Sample Category Title

Euro Area and US PMIs Surprise to the Upside

In focus today

From the US, April durable goods orders and revised May Michigan consumer sentiment survey are due for release. The flash release showed consumers' inflation expectations ticking notably higher, but the recent decline in retail gasoline prices could mean that expected inflation has also moved lower. The Fed's Waller (voter) will be on the wires in the afternoon, his views have often reflected broader consensus among the FOMC participants.

Swedish PPI for the month of April is published today. In March, the import price index's seasonally adjusted three-month rate turned positive again (albeit very mildly). Sweden therefore no longer import deflation at the producer level. Meanwhile, the Riksbank is currently (23-24/5) hosting a high-level academic conference on inflation targeting, with speakers such as Olivier Blanchard and Mervyn King on today's agenda. The conference can be streamed via the following link.

Economic and market news

What happened overnight

In Japan, inflation slowed further in April, with headline CPI in at 2.5% y/y (prior: 2.7%) and core inflation at 2.2% (cons: 2.2%, prior: 2.6%), in line with consensus expectations. This will make the Bank of Japan (BoJ) more cautious about future rate hikes. However, we still await the effects from the wage hikes at 5.25%, which Japanese firms agreed to earlier this spring.

What happened yesterday

Euro area PMI rose slightly more than expected in May to 52.3 (cons: 52.0, prior: 51.7). Services PMI was unchanged at 53.3 in contrast to expectation of a rise (cons: 53.6, prior: 53.3) while manufacturing PMI rose more than expected to 47.4 (cons: 46.1, prior: 45.7). With the composite PMI above 50 for three consecutive months the momentum is gathering in the euro area economy. The increase in manufacturing PMIs was driven especially by rising new orders. Most importantly, the service sector price index ticked down in both output and inputs costs, meaning it is at the lowest level in three years, but still above the historical average. This is good news for the ECB, but risks nevertheless persist as the employment index continued to rise in May and activity is gathering momentum.

Euro area wage growth picked up in Q1 rising to 4.69% y/y from 4.49% in Q4. Hence, the wage pressure in the euro area economy is still substantial. This leaves upside risks to the inflation outlook especially on services inflation due to a relatively larger role of wages. Especially domestically driven services inflation has been a key concern for the ECB lately in their communication. With high wage growth the upside risks to inflation thereby persists as the labour market is also tight.

In the US, flash PMIs surprised to the upside as well, driven especially by stronger services activity. Composite index remains firmly in 'growth territory'. Output price indices (key measures of inflation pressure) remain mostly unchanged, services 54.0 (from 53.7) and manufacturing 54.5 (from 54.7) - close to long-term averages.

In the UK, preliminary PMIs surprised to the downside. Manufacturing measure rose into expansionary territory at 51.3 (from 49.1) as the manufacturing sector continues to recover. Services and the composite measure remain above 50 but drop to 52.9 (from 54.7) and 52.8 (from 54.0) respectively. Businesses reported the softest increase in average selling prices for over three years and private sector firms continue to increase prices at a slower rate. Overall, good news for the BoE on track for a summer cut with growth pick-up up after a technical recession in H2 and survey signals point to price pressures easing.

The Central Bank of Turkey kept its policy rate unchanged at 50% as widely expected. The monetary policy statement was also broadly unchanged. The committee continues to highlight that the tight monetary stance will be maintained until a significant and sustained decline in the underlying trend of monthly inflation is observed, and inflation expectations converge to the projected forecast range. The central bank expects disinflation will be established in the second half of 2024.

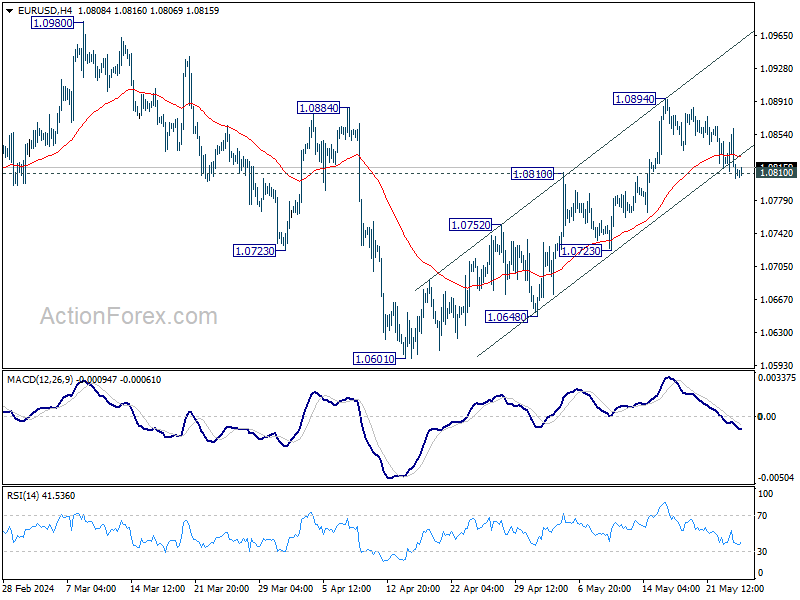

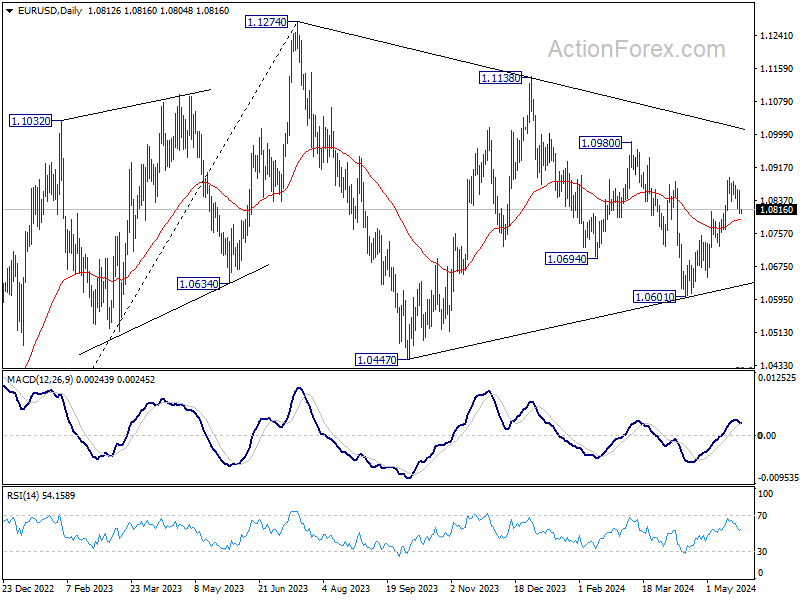

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0794; (P) 1.0827; (R1) 1.0850; More...

Intraday bias in EUR/USD remains neutral for the moment. On the upside, break of 1.0894 will resume the rise from 1.0601 to 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed at 1.0601 already. However, firm break of 1.0810 will dampen this bullish case, and turn bias back to the downside for 1.0723 support.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

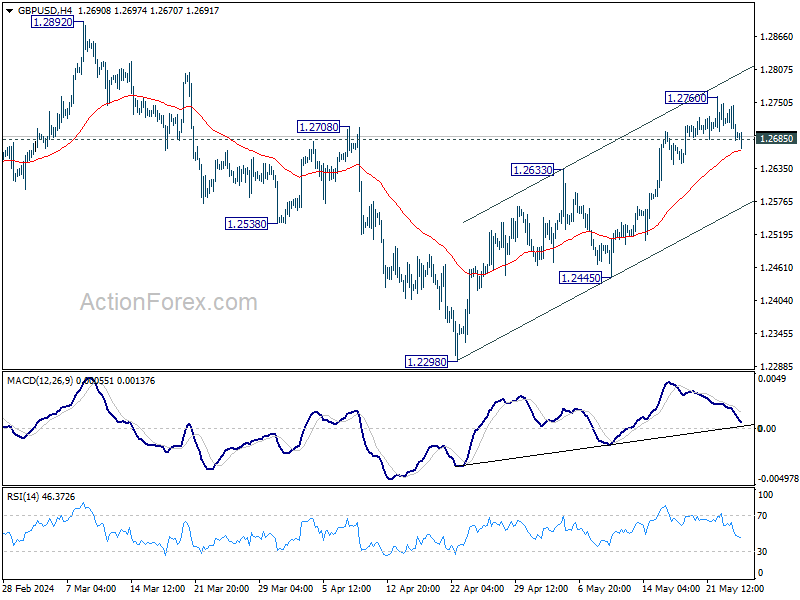

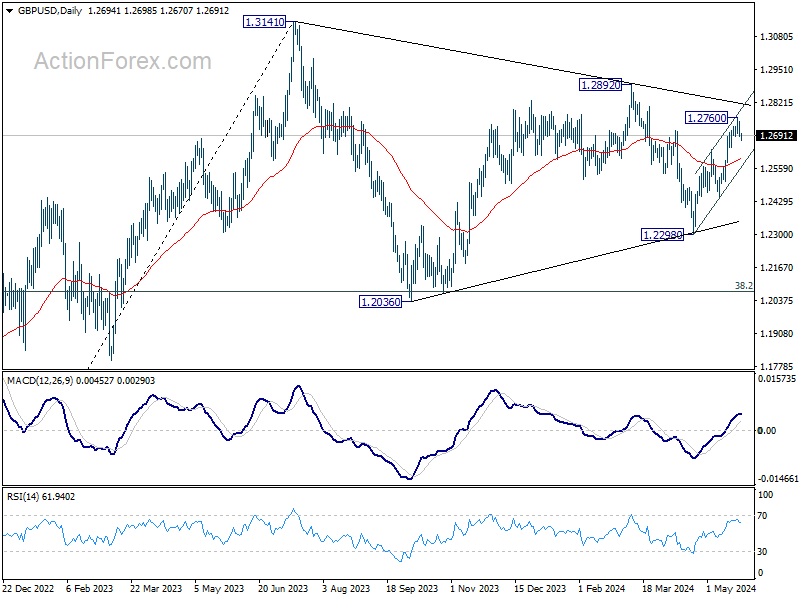

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2674; (P) 1.2710; (R1) 1.2736; More...

Breach of 1.2685 minor support suggests short term topping at 1.2760 already. Intraday bias is mildly on the downside. Firm break of 55 4H EMA (now at 1.2661) will target near term channel support (now at 1.2563). On the upside, break of 1.2760 will resume the rebound from 1.2298 towards 1.2892 resistance.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351 (2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

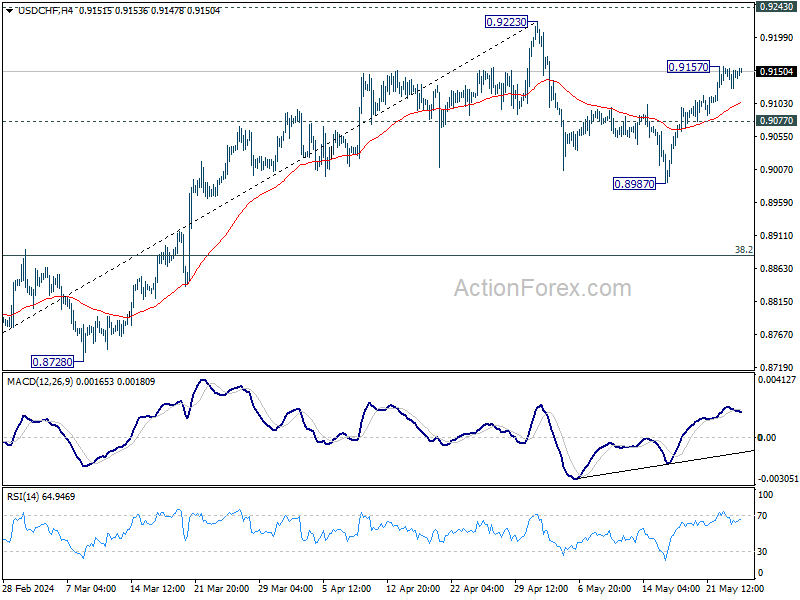

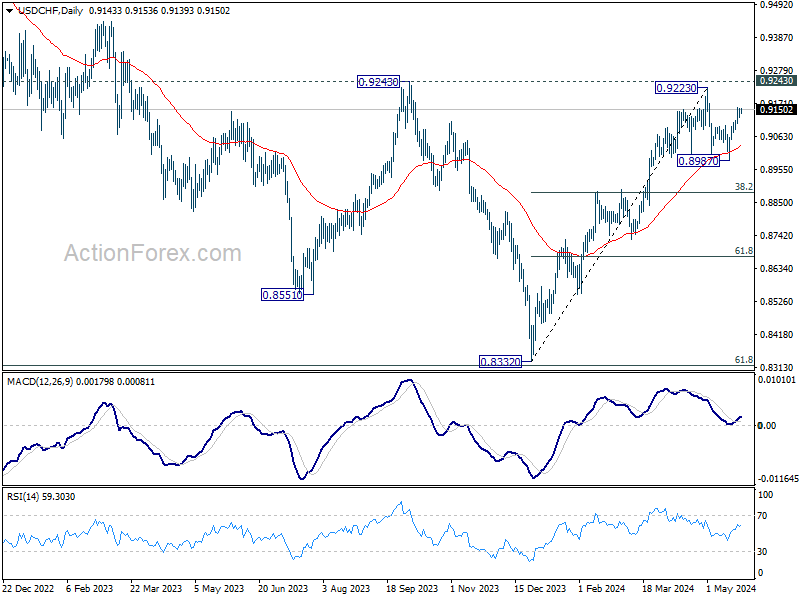

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9128; (P) 0.9143; (R1) 0.9160; More....

Intraday bias in USD/CHF remains neutral first and further rise is in favor with 0.9077 minor support intact. On the upside, above 0.9157 will resume the rebound from 0.8987 to retest 0.9223 high. On the downside, break of 0.9077 support will bring retest of 0.8987. Break there will resume the fall from 0.9223 to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

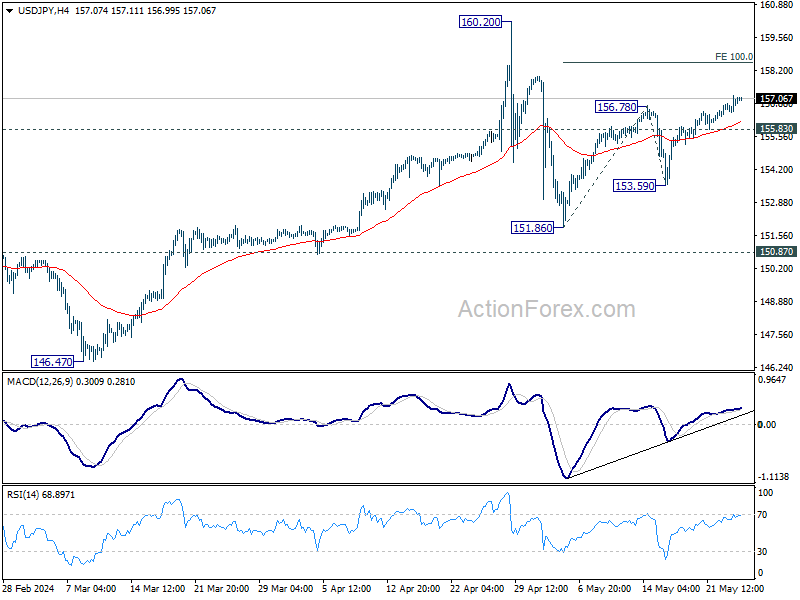

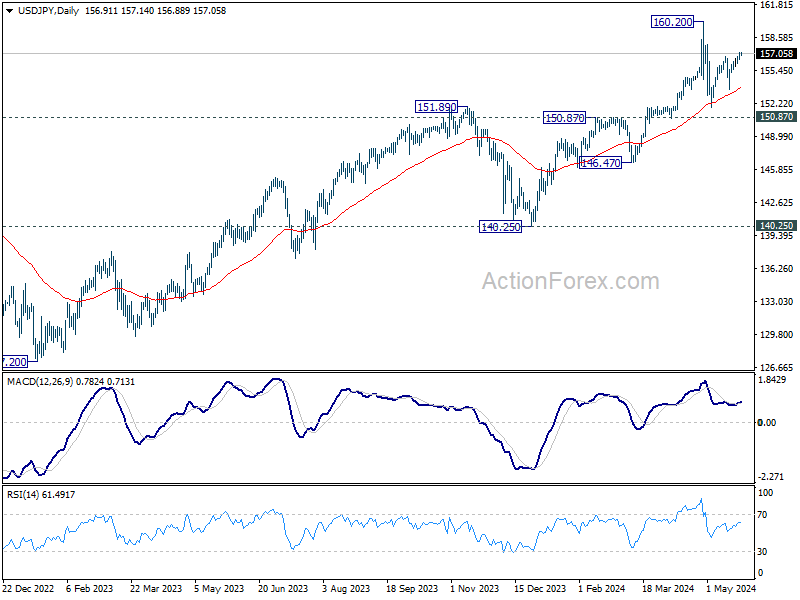

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.55; (P) 156.92; (R1) 157.30; More...

Intraday bias in USD/JPY is back on the upside with break of 156.78 resistance. Rise from 161.86, as the second leg of the corrective pattern from 160.20, should now target 100% projection of 151.86 to 156.78 from 153.59 at 158.51. On the downside, below 155.83 minor support will turn intraday bias neutral first. Further break of 153.69 will target 151.86 and below as the third leg.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

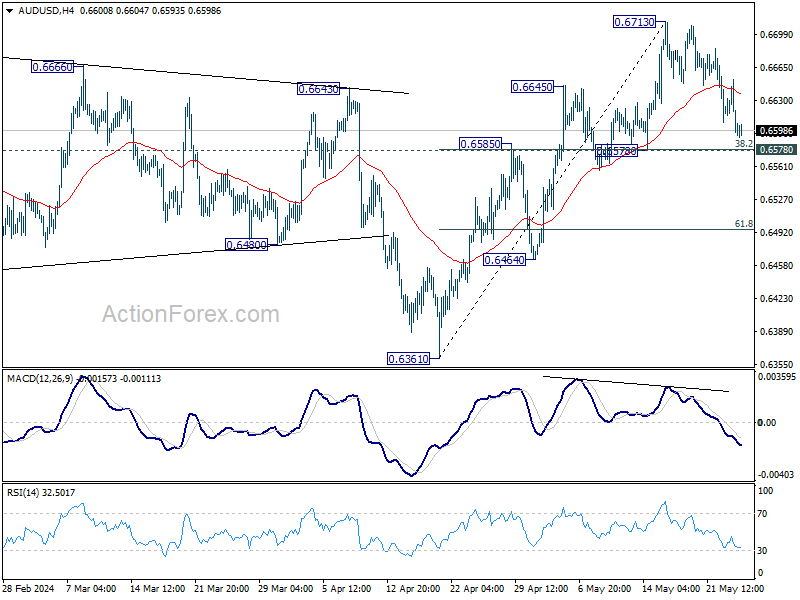

AUD/USD Daily Report

Daily Pivots: (S1) 0.6586; (P) 0.6619; (R1) 0.6641; More...

While AUD/USD's retreat from 0.6713 extends lower, it's staying above 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579. Intraday bias remains neutral for the moment, and further rally is in favor. As noted before, fall from 0.6870 has probably completed with three waves down to 0.6361 already. Above 0.6713 will target 0.6870 resistance next. However, firm break of 0.6578 will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Waning Reflation Appetite?

The week hasn’t been pleasant for the market bulls. On Wednesday, the FOMC minutes showed the disturbing truth that ‘many’ Fed members wondered whether keeping the rates ‘high for longer’ was sufficiently restrictive to tame inflation, and if hiking the rates wouldn’t be a better idea. Then, the UK PM Sunak announced a general election beginning of July – way earlier than many expected – abating the slightest glimmer of hope to see the Bank of England (BoE) cut its rates in June. Meanwhile, the latest British CPI data came in hotter-than-expected, anyway, warning that the policy easing wouldn’t necessarily be on the pipeline for June. Across the Channel, the data released this week showed that wage growth in the euro area increased 4.7% in Q1 – a red flag for officials who have been banking on a slowdown to keep inflation in check. And finally, a set of too-strong-to-be-pleasant data from the US gave a final punch to the bulls. The US services PMI accelerated way faster than expected in May, according to the S&P’s preliminary PMI data, manufacturing activity also improved, while jobless claims came in soft. The US 2-year yield – which captures the rate expectations – advanced to 4.95%, the 10-year gilt yield reached 4.25%, the 10-year Bund yield hit 2.60%, the S&P500 and Nasdaq sold off from a record, the Stoxx 600 managed to eke out a small gain, but the FTSE 100 is down by more than 1.50% since last week’s peak, hit by a decent decline in energy prices as well.

Waning reflation appetite?

US crude extended losses below the 100-DMA for a third session, and is set for a further fall toward the $75pb level. Copper futures gave back almost 10% since the Monday peak and gold lost more than $100 per ounce since Monday record. If the reflation trade loses momentum due to a hawkish shift in major central bank expectations, we shall see a period of pullback and profit-taking in risk assets, and a further dollar appreciation against major counterparts.

The US dollar index strengthened past the 50-DMA following the hawkish Federal Reserve (Fed) minutes and yesterday’s strong economic data, the EURUSD slipped below its 100-DMA and is preparing to test the 1.08 support. Cable eased below 1.27 and could reasonably expected to extend losses on the back of fading appetite before the general election, while the USDJPY is now back above 157. Inflation data out this morning showed a slowdown in core CPI to 2.2%, ruling out any sense of emergency for the BoJ to continue hiking the rates. And the AUDUSD tipped a toe below the 66 cents mark this morning and could lose the latest positive momentum if the pair slips below 0.6580, the major 38.2% Fibonacci retracement on the latest rebound.

Clear skies

Nvidia remains a well-sheltered harbor from the rising hawkish winds. Nvidia jumped more than 9% after beating revenue expectations for Q1 and exceeding the forecast for the current quarter. Nvidia is catapulted to the overbought market territory following yesterday’s rally, but nothing suggests that the company’s good fortunes, or demand for AI, are about to reverse. Therefore, there is a good chance that the $1000 per share level becomes the new dip for those who are willing to jump on the back of a bull.

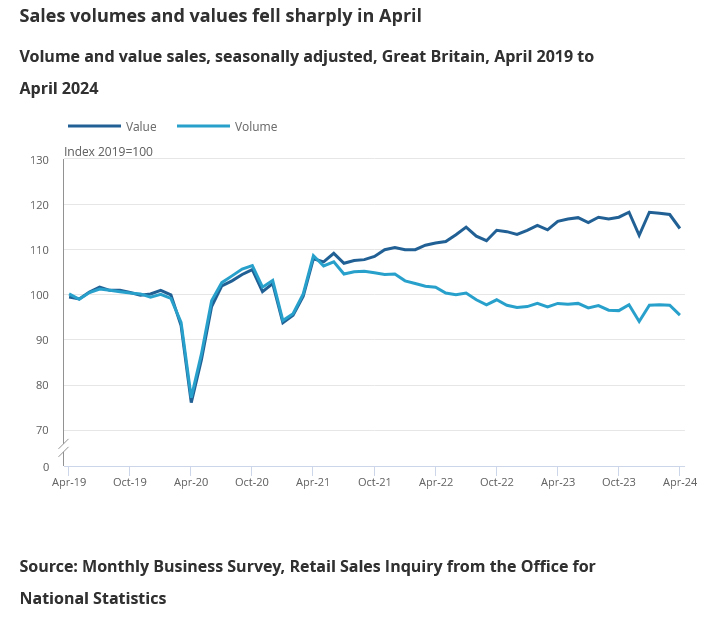

UK retail sales falls -2.3% mom in Apr, vs exp -0.6% mom

UK retail sales volume fell sharply by -2.3% mom in April, much worse than expectation of -0.6% mom. Sales volumes fell across most sectors, with clothing retailers, sports equipment, games and toys stores, and furniture stores doing badly as poor weather reduced footfall. More broadly, sales volumes rose by 0.7% in the three months to April 2024 when compared with the previous three months

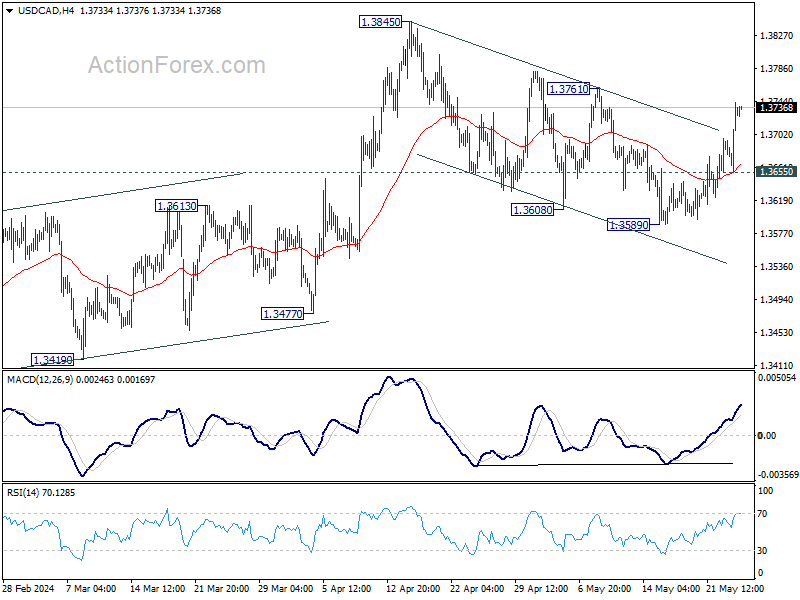

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3676; (P) 1.3710; (R1) 1.3763; More...

USD/CAD's rebound from 1.3589 extended higher today. The development indicates that correction from 1.3845 has completed with three waves down to 1.3589. Intraday bias is back on the upside for 1.3761 resistance first. Break there will bring retest of 1.3845 high. On the downside, below 1.3655 minor support will dampen this bullish case and turn intraday bias neutral again first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Dollar Gains Momentum as Fed Hike Re-Enters Markets Pricing, Despite Ultra Low Odds

Dollar's rebound is gathering momentum, as fueled by yesterday's data indicating a resurgence in the services sector, which could impede disinflation progress. While fed fund futures still reflect over 50% probability of a rate cut in September, there is now a 0.6% chance of a rate hike—an occurrence not seen for quite some time. Currently, the Dollar is the week's strongest performer, with the upcoming durable goods orders report likely to influence its next move.

Sterling follows as the second strongest currency this week, supported by higher-than-expected inflation data, which quashed hopes for a June rate cut by BoE. The focus now shifts to the upcoming UK retail sales data for further direction. Euro is also performing well as the third strongest, bolstered by strong Eurozone PMI data.

In contrast, Australian Dollar is the worst performer this week, dragged down by pullback in global risk sentiment. Yen is the second weakest, followed by New Zealand Dollar. Swiss Franc and Canadian Dollar are positioned in the middle.

Technically, EUR/GBP remains a major focus for the rest of the week. It's now eyeing 0.8491/97 support zone. Decisive break there will confirm resumption of whole down trend from 0.9267 (2022 high). Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

In Asia, at the time of writing, Nikkei is down -0.97%. Hong Kong HSI is down -1.24%. China Shanghai SSE is down -0.35%. Singapore Strait Times is down -0.37%. Japan 10-year JGB yield is up 0.006 at 1.009. Overnight, DOW fell -1.53%. S&P 500 fell -0.74%. NASDAQ fell -0.39%. 10-year yield rose 0.041 to 4.475.

Japan's core CPI eases to 2.2% in Apr, marking second month of slowdown

Japan's CPI core, which excludes food, decelerated from 2.6% yoy to 2.2% yoy in April. This aligns with market expectations and marks the second consecutive month of decline from February's 2.8%. Despite the slowdown, core inflation has remained at or above BoJ's 2% target for the 25th straight month.

CPI core-core, which strips out both food and energy costs, also showed signs of easing, slowing from 2.9% yoy to 2.4% yoy. This is the slowest pace of increase since September 2022. Meanwhile, headline CPI, which includes all items, fell from 2.7% yoy to 2.5% yoy.

A closer look at the major components reveals varied trends. Food prices rose by 3.5% yoy, but this was a moderation from 4.6% yoy increase seen in March. The surge in accommodation fees, up 18.8% yoy, was driven by a revival in inbound tourism. Energy prices edged up slightly by 0.1% yoy, with increases in kerosene and gasoline prices leading the way. Service prices also showed a deceleration, rising by 1.7% yoy compared to 2.1% yoy increase in the previous month.

RBNZ stresses vigilance on inflation, prepared to raise rates if necessary

In an interview today, RBNZ Assistant Governor Karen Silk highlighted the central bank's readiness emphasized that there are "risks still to the upside in the near term" regarding inflation. She stated that RBNZ is "absolutely" prepared to raise interest rates if necessary, adding, "Right now we are saying that the level of restrictiveness is there, but we are awake at the wheel."

Silk pointed out that the central bank's primary concern is domestic inflation, particularly noting the significant miss last quarter when non-tradables inflation hit 5.8%, compared to RBNZ's forecast of 5.3%. "Our concern is in that near term, around what are we really seeing in terms of domestic aligned inflation," she explained.

Separately, Deputy Governor Christian Hawkesby reinforced the cautious stance, stating that "cutting interest rates is not part of near-term discussion." He acknowledged the near-term inflation risks are to the upside but expressed confidence that medium-term inflation is returning to target.

Hawkesby emphasized that no single data point will trigger a rate hike, but the bank is closely watching domestic inflation pressures and expectations. He also noted the significant uncertainty surrounding tradable inflation moving forward.

RBNZ's central projection is for headline inflation to fall back into its 1-3% target band by the fourth quarter of this year. However, the bank now projects that it won't achieve its 2% goal until mid-2026.

New Zealand's exports falls -2.6% yoy in Apr, imports down -0.7% yoy

In April, New Zealand's goods exports fell by -2.6% yoy to NZD 6.4B, while goods imports decreased by -0.7% yoy to NZD 6.3B. Contrary to expectations of a NZD -202m deficit, trade balance recorded a surplus of NZD 92m.

Examining the top monthly export movements by country, exports to China decreased by NZD -206m (-11% yoy), and exports to Australia fell by NZD -17m (2.4% yoy). In contrast, exports to the US increased by NZD 35m (4.9% yoy), exports to EU rose by NZD 62m (13% yoy), and exports to Japan surged by NZD 91m (26% yoy).

On the import side, imports from China increased by NZD 120m (10% yoy), and imports from South Korea soared by NZD 371m (119% yoy). However, imports from the EU decreased by NZD -79m (-8.1% yoy), and imports from the US dropped by NZD -154m (24% yoy). Imports from Australia grew modestly by NZD 9.8m (1.4% yoy).

Fed's Bostic: Inflation not yet at safe point for rate cuts

Atlanta Fed President Raphael Bostic emphasized caution regarding interest rate cuts, stating that the US economy is not yet past the "worry point" for inflation to return to the target of 2%.

Speaking at an event overnight, Bostic highlighted the robustness of job growth, describing it as "a lot of energy in the economy." This robust job growth gives him confidence in maintaining a "more restrictive level" of monetary policy, as he doesn't believe there's a risk of "falling into a contractionary environment."

Bostic also mentioned the need to be "a little more patient" and ensure inflation is on a clear path to 2% before considering rate cuts.

He underscored the importance of moving in "one direction only" to avoid the uncertainty that would come from cutting rates only to raise them again. This approach, he believes, would prevent creating "policy uncertainty."

Looking ahead

UK retail sales and Germany GDP final are the focuses in European session. Later in the day, Canada will release retail sales. US will publish durable goods orders.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3676; (P) 1.3710; (R1) 1.3763; More...

USD/CAD's rebound from 1.3589 extended higher today. The development indicates that correction from 1.3845 has completed with three waves down to 1.3589. Intraday bias is back on the upside for 1.3761 resistance first. Break there will bring retest of 1.3845 high. On the downside, below 1.3655 minor support will dampen this bullish case and turn intraday bias neutral again first.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Apr | 91M | -202M | 588M | 476M |

| 23:01 | GBP | GfK Consumer Confidence May | -17 | -18 | -19 | |

| 23:30 | JPY | National CPI Y/Y Apr | 2.50% | 2.70% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Apr | 2.20% | 2.20% | 2.60% | |

| 23:30 | JPY | National CPI ex Food & Energy Y/Y Apr | 2.40% | 2.90% | ||

| 06:00 | GBP | Retail Sales M/M Apr | -0.60% | 0.00% | ||

| 06:00 | EUR | Germany GDP Q/Q Q1 F | 0.20% | 0.20% | ||

| 12:30 | CAD | Retail Sales M/M Mar | -0.10% | -0.10% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Mar | -0.20% | -0.30% | ||

| 12:30 | USD | Durable Goods Orders Apr | 0.50% | 2.60% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Apr | 0.10% | 0.20% | ||

| 14:00 | USD | Michigan Consumer Sentiment May | 67.4 | 67.4 |