Sample Category Title

EUR/GBP Mid-Day Outlook

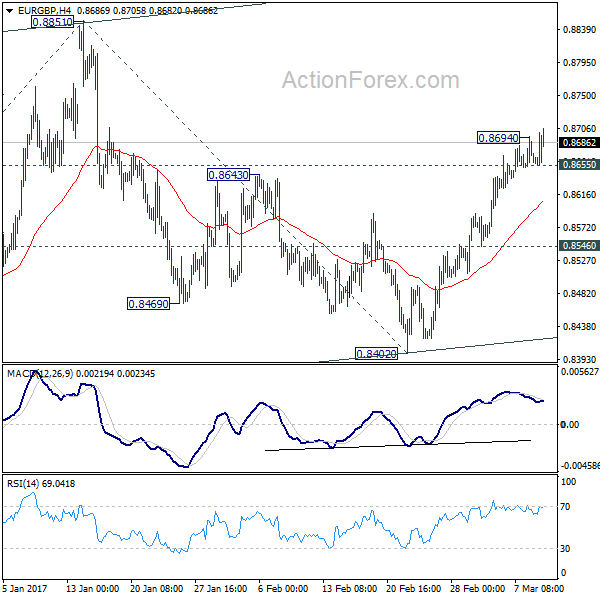

Daily Pivots: (S1) 0.8645; (P) 0.8670; (R1) 0.8686; More...

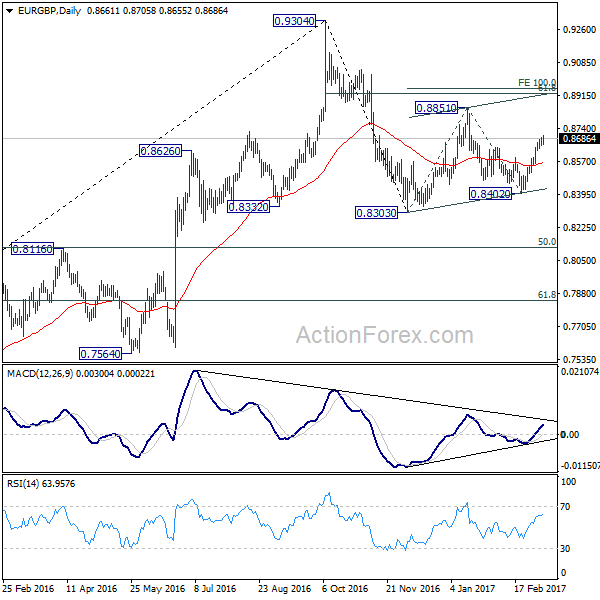

EUR/GBP breaches 0.8694 temporary top but with weak upside moment as seen in 4 hour MACD. Nonetheless, intraday bias is mildly back on the upside side. Rise from 0.8402 is viewed as the third leg of the corrective price actions from 0.8303.Such rally would target 0.8851 resistance and above. However, whole price actions from 0.8303 are viewed as the second leg of the correction from 0.9304. Hence, we'd expect strong resistance from 100% projection of 0.8303 to 0.8851 from 0.8402 at 0.8950 to limit upside. On the downside, below 0.8655 minor support will turn bias neutral again. But further rise would remain in favor as long as 0.8546 support holds.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Deeper fall cannot be ruled out yet. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Overall, the corrective pattern would take some time to complete before long term up trend resumes at a later stage. Break of 0.9304 will pave the way to 0.9799 (2008 high).

Trade Idea: EUR/GBP – Buy at 0.8600

EUR/GBP - 0.8697

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Buy at 0.8600, Target: 0.8700, Stop: 0.8560

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8600, Target: 0.8700, Stop: 0.8560

Position : -

Target : -

Stop : -

As the single currency has edged higher again after recent rally above resistance at 0.8646, adding credence to our view that the fall from 0.8857 has ended at 0.8403 and upside bias remains for the rally from there to extend further gain to 0.8740-50, however, loss of near term upward momentum should prevent sharp move beyond 0.8770 and price should falter well below 0.8800, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on pullback as 0.8600 should limit downside. Below support at 0.8547 would suggest first leg of rebound from 0.8403 has ended, bring weakness to 0.8520-25 but support at 0.8509 should contain downside and bring another rise later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Buy at 1.3400

USD/CAD - 1.3507

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term down

Original strategy :

Buy at 1.3375, Target: 1.3525, Stop: 1.3315

Position: -

Target: -

Stop: -

New strategy :

Buy at 1.3400, Target: 1.3570, Stop: 1.3340

Position: -

Target: -

Stop:-

The greenback has continued trading with a firm undertone, suggesting recent upmove from 1.2969 is still in progress and may extend further gain to 1.3570-75, overbought condition should prevent sharp move beyond 1.3600-10 and reckon 1.3650 would hold from here, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy on pullback as 1.3400-10 should limit downside. Only below minor support at 1.3372 would defer and suggest top is possibly formed, risk correction to 1.3330 and possibly to 1.3290-00 but price should stay well above indicated previous resistance at 1.3212 (now support), bring another rise later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

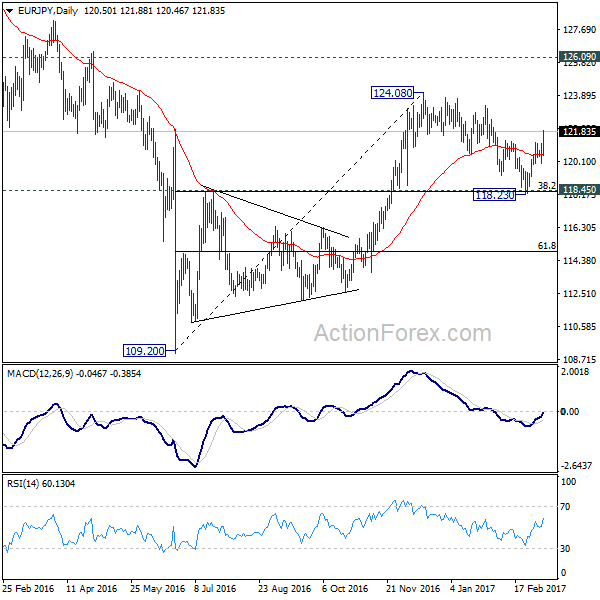

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 120.01; (P) 120.56; (R1) 121.11; More...

EUR/JPY's strong rally today and break of 121.32 resistance firstly confirms resumption of rise from 118.23. More importantly, this should confirm completion of the corrective fall from 124.08, after defending 118.45 cluster support (38.2% retracement of 109.20 to 124.08 at 118.39). Intraday bias is now back on the upside for a test on 123.30/124.08 resistance zone. Break will extend larger rally from 109.20 to next key resistance at 126.09. On the downside, break of 120.01 support is now needed to indicate completion of the rise from 118.23. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 109.20 medium term bottom are seen as part of a medium term corrective pattern from 149.76. Strong rebound from 118.45 resistance turned support suggests that it's still in progress. Break of 124.08 will target 126.09 key resistance level. We'd be cautious on strong resistance there to limit upside. However, sustained break there will be a strong sign of medium term momentum and could target 141.04 resistance next.

Euro Lifted by Cautiously Upbeat Draghi … For Now

Euro hesitates initially after ECB kept monetary policies unchanged today as widely expected. Markets seem to be unsure about the relatively slight revision in 2018 and 2019 inflation projections. Nonetheless, the overall cautious yet positive tone in president Mario Draghi's press conference is giving the common currency some support. EUR/JPY took out 121.32 resistance earlier today and stays firm. EUR/AUD is also extending recent rebound. At the same time, while EUR/USD rebounds, it's bounded in recent range of 1.0493/0630 and maintains a neutral outlook. EUR/GBP breached 0.8694 temporary top earlier today but lack follow through momentum. Euro traders would likely turn their focus back to politics once the impact from ECB fades.

As planned, monthly asset purchase size will be lowered to EUR 60b starting April, down from current EUR 80b. The asset purchase program (APP) will run till December 2017. Main refinancing rate is held at 0.00% while deposit rate is kept at -0.4%. ECB stayed open to further easing and noted that "we stand ready to increase our asset purchase programme in terms of size and/or duration."

Growth and inflation projection revised up

In the introductory statement to press conference, ECB president Mario Draghi acknowledged the increase in "headline inflation" and attributed that "largely on account of rising energy and food price inflation." Inflation would likely stay around 2% level "in the coming months. However, he also pointed out that "underlying inflation pressures continue to remain subdued." And ECB will look through the changes "if judged to be transient".

In the updated staff macroeconomic projections ECB projects headline HICP to hit 1.7% in 2017, 1.6% in 2018 and 1.7% in 2019. 2017 projection was significantly revised up. But for 2018, that was just a "slight revision" while 2019 projection was unchanged.

ECB now sees GDP to grow 1.8% in 2017, 1.7% in 2018 and 1.6% in 2019. There were "slight" upward revision in 2017 and 2018. Draghi also noted that "the risks surrounding the euro area growth outlook have become less pronounced, but remain tilted to the downside and relate predominantly to global factors."

US initial claims jumped 20k, stayed low

US initial jobless claims rose 20k to 243k in the week ended March 4, above expectation of 237k. The four week moving average rose to 236.5k, up from 234.25k. That, nonetheless, marketed the 105 straight week of sub 300k reading, the longest streak since 1970. Continuing claims dropped 6k to 2.06m in the week ended February 25. Challenger report showed -40% yoy drop in planned layoffs in February. Import price index rose 0.2% mom in February. Released from Canada new housing price index rose 0.1% mom in January. Capacity utilization rate rose to 82.2% in Q4.

Oil Slump drags down commodity currencies

Commodity currencies are generally weak today. In particular, Canadian dollar is dragged down by weakness in oil price. WTI's fall accelerates this week and broke 50 handle to as low as 48.79 so far. The DOE/EIA reported yesterday that total crude oil and petroleum products stocks dropped -2.38 mmb to 1346.83 mmb in the week ended March 3. Crude oil inventory soared 8.21 mmb to 528.39 mmb with stock-builds seen in ALL of 5 PADDs. Cushing stock gained 0.87 mmb to 64.4 mmb while utilization rate dropped -0.1% to 85.9%. For refined oil products, gasoline inventory sank -6.56 mmb to 249.33 mmb although demand gained 6.7% to 9.27M bpd. Production increased 4.1% to 9.84M bpd while imports slumped -47.07% to 0.24M bpd during the week. Distillate inventory dropped -2.68 mmb to 16153 mmb as demand soared 7.29% to 4.09M bpd. Production increased 0.38% to 4.77M bpd while imports jumped 26.67% to 0.27M bpd during the week.

Elsewhere...

Japan labor cash earnings rose 0.5% yoy in January. Machine tool orders rose 9.1% yoy in February. China CPI dropped sharply to 0.8% yoy in February. PPI rose to 7.8% yoy.

Swiss unemployment rate was unchanged at 3.3% in February.

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 120.01; (P) 120.56; (R1) 121.11; More...

EUR/JPY's strong rally today and break of 121.32 resistance firstly confirms resumption of rise from 118.23. More importantly, this should confirm completion of the corrective fall from 124.08, after defending 118.45 cluster support (38.2% retracement of 109.20 to 124.08 at 118.39). Intraday bias is now back on the upside for a test on 123.30/124.08 resistance zone. Break will extend larger rally from 109.20 to next key resistance at 126.09. On the downside, break of 120.01 support is now needed to indicate completion of the rise from 118.23. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 109.20 medium term bottom are seen as part of a medium term corrective pattern from 149.76. Strong rebound from 118.45 resistance turned support suggests that it's still in progress. Break of 124.08 will target 126.09 key resistance level. We'd be cautious on strong resistance there to limit upside. However, sustained break there will be a strong sign of medium term momentum and could target 141.04 resistance next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y Jan | 0.50% | 0.30% | 0.10% | 0.50% |

| 00:01 | GBP | RICS House Price Balance Feb | 24% | 23% | 25% | 24% |

| 01:30 | CNY | CPI Y/Y Feb | 0.80% | 1.80% | 2.50% | |

| 01:30 | CNY | PPI Y/Y Feb | 7.80% | 7.50% | 6.90% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Feb P | 9.10% | 3.50% | ||

| 06:45 | CHF | Unemployment Rate Feb | 3.30% | 3.30% | 3.30% | |

| 12:30 | USD | Challenger Job Cuts Y/Y Feb | -40.00% | -38.80% | ||

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:30 | CAD | Capacity Utilization Rate Q4 | 82.20% | 82.60% | 81.90% | |

| 13:30 | CAD | New Housing Price Index M/M Jan | 0.10% | 0.10% | 0.10% | |

| 13:30 | USD | Import Price Index M/M Feb | 0.20% | 0.10% | 0.40% | |

| 13:30 | USD | Initial Jobless Claims (MAR 04) | 243K | 237k | 223k | |

| 15:30 | USD | Natural Gas Storage | -59B | 7B |

(ECB) Introductory Statement to the Press Conference

Mario Draghi, President of the ECB,

Vítor Constâncio, Vice-President of the ECB,

Frankfurt am Main, 9 March 2017

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at present or lower levels for an extended period of time, and well past the horizon of our net asset purchases. Regarding non-standard monetary policy measures, we confirm that we will continue to make purchases under the asset purchase programme (APP) at the current monthly pace of €80 billion until the end of this month and that, from April 2017, our net asset purchases are intended to continue at a monthly pace of €60 billion until the end of December 2017, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The net purchases will be made alongside reinvestments of the principal payments from maturing securities purchased under the APP.

Our monetary policy measures have continued to preserve the very favourable financing conditions that are necessary to secure a sustained convergence of inflation rates towards levels below, but close to, 2% over the medium term. Their ongoing pass-through to the borrowing conditions for firms and households benefits credit creation and supports the steadily firming recovery of the euro area economy. Sentiment indicators suggest that the cyclical recovery may be gaining momentum. Headline inflation has again increased, largely on account of rising energy and food price inflation. However, underlying inflation pressures continue to remain subdued. The Governing Council will continue to look through changes in HICP inflation if judged to be transient and to have no implication for the medium-term outlook for price stability.

A very substantial degree of monetary accommodation is still needed for underlying inflation pressures to build up and support headline inflation in the medium term. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase our asset purchase programme in terms of size and/or duration.

Let me now explain our assessment in greater detail, starting with the economic analysis. Euro area real GDP increased by 0.4%, quarter on quarter, in the fourth quarter of 2016, following a similar pace of growth in the third quarter. Incoming data, notably survey results, increase our confidence that the ongoing economic expansion will continue to firm and broaden. The pass-through of our monetary policy measures is supporting domestic demand and facilitates the ongoing deleveraging process. The recovery in investment continues to be promoted by very favourable financing conditions and improvements in corporate profitability. Moreover, rising employment, which is also benefiting from past structural reforms, is having a positive impact on households' real disposable income, thereby providing support for private consumption. Also, there are signs of a somewhat stronger global recovery and increasing global trade. However, economic growth in the euro area is expected to be dampened by a sluggish pace of implementation of structural reforms and remaining balance sheet adjustment needs in a number of sectors.

This assessment is broadly reflected in the March 2017 ECB staff macroeconomic projections for the euro area, which foresee annual real GDP increasing by 1.8% in 2017, by 1.7% in 2018 and by 1.6% in 2019. Compared with the December 2016 Eurosystem staff macroeconomic projections, the outlook for real GDP growth has been revised upwards slightly in 2017 and 2018. The risks surrounding the euro area growth outlook have become less pronounced, but remain tilted to the downside and relate predominantly to global factors.

According to Eurostat's flash estimate, euro area annual HICP inflation increased further to 2.0% in February, up from 1.8% in January 2017 and 1.1% in December 2016. This reflected mainly a strong increase in annual energy and unprocessed food price inflation, with no signs yet of a convincing upward trend in underlying inflation. Headline inflation is likely to remain at levels close to 2% in the coming months, largely reflecting movements in the annual rate of change of energy prices. Measures of underlying inflation, however, have remained low and are expected to rise only gradually over the medium term, supported by our monetary policy measures, the expected continuing economic recovery and the corresponding gradual absorption of slack.

This pattern is also reflected in the March 2017 ECB staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.7% in 2017, 1.6% in 2018 and 1.7% in 2019. By comparison with the December 2016 Eurosystem staff macroeconomic projections, the outlook for headline HICP inflation has been revised upwards significantly for 2017 and slightly for 2018, while remaining unchanged for 2019. The staff projections are conditional on the full implementation of all our monetary policy measures.

Turning to the monetary analysis, broad money (M3) continues to expand at a robust pace, with an annual rate of growth of 4.9% in January 2017, after 5.0% in December 2016. As in previous months, annual growth in M3 was mainly supported by its most liquid components, with the narrow monetary aggregate M1 expanding at an annual rate of 8.4% in January 2017, after 8.8% in December 2016.

Loan dynamics followed the path of gradual recovery observed since the beginning of 2014. The annual growth rate of loans to non-financial corporations was 2.3% in January 2017, as in the previous month. The annual growth rate of loans to households was 2.2% in January 2017, after 2.0% in December 2016. Although developments in bank credit continue to reflect the lagged relationship with the business cycle, credit risk and the ongoing adjustment of financial and non-financial sector balance sheets, the monetary policy measures put in place since June 2014 are significantly supporting borrowing conditions for firms and households and thereby credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need for a continued very substantial degree of monetary accommodation to secure a sustained return of inflation rates towards levels that are below, but close to, 2% without undue delay.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute much more decisively to strengthening economic growth. The implementation of structural reforms needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost potential output growth. Against the background of overall limited implementation of country-specific recommendations in 2016, greater reform effort is necessary in all euro area countries in 2017. Regarding fiscal policies, all countries should intensify efforts towards achieving a more growth-friendly composition of public finances. A full and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalances procedure over time and across countries remains crucial to ensure confidence in the EU's governance framework.

We are now at your disposal for questions.

Yen Dips to 3-Week Lows, Japanese Mfg. Report Next

USD/JPY has edged higher in the Thursday session. Currently, the pair is trading at 114.60. In Japan, Average Cash Earnings improved to 0.5%, above the estimate of 0.3%. This marked the highest gain since July 2016. Preliminary Machine Tool Orders jumped to 9.1%. Later in the day, we'll get a look at a key manufacturing report, the BSI Manufacturing Index. The indicator is expected to climb to 8.4 points. In the US, today's key event is unemployment claims, with the markets expecting the indicator to climb to 239 thousand. On Friday, employment numbers will again be in the spotlight, with the release of Nonfarm Payrolls, Average Hourly Earnings and the unemployment rate.

The Japanese manufacturing sector has long been a weak spot in the economy. However, the sector has been showing signs of improvement in 2017. After over a year of declines, Preliminary Machine Tool Orders has posted two straight gains, including a strong gain of 9.1% in February. The BSI Manufacturing Index, a quarterly indicator, is also pointing upwards. The index, which is based on a survey of large manufacturers, improved to 7.5 in the fourth quarter, pointing to optimism. The markets are predicting even better news in Q1, with the estimate standing at 8.4 points. Meanwhile, the Japanese yen has lost ground in March, falling 1.3 percent. The yen is within striking distance of the 115 line, which has held in resistance since January 27.

The Federal Reserve waited an entire year to raise rates in December, but appears ready to make a Mach move. The odds of a March hike continue to climb, and are currently at 88% percent, according to the CME Group. Fed policymakers have been dropping hints of a March move, and a red-hot labor market and higher inflation levels present further arguments in favor higher rates. Earlier in the year, the Fed had said that it wanted to wait until it had a clearer idea of President Trump's economic policy before it tightened monetary policy. However, Trump has not backed up his promises to reform the tax code and increase fiscal spending with any details. Some Fed policymakers wanted to raise rates earlier this year, so Fed Chair Yellen is under pressure to make a move, and it appears virtually certain that the Fed will raise rates by a quarter-point on March 15.

ECB Keeps Rates Static, Draghi in Focus

The muted market reaction following the European Central Bank's decision to leaving key interest rates unchanged in March should be no surprise. Markets had already priced in such an outcome with the main focus directed towards Mario Draghi's press conference which may come under heavy scrutiny. Although growth and inflation in the Eurozone have followed a positive trajectory, the mounting uncertainty around the elections in Europe could force the Central Bank to adopt a dovish stance. Investors may seize this opportunity to obtain some clarity on how the Central Bank plans to mitigate the shocks from the rising political risks. With Draghi likely to face some tough questions concerning the high-risk elections in France and the Netherlands, the Euro could be injected with volatility.

It is becoming visibly clear that the growing threat of Eurosceptic parties disrupting the unification of the Eurozone has left the Euro vulnerable to steep losses in the first quarter of 2017. Euro weakness may remain a dominant theme with anxiety set to heighten as the election process in France, Germany and the Netherlands get under way. The EURUSD is fundamentally bearish and a strengthening Dollar from the prospects of higher US interest rates could open a path towards 1.0350 in the medium to longer term. Technical traders could utilize the technical bounce on the EURUSD to send prices back down towards 1.0500 in the short term.

Commodity spotlight - Gold

Gold received a pummelling this week, with prices crashing to a fresh five-week low at $1203.13 during Thursday's trading session as expectations heightened over the Federal Reserve raising US interest rates next week. A dominant Dollar acquired from the bullish sentiment towards the US economy has attributed to Gold's sharp selloff with bears firmly in control on the daily charts. The downside momentum remains healthy with steeper declines expected in the short term if NFP exceeds expectations on Friday. From a technical standpoint, Gold is under intense pressure with previous support around $1210 acting as a light resistance for a decline lower towards $1200. A solid breakdown below $1200 could open a path towards the next relevant support at $1190.

Currency spotlight - GBPUSD

The ongoing Brexit woes have effectively limited any meaningful gains on Sterling during trading this week. Investors seem to have overlooked Wednesday's spring Budget with sellers simply exploiting the rising anxiety ahead of the Article 50 invocation to attack the Sterling on Thursday. Sterling may find itself under renewed rounds of selling if the Brexit uncertainties persist this month. From a technical standpoint, the GBPUSD is bearish on the daily charts. Weakness below 1.2150 could encourage a further depreciation towards 1.2000.

GBPUSD: Bearish, Remains Vulnerable To The Downside

GBPUSD: The pair continues to face further weakness following more declines on Wednesday. Support lies at the 1.2150 level where a break will turn attention to the 1.2100 level. Further down, support lies at the 1.2050 level. Below here will set the stage for more weakness towards the 1.2000 level. Conversely, resistance stands at the 1.2250 levels with a turn above here allowing more strength to build up towards the 1.2300 level. Further out, resistance resides at the 1.2350 level followed by the 1.2300 level. On the whole, GBPUSD continues to face downside threats but with caution.

USDJPY Intra-day Elliott Wave View

JPY (USDJPY) made a new high above last Friday's peak and now seems to be pulling back. Move up from 113.53 ((x)) low could be viewed as a 5 swing Leading Diagonal Elliott Wave structure. There is RSI divergence (not showing) between red wave iii and blue (a) which further supports the idea of JPY move up from 113.53 low being a diagonal structure. As per Elliott Wave theory, after a 5 wave move up or diagonal structure higher completes, pair should make a corrective pull back before rallying again. Decline from 114.93 -114.48 could be viewed as just the first leg of proposed wave (b) pull back. As current bounce stays below 114.93, pair has scope to make another push lower to complete wave (b) pull back before it turns higher again in wave (c) towards 115.30 -116.11 area. As pair is showing 5 waves up from 113.53 low, we don't like selling the pair in proposed wave (b) pull back and expect it to find intra-day buyers in the dip as far as price stays above 113.53 low and the pivot there remains intact. Break above 114.93 would suggest wave (b) completed already at 114.48 and pair has started the next leg higher in wave (c) toward the above mentioned area.

JPY (USDJPY) 1 Hour Chart