Sample Category Title

NZ First Impressions: Retail Trade, March Quarter 2024

Retail spending was much stronger than expected in the March quarter. However, the longer-term trend in spending remains weak.

March quarter real retail sales (volumes): +0.5% (Prev: -1.8%)

- Westpac f/c: -0.5%, Market: -0.3%

March quarter nominal sales level: +0.7% (Prev: -1.4%)

Annual changes (March 2024 vs March 2023)

- Nominal sales: 0.6%

- Volume of goods sold: -2.4%

Retail spending rose 0.5% in the March quarter. That was well above our own and market expectations for a fall in spending in the early part of the year.

However, rather than pointing to a resurgence in spending appetites, March’s rise in spending looks more like a bounce after the very large decline in the previous quarter. The broader trend in spending remains down.

What drove spending in the March quarter?

Growth in spending over the March quarter was underpinned by a rise in spending on groceries (+0.6%), hospitality spending (+2.6%), recreational goods (+4.7%) and apparel (+2.4%). Most of those are areas that recorded sharp declines last quarter.

On the downside, recent months have seen continued softness in hardware/building supplies (-2.8%) and spending in department stores (-1.2%).

What does this tell us about the strength of spending?

Much of the strength in today’s result was a bounce after earlier weakness. The longer-term trend in spending remains weak. Compared to this time last year, spending levels are still down 2.4%. That’s despite population growth of around 2.7%.

Much of that weakness has been due to continued pressures on living costs. Nominal spending levels have been tracking sideways, with households getting less in their shopping trollies.

Overall, we continue to expect softness in spending over the coming months. That’s consistent with recent retail card spending reports and feedback from retailers (many of whom have reported missing sales targets in recent months).

Implications for GDP growth

Today’s result was higher than expected. We’re currently forecasting a modest 0.1% rise in March quarter GDP. We’ll review that number over the coming weeks as more data comes to hand.

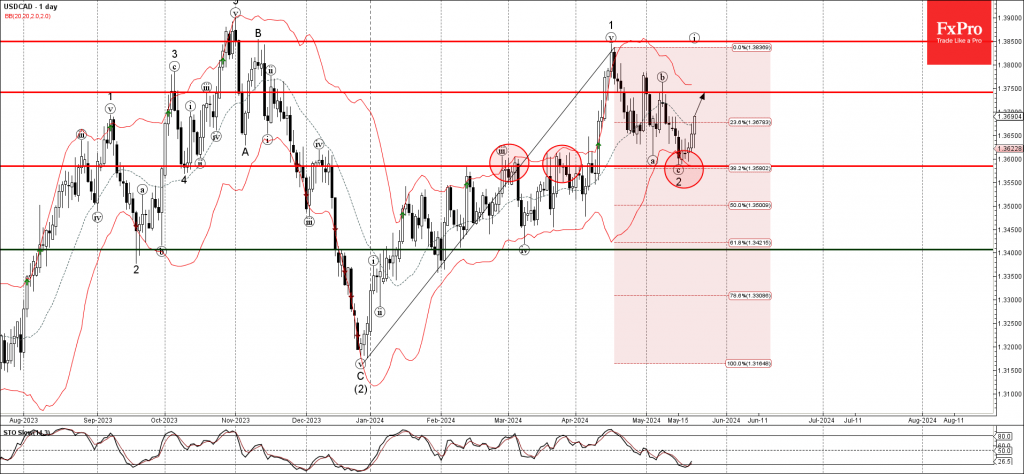

USDCAD Wave Analysis

- USDCAD reversed from pivotal support level 1.3585

- Likely to rise to resistance level 1.3750

USDCAD currency pair recently reversed up from the pivotal support level 1.3585 (former strong resistance from December, February and March) intersecting with the lower daily Bollinger Band and the 38.2% Fibonacci correction of the upward impulse from December.

The upward reversal from the support level 1.3585 stopped the previous minor ABC correction 2.

Given the strength of the support level 1.3585, USDCAD currency pair can be expected to rise further to the next resistance level 1.3750.

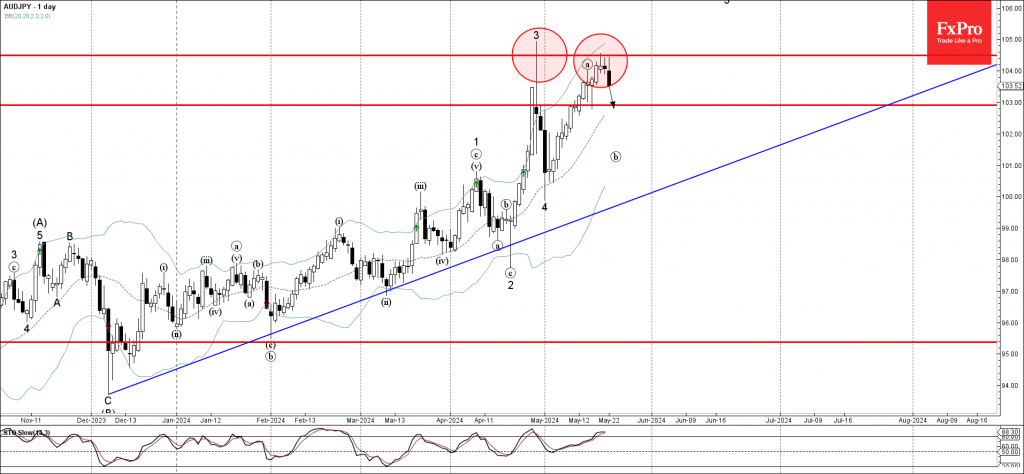

AUDJPY Wave Analysis

- AUDJPY reversed from resistance level 104.50

- Likely to fall to support level 103.00

AUDJPY currency pair recently reversed down from the key resistance level 104.50, which stopped the previous sharp upward impulse wave 3.

The price formed two consecutive Japanese candlesticks reversal patterns Doji – signalling the strength of this resistance level.

Given the strength of the resistance level 104.50 and the overbought daily Stochastic, AUDJPY currency pair can be expected to fall further to the next support level 103.00.

Fed Minutes Continue to Underscore Fed’s Data Dependent Approach

The minutes from the April 30-May 1, 2024 Federal Open Market Committee (FOMC) interest rate announcement acknowledged the recent lack of progress in curtailing inflation and continued to highlight the upside risks to the inflation outlook.

Specifically, Committee members noted that, "the recent increases in inflation had been relatively broad based and therefore should not be overly discounted." At the same time, Committee members noted that the disinflation process would likely take longer than previous thought.

When discussing the appropriate policy actions, "all participants judged that, in light of current economic conditions and their implications for the outlook for employment and inflation, as well as the balance of risks, it was appropriate to maintain the target range for the federal funds rate at 5¼ to 5½ percent."

On future policy decisions, participants continued to note that the "future path of the policy rate would depend on incoming data, the evolving outlook, and the balance of risks." Some members cited a willingness to increase rates should it be required given the inflation backdrop.

In examining the restrictiveness of current policy, several members expressed "uncertainty" on the degree of policy restriction. This uncertainty stems from a host of factors including the potential that policy may be having smaller effects than in the past given the upward drift in the neutral rate.

Key Implications

Today's minutes continued to underscore the Fed's willingness to maintain rates at their current levels, giving today's restrictive policy stance more time to work. With Chair Powell and other FOMC members recently acknowledging the "lack of further progress", market pricing for the first-rate cut has been pushed to November.

Since the May FOMC meeting, the April reading on inflation broke the string of three consecutive prints which surprised to the upside registering just below expectations. Nonetheless, one good inflation print is unlikely to give the Fed confidence that inflation is once again trending favorably. We expect inflation to gradually drift lower through the second half of the year, but with progress likely to come more incrementally, the first-rate cut is not expected until the fourth quarter.

Sunset Market Commentary

Markets

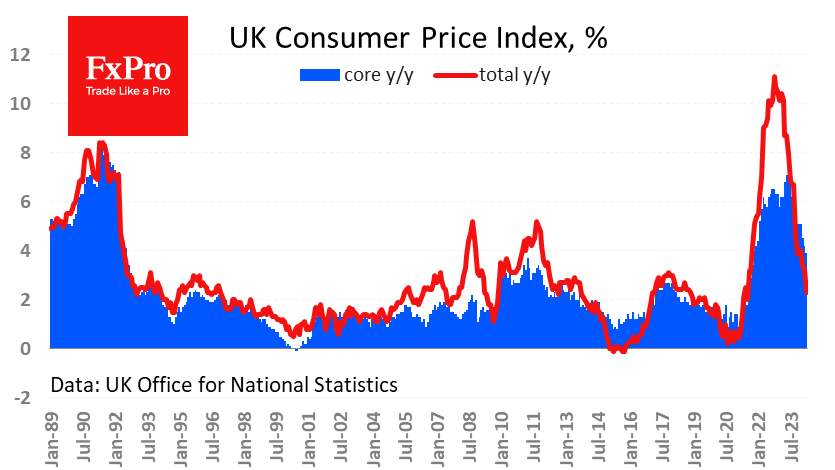

April UK inflation figures set the tone from the start of trading. The Bank of England, with a leading role for chair Bailey, hyped the number way in advance as coming a long way in the direction of the 2% inflation target. That was because of the anticipated drop in the cap on regulated energy prices which would put the UK on a European instead of US-style inflation trajectory. BoE comments were split on following Frankfurt with a June rate cut or keeping rates higher for longer like the Fed. The May policy meeting and report contained arguments for both scenarios. This morning’s inflation report settles the debate and calls for surrender by the BoE Chair. Headline inflation slowed from 0.6% M/M to 0.3% M/M but consensus hoped for a 0.1% outcome. The Y/Y figure slowed from 3.2% to 2.3% instead of 2.1%. The picture becomes more troublesome when looking at core measure. UK core CPI accelerated from 0.6% M/M to 0.9% M/M with the Y/Y-number only retreating from 4.2% to 3.9% instead of 3.6%. Services inflation even came in at an astonishing 1.5% M/M with the annual figure remaining sticky at 5.9% (from 6%). UK markets drew firm conclusions. The market implied probability of a June rate cut fell from roughly 50% to barely 15%. A first cut is now only (completely) discounted by the November (!) BoE policy meeting. UK gilts obviously underperformed German Bunds and US Treasuries. UK yields today rise by 8.9 bps (30-yr) to 12.7 bps (2-yr) compared with 4-5 bps increases in Germany and 3-4 bps gains in the US. Sterling outperformed with EUR/GBP in first instance dropping from 0.8540 to 0.8520, but now gradually looking for a test of the (strong) support zone at 0.85. Cable set a new short term high around 1.2750 before being called back by today’s genuine USD strength (EUR/USD 1.0835). In a broader perspective, today’s UK CPI figures make you wonder whether Europe (alone) can buck the global trend of stickier (core) inflation. Tomorrow’s PMI surveys and Q1 wage data are a first reference. EMU PMI’s showed the EMU economy gradually coming back to live in recent months with price gauges already running at highest levels in (over) a year. Q1 wage numbers will like remain sticky at levels around 4.5% annualized. Put against today’s context, this could cause some further underperformance of the front end of the European curve.

News & Views

Polish sold industrial output, which tends to be very volatile in M/M figures, declined by 2.2% M/M in April but this still lifted the Y/Y-measure to a higher than expected 7.9%. In the period January-April of 2024, production of industry was 0.9% Y/Y. An increase in sold production was reported in 31 (out of 34) industry divisions. Polish employment was unchanged in April from March, but declined 0.4% Y/Y. Average wages eased slightly M/M in April (-1.6% M/M). According to the statistical office, this decrease was due to a higher scale of payments (special payments) in the previous month. Y/Y average wages rose 11.3%, from 12% in March. The rise was marginally softer than expected. In January, the statutory minimum salary was raised by 17.8%. With headline and core inflation in April at respectively 2.4% and 4.1%, Y/Y this still suggests a solid rise in disposable income. The zloty is falling prey to profit taking (EUR/PLN 4.268 from 4.2525) but a similar move is visible in the forint and to a lesser extent in the Czech koruna. Today’s data won’t change assessment of the National bank of Poland that it will keep rates unchanged until the end of the year.

In its monthly report, the Bundesbank indicated that negotiated wages in the first quarter rose 6.2%. The rise was higher than expected. The data suggest that the euro-wide negotiated wage data of the ECB might be higher than expected tomorrow. In a broader analysis of the economy, the Buba also indicated that its expects inflation to rise again in May and to stay at slightly higher level in the coming months. While this is mainly due to base effects, the Buba also warns that there remain risks to the disinflation process because of wage rises.

Graphs

Japanese 10-yr yield rises above 1% for the first time since 2012

EUR/GBP: ready to test 0.85 support on sticky inflation print

UK 2-yr yield tries to break the downward trend with money markets pushing a first rate cut to November

Brent crude testing the recent downside as questions on global growth remain

UK Inflation Distanced the Expected Rate Cut

Inflation in the UK exceeded forecasts, making traders and investors cautious about the prospects for policy easing in the coming months.

Consumer prices rose by 0.3% m/m vs. 0.2% expected. Annual inflation slowed to 2.3% last month from 3.2% in March. This is the lowest level in two years, comfortably close to the Bank of England’s target but above the forecast of 2.3%.

Core inflation has been gently slowing over the past 12 months but has only fallen to 3.9% y/y from a peak of 7.1% y/y. Meaningful progress, but quite far from the desired level. In our view, the high growth rate of the core price index is the most important factor pushing forward the date of policy easing.

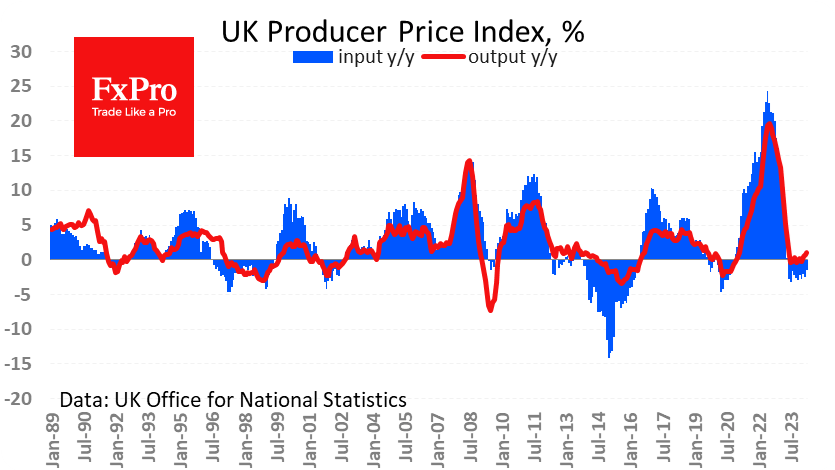

At the same time, producer prices have been at comfortably low levels for an extended period. The producer price index loses 1.5% y/y on entry, having remained in negative territory for the past 11 months. The Output Price Index is rising at a rate of 1.1% y/y, accelerating over the past three months from a low of -0.2% in February. Nevertheless, this is a relatively low rate that does not prevent policy easing.

Thus, the most intense inflationary pressure is centred on the retailers’ stage. This is probably the result of rising labour costs or an attempt to compensate for narrow margins in previous years.

The persistence of inflation translating into tighter monetary policy is causing pressure on the UK equity market. The FTSE100 is losing around 0.75%, smoothly forming a peak during the previous week. Inflation data looks like a worthwhile reason to start a correction that could take the index back to 8200 or even 8000 from the current 8360 before we see buying activity.

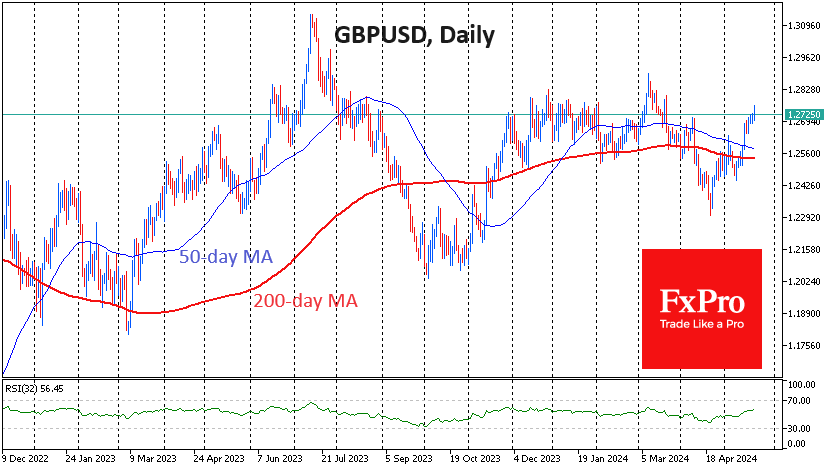

At the same time, this is good news for the pound, which hit a 2-month high against the dollar, rising above 1.2750 shortly after publication. This is an important area of resistance for the past 11 months. A further continuation of inflation higher than G10 currencies has the potential to lift GBPUSD to the next leg up to the 1.30-1.40 area. Should the economy stumble, and with it inflation, this would remove the divergence in monetary policy and put pressure back on the pound, leaving it in the 1.20-1.27 range.

GBP/USD Shrugs as UK Inflation Higher Than Expected

The British pound edged higher earlier today but has pared most of those gains. GBP/USD is trading at 1.2703, up 0.06% early in the North American session.

UK inflation declines less than expected

UK inflation fell sharply in April, falling to 2.3% y/y. This was down from 3.2% in March and the lowest rate since July 2021 but higher than the market estimate of 2.1%. On a monthly basis, inflation dropped to 0.3%, down from 0.6% in March and just above the market estimate of 0.2%. Food prices fell while higher gasoline prices and services inflation contributed to upward pressure on CPI.

Core CPI eased to 3.9% y/y, down from 4.2% in March but above the market estimate of 3.6%. The monthly reading surprised with a 0.9% gain, higher than the March gain of 0.6% and above the market estimate of 0.7%.GBP

The inflation report was on the whole positive but the rise in April core CPI left investors with a sour taste and dampened expectations for rate cut in June. The money markets have lowered pricing of a June rate cut to just 18%, compared to 50% on Tuesday.

The Bank of England has made inflation its number one priority and can point to an inflation rate that is closing in on the 2% target, after hitting a high of 11.2% in October 2022. The private sector is groaning under the weight of interest rates at 5.25% and the BOE has signaled that a rate hike is a possibility this summer but may have to delay an initial rate cut to August, as inflation remains sticky.

In the US, we’ll get a look at the FOMC minutes of the meeting earlier this month. The minutes may provide insight into the mood of FOMC members. Based on the message that the Fed has been steadily feeding the markets, the minutes will likely be hawkish. The markets have priced in a rate hike in September but Fed members have pointed to high inflation as a reason to maintain rates in restrictive territory until there is clear evidence that inflation will remain sustainable around the 2% target.

GBP/USD Technical

- There is support at 1.2641 and 1.2570

- 1.2772 and 1.2843 are the next resistance lines

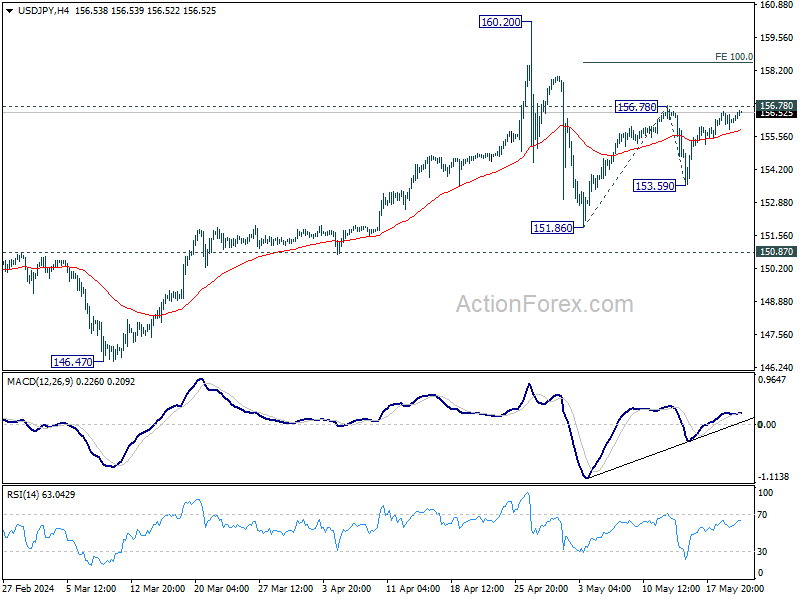

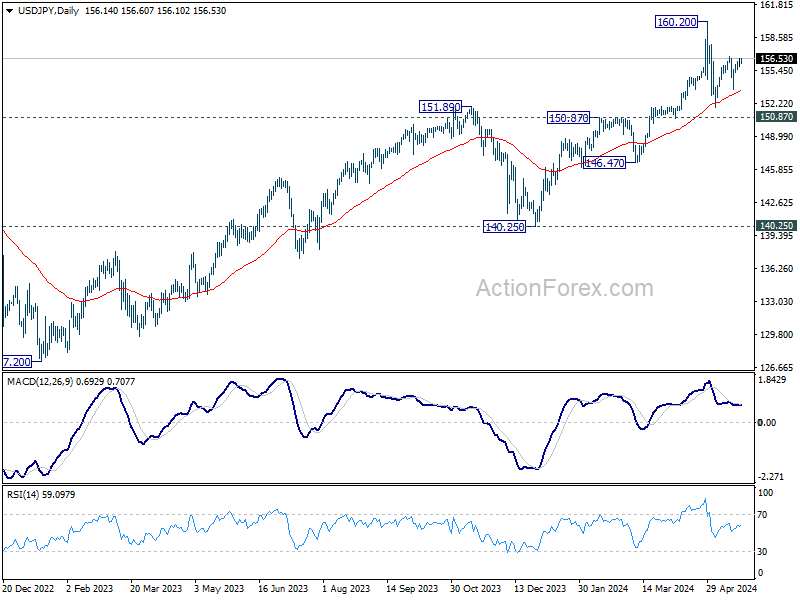

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.75; (P) 156.03; (R1) 156.56; More...

No change in USD/JPY's outlook and intraday bias stays neutral. Price actions from 160.20 are seen as a corrective pattern. On the upside, break of 156.78 will resume the rise from 151.86, as the second leg, to 100% projection of 151.86 to 156.78 from 153.59 at 158.51. On the downside, below 153.59 will target 151.86 and below as the third leg.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

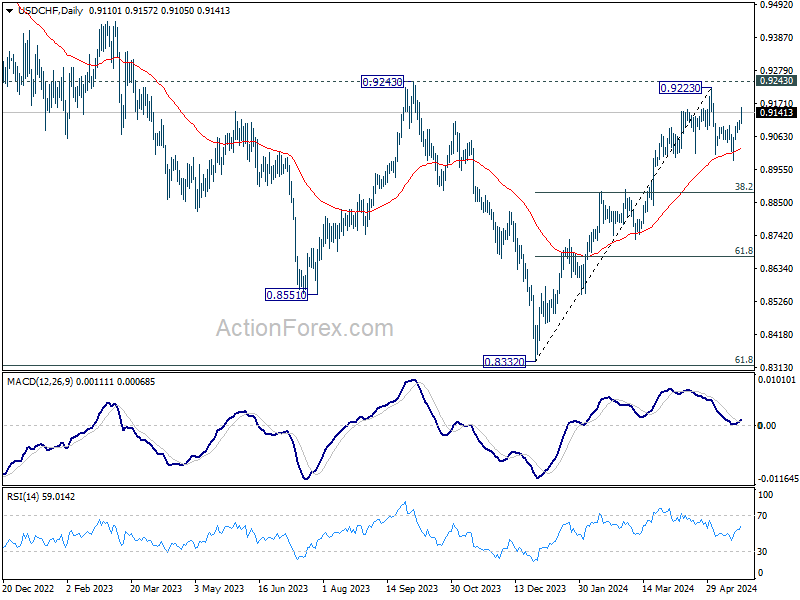

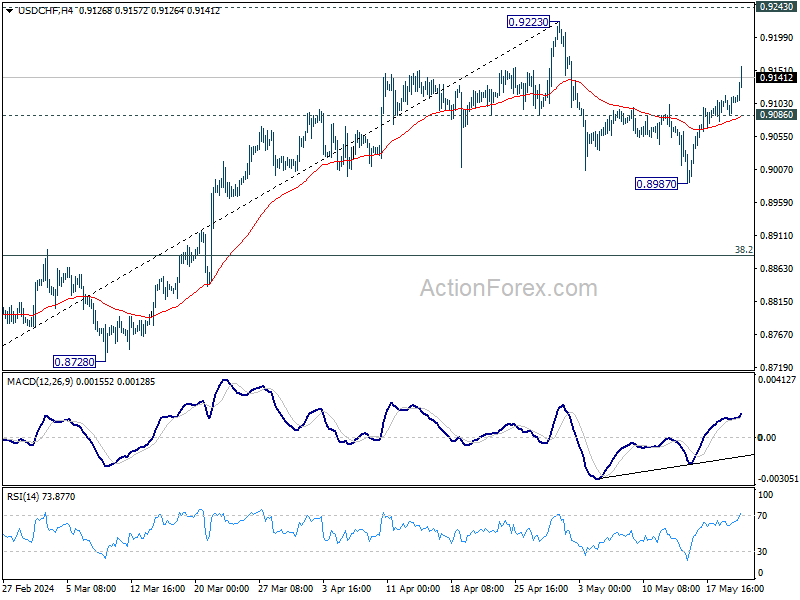

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9092; (P) 0.9104; (R1) 0.9122; More....

USD/CHF's rebound from 0.8987 extends higher today, and intraday bias stays on the upside. Further rally would be seen to 0.9223 resistance. On the downside, below 0.9086 minor support will turn intraday bias neutral first. Further break of 0.8987 will resume the fall from 0.9223 to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.