Sample Category Title

Dollar Struggles to Keep Momentum in Indecisive Markets

In the forex market, clear weakness of Yen, Swiss Franc, and Kiwi contrasts with a broader sense of indecision elsewhere. Dollar's rally attempt quickly lost momentum as it struggled to break through near-term resistance levels against both the Euro and Sterling. Additionally, the greenback remains stuck within familiar ranges against the Aussie and Loonie, a trend that has persisted since early Q2. Market participants are now eyeing Fed Chair Jerome Powell's speech at the ECB forum today, though it is unlikely to offer any significant new insights. Traders are more focused on tomorrow's ISM Services PMI and Friday's Non-Farm Payroll report before making substantial moves.

At this point in the week, Euro is the best performer, although it lacks follow-through momentum due to political uncertainties in France. Sterling is the second strongest currency, followed by Dollar. On the other hand, Swiss Franc remains the worst performer, followed by Kiwi and Yen. The Aussie and the Loonie are positioned in the middle of the performance spectrum.

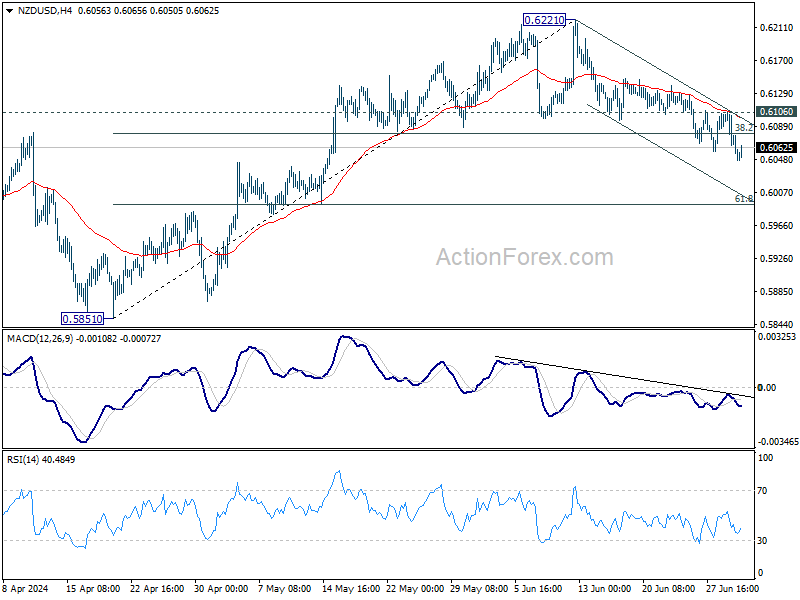

Technically, NZD/USD's fall from 0.6221 resumed today and further decline is expected as long as 0.6106 resistance holds. Even as a corrective move, current decline would now target 61.8% retracement of 0.5851 to 0.6221 at 0.5992. However, firm break of 0.6106 will argue that the pullback has completed and bring retest of 0.6221 high instead.

In Europe, at the time of writing, FTSE is down -0.44%. DAX is down -1.14%. CAC is down -0.84%. UK 10-year yield is down -0.0409 at 4.246. Germany 10-year yield is down -0.007 at 2.601. Earlier in Asia, Nikkei rose 1.12%. Hong Kong HSI rose 0.29%. China Shanghai SSE rose 0.08%. Singapore Strait Times rose 0.88%. Japan 10-year JGB yield rose 0.0276 to 1.092.

Fed's Goolsbee suggests rate cuts if inflation declines further

Chicago Fed President Austan Goolsbee has suggested that Fed should consider cutting interest rates if inflation continues its downward trajectory towards the 2% target. He emphasized the importance of adjusting monetary policy to align with changing inflation dynamics.

Goolsbee explained that holding the current rate as inflation decreases effectively tightens monetary conditions. He noted, "If you sit with the rate somewhere while inflation goes down, you're tightening. The reason that you would want to tighten is if you think that you're not on a path to 2%."

Furthermore, Goolsbee pointed out the importance of balancing inflation control with overall economic stability. He noted, "If employment starts falling apart or if the economy begins to weaken, which you've seen some warning signs, you've got to balance that off with how much progress you're making on the price front." While acknowledging that the unemployment rate remains relatively low, he also highlighted its recent upward trend, indicating potential economic softening.

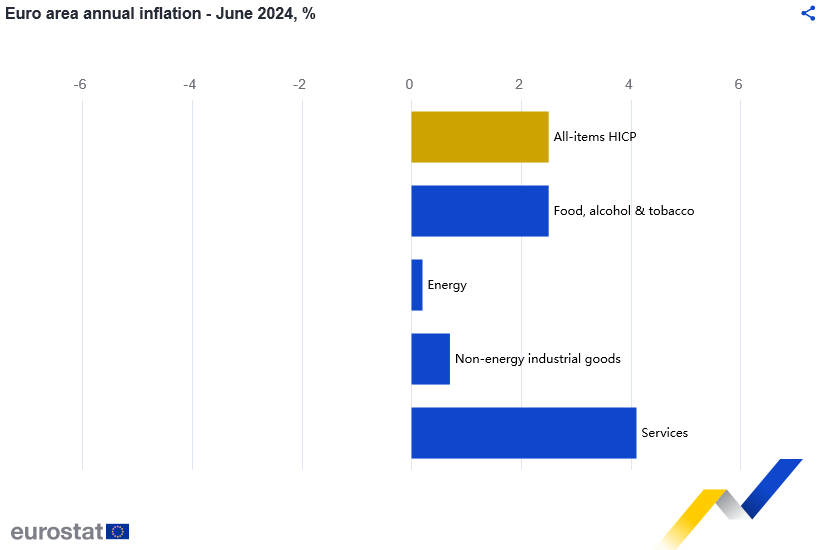

Eurozone CPI slowed to 2.5% in Jun, but core unchanged at 2.9%

Eurozone CPI slowed from 2.6% yoy to 2.5% yoy in June, matched expectations. CPI core (ex-energy, food, alcohol & tobacco) was unchanged at 2.9% yoy, above expectation of 2.8% yoy.

Looking at the main components, services is expected to have the highest annual rate in June (4.1%, stable compared with May), followed by food, alcohol & tobacco (2.5%, compared with 2.6% in May), non-energy industrial goods (0.7%, stable compared with May) and energy (0.2%, compared with 0.3% in May).

ECB's Lane highlights need for more data on services inflation

ECB Chief Economist Philip Lane emphasized today that June inflation data alone will not suffice to address questions surrounding services inflation, suggesting the ECB may delay further interest rate cuts until additional data is available.

Lane noted, "The key is really services inflation. What we've seen in the last days is that services inflation remains the outlier, and what we need to see is whether higher services inflation is a backward element and is a legacy of the rapid disinflation or is it a persistent element. We need time to work on it."

On the political front, Lane downplayed concerns about France's recent political turmoil impacting markets significantly, stating, "It is clearly natural in an election for the market to reprice. There are elections all the time, there are movements in spreads all the time. Of course, France is an important country, but this looks like an ordinary repricing to me."

Other ECB Governing Council members also shared their perspectives at the ECB forum. Lithuania's Gediminas Simkus aligned with expectations for further rate cuts, stating, "Expectations for two more cuts this year are in line with my own thinking, if data evolve as expected." Similarly, Belgium's Pierre Wunsch remarked, "The first two rate cuts are relatively easy as long as inflation hovers around 2.5% because we will still clearly be restrictive."

RBA minutes: The narrow path is becoming narrower

Minutes of RBA's June meeting emphasize the need to remain "vigilant to upside risks to inflation". The RBA noted that the information received since the previous meeting reinforced this need, underscoring the "extent of uncertainty" in the current economic environment, which makes it "difficult either to rule in or rule out" future changes in interest rates.

Concerns were raised about the "narrow path" to bringing inflation back to target within a reasonable timeframe without significantly deviating from full employment. This path, according to the minutes, is "becoming narrower."

The decision to keep the cash rate target unchanged at 4.35% was deemed the stronger option compared to another rate hike. Data received since May meeting "had not been sufficient" to alter RBA's assessment that inflation would return to target by 2026, despite "some elevated upside risk" surrounding the forecast. Moreover, the minutes revealed that the members felt there was "not enough evidence" to suggest that the outlook for aggregate demand had strengthened.

NZIER survey shows rising pessimism among New Zealand firms

The NZIER Quarterly Survey of Business Opinion for Q2 reveals increasing pessimism among New Zealand firms. A net 44% of firms are now pessimistic about the economy's outlook over the next six months, up from 25% in Q1. Additionally, a net 28% reported a deterioration in their own trading during the three months through March, marking the weakest reading since mid-2020 during the COVID-19 pandemic.

Employment figures are equally concerning. A net 25% of firms laid off workers in Q2, the highest level since the global financial crisis in 2009. Furthermore, a net 10% expect to reduce staff numbers in the three months through September. Profit expectations are also bleak, with a net 34% of firms anticipating weaker profits in the third quarter, accompanied by falling investment intentions.

On a slightly more positive note, only a net 23% of firms expect to increase prices in Q3, the lowest since 2021. Additionally, companies are finding it easier to recruit workers, signaling reduced wage pressure. Fewer companies also reported rising costs, suggesting some relief from inflationary pressures.

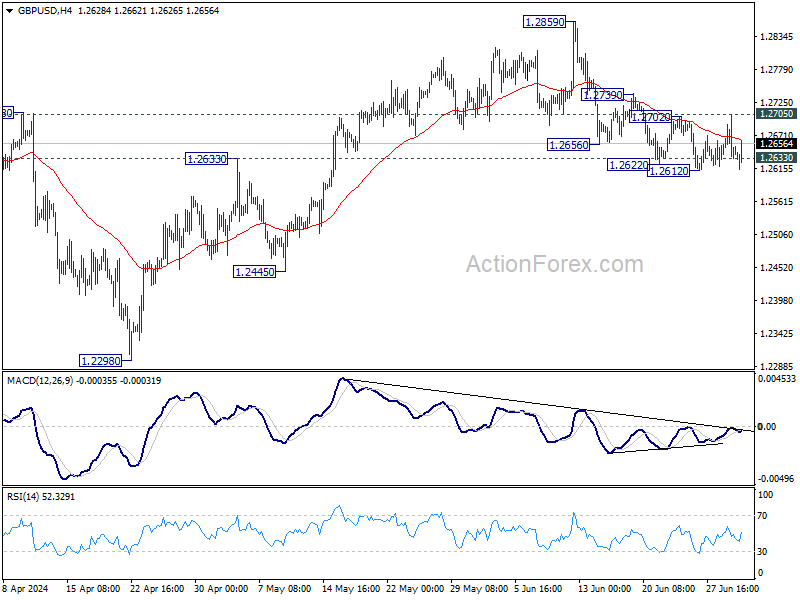

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2622; (P) 1.2661; (R1) 1.2690; More...

GBP/USD recovered ahead of 1.2612 support as range trading continues. Intraday bias remains neutral at this point. On the upside, firm break of 1.2705 resistance will argue that pull back from 1.2859 has completed, and bring retest of this high instead. Nevertheless, sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

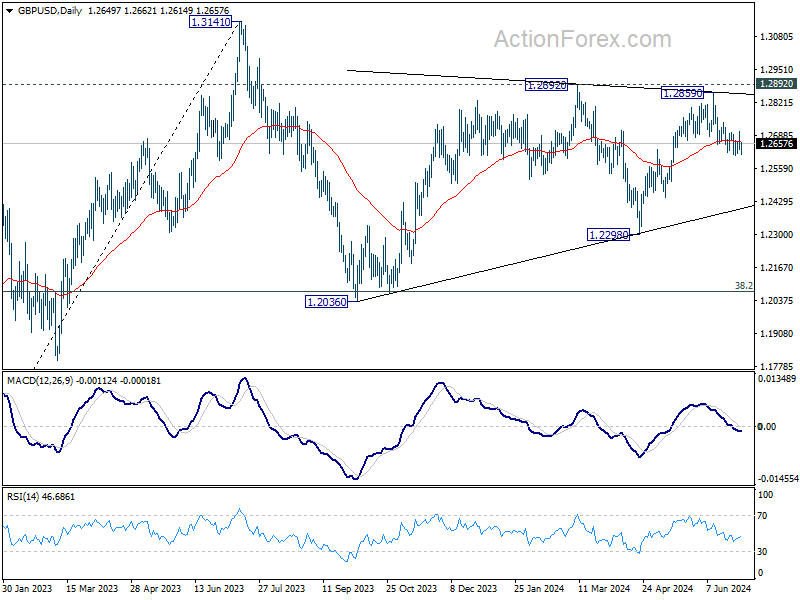

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | -1.70% | -1.90% | -2.10% | |

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 09:00 | EUR | Eurozone Unemployment Rate May | 6.40% | 6.40% | 6.40% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun P | 2.50% | 2.50% | 2.60% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun P | 2.90% | 2.80% | 2.90% | |

| 13:30 | CAD | Manufacturing PMI Jun | 50.2 | 49.3 |

Stocks Held Back Crypto Gains

Market picture

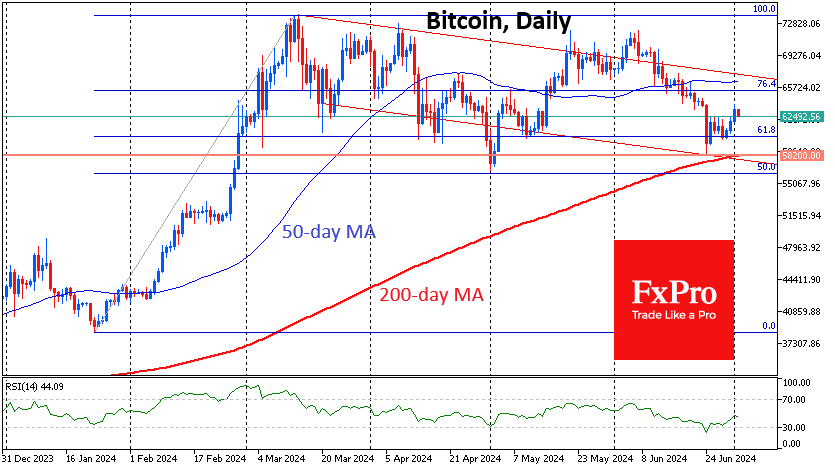

The crypto market retreated by 0.6% in 24 hours to a total cap of $2.31 trillion. The cautious mood can be attributed to a downward move in US and European stock markets and the momentum of a stronger dollar. However, the dynamics of coins are not homogeneous. The decline of more than 1% in Bitcoin, Ethereum, and BNB contrasts with the growth of more than 2.5% in Toncoin, Cardano, and Tron. Temporary institutional favourites are suffering losses due to the pull from risk in traditional financial markets.

Bitcoin has pulled back to $62.6K after two failed attempts to consolidate above $63.0K on Monday. Continued market wariness could bring the price back to the $60K area in the near term, forcing a retest of the 61.8% retracement level from the January lows to the March highs.

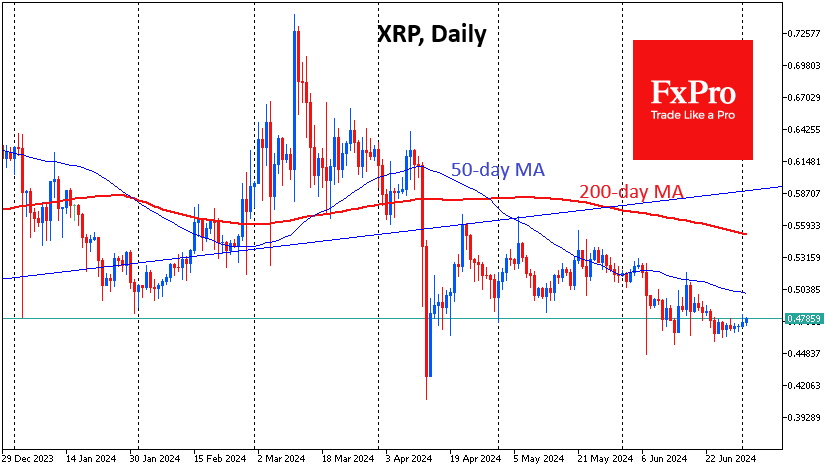

At the end of last month, volatility in XRP was falling after the price returned to the most important support of the last 12 months. Since Saturday, there has been a dominance of buyers, keeping the balance of power on the bullish side until Tuesday morning. In our view, confirmation of the bullish trend recovery is required, which could be a retracement of the $0.50 price where the important round level and the 50-day moving average are combined.

News background

According to CoinShares, crypto fund investments fell by a paltry $30 million last week after outflows of $584 million a week earlier. Bitcoin investments were up $10 million, while Solana was up $1.6 million; Ethereum was down $61 million. Grayscale’s bitcoin ETF saw outflows of $153 million for the week.

Weekly trading volumes rose 43% to $6.2B but remain well below the $14.2bn average for the year.

Bitcoin is looking for the next big catalyst for an upward move. It’s not on the horizon yet, but DigitalX expects things could change as the US election approaches.

The US Treasury Department has approved a new reporting order requiring cryptocurrency brokers, including exchanges and payment processors, to report all sales and exchanges of digital assets to the IRS, regardless of the amount of the transaction.

Vitalik Buterin suggested a way to speed up transactions in Ethereum. One option to increase throughput could be to change the architecture of slots and epochs. According to Arkham, Buterin owns over $857 million in crypto assets.

Circle was the first to receive a licence to issue stablecoins under the new Cryptocurrency Regulation Act in the European Union (MiCA). Circle Mint France was granted the right to issue EURC and USDC euro-denominated stablecoins.

Apollo Crypto noted that NFT sales collapsed by 44% in the second quarter due to the crypto market’s downturn and the meme token boom. This is largely due to interest in ‘political’ and celebrity-created meme coins.

Air purifier manufacturer Kronos Advanced Technologies became the first US public company to accept payment for its products using SHIB tokens.

Fed’s Goolsbee suggests rate cuts if inflation declines further

Chicago Fed President Austan Goolsbee has suggested that Fed should consider cutting interest rates if inflation continues its downward trajectory towards the 2% target. He emphasized the importance of adjusting monetary policy to align with changing inflation dynamics.

Goolsbee explained that holding the current rate as inflation decreases effectively tightens monetary conditions. He noted, "If you sit with the rate somewhere while inflation goes down, you're tightening. The reason that you would want to tighten is if you think that you're not on a path to 2%."

Furthermore, Goolsbee pointed out the importance of balancing inflation control with overall economic stability. He noted, "If employment starts falling apart or if the economy begins to weaken, which you've seen some warning signs, you've got to balance that off with how much progress you're making on the price front." While acknowledging that the unemployment rate remains relatively low, he also highlighted its recent upward trend, indicating potential economic softening.

EUR/USD: Euro Bulls Should Not be Complacent after French Election

- Sovereign credit risk remains elevated in France despite yesterday’s rallies seen in the EUR/USD, CAC 40 & DAX ex-post first round of the French legislative election.

- Speculative net capital outflows & bearish sentiment in CAC 40 & DAX may trigger a negative feedback loop into the EUR/USD.

- EUR/USD at risk of breaking down below 1.0656

The EUR/USD gapped up by 26 pips at the start of yesterday, 1 July Asian session from last Friday, 28 June US session close of 1.0713 on a positive backdrop that preliminary results of the first round of the French legislation election that saw Le Pen’s far-right National Rally party took the lead but without a majority foothold ahead of the far-left coalition party, New Popular Front while French President Macron’s centrist alliance dwindled to third place. The National Rally party fell short of obtaining the absolute majority of 289 seats to control the French Parliament.

Together with news flow that reported horse-trading activities have taken place between the far-left and Macron’s centrist party to prevent Le Pen’s National Rally from securing a majority foothold in the upcoming second round of voting that occurs this Sunday, 7 July, the EUR/USD rallied further during the start of yesterday’s European session to print an intraday high of 1.0777, that’s summed up to an intraday gain high watermark of +64 pips/+0.60% from last Friday, US session close.

Similar intraday positive performances can also be observed on the benchmark stock indices for France and Germany where the CAC 40 and DAX recorded an intraday gain high watermark of +1.91% and +1.24% from their respective closing levels of last Friday.

Reversal of yesterday’s intraday gains in the EUR/USD, CAC 40 & DAX

However, these intraday rallies cannot be maintained, and the EUR/USD ended yesterday’s session,1 July with a meagre daily gain of just +0.25%, and a similar reversal can also be seen on the French and German stock markets where the CAC 40 and DAX pared back almost 50 percent or more of their early intraday gains yesterday to record closing daily gains of +1.09% and +0.30% respectively.

Sovereign credit risk remains elevated in France

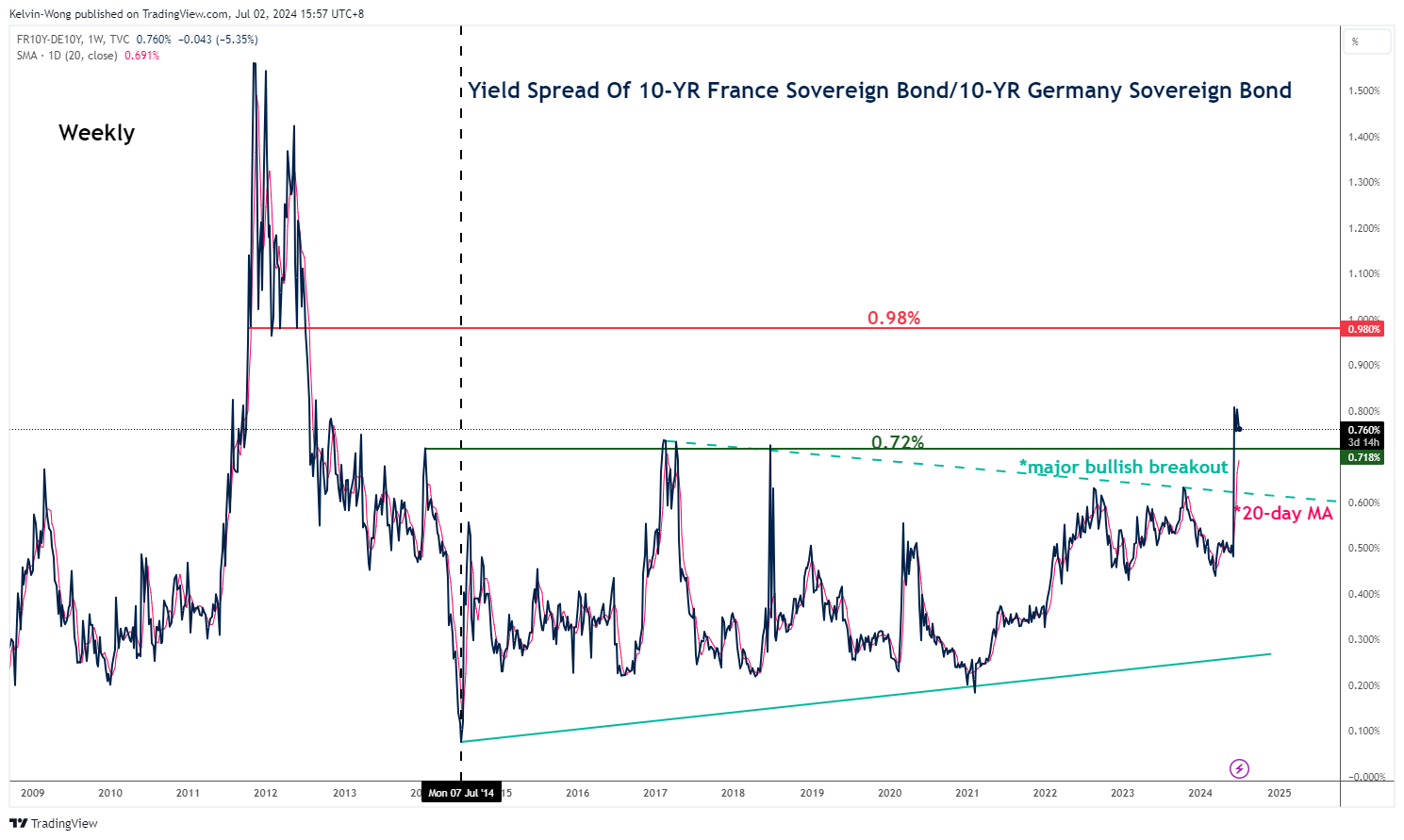

Fig 1: Yield spread of 10-year French & German government bonds as of 2 Jul 2024 (Source: TradingView, click to enlarge chart)

Even though, the yield spread between the 10-year France and German sovereign bond has inched lower slightly to 0.765% at this time of the writing from a 12-year high of 0.82% printed last Thursday, 27 June; it remains at an elevated level according to its trend analysis.

The yield spread is still evolving within a short-term uptrend phase after a major bullish breakout that occurred on the week of 10 June 2024 as it remains supported at 0.72% which corresponds to a rising 20-day moving average with the next medium-term resistance coming in at 0.98% (see Fig 1).

Also, if Macron’s centrist alliance decides to support the far-left coalition, the New Popular Front party now in second place after the first round of voting with a projected vote share of 28% to 29%, it may allow the far-left party an easier maneuver ticket in the France parliament to advocate their more aggressive fiscal spending policies and tax cuts as compared to the far-right which in turn is likely to widen France’s last year excessive budget deficit of 5.5% that breached EU’s benchmark budget deficit ceiling of 3%.

Therefore, the bond vigilantes are still on the lookout for a possible uptick in credit risk in France which in turn may spread to the wider Eurozone due to the contagion effect as European banks do have significant holdings of French sovereign bonds since France is one of the economic anchors in the EU other than Germany.

Current short-term bearish trends in CAC 40 & DAX trend may trigger negative sentiment towards the Euro

Fig 2: France CAC 40 medium-term trend as of 2 Jul 2024 (Source: TradingView, click to enlarge chart)

Fig 3: Germany DAX medium-term trend as of 2 Jul 2024 (Source: TradingView, click to enlarge chart)

As seen in the daily technical charts of the French CAC 40 and German DAX, both of them are still evolving in short-term bearish trends as their respective price actions remain below their respective downward-sloping 20-day moving averages with bearish momentum conditions seen in their daily RSI momentum indicators.

Interestingly, yesterday’s price actions of the CAC 40 and German DAX have shaped daily key bearish reversals right below their respective key short-term pivotal resistances of 7,725 and 18,465 respectively (see Fig 2 & 3).

The short-term movements in the FX market are also impacted by short-term speculative equities-related capital flows. Given the prevailing short-term bearish trends that are still intact on the CAC 40 and DAX, in turn, may see net short-term capital outflows that can likely trigger a double-whammy negative impact on the EUR/USD at least on a short-term horizon from both flows and sentiment perspectives.

Watch the 1.0770/0790 key short-term resistance on EUR/USD

Fig 4: EUR/USD short-term trend as of 2 Jul 2024 (Source: TradingView, click to enlarge chart)

Current price actions of the EUR/USD have wiped out yesterday’s post-French election results-induced rally after a bearish reversal right at the intersection of all three key moving averages (20-day, 50-day, and 200-day), and the 4-hour RSI momentum indicator has flashed out a bearish condition (see Fig 4).

These observations from a technical analysis perspective suggest low odds of a potential recovery or bottoming configuration at play for the EUR/USD.

If the 1.0770/0790 key short-term pivotal resistance holds, a break below 1.0656 support (lower limit of the “Symmetrical Triangle” range from 3 October 2023 low) may trigger further downside pressure to expose the next intermediate supports at 1.0620/0600 and 1.0530.

However, a clearance above 1.0770/0790 negates the bearish tone for a squeeze up towards the upper limit of the “Symmetrical Triangle “range to see the next intermediate resistances coming in at 1.0815, 1.0850, and 1.0925/0940.

Australian Dollar Eyes Retail Sales

The Australian dollar has posted slight losses on Tuesday. AUD/USD is trading at 0.6649 in the European session, down 0.15% on the day.

Australian retail sales expected to improve

Australian consumers have been in frugal mood and have reduced their discretionary spending. Consumers have been squeezed by high borrowing costs and the high cost of living. Retail sales ticked upwards by only 0.1% m/m in April. The gain was negligible, considering that Australia’s population has been swelling due to an increase in immigration. The May retail sales report on Wednesday is expected to show some improvement, with a market estimate of 0.3% m/m.

RBA minutes: higher rates could be needed

The RBA minutes from the meeting earlier this month noted that the Board decided that the case to hold rates was stronger than for hiking. The RBA held rates at 4.35% for a fifth straight time but the Board raised concerns about the rise in inflation expectations and warned that it might have to raise rates if the current policy was not “sufficiently restrictive”.

The takeaway is that the RBA won’t be abandoning its “higher for longer” stance anytime soon. The second-quarter inflation report will be released on July 31 and will be a key factor in the RBA’s rate decision a week later.

The weak Australian economy could use a rate cut but the Reserve Bank of Australia is handcuffed due to rising inflation, particularly service inflation. CPI jumped to 4.0% in May, up from 3.6% in April and higher than the market estimate of 3.8%. The RBA may have to delay an initial rate cut until 2025 if there is no significant progress in the battle against inflation.

The RBA’s target range is 2% to 3% and the final phase of bringing inflation back down to the target range has proven elusive despite high interest rates. There is a real possibility that the RBA could raise rates in order to dampen inflation, a specter that consumers and businesses hope does not materialize.

AUD/USD Technical

AUD/USD tested resistance at 0.6660 earlier. Above, there is resistance at 0.6699

0.6630 and 0.6591 are the next support levels

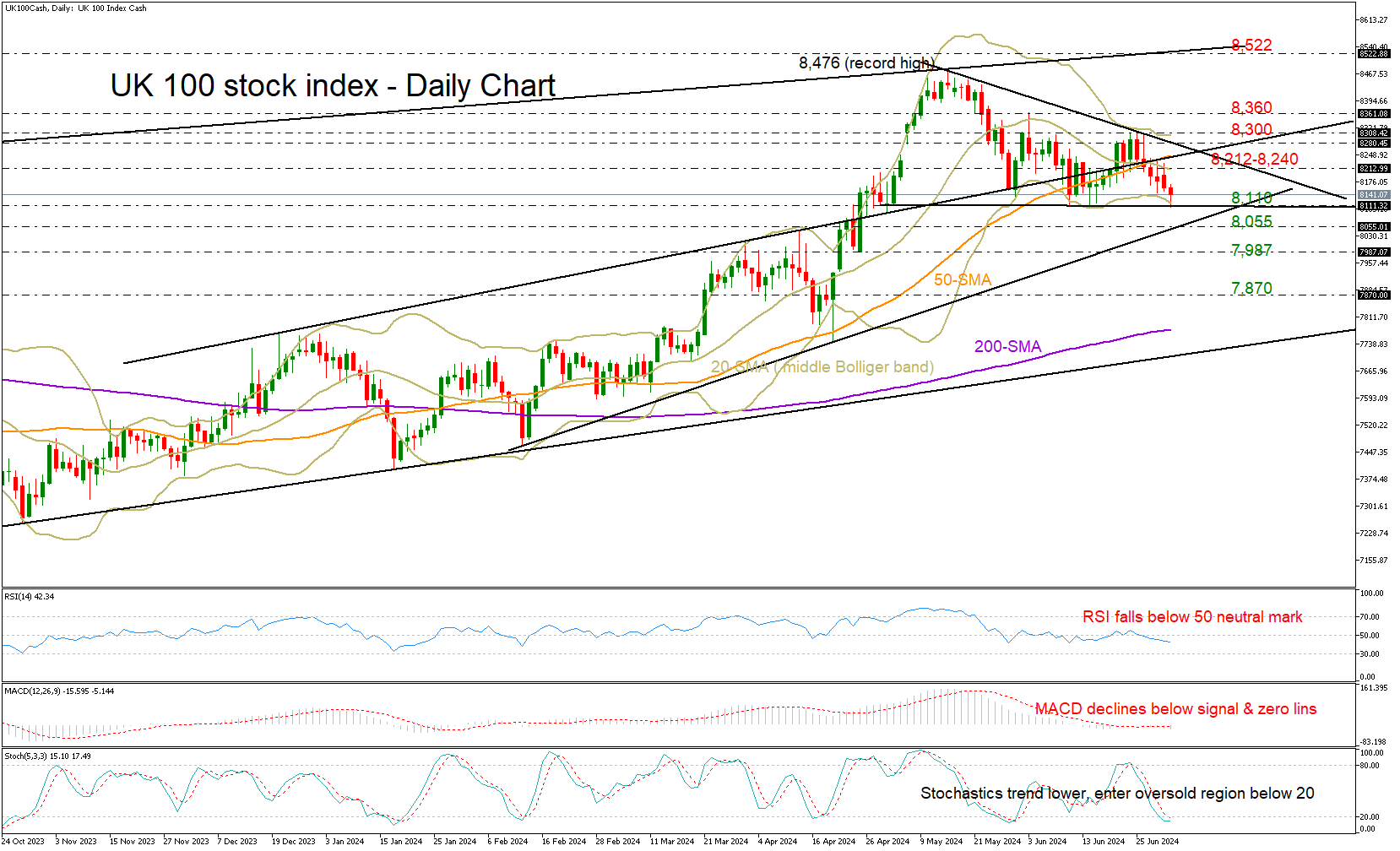

UK 100 Index Experiences Pre-election Decline

- UK 100 index erases June’s recovery attempt as the UK election looms

- A break below 8,055 could worsen short-term outlook

The UK 100 stock index (cash) continues to suffer for the sixth consecutive trading day, extending its downleg aggressively to the critical support zone of 8,110 on Tuesday ahead of the election day on July 4.

The index could not mark a new higher high above the key resistance area of 8,300 and the important resistance line from February 2022, increasing fears that the negative reversal from the 8,476 record high could gain more legs.

Discouragingly, the 20- and 50-day simple moving averages (SMAs) have already posted a bearish cross, promoting the case of a bearish continuation. In addition to this, the RSI is currently losing ground below its 50 neutral mark and the MACD is diminishing below its zero and signal lines, both reflecting a clear bearish bias.

A step below the base of 8,110 could dampen market sentiment, but traders may not rush to sell the index until the price drops decisively below the ascending trendline at 8,055. Note that the stochastic oscillator is already within the oversold region, while the price itself is hovering near the lower Bollinger band. Hence, a pause in the ongoing bearish phase is likely. Yet, if the bears claim the 8,055 area, the next stop could be around April’s constraining region of 7,987, a break of which could cause a sharper downfall towards the 7,870 zone.

On the upside, the bulls must exit the triangle and knock down the wall at 8,300 in order to boost buying appetite towards the 8,360-8,400 barrier, but before that, they should first claim the 20- and 50-day SMAs at 8,212 and 8,245 respectively. Long-term traders might wait for a bullish trend extension above the crucial resistance line at 8,522 before driving towards the 8,600 psychological mark.

In summary, the UK 100 stock index is holding a bearish bias in the short-term picture, but selling interest could stay balanced until the price slides below 8,055.

Eurozone CPI slowed to 2.5% in Jun, but core unchanged at 2.9%

Eurozone CPI slowed from 2.6% yoy to 2.5% yoy in June, matched expectations. CPI core (ex-energy, food, alcohol & tobacco) was unchanged at 2.9% yoy, above expectation of 2.8% yoy.

Looking at the main components, services is expected to have the highest annual rate in June (4.1%, stable compared with May), followed by food, alcohol & tobacco (2.5%, compared with 2.6% in May), non-energy industrial goods (0.7%, stable compared with May) and energy (0.2%, compared with 0.3% in May).

Full Eurozone CPI release here.

Silver Price Analysis: Awaiting Powell’s Comments

Today, at 16:30 GMT+3, the Federal Reserve Chairman is scheduled to speak. Market participants are looking for more clarity on the Fed's plans regarding interest rate cuts following the release of inflation data last Friday.

According to Trading Economics, Fed officials have repeatedly called for caution before cutting rates, and Federal Reserve Board member Michelle Bowman stated that she is open to further rate hikes if progress in combating inflation stalls or reverses.

Powell's speech will significantly impact many financial markets, including the precious metals market, as lowering interest rates could increase the appeal of gold and silver as "safe haven" assets compared to bonds.

It is important to note that besides the Fed's monetary policy, the XAG/USD price is significantly influenced by news about the Chinese economy – the largest consumer of silver. The demand outlook remains uncertain, considering that official data for June indicated a second consecutive month of production decline.

Technical analysis of the XAG/USD chart provides more useful information:

→ Silver prices were in an upward trend (indicated by a blue channel), peaking at a multi-year high reached in late May above the $31 per ounce level.

→ The ATR indicator pointed to increased activity during those days. It is likely that major players used the buoyant market, supported by optimistic news, to close long positions.

→ Regardless, silver prices have since started forming a downward trend (indicated by a red colour). The $31 level has shown signs of resistance, and the lower boundary of the blue channel has been broken.

→ The $28.75 level (former resistance) is now showing signs of support.

It is possible that the broad range of $28.75 - $31.00 will become a zone where the silver price finds equilibrium, resilient to various influencing factors, including today's speech by Powell. Be prepared for volatility spikes.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

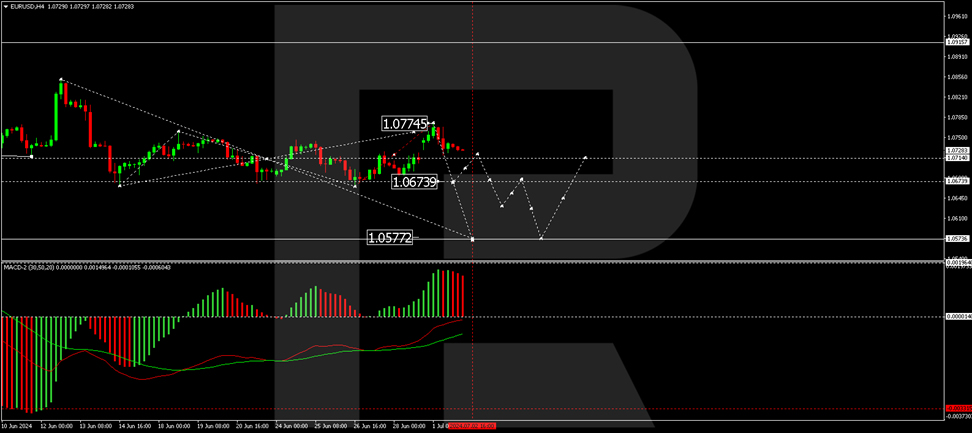

EUR/USD Struggles to Maintain Gains Amid Mixed Economic Signals

The EUR/USD pair experienced a noticeable uptick yesterday, but failed to sustain its peak, settling at 1.0732 today. Early gains were buoyed by the initial outcomes from France's parliamentary elections, which did not reflect the worst-case scenario, sparking a temporary surge in risk appetite and bolstering the euro.

However, last evening's economic indicators from the U.S. painted a mixed picture, dampening the initial enthusiasm. The ISM Manufacturing Index for June dipped to 48.5 from 48.7, falling short of expectations and remaining below the pivotal 50-point mark that delineates expansion from contraction. Conversely, Markit's Manufacturing PMI indicated a slight improvement, rising to 51.6 from 51.3.

Additionally, a report showed a 0.1% month-on-month decline in U.S. construction spending for May, a reversal from the previous increase of 0.3% and weaker than anticipated, suggesting a potential slowdown in the construction sector and broader economic support.

Market participants are now turning their attention to an upcoming speech by Jerome Powell, Chair of the Federal Reserve, for further clues on the direction of U.S. monetary policy.

Technical analysis of EUR/USD

The EUR/USD pair completed a correction to 1.0774 but is now forming a declining wave towards 1.0675. Should this level be reached, a minor correction to 1.0714 may occur before a potential further drop to 1.0630, and potentially extending down to 1.0573. The MACD indicator underlines this bearish outlook with its signal line positioned below zero and histograms trending downwards.

On the hourly chart, the pair is currently crafting a declining structure with an initial target at 1.0675. Following this, a correction towards 1.0714 is plausible, before a continuation of the downtrend to 1.0640. The Stochastic oscillator corroborates this view, with its signal line approaching the 20 level, indicating a potential for further declines before a rebound towards 50 might occur.

Market outlook

Investors will continue to assess the blend of economic data and central bank signals, particularly from the Fed, to gauge the potential trajectory of interest rates and their impact on currency valuations. Today's speech by Jerome Powell could be particularly pivotal in setting market expectations moving forward.

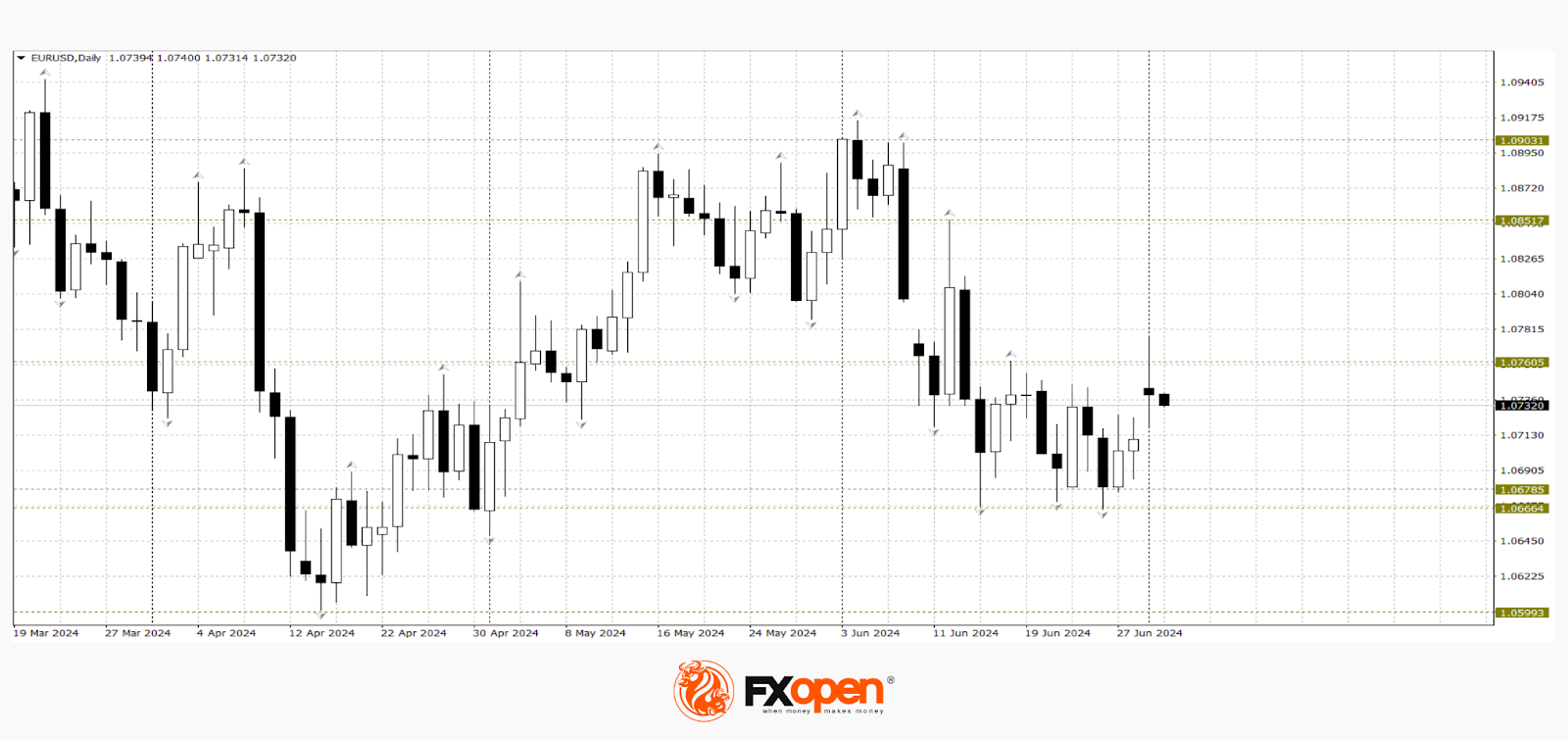

Pound and Euro Test Key Support Levels: Is a Breakout Possible?

European currencies are showing surprising resilience. Despite the general strengthening of the dollar and strong macroeconomic data from the US, EUR/USD and GBP/USD continue to trade above strategically important levels:

- EUR/USD has been testing 1.0660 for over three weeks but cannot establish itself below this level.

- GBP/USD buyers have been holding off sellers for a second week at the 1.2610-1.2600 level.

EUR/USD

The recent parliamentary elections in France, with the first round concluding last Sunday, have contributed to a slight strengthening of the euro. The pair opened with a small price gap and managed to strengthen by over 60 pips within a few hours. Experts attribute the rise in the single European currency to the possibility that Le Pen's far-right party might outpace President Emmanuel Macron's centrist alliance and the left-wing "New People's Front" with fewer votes than needed for an absolute majority after the second and final round of voting.

Technical analysis of the EUR/USD pair indicates continued range-bound trading between 1.0760-1.0660. A breakout and consolidation above 1.0760 could lead to a renewed rise towards 1.0900-1.0850. Breaking the three-week support at 1.0660 could result in a retest of the April low this year at 1.0590.

Events that could impact the pair's pricing include:

- Today at 12:00 (GMT+3): Eurozone core Consumer Price Index (CPI) for June

- Today at 13:30 (GMT+3): Speech by European Central Bank (ECB) representative Elizabeth Schnabel

- Today at 16:30 (GMT+3): Speech by US Federal Reserve Chairman Jerome Powell

GBP/USD

For the second week, the GBP/USD currency pair is trading within a relatively narrow 100-pip range, which is unusual for it. Yesterday, the price surged sharply to 1.2700 but just as sharply fell, closing the day with a candle featuring a long upper shadow, which may indicate weakness among pound buyers. According to technical analysis of the GBP/USD pair, a break below 1.2600 could renew the downward trend towards 1.2560-1.2450. The bearish scenario could be nullified if the price confidently consolidates above 1.2700.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.