Sample Category Title

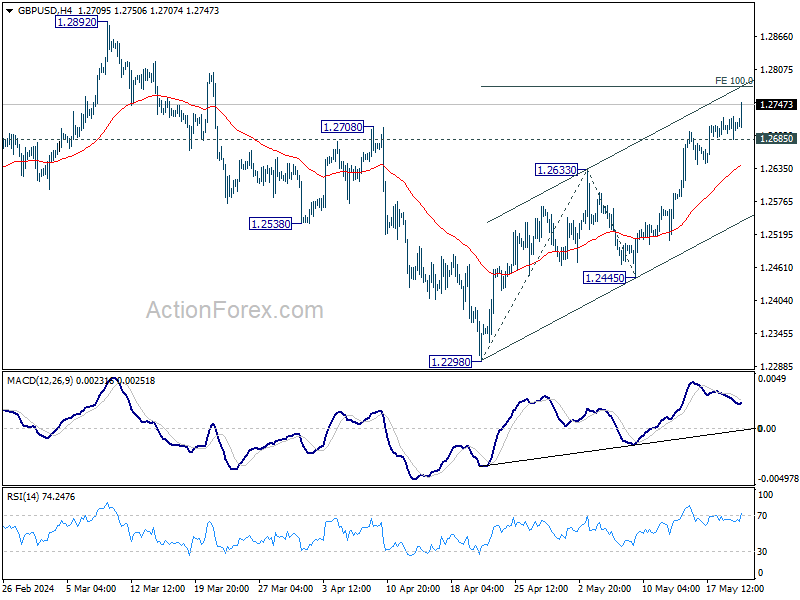

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2689; (P) 1.2708; (R1) 1.2729; More...

GBP/USD's rally from 1.2298 continues today and intraday bias stays on the upside. Further rally should be seen to 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780. Firm break there will target 1.2892 resistance next. On the downside, below 1.2685 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

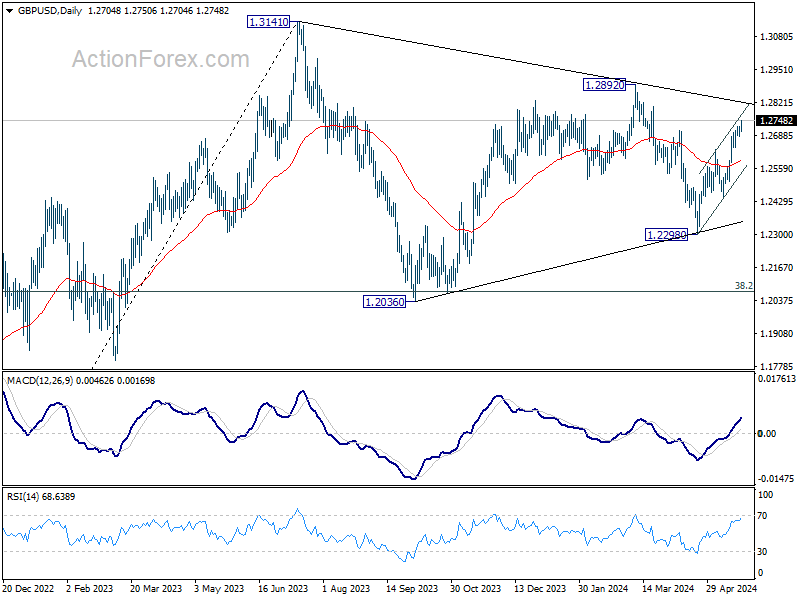

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

UK CPI down to 2.3% in Apr, core CPI falls to 3.9%, both above expectations

UK CPI slowed sharply from 3.2% yoy to 2.3% yoy in April, but above expectation of 2.1% yoy. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 4.2% yoy to 3.9% yoy, above expectation of 3.6% yoy.

CPI goods annual rate turned negative from 0.8% yoy to -0.8% yoy. But CPI services annual rate eased just slightly from 6.0% yoy to 5.9% yoy.

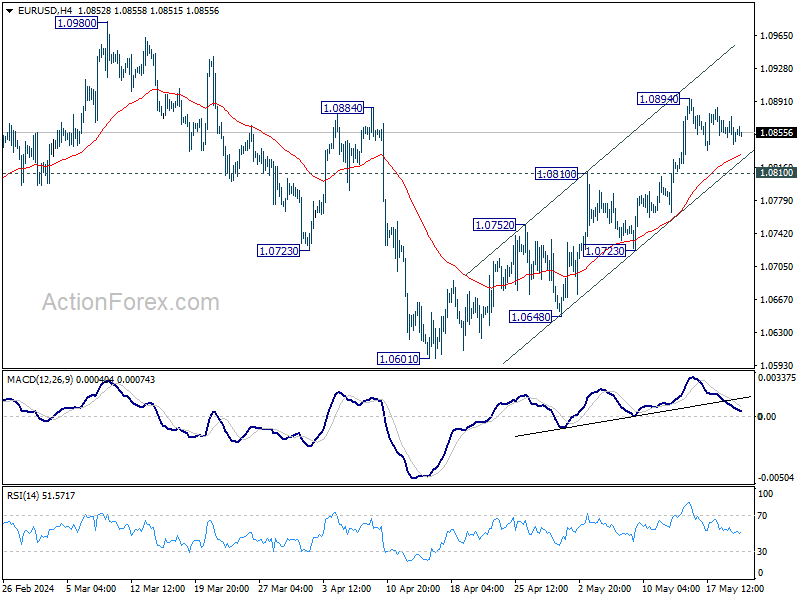

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0840; (P) 1.0857; (R1) 1.0872; More...

Intraday bias in EUR/USD stays neutral and consolidations continue below 1.0894. Further rally is expected as long as 1.0810 resistance turned support holds. Break of 1.0894 will resume the rise to 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed at 1.0601 already.

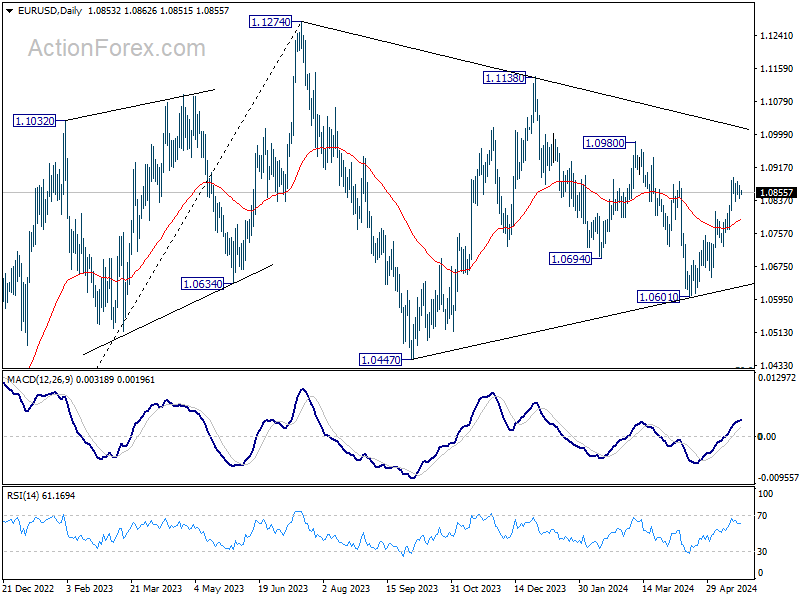

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

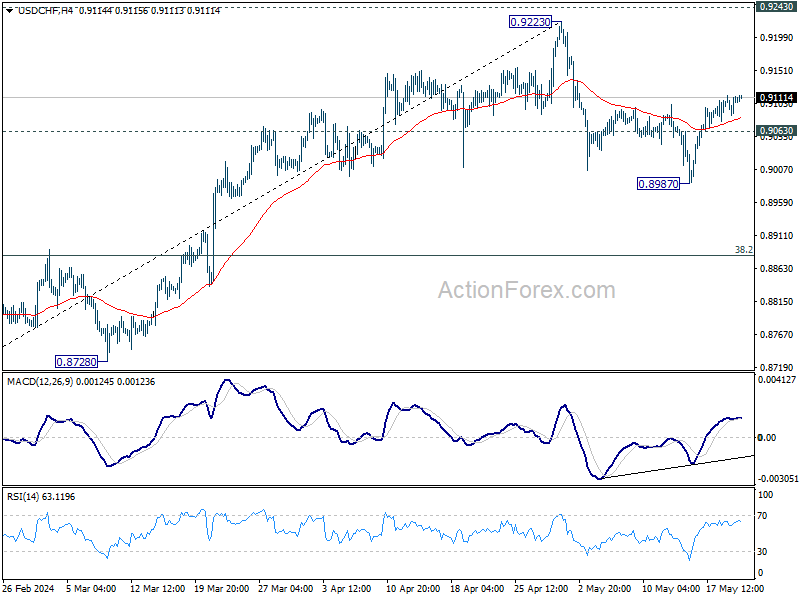

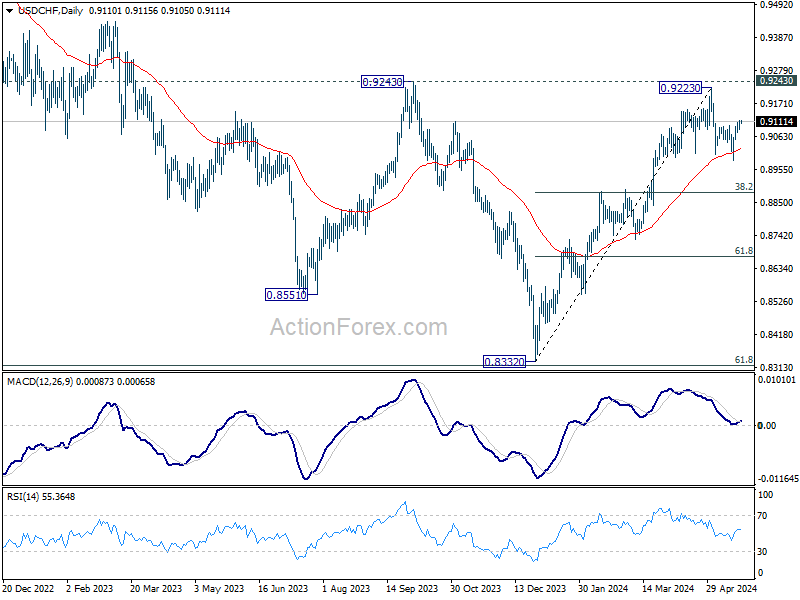

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9092; (P) 0.9104; (R1) 0.9122; More....

Intraday bias in USD/CHF stays mildly on the upside for the moment. Corrective fall from 0.9223 might have completed with three waves down to 0.8987 already. Further rally should be seen back to retest 0.9223. On the downside, below 0.9063 minor support is turned neutral first. Further break of 0.8987 will resume the fall from 0.9223 to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

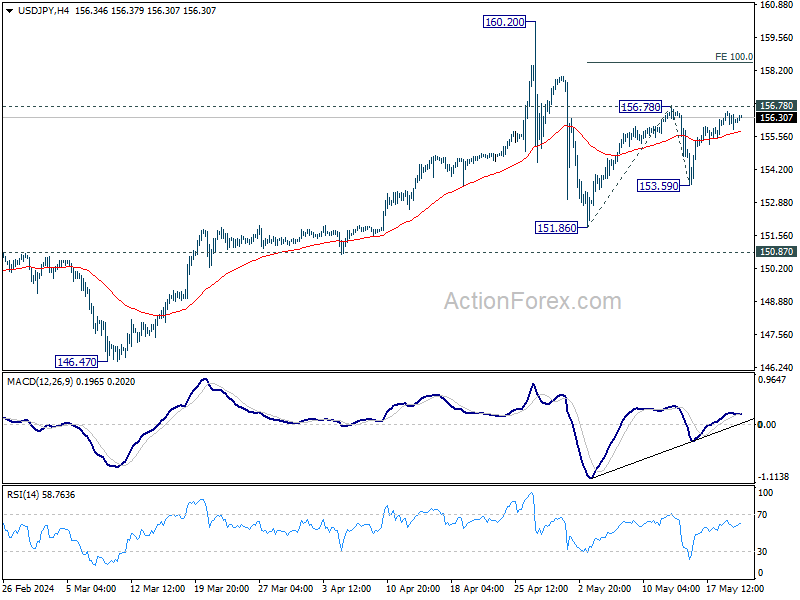

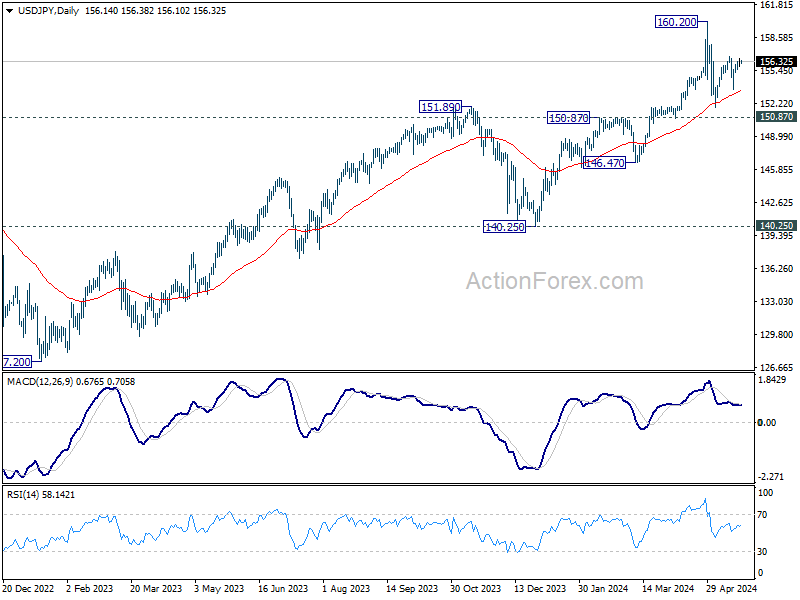

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.75; (P) 156.03; (R1) 156.56; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. Price actions from 160.20 are seen as a corrective pattern. On the upside, break of 156.78 will resume the rise from 151.86, as the second leg, to 100% projection of 151.86 to 156.78 from 153.59 at 158.51. On the downside, below 153.59 will target 151.86 and below as the third leg.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

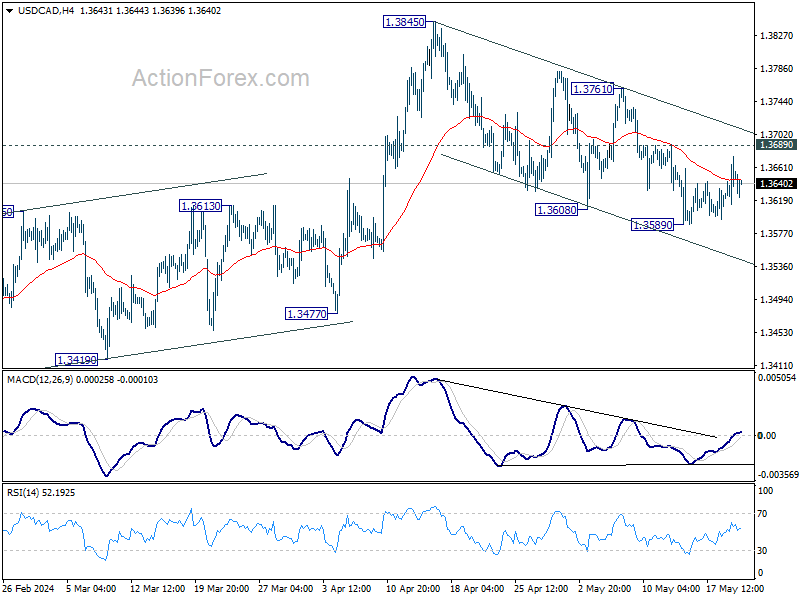

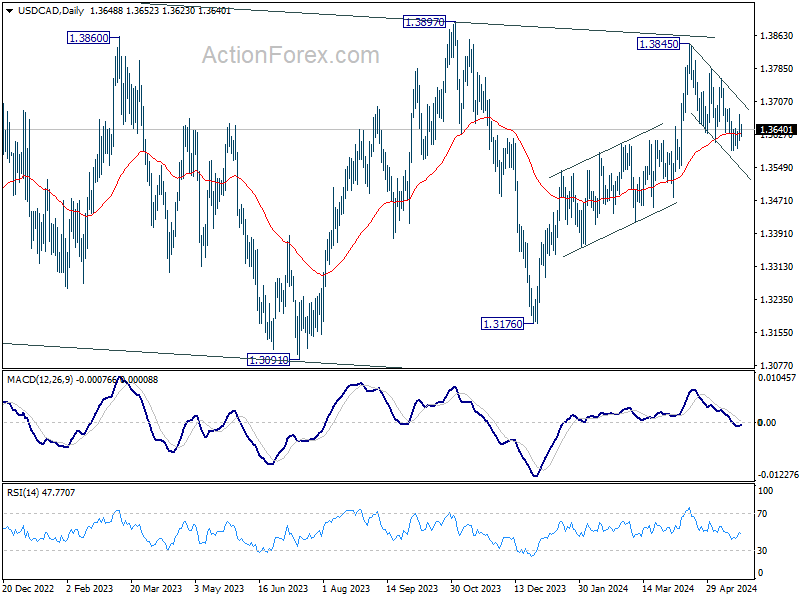

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3621; (P) 1.3648; (R1) 1.3682; More...

Intraday bias in USD/CAD remains neutral for the moment. Strong bounce from current level will confirm support by 55 D EMA (now at 1.3628). Break of 1.3689 minor resistance will argue that correction from 1.3845 has completed, and bring stronger rally to 1.3761 resistance. However, sustained break of 55 D EMA will argue that whole rise from 1.3176 has completed already, and turn outlook bearish.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

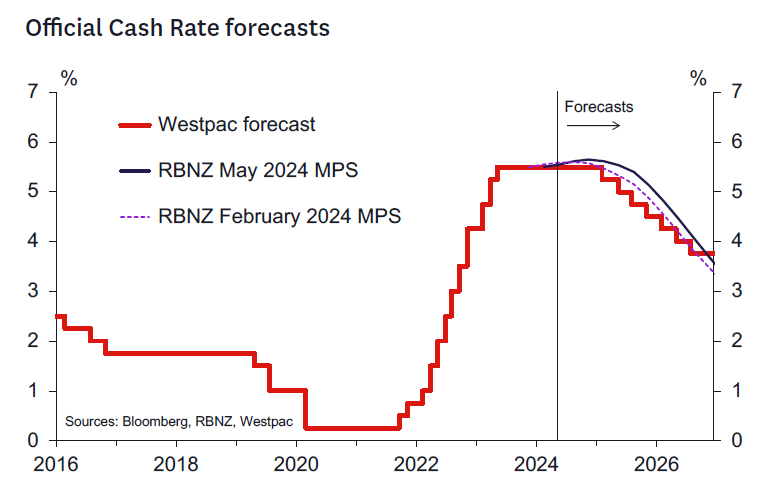

RBNZ Review: Doing the Hard Yards

- The RBNZ left the OCR at 5.5% at its May policy meeting, as was widely expected.

- The RBNZ discussed the possibility of tightening at this meeting but concluded that they retain sufficient confidence to leave the OCR unchanged. Cuts were not discussed.

- The revised projections lifted the OCR track. A first easing is forecast in the August 2025 Monetary Policy Statement, which is pushed out from the previous May 2025 view.

- The track suggests a significant risk of a tightening in the November Statement. This could occur if forecast declines in inflation later in 2024 don't eventuate, but still seems unlikely.

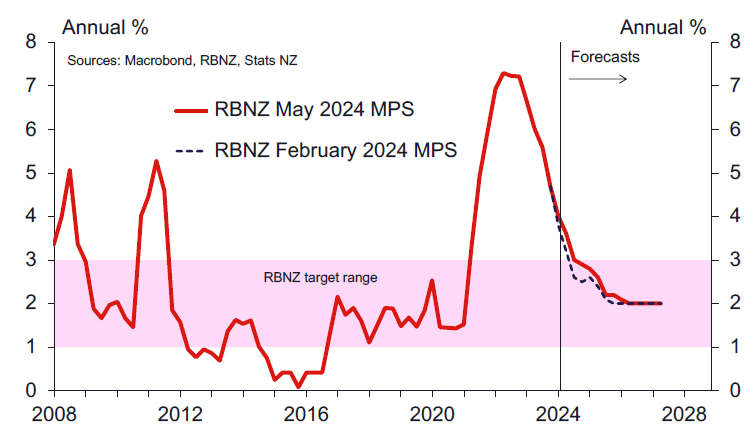

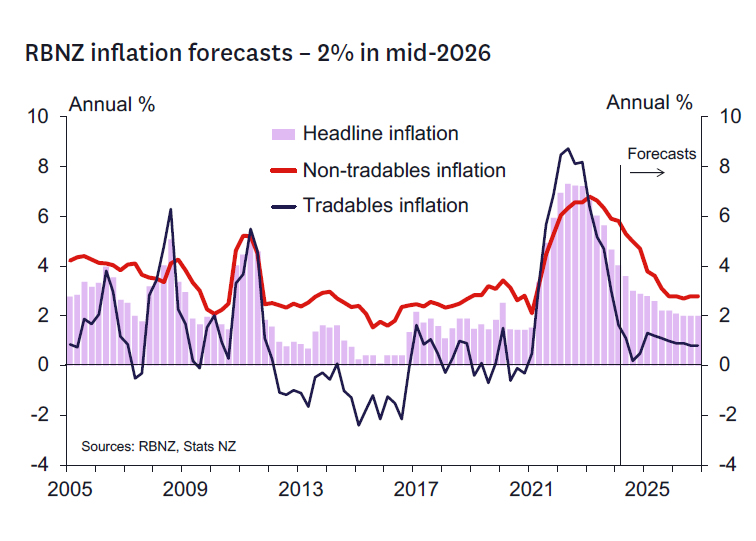

- Inflation is forecast to fall back inside the 1-3% band in Q4 this year, and to return to 2% in Q2 2026. This is another significant revision outward.

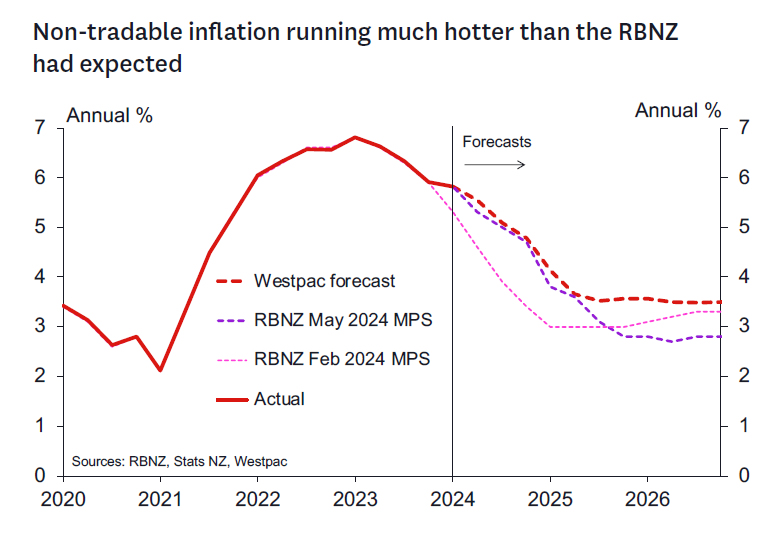

- The RBNZ assesses the risk profile for inflation as lying to the upside in the shorter term and is more balanced over the medium term. The risk profile is decidedly to the upside for nontradables inflation pressures.

- The RBNZ's forecasts for economic growth have been revised down significantly, which helps them retain confidence that inflation will ultimately fall.

- The neutral OCR has been revised up 25bps to 2.75% - this is a driver of longer-term OCR projections.

- Today's RBNZ update leaves us comfortable for now with our forecast of a first policy easing in February next year, followed by only gradual policy easing thereafter. Future inflation data will be key in driving our OCR view with the risk that easing comes later than currently expected.

OCR remains on hold, tightening possible and rates higher for longer.

The RBNZ's May 2024 policy decision and the messages in the accompanying Monetary Policy Statement were surprisingly hawkish.

As polls of analysts had indicated and markets had priced, the OCR was left at 5.5%.

The key area of hawkishness was with respect to the forward profile for the OCR. The RBNZ defied market expectations and revised up their interest rate forecasts. These now incorporate a material risk of a hike in the November Statement, as well as a delay in the timing of the first easing from the May 2025 timeframe assumed in the February Statement to around August 2025 in the current forecasts. The RBNZ continues to maintain that monetary policy will need to remain restrictive for a sustained period to return inflation back inside the target range.

Two key factors are driving the RBNZ to this "higher for longer" position despite a weak domestic economy. Most importantly, the inflation news has not been as supportive as hoped – especially with respect to nontradables inflation. This has led the RBNZ to revise up their inflation forecasts and project a slower decline going forward. Secondly, the RBNZ has revised up its neutral OCR estimate to 2.75%. This latter change has a more significant impact on the RBNZ's longer-term OCR forecasts.

The RBNZ sees near-term upside risks to inflation that reflect the recent stickiness of non-tradable inflation. Further out, the weaker domestic economy and assumed favourable inflation expectations and wage dynamics help them retain confidence that given time inflation will fall to target. But that fall is taking longer than previously thought given the near-term upside surprises. The RBNZ have revised down their economic growth forecasts, but this is balanced by a downgrade in view of the economy's productive potential.

These near-term risks are likely to be important for the policy outlook. The OCR profile peaks at 5.65% in Q4 of 2024. This suggests a material risk of a further tightening in the November Statement (perhaps a 60% or higher chance). We think this raises the stakes of the inflation outturns due between now and November. The RBNZ will need these to significantly moderate to keep the 5.5% OCR peak strategy in place and leave open the prospect of easing in H2 2025. Having said this, the Governor and his staff went to pains to emphasise that these interest rate forecasts could not be taken literally given forecast uncertainties.

CPI inflation taking longer to cool.

The policy outlook above is based on a revised forecast that shows annual CPI inflation falling back inside the 1-3% band in the December quarter of this year – but only just. The RBNZ now forecasts that inflation will end 2024 at a rate of 2.9%. That's in line with our own forecasts but is considerably higher than their previous forecast of 2.5% inflation by the end of this year.

On top of that, the RBNZ now expects that it will take even longer to get inflation back to the 2% target mid-point. The May MPS forecasts don't have inflation back at 2% until mid-2026 (compared to late 2025 in their previous forecasts). That's even with the upward revision to their OCR forecasts.

The key issue for the RBNZ is the persistent strength in domestic inflation, which has surprised to the upside of the RBNZ's assumptions for a year now. The minutes accompanying today's decision noted that "persistence in non-tradable inflation remains a significant upside risk."

Like the RBNZ, we expect that non-tradable inflation will drop back over the course of this year, but only gradually. While inflation in interest rate-sensitive areas of the economy (like the cost of property maintenance) are dropping back, other prices like rents, insurance charges and local council rates have held at firm levels. But although the RBNZ is now factoring in a more gradual easing in those costs, we still think the RBNZ could continue to be surprised to the upside on this front. That would be very important for the RBNZ's stance over the coming quarters.

Balanced against that risk of persistent domestic inflation, imported inflation has fallen well short of the RBNZ's forecasts. We expect that will continue to be the case over the coming year. That will be important for helping to keep inflation expectations anchored in the face of lingering domestic pressures.

Near-term GDP growth forecasts revised down.

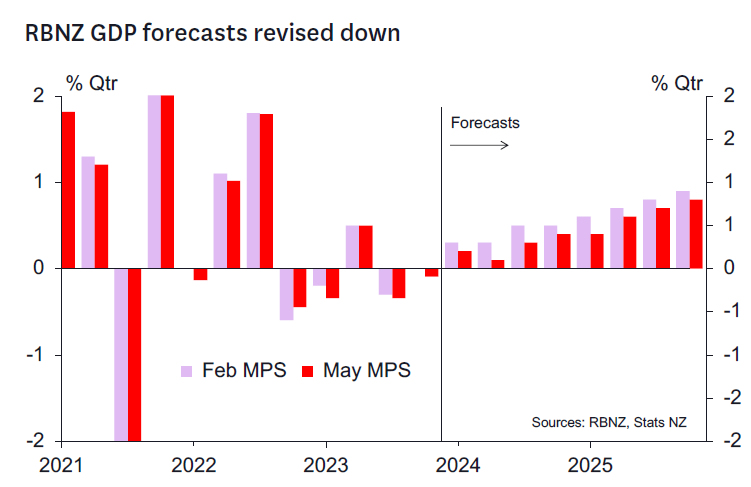

The RBNZ have revised down their forecasts for GDP growth and now expect the economy to grow by 1% in 2024 and 2.4% in 2025 – both down by 0.6% on their previous forecasts.

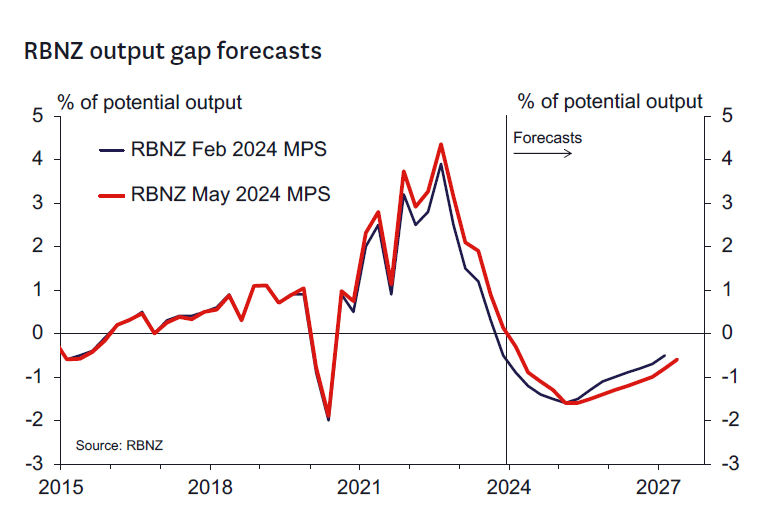

While a downward revision to GDP growth might ordinarily lead to a more negative output gap, on this occasion the RBNZ have revised up their assessment of the positive output gap in recent years. Given the ongoing upward surprises seen in non-tradables inflation, to better explain the inflation that has been seen the RBNZ have revised down their assessment of trend productivity and so have revised up their assessment of the positive output gap seen in recent years. As a result, despite a weaker forecast for GDP growth, the output gap is less negative over the next year than forecast in the February MPS, before turning more negative from the second half of 2025.

RBNZ takes more hawkish stance regarding impact of fiscal policy.

It is worth noting that the RBNZ's forecast for government expenditure in the projections is based on the Treasury's Half Year Economic and Fiscal Update (HYEFU) 2023. And while that has not changed since the February MPS, the RBNZ notes that due to downward revisions to potential output growth, government expenditure is higher as a proportion of potential output than projected previously. In the RBNZ's judgement, this makes the forecast decline in spending less disinflationary than was projected previously.

RBNZ policymakers also discussed the implications of the publicly announced aspects of Budget 2024. While the net impact on aggregate spending is expected to be broadly neutral over an extended horizon, the RBNZ raised the possibility that timing differences associated with reactions to changes in government spending and tax cuts might pose an upside risk to aggregate demand. That is, the RBNZ posed the possibility that reductions in government spending to date (albeit those mainly initiated by the previous government) may already be reflected in the soft high frequency indicators for GDP growth seen in recent months – which the RBNZ has taken onboard in downgrading its forecasts – whereas impending tax cuts may not yet be factored into spending decisions. This assessment seems debateable as it might also be reasonable to think that most of the new Government's spending cuts are yet to take effect, while tax cuts have been equally well foreshadowed and so may also already be underpinning spending for those households that are not cash constrained. The data will ultimately tell the tale.

We will have more to say about our view regarding the impact of fiscal policy next week in our coverage of Budget 2024.

Westpac's view: Doing the hard yards.

The overall messaging from the RBNZ today was very much consistent with that in our recently updated Economic Overview – that is, there are still "hard yards" to be done to bring annual CPI inflation down to the 2% target midpoint in a timely and sustainable manner, and thus monetary policy easing remains unlikely this year. Our baseline view remains that the first 25bp policy easing will occur in February next year, to be followed by a series of gradual (once a quarter) 25bp reductions that will eventually lower the OCR to around 3.75% in 2026.

The key surprise we took from this Statement is that it seems to take risks of an early rate cut off the table. Recent activity data has been weak (although not really much weaker than our forecasts) which has driven speculation that the RBNZ might be ready to adopt a dovish tilt. There is no sign of this here. Rather, any easing prospect has been pushed out further into the future.

We now find a large gap between our own OCR forecast of an easing in February 2025 and the RBNZ's August 2025 view even though our inflation forecasts are fairly similar this year and somewhat more pessimistic on how fast inflation will fall over 2025. There is some risk that our February 2025 OCR cut may prove too optimistic. We will make an assessment on this on review of the Q2 CPI in July and the RBNZ's updated view in the August Statement.

Upcoming key events.

Looking ahead, the following are the key domestic events and data releases that will help shape views ahead of the next two RBNZ policy reviews on 10 July and 14 August.

- Budget 2024, 30 May: The full details of Budget 2024 will be incorporated formally into the updated projections that the RBNZ will publish in the 14 August MPS. While Budget 2024 will provide details regarding spending levels and policy specifics (such as the size of the tax cuts), there will still be uncertainty about how the RBNZ will assess the economic impact (for example, the assumption the RBNZ makes about how much of any tax cut is saved).

- GDP (March quarter), 20 June: The GDP report will have an important bearing on the RBNZ's assessment of the economy's momentum and how the output gap is evolving.

- QSBO Business Survey (June quarter), 2 July: This survey contains a rich set of key capacity and inflation indicators and will be the final major data release ahead of the July review.

- CPI (June quarter), 17 July: The RBNZ will be looking for signs that inflation is on track to move back inside the target range this year and that the substantial upside surprise seen in non-tradables inflation in the March quarter has not continued.

- Labour market surveys (June quarter), 7 August: The RBNZ will looking for signs of a further easing of pressures in the labour market, including a further rise in the unemployment rate and confirmation that labour cost inflation is now on a clear downward trend.

- RBNZ Survey of Expectations (September quarter), 8 August: A further decline in inflation expectations would be welcomed as a sign that the RBNZ's policy stance remains credible.

In addition to the indicators above, monthly spending, housing, migration and business sentiment/survey indicators will continue to warrant attention. And developments in global activity, inflation and commodity prices will also be monitored very closely by the RBNZ.

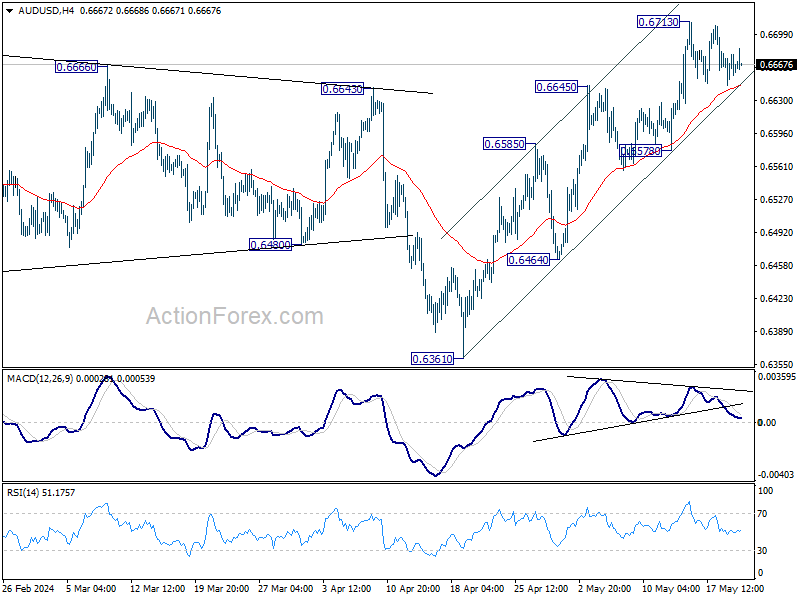

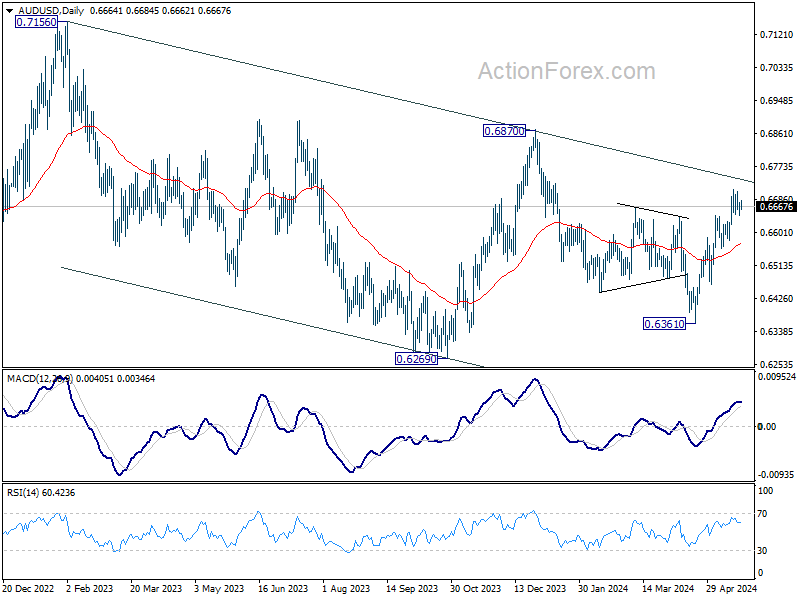

AUD/USD Daily Report

Daily Pivots: (S1) 0.6649; (P) 0.6664; (R1) 0.6681; More...

AUD/USD is staying in consolidation from 0.6713 and intraday bias remains neutral. Further rally is expected as long as 0.6578 support holds. As noted before, fall from 0.6870 has probably completed with three waves down to 0.6361 already. Above 0.6713 will target 0.6870 resistance next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

NZD Spikes on Hawkish RBNZ Decision, Focus Shifts to UK Inflation Data

New Zealand Dollar surged sharply higher following RBNZ's unexpectedly hawkish rate decision. While OCR was left unchanged, the central bank signaled the increased possibility of another rate hike this year and delayed projected timing of the first rate cut to the second half of 2025. However, Kiwi quickly gave back some of its gains after RBNZ Governor Adrian Orr tempered expectations in his press conference. Orr emphasized that the OCR track is a only central projection, not a guaranteed outcome, and expressed satisfaction that inflation expectations are declining.

Market attention now turns to the upcoming UK inflation data. Headline CPI is anticipated to drop significantly from 3.2% to 2.1% in April, while core CPI is expected to decrease from 4.2% to 3.6%. BoE has indicated that a rate cut this summer is possible, but the timing will depend on the data. Currently, markets are pricing in almost a 100% chance of a rate cut in August and a 50/50 chance in June. Any upside surprises in today's inflation figures would strengthen the case for a later rate cut.

In other currency movements, all major pairs and crosses are trading within yesterday's ranges, except for Kiwi pairs. For the week, Sterling is currently the strongest, followed by Dollar and Euro. Yen is the weakest, followed by Aussie and then Kiwi. Swiss Franc and Canadian are positioning in the middle.

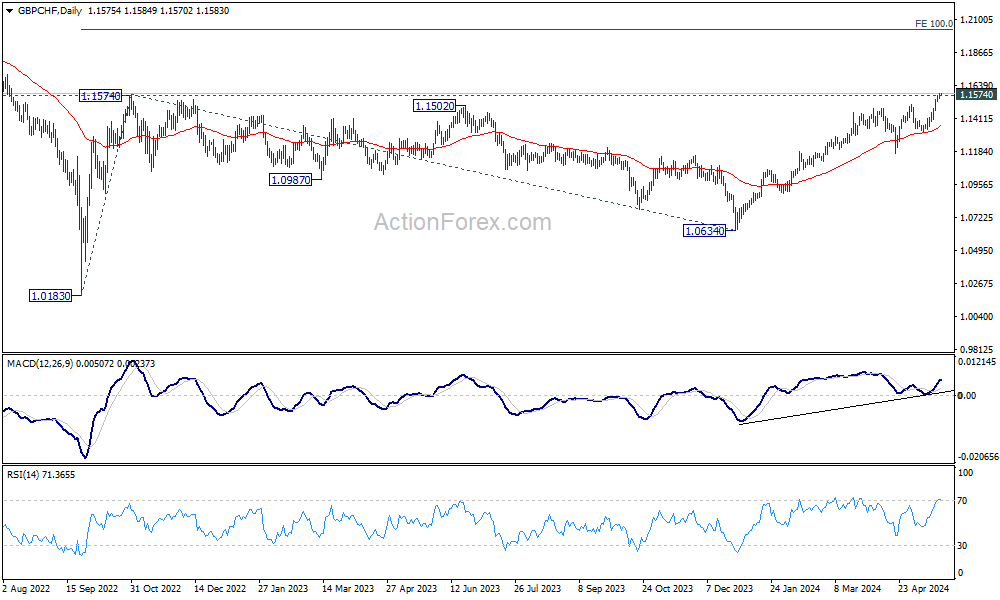

Technically, GBP/CHF's breach of 1.1574 resistance suggests that larger rise from 1.0183 (2022 low) is trying to resume. Sustained trading above this will confirm this bullish case, and target 100% projection of 1.0183 to 1.1574 from 1.0634 at 1.2025 in the medium term. In case of retreat, outlook will remain bullish as long as 55 D EMA (now at 1.1361) holds.

In Asia, at the time of writing, Nikkei is down -0.72%. Hong Kong HSI is up 0.18%. China Shanghai SSE is up 0.02%. Singapore Strait Times is down -0.19%. Japan 10-year JGB yield is up 0.0084 at 0.993. Overnight, DOW rose 0.17%. S&P 500 rose 0.25%. NASDAQ rose 0.22%. 10-year yield fell -0.023 to 4.414.

RBNZ holds steady at 5.50% but signals potential hike later in 2024

RBNZ kept Official Cash Rate unchanged at 5.50%, as widely anticipated. However, RBNZ surprised markets by raising its projected rate path, suggesting the possibility of another rate hike later this year. Additionally, the timeline for rate cuts has been pushed further into the latter half of 2025. According to key forecast variables, the OCR is expected to rise from the current 5.5% to 5.7% in Q4 2024 before declining to 5.4% in Q3 2025.

Minutes of the meeting highlighted that members agreed on the "significant upside risk" posed by persistent non-tradable inflation. They noted that the influence of recent inflation outcomes on future inflation expectations is critical for price setting, wage expectations, and the stance of monetary policy. Moreover, slower output growth than currently assumed could reduce the pace at which spending can grow without increasing inflationary pressures.

"Monetary policy may need to tighten and/or remain restrictive for longer if wage and price setters do not align with weaker productivity growth rates," the minutes stated.

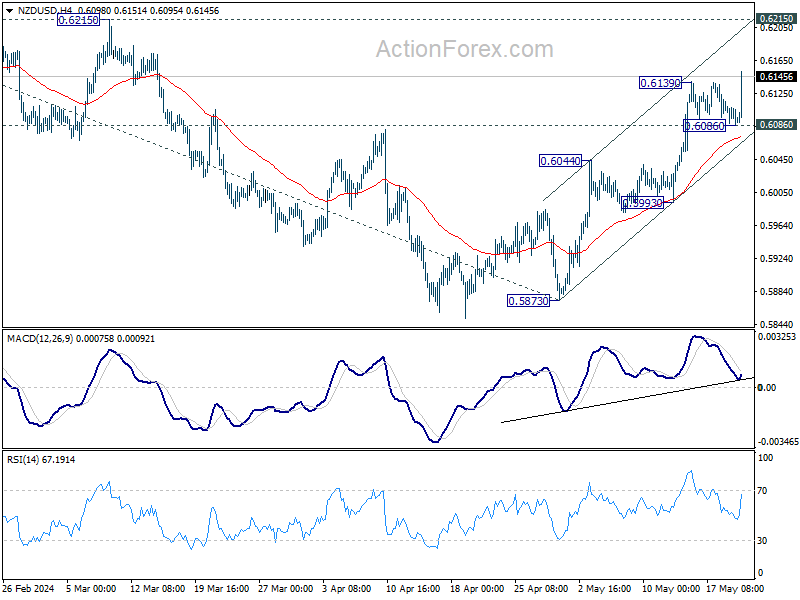

NZD/USD bounces after hawkish RBNZ hold, AUD/NZD dives

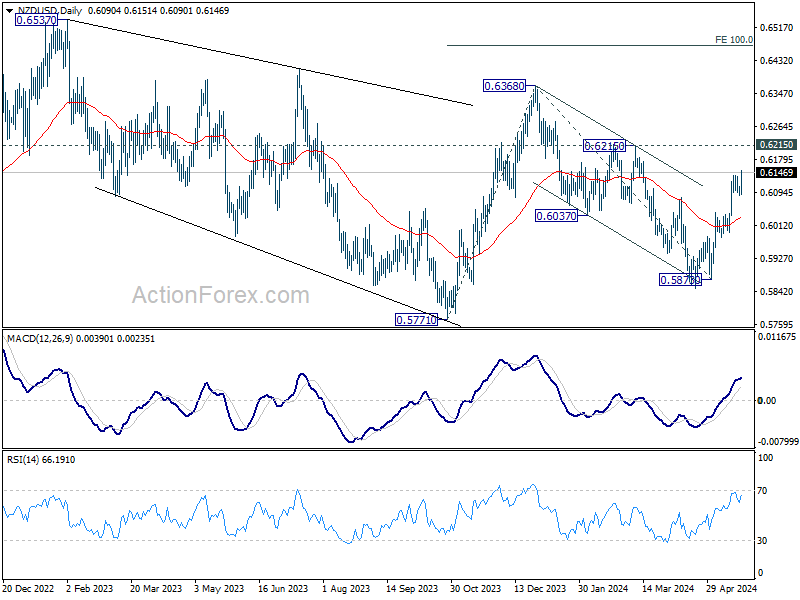

NZD/USD rises sharply after the hawkish RBNZ hold today. Break of 0.6139 confirms resumption of rally from 0.5873. Further rise is now expected as long as 0.6086 support holds. Next near term target is 0.6215 resistance.

Current development also affirms the view that NZD/USD's corrective fall from 0.6368 has completed with three waves down to 0.5870. Decisive break of 0.6215 should pave the way through 0.6368 to resume the rise from 0.5771 (2023 low).

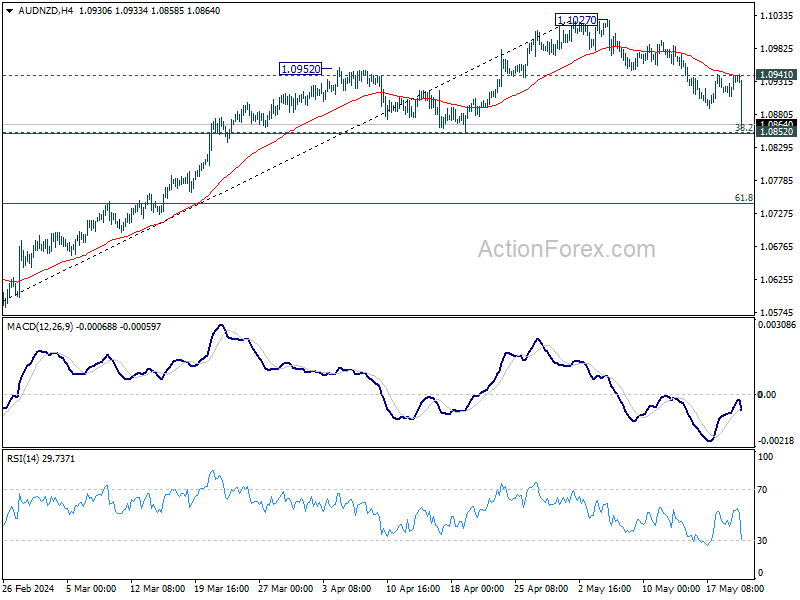

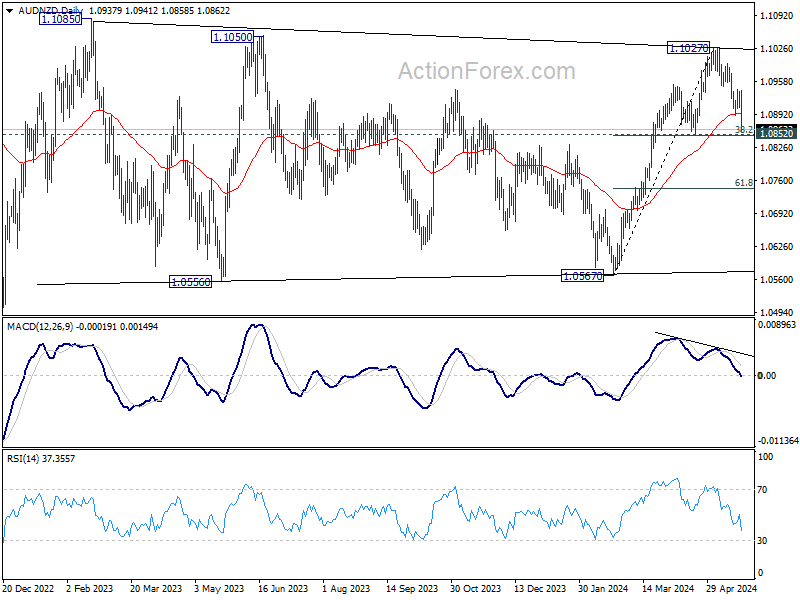

AUD/NZD dives in tandem with broad based Kiwi strength. Immediate focus is now on 1.0852 cluster support (3872% retracement of 1.0567 to 1.1027 at 1.0851. Sustained break there should confirm that whole rise from 1.0567 has completed. Decline from 1.1027 is another falling leg in the medium term range pattern from 1.1085, and should target 61.8% retracement at 1.0743 and below. This will remain the favored case as long as 1.0941 resistance holds.

Japan's exports rise 8.3% yoy in Apr, imports up 8.3% yoy

In April, Japan's exports increased by 8.3% yoy to JPY 8981B, falling short of expected 11.1% growth. Nonetheless, this marks the fifth consecutive month of export growth and sets a record for April. Key contributors to this growth included hybrid cars, semiconductor-making equipment, and chips.

Imports also rose by 8.3% yoy to JPY 9443B, slightly below expected 9.0% increase, and set a record for the month. The weak Ten continues to inflate import costs for resource-scarce Japan, with crude oil prices jumping 17.7% yoy, compared to a 2.6% yoy increase in Dollar terms. This resulted in a trade balance deficit of JPY -463B.

On a seasonally adjusted basis, exports rose 0.9% mom to JPY 8843B, while imports decreased by -0.5% mom to JPY 9403B, leading to a trade balance deficit of JPY -561B.

ECB's Nagel: June cut plausible, not on autopilot afterwards

In a newspaper interview, ECB Governing Council member Joachim Nagel expressed optimism about the current economic outlook, noting that "wage growth is expected to moderate as inflation continues to recede." He highlighted that recent developments are "heading in the right direction."

Nagel suggested that a first rate reduction in three weeks is "plausible," provided that incoming data and new projections align with policymakers' expectations. However, he cautioned against rushing into additional monetary easing, emphasizing, "We should not cut rates hastily and jeopardize what we have achieved."

He also underscored the high level of uncertainty, stating, "Even if rates are lowered for the first time in June, that does not mean we will cut rates further" in subsequent meetings. Nagel stressed that ECB's approach is not automatic, saying, "We are not on auto-pilot."

BoE's Bailey signals next move as rate cut amid expected drop in inflation

BoE Governor Andrew Bailey indicated overnight that he anticipates the next move in monetary policy will be a rate cut. He expects a significant decline in April's UK inflation data, but questions remain about how long the current level of monetary policy restriction will need to be maintained.

Bailey addressed the IMF's suggestion to hold a press conference after each rate-setting meeting, rather than just four times a year. He stated, "We will roll that question that the IMF have given to us into our thinking about implementing Ben Bernanke's changes."

Fed's Waller: Several months of data needed before supporting rate cuts

Fed Governor Christopher Waller emphasized in a speech yesterday that "several more months" of favorable inflation data are necessary before he would consider supporting interest rate cuts.

While the latest CPI data was a "reassuring signal" indicating that inflation is not accelerating, Waller noted that the progress shown was "small."

Waller highlighted that current data on spending and labor market suggest that monetary policy is at an "appropriate setting" to exert downward pressure on inflation.

However, "in the absence of a significant weakening in the labor market, I need to see several more months of good inflation data before I would be comfortable supporting an easing in the stance of monetary policy," he said.

Looking ahead

UK CPI, PPI are the main focus in European session. Later in the day, US will release existing home sales and FOMC minutes.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6649; (P) 0.6664; (R1) 0.6681; More...

AUD/USD is staying in consolidation from 0.6713 and intraday bias remains neutral. Further rally is expected as long as 0.6578 support holds. As noted before, fall from 0.6870 has probably completed with three waves down to 0.6361 already. Above 0.6713 will target 0.6870 resistance next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Apr | -0.56T | -0.73T | -0.70T | -0.68T |

| 23:50 | JPY | Machinery Orders M/M Mar | 2.90% | -1.80% | 7.70% | |

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 06:00 | GBP | CPI M/M Apr | 0.20% | 0.60% | ||

| 06:00 | GBP | CPI Y/Y Apr | 2.10% | 3.20% | ||

| 06:00 | GBP | Core CPI Y/Y Apr | 3.60% | 4.20% | ||

| 06:00 | GBP | RPI M/M Apr | 0.50% | 0.50% | ||

| 06:00 | GBP | RPI Y/Y Apr | 3.30% | 4.30% | ||

| 06:00 | GBP | PPI Input M/M Apr | 0.40% | -0.10% | ||

| 06:00 | GBP | PPI Input Y/Y Apr | -1.20% | -2.50% | ||

| 06:00 | GBP | PPI Output M/M Apr | 0.40% | 0.20% | ||

| 06:00 | GBP | PPI Output Y/Y Apr | 1.20% | 0.60% | ||

| 06:00 | GBP | PPI Core Output Y/Y Apr | 0.10% | |||

| 06:00 | GBP | PPI Core Output M/M Apr | 0.30% | |||

| 06:00 | GBP | Public Sector Net Borrowing(GBP) Apr | 18.5B | 11.0B | ||

| 14:00 | USD | Existing Home Sales Apr | 4.18M | 4.19M | ||

| 14:30 | USD | Crude Oil Inventories | -2.4M | -2.5M | ||

| 18:00 | USD | FOMC Minutes |

NZD/USD bounces after hawkish RBNZ hold, AUD/NZD dives

NZD/USD rises sharply after the hawkish RBNZ hold today. Break of 0.6139 confirms resumption of rally from 0.5873. Further rise is now expected as long as 0.6086 support holds. Next near term target is 0.6215 resistance.

Current development also affirms the view that NZD/USD's corrective fall from 0.6368 has completed with three waves down to 0.5870. Decisive break of 0.6215 should pave the way through 0.6368 to resume the rise from 0.5771 (2023 low).

AUD/NZD dives in tandem with broad based Kiwi strength. Immediate focus is now on 1.0852 cluster support (38.2% retracement of 1.0567 to 1.1027 at 1.0851). Sustained break there should confirm that whole rise from 1.0567 has completed. Decline from 1.1027 is another falling leg in the medium term range pattern from 1.1085, and should target 61.8% retracement at 1.0743 and below. This will remain the favored case as long as 1.0941 resistance holds.