Sample Category Title

EUR/USD: Recovery Needs Further Positive Signals to Resume

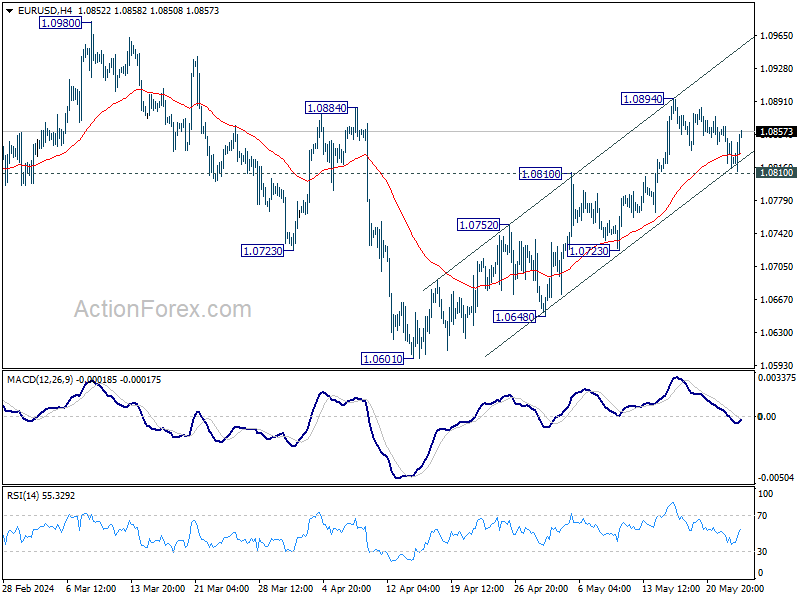

The Euro regained traction and bounced 0.3%, after pullback from 1.0895 (May 16 high) was repeatedly rejected at 100DMA (1.0814), generating initial signal of a double-bottom and potential end of corrective phase.

Fresh strength so far retraced over 50% of 1.0895/1.0812 pullback and on track complete bullish engulfing pattern on daily chart, which would reinforce reversal signal.

Daily MA’s returned to bullish setup, with 10/200DMA golden cross and converged 20/200DMA’s about to form another cross, while positive momentum remains strong and adds to improved technical picture.

Better than expected May PMI data from Germany and Eurozone, released earlier today, positively impacted the single currency by adding to bets for ECB’s June rate cut, however, upbeat US PMI data partially offset the positive impact.

Daily close above broken 50% retracement level (1.0853) will be a minimum requirement to keep fresh bulls intact for further recovery and possible attack at key near-term barriers at 1.0891/95 (Fibo 76.4% / May 16 peak.

On the other hand, dip and close below rising 10DMA (1.0838) would weaken near-term structure and risk renewed attack at key 100DMA support, loss of which would shift near-term focus to the downside.

Res: 1.0838; 1.0885; 1.0891; 1.0942.

Sup: 1.0838; 1.0814; 1.0786; 1.0760.

Sunset Market Commentary

Markets

European May PMIs were generally speaking good. The services reading stabilized at a decent 53.3 in May but a better-than-expected improvement in the admittedly still struggling manufacturing sector (from 45.7 to 47.4) lifted the composite figure to the highest in a year (52.3). S&P Global estimates Q2 growth at 0.3% while projecting an annual 1% growth (with upside) risks for 2024. Faster increases in private sector business activity, new orders and employment were recorded. Services continued to compensate for manufacturing in every of the aforementioned components. That said, the rate of contraction in manufacturing output (nearing stabilization) and new orders was the slowest since long. Business confidence hit a 27-month high. Meanwhile, rates of inflation of both input costs and output prices softened from April. That’s little reason to cheer though as they remained above pre-pandemic averages in each case. In addition, the widely anticipated outcome of the Q1 negotiated wages defied expectations for a decline and instead picked up from 4.5% to 4.7%. That matched the 2023Q3 three-decade high. The ECB, among those anticipating a slowdown as well, did its best to downplay the result in a blog post. They attributed it to (German) one-offs and said that based on a range of indicators, including its own tracker, wage growth would decelerate in 2024 from current elevated levels. Be that as it may, ECB policymakers themselves have highlighted the importance of today’s outcome for future policy (after a June cut) numerous times and it’s all too easy to be splitting hairs afterwards. German Bunds naturally underperform US Treasuries today. Yields in the country rise up to 6.2 bps at the front with the 2-yr yield hitting new YtD highs. The European swap counterpart is coming close. Money markets pared conviction on three ECB rate cuts this year to less than 50%. US rates in choppy trading trade flat to slightly higher (+/- 1bp) after another strong weekly jobless claims reading (215k vs 220k expected) erased earlier (small) losses. Gilt yields initially extended yesterday’s CPI driven surge before reversing course following the PMIs (see below). They currently trade 0.4-1.2 bps lower.

The euro takes the upper hand against the dollar, bringing the EUR/USD pair from 1.0823 to 1.086 currently. Technically nothing has changed though with first resistance levels at 1.0895 never having come under pressure. The common currency also got some respite against the British pound. EUR/GBP rebounded from an important support level around 0.85 to change hands in the 0.852 area with the move gaining traction after the UK PMIs. Equity markets trade in positive territory, helped by stellar Nvidia results released yesterday after US trading hours. The EuroStoxx50 adds 0.5%, Wall Street opens with about 1% gains for the Nasdaq.

News & Views

The Turkish central bank (CBRT) kept its policy rate unchanged at 50% and sticks with a tightening bias in case a significant and persistent deterioration in inflation is foreseen. Recent indicators point to a slowdown in domestic demand compared to Q1 2024. In addition to the high level of and the stickiness in services inflation, inflation expectations, geopolitical risks, and food prices keep inflationary pressures alive. Considering the lagged effects of the monetary tightening, the Committee decided to keep the policy rate unchanged, but reiterated that it remains highly attentive to those inflation risks. The Turkish lira keeps near historically low levels around EUR/TRY 35.

The UK Composite PMI unexpectedly declined from 54.1 to 52.8 in May while consensus was looking for a stabilization. A revival in manufacturing production (51.3 from 49.1; 22-month high) couldn’t make up for a setback in services (52.9 from 55; 6-month low). Business activity growth was again accompanied by a rise in new order volumes and an uptick in export sales, but ongoing hiring challenges meant that the rate of job creation remained only marginal. At the same time, UK businesses reported the softest increase in average selling prices for over three years, partly linked to a slowdown in input cost inflation after April’s steep rise. Survey respondents highlighted a softening of labour cost pressures following the increase in the National Living Wage, with services firms especially seeing a drop in input price inflation. Today’s survey data are consistent with GDP rising around 0.3% in Q2.

Graphs

German 2-yr yield hits new YtD high in the wake of improving PMIs and …

... record-matching wage growth in the EMU (2024Q1 data). ECB’s manouvring room after a June cut becomes increasingly limited.

EUR/GBP rebounds after nearing critical support around 0.85. A setback in UK services PMI weighs on sterling.

EUR/CHF nearing parity as scope for rate cuts in Switzerland contrasts with Europe

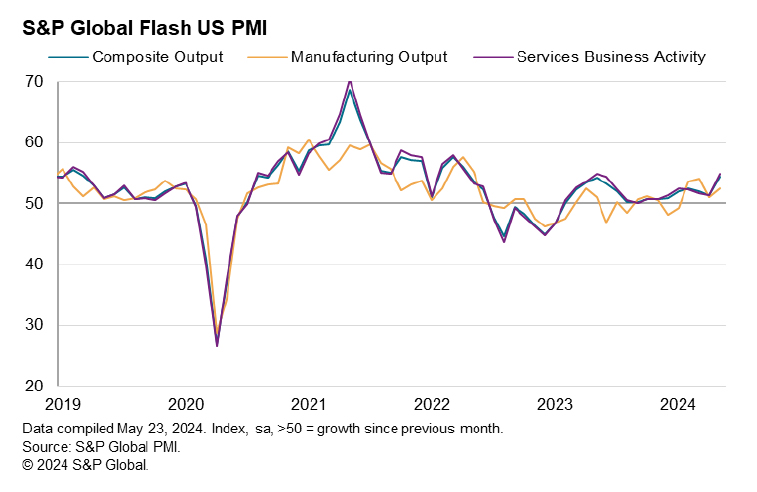

US PMI composite jumps to 25-month high, upturn accelerates again

US PMI Manufacturing rose from 50.0 to 50.9 in May. PMI Services rose fro 51.3 to 54.8, a 12-month high. PMI Composite rose from 51.3 to 54.4, a 25-month high.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"The US economic upturn has accelerated again after two months of slower growth, with the early PMI data signalling the fastest expansion for just over two years in May. The data put the US economy back on course for another solid GDP gain in the second quarter.

"Not only has output risen in response to renewed order book growth, but business confidence has lifted higher to signal brighter prospects for the year ahead. However, companies remain cautious with respect to the economic outlook amid uncertainty over the future path of inflation and interest rates, and continue to cite worries over geopolitical instabilities and the presidential election.

"Selling price inflation has meanwhile ticked higher and continues to signal modestly above-target inflation. What's interesting is that the main inflationary impetus is now coming from manufacturing rather than services, meaning rates of inflation for costs and selling prices are now somewhat elevated by pre-pandemic standards in both sectors to suggest that the final mile down to the Fed's 2% target still seems elusive."

USD/JPY Steady as Japanese PMIs Mixed

The Japanese yen is slightly lower on Thursday. USD/JPY is trading at 156.70, down 0.08% on the day at the time of writing.

Japan’s PMIs for April were a mixed bag and the yen didn’t show much reaction. Services PMI dipped to 53.6, down from 54.3 in March and just shy of the forecast of 53.8. This was the smallest growth in services since February.

Manufacturing PMI showed improvement and rose to 50.5, up from 49.6 in March and above the market estimate of 49.7. This was the first growth since May 2023 as manufacturing has been in a prolonged slump. The 50 level separates contraction from growth.

The Japanese economy is showing signs of improving after first-quarter GDP declined. Inflation has been easing, which could hamper the ability of the Bank of Japan to increase rates without reigniting deflation.

FOMC minutes: Fed considered a rate hike at May meeting

With inflation falling around the globe, major central banks have been under pressure to lower interest rates. The central banks remain cautious, however, and the Fed minutes indicated that there was a discussion to raise rates at the May 1st meeting. Other central banks are also unclear about their rate path – the Reserve Banks of Australia and New Zealand held rates at their most recent meetings but also considered hiking rates.

The FOMC minutes noted that policy makers are not confident about lowering rates at this stage and want to see more evidence that inflation will continue to drop and remain sustainable around the 2% target. This message is consistent with what we have been hearing from a host of Fed members, although the markets have priced in a September rate cut.

USD/JPY Technical

- USD/JPY tested support at 156.02 earlier. Below, there is support at 156.33

- 157.07 and 157.32 are the next resistance lines

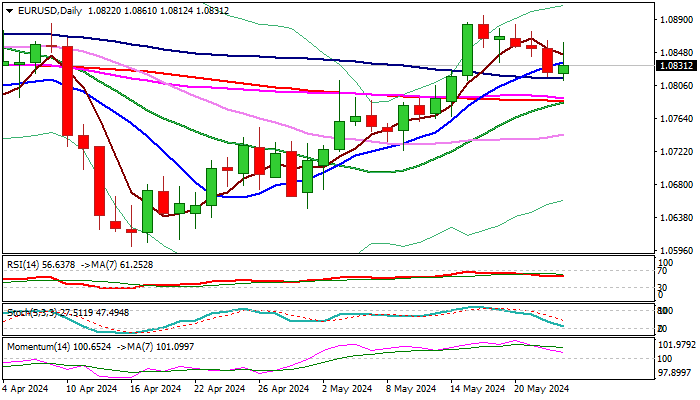

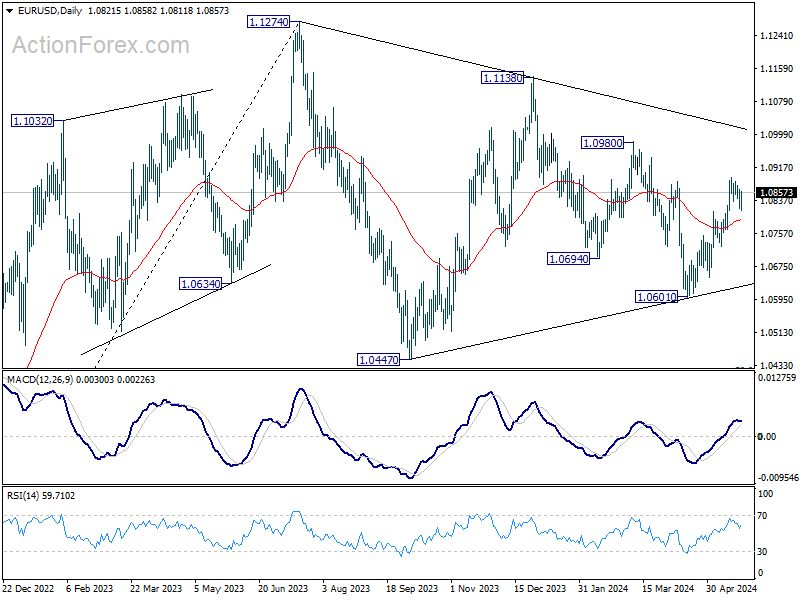

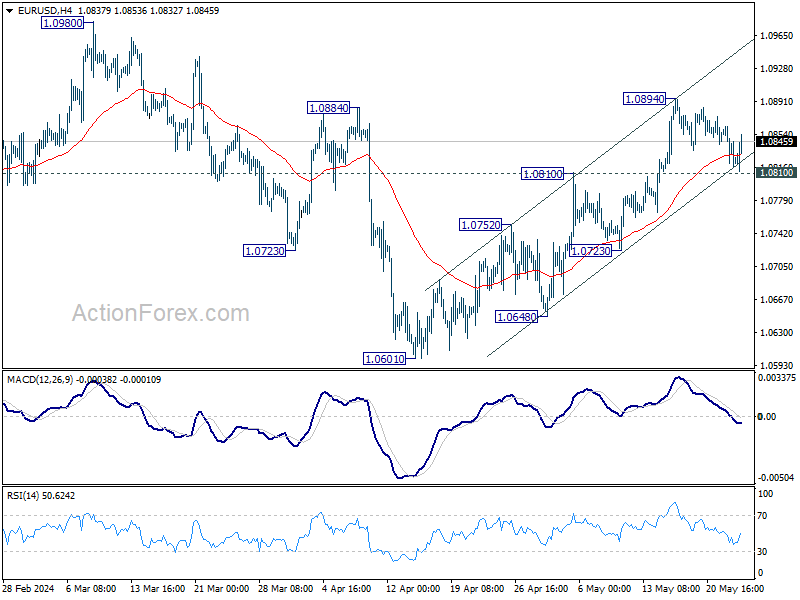

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0805; (P) 1.0834; (R1) 1.0852; More...

EUR/USD recovers ahead of 1.0810 resistance turned support. Intraday bias stays neutral at this point. On the upside, break of 1.0894 will resume the rise from 1.0601 to 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed at 1.0601 already. However, firm break of 1.0810 will dampen this bullish case, and turn bias back to the downside for 55 D EMA (now at 1.0791) and below.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

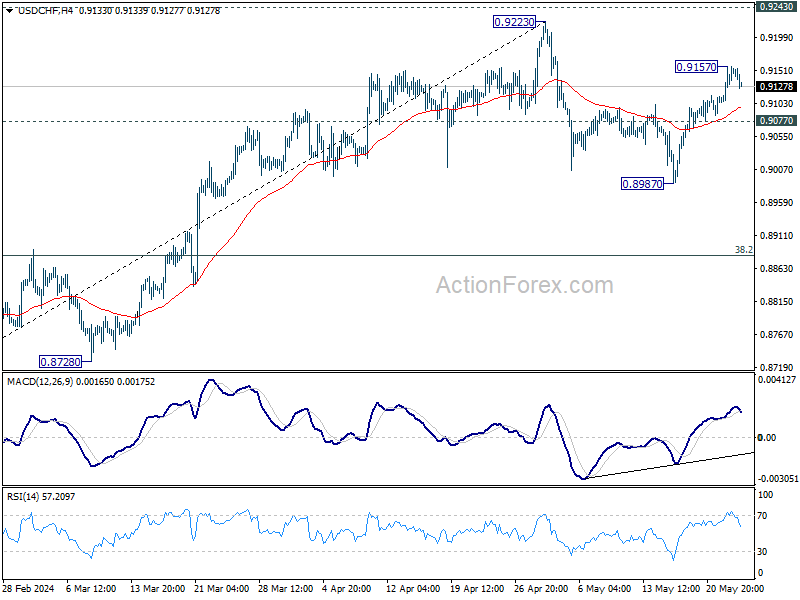

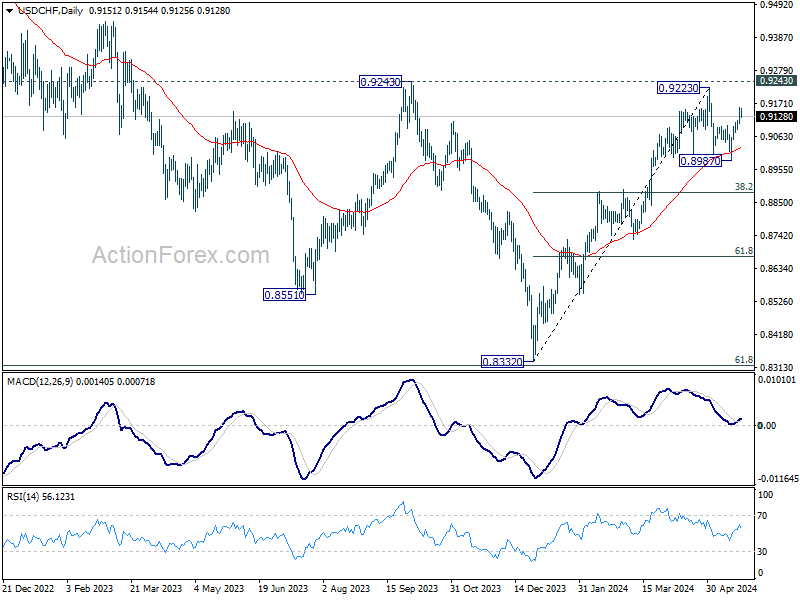

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9117; (P) 0.9138; (R1) 0.9178; More....

Intraday bias in USD/CHF is turned neutral with current retreat. On the upside, above 0.9157 will resume the rebound from 0.8987 to retest 0.9223 high. On the downside, break of 0.9077 support will bring retest of 0.8987. Break there will resume the fall from 0.9223 to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

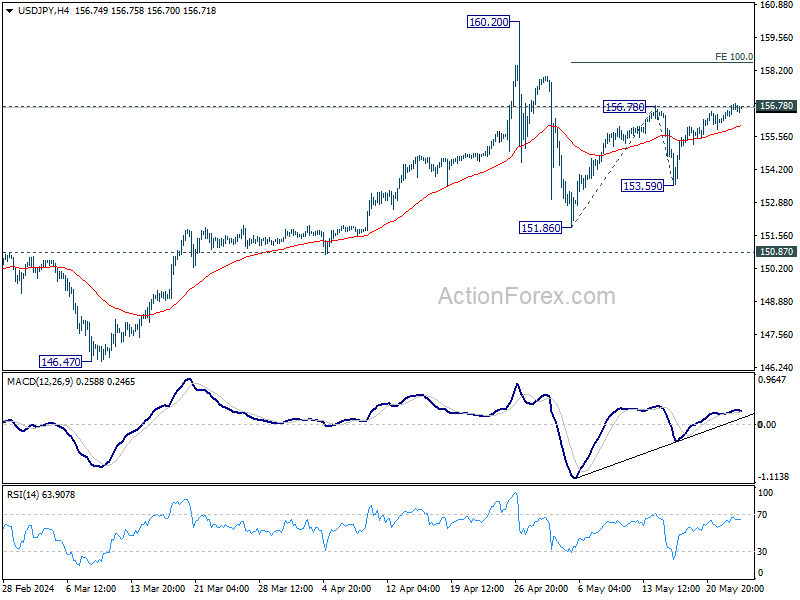

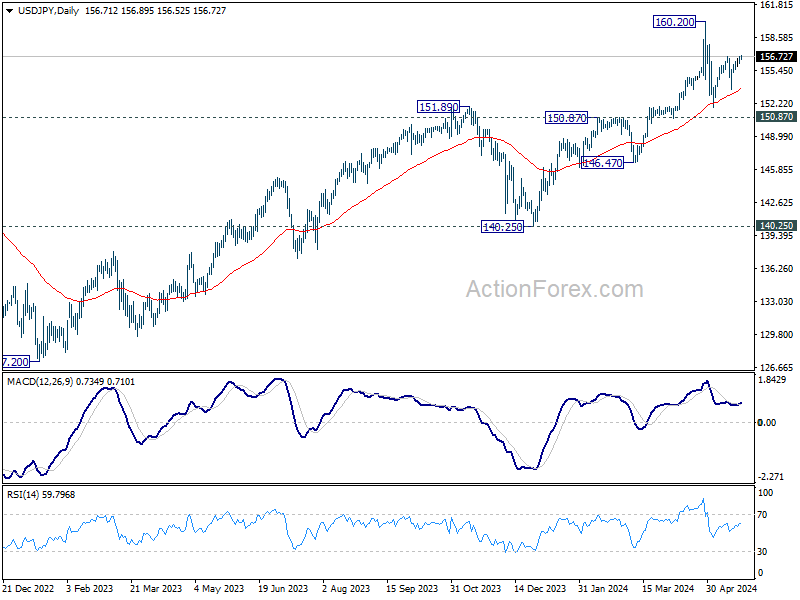

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.33; (P) 156.58; (R1) 157.07; More...

Intraday bias in USD/JPY stays neutral and outlook is unchanged. Price actions from 160.20 are seen as a corrective pattern. On the upside, break of 156.78 will resume the rise from 151.86, as the second leg, to 100% projection of 151.86 to 156.78 from 153.59 at 158.51. On the downside, below 153.59 will target 151.86 and below as the third leg.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

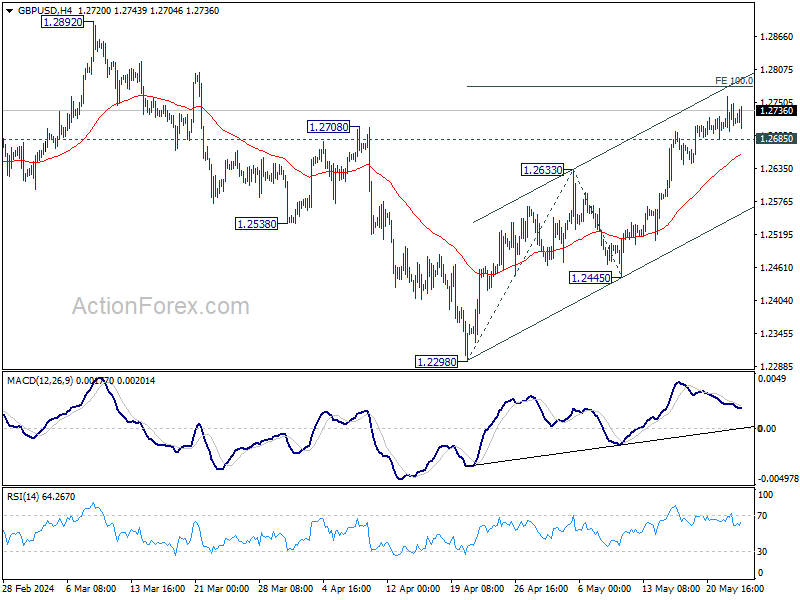

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2691; (P) 1.2726; (R1) 1.2753; More...

Intraday bias in GBP/USD stays neutral for the moment. On the upside. decisive break of 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780 will extend the rally from 1.2298 to 1.2892 resistance next. However, break of 1.2685 will minor support will turn bias back to the downside, for retreat to 55 4H EMA (now at 1.2661) and below.

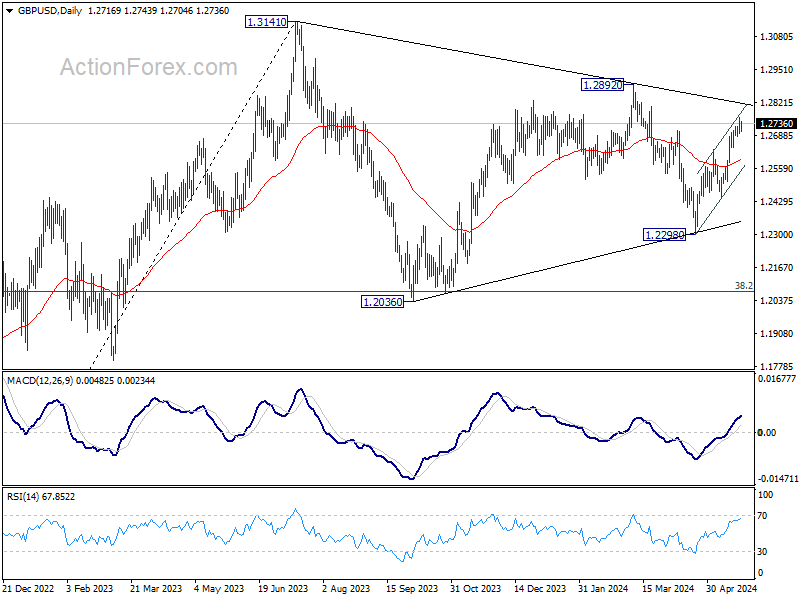

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351 (2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Euro Recovers on Eurozone PMIs, But Gains Limited

As trading progresses into US session, activity in the forex markets remains relatively muted. Euro is showing signs of recovery ahead of key support levels against Dollar and crucial support against Sterling. Eurozone PMIs revealed that economic recovery is strengthening, with Germany, the region's largest economy, finally catching up. Despite this positive data, Euro's gains are still modest.

Currently, New Zealand Dollar is the strongest performer of the day, supported by strong retail sales data. Following closely is Australian Dollar while Swiss Franc is the third strongest. On the other end of the spectrum, Dollar is the weakest performer, trailed by Japanese Yen and British Pound. Canadian Dollar and Euro are positioned in the middle of the performance spectrum.

Technically, focus is now on whether EUR/USD could extend the bounce from slightly above 1.0810 resistance turned support. Further break of 1.0894 will confirm underlying bullishness momentum. Rise from 1.0601 should then target 1.0980 resistance next.

In Europe, at the time of writing, FTSE is flat. DAX is up 0.41%. CAC is up 0.50%. UK 10-year yield is down -0.021 at 4.215. Germany 10-year yield is up 0.012 at 2.551. Earlier in Asia, Nikkei rose 1.26%. Hong Kong HSI fell -1.70%. China Shanghai SSE fell -1.33%. Singapore Strait Times rose 0.44%. Japan 10-year JGB yield rose 0.002 to 1.003.

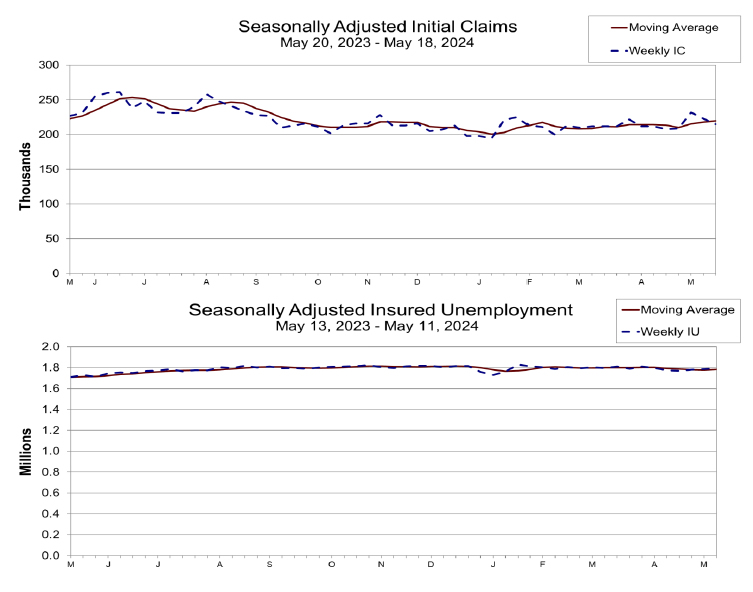

US initial jobless claims falls to 215k, vs exp 220k

US initial jobless claims fell -8k to 215k in the week ending May 18, below expectation of 220k. Four-week moving average rose 2k to 220k. Continuing claims rose 8k to 1794k in the week ending May 11. Four-week moving average of continuing claims rose 5k to 1782k.

UK PMI manufacturing rises to 22-month high, services growth slows

UK PMI Manufacturing rose from 49.1 to 51.3 in May, surpassing expectations of 49.2 and reaching a 22-month high. However, PMI Services fell from 55.0 to 52.9, below the anticipated 54.8 and marking a 6-month low. Consequently, PMI Composite dropped from 54.1 to 52.8.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, stated that the flash PMI indicates a "further expansion" of UK business activity, aligning with GDP growth of around 0.3% in Q2. He highlighted an "encouraging revival of manufacturing accompanied by sustained, but slower, service sector growth."

The survey also revealed positive news regarding service sector inflation, which is cooling. Companies reported the slowest price growth in over three years, with headline inflation falling close to BoE's target. Williamson noted that the PMI data support the view that BoE will start cutting interest rates in August, assuming the data continues to improve over the summer.

Eurozone PMI composite hits 12-month high at 52.3, pointing to 0.3% GDP growth in Q2

In May, Eurozone's PMI Manufacturing rose from 45.7 to 47.4, surpassing expectations of 46.6 and marking a 15-month high. PMI Services remained unchanged at 53.3, slightly below the forecast of 53.5. PMI Composite increased from 51.7 to 52.3, reaching a 12-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that Eurozone's economy is "gathering further strength." He highlighted that new orders are growing at a healthy rate, and companies' confidence is reflected in a steady hiring pace.

Additionally, de la Rubia pointed out some positive developments for ECB. Rates of inflation for input and output prices in the services sector have softened. This trend supports ECB's apparent stance to cut rates at the upcoming meeting on June 6.

Incorporating PMI numbers into their GDP nowcast, de la Rubia suggested that Eurozone will likely grow at a rate of 0.3% during Q2, effectively dispelling fears of a recession. He further indicated that GDP growth rate of nearly 1% could be achievable this year, with potential for even higher growth.

Also released, French PMI Manufacturing rose from 45.3 to 46.7 in May. PMI Services fell from 51.3 to 49.4. PMI Composite fell from 50.5 to 49.1, back in contraction.

Germany PMI Manufacturing rose from 42.5 to 45.4 in May, a 4-month high. PMI Services rose from 53.2 to 53.9, an 11-month high. PMI Composite rose from 50.6 to 52.2, a 12-month high.

Japan's PMI manufacturing rises to 50.5, first expansion in a year

Japan's PMI Manufacturing rose from 49.6 to 50.5 in May, exceeding expectations of 49.7 and signaling improving business conditions for the first time in a year. Meanwhile, PMI Services declined from 54.3 to 53.6, and PMI Composite inched up from 52.3 to 52.4.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, noted that Japan's private sector expansion accelerated for the third consecutive month, reaching its fastest pace since August 2023. This suggests continued growth momentum midway through Q2, hinting at a better GDP reading after the disappointing Q1 results.

Pan highlighted that the expansion in business activity remained "services-led," but the "near-stabilization" of manufacturing output offers hope for broader growth later in the year.

Both input cost and output price inflation rates eased, indicating "softer inflationary pressures across official gauges." However, manufacturers continue to face rising cost pressures, partly due to "yen fluctuations," which remain an important factor to monitor.

Australia PMI composite dips to 52.6, increasing cost pressures

Australia's PMI Manufacturing remained steady at 49.6 in April, a joint 9-month high. PMI Services dropped slightly from 53.6 to 53.1, while PMI Composite decreased from 53.0 to 52.6.

Warren Hogan, Chief Economic Advisor at Judo Bank, noted that PMI remains "firmly in expansionary territory," and pointed to growth at "around the long-term trend rate, if not a touch higher".

However, Hogan warned that weak consumer spending will drag on growth in the first half of the year. Despite this, businesses are still hiring, with the employment index reaching a 6-month high.

Composite input price index hit a 6-month high, with service industry cost pressures rising slightly. Hogan remarked, "This does not suggest a material step down in domestic inflation pressures in Q2."

Additionally, manufacturing input prices hit a one-year high in May, raising doubts about further deflation in domestic goods prices. This has been crucial in bringing inflation below 4% over the past year. Any increase in goods inflation, alongside high service sector inflation, poses a significant concern for RBA, which expects inflation to decrease over the next 18 months.

NZ retail sales up 0.5% in Q1, ending two-year downturn

New Zealand's retail sales volumes rose by 0.5% qoq to NZD 25B in Q1, significantly outperforming the anticipated -0.3% qoq decline. Sales values increased by 0.7% qoq to NZD 30B.

"In the March quarter, we saw a modest increase in retail activity, with growth across most industries," said Melissa McKenzie, business financial statistics manager. "This followed two years of declines."

Of the 15 retail industries, nine experienced higher sales volumes during the quarter. The most notable contributions came from food and beverage services, which rose by 2.2%, motor vehicle and parts retailing, which increased by 1.1%, recreational goods retailing, which surged by 4.7%, and accommodation, which climbed by 4.1%.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2691; (P) 1.2726; (R1) 1.2753; More...

Intraday bias in GBP/USD stays neutral for the moment. On the upside. decisive break of 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780 will extend the rally from 1.2298 to 1.2892 resistance next. However, break of 1.2685 will minor support will turn bias back to the downside, for retreat to 55 4H EMA (now at 1.2661) and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351 (2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q1 | 0.50% | -0.30% | -1.90% | -1.80% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q1 | 0.40% | 0.00% | -1.70% | -1.60% |

| 23:00 | AUD | Manufacturing PMI May P | 49.6 | 49.6 | ||

| 23:00 | AUD | Services PMI May P | 53.1 | 53.6 | ||

| 00:30 | JPY | Manufacturing PMI May P | 50.5 | 49.7 | 49.6 | |

| 00:30 | JPY | Services PMI May P | 53.6 | 54.3 | ||

| 01:00 | AUD | Consumer Inflation Expectations May | 4.10% | 4.60% | ||

| 07:15 | EUR | France Manufacturing PMI May P | 46.7 | 45.5 | 45.3 | |

| 07:15 | EUR | France Services PMI May P | 49.4 | 51.5 | 51.3 | |

| 07:30 | EUR | Germany Manufacturing PMI May P | 45.4 | 43.5 | 42.5 | |

| 07:30 | EUR | Germany Services PMI May P | 53.9 | 53.5 | 53.2 | |

| 08:00 | EUR | Eurozone Manufacturing PMI May P | 47.4 | 46.6 | 45.7 | |

| 08:00 | EUR | Eurozone Services PMI May P | 53.3 | 53.5 | 53.3 | |

| 08:30 | GBP | Manufacturing PMI May P | 51.3 | 49.2 | 49.1 | |

| 08:30 | GBP | Services PMI May P | 52.9 | 54.8 | 55 | |

| 12:30 | USD | Initial Jobless Claims (May 17) | 215K | 220K | 222K | 223K |

| 13:45 | USD | Manufacturing PMI May P | 50.1 | 50 | ||

| 13:45 | USD | Services PMI May P | 51.5 | 51.3 | ||

| 14:00 | USD | New Home Sales Apr | 674K | 693K | ||

| 14:00 | EUR | Eurozone Consumer Confidence May P | -14 | -15 | ||

| 14:30 | USD | Natural Gas Storage | 84B | 70B |

US initial jobless claims falls to 215k, vs exp 220k

US initial jobless claims fell -8k to 215k in the week ending May 18, below expectation of 220k. Four-week moving average rose 2k to 220k.

Continuing claims rose 8k to 1794k in the week ending May 11. Four-week moving average of continuing claims rose 5k to 1782k.