Sample Category Title

Sunset Market Commentary

Markets:

Trading was again confined to rather tight ranges today. US yields created some breathing space end last week compared to important support levels (4.7% area US 2-y yield, 4.3/37% area 10-y yield), but for now follow-through gains look rather difficult. Eco were few today, but there were interesting comments from Fed governors. Fed’s Waller at least isn’t impressed by recent ‘softer’ data. He admitted that further rate hikes are probably unnecessary. Prices are not accelerating any further and progress toward to the 2% target has likely resumed. In the absence of a significant weakening of the labour market, Waller indicated he still needs several months of good inflation data before feeling comfortable on supporting an easing in the stance of monetary policy. More or less at the same time, Atlanta Fed Bostic also said he expects inflation to decline slowly which will probably allow the Fed only to start cutting rates in Q4. He also said that rates are restrictive, but efficacy could be lower as the Fed is making up its mind on the long term neutral rate. Both the comments of Waller and Bostic pushed US yields higher in a first reaction, but these didn’t last. On the contrary, US yields are ceding between 2.5 bps (2-y) and 4 bps (30-y). Admittedly at different levels, but graphs currently even suggest that the downside in EMU/German yields even might be a bit more solid, with the ECB Q1 negotiated wage data an PMI’s later this week potentially providing some further guidance. German yields decline 2-3 bps across the curve. A mild bond market climate this time doesn’t help any further equity gains. The Eurostoxx is falling prey to profit taking (-0.85%). US equities also show some hesitation after touching new record levels last week (S&P 500, -0.1%)) or yesterday (Nasdaq today-0.35%).

Today’s market set-up (lower yields but at the same time also softer equities) doesn’t really help the dollar. DXY gains marginally (104.6) as does USD/JPY (156.3). EUR/USD tried to regain some ground earlier this morning but couldn’t maintain the intraday momentum (unchanged near EUR/USD 1.0855). For now sterling easily keeps recent gains against the dollar (GBP 1.271) and the euro (EUR/GBP 0.8545). CBI May data on manufacturing were mixed at best. Expected production rebounded, but inventories are high, orders’ growth contracted at the fastest pace since November and expected growth of selling prices eased more than expected. CBI data often have only a limited impact on markets. However, comments from BoE governor Bailey later today and tomorrow’s April CPI data for sure are able to move the market. We see risks for UK interest rate markets to more toward a more ECB like scenario (first cut in June) if the April CPI drops close to 2%. This might also cap recent sterling outperformance.

News & Views

Canadian inflation slowed slightly in April, from 0.6% M/M to 0.5% M/M (in line with consensus). The Y/Y-pace decelerated from 2.9% to 2.7%, the lowest since March 2021. The broad-based slowdown was driven by food prices (-0.2% M/M & +2.3% Y/Y), services (+0.2% M/M & +4.2% Y/Y) and durable goods (-0.3% M/M & -0.8% Y/Y). Gasoline prices rose 7.9% M/M and 6.1% Y/Y. Shelter costs continued to contribute positively (+0.5% M/M & +6.4% Y/Y). The Bank of Canda’s preferred core inflation gauge (trimmed mean) slowed from 3.2% Y/Y to 2.9% Y/Y in April, but the 3-month annualized pace reaccelerated for the first time since December (1.64% from 1.35% according to Bloomberg calculations). It’s unclear whether today’s report is sufficient for the Bank of Canada to tick the box of further sustained easing in core inflation (key condition to shift to an easier policy) at its June policy meeting. The market implied probability of a rate cut is 60%, but we don’t see the BoC moving (way) in advance of the Fed. The Loonie loses some ground against the greenback today, trading at USD/CAD 1.3660 from 1.3620.

The National Bank of Hungary cut its policy rate as expected by 50 bps from 7.75% to 7.25%. The decision was unanimous. Looking ahead, risks surrounding global and domestic inflation and volatility in international investor sentiment warrant a careful and patient approach. The decline in Hungarian core inflation will stop in Q2 and it will fluctuate between 4.5% and 5% in the remainder of the year. Decisions on any further reductions in the base rate will be taken in a cautious and data-driven manner. MNB vice-governor Virag at the press conference suggested a final rate 25 bps or 50 bps rate cut at the June meeting but afterwards, the room for more rate cuts is very, very limited. The Hungarian forint rose to EUR/HUF 385 after the policy decision, the strongest HUF-level since early February

Graphs

USD/CAD: Loonie eases as Canadian inflation moderates further. The jury is still out on the timing of first BoC rate cut

EUR/HUF: forint holding strong as MNB will end rate cuts after June as core inflation is expected to hold near 4.5%-5%.

Dow Jones: US equity rally slows after touching record levels last week/yesterday.

US 2-y yield (for now) fails to extend rebound off key support levels touched last week.

Fed’s Waller: Several months of data needed before supporting rate cuts

Fed Governor Christopher Waller emphasized in a speech today that "several more months" of favorable inflation data are necessary before he would consider supporting interest rate cuts.

While the latest CPI data was a "reassuring signal" indicating that inflation is not accelerating, Waller noted that the progress shown was "small."

Waller highlighted that current data on spending and labor market suggest that monetary policy is at an "appropriate setting" to exert downward pressure on inflation.

However, "in the absence of a significant weakening in the labor market, I need to see several more months of good inflation data before I would be comfortable supporting an easing in the stance of monetary policy," he said.

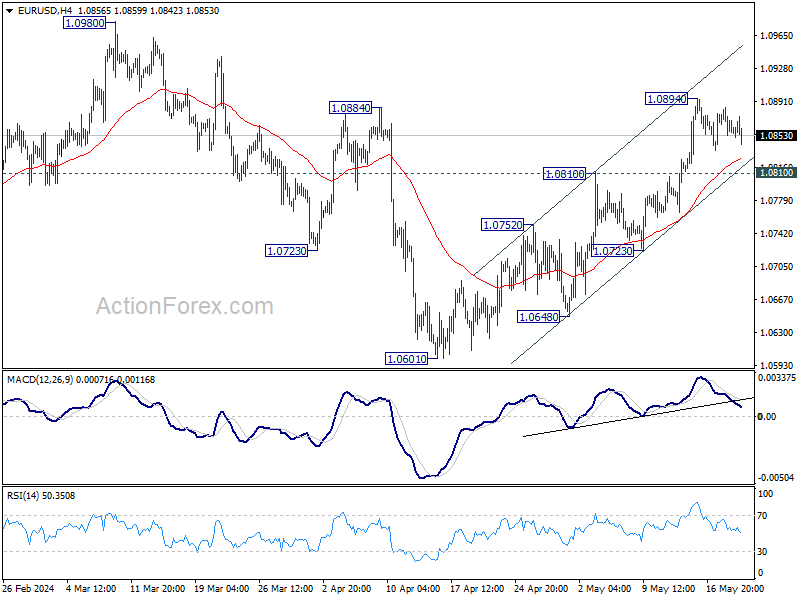

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0846; (P) 1.0865; (R1) 1.0877; More...

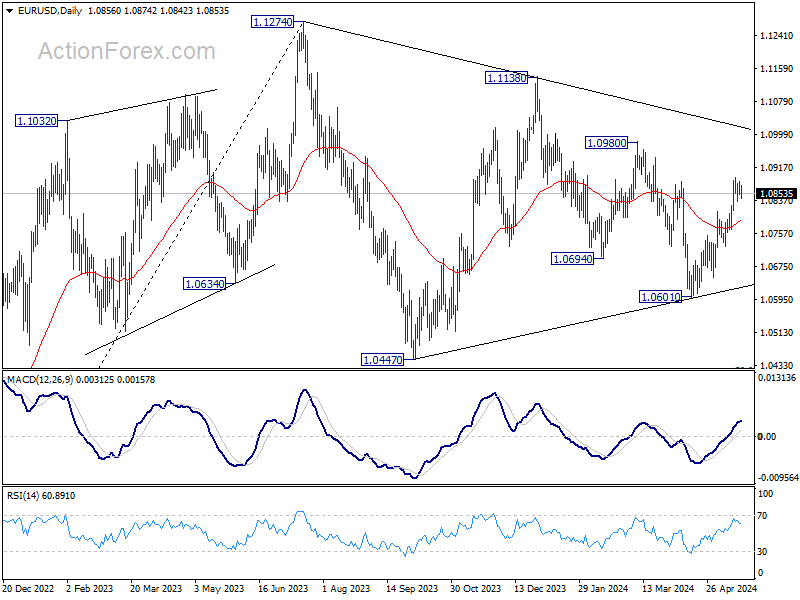

EUR/USD is still bounded in consolidations below 1.0894 and intraday bias stays neutral. Further rally is expected as long as 1.0810 resistance turned support holds. Break of 1.0894 will resume the rise to 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed at 1.0601 already.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

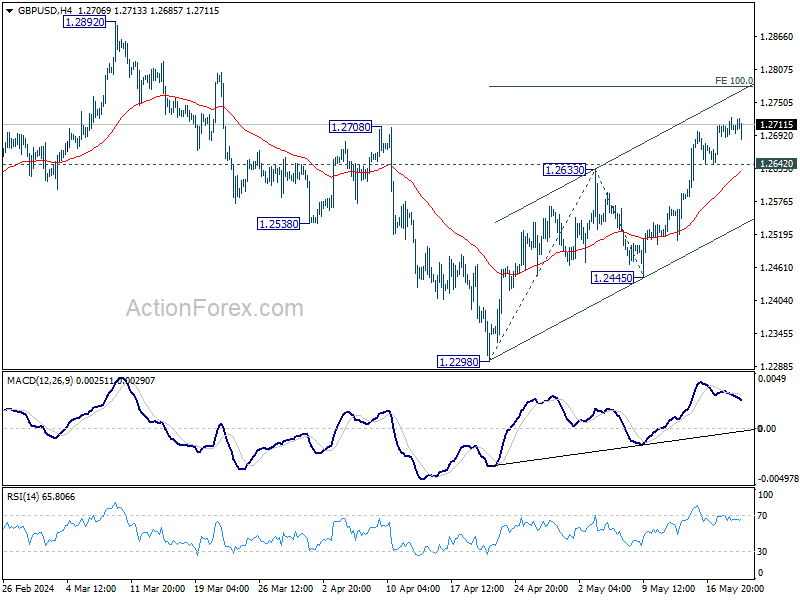

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2687; (P) 1.2707; (R1) 1.2725; More...

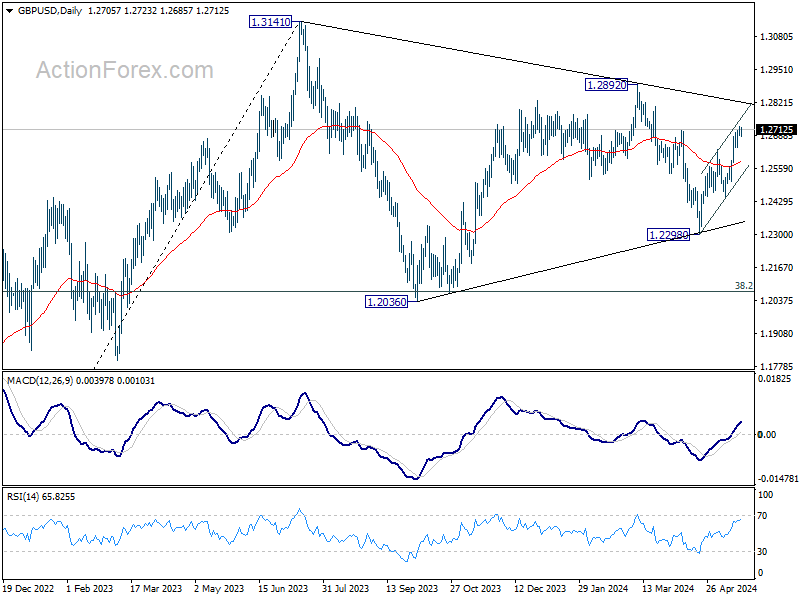

Intraday bias in GBP/USD remains on the upside at this point. Rise from 1.2298 would target 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780. On the downside, below 1.2642 minor support will turn intraday bias neutral again. But further rise will now remain in favor as long as 1.2445 support holds, in case of retreat.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

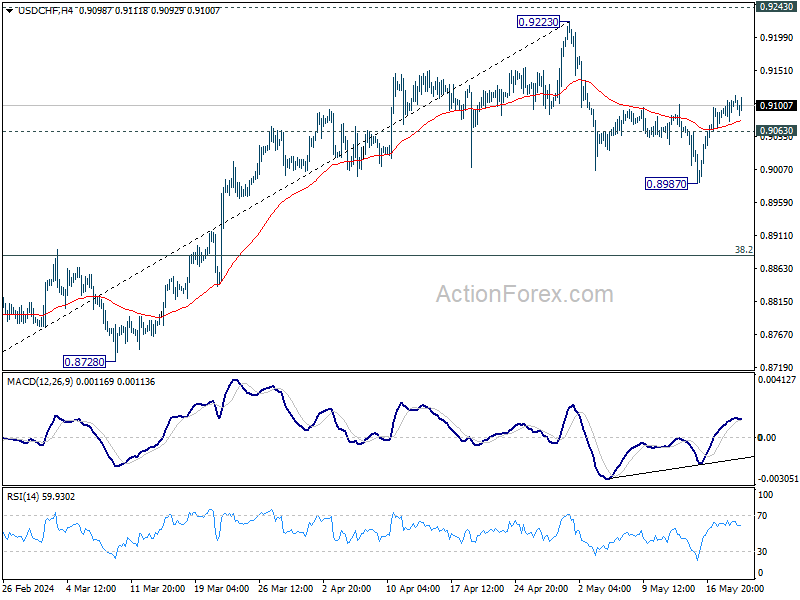

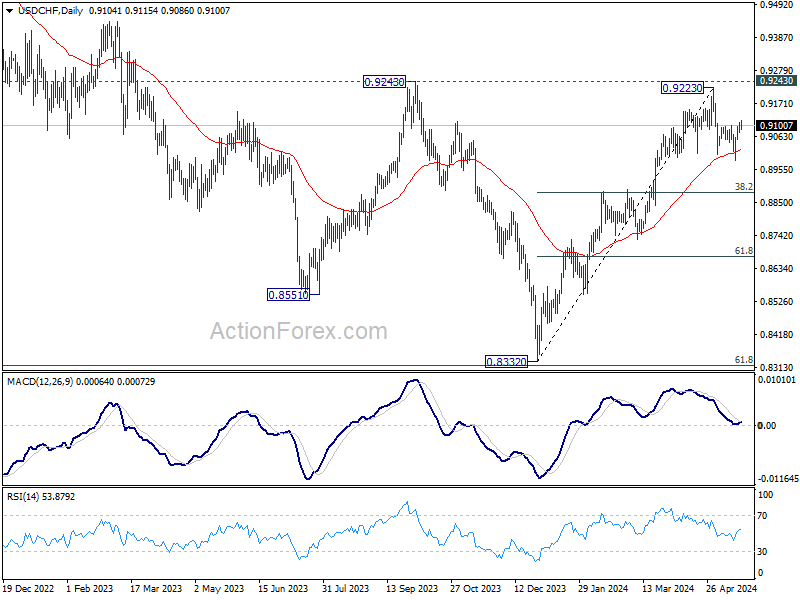

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9087; (P) 0.9098; (R1) 0.9118; More....

Intraday bias in USD/CHF stays mildly on the upside at this point. Corrective fall from 0.9223 might have completed with three waves down to 0.8987 already. Further rally should be seen back to retest 0.9223. On the downside, below 0.9063 minor support is turned neutral first. Further break of 0.8987 will resume the fall from 0.9223 to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

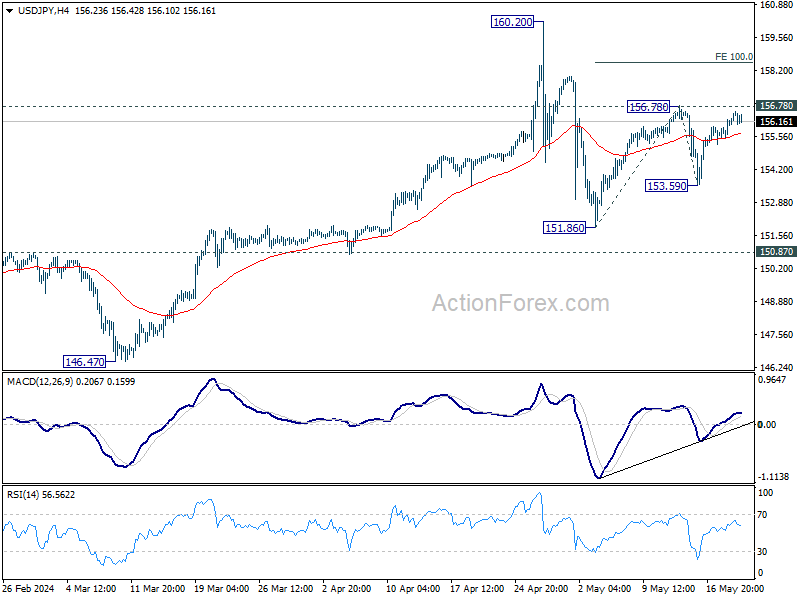

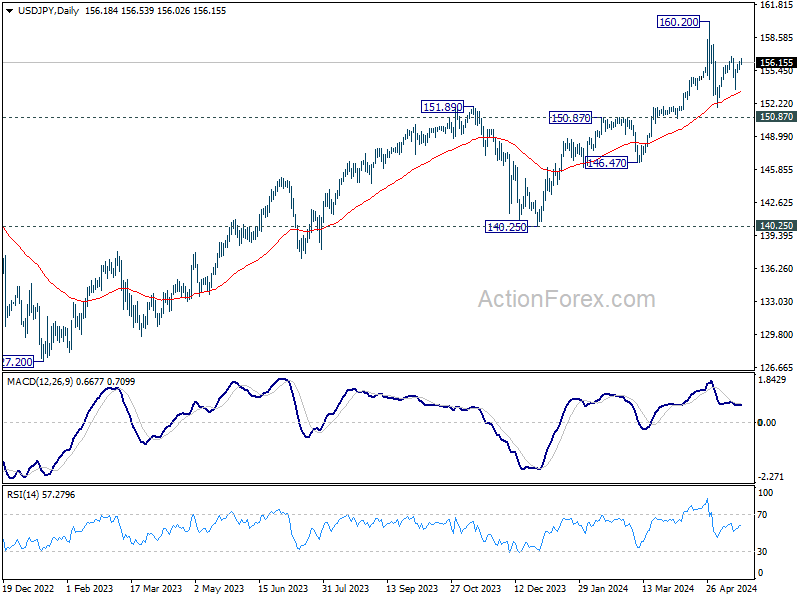

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.75; (P) 156.03; (R1) 156.56; More...

Outlook in USD/JPY is unchanged and intraday bias stays neutral. Price actions from 160.20 are seen as a corrective pattern. On the upside, break of 156.78 will resume the rise from 151.86, as the second leg, to 100% projection of 151.86 to 156.78 from 153.59 at 158.51. On the downside, below 153.59 will target 151.86 and below as the third leg.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Canada: Inflation Cools Further in April

Headline CPI inflation edged lower in April to 2.7% year-on-year (y/y), matching expectations. The broad-based deceleration was led by food prices, services and durable goods.

However, higher prices at the pump in April worked against the cooling in inflation. Gasoline prices were up 6.1% versus a year ago, up from 4.5% in March. But it wasn't entirely due to the increase in the federal carbon levy. Statistics Canada cited that higher oil prices and the switch to summer blends were also factors lifting prices at the pump. Excluding gasoline, all-items CPI slowed to 2.5% y/y in April, down from 2.8% in March.

Goods inflation as a whole continued to slow, up only 1% y/y in April, as prices for durable goods (like furniture and appliances) are in deflation, down 0.8% y/y. Consumers are also seeing lower inflation for food, which is at 2.3% y/y in April, down from a peak of 10% last year.

Shelter inflation has been a thorn in the Bank of Canada's side, but it took a small step in the right direction in April, up 6.4% y/y, down a tenth from March. Rent inflation cooled slightly to 8.2% y/y as did mortgage interest costs, which remain high at 24.5% y/y. Leaning against these increases, homeowner's replacement cost is down 0.9% versus a year ago. CPI ex-shelter was up only 1.2% y/y on April.

In other good news, the Bank of Canada's preferred "core" inflation measures continued to make progress towards the 2% target in April. The average of the Bank's median and trim measures was 2.8% y/y in April, down from 3.1% in March. The three and six month annualized pace of core inflation – at 1.6% and 2.4% - continue to point to a lower year-on-year pace of price growth going forward.

Key Implications

April was another month of good news on Canadian inflation. The BoC's preferred inflation gauges moved into the 1-3% target range for the first time in nearly three years. However, at 2.8% it is still close to the top of the BoC's range, and we expect the bank will want to see a bit more confirmation before taking rates lower and lean towards a July cut.

However, markets have found today's inflation number a bit more reassuring, and have increased the odds of a June cut to better than 50-50. But June or July, Canadians can be increasingly confident that alongside lower inflation, interest rates are headed lower soon.

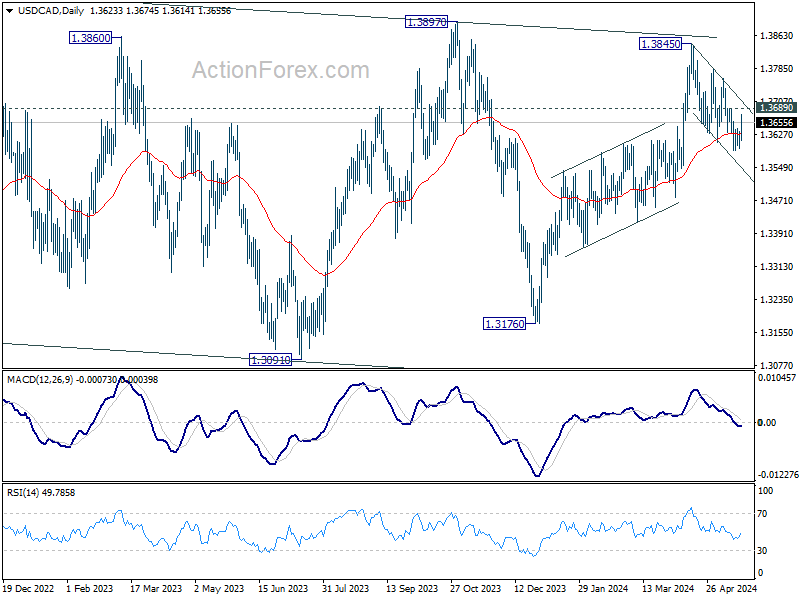

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3602; (P) 1.3618; (R1) 1.3641; More...

USD/CAD recovered notably today but stays below 1.3689 resistance. Intraday bias stays neutral first. Strong bounce from current level will confirm support by 55 D EMA (now at 1.3628). Break of 1.3689 minor resistance will argue that correction from 1.3845 has completed, and bring stronger rally to 1.3761 resistance. However, sustained break of 55 D EMA will argue that whole rise from 1.3176 has completed already, and turn outlook bearish.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

CAD Sinks after CPI, NZD Await RBNZ

Canadian Dollar sees a broad decline in early US session due to growing speculation about rate cut by BoC in the near future. April's headline CPI slowed as expected, despite a significant increase in gasoline prices. Core inflation measures also showed more progress in disinflation than anticipated. While it remains uncertain if this progress will be enough to prompt BoC to ease policy at next meeting, speculation is likely to intensify ahead of June 5 meeting.

Meanwhile, New Zealand Dollar followed Loonie as the second weakest performer of the day. Attention is now turning to RBNZ rate decision scheduled for tomorrow, with most market participants expecting the central bank to hold the rate steady at 5.50%. While many analysts see November as the likely timing for the first rate cut, this view is not universally held. The upcoming OCR forecasts from RBNZ will be closely scrutinized, particularly to see if they adjust to remove the possibility of another rate hike. However, it remains uncertain whether RBNZ will move up the timeline for the first rate cut from next year.

Elsewhere in the currency markets, Dollar is currently the third weakest. Swiss Franc has emerged as the strongest performer, followed the British Pound and Australian Dollar. Euro and Japanese Yen are positioned in the middle of the performance spectrum.

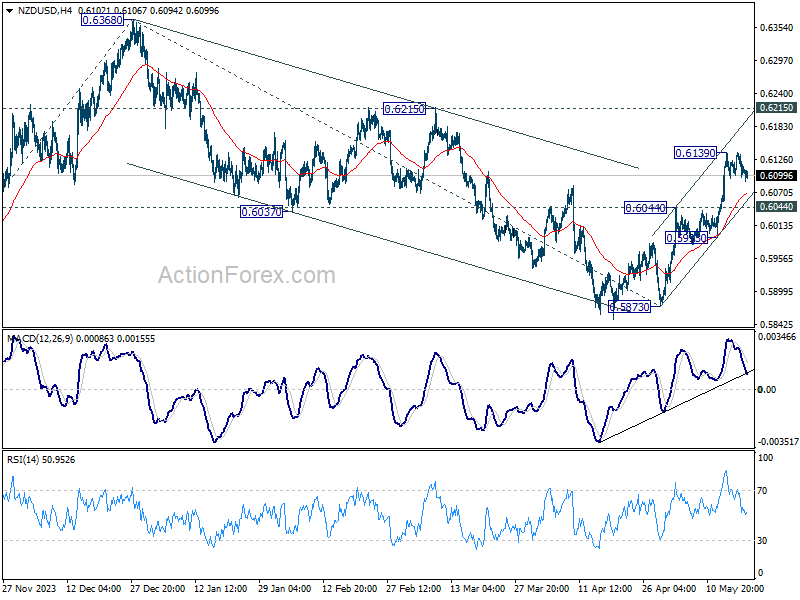

Technically, NZD/USD turned sideway after rebounding to 0.6139, but the retreat is so far shallow. Further rise is expected as long as 0.6044 resistance turned support holds. Above 0.6139 will resume the rally from 0.5873 to 0.6215 resistance. Decisive break there should confirm that whole corrective fall from 0.6368 has completed at 0.5873 already, and bring retest of 0.6368 next.

In Europe, at the time of writing, FTSE is down -0.42%. DAX is down -0.53%. CAC is down -1.06%. UK 10-year yield is down -0.029 at 4.147. Germany 10-year yield is down -0.0168 at 2.518. Earlier in Asia, Nikkei fell -0.31%. Hong Kong HSI fell -2.12%. China Shanghai SSE fell -0.42%. Singapore Strait Times fell -0.19%. Japan 10-year JGB yield rose 0.0051 to 0.985.

Canada's CPI falls to 2.7% in Apr, matches expectations

Canada's CPI slowed from 2.9% yoy to 2.7% yoy in April, matched expectations. Ex-gasoline, CPI slowed from 2.8% yoy to 2.5% yoy. Gasoline prices accelerated from 4.5% yoy to 6.1% yoy. Food prices slowed from 1.9% yoy to 1.4% yoy. On a monthly basis CPI rose 0.5% mom, matched expectations.

Looking at the core measures, CPI median slowed from 2.9% yoy to 2.6% yoy, below expectation of 2.7% yoy. CPI trimmed slowed from 3.2% yoy to 2.9% yoy, matched expectations. CPI common slowed from 2.9% yoy to 2.6% yoy, below expectation of 2.8% yoy.

IMF recommends BoE cut rates by 50-75 bps in 2024

IMF issued a report today suggesting that with UK inflation currently 2% above its neutral rate estimate, BoE should consider moving towards monetary easing.

IMF highlighted the risks of "delayed easing", cautioning that while BoE emphasizes the need to wait for clearer signs of reduced inflation persistence, holding off too long could be detrimental.

Additionally, keeping the Bank Rate unchanged as inflation and inflation expectations decrease would "raise ex-post real rates", which could hinder or even reverse the economic recovery. This scenario might lead to "extended undershooting of the inflation target".

To address these concerns, IMF recommends that BoE implement rate cuts totaling 50-75 basis points in 2024. This would help balance the risks of premature easing against the need to support economic growth and ensure inflation remains on target.

Eurozone goods exports down -9.2% yoy in Mar, imports down -12.0% yoy

Eurozone goods exports fell -9.2% yoy to EUR 245.5B in March. Goods imports fell -12.0% yoy to EUR 221.3B. Trade balance recorded EUR 24.1B surplus. Intra-Eurozone trade fell -12.4% yoy to EUR 222.1B.

In seasonally adjusted term, goods exports rose 0.1% mom to EUR 237.7B. Goods imports fell -0.1% mom to EUR 220.4B. Trade surplus widened slightly from EUR 16.7B to 17.3B. Intra-Eurozone trade fell -0.5% mom to EUR 213.7B.

RBA minutes highlight debate over rate hike

RBA minutes from May 7 meeting reveal that a rate hike was considered but ultimately, the decision was made to hold cash rate target steady at 4.35%. The board emphasized that recent data indicated that "risks around inflation had risen somewhat," acknowledging the considerable uncertainty and the difficulty in "ruling in or ruling out" future changes in interest rate.

The minutes detailed that raising the cash rate could be appropriate if the board believed that the staff forecasts were "overly optimistic" about the forces driving down inflation, leaving the balance of risks tilted to the upside. Additionally, a higher cash rate might be necessary even with ongoing weakness in aggregate demand if "other factors slowed the pace of disinflation."

Conversely, the decision to hold the cash rate steady was based on the view that, although there had been significant updates on the economy since the last meeting, these updates were "not sufficient to warrant a change in the stance of monetary policy." Inflation was still declining towards the target, and the new information "did not materially alter its trajectory."

Australian Westpac consumer sentiment falls -0.3% mom amid budget disappointment

Australia Westpac Consumer Sentiment index fell by -0.3% mom to 82.2 in May. Westpac highlighted that the primary takeaways from the May survey are "no let-up in the weak consumer environment" and the cautious mindset of consumers. Consumers are more inclined to use funds from fiscal measures to repair their finances rather than go on spending sprees, which aligns with RBA's efforts to bring inflation back to target.

The May survey, conducted during budget week, provided a clear comparison of sentiment before and after the budget announcement. Sentiment among those surveyed before the budget was relatively optimistic, with an index reading of 86.8, marking a 5.3% increase from April. However, sentiment plummeted to 76.6 after the budget announcement, reflecting a 7% decline from April. This -11.8% drop in sentiment post-budget contrasts with a -7.4% decline observed last year.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3602; (P) 1.3618; (R1) 1.3641; More...

USD/CAD recovered notably today but stays below 1.3689 resistance. Intraday bias stays neutral first. Strong bounce from current level will confirm support by 55 D EMA (now at 1.3628). Break of 1.3689 minor resistance will argue that correction from 1.3845 has completed, and bring stronger rally to 1.3761 resistance. However, sustained break of 55 D EMA will argue that whole rise from 1.3176 has completed already, and turn outlook bearish.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence May | -0.30% | -2.40% | ||

| 01:30 | AUD | RBA Minutes | ||||

| 06:00 | EUR | Germany PPI M/M Apr | 0.20% | 0.10% | 0.20% | |

| 06:00 | EUR | Germany PPI Y/Y Apr | -3.30% | -3.20% | -2.90% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Mar | 35.8B | 30.2B | 29.5B | 28.9B |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | 17.3B | 19.9B | 17.9B | 16.7B |

| 12:30 | CAD | CPI M/M Apr | 0.50% | 0.50% | 0.60% | |

| 12:30 | CAD | CPI Y/Y Apr | 2.70% | 2.70% | 2.90% | |

| 12:30 | CAD | CPI Median Y/Y Apr | 2.60% | 2.70% | 2.80% | 2.90% |

| 12:30 | CAD | CPI Trimmed Y/Y Apr | 2.90% | 2.90% | 3.10% | |

| 12:30 | CAD | CPI Common Y/Y Apr | 2.60% | 2.80% | 2.90% |

NZD/USD Steady Ahead of RBNZ Rate Announcement

The New Zealand dollar is almost unchanged on Tuesday. NZD/USD is down 0.06%, trading at 0.6102 in the European session at the time of writing.

RBNZ expected to maintain cash rate

The Reserve Bank of New Zealand has shown it can be patient, having held the cash rate at 4.35% for six straight times. The central bank is expected to maintain rates yet again at Wednesday’s meeting as inflation has remained stubbornly high.

Inflation has been moving lower and fell to 4% in the first quarter, down from 4.7% in the fourth quarter of 2023. However, this remains double the midpoint of the 1-3% target range and is too high for the RBNZ to start trimming rates in the near-term.

At the same time, economic data for the first quarter was soft which should result in disinflation. The unemployment rate rose to 4.3% in the first quarter, private wage growth decelerated and GDP contracted by 0.1% q/q.

The RBNZ had its mandate limited to inflation in December; previously, the central bank was mandated to maintain low inflation and full employment. Still, the strength of the labor market and wage growth will be eyed by the central bank as it determines its rate policy.

The Federal Reserve continues to sound hawkish about rate policy and remains cautious about rate cuts. On Monday, Fed Vice Chair Philip Jefferson said that it was too early to tell if the downtrend in inflation would be “long lasting”. Fed Vice Chair of Supervision Michael Barr said that first-quarter inflation data was disappointing and was not supportive of easing monetary policy. For a second straight day, there are no US economic releases and we’ll hear from a host of FOMC members, which could provide insights about the Fed’s rate policy plans.

NZD/USD Technical

- NZD/USD is tested support at 0.6089 earlier . Below, there is support at 0.6039

- 0.6185 and 0.6235 are the next resistance lines