Sample Category Title

Brent Oil Returned above 200 SMA

Brent oil returned above 200 SMA ($50.80), following several unsuccessful attempts to clearly break below it, with one of downticks also briefly probing below psychological $50.00 support.

Overall structure remains weak and sees risk of renewed attempts lower and final break below 200SMA and $50 support.

Daily Tenkan-sen ($51.17) limits upside attempts for now, however, room for further upticks exists.

Strong resistance zone between $52.34 and $52.63 (Fibo 38.2% of $56.62/$49.70 downleg / falling 20SMA / 16 Mar lower top) should cap extended recovery actions, before broader bears resume.

Below $50.00/$49.70 triggers, next good support lies at $49.1 (Fibo 61.8% of $43.56/$58.36).

Res: 51.17; 51.33; 51.57; 52.34

Sup: 50.80; 50.00; 49.70; 49.21

Dollar Crossroads

In a perfect world, every breakout is clean and steady but on Monday the US dollar fell below some critical levels but bounced instead of wilting. We look at what's coming next. Yellen's speech about labout markets due at 12:50 ET (17:50 London). After closing both EURCAD and EURAUD trades at a profit, one of the traded will be re-opened later this evening. Which one will it be? Find out in the Premium video due up shortly.

Yen is again the best performer. followed by the franc and pound, while Kiwi and Aussie are the worst performers. As the healthcare deal fell apart on Friday, it held together. But on Monday as the Republican party looked like it was straining, the dollar began to crumble.

We have been writing about the burgeoning positive signs in the euro for weeks and on Monday it finally broke out. EUR/USD was the big technical story as it broke the February and December highs as it gapped higher. It continued through the 200-day moving average and 1.09 as levels cascaded.

It was similar in GBP/USD and USD/JPY as important levels were tested. What finally stopped the selling was support at 110.00 in USD/JPY and GBPUSD resistance at 1.2640. That held and then sentiment began to turn. The S&P 500 proved it's a juggernaut once again as it erased a 22-point decline to finish just 2 points lower.

Economic news is light. Fundamentally the focus remains on politics. Talk that Republicans hadn't yet given up on healthcare was perhaps the positive spark but that might be stretching it.

Another factor to note was quarter-end and Japanese fiscal year end. Flows will be lumpy and the market will thin in the days ahead. Ideally, the dollar would break and it would extend but given the politics and calendar, it's not a surprise that the market is tentative. There isn't a screaming reason to sell dollars even if Republicans stumbled further. What we will probably see is a continue paradigm where the US dollar has small gains on good news and large losses on bad news.

The Asia-Pacific calendar is light but we note that Japanese economic minister Ishihara said authorities are closely watching market moves. That's soft jawboning but expect more if USD/JPY breaks 110.00.

Trade Idea Update: USD/CHF – Sell at 0.9910

USD/CHF - 0.9840

Original strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

The greenback found support at 0.9813 yesterday and has recovered, suggesting consolidation above this level would be seen and corrective bounce to 0.9880 is likely but upside should be limited to 0.9900-10 and bring another decline later, below said support at 0.9813 would confirm recent decline has resumed and extend weakness to 0.9795-00, however, loss of downward momentum should prevent sharp fall below 0.9770-75 (100% projection of 1.0171-0.9942 measuring from 1.0003), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on subsequent rebound as 0.9900-10 should limit upside. Only above said resistance at 0.9960 would abort and signal low is formed, bring retracement of recent decline towards indicated previous resistance at 1.0003.

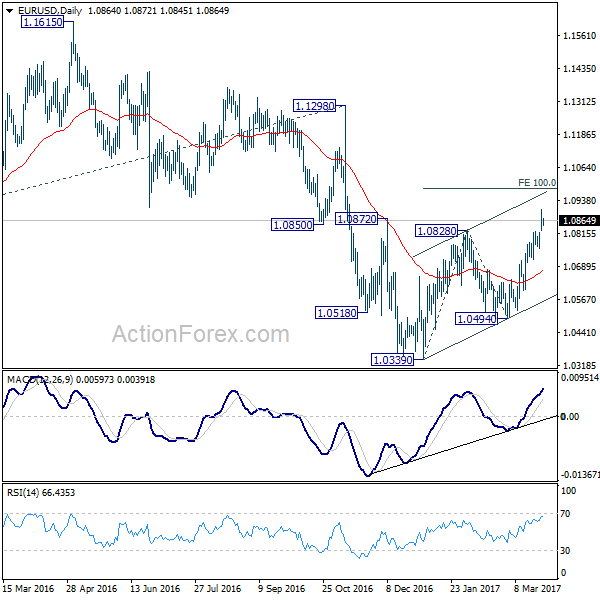

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0822; (P) 1.0864 (R1) 1.0904; More.....

A temporary top is in place at 1.0905 and intraday bias in EUR/USD is turned neutral for some consolidations. Further rise is expected as long as 1.0760 minor support holds. Above 1.0905 will turn bias to the upside for 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. At this point, we're still treating rise from 1.0339 as a correction. Hence, we'd expect strong resistance from 1.0983 to limit upside and bring near term reversal. On the downside, break of 1.0760 support will turn bias back to the downside for 1.0494 support. However, firm break of 1.0983 will dampen our view and put focus on 1.1298 key resistance.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

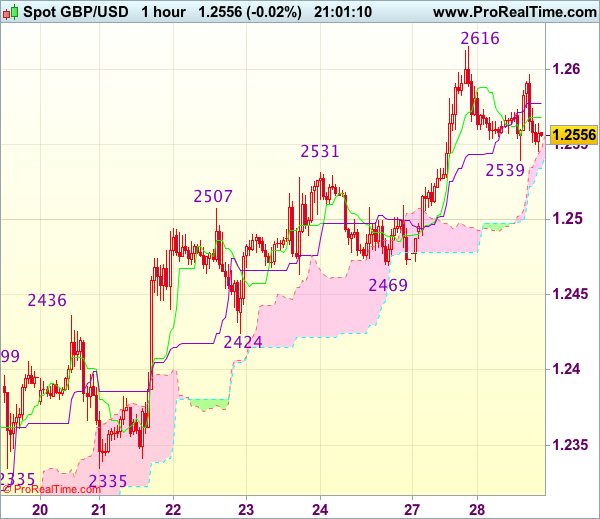

Trade Idea Update: GBP/USD – Buy at 1.2490

GBP/USD - 1.2551

Original strategy :

Buy at 1.2490, Target: 1.2600, Stop: 1.2455

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2490, Target: 1.2600, Stop: 1.2455

Position : -

Target : -

Stop : -

Cable’s retreat after rising to 1.2616 yesterday suggests consolidation below this level would be seen and below 1.2530 would bring retracement to 1.2490-00, however, price should stay well above support at 1.2469, bring another upmove later, above said resistance at 1.2616 would extend recent rise from 1.2109 to 1.2635-40, however, loss of upward momentum should prevent sharp move beyond 1.2670-80 and price should falter below previous resistance at 1.2706, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent retreat. Only below support at 1.2469 (Friday’s low) would abort and signal top is formed, bring retracement of recent upmove towards previous support at 1.2424 which is likely to hold from here.

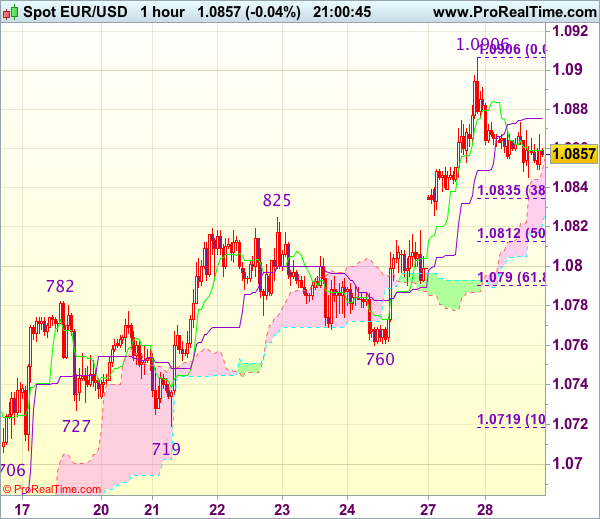

Trade Idea Update: EUR/USD – Buy at 1.0800

EUR/USD - 1.0863

Original strategy :

Buy at 1.0800, Target: 1.0900, Stop: 1.0765

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0800, Target: 1.0900, Stop: 1.0765

Position : -

Target : -

Stop : -

As the single currency has retreated after surging to 1.0906 yesterday, suggesting consolidation below this level would be seen and pullback to 1.0835 (38.2% Fibonacci retracement of 1.0719-1.0906) is likely, however, reckon downside would be limited to 1.0810-15 (50% Fibonacci retracement), bring another rise later, above said resistance at 1.0906 would extend recent upmove to 1.0930-35 (61.8% Fibonacci retracement of 1.1300-1.0340) but loss of near term upward momentum should prevent sharp move beyond 1.0955-60 and price should falter below 1.0990-00.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0800-10 should limit downside. Only below support at 1.0760 would abort and signal top is formed, bring retracement of recent upmove to 1.0730 but 1.0719 support should remain intact.

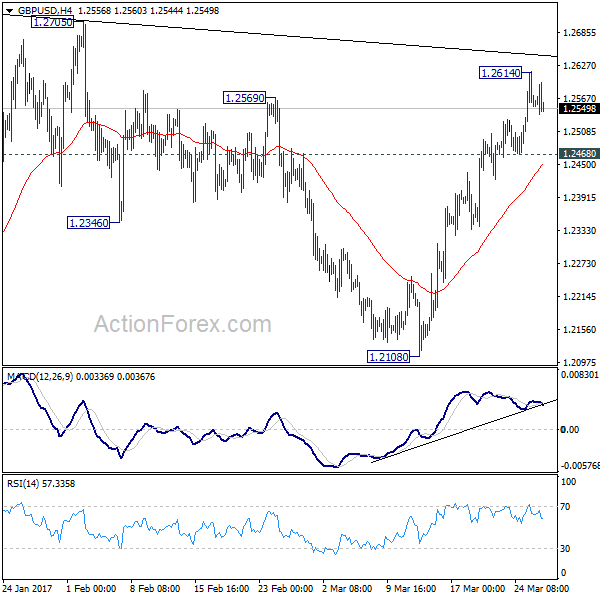

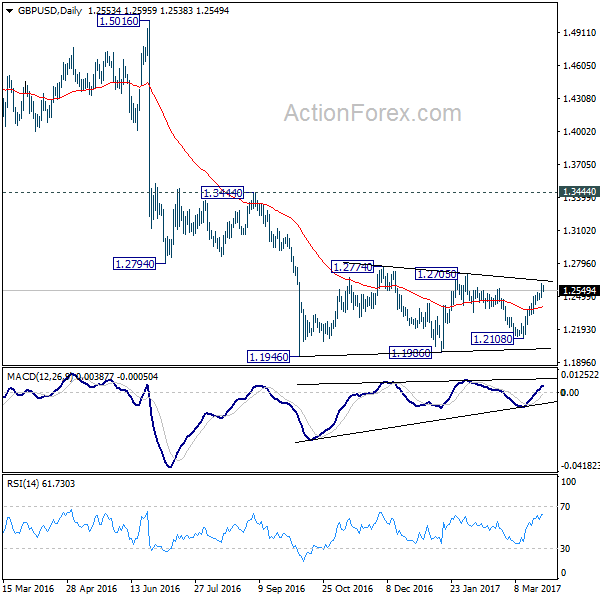

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2488; (P) 1.2551; (R1) 1.2621; More...

A temporary top is in place at 1.2614 in GBP/USD. Intraday bias is turned neutral for some consolidations. Another rise is expected as long as 1.2468 minor support holds. Above 1.2614 will target 1.2705/2774. Nonetheless, rise from 1.2108 is seen as part of the consolidation pattern from 1.1946. We'd expect upside to be limited by 1.2705/2774 to bring down trend resumption eventually. On the downside, below 1.2468 minor support will turn bias back to the downside for 1.2108 support first. Though, sustained break of 1.2774 will extend the rise towards 1.3444 key resistance level.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Trade Idea Update: USD/JPY – Sell at 111.20

USD/JPY - 110.30

Original strategy :

Sell at 111.20, Target: 110.20, Stop: 111.55

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.20, Target: 110.20, Stop: 111.55

Position : -

Target : -

Stop : -

The greenback recovered after falling to 110.11 and consolidation above this level would be seen and corrective bounce to 110.95-00 cannot be ruled out, however, reckon upside would be limited to 111.15-20 (38.2% Fibonacci retracement of 112.90-110.11) and price should falter well below resistance at 111.48, bring another decline later, below said support at 110.11 would signal recent decline is still in progress and may extend weakness to 109.95-00 but loss of downward momentum should prevent sharp fall below 109.70-75 and reckon 109.50 would hold.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 111.15-20 should limit upside. Above 111.48-51 (previous resistance and 50% Fibonacci retracement of 112.90-110.11) would abort and signal low is formed, bring a stronger rebound to 111.80-85 first (61.8% Fibonacci retracement).

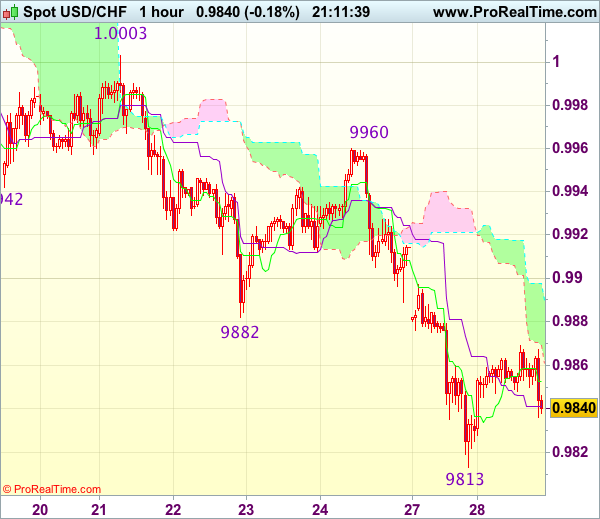

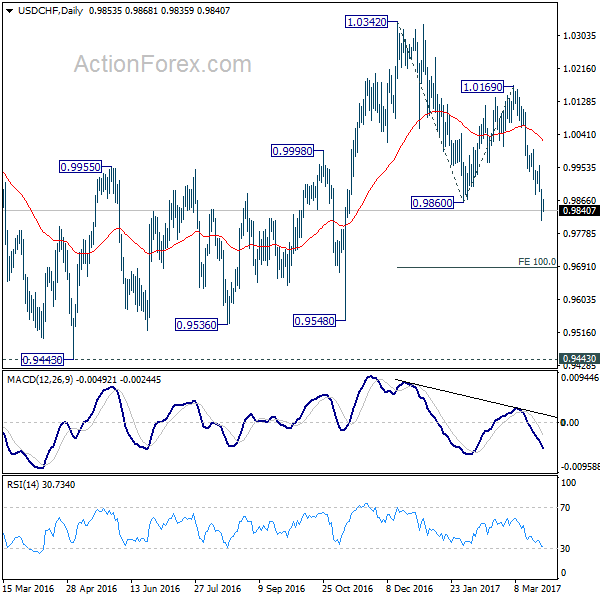

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9812; (P) 0.9854; (R1) 0.9894; More.....

Intraday bias in USD/CHF is turned neutral with a temporary low in place at 0.9812. Some consolidation could be seen. But deeper fall is still expected as long as 0.9959 resistance holds. Below 0.9812 will extend the current decline from 1.0342 to 100% projection of 1.0342 to 0.9860 from 1.0169 at 0.9687 and possibly below. However, break of 0.9959 will indicate short term bottoming and turn bias back to the upside for 55 day EMA (now at 1.0022).

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of deeper fall, we'd expect strong support from 0.9443/9548 support zone.

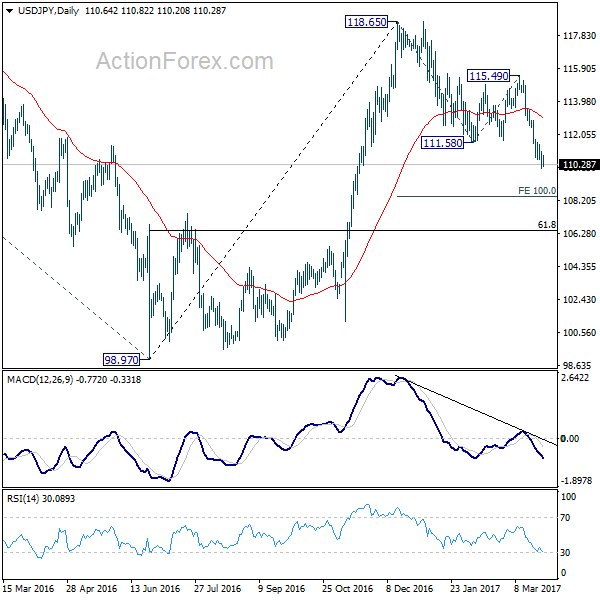

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.16; (P) 110.60; (R1) 111.10; More...

USD/JPY consolidates above 110.10 temporary low and intraday bias is neutral for the moment. As long as 111.57 resistance holds, deeper decline is expected in the pair. Below 110.10 will extend the current fall from 118.65 to 100% projection of 118.65 to 111.58 from 115.49 at 108.42 and possibly below. Meanwhile, firm break of 111.57 will indicate short term bottoming and bring rebound back to 55 day EMA (now at 113.09).

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. sustained trading below 55 week EMA (now at 111.11) will indicates that such consolidation is not completed. And another fall would be seen back to 98.97 as the third leg. In that case, downside would be contained by 61.8% retracement of 75.56 to 125.95 at 94.77 to complete the correction. On the upside, above 115.49 will extend the rise from 98.97 to retest 125.85 first. Overall, up trend from 75.56 is expected to resume after the consolidation from 125.85 completes.