Sample Category Title

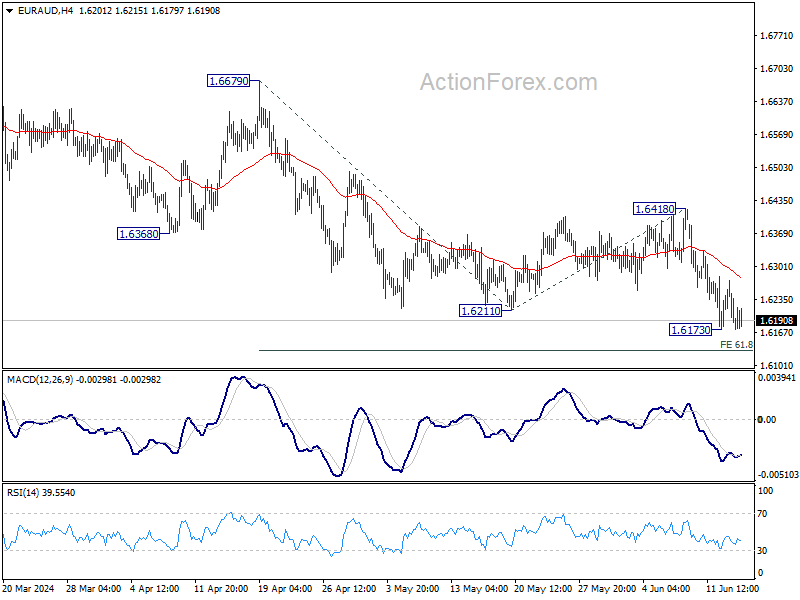

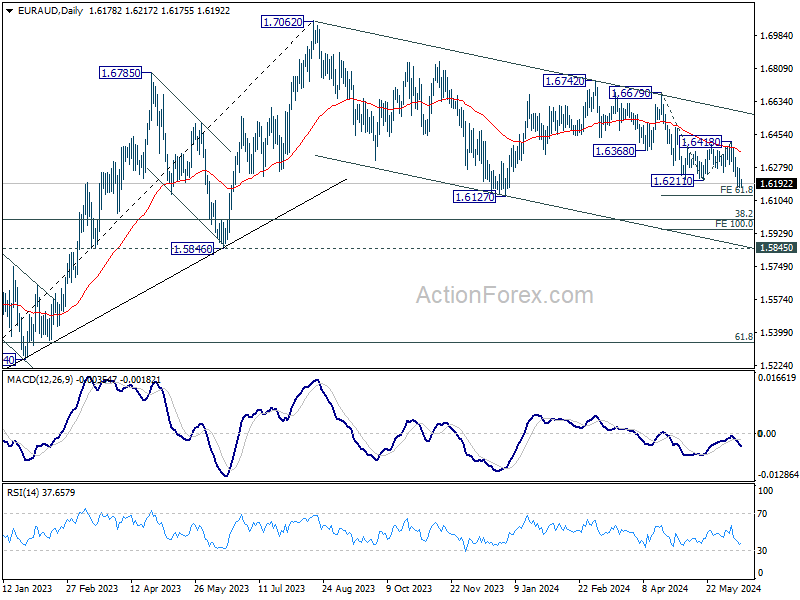

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6146; (P) 1.6210; (R1) 1.6245; More...

Intraday bias in EUR/AUD remains neutral at this point, and outlook stays bearish with 1.6418 resistance intact. On the downside, break of 1.6173 will resume the decline from 1.6742, as the third leg of the correction from 1.7062. Next target is 61.8% projection of 1.6679 to 1.6211 from 1.6418 at 1.6129.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

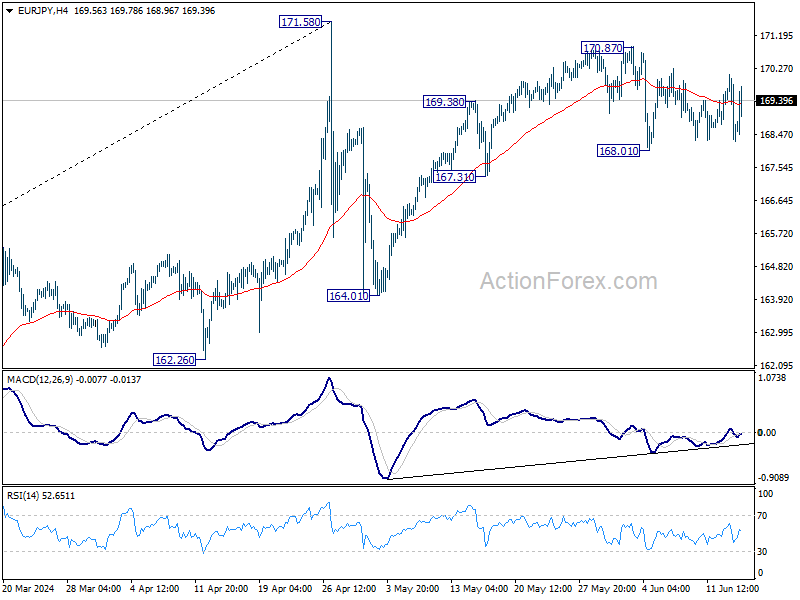

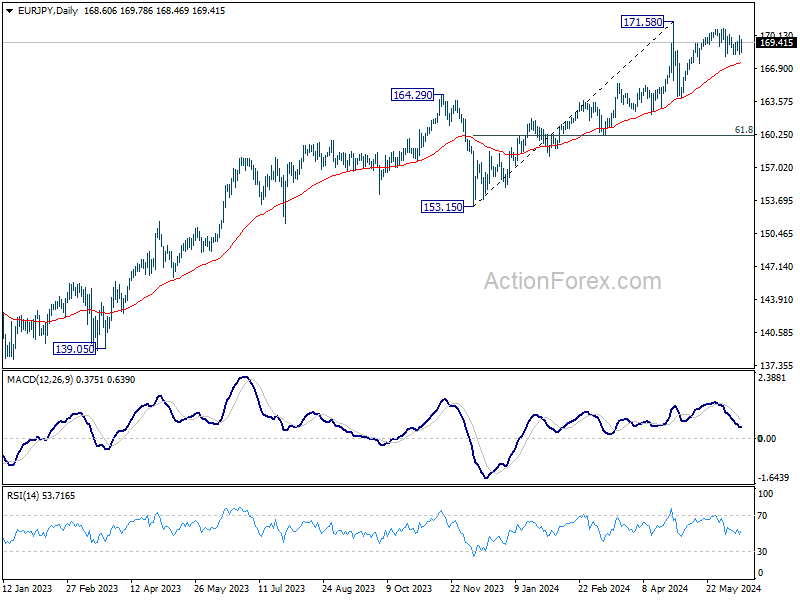

EUR/JPY Daily Outlook

Daily Pivots: (S1) 167.88; (P) 169.01; (R1) 169.74; More...

EUR/JPY is still bounded in sideway trading and intraday bias remains neutral. On the downside, break of 168.01 support will strengthen the case that rise from 164.31 has completed at 170.78 already. Intraday bias will be back on the downside for 167.31 support, and then 164.01. Nevertheless, break of 170.87 will resume the rally to retest 171.58 high instead.

In the bigger picture, a medium top was formed at 171.58 after brief breach of 169.96 (2008 high). But as long as 55 W EMA (now at 159.51) holds, price actions from there is seen as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

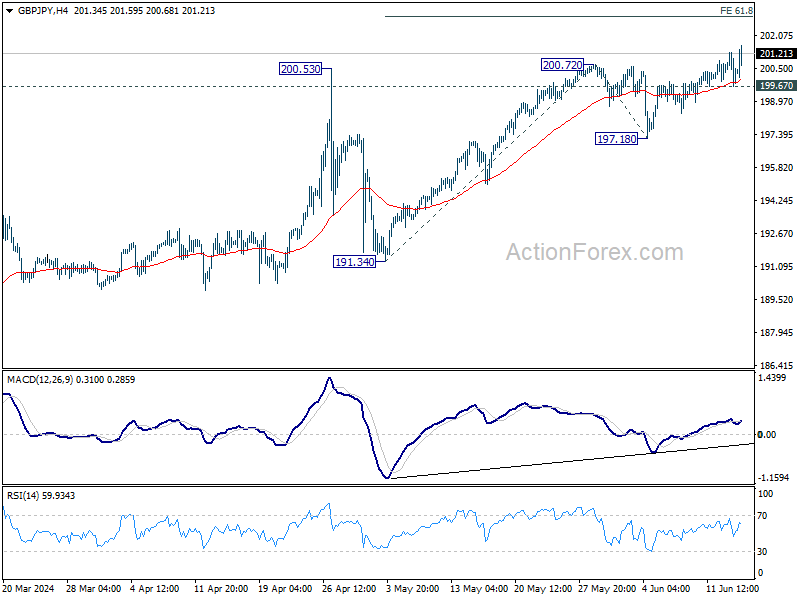

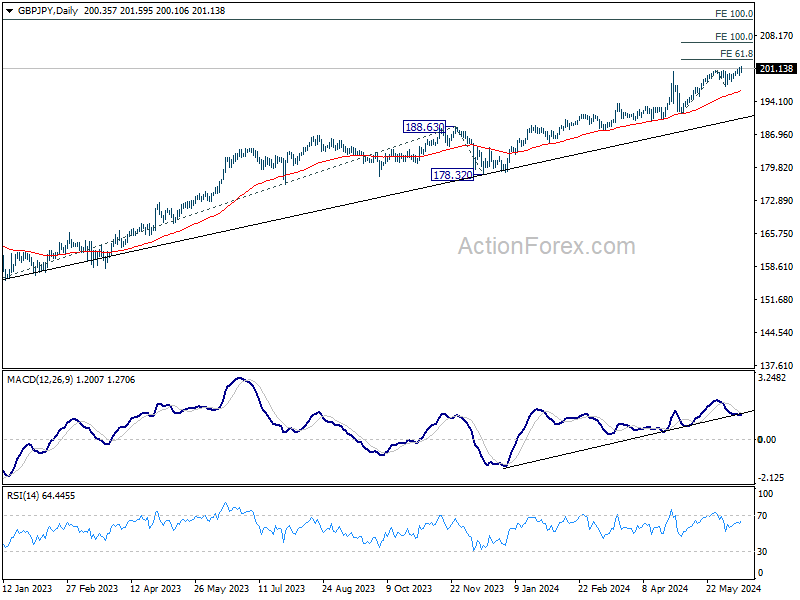

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.62; (P) 200.47; (R1) 201.25; More...

While upside moment isn't too unconvincing, intraday bias in GBP/JPY stays on the upside for now. Current up trend should target Next target is 61.8% projection of 191.34 to 200.72 from 197.18 at 202.97. On the downside, below 199.67 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

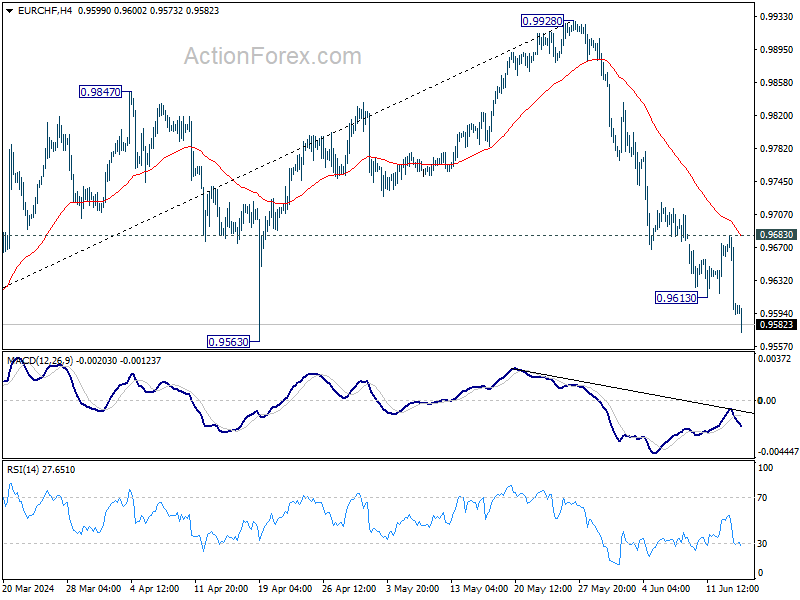

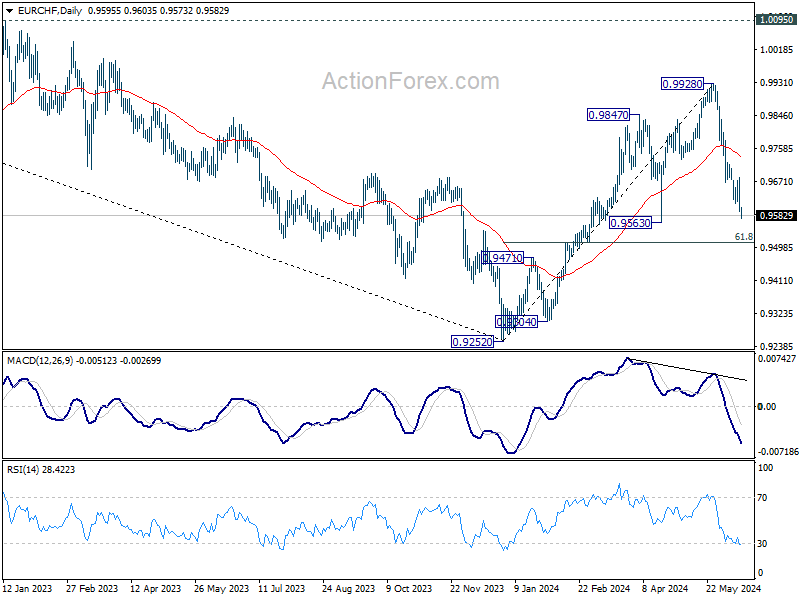

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9568; (P) 0.9626; (R1) 0.9658; More....

EUR/CHF's fall from 0.9928 resumed after brief recovery and intraday bias is back on the downside for 0.9563 support. Decisive break there will argue that whole rise from 0.9252 has completed, and bring deeper fall to 61.8% retracement of 0.9252 to 0.9928 at 0.9510. For now, risk will stay on the downside as long as 0.9683 resistance holds, in case of recovery.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004. However, firm break of 0.9563 will suggest that the rally has completed and retain medium term bearishness.

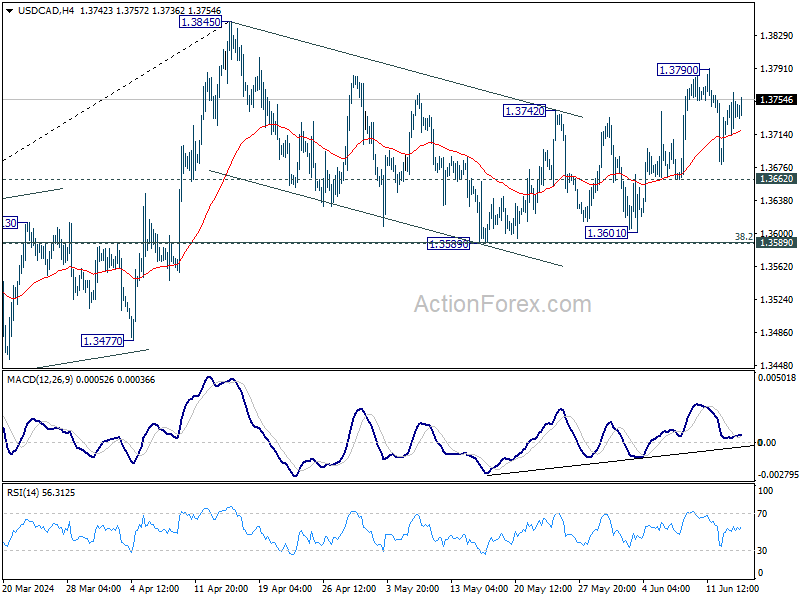

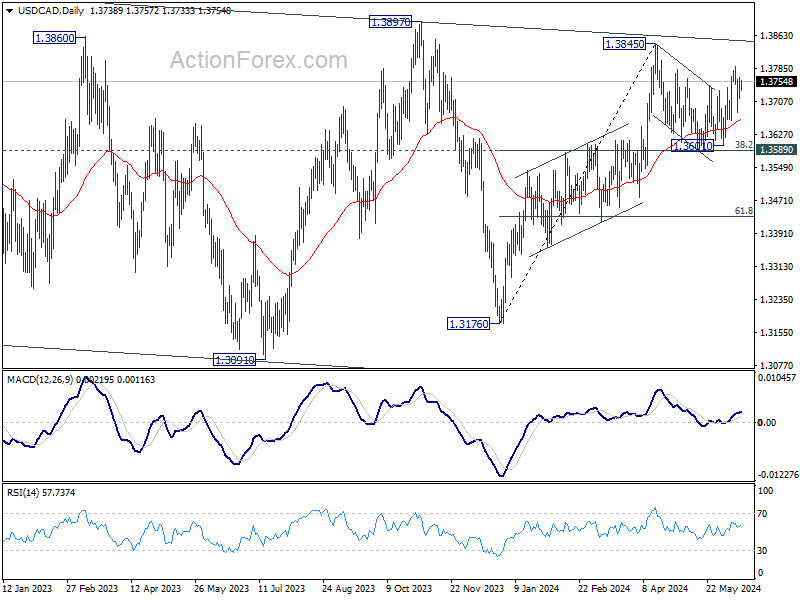

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3711; (P) 1.3738; (R1) 1.3765; More...

Intraday bias in USD/CAD remains neutral and further rise is in favor with 1.3662 support intact. On the upside, above 1.3790 will resume the rebound from 1.3589 to retest 1.3845 high. Firm break there will resume larger rally. Nevertheless, break of 1.3662 will turn bias to the downside to extend the corrective pattern from 1.3845 with another falling leg.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

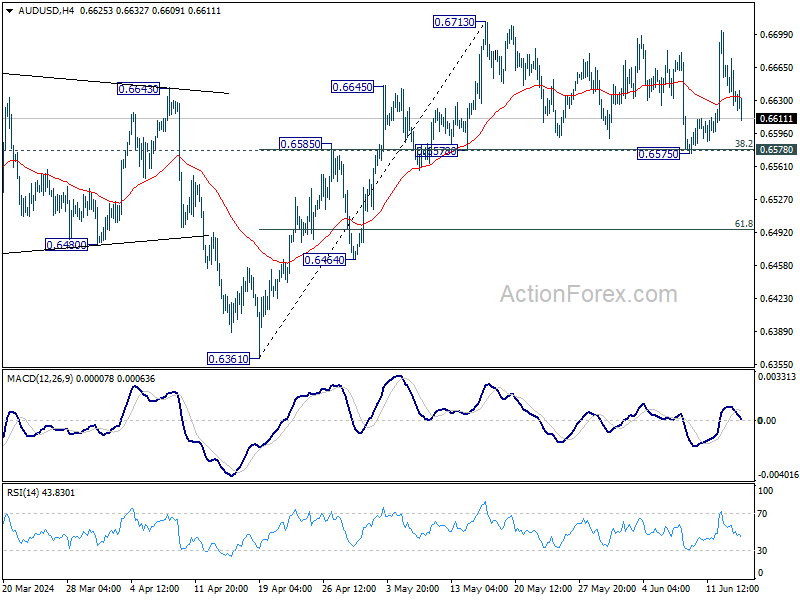

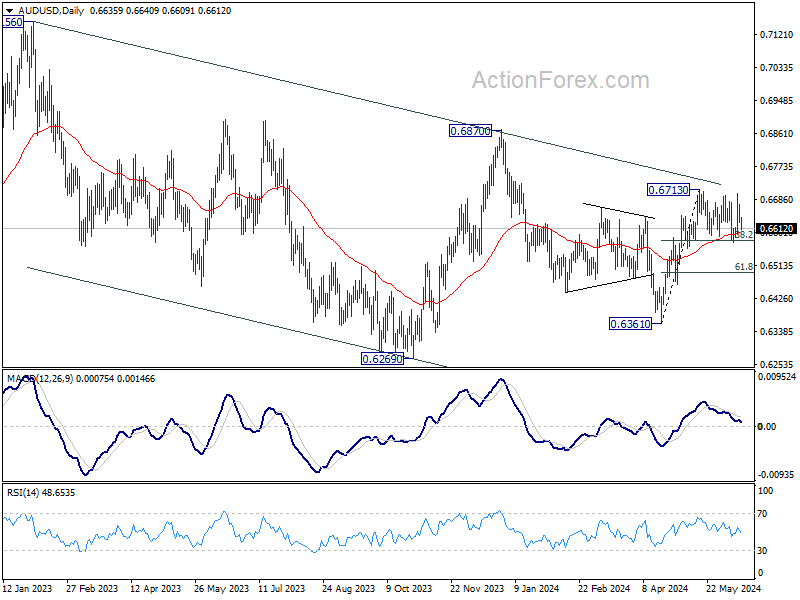

AUD/USD Daily Report

Daily Pivots: (S1) 0.6617; (P) 0.6646; (R1) 0.6666; More...

Intraday bias in AUD/USD remains neutral for the moment as range trading continues. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) will bring deeper fall to 61.8% retracement at 0.6495 instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

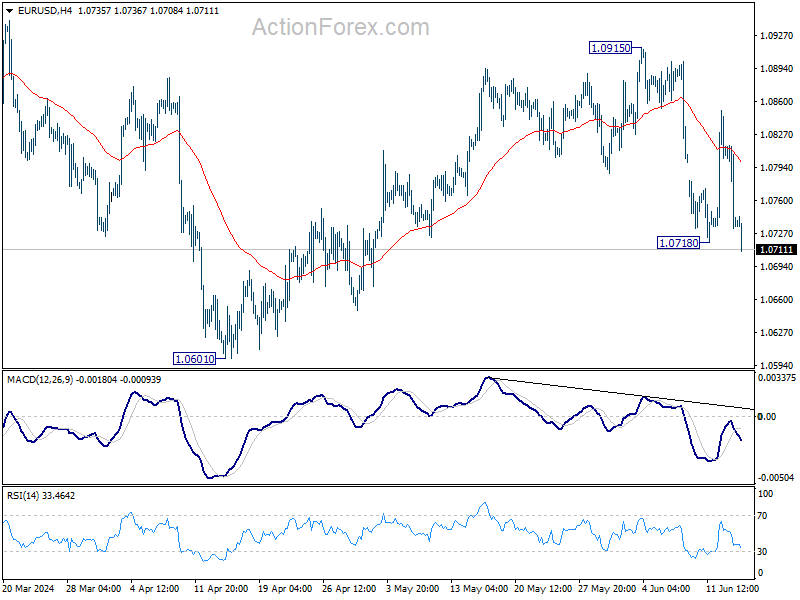

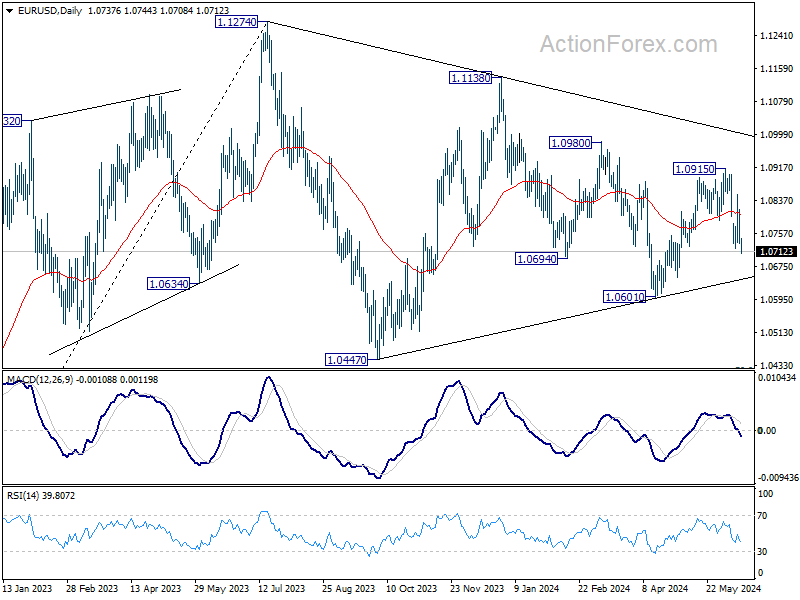

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0709; (P) 1.0763; (R1) 1.0793; More....

EUR/USD's break of 1.0718 support revives that case that rise from 1.0601 has completed at 1.0915. Fall from there is seen as another leg inside the corrective pattern from 1.1274 high. Intraday bias is back on the downside for 1.0601 support first. Firm break there will target 1.0447 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, which might still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. Nevertheless, on the upside, firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high.

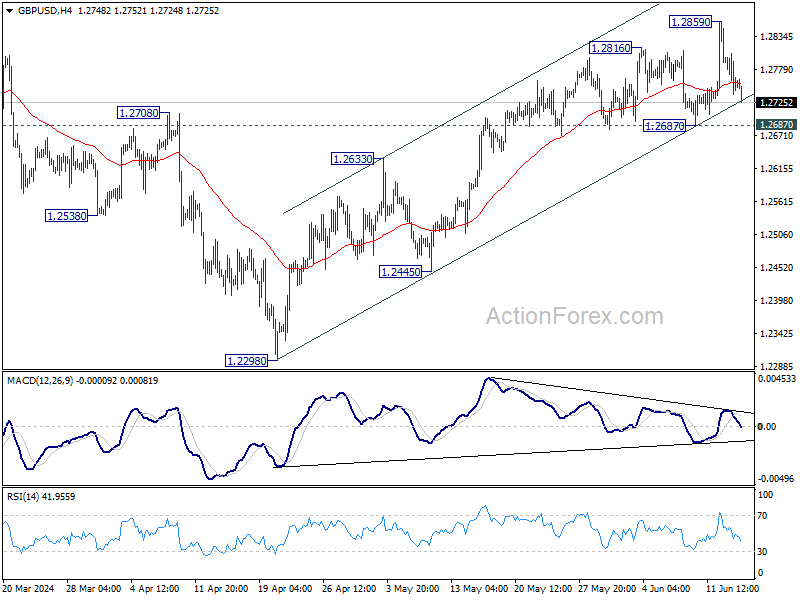

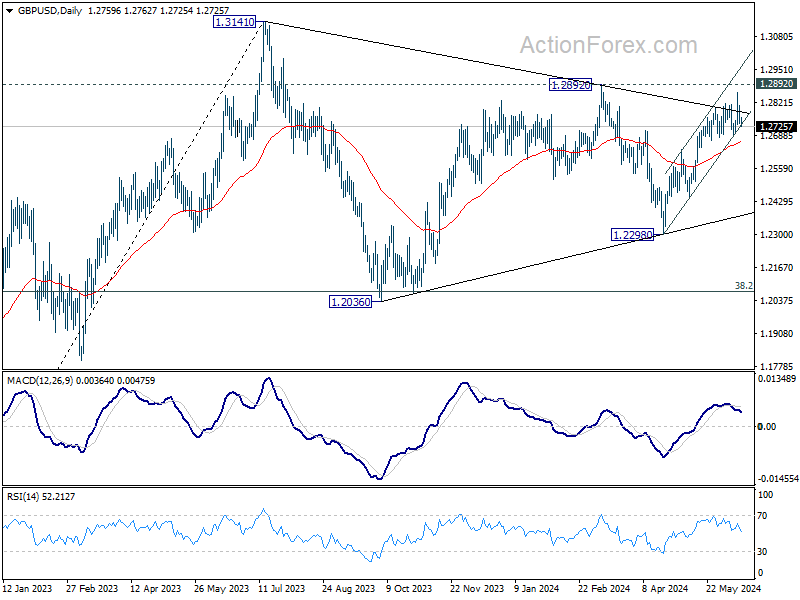

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2732; (P) 1.2770; (R1) 1.2802; More...

Intraday bias in GBP/USD remains neutral at this point. Further is expected with 1.2687 support intact. Break of 1.2859 will target 1.2892 resistance. Decisive break there will strengthen the case that correction from 1.3141 has completed, and bring further rally to retest this high. However, firm break of 1.2687 will suggest near term reversal, and turn bias back to the downside for 1.2445/2633 support one instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

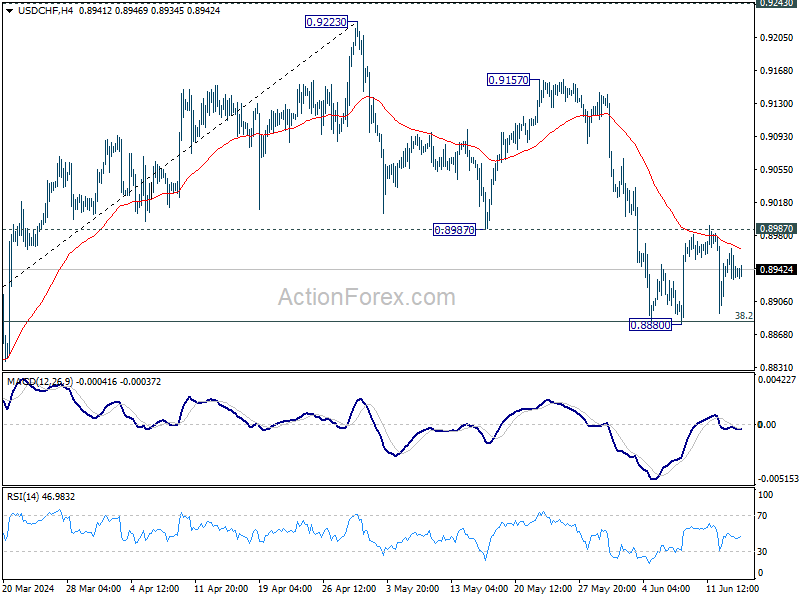

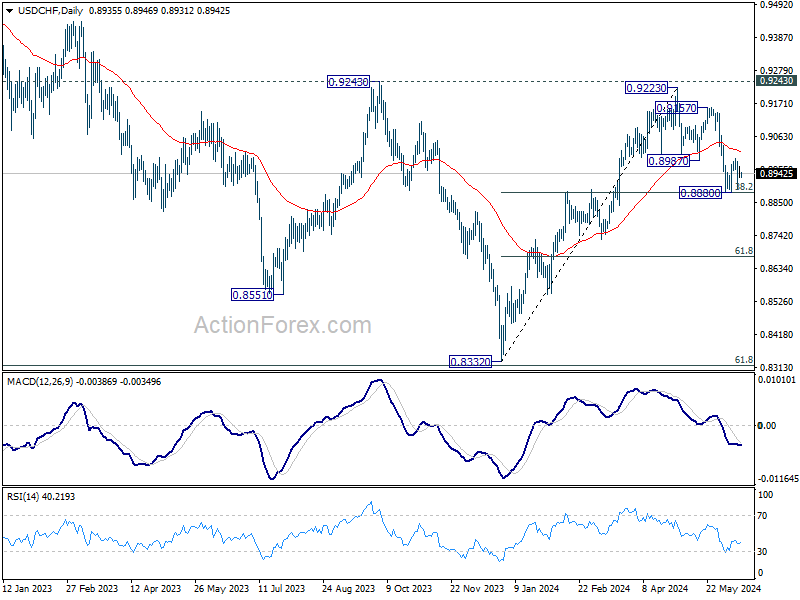

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8921; (P) 0.8945; (R1) 0.8962; More….

Intraday bias in USD/CHF remains neutral for the moment and more sideway trading could be seen. On the downside, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

USD/JPY Nearing April JPY-Intervention Levels in Wake of BoJ

Markets

Core bond yields stumbled yesterday. US yields dropped between 5.5 (2-yr) and 7.8 bps (30-yr) on a combination of slower than expected PPI numbers (negative even in the headline reading), a jump in weekly jobless claims to the highest in nine months (242k) and a $22bn 30-yr auction that stopped through (4.403% vs 4.418% WI) and attracted solid investor demand. The US 2-yr tested the post-Fed low but prevented a break/close below for the time being. The 10-yr hit the lower bound of a downward sloping trend channel in place since end April. German yields slipped 4.7 (30-yr) to 8.2 (2-yr) bps. The move was inspired by the US as well as the result of lingering European/French political uncertainty with another round of disastrous polls for Macron’s group hitting the wires. The French president reiterated he plans to stay in power until 2027. But it appears that the more he does so, the less markets believe him. The 10-yr OAT/swapspread jumped to the highest level since early 2014 and is trading a mere 2 bps below Portugal’s. European stock markets tanked about 2%, contrasting with the S&P500 and Nasdaq in the US extending their record run. The euro didn’t escape the sharp European repricing and slid from EUR/USD 1.0809 at the open to 1.0737. The common currency hit a new YtD low against sterling with EUR/GBP closing at 0.8413, the weakest level since August 2022. The Swiss franc banked on its safe haven status. EUR/CHF eased to 0.959 as a weak euro is now taking over from/complementing a SNB-powered CHF. USD/JPY finished only slightly higher yesterday as both a strong US dollar and JPY against the risk-off background kept each other in check. That changed this morning though with the pair nearing the April JPY-intervention levels in the wake of the BoJ policy meeting (cfr. infra). The remaining eco calendar contains US consumer sentiment (Michigan University), which is unlikely to leave a material mark on markets. US bond yields currently recover some ground by adding less than 3 bps across the curve. We continue to err on the side of caution going into the weekend though, especially for Europe. Reports of the 2025 budget stand-off pushing the German government to the brink are obviously not helping in the current environment. The ruling coalition also got a beating in the European elections while the far-right gained. The vote is seen as a gauge for next year’s federal elections in Germany. In case of renewed risk aversion, first support in the German 10-yr yield pops up at 2.4%. If EUR/USD 1.0695/1.0712 breaks, there’s little in the way for a return towards 1.06.

News & Views

The Bank of Japan kept its policy target range unchanged at 0%-0.1% this morning as expected. The central bank will continue conducting bond purchases as set out on March until the next, July, meeting. The BoJ also decided in a 8-1 majority vote that it would reduce its purchase amount of JGB’s to ensure that long-term interest rates would be formed more freely in financial markets. At the July meeting, a detailed taper plan will be communicated. In order not to shock markets, the process will last one to two years. Japan’s economy is likely to keep growing at a pace above its potential growth rate. Simultaneously, the year-on-year rate of increase in the CPI is projected to be pushed up through fiscal 2025 by factors such as a waning of the effects of fiscal measures. Underlying CPI is expected to gradually increase as the output gap improves and medium- to long-term inflation expectations rise with a virtuous cycle between wages and prices continuing to intensify. BoJ governor Ueda will still hold a press conference at 8:30 am CET. The Japanese yen already faces renewed selling pressure because of the ultra-cautious policy normalization process of the BoJ. USD/JPY hits 158 for the first time since end-of-April FX interventions.

Czech National Bank governor Michl in a speech yesterday set out his strategy for the next CNB meetings. The debate at the next meeting at the end of June will probably be about whether to cut by 50 or by 25 bps (currently 5.25%). Both options are open, and in both cases, the CNB will still be in restrictive territory. Then they will be very cautious about further rate cuts. They will assess new data at each meeting and decide accordingly. The rate cutting process can be paused or stopped at any time if inflation, especially core inflation, is not in line with their forecast. The CNB will stay hawkish and do everything in its power to achieve long-term price stability and not trigger inflation. The closer they get to neutral (current estimate 3%-3.5%), the more likely that they’ll slow down or even interrupt policy normalization.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. For the time being, though, the political narrative dominates. After hitting a new YtD top at 2.7%, the German 10-yr yield corrected lower on safe haven bids.

US 10y yield

The Fed is seeking more evidence than just one slower-than-expected (May) CPI is providing. Upgraded inflation forecasts and a higher neutral rate complicate the exact timing of a first cut further. June dots suggest one move in 2024 followed by four more next year. Markets are positioned more aggressively, turning the recent low in yields into a technical support zone. The US 10-y yield remains stuck in the 4.3/4.7% trading range.

EUR/USD

EUR/USD is trapped in the 1.06-1.09 range. The desynchronized rate cut cycle with the ECB exceptionally taking the lead, strong US May payrolls and a swing to the right in European elections pulled the pair away from 1.09 resistance. The Fed meeting balanced the weaker than expected US CPI outcome. Euro fragility makes a return to the 1.06 downside more likely than not.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Slower than expected April disinflation and a surprise general election on July 4 suggest that a June cut in line with the ECB looks improbable. Sterling gained momentum with money markets now discounting a Fed-like scenario. EUR/GBP tested the 2023 & 2024 lows near 0.85. Euro weakness eventually pulled the trick after French president Macron called snap elections following a weak showing in EU elections.