Sample Category Title

Dollar Yen Set To Stumble As The Week Comes To A Close

Key Points:

- Strong zone of resistance should encourage a reversal.

- Losses likely to be limited to the 113.00 handle.

- US employment data could prevent the forecasted decline from occurring.

The Dollar Yen's recent uptrend could be on thin ice as it is now pushing the upper limits of its ascending channel structure. As a result of this, we could be about to a slip back to around the 113.00 handle within a week or so. However, we are unlikely to see the long-term uptrend end just yet so we shouldn't expect to see downside extend far beyond this level.

Firstly, let's take a look at the channel in question which should be about to exert some downward pressure on the USDJPY. As is illustrated below, the upside constraint of the channel is now very much insight which will be causing some of the bullish momentum to wear thin. Moreover, we also have the 50.0% Fibonacci retirement reinforcing resistance around the 115.35 mark which will severely cap upside potential.

Furthermore, bearish sentiment could be about to return due, in no small part, to the movement of the stochastics into overbought territory. Whilst it's true that the oscillator has been signalling this for a while, now that we have reached the upside of the channel there should be additional impetus for the pair to retrace. Such a maneuverer would also be in line with the Bollinger band analysis which is highly suggestive of a near-term decline for the USDJPY. Specifically, the pair has pushed the upper band fairly hard over the past few sessions and is now looking ready to return to the central tendency of the bands.

Once we do see a decline move into full swing, we can expect it to extend to around the 113.00 handle before support provides another impasse. This is largely a result of the projected downside constraint of the bullish channel but the 100 day EMA could also present an additional challenge for the bears seeking to break the medium-term trend. When this firm support has been reached, we should see bullish sentiment return which could begin to move the USDJP towards that January high.

Ultimately, this technical forecast is somewhat contingent on the US Employment data exceeding expectations by too greater margin. As a result, it will be worth keeping a close eye on the results as they are released to avoid being caught off guard. Although, the slip in the unemployment rate to 4.7% has been largely priced in which should mean it's the NFP numbers that are more likely to upset the apple cart here. Luckily, the ADP numbers have already inflated the market's expectations which could actually work in favour of the above forecast.

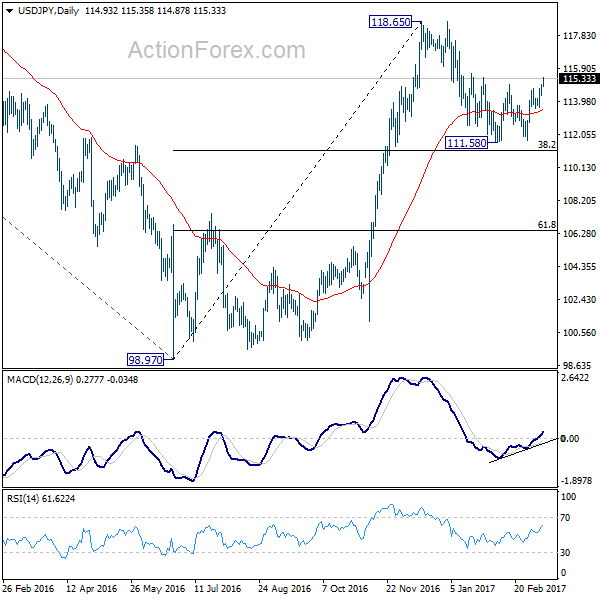

USD/JPY Daily Outlook

Daily Pivots: (S1) 114.47; (P) 114.74; (R1) 115.19; More...

USD/JPY's rise and break of 114.94 resistance should confirm near term reversal on double bottom pattern (111.58, 111.68). That's whole correction from 118.65 is completed at 111.58. Intraday bias is now back on the upside for a test on 118.65 resistance. Break will resume whole rally from 98.97 and target 125.85 high next. On the downside, break of 113.60 support is now needed to indicate completion of the current rise. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Dollar and Yield Higher ahead of NFP, Yen Tumbles

Dollar is trading as the strongest major currency for the week as markets await employment data from US. The general consensus is that barring a disastrous non-farm payroll report, Fed will still hike interest rate in the FOMC meeting next week. It would be a big blow to the credibility of Fed if they don't deliver after the chorus of hawkish messages. Nonetheless, the NFP numbers, including the headline job growth and wage growth, are still important for Fed to determine the policy path for the year. FOMC members generally maintained the expectation of three rate hikes this year. But now that the first hike will likely be done next week, there is indeed possibility for four hikes should the economy perform well with boost from US president Donald Trump's expansive policies.

Other data point to strong NFP

Economists are expecting NFP to show 190k growth in US job market in February, down from prior month's 227k. Unemployment rate is expected to drop from 4.8% to 3.7%. Average hourly earnings growth is expected to pick up again and rise to 0.3% mom. Other employment related data were generally positive. ADP report showed 298k growth in private sector jobs, much higher than expectation of 184K. Employment component of ISM manufacturing dropped from 56.1 to 54.2 but stayed well in expansion territory. On the other hand, employment component of ISM non-manufacturing rose from 54.7 to 55.2. The four week moving average of initial jobless claims dropped fro 245k to 237k during the period. Conference board consumer confidence rose from 111.6 to 114.8 hitting the highest level in 15 years. We'll more likely get an upside surprise in NFP today.

10 year yield heading for a breakout

TNX jumped for another day overnight by closing at 2.598, up 0.046. 2.621 key resistance level is now in sight. Today's job data could be a stimulus for this breakout for resuming up trend from 1.336. If not, traders would probably wait for Fed's new projection before acting. Nonetheless, further rise is now in favor as long as 2.545 minor support holds. Sustained trading above 2.621 will pave the way for next key resistance level at 3.036.

Euro boosted by upbeat Draghi

Euro surged yesterday on upbeat tone of ECB president Mario Draghi during the post meeting press conference. The common currency is trading as the second strongest major currency for the week. Strength is particularly notable against Yen. Despite no change in the policy rate and the QE program, the euro gained as President Mario Draghi added some upbeat flavors at the press conference and as the staff upgraded the inflation forecasts. The members continued to see risks to growth skewed to the downside, but agreed that they are "less pronounced" now. While the forward guidance in the statement maintained that "interest rates will stay low, or lower for an extended period of time", the members had discussions of its removal at the meeting. More in Cautiously Optimistic Draghi Sees No Urgency to Add Stimulus, Risks Less Pronounced

Elsewhere...

Japan BSI large manufacturing dropped to 1.1 in Q1. Australia home loans rose 0.5% in January. Germany will release trade balance in European session. UK will also release trade balance plus productions. Canada will release job report in US session, together with US NFP.

USD/JPY Daily Outlook

Daily Pivots: (S1) 114.47; (P) 114.74; (R1) 115.19; More...

USD/JPY's rise and break of 114.94 resistance should confirm near term reversal on double bottom pattern (111.58, 111.68). That's whole correction from 118.65 is completed at 111.58. Intraday bias is now back on the upside for a test on 118.65 resistance. Break will resume whole rally from 98.97 and target 125.85 high next. On the downside, break of 113.60 support is now needed to indicate completion of the current rise. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q1 | 1.1 | 8.4 | 7.5 | |

| 0:30 | AUD | Home Loans Jan | 0.50% | -1.00% | 0.40% | 0.20% |

| 7:00 | EUR | German Trade Balance (EUR) Jan | 18.0B | 18.4B | ||

| 9:30 | GBP | Industrial Production M/M Jan | -0.50% | 1.10% | ||

| 9:30 | GBP | Industrial Production Y/Y Jan | 3.20% | 4.30% | ||

| 9:30 | GBP | Manufacturing Production M/M Jan | -0.70% | 2.10% | ||

| 9:30 | GBP | Manufacturing Production Y/Y Jan | 2.90% | 4.00% | ||

| 9:30 | GBP | Construction Output M/M Jan | -0.40% | 1.80% | ||

| 9:30 | GBP | Visible Trade Balance (GBP) Jan | -11.1B | -10.9B | ||

| 13:30 | CAD | Net Change in Employment Feb | -15.5k | 48.3k | ||

| 13:30 | CAD | Unemployment Rate Feb | 6.80% | 6.80% | ||

| 13:30 | USD | Change in Non-farm Payrolls Feb | 190k | 227k | ||

| 13:30 | USD | Unemployment Rate Feb | 4.70% | 4.80% | ||

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.30% | 0.10% | ||

| 15:00 | GBP | NIESR GDP Estimate Feb | 0.60% | 0.70% |

CL_F Elliott Wave View: Bounce Expected Soon

Short term Elliottwave view in Crude Oil (CL_F) suggests that the instrument is currently correcting cycle from 11/14/2016 low (42.21) in 3, 7, or 11 swing before the next leg higher. Revised view suggests the decline starting from 1/3 high (55.24) is unfolding as a flat Elliottwave structure where Minor wave A ended at 50.71 and Minor wave B ended at 54.94. Minor wave C is in progress and subdivided as 5 waves diagonal where Minute wave ((i)) ended at 52.54, Minute wave ((ii)) ended at 53.8, and Minute wave ((iii)) ended at 50.05 and Minute wave ((iv)) ended at 50.85. The current pullback has reached minimum swing and extension to finish cycle from 1/3 high, but while short term bounce fails below 50.85, another leg lower can’t be ruled out towards 46.8 – 47.5 area to end Intermediate wave (4) pullback. Afterwards, look for Crude Oil to resume the rally higher or at least bounce in 3 waves to correct cycle from 1/3 high. We don’t like selling the proposed pullback and expect Crude Oil to find support soon once wave ((v)) of (4) is confirmed complete, provided that pivot at 11/14/2016 (42.21) stays intact.

CL_F 1 Hour Chart

Foreign Exchange Market Commentary

EUR/USD

The common currency got a temporal boost from a more hawkish-than-expected ECB's Draghi, but the EUR/USD pair was unable to regain the 1.0600 level, with a spite up to 1.0614 being quickly reverted. The European Central Bank left its monetary policy unchanged, announcing no foreseeable change to the current easing path. However, policymakers reviewed their inflation and growth forecast, with modest upward revisions for this year and the next, but none for 2019. Overall, Draghi was more optimistic than usual about the economic outlook, but he avoided being too optimistic, or comment on the end of QE, succeeding in maintaining the EUR under control. The ECB does not need an expensive currency, now that the fragile recovery is trying to firm up.

All eyes are now on the US NFP report, and how it could affect Fed's rate decision next week. During the past three weeks, US FOMC's members have endeavored to anticipate a rate March hike working in advance to maintain volatility restrain, pretty much what Draghi did this Thursday with a mixed statement. Last Friday, Fed's Yellen said that the move will depend on inflation and employment maintaining the current levels of progress, so the market is waiting for this report to confirm next week's move. This particular time, wages will be as relevant as the headline reading, as if wages disappoint, uncertainty will likely push the greenback lower.

From a technical point of view, the EUR/USD pair continues lacking a clear directional strength and with the risk still lean towards the downside, as the pair is unable to advance beyond 1.0600. In the 4 hours chart, the price continued moving back and forth around a major Fibonacci support at 1.0565, while the 20 and 100 SMAs have turned horizontal a bunch of pips above the level. The Momentum indicator has recovered ground, now heading higher in neutral territory, but the RSI indicator has turned horizontal around 55, indicating the absence of upward strength. Upcoming moves will be determinate by the NFP outcome with 1.0520, and 1.0635 being the breakout levels to take care of, to see some follow-through.

Support levels: 1.0565 1.0520 1.0490

Resistance levels: 1.0600 1.0635 1.0660

USD/JPY

The USD/JPY pair advanced up to 114.96 before pulling back modestly, retaining a positive tone ahead of Friday's US Payroll report. The Japanese yen weakened amid rising US yields and in spite of tepid US data, as weekly unemployment claims rose to a seasonally adjusted 243K in the week ending March 4th, against market's expectations of 235K. As for US yields, the 10-year note benchmark ended at 2.58%, up from Wednesday's 2.55%, while the 2-year note yield surged to 1.38%, its highest in over eight years. The Japanese macroeconomic calendar will remain pretty light during the upcoming Asian session, which means that the pair will likely hold between the 114.50/115.00 range, ahead of US news. The technical picture is moderately bullish as in the 4 hours chart, the price is well below its 100 and 200 SMAs that anyway remain horizontal and both together in the 113.30 region, while technical indicators have turned modestly lower within positive territory. The key is the Fibonacci support at 114.55, as a break below it will increase chances of a downward extension towards 114.15, while on the other hand, an advance beyond 115.00, on a strong US NFP report, will lead to an approach to the 116.00 region.

Support levels: 114.55 114.15 113.70

Resistance levels: 114.95 115.30 115.80

GBP/USD

The GBP/USD pair closed in the red for a fourth consecutive day, having extended its decline by a few pips to a fresh 7-week low of 1.2133. An early advance was contained by selling interest on an approach to the 1.2200 level, with the pair confined to Wednesday's range, amid the absence of UK headlines. This Friday, however, the UK will release its January trade balance and industrial and manufacturing production figures, whilst the BOE will release its Consumer Inflation Expectations report, all set to determinate the health of the local economy. From a technical point of view, the risk remains towards the downside, with a bearish 20 SMA, currently at 1.2190, leading the way lower as approaches to the level have triggered downward moves ever since the month started. In the same chart, technical indicators have managed to bounce from near oversold levels, but remain well below their mid-lines, not enough to support additional gains. A recovery beyond 1.2220 could see the pair correcting higher, but selling interest is now aligned around 1.2260, the 61.8% retracement of the January rally.

Support levels: 1.2130 1.2085 1.2040

Resistance levels: 1.2190 1.2220 1.2260

GOLD

Gold prices remained under pressure, with spot trading as low as $1,201.40 a troy ounce and settling a few cents above the 1,204.00 threshold, its lowest settlement in over a month. Gold prices have fallen seven out of the last eight days, on speculation the US Federal Reserve will raise its benchmark rates as soon as next Wednesday. Adding to the bearish case of the bright metal, was low physical demand from Indian jewelers. The daily chart for the commodity shows that it extended its slide below the 38.2% retracement of the latest recovery at 1,209.75, the immediate resistance, whilst the price has moved further below the 20 and 200 DMAs. The 100 DMA offers an immediate support at 1,197.30, while technical indicators have partially lost their bearish strength near oversold readings, but are far from indicating downward exhaustion. In the shorter term, the 4 hours chart shows that technical indicators have turned flat within oversold territory, but also that the 20 SMA has accelerated its decline above the current level, and after extending below the 100 and 200 SMAs, supporting additional declines for this Friday.

Support levels: 1,197.30 1,188.20 1,180.50

Resistance levels: 1,209.60 1,214.20 1,221.70

WTI CRUDE

Crude oil prices plummeted for a second consecutive day, with West Texas Intermediate crude futures down to $48.66 a barrel, its lowest since late November. US light, sweet crude closed the day at $48.83 a barrel, undermined by the advance of US stockpiles to record highs, as reported by the EIA on Wednesday. Hopes that the OPEC output cut deal will help reducing the global glut were diluted by the continued increase in US production. The daily chart shows that the commodity is currently around its 200 DMA, after breaking below the 100 DMA on Wednesday, whilst the Momentum indicator maintains its bearish slope within negative territory, and the RSI indicator extended its decline down to 24, where it stands ahead of the Asian opening. In the 4 hours chart, technical indicators have lost their bearish strength but remain in extreme oversold levels, with the RSI currently at 18, whilst the price is far below its moving averages, still trying to catch up with the latest sharp slide.

Support levels: 48.60 48.00 47.30

Resistance levels: 49.50 50.10 50.80

DJIA

US indexes closed the day flat, with the Dow Jones Industrial Average up 3 points, to 20,858.74, the S&P ending the day at 2,364.87, 0.08% higher, and the Nasdaq Composite down 4 points, to 5,834.26. Investors remained side-lined ahead of the US employment report to be released this Friday, as upbeat figures can reinforce the possibility of a Fed rate hike next week. Within the Dow, industrial underperformed, with Caterpillar down 1.88% and General Electric by 0.47% being among the worst performers. Johnson & Johnson led advancers, adding 1.44%, followed by El du Pont that added 0.78%. The daily chart for the Dow shows that the index bounced from a daily low of 20,777, holding above the 20 DMA that anyway is losing upward strength. The Momentum indicator continued heading lower within positive territory, but the RSI indicator turned flat around 64, limiting the downward potential. In the 4 hours chart, the index is trapped between a bearish 20 SMA and a bullish 100 SMA, whilst technical indicators hover within bearish territory, with no clear directional strength.

Support levels: 20,833 20,777 20,738

Resistance levels: 20,899 20,950 21,017

FTSE 100

The FTSE 100 extended its decline, losing 0.27% or 19 points this Thursday, and closing at 7,314.96. Falling oil and commodities prices weighed on the index, although the worst performer was Morrison Supermarkets that lost 6.56% after the company expressed its concerns about how imported food prices, with the Pound weak, could affect its business. Lower commodity prices also affected the benchmark, with oil and mining-related equities closing in the red. Anglo American lost 4.61%, Glencore closed 3.66% lower, whilst BHP Billiton ended down 3.37%. Financials were among the best performers, with Aviva up 6.46% followed by Capita that added 4.67%. The technical picture is neutral as in the daily chart, the index settled around its 20 DMA, whilst technical indicators head modestly lower, but hold above their mid-lines, lacking enough strength to confirm a bearish breakout. In the 4 hours chart, the index recovered quickly after a brief slide below a bullish 100 SMA, but remains below a bearish 20 SMA, whilst indicators bounced within bearish territory, but remain below their mid-lines, indicating that the benchmark lacks upward strength and may fall further on a break below 7,262, the daily low.

Support levels: 7,306 7,262 7,238

Resistance levels: 7,345 7,397 7,420

DAX

European equities edged marginally higher, helped by an advance in banking equities, with the German DAX up 11 points or 0.09% to end at 11,978.39. Optimistic comments from ECB's head, Mario Draghi, underpinned the sector, although gains were offset by falling oil prices that dragged energy shares lower. In Germany, Bayerische Motoren Werke led decliners, down 2.46%, while Merck followed, ending the day down 2.38%. Deutsche Bank was among the best performers, adding 2.08%, whilst Commerzbank gained 1.01%. From a technical point of view, the index has made little progress, as it held a few points above a still bullish 20 DMA, while the Momentum indicator remains flat around its 100 level and the RSI indicator turned modestly higher, but remains below its previous weekly highs. In the 4 hours chart, the index spiked briefly beyond a still bearish 20 SMA, but settled below it, whilst technical indicators continue hovering around their mid-lines, failing to provide directional clues.

Support levels: 11,920 11,877 11,832

Resistance levels: 12,010 12,053 12,100

Cautiously Optimistic Draghi Sees No Urgency to Add Stimulus, Risks Less Pronounced

Despite no change in the policy rate and the QE program, the euro gained after the ECB announcement, as President Mario Draghi added some upbeat flavors at the press conference and as the staff upgraded the inflation forecasts. The members continued to see risks to growth skewed to the downside, but agreed that they are "less pronounced" now. While the forward guidance in the statement maintained that "interest rates will stay low, or lower for an extended period of time", the members had discussions of its removal at the meeting. The single currency rose from a 3-day low of 1.0523 to as high as 1.0615 against US dollar. The pair gained +0.34% for the day. Global yields were also driven higher on possibility of a chance in ECB's policy measures. The 10-year German bund yield added +5.6 bps to 0.421% at close, whilst the 10-year US Treasury yield climbed further higher to about 2.6%.

While affirming the pledge to maintain accommodative policies and noted there has not been "any significant development on the wages front", Draghi suggested that the members are "more optimistic about the growth forecast, we have to see how these improved prospects, as far as growth is concerned, translate into higher headline inflation". Draghi admitted that it is less likely for further measures to support the Eurozone economy as the threats to recovery have diminished. As he suggested, "there is no sign of a convincing upward trend in underlying inflation". Yet, he added that "there was a general recognition that the balance of risk has improved, certainly as far as growth is concerned" and "there is no longer that sense of urgency in taking further actions".

The economic projections were largely unchanged from previously, with the only tweak on inflation. The staff revised up their forecasts for headline HICP inflation by +0.4 percentage point to +1.7% y/y for this year, and by +0.1 percentage points +1.6% y/y for 2018. The reading for 2019 stayed unchanged at +1.7%. The forecasts for core inflation stayed unchanged at +1.1% this year but that for 2019 was revised +0.1 percentage point higher to +1.8% y/y. Meanwhile, the staff revised up their GDP growth forecasts to +1.8% for 2017 and +1.7% for 2018, both up +0.1 percentage point from the previous estimates, while the projection for 2019 stayed unchanged at +1.7%.

The accompanying statement contained little new information. The ECB reiterated the stance to keep interest rates "at present or lower levels for an extended period of time, and well past the horizon of our net asset purchases". It retained the reference that the central bank would "continue to make purchases under the asset purchase program (APP) at the current monthly pace of 80B euro until the end of this month and that, from April 2017, our net asset purchases are intended to continue at a monthly pace of 60B euro until the end of December 2017, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim". Draghi admitted at the Q&A session that there was "a cursory discussion about whether to remove the word 'lower' from the forward guidance". Note also that the reference that "If warranted, to achieve its objective the Governing Council will act by using all the instruments available within its mandate" if removed. Draghi explained that the removal signals the lack of "urgency in taking further actions while maintaining the accommodative monetary policy stance including the forward guidance".

Market Morning Briefing

STOCKS

Dow (20858.19, +0.01%) made an intra-day low of 20777, just levels above our expected 20750 and closed the session at higher levels. Sideways consolidation is possible in the next few sessions with a possibility of seeing some more fall in the near term.

Dax (11978.39, +0.09%) is holding above the daily trend support and while that holds, we could see a rise towards resistance near 12100-12200 levels.

Nikkei (19578.92, +1.35%) could come off in the near term from 19620 to re-test levels near 19400 or lower. While the US-Japan yield spread gives indication of a sharp fall from crucial resistance levels, the immediate upside for Nikkei could be limited. (Refer to Forex and Interest Rates section below)

Shanghai (3217.12, +0.01%) traded lower as expected and could either move down towards 3175 or consolidate within the 3250-3200 region for some more time.

Nifty (8927.00, +0.03%) is stuck within the 8970-8880 region (broader range of 8800-9000) and may remain sideways today also. The election results due tomorrow could trigger some movement on Tuesday as Indian markets would be closed on Monday for HOLI.

COMMODITIES

Gold (1199) has shifted into a new bearish trading zone of 1128-1226. Weekly profit taking my pull gold towards 1200-20 but We will remain bearish until it will close above1230-35. Crucial supports are poised at 1183 and 1169. A close below 1169 could open up 1128 and 1054 levels respectively.

Silver (16.94) also moved lower in line with our expectation and closed below 17. Crucial support is at 16.70. A close bellow that could open up 15.78. Bias will remain bearish while it is trading below 17.75.

Copper (2.60) is hovering around its crucial support of 2.55-60. We might see short term pull back towards 2.70. We have few important US data (Average hourly earnings, Non Firm employment change and unemployment rate) today at 7:00 pm IST, which may influence the price of copper and silver respectively.

Major weekly trend line support has been broken form both Breant (52.54) and WTI (49.61). We may see short term pull back rally toward 54 in brent and 51 in wti due to weekly profit taking, though the bias is still bearish. Immediate support for Brent is at 45.42 and WTI at 44. We would not be surprised if we will see these lavels within few weeks of time.

FOREX

No change in stance was announced in the ECB meet, as expected but a surge in the German yields (Check Interest rates section) pushed Euro (1.0595) higher but it still may remain stuck in the range of 1.0500-1.0650 till the FOMC meet next week.

Failure to rise above 102.30 has kept the Dollar Index (101.91) stable and it may possibly spend the next couple of sessions in the range of 101.20-102.30. New range could be established after the FOMC meet.

Dollar-Yen (115.20) has rallied sooner than expected as it trades above the previous month high of 114.98 now. While the chances of further rise to 117.50 or even 118.60 can’t be ignored now, the danger comes from the US-Japan10Yr facing crucial resistance near the current levels, which if holds, can push the Dollar Yen down.

Pound (1.2161) is in a pause mode in the narrow band of 1.2100-1.2200 for the last 2-3 sessions after the 6-week long downtrend but it remains to be seen if any bottoming price action may take place around the current levels or a another decline towards 1.20 levels will take place.

Aussie (0.7519) is hanging on to the 0.75 levels by the skin of its teeth with bidirectional possibilities open in the near term. If 0.75 holds, then another bounce to 0.7600-30 levels can be seen but a break below 0.75 may drag it down to 0.7350-00 levels. Wait and watch.

Dollar-Rupee (66.72) is trading at 66.73 in the NDF market today, apparently indifferent to the just released exit polls. Possibly the probability of no majority for any single party in the all important state of UP keeps the currency stable for now and the actual movement may come next week, after the actual result. Technically, no bias in the range of 66.50-66.95.

INTEREST RATES

The German yields are trading higher, not impacted much by the ECB meeting yesterday. The 5Yr (-0.39%), 10YR (0.423%) nd 30YR (1.24%) are up from previous levels of -0.41%, 0.39% and 1.21% respectively and could move higher in the near term.

The German 10-2YR (1.2730%) has risen sharply breaking above the immediate resistance near 1.16%. Another resistance is visible near 1.30% which if holds could produce some rejection towards 1.20%.

The US-Japan 10YR (2.53%) has indeed risen from levels near 2.484% yesterday and has come up to test medium term resistance near current levels. While that holds, a corrective dip is expected in the coming sessions. Else a break above the crucial resistance could indicate further upside for both Nikkei and Dollar-Yen.

ECB Review: Hawkish Twist But Full QE Implementation Is Needed

The ECB kept all policy measures unchanged at today's meeting, which was in line with our expectations. The ECB also maintained its forward guidance on policy rates as it still expects rates 'to remain at present or lower levels for an extended period of time, and well past the horizon of our net asset purchases'. Regarding the QE purchases the ECB also continued to have an easing bias as it communicated that it stands ready to increase QE in terms of size and/or duration.

However, Draghi had a hawkish tone during the Q&A session as he said the Governing Council discussed whether to remove the 'lower levels' from the forward guidance on policy rates. According to Draghi, the forward guidance in terms of lower policy rate levels was an expectation and the probability of this expectation materialising had gone down. Added to this, the ECB removed a sense of urgency in taking further actions as the introductory statement no longer included 'If warranted to achieve its objective, the Governing Council will act by using all the instruments available within its mandate.'

In our view, a next step from the ECB when moving in a less dovish monetary policy direction is to remove the 'lower levels' from the forward guidance. However, according to Draghi this is a very small step and in our view it also does not mean the ECB will hike policy rates in the near future. We expect the ECB to continue to communicate that policy rates will remain at present levels for an extended period of time, and well past the horizon of the QE purchases. Hence, it should not start to communicate that policy rates could be hiked before the QE purchases have stopped running.

The ECB revised its headline inflation forecast upward this and next year while it lifted its core inflation forecast for 2018 and 2019. In our view, the ECB was already very optimistic in its core inflation forecast before the upward revision to the March projection and we expect the ECB will have to lower its core inflation projection later in time, which could be followed by a return to a more dovish stance. Related to this, Draghi very clearly said the ECB's inflation forecasts are conditional on full implementation of the monetary policy measures.

Along these lines, Draghi repeated that underlying price pressure remains subdued and we stick to our view that the ECB will extend its QE purchases beyond December 2017. This should follow as we expect core inflation to stay below 1.0% during most of this year and as we expect that core inflation will have to exceed 1.0% for a number of months before the ECB will announce QE tapering.

On the very short-end German yield curve, Draghi said the ECB was monitoring distortions. According to Draghi the moves were mainly driven by 1) an increasing fraction not having access to the deposit facility, 2) 'safe haven' flows, and 3) to a lesser extent the QE purchases. It appeared that it was still early days for this analysis and that the ECB could come back to the issue at upcoming meetings. In our view, this communication is a usual first step when the ECB acknowledges an issue.

The market reacted by sending German government bond yields higher by around 5bp beyond the 10Y point. Against this, Schatz did not sell-off, probably reflecting Draghi's comment that the distortions to a lesser extent were due to the QE purchases. EUR/USD is trading slightly higher at 1.058 from 1.054 this morning.

Changes to the ECB's projections

The ECB lifted its headline inflation projection considerably in 2017 and slightly in 2018, but kept it unchanged in 2019. The higher 2017 forecast was due to energy and food price inflation

Switching Playbook

Focus overnight was all ECB. While the markets were preparing for the ECB to move in a more positive direction the sultan of sophistry, Mario Draghi, was at his best firing knuckleball during his prepared comments but finishing with a wicked curve ball. While interest rates remain on hold and the prepared statement was arguably dovish Draghi's press conference forward guidance suggested that a shift in policy was on the horizon which kicked the Euro bulls into overdrive as there will little ambiguity between political uncertainty and data strength during his presser.

Commodity prices continue to drop like a sack of potatoes with Oil leading the charge as bearish market forces, rather than anticompetitive price fixing politics are now in the driver's seat.

Euro

Given Draghi's hawkish tilt, markets ferociously bought EUR across with both EURUSD and EURJPY leading the charge. Expect the EUR crosses to remain buoyant. However, given high USD demand, which is projected to accelerate as we near next week's FOMC, he EURUSD gains will likely be capped during the FOMC buildup.

Amazing what a subtle shift in the ECB playbook can do for EUR sentiment leaving many wondering what ever happened to dovish Draghi.

Australian Dollar

Commodity prices have hit the skids as the China expansion motor is looking a bit lethargic these days.

While it's not just an oil storyline as both copper and iron ore are looking extremely vulnerable, but oil prices are indeed providing the grease for this slippery commodity slope.

EURAUD has been in demand, pressuring the Aussie, as the markets seize the current story line that the EUR will hold firm against everything but the dollar even more so versus commodity currencies which are struggling in the face plummeting oil prices.

All the while US yields look stationed to make higher highs which are blending into a toxic cocktail for the Australian Dollar

Japanese yen

Both EURJPY and USDJPY demand have weighed on Yen sentiment and while the critical 115 level has held, but now at close range, it's more about when rather then if, as we approach what is expected to be an attractive Non-Farm Payroll number

EM Asia

US yields have certainly kicked into high gear since stellar ADP print. With tonight's NFP supposed to come in well, the market will continue gearing up for the anticipated rate hike next week.None the less there appears to be little panic in EM Asia as the dealers are not chasing the USD move higher as they have been prone to in the past, but pockets of USD selling interest continues to emerge as the broader market is still uncertain about the pace of US tightening. The USD continues to lag US bond yields which may imply that after the FOMC is done the dollar may peak and reverse. However much of the speculation on APAC EM is the resumption of buoyant risk appetite and a continued improvements in the global growth story line, all of which is open to much debate.

Elliott Wave Analysis: EURUSD Intraday View

EURUSD found some support today from 1.0524 level, which was quite aggressive bullish move, but for now still only with three waves, so as long that's the case we need to consider bearish prices. 1.0542 break would be strong confirmation for a decline beneath 1.0524 and then towards 1.0500.

EURUSD, 1H