and other measures to boost potential growth must accompany monetary easing to raise long-term inflation expectations

PBoC skipped its open market operations (OMO) for 4th straight session; drained CNY70B v CNY70B prior; Shanghai Composite -0.4%

Europe:

PM May signed letter invoking Article 50 that would begin the 2-year Brexit negotiation process; letter expected to be delivered to EU on Wed

BOE's McCafferty (former hawk) stated that BOE would be raising interest rates when economy was strong enough. Did not know whether he would vote for a rate hike at next MPC meeting. Growth in UK would likely to become anemic rather than enter recession

Germany Fin Min Schaeuble reportedly rejected deferment of Greek interest payments believing it would amount to a new loan

SNB's Maechler stated that he expected world interest rate environment to persist at low levels for some time. Inflation was a large reason for SNB keeping monetary policy unchanged earlier this month; inflation outlook remains fragile

Americas:

Fed Chair Yellen: job market has improved substantially since recession; pockets of persistently high US unemployment remain

Fed's Powell (moderate, voter) Fed should be moving slowly toward a more neutral stance and saw scope for more rate hikes this year

Fed's Kaplan (moderate, voter): reiterates Fed should be taking steps to raise rates patiently and gradually

Fed's George (hawk, non-voter): FOMC is committed to raising rates gradually; quick rate hikes would be a shock to the economy

Energy:

Weekly API Oil Inventories: Crude: +1.9M v +4.5M prior (8th build in the past 10 weeks)

Economic Data

(JP) Japan Mar Small Business Confidence: 50.5 v 47.7 prior (1st time above the 50 level since Mar 2014)

(DE) Germany Feb Import Price Index M/M: 0.7% v 0.4%e; Y/Y: 7.4% v 7.0%e

(CH) Swiss Feb UBS Consumption Indicator: 1.50 1.44 prior

(FR) France Mar Consumer Confidence (in-line): 100 v 100e

(SE) Sweden Mar Consumer Confidence (miss): 102.6 v 104.0e; Manufacturing Confidence (miss): 112.7 v 117.0e; Economy Tendency Survey: 109.2 v 110.6e

(TH)Thailand Central Bank (BOT) left its Benchmark Interest Rate unchanged at 1.50% (as expected)

(IT) Italy Mar Consumer Confidence (beat): 107.6 v 106.6e; Manufacturing Confidence (beat): 107.1 v 106.0e, Economic Sentiment: 105.1 v 104.3 prior

(CH) Swiss Mar Credit Suisse Expectations Survey: 29.6 v 19.4 prior

(UK) Feb Net Consumer Credit: £1.4B v £1.3Be; Net Lending: £3.5B v £3.5Be

(UK) Feb Mortgage Approvals: 68.3K v 69.1Ke

Fixed Income Issuance:

(IN) India sold total INR100B vs. INR100B indicated in 3-month and 12-month Bills

(EU) ECB allotted $4.5B in 7-day USD Liquidity Tender at fixed 1.36% vs $1.01B prior

(NO) Norway sold NOK4.0B vs. NOK4.0B indicated in 2027 bonds; Avg Yield: 1.70% v 1.74% prior; Bid-to-cover: 2.30x v 2.41x prior (IT) Italy Debt Agency (Tesoro) sold €6.5B vs. €6.5B indicated in 6-month Bills ; Avg yield: -0.294% v -0.294% prior; Bid-to-cover: 1.59x v 1.52x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 +0.3% at 3,475, FTSE flat at 7,343, DAX +0.5% at 12,210, CAC-40 +0.3% at 5,061, IBEX-35 flat at 10,384, FTSE MIB flat at 20,327, SMI +0.2% at 8,615, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European equity indices are trading higher as official Brexit negotiations are scheduled to begin later in the session, and as market participants digest Trump's failed health-care bill; Banking stocks trading generally higher across the board; shares of Engie leading the gains in the Eurostoxx after receiving an analyst upgrade overnight, with banking stocks Deutsche Bank, BNP and ING also trading higher; shares of 3I leading the gains in the FTSE 100 after receiving an analyst upgrade; energy, commodity and mining stocks also trading notably higher in the index as copper and oil prices trade higher intraday.

Upcoming scheduled US earnings (pre-market) include Omnova Solutions, Paychex, SecureWorks, and Unifirst Corp.

Equities (as of 09:45 GMT)

Consumer Discretionary: [Flybe Group FLYB.UK -5.2% (trading update, analyst downgrade), Grammer GMM.DE +5.9% (FY16 results, raises div), TUI TUI.UK -0.1% (trading update)]

Energy: [SMA Solar S92.DE +1.9% (sale of subsidiary SMA Railway Technology, outlook)]

Financials: [3i Group III.UK +2.8% (analyst upgrade)]

Healthcare: [Allergy Therapeutics AGY.UK +7.8% (H1 results), Circle Holdings CIRC.UK +21.9% (to be acquired by Toscafund for 30p/shr cash; FY16 results), Stada Arzneimittel SAZ.DE -0.8% (final FY16 results)]

Industrials: [Daimler DAI.DE +1.3% (CEO comments), Stagecoach SGC.UK +3.2% (trading update, analyst upgrade), Sika SIK.CH +0.6% (raises dividend)]

Technology: [Euromicron EUCA.DE +2.9% (FY16 results), Siemens SIE.DE +1.1% (unit awarded $4.13B DoD contract)]

Utilities: [Engie ENGI.FR +2.9% (analyst upgrade)]

Speakers

UK Chancellor Hammond expressed optimism that the UK could get a sensible and pragmatic deal with Europe. Sought a deep and special relationship with EU and understand that UK could not cherry pick. Confident could get a new EU customs agreement and wanted security and defense ties

Swiss KOF Institute spring forecasts noted that Swiss economy was in good shape and growth prospects were encouraging. Sluggish employment growth was likely to hold back any major improvement of the unemployment rate. Inflation was back in the positive zone, a significant increase in prices was not expected

South Africa Central Bank (SARB) stated that it would not bow to any pressure (**Reminder: SARB meets on Thursday, Mar 30th)

Thailand Central Bank Policy Statement noted that the decision to keep policy steady was unanimous. Reiterated view that monetary policy to remain accommodative and ready to use appropriate policy mix. Govt spending was driving the economy and saw greater risks to growth. Reiterated view that THB currency (Baht) strength was not good for economy; FX could face higher volatility

Currencies

The formal trigger of the Brexit process was the main theme in the session. PM May signed the letter invoking Article 50 that would begin the Brexit process while Sir Tim Barrow, the UK's permanent representative in Brussels would formally hand over Article 50 letter from the British government to the European council president, Donald Tusk later in the session.

GBP/USD was under pressure as the Brexit process was being set in motion. The pair was off approx. 0.5% in early European trading. Dealers cited "Brexit anxiety' for the GBP's soft tone although some analyst pondered whether investors had already priced a ‘hard Brexit'.

The USD was a tad firmer over the past 24 hours as impressive US economic strength kept the door open for continued gradual rate hikes by the Fed. Numerous Fed officials over the past day reiterated their view for steady pace in normalization. Interest rate divergences still remain in favor for the greenback (Both BOC and SNB hinted that was premature to consider tightening at their respective central banks at this time.

Fixed Income:

Bund futures trade at 160.57 down 3 ticks recovering from earlier 160.18 lows, as earlier equity strength begins to wain. Resistance remains at 160.74 then 161.06 followed by 161.44. Support remains at 160.04 followed by 159.73 then 159.41.

Gilt futures trade at 126.83 down 24 ticks, as Britain formally triggers Article 50. Support remains at 126.30 followed by 126.05. Resistance remains at 127.35 followed by 127.89. Short Sterling futures trade flat to down 1bp with Jun17Jun18 spread inching higher to 23.5Bp.

Wednesday's liquidity report showed Tuesday's excess liquidity rose to €1.347T a rise of €14B from €1.333T prior. Use of the marginal lending facility rose to €319M from €207M prior.

Corporate issuance saw a pick up with $10.9B coming to market via 7 issuers headlines by Applied Materials $2.2B 2 part offering, Rockwell Collins $4.65B 5 part offering and Ford 3 part $1.75B offering. This puts monthly issuance at $119.5B.

Looking Ahead

05:30 (EU) ECB allotment in 3-month LTRO tender

05:35 (SE) Sweden Central bank (Riksbank) Dep Gov Floden

06:00 (RU) Russia to sell OFZ Bonds

06:00 (FI) Finland to sell €1.0B in 0.00% Sept 2023 RFGB bond

06:00 (CZ) Czech Republic to sell 0.95% 2030 bond

06:45 (US) Daily Libor Fixing

07:00 (US) MBA Mortgage Applications w/e Mar 24th: No est v -2.7% prior

07:00 (UK) PM May question time in House of Commons

07:30 (UK) UK official to deliver Article 50 letter to EU

08:00 (BR) Brazil Jan IBGE Services Sector Volume Y/Y: No est v -5.7% prior

08:15 (UK) Baltic Dry Bulk Index

08:45 (EU) EU President Tusk on Brexit - 09:20 (US) Fed's Evans (dove, voter)

09:30 (BR) Brazil Feb Total Outstanding Loans (BRL): No est v 3.074T prior; M/M: No est v -1.0% prior

09:45 (DE) German Chancellor Merkel attends conference in Berlin

10:00 (US) Feb Pending Home Sales M/M: +2.5%e v -2.8% prior; Y/Y: No est v 2.7% prior

10:30 (US) Weekly DOE Crude Oil Inventories

11:00 (EU) EU's Moscovici participates in Citizens Dialogue in Brussels

11:30 (US) Fed's Rosengren (moderate, non-voter) in Boston

11:30 (US) Treasury to sell 2-Year Floating Rate Notes Reopening

12:00 (CA) Canada to sell 2-Year Bonds

12:50 (BE) ECB's Praet (Belgium, chief economist) in Frankfurt

13:00 (US) Treasury to sell 7-Year Notes

13:15 (US) Fed's Williams (moderate, non-voter) in NY