Sample Category Title

Cliff Notes: Consumers and Central Banks Seek Confidence

Key insights from the week that was.

In Australia, Westpac-MI Consumer Sentiment is still yet to show any material signs of recovery. In May, the headline index remained locked in deeply pessimistic territory, moving 0.3% lower to 82.2. The latest update captured consumer reactions to the Federal Budget, which included a number of cost-of-living relief measures. The Budget was well received, with fewer households than usual expecting to be ‘worse off’ post-Budget than traditionally is the case. That said, the survey suggests households plan to save around 80% of the benefit from the Stage 3 tax cuts. Such an outcome would aid the RBA in their goal to ensure inflation returns to, and remains sustainably, at target.

Here and now however, headwinds continue to be felt. The sub-index tracking family finances versus a year ago fell 3.6% to 63.2, while views on ‘time to buy a major household item’ declined 2.8% to 76.5; these indexes are now 28% and 39% below their respective long-run averages. The higher-than-expected Q1 inflation outcome is likely the chief culprit, and helps explain the positive reception the Budget has received. Thankfully, forward views on finances continue to improve, ‘finances next twelve months’ rising another 0.7% to 96.1, only 10% below the long-run average. Also encouraging is that the one-year and five-year economic outlook measures remain constructive, lifting 0.7% and 2.6% respectively, the 5-year view now in line with the historic average.

The RBA May Minutes provided more colour around the Board’s deliberations, in particular the considerations for monetary policy of stronger-than-expected inflation outcomes. The case for another hike was premised on risk judgements, the two main considerations being that staff forecasts could be viewed as “overly optimistic about the forces that would drive down inflation” and that consumption may “pick up somewhat more rapidly if labour market outcomes remained benign”. The case for leaving policy unchanged was deemed stronger though, the Board of the view that, while recent updates have slightly tilted the balance of risks, it is not to the degree that warrants further tightening. The Board expects inflation to continue decelerating towards target as demand and supply come into better balance, but it needs more confidence in this view before debating the timing and scale of easing. We continue to believe the Board will have this confidence by November, allowing the RBA to embark on a measured rate cutting cycle, 25bps per quarter to 3.10% in Q4 2025. The coordination between fiscal and monetary policy frameworks was explored in this week’s essay from Chief Economist Luci Ellis.

The RBNZ’s May Monetary Policy Statement meanwhile highlighted that significant risks remain for New Zealand’s inflation outlook. Inflation is forecast to fall back into the 1-3% band at the end of 2024, but is now not anticipated to return to the 2% mid-point until mid-2026. The RBNZ cash rate track points to the risk of another hike in late-2024 and the first cut not occurring until August 2025. Westpac remains of the view that the first cut will come earlier, in February 2025; but that the ensuing cutting cycle will be gradual, and the end-point in mid-2026 100bps above the RBNZ’s upwardly revised estimate of neutral (3.75% versus 2.75%).

Further afield, S&P Global flash PMIs for May were constructive regarding activity but highlighted lingering inflation risks. The US measures received the most attention, the services PMI jumping 3.5pts, while the manufacturing PMI retraced half April’s loss. Unnerving some participants was an acceleration in input prices for manufacturing and services; however, output prices were little changed in the month, and all of the price indexes remain well below the elevated readings of 2021-23. If employment slows in coming months, as this survey suggests, further pressure will be placed on output prices. As alluded to by FOMC members and the minutes this week (see below), inflation risks remain; but a return to, or very near, the 2.0% inflation target during the next 6-12 months is most probable.

Over in the UK, the service and manufacturing indexes came in below the market’s expectations and April’s outcomes, but were still expansionary. Helpfully, UK businesses reported that cost and wage pressures continue to abate, setting the scene for rate relief later in 2024 despite the latest CPI report coming in above expectations – April seeing a headline rise of 0.3% against the consensus estimate of 0.1% as services inflation held up. The Euro Area results also point to abating consumer price risks; input prices continue to grow at a robust pace, but selling prices are under pressure. As the ECB begins to cut interest rates from mid-year, the services sector should gain further strength. Having recovered to a 15-month high, the manufacturing index suggests European manufacturers are ready to benefit from stronger growth at home and abroad. This is also the case for Japan’s manufacturers, the Jibun manufacturing PMI returning to growth in May after almost 18 months of contraction. Japan’s service sector meanwhile continues to benefit from Yen weakness and nascent positive real income growth amongst households.

With other data inconsequential, for much of the week, the market again focused on the subtleties of US FOMC policy guidance. From the minutes and the members who spoke, the message was clear: as yet, the FOMC do not have enough confidence in the inflation outlook to begin cutting; but policy is considered restrictive and effective; hence a return to target inflation is believed to be only a matter of time, with further tightening only required if inflation surprises to the upside.

Japan’s core CPI eases to 2.2% in Apr, marking second month of slowdown

Japan's CPI core, which excludes food, decelerated from 2.6% yoy to 2.2% yoy in April. This aligns with market expectations and marks the second consecutive month of decline from February's 2.8%. Despite the slowdown, core inflation has remained at or above BoJ's 2% target for the 25th straight month.

CPI core-core, which strips out both food and energy costs, also showed signs of easing, slowing from 2.9% yoy to 2.4% yoy. This is the slowest pace of increase since September 2022. Meanwhile, headline CPI, which includes all items, fell from 2.7% yoy to 2.5% yoy.

A closer look at the major components reveals varied trends. Food prices rose by 3.5% yoy, but this was a moderation from 4.6% yoy increase seen in March. The surge in accommodation fees, up 18.8% yoy, was driven by a revival in inbound tourism. Energy prices edged up slightly by 0.1% yoy, with increases in kerosene and gasoline prices leading the way. Service prices also showed a deceleration, rising by 1.7% yoy compared to 2.1% yoy increase in the previous month.

RBNZ stresses vigilance on inflation, prepared to raise rates if necessary

In an interview today, RBNZ Assistant Governor Karen Silk highlighted the central bank's readiness emphasized that there are "risks still to the upside in the near term" regarding inflation. She stated that RBNZ is "absolutely" prepared to raise interest rates if necessary, adding, "Right now we are saying that the level of restrictiveness is there, but we are awake at the wheel."

Silk pointed out that the central bank's primary concern is domestic inflation, particularly noting the significant miss last quarter when non-tradables inflation hit 5.8%, compared to RBNZ's forecast of 5.3%. "Our concern is in that near term, around what are we really seeing in terms of domestic aligned inflation," she explained.

Separately, Deputy Governor Christian Hawkesby reinforced the cautious stance, stating that "cutting interest rates is not part of near-term discussion." He acknowledged the near-term inflation risks are to the upside but expressed confidence that medium-term inflation is returning to target.

Hawkesby emphasized that no single data point will trigger a rate hike, but the bank is closely watching domestic inflation pressures and expectations. He also noted the significant uncertainty surrounding tradable inflation moving forward.

RBNZ's central projection is for headline inflation to fall back into its 1-3% target band by the fourth quarter of this year. However, the bank now projects that it won't achieve its 2% goal until mid-2026.

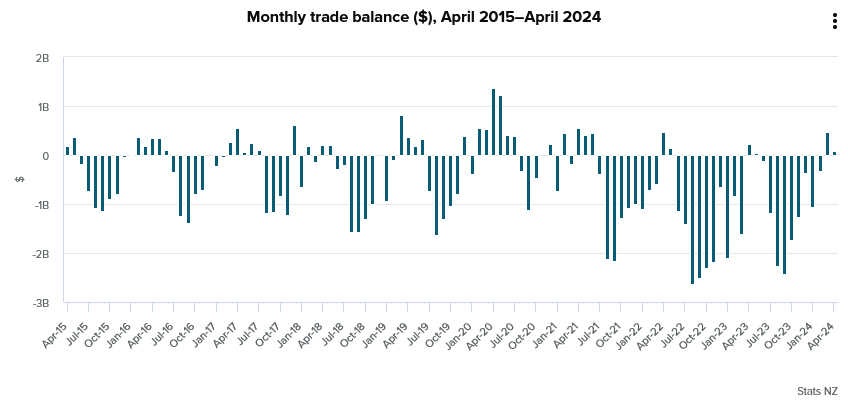

New Zealand’s exports falls -2.6% yoy in Apr, imports down -0.7% yoy

In April, New Zealand's goods exports fell by -2.6% yoy to NZD 6.4B, while goods imports decreased by -0.7% yoy to NZD 6.3B. Contrary to expectations of a NZD -202m deficit, trade balance recorded a surplus of NZD 92m.

Examining the top monthly export movements by country, exports to China decreased by NZD -206m (-11% yoy), and exports to Australia fell by NZD -17m (2.4% yoy). In contrast, exports to the US increased by NZD 35m (4.9% yoy), exports to EU rose by NZD 62m (13% yoy), and exports to Japan surged by NZD 91m (26% yoy).

On the import side, imports from China increased by NZD 120m (10% yoy), and imports from South Korea soared by NZD 371m (119% yoy). However, imports from the EU decreased by NZD -79m (-8.1% yoy), and imports from the US dropped by NZD -154m (24% yoy). Imports from Australia grew modestly by NZD 9.8m (1.4% yoy).

Fed’s Bostic: Inflation not yet at safe point for rate cuts

Atlanta Fed President Raphael Bostic emphasized caution regarding interest rate cuts, stating that the US economy is not yet past the "worry point" for inflation to return to the target of 2%.

Speaking at an event overnight, Bostic highlighted the robustness of job growth, describing it as "a lot of energy in the economy." This robust job growth gives him confidence in maintaining a "more restrictive level" of monetary policy, as he doesn't believe there's a risk of "falling into a contractionary environment."

Bostic also mentioned the need to be "a little more patient" and ensure inflation is on a clear path to 2% before considering rate cuts.

He underscored the importance of moving in "one direction only" to avoid the uncertainty that would come from cutting rates only to raise them again. This approach, he believes, would prevent creating "policy uncertainty."

Hand in Hand is the Surer Way to Land

Households are cutting consumption in a textbook response to higher interest rates. This, and a likely future of inflationary supply shocks, warrants a more coherent design to fiscal and monetary policy frameworks.

This week saw the RBA Board minutes observe that many households have been pulling back on spending even when their incomes have not been falling. We also saw a similar implication from the May release of the Westpac–Melbourne Institute Consumer Sentiment Survey.

As Westpac Economics colleague Matt Hassan noted, most households who expect to receive a tax cut plan to save most or all of it. Altogether, around 80% of the increase in post-tax income is planned to be saved. Plans do not always pan out and the households that do not expect to receive the tax cut might spend that pleasant surprise. Even still, these results tilt more to saving than did the responses to surveys concerning previous rounds of stimulus.

That households plan to save more out of the extra income than in previous episodes should not come as a surprise. It is the expected implication of contractionary monetary policy. One of the main ways that monetary policy dampens demand is by changing the incentive to save versus borrow or spend. It does not need to reduce people’s incomes to change their behaviour. The RBA minutes referred to this as ‘simply choosing’ to spend less, but there is no mystery behind the choice. It is what economists call the ‘intertemporal substitution channel’. People ‘simply choose’ to respond to the incentives created by higher interest rates.

Intertemporal substitution is likely to be more powerful than the ‘cash flow channel’ working via lowering the incomes of households with mortgages, not least because it affects everyone. In the Australian context, though, it is often forgotten. Because variable-rate mortgages predominate in the Australian market, the mortgage cash flow channel receives far more attention than its overall impact warrants. The commentary in the RBA minutes and the downward revision to its consumption forecasts suggest that the RBA, too, might have over-focused on the cash flow channel in its recent analysis.

Higher mortgage rates have been a struggle for many households recently. Across the whole household sector, though, they have not been as big a drag on incomes as inflation itself or the resulting tax bracket creep. As we have been highlighting for some time, higher tax payments have done more to weigh on real household incomes than higher net interest payments have done. And as we have also been highlighting, this additional fiscal squeeze distinguishes Australia from some peer economies, including the United States and Canada where tax brackets are CPI-indexed. It means that one cannot read across from those countries’ experiences to infer how much monetary contraction is needed here, or for how long. It matters if fiscal and monetary policy are working hand in hand or not.

Such a policy alignment contrasts with the common presumption that monetary policy needs to offset fiscal policy, in a macro-policy version of Newton’s Third Law. Post-Budget commentary arguing that additional spending would need to be met with higher rates falls into this camp. It assumes that there is no spare capacity in the economy when the spending occurs, so inflation must rise if it is not offset. It also tends to understate the role of automatic stabilisers relative to conscious policy decisions. In fact, so-called ‘parameter variations’ – in other words, the economy turning out differently than expected – have typically shifted budget outcomes more than explicit policy decisions have.

In the same vein, if monetary policy is poised to become a bit less contractionary late this year, it would make sense for fiscal policy to be set with a similar stance. It would certainly make fiscal and monetary policy more coherent – and the impact less uneven – than choosing this moment to achieve a significant fiscal consolidation, in the name of long-term sustainability or demand-shock absorption.

Treating monetary and fiscal policy purely as counterbalances rather than working in the same direction also sits oddly with the likely future of climate and supply-driven inflation shocks. If Australia and the world are indeed facing a more inflationary environment – or as the RBA Governor put it, ‘shock after shock after shock’ – surely it would make sense to refine the economic policy architecture to be more resistant to inflationary surges. And again, it would make sense for fiscal policy and monetary policy to operate hand in hand. This can be achieved by good system design as well as conscious coordination, without necessarily detracting from the independence of the central bank.

One obvious improvement would be stop indexing administered prices such as education fees and subsidised medicines to the CPI. This simply propagates a surge in inflation into the following year. Indexing by 2½%, the midpoint of the RBA’s inflation target, would avoid this issue.

Another refinement that would improve the response to inflation surges would be to index tax brackets by 2½%, as we have previously advocated. Fixed tax brackets lean against inflationary surges via bracket creep. This form of automatic stabilisation has its advantages. However, as we have seen in Australia recently, it can overdo the negative consumption response to inflation surges, leaving other sectors such as public demand or business investment relatively untouched. And without periodic tax cuts, the share of income paid in tax will rise forever. On the other hand, indexing brackets to CPI, as the US and Canadian tax systems do, means monetary policy and explicit fiscal actions must shoulder the load of inflation control. Lifting tax thresholds at a fixed rate retains the stabilisation properties of fixed brackets while avoiding the bias to higher taxation over time.

Indexing by 2½% would be preferable to CPI indexation in a range of other domains, too. Governments and others could build a preference for contract bids with escalation clauses fixed at 2½% annually, not CPI-linked indexation clauses. Capital gains could be taxed at the full marginal rate on a ‘real’ return using a 2½% annual inflation rate. This would remove the tax preference for capital gains over rental income – a significant distortion in the housing market – without the complexity of the pre-1999 system and without having to touch negative gearing. And all of these policy refinements would help anchor inflation expectations by keeping that 2½% figure front of mind.

There are, of course, other refinements that would help make the system more resistant to inflationary surges. Enhancing the automatic stabilisers in fiscal policy is one, for example by targeting welfare payments appropriately (though Australia is already much further down this road than peer economies). Efforts to make the supply side more resilient to shocks would also help. And fiscal austerity now, to minimise government debt and create space for stimulus later, might be less useful if future shocks are more likely to be supply-driven and inflationary, rather than demand shocks.

Achieving a soft landing after a large shock cannot be left to one policy tool that operates unevenly across the community and is not well tuned to all kinds of shock. Policies working hand in hand are a surer way to land.

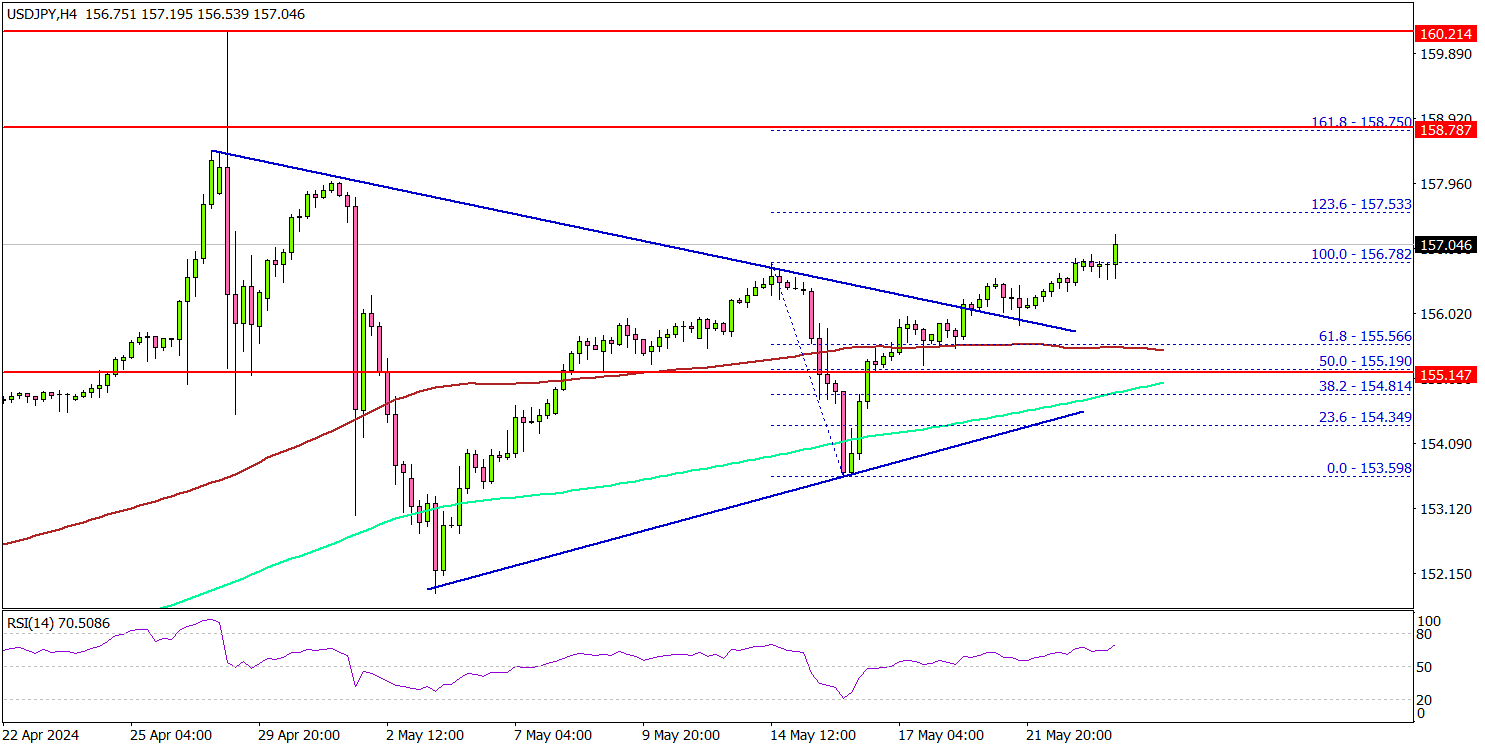

USD/JPY Restarts Increase But Lacks Bullish Momentum

Key Highlights

- USD/JPY started a fresh increase above the 156.00 resistance.

- It broke a major contracting triangle with resistance at 156.10 on the 4-hour chart.

- Gold price declined heavily and moved in the red zone below $2,380.

- Oil prices are still struggling to recover above the $80.00 resistance.

USD/JPY Technical Analysis

The US Dollar formed a base above 153.50 and started a decent increase against the US Dollar. USD/JPY broke the 154.80 and 155.50 resistance levels to move into a positive zone.

Looking at the 4-hour chart, the pair even settled above the 200 simple moving average (green, 4-hour) and the 100 simple moving average (red, 4-hour). The pair broke a major contracting triangle with resistance at 156.10.

There was also a move above the last swing high at 156.78. On the upside, the first major resistance is near 157.50. A clear move above the 157.50 resistance might send it toward the 158.50 level.

Any more gains might call for a move toward the 160.00 level in the near term. If there is no move above the 157.50 resistance, the pair might correct gains.

Immediate support is near the 156.50 level. The next major support is at 156.20. If there is a downside break below the 156.20 support, the pair might test the 100 simple moving average (red, 4-hour) at 155.50. Any more losses might send the pair toward the 154.20 level.

Looking at Gold, the bears took control and there was a sharp decline below the $2,380 support zone. The next major support sits at $2,300.

Economic Releases

- US Durable Goods Orders for April 2024 – Forecast -0.8% versus +2.6% previous.

- US Durable Goods Orders ex Defense for April 2024 – Forecast -0.4% versus +2.3% previous.

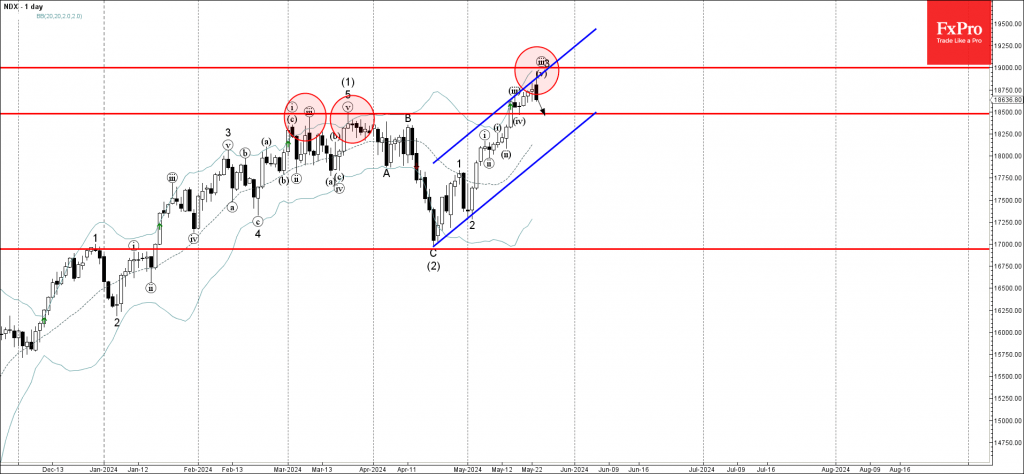

NASDAQ 100 Index Wave Analysis

- NASDAQ 100 Index reversed from round resistance level 19000.00

- Likely to fall to support level 18500.00

NASDAQ 100 Index today reversed down from the resistance area located between the round resistance level 19000.00 and the upper daily Bollinger Band.

The resistance level 19000.00 was strengthened by the resistance trendline of the daily up channel from the end of April.

Given the strength of the resistance level 19000.00 and the overbought daily Stochastic, NASDAQ 100 Index can be expected to fall further to the next support level 18500.00.

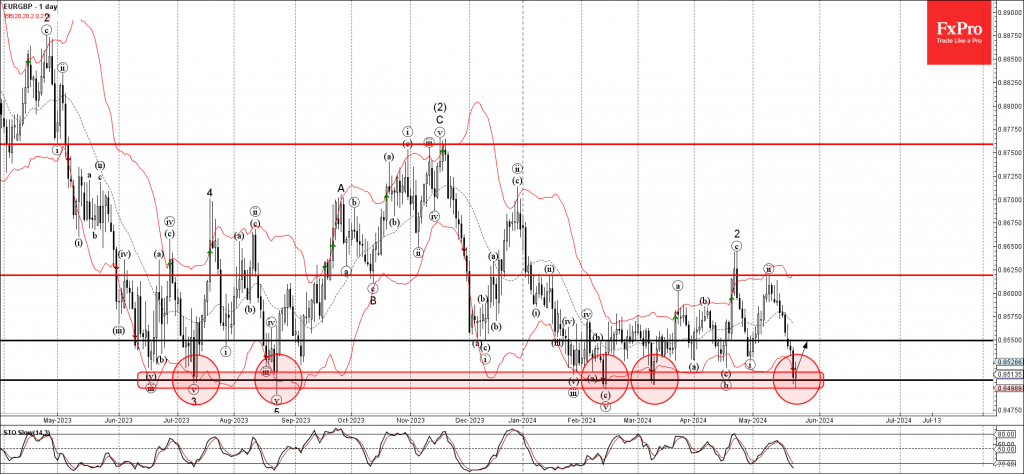

EURGBP Wave Analysis

- EURGBP reversed from long-term support level 0.8500

- Likely to test resistance level 0.8550

EURGBP currency pair today reversed up from the major long-term support level 0.8500 (which has been steadily reversing all downward impulse of this pair from July of 2023) intersecting with the lower daily Bollinger Band.

The upward reversal from the support level 0.8500 stopped the previous impulse waves 3 and (3).

Given the strength of the support level 0.8500 and the oversold daily Stochastic, EURGBP currency pair can be expected to rise further to the next resistance level 0.8550.