Sample Category Title

Dollar Firm as Sticky Inflation Lifts Fed Expectations, Sterling Hit by UK Leadership Crisis

Dollar stayed broadly firm after another major upside surprise in US inflation data reinforced expectations that the Federal Reserve will need to keep policy restrictive for longer. Sterling, meanwhile, remained under heavy pressure as Britain’s political crisis deepened further amid growing speculation that Prime Minister Keir Starmer could soon face a formal leadership challenge.

The latest US Producer Price Index report added to inflation concerns that had already intensified following Tuesday’s hotter-than-expected CPI release. The data reinforced concerns that elevated energy prices tied to the Middle East conflict are beginning to spread more deeply through the broader economy. PPI is widely viewed as a leading indicator for consumer inflation because higher production costs are eventually passed through to retail prices.

Fed rate expectations shifted further in response. Futures markets continued reducing expectations for policy easing this year, while implied odds of an additional Fed hike by year-end rose toward 40%. Some investors believe policymakers may eventually consider an “insurance” rate hike if inflation data over the coming months fails to reverse meaningfully.

Sterling, by contrast, came under renewed selling pressure as UK political instability intensified. Reports suggested Health Secretary Wes Streeting is preparing for his resignation and a possible formal leadership challenge against Prime Minister Keir Starmer as early as Thursday. According to reports, Streeting’s allies have already begun canvassing MPs in an effort to secure the 81 members needed to trigger a formal contest. The developments reinforced fears that Britain may be entering a prolonged period of political paralysis just as markets grow increasingly sensitive to rising gilt yields and fiscal risks.

Meanwhile, comments from ECB policymakers highlighted growing divisions inside the Governing Council over how to respond to the latest energy-driven inflation shock. Finland’s Olli Rehn warned of stagflation risks, arguing the ECB should avoid reacting mechanically to oil-driven inflation spikes while growth remains near stagnation. He stressed the importance of monitoring second-round effects such as wages and inflation expectations before committing to further tightening.

By contrast, Estonia’s Madis Muller adopted a significantly more hawkish tone, saying a June rate hike is “likely” unless there is a rapid resolution to Strait of Hormuz disruptions and a sharp decline in oil prices. French policymaker François Villeroy de Galhau struck the most cautious tone of the three, emphasizing that current inflation pressures remain largely energy-driven and warning against tightening prematurely before there is clearer evidence of persistent core inflation acceleration.

Overall for the week so far, Dollar is staying as the strongest performer but capped below last week's high against all but Sterling. Aussie is the second best, and then Loonie. The Pound is currently the worst, followed by Swiss Franc, and then Yen. Euro and Kiwi are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.10%. DAX is up 0.35%. CAC is down -0.44%. UK 10-year yield is down -0.014 at 5.093. Germany 10-year yield is down -0.003 at 3.107. Earlier in Asia, Nikkei rose 0.84%. Hong Kong HSI rose 0.15%. China Shanghai SSE rose 0.67%. Singapore Strait Times rose 1.17%. Japan 10-year JGB yield rose 0.049 to 2.593.

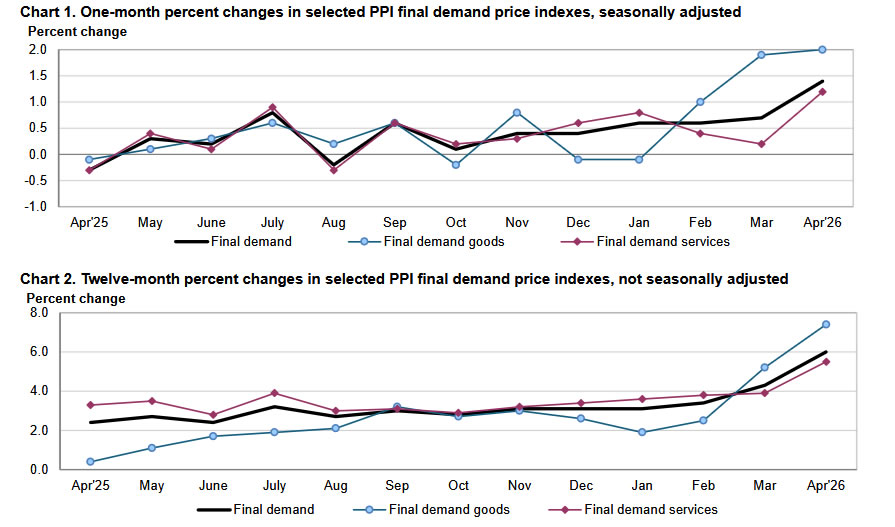

US PPI Surges to Highest Since 2022 as Upstream Inflation Pressures Intensify

US wholesale inflation delivered a major upside surprise in April as producer prices surged at the fastest monthly pace since 2022. Importantly, the pressure was not limited to energy alone, with both services and core producer prices accelerating sharply and reinforcing “higher for longer” Fed expectations. Read More.

Eurozone GDP Expands Just 0.1% in Q1, Annual Growth Slows to 0.8%

Eurozone growth lost momentum again in early 2026 as high energy prices and weak industrial activity continued weighing on the economy. Employment growth also softened, reinforcing concerns that Europe’s recovery remains fragile despite still-resilient labor markets. Read More.

Eurozone Industrial Production Misses Forecast as Energy Output Falls

Eurozone industrial production improved modestly in March, but the underlying details showed a highly uneven recovery. While capital goods and investment-related sectors strengthened, consumer goods output weakened sharply, highlighting persistent softness in household demand across Europe. Read More.

OECD Sees BoJ Raising Rates to 2% by End-2027

The OECD believes Japan’s monetary normalization cycle is still in its early stages, projecting the BOJ’s policy rate will rise from 0.75% to 2% by the end of 2027. Strong wage growth, resilient domestic demand, and improving inflation dynamics are increasingly supporting the case for continued tightening. Read More.

New Zealand Inflation Expectations Jump as RBNZ OCR Outlook Turns Hawkish

The RBNZ’s latest Survey of Expectations showed inflation concerns intensifying sharply in New Zealand, with one-year CPI expectations surging above 3.4% while markets also lifted their outlook for future OCR settings. At the same time, growth expectations weakened noticeably, highlighting a more difficult balancing act for policymakers. Read More.

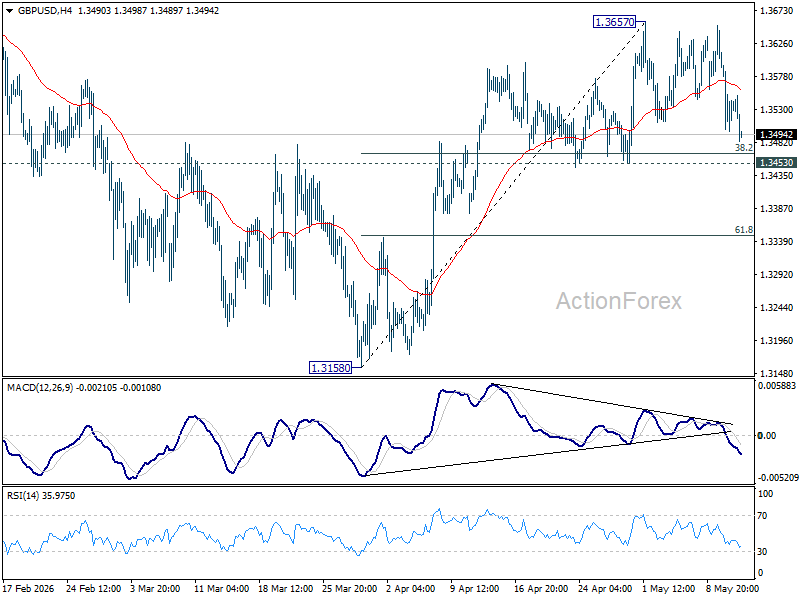

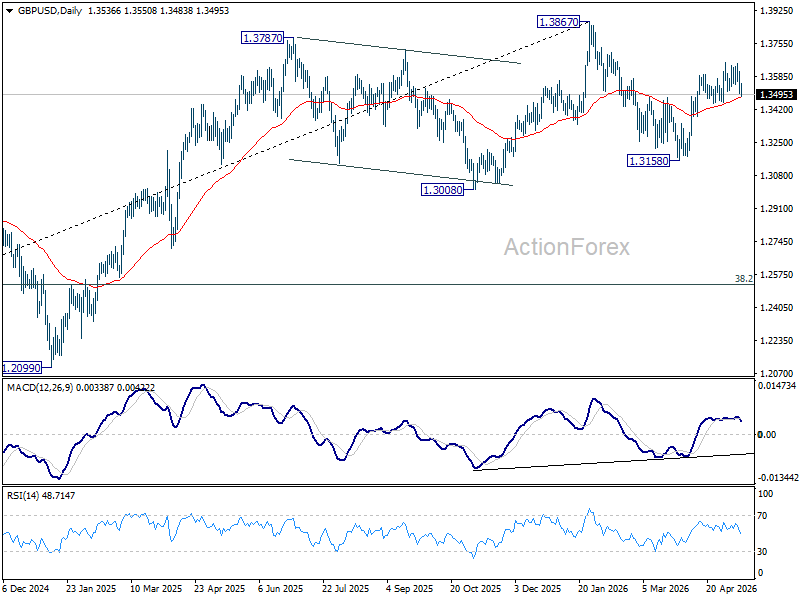

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3488; (P) 1.3548; (R1) 1.3597; More...

GBP/USD weakens again today but stays above 1.3453 support. Intraday bias remains neutral and further rally is still mildly in favor. On the upside, firm break of 1.3657 will resume the rally from 1.3158 to retest 1.3867 high. However, decisive break of 1.3453 will argue that the rebound has already completed, and turn bias to the downside for retesting 1.3158 instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

US PPI Surges to Highest Since 2022 as Upstream Inflation Pressures Intensify

US producer prices surged far more than expected in April, reinforcing concerns that inflation pressures are broadening across the economy and strengthening the case for the Federal Reserve to keep policy restrictive for longer. Headline PPI rose 1.4% mom, accelerating from 0.7% mom previously and well above expectations of 0.5% mom. The increase marked the largest monthly rise since March 2022.

The details of the report showed inflation pressures spreading across both services and goods categories. Nearly 60% of the monthly increase came from a 1.2% mom rise in final demand services prices, while final demand goods prices climbed 2.0% mom. Core producer prices excluding foods, energy, and trade services increased 0.6% mom, matching the strongest monthly gain since October 2025 and suggesting that underlying inflation momentum remains firm even beyond volatile commodity categories.

On an annual basis, headline PPI accelerated sharply from 4.3% yoy to 6.0% yoy, far exceeding expectations of 4.9% yoy and marking the strongest yearly increase since December 2022. Core PPI excluding foods, energy, and trade services rose 4.4% yoy, the highest since February 2023.

The report is likely to reinforce market expectations that the Fed will remain firmly on hold in the near term, while also increasing concern that rising energy prices linked to the Middle East conflict may now be feeding more persistently into broader inflation across the economy.

| Indicator | Previous | Latest |

|---|---|---|

| Headline PPI (MoM) | 0.7% | 1.4% |

| Headline PPI (YoY) | 4.3% | 6.0% |

| Ex Food, Energy & Trade (MoM) | 0.6% | |

| Ex Food, Energy & Trade (YoY) | 4.4% | |

| Final Demand Services | 1.2% | |

| Final Demand Goods | 2.0% |

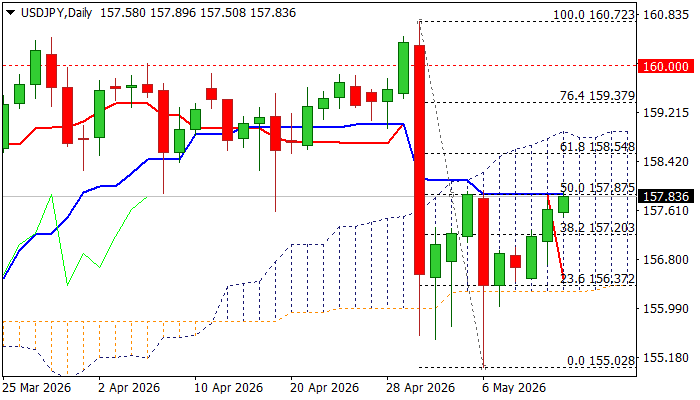

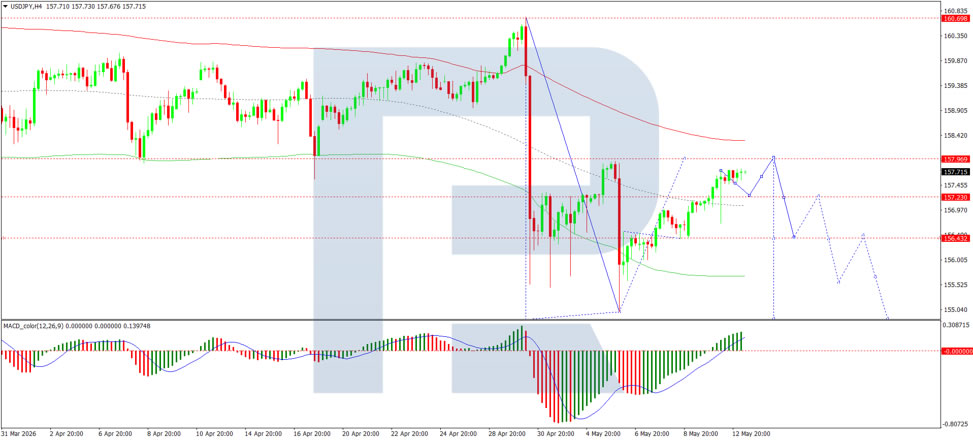

USDJPY Rallies for the Third Day on Geopolitical Uncertainty, Higher US Inflation

USDJPY advances for the third straight day, as stalling peace talks in the Middle East fuel uncertainty and boost dollar’s safe-haven appeal, while fresh rise of inflation in the US adds to Fed’s hawkish stance that underpins the greenback.

Fresh advance emerged after USDJPY’s strong fall from Japan’s authorities’ interventions, ran out of steam that resulted in multiple failure at the base of thick daily cloud and formation of bear-traps, which contributed to reverse of direction and subsequent strong bounce.

Bulls cracked important resistances at 157.90 zone (May 5 lower top / daily Kijun-sen / 50% retracement of 160.72/155.02 fall) with break and close above this barrier needed to generate fresh bullish signal and strengthen near-term structure, which is still fragile (14-d momentum is in negative territory / Stochastic is overbought and DMAs in mixed setup) and warns that recovery may face increased headwinds.

On the other hand, Doji reversal pattern is forming on weekly chart and provides support, as weekly studies are predominantly bullish.

We will continue to closely monitor developments on geopolitical front, which strongly influences market action, as well as reaction at key 157.90 barrier.

Firm break higher to open way for further recovery and expose targets at 158.55 (Fibo 61.8%) and more significand daily cloud top (158.81).

Conversely, failure to clear 157.90 pivot at first attempt would probably keep the price on hold for consolidation, with 100DMA (157.36) marking significant support, which should hold dips to keep near-term bulls in play.

Res: 157.90; 158.25; 158.55; 158.81

Sup: 157.50; 157.36; 157.10; 156.72

Clouds Over the Pound

- Starmer’s power struggle and the associated political risks are weighing on the pound.

- A potential new energy crisis is looming over the euro.

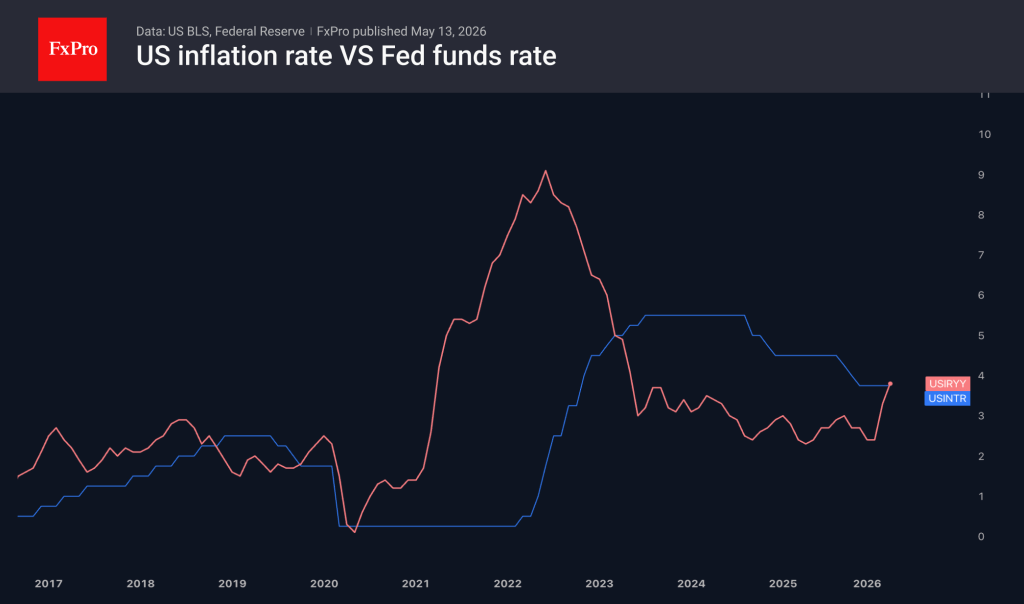

The US dollar reacted calmly to the April US inflation data. Consumer prices surged to a three-year high of 3.8% y/y, raising the chances of the Fed tightening monetary policy this year to 33%, from 16% a week earlier. The date when the probability of a rate hike from current levels exceeds 50% has now shifted from April to March 2027.

The biggest problem is the rise in energy prices. These are always volatile, and monetary policy can do little to address them. Therefore, central banks generally focus on core inflation. In April, it rose to 2.8%. The figure is moving further away from the 2% target and, due to second-order effects, could rise further. On the other hand, CPI indices remain well below their 2022 levels, so there is no need yet for the Fed to tighten monetary policy aggressively.

Meanwhile, MUFG highlights the depletion of gas stocks in the Amsterdam–Rotterdam–Antwerp energy hub. Natural gas prices in Europe have not risen as sharply as they did four years ago, due to full storage facilities. However, should the situation deteriorate, the risk of a decline in the EURUSD exchange rate will begin to mount.

Goldman Sachs cites the ongoing energy shock, the strength of the US economy, high inflation, and the associated rise in Treasury bond yields as arguments in favour of selling EURUSD. The bank also recommends buying the US dollar against the pound and the Swedish krona.

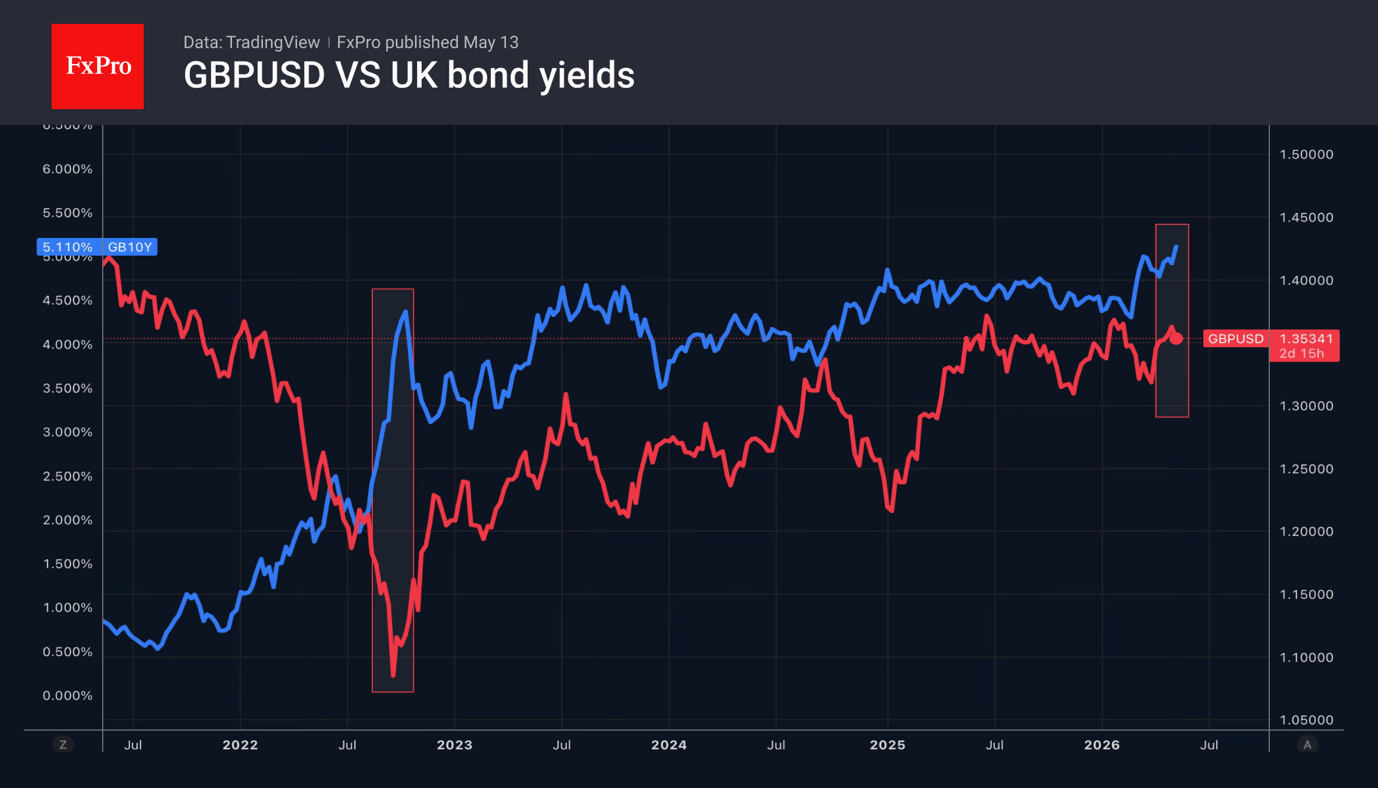

The British pound recorded its worst daily fall since early April. Following Labour’s defeat in the local elections, an increasing number of party members are calling for Keir Starmer to step down as leader. The Polymarket betting market has raised the probability of such an outcome by the end of 2026 from 48% to 66% in just a few days.

Investors fear that the government will be led by a proponent of fiscal stimulus, reigniting the conflict between loose fiscal policy and tight monetary policy, as in 2022. At that time, GBPUSD plummeted to a historic low. So far, parallels can only be seen in the debt market, where, against a backdrop of bond sell-offs, yields on 30-year Gilts have risen to their highest level since 1998.

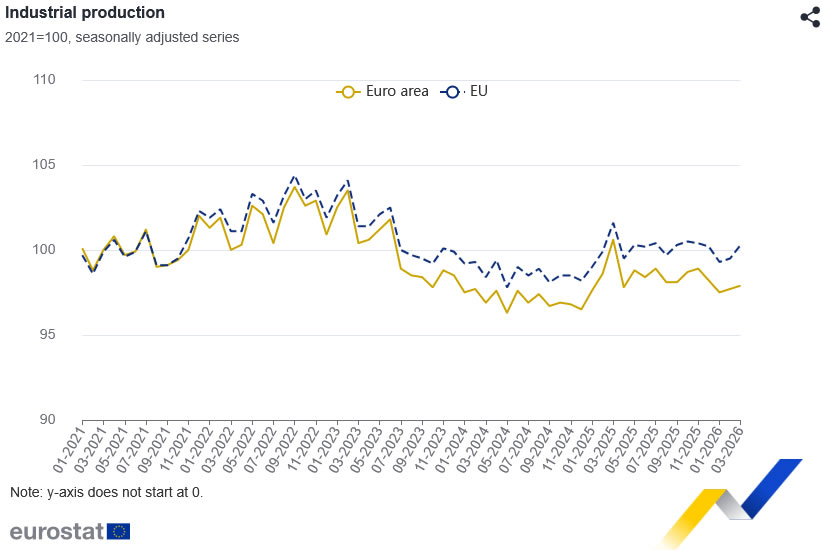

Eurozone Industrial Production Misses Forecast as Energy Output Falls

Eurozone industrial production rose 0.2% mom in March, slightly below expectations of 0.3% mom. Across the broader European Union, industrial production increased a stronger 0.8% mom, helped by robust gains in several Eastern European economies.

The Eurozone sector breakdown showed a mixed picture beneath the headline improvement. Output of capital goods rose 1.1% mom while intermediate goods production increased 0.9% mom, suggesting some resilience in investment-related manufacturing activity. Durable consumer goods also edged up 0.5% mom. However, energy production fell -1.5% mom, while non-durable consumer goods output plunged -4.5% mom.

Among member states, Denmark recorded the strongest monthly gain with industrial output surging 8.4%, followed by Bulgaria at 5.8% and Poland at 5.4%. By contrast, Belgium, Estonia, and Sweden all recorded notable declines.

| Indicator | Latest (mom) |

|---|---|

| Eurozone Industrial Production | 0.2% |

| EU Industrial Production | 0.8% |

| Intermediate Goods Output | 0.9% |

| Capital Goods Output | 1.1% |

| Durable Consumer Goods Output | 0.5% |

| Energy Production | -1.5% |

| Non-Durable Consumer Goods Output | -4.5% |

| EU Countries | |

| Denmark Industrial Output | 8.4% |

| Bulgaria Industrial Output | 5.8% |

| Poland Industrial Output | 5.4% |

| Belgium Industrial Output | -3.0% |

| Estonia Industrial Output | -2.6% |

| Sweden Industrial Output | -1.9% |

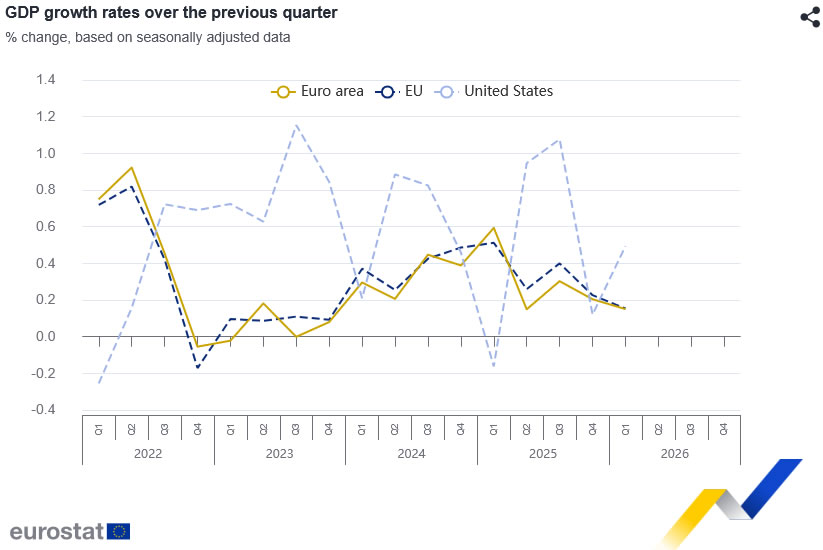

Eurozone GDP Expands Just 0.1% in Q1, Annual Growth Slows to 0.8%

Eurozone economic growth slowed further in the first quarter of 2026 as higher energy costs, weak industrial activity, and lingering geopolitical uncertainty continued weighing on momentum.

According to Eurostat’s flash estimate, seasonally adjusted GDP rose just 0.1% qoq in the Eurozone, down from 0.2% growth in Q4 of 2025. Across the broader European Union, GDP increased 0.2% qoq, unchanged from the previous quarter. The annual growth picture also weakened noticeably. Eurozone GDP growth slowed from 1.3% yoy to 0.8% yoy in Q1. EU-wide annual growth decelerated from 1.4% yoy to 1.0% yoy.

Labor market conditions remained positive but also showed signs of cooling. Employment growth eased from 0.2% qoq to 0.1% qoq in both the Eurozone and the EU during the first quarter. On an annual basis, eurozone employment growth slowed from 0.7% yoy to 0.5% yoy, while EU employment growth held at 0.6% yoy.

| Indicator | Previous | Latest |

|---|---|---|

| Eurozone GDP (QoQ) | 0.2% | 0.1% |

| EU GDP (QoQ) | 0.2% | 0.2% |

| Eurozone GDP (YoY) | 1.3% | 0.8% |

| EU GDP (YoY) | 1.4% | 1.0% |

| Eurozone Employment (QoQ) | 0.2% | 0.1% |

| EU Employment (QoQ) | 0.2% | 0.1% |

| Eurozone Employment (YoY) | 0.7% | 0.5% |

| EU Employment (YoY) | 0.6% | 0.6% |

USD/JPY Continues to Climb Amid External and Domestic Pressures

USD/JPY rose to 157.65 on Wednesday, marking a third consecutive day of gains. The yen came under pressure following stronger-than-expected US inflation data, reinforcing expectations that the Federal Reserve will maintain its hawkish stance.

Market focus remains on the Bank of Japan. Following its April meeting, some policymakers signalled the possibility of a further rate hike. Rising global oil prices are adding to inflationary pressures in Japan. The OECD forecasts that the BoJ’s key rate could reach 2% by the end of 2027.

Currency markets are also watching for potential interventions. US Treasury Secretary Scott Bessent noted that Washington and Tokyo view excessive currency volatility as undesirable, which was seen as indirect support for Japan’s efforts to stabilise the yen.

Technical Analysis

On the H4 chart, USD/JPY is trading around 157.33, with a breakout suggesting further upside towards 157.97. A short-term correction to 156.50 is possible before a potential move higher resumes. The MACD indicator, above zero and pointing firmly upwards, supports further gains.

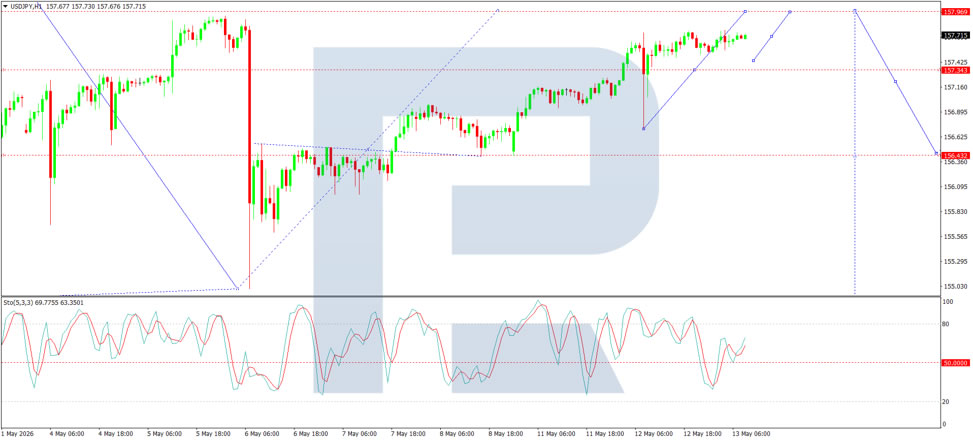

On the H1 chart, USD/JPY has reached 157.77 and is moving lower towards 157.30. A subsequent rise towards 157.97 is possible. The Stochastic oscillator confirms short-term bullish momentum, although a pullback may develop, indicating some near-term downside risk.

Conclusion

USD/JPY is advancing under both external and domestic influences, supported by technical indicators. While short-term corrections are possible, the broader trend remains upward.

Ethereum is Losing Volatility

Market Overview

The crypto market has been hovering around $2.7 trillion in market cap for the past 7 days. Interestingly, while recording relatively stable levels at the start of the day in Europe, the market deviates from this level by almost 2%, only to return to equilibrium very quickly, with yesterday’s leaders turning into underperformers. Over the past 24 hours, the top performers have been NEAR (+5%), TRUMP (+3.8%), and Neo (+3.5%), while the underperformers have been Toncoin (-8%), Theta (-5.2%), and BAT (-2.2%).

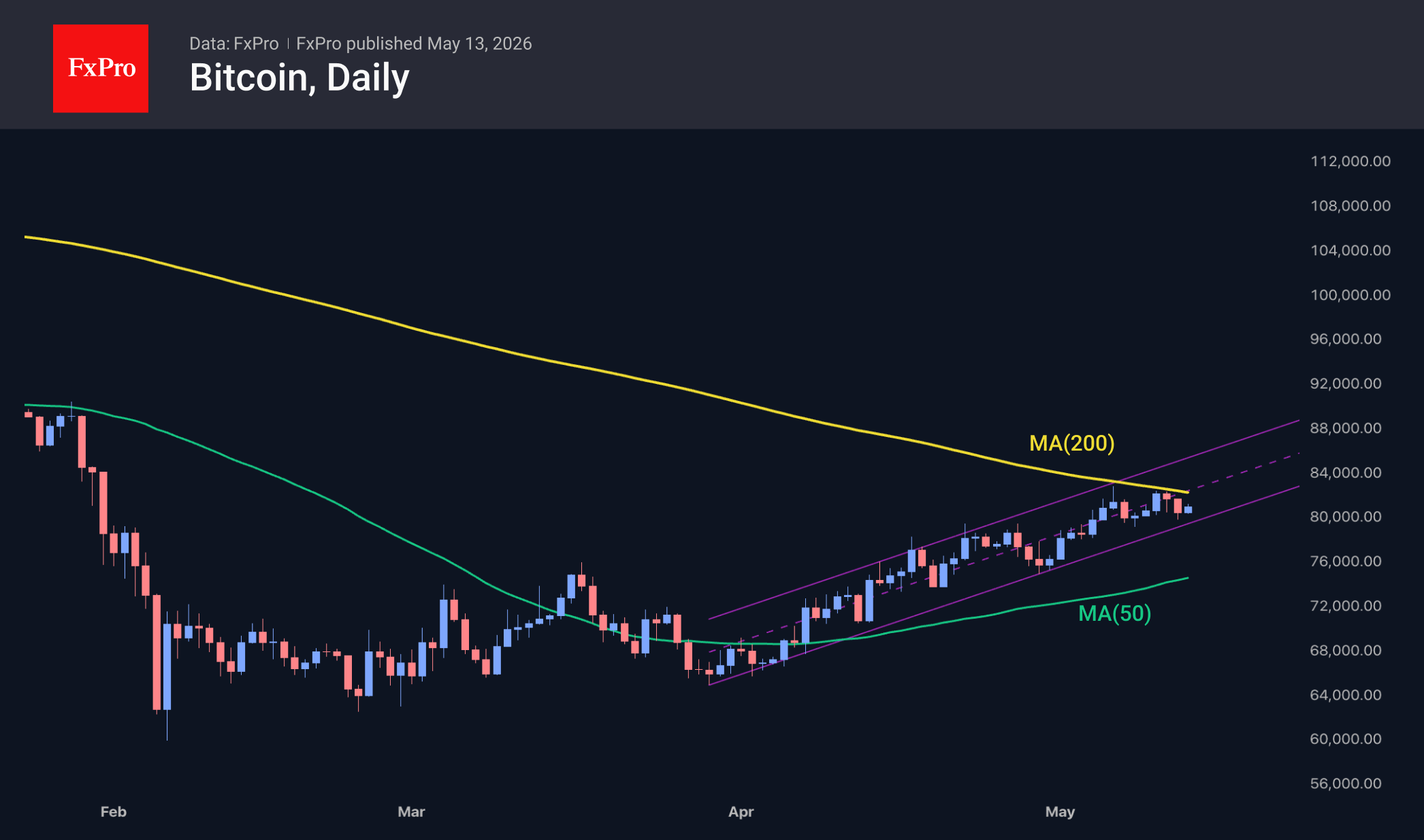

Bitcoin continues to settle quietly at levels above $80K, yet to decide on a breakout above the 200-day moving average. It seems that traders are paying excessive emotional attention to this technical aspect. By way of comparison, just over a year ago, Bitcoin crossed this curve quite freely in both directions.

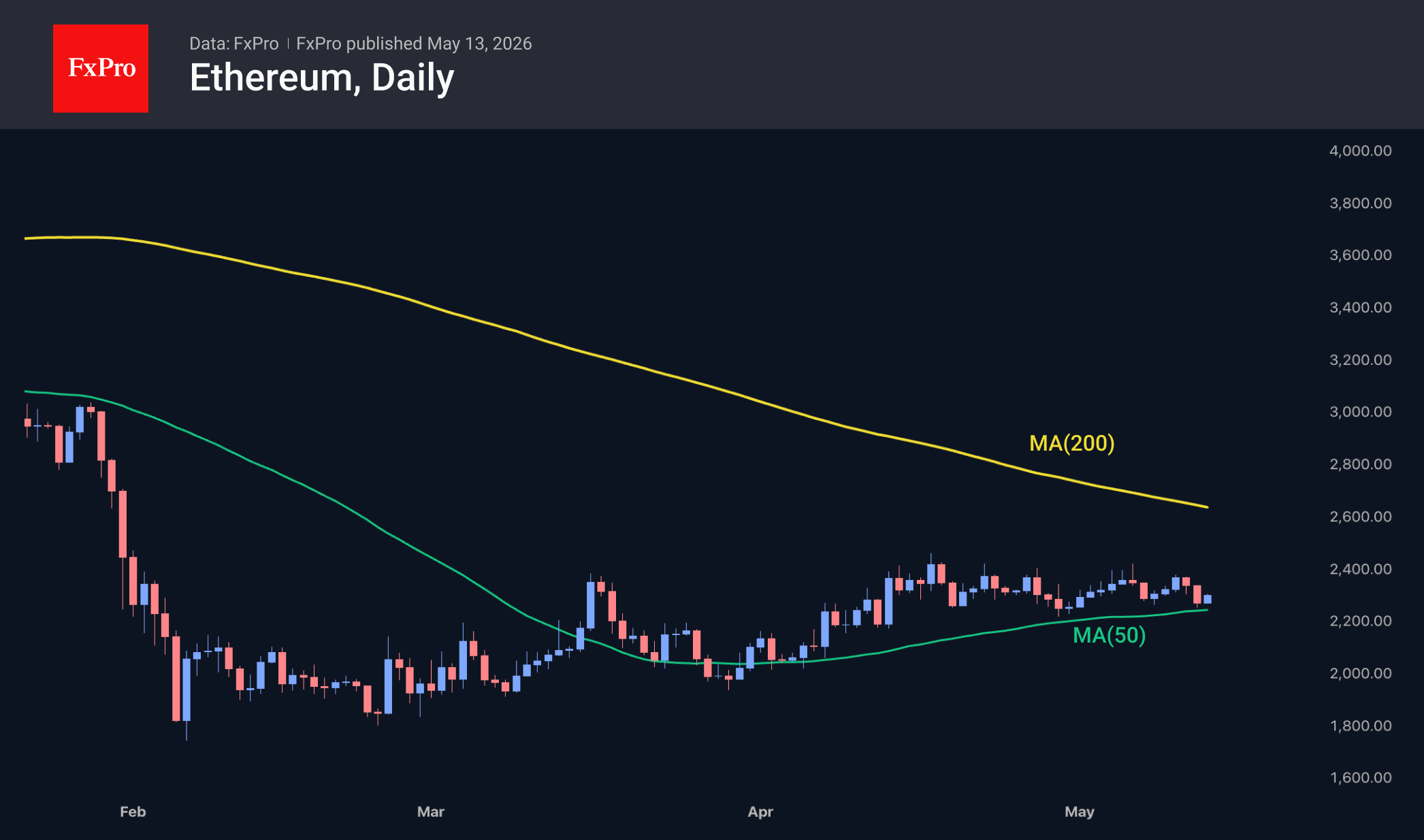

Ethereum has lost all the gains made since the end of last month, once again testing the support level at $2,240, near which the 50-day moving average also lies. Furthermore, over the last four weeks, the second-largest cryptocurrency has been forming a sequence of lower local highs. This has not yet turned into a downtrend, as there is no sequence of lower local lows. The situation resembles a coiled spring.

News Background

The decline in volatility of the leading cryptocurrency and the inflow of institutional capital have altered market cycles, making the current cycle unique, according to CryptoQuant. Price movements now differ from historical data.

Mining company MARA reported a net loss of $1.3 billion and the sale of more than 20,000 bitcoins for the first quarter. The main reason for the negative result was a drawdown in treasury reserves, driven by BTC falling by more than 20% over the quarter. Another major miner, CleanSpark, reported a first-quarter loss of $378 million.

Democratic Party representatives in the US Congress are calling for a ban on officials profiting from crypto assets. Without a compromise on ethical issues, the CLARITY Act will not get a green light. Lawmakers plan to finalise work on it by August.

Despite its popularity, Bitcoin can hardly be called a safe-haven asset, said Ray Dalio, founder of investment firm Bridgewater Associates. In his view, only gold is worthy of that title. The billionaire cited the lack of privacy as one of the main reasons: all transactions are visible on the public blockchain.

Elliptic has raised $120 million to develop tools for tracking cryptocurrencies. The company will use the funds to create and launch AI agents that perform the tasks of compliance officers.

EUR/USD Revisits Support While USD/JPY Eyes Bigger Recovery Move

EUR/USD declined from 1.1800 and traded below 1.1750. USD/JPY is rising and might gain pace above 158.00 and 158.80.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline after a decent move to 1.1800.

- There was a break below a key bullish trend line with support at 1.1765 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 156.40 and 157.10 levels.

- There is a major bullish trend line forming with support at 157.40 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair climbed above the 1.1780 resistance zone before the bears appeared, as discussed in the previous analysis. The Euro started a fresh decline and traded below 1.1765 against the US Dollar.

There was a break below a key bullish trend line with support at 1.1765. The pair declined below 1.1750 and tested 1.1720. A low was formed near 1.1721 and the pair started a consolidation phase.

There was a minor recovery wave above 1.1740 and the 23.6% Fib retracement level of the downward move from the 1.1787 swing high to the 1.1721 low. EUR/USD is still trading below 1.1750 and the 50-hour simple moving average.

On the upside, the pair is now facing hurdles near 1.1745. The next key resistance is 1.1755 and the 50% Fib retracement. The main barrier for the bulls could be 1.1785. A clear move above 1.1785 could send the pair toward 1.1840. An upside break above 1.1840 could set the pace for another increase. In the stated case, the pair might rise toward 1.1920.

If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.1720. The next important region for buyers sits at 1.1700. If there is a downside break below 1.1700, the pair could drop toward 1.1675. Any more losses might send the pair toward 1.1640.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a fresh upward move from 155.00. The US Dollar gained bullish momentum above 156.50 against the Japanese Yen.

It even cleared the 50-hour simple moving average and 157.00. The pair climbed above 157.50 and traded as high as 157.78. The pair is now consolidating gains above the 23.6% Fib retracement level of the upward move from the 155.03 swing low to the 157.78 high.

The current price action above 157.40 is positive. Immediate resistance on the USD/JPY chart sits at 157.80. The first key hurdle is near 158.00. If there is a close above 158.00 and the RSI moves above 65, the pair could rise toward 158.80.

The next major stop for the bulls could be 159.50, above which the pair could test 160.00 in the coming days. On the downside, the first major support is 157.40, a bullish trend line, and the 50-hour simple moving average.

The next area of interest for buyers could be 157.10. If there is a close below 157.10, the pair could decline steadily. In the stated case, the pair might drop toward the 50% Fib retracement at 156.40. Any more losses might open the doors for a drop to 155.00.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Chart Alert: Nasdaq 100 Faces Pullback Risk as Semiconductor Rally Shows Signs of Exhaustion

Key Takeaways

- Nasdaq 100 extended its medium-term bullish trend to a fresh record high of 29,390, supported largely by explosive gains in semiconductor and AI-related stocks such as Intel, Advanced Micro Devices, and SanDisk.

- The strong correlation between the Nasdaq 100 and the iShares Semiconductor ETF suggests that emerging exhaustion signals in semiconductor stocks could trigger a near-term corrective pullback in the broader tech-heavy index.

- Bearish technical indicators, including bearish RSI divergence, overstretched price action above the 20-day moving average, and Bollinger Band exhaustion conditions, point to rising risks of a short-term mean reversion decline below the 29,505/615 resistance zone.

The price actions of the US Nasdaq CFD index, a proxy of the Nasdaq 100 E-mini futures, have surged as expected. It rallied by 3.2% from Friday, 8 May 2026 intraday low of 28,480 to hit a fresh all-time intraday high of 29,390 on Monday, 11 May 2026 in the US session.

Its current medium-term uptrend phase has been in place since the 30 March 2026 low, and a significant contribution of the gains has come from US semiconductor and AI-hardware-related stocks, such as SanDisk, up 151%, Intel, up 150%, and Advanced Micro Devices, up 105%, in the past three months.

US Semiconductors Are Showing Signs of Medium-Term Bullish Exhaustion

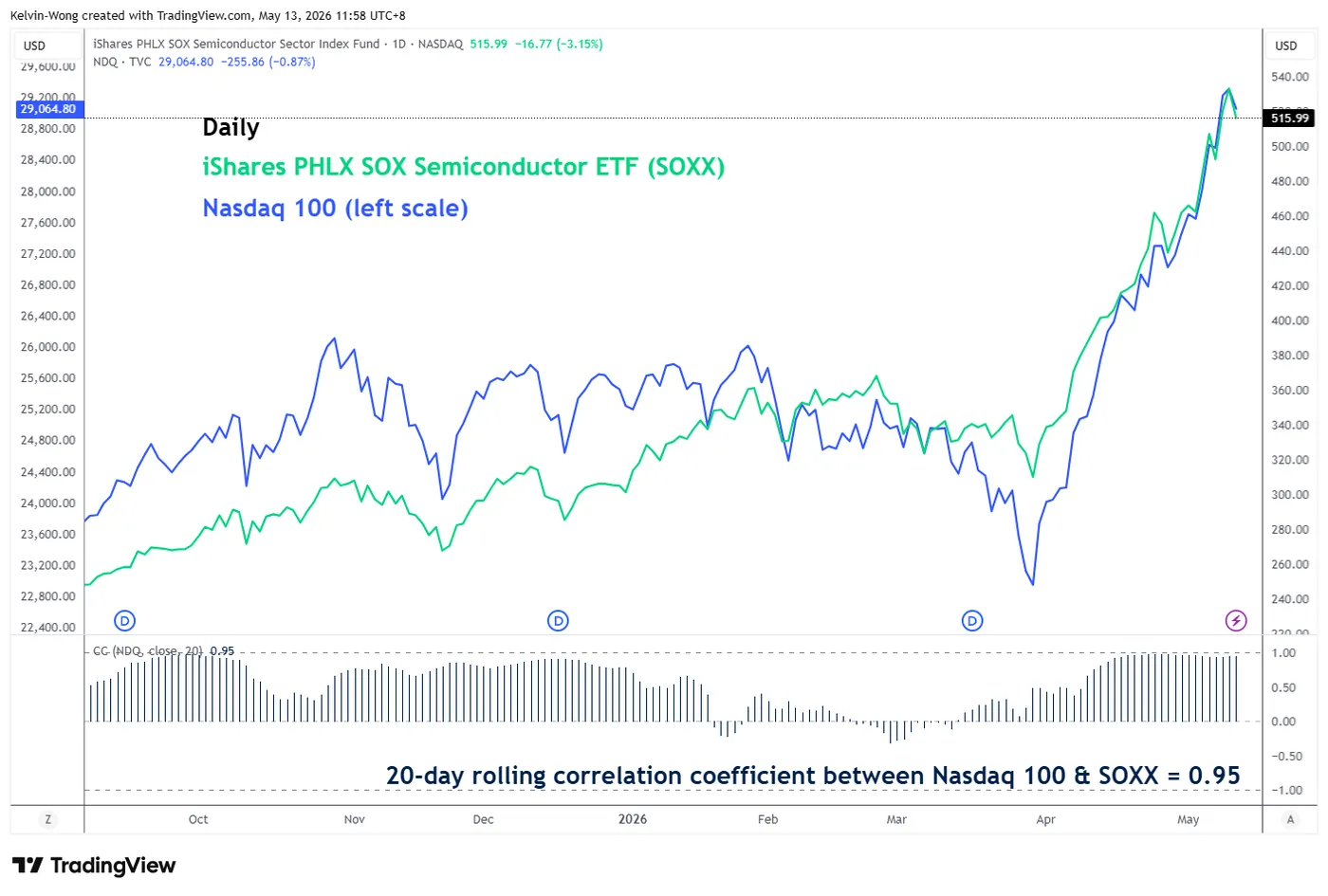

Fig. 1: Correlation of iShares PHLX SOX Semiconductor ETF, SOXX, with Nasdaq 100 as of 12 May 2026. Source: TradingView.

Fig. 2: iShares PHLX SOX Semiconductor ETF, SOXX, medium-term trend as of 12 May 2026. Source: TradingView.

The price movement of the Nasdaq 100 and the iShares Philadelphia, PHLX, Semiconductor Sector exchange-traded fund, SOXX, has moved in almost perfect direct lockstep.

The 20-day rolling coefficient between the Nasdaq 100 and SOXX stands at 0.95, which indicates that future movements of US semiconductor stocks, using SOXX as a bellwether, are likely to have a significant influence and impact on the Nasdaq 100.

The prior 6-week consecutive rally of the SOXX has reached an overstretched volatility condition, as seen in the daily Bollinger Bands indicator.

The daily price action of SOXX had a daily close above the upper Bollinger Band, two standard deviations away from the 20-day moving average, on Monday, 11 May 2026, coupled with a bearish divergence condition seen on the daily RSI momentum indicator at its overbought zone.

These observations suggest the bullish impulsive up move of SOXX since the 30 March 2026 low has reached a potential bullish exhaustion condition, where the next movement may be a multi-day corrective decline sequence, in turn triggering a negative feedback loop into the Nasdaq 100.

Let’s now uncover the short-term, 1- to 3-day, trajectory of the Nasdaq 100 from a technical analysis perspective.

Nasdaq 100: At Risk of Minor Mean Reversion Decline Below 29,505/615

Fig. 3: US Nasdaq 100 CFD index minor trend as of 13 May 2026. Source: TradingView.

Trend bias: Minor corrective decline below 29,505/615 key short-term pivotal resistance within medium-term uptrend.

Supports: 28,660, 28,460/280, and 27,850, close to the 20-day moving average.

Next resistances: 29,893/953 and 30,410/417, Fibonacci extension clusters.

Key Elements Supporting the Near-Term Bearish Bias on the Nasdaq 100

- The current all-time intraday high of 29,390 printed on Monday, 11 May 2026, has moved significantly away from its 20-day moving average by almost 6%.

- The hourly RSI momentum indicator flashed a bearish divergence condition on Monday, 11 May 2026.

- The hourly RSI momentum indicator staged a bearish breakdown below its key ascending support on Tuesday, 12 May 2026.