Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9092; (P) 0.9104; (R1) 0.9122; More....

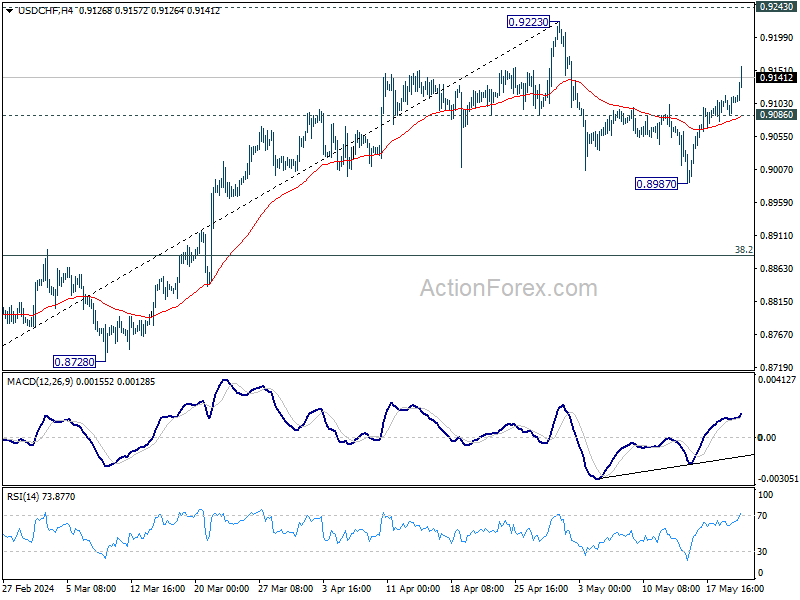

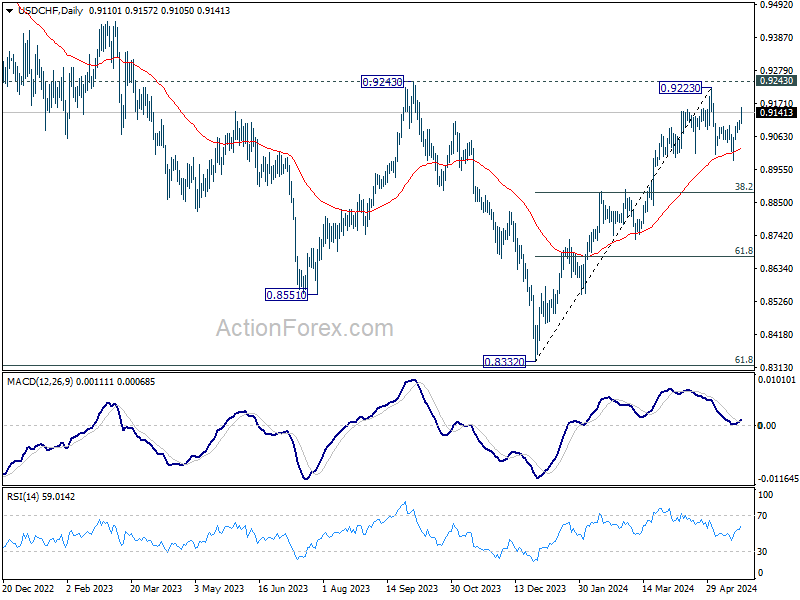

USD/CHF's rebound from 0.8987 extends higher today, and intraday bias stays on the upside. Further rally would be seen to 0.9223 resistance. On the downside, below 0.9086 minor support will turn intraday bias neutral first. Further break of 0.8987 will resume the fall from 0.9223 to 38.2% retracement of 0.8332 to 0.9223 at 0.8883.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0840; (P) 1.0857; (R1) 1.0872; More...

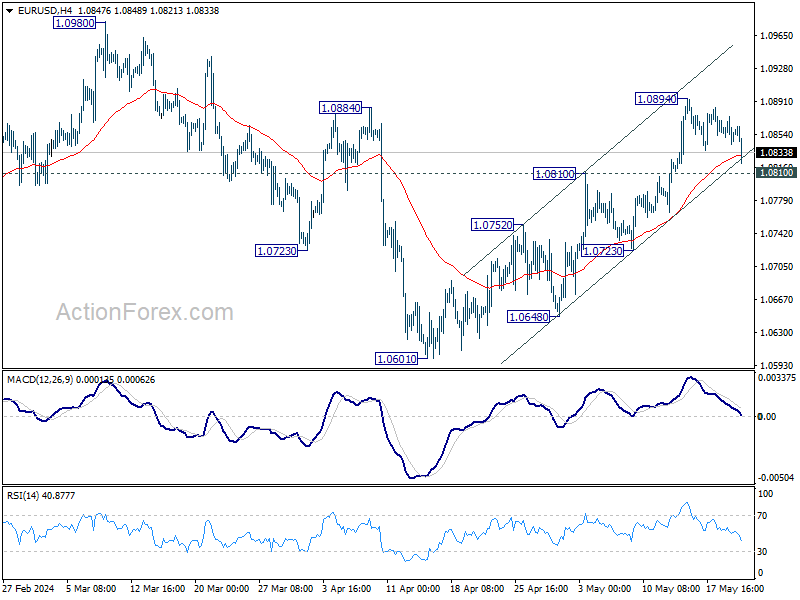

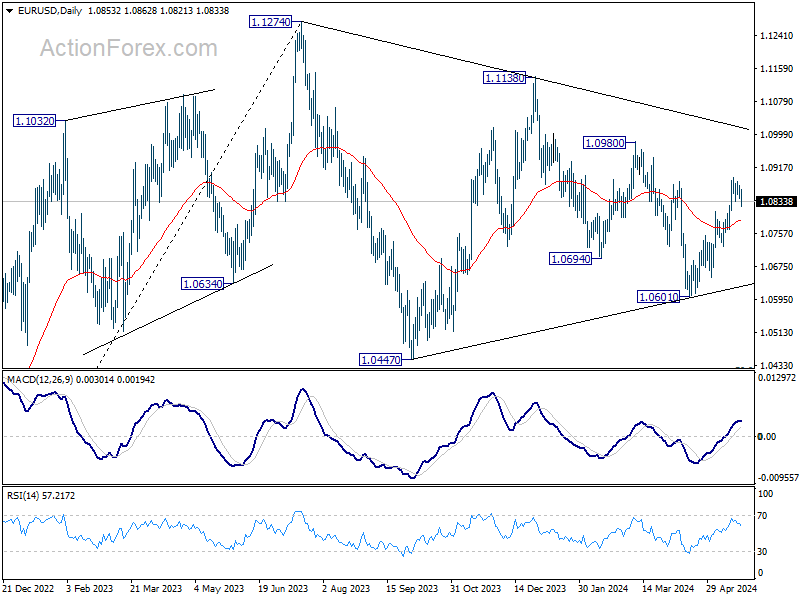

EUR/USD dips notably today but stays above 1.0810 resistance turned support. Intraday bias remains neutral and further rally is still in favor. On the upside, break of 1.0894 will resume the rise from 1.0601 to 1.0980 resistance. Decisive break there will confirm that whole fall from 1.1138 has completed at 1.0601 already. However, firm break of 1.0810 will dampen this bullish case, and turn bias back to the downside.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

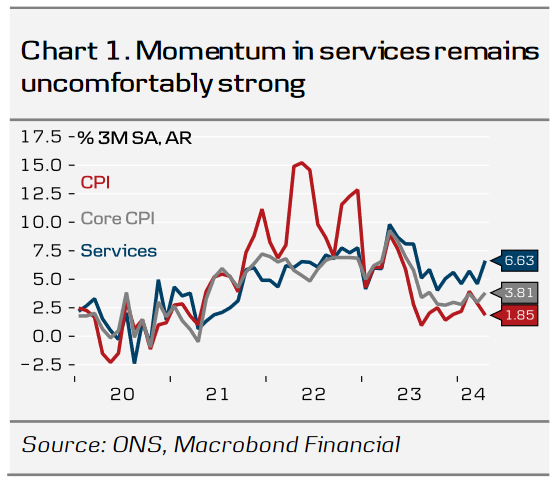

Bank of England – Revised BoE Call – Hot Service Inflation Spells Trouble

- On the back of continued strong inflationary pressures in the service sector, as evident in the April inflation print, we revise our BoE call. We now expect the first 25bp cut in August (prev. June).

- We expect quarterly cuts from August and through 2025, leaving the Bank Rate at 3.75% by the end of 2025.

Inflation in April surprised significantly to the topside across the board, relative to both the consensus expectation and the BoE's forecast from the May monetary policy report. Headline came in at 2.3% y/y (cons: 2.1%, BoE: 2.1%, prior: 3.2%,), core at 3.9% (cons: 3.6%, prior: 4.2%) and services a 5.9% y/y (cons: 5.4%, BoE: 5.5%, prior: 6.0%).

Although the year-on-year measures dropped notably due to base effects from energy prices and April-specific annual price adjustments (e.g rents, telephone contracts and tv licence fees), the underlying momentum remains strong. The big driver was services with a broad range of services such as hotels, restaurants and recreation and culture services delivering upward contributions. Service inflation remains key for the BoE as it uses it as a measure of inflation persistence alongside tightness of the labour market and wage growth. Worryingly, alongside the big BoE forecast miss, the momentum in service inflation picked up in April (see chart 1). Likewise, wage growth remains elevated with the labour market still tight by historical standards.

Following today's topside surprise and the May print unlikely to deliver an equally large downside surprise to sway the majority of the MPC to vote for a cut, we now expect the first 25bp cut in August.

Our call. We now expect the BoE to deliver the first cut of 25bp in August (June previously). Given the later start to the cutting cycle, we subsequently now only expect one 25bp cut in the following quarter, totalling 50bp of cuts for 2024 (previously 75bp). Markets are pricing 40bp for the remainder of the year with the first 25bp cut fully priced by November.

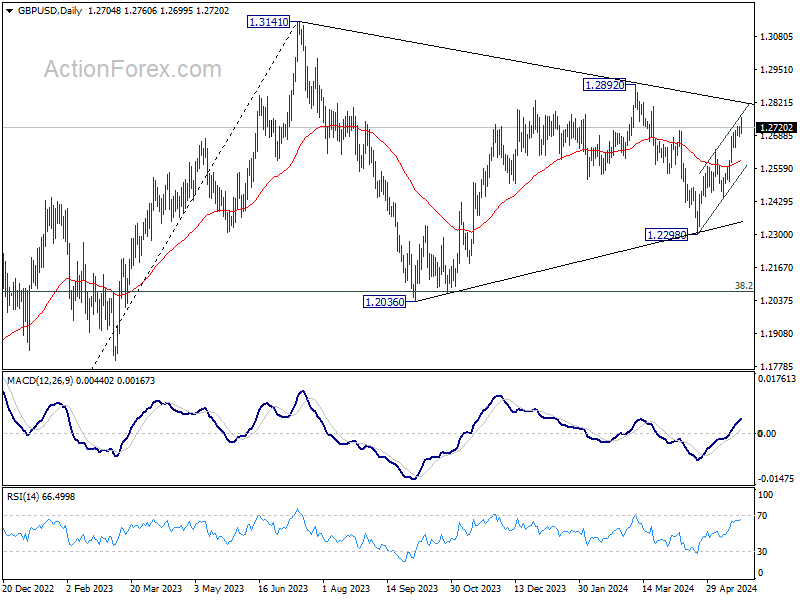

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2689; (P) 1.2708; (R1) 1.2729; More...

Intraday bias in GBP/USD remains on the upside for 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780. Firm break there will target 1.2892 resistance next. However, break of 1.2685 will minor support will turn bias back to the downside, for retreat to 55 4H EMA (now at 1.2644).

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Sterling Up as BoE June Cut Hopes Diminish; But Dollar and Kiwi Outshine

Sterling climbed broadly today after data showed that UK disinflation progress was slower than anticipated, with services inflation remaining persistently high. This development dashed hopes for an imminent rate cut by BoE, causing the odds of a rate cut in June to plummet from around 50% to below 20%. Despite this, the notable declines in both headline and core CPI keep the possibility of a rate cut at the BoE's August meeting alive.

While the Pound is performing well, it has been outpaced by New Zealand Dollar and US Dollar. Kiwi surged earlier following hawkish RBNZ statement and forecast. The central bank left OCR unchanged but signaled an increased likelihood of another rate hike this year and delayed the projected timing of the first rate cut to the latter half of 2025.

Dollar is gaining strength amid mild risk aversion and recovery in treasury yields. The focus now shifts to minutes from FOMC meeting. Traders will be looking for hints about the timing of the first rate cut by Fed, although it is unlikely they will find any new information. The minutes are expected to reinforce Fed's stance that rates will remain elevated for an extended period, with the next move likely being a cut, but timing contingent on further economic data.

On the flip side, Swiss Franc is the worst performer of the day, driven by expectations that the yield gap between Switzerland and other major economies will persist. Euro follows as the second worst, with ECB still on track for a rate cut in June, the Japanese Yen ranks third worst. Canadian Dollar and Australian Dollar are positioned in the middle of the performance spectrum.

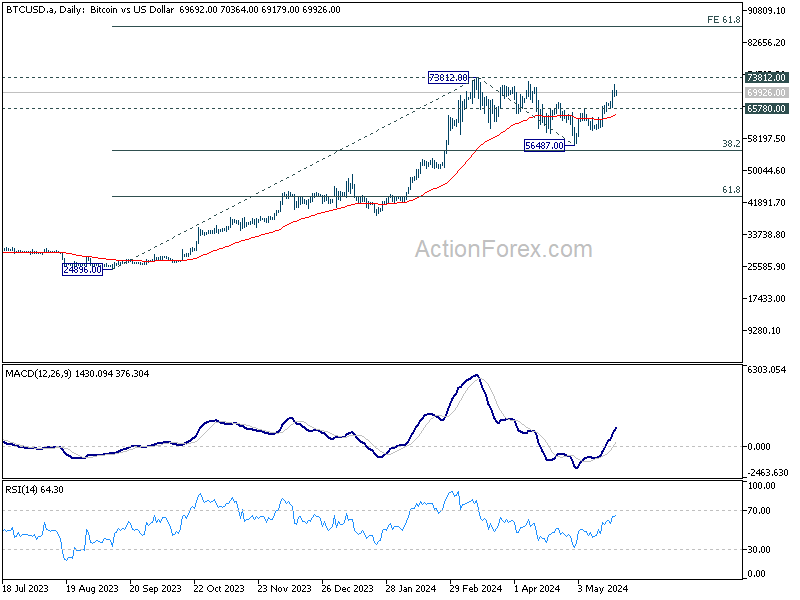

Technically, Bitcoin is quickly approaching 73812 record high as near term rally extends. Decisive break there will confirm up trend resumption for 61.8% projection of 24896 to 73812 from 65780 at 86717 next. On the downside, break of 65780 support will delay the bullish case and bring more consolidations first.

In Europe, at the time of writing, FTSE is down -0.69%. DAX is down -0.32%. CAC is down -0.69%. UK 10-year yield is up 0.1178 at 4.245. Germany 10-year yield is up 0.048 at 2.552. Earlier in Asia, Nikkei fell -0.85%. Hong Kong HSI fell -0.13%. China Shanghai SSE rose 0.02%. Singapore Strait Times fell -0.19%. Japan 10-year JGB yield rose 0.0160 to 1.001.

Bundesbank sees German economy gradually gaining momentum in Q2

In its monthly report, Bundesbank indicated that Germany's economic output is "likely to increase slightly again" in Q2. The general trend suggests that the economy is gradually "picking up speed," with positive impulses expected from private consumption and a "further recovery" in the service sector.

The Bundesbank also noted that energy-intensive sectors in industry could "recover moderately." However, it highlighted that a broad-based increase in new orders is still lacking, which is necessary for a thorough recovery. The improved business expectations in the manufacturing sector are anticipated to significantly boost production only in the second half of the year.

Additionally, Bundesbank expects inflation to rise again in May and fluctuate at a slightly higher level in the coming months. This is primarily due to base effects, such as the introduction of the "Germany Ticket" in local passenger transport last May, which will influence year-on-year comparisons.

UK CPI down to 2.3% in Apr, core CPI falls to 3.9%, both above expectations

UK CPI slowed sharply from 3.2% yoy to 2.3% yoy in April, but above expectation of 2.1% yoy. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 4.2% yoy to 3.9% yoy, above expectation of 3.6% yoy.

CPI goods annual rate turned negative from 0.8% yoy to -0.8% yoy. But CPI services annual rate eased just slightly from 6.0% yoy to 5.9% yoy.

RBNZ holds steady at 5.50% but signals potential hike later in 2024

RBNZ kept Official Cash Rate unchanged at 5.50%, as widely anticipated. However, RBNZ surprised markets by raising its projected rate path, suggesting the possibility of another rate hike later this year. Additionally, the timeline for rate cuts has been pushed further into the latter half of 2025. According to key forecast variables, the OCR is expected to rise from the current 5.5% to 5.7% in Q4 2024 before declining to 5.4% in Q3 2025.

Minutes of the meeting highlighted that members agreed on the "significant upside risk" posed by persistent non-tradable inflation. They noted that the influence of recent inflation outcomes on future inflation expectations is critical for price setting, wage expectations, and the stance of monetary policy. Moreover, slower output growth than currently assumed could reduce the pace at which spending can grow without increasing inflationary pressures.

"Monetary policy may need to tighten and/or remain restrictive for longer if wage and price setters do not align with weaker productivity growth rates," the minutes stated.

Japan's exports rise 8.3% yoy in Apr, imports up 8.3% yoy

In April, Japan's exports increased by 8.3% yoy to JPY 8981B, falling short of expected 11.1% growth. Nonetheless, this marks the fifth consecutive month of export growth and sets a record for April. Key contributors to this growth included hybrid cars, semiconductor-making equipment, and chips.

Imports also rose by 8.3% yoy to JPY 9443B, slightly below expected 9.0% increase, and set a record for the month. The weak Ten continues to inflate import costs for resource-scarce Japan, with crude oil prices jumping 17.7% yoy, compared to a 2.6% yoy increase in Dollar terms. This resulted in a trade balance deficit of JPY -463B.

On a seasonally adjusted basis, exports rose 0.9% mom to JPY 8843B, while imports decreased by -0.5% mom to JPY 9403B, leading to a trade balance deficit of JPY -561B.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2689; (P) 1.2708; (R1) 1.2729; More...

Intraday bias in GBP/USD remains on the upside for 100% projection of 1.2298 to 1.2633 from 1.2445 at 1.2780. Firm break there will target 1.2892 resistance next. However, break of 1.2685 will minor support will turn bias back to the downside, for retreat to 55 4H EMA (now at 1.2644).

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Apr | -0.56T | -0.73T | -0.70T | -0.68T |

| 23:50 | JPY | Machinery Orders M/M Mar | 2.90% | -1.80% | 7.70% | |

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 06:00 | GBP | CPI M/M Apr | 0.30% | 0.20% | 0.60% | |

| 06:00 | GBP | CPI Y/Y Apr | 2.30% | 2.10% | 3.20% | |

| 06:00 | GBP | Core CPI Y/Y Apr | 3.90% | 3.60% | 4.20% | |

| 06:00 | GBP | RPI M/M Apr | 0.50% | 0.50% | 0.50% | |

| 06:00 | GBP | RPI Y/Y Apr | 3.30% | 3.30% | 4.30% | |

| 06:00 | GBP | PPI Input M/M Apr | 0.60% | 0.40% | -0.10% | -0.20% |

| 06:00 | GBP | PPI Input Y/Y Apr | -1.60% | -1.20% | -2.50% | |

| 06:00 | GBP | PPI Output M/M Apr | 0.20% | 0.40% | 0.20% | |

| 06:00 | GBP | PPI Output Y/Y Apr | 1.10% | 1.20% | 0.60% | 0.70% |

| 06:00 | GBP | PPI Core Output M/M Apr | 0.00% | 0.30% | ||

| 06:00 | GBP | PPI Core Output Y/Y Apr | 0.20% | 0.10% | 0.20% | |

| 06:00 | GBP | Public Sector Net Borrowing(GBP) Apr | 18.5B | 11.0B | ||

| 14:00 | USD | Existing Home Sales Apr | 4.18M | 4.19M | ||

| 14:30 | USD | Crude Oil Inventories | -2.4M | -2.5M | ||

| 18:00 | USD | FOMC Minutes |

New Zealand Dollar Climbs after Hawkish RBNZ Announcement

The New Zealand dollar has pushed higher on Wednesday. NZD/USD is up 0.54%, trading at 0.6124 in the European session at the time of writing. The New Zealand dollar rose as high as 0.6152 (0.80%) in the Asian session after the RBNZ meeting but has pared much of these gains.

RBNZ holds rates but says inflation too high

The Reserve Bank of New Zealand held the cash rate at 5.5% at today’s meeting, as expected. This marks the seventh straight time that the RBNZ has held rates, as it continues its “higher for longer” rate policy.

The monetary policy statement was decidedly hawkish and this provided a boost for the New Zealand dollar. The statement noted that rates might have to remain at a restrictive level for longer than anticipated … to ensure the inflation target is met”.

This language was surprisingly hawkish and was indicative of the RBNZ’s frustration at the slow decline in inflation. New Zealand’s inflation rate has fallen sharply but the first-quarter figure of 4% was higher than the 3.8% forecast of the central bank. The RBNZ’s steep rate-tightening cycle has slashed inflation but it remains at double the midpoint of the 1-3% target range.

The RBNZ has pushed back its expectation of CPI falling within the target range of 1-3% from the third quarter of this year to the fourth quarter. More importantly, the RBNZ has raised the possibility of a rate hike before the end of the year to 60%. The money markets remain more optimistic that rates have peaked and have priced in three rate cuts in the fourth quarter.

NZD/USD Technical

- There is resistance at 0.6185 and 0.6235

- 0.6039 are the next support levels

Bundesbank sees German economy gradually gaining momentum in Q2

In its monthly report, Bundesbank indicated that Germany's economic output is "likely to increase slightly again" in Q2. The general trend suggests that the economy is gradually "picking up speed," with positive impulses expected from private consumption and a "further recovery" in the service sector.

The Bundesbank also noted that energy-intensive sectors in industry could "recover moderately." However, it highlighted that a broad-based increase in new orders is still lacking, which is necessary for a thorough recovery. The improved business expectations in the manufacturing sector are anticipated to significantly boost production only in the second half of the year.

Additionally, Bundesbank expects inflation to rise again in May and fluctuate at a slightly higher level in the coming months. This is primarily due to base effects, such as the introduction of the "Germany Ticket" in local passenger transport last May, which will influence year-on-year comparisons.

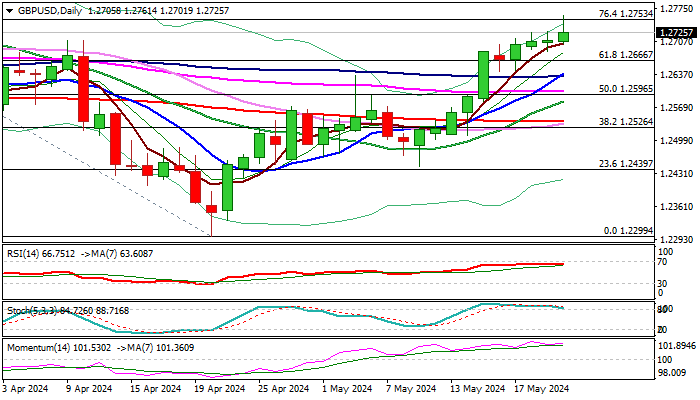

GBP/USD: Cable Hits Two-Month High After Inflation Data

Cable rose to two-month high (1.2761) on Wednesday, after UK inflation data for April showed that prices pressure eased below expectations, hurting bets for BoE’s June rate cut.

Fresh acceleration higher generates initial signal of bullish continuation after the price action held in a sideways mode in past two days and struggling to register a clear break above 1.2700 round-figure barrier, which proved to be a significant obstacle.

Traders stayed in a quiet mode in the past few sessions, awaiting release of April inflation data, which initially dented bets that the BoE would start easing its monetary from June.

Fresh advance probed through pivotal Fibo barrier at 1.2753 (Fibo 76.4% of 1.2893/1.2299) but needs to register a daily close above here to confirm signal.

Daily studies are in full bullish configuration (positive momentum remains strong / MA’s created a number of bull-crosses / north-heading daily Tenkan / Kijun-sen in bullish setup and converging), but overbought conditions likely contributed to subsequent pullback from new high and may continue to obstruct bulls.

According to the current technical picture and the latest economic data, dips should be shallow (ideally to be contained above 1.2700 handle and not to exceed broken Fibo 61.8% (1.2666) to keep bulls intact for firm break of 1.2753 pivot, which would expose targets at 1.2803 (Mar 23 lower top) and 1.2893 (2024 high, posted on Mar 8).

Res: 1.2753; 1.2761; 1.2803; 1.2823.

Sup: 1.2700; 1.2666; 1.2635; 1.2602.

New Zealand Dollar Shows Steady Rise

The NZD/USD pair is preparing for a mid-week rally, approaching the 0.6116 level. These current values mark the highest point for the Kiwi in two months, following the Reserve Bank of New Zealand's decision to maintain its monetary policy structure unchanged during the May meeting.

The interest rate remains at 5.5% per annum, as anticipated.

The RBNZ has determined that maintaining a restrictive monetary policy is necessary to ensure inflation returns to target within the planned timeframe. The central bank has noted a cooling labour market and rising unemployment as potential risks. Support factors include higher housing rents, insurance costs, and increasing utility rates.

According to the official forecast, the consumer price index in New Zealand is expected to return to the 1-3% range by the end of 2024.

Overall, the NZD exchange rate is poised to increase. The RBNZ's policy is viewed as balanced and consistent, which helps mitigate the risks of excessive volatility for the Kiwi.

On a broader scale, investors are awaiting the minutes from the latest US Federal Reserve meeting, which will provide further insights into the Fed's upcoming steps.

NZD/USD technical analysis

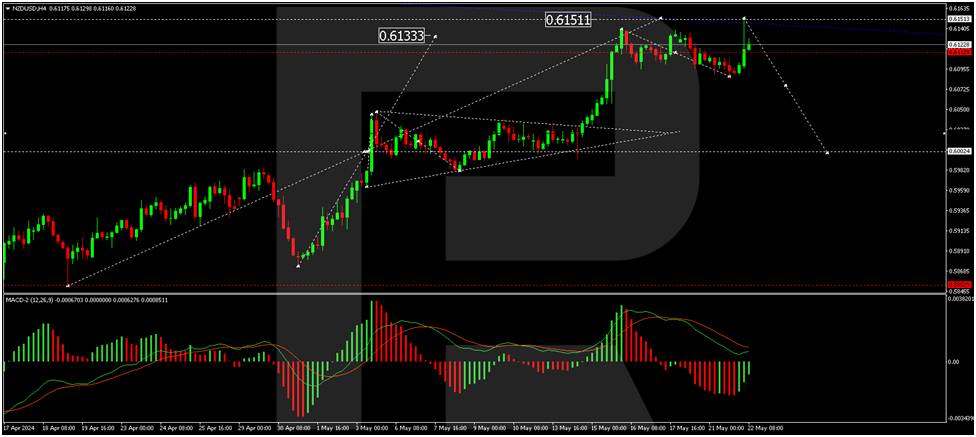

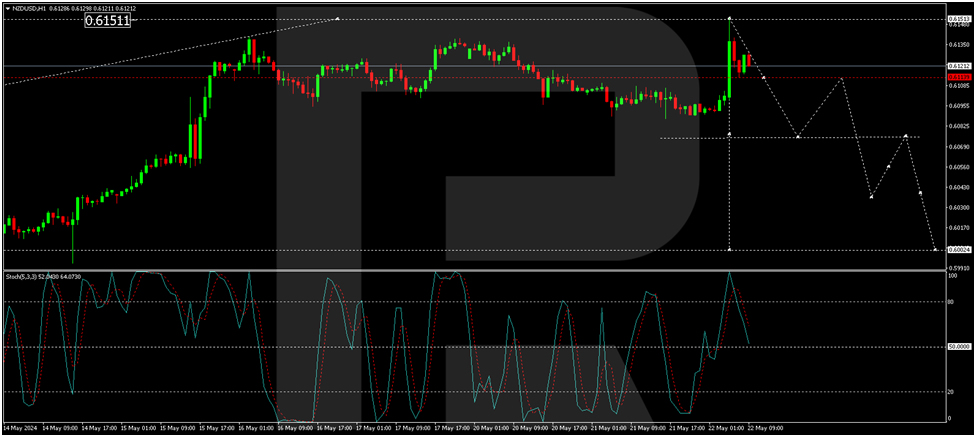

On the H4 chart of NZD/USD, a consolidation range has formed around the 0.6000 level. Following an upward breakout, a growth wave to 0.6151 has been achieved. A consolidation range is currently emerging around 0.6114. A downward breakout from this range could open the potential for a decline to 0.6000, the first target. After reaching this level, a correction wave to 0.6075 (testing from below) is possible, followed by a further decline along the trend to 0.5853. This scenario is technically supported by the MACD indicator, with its signal line above zero but directed strictly downwards.

On the H1 chart, an impulse of decline to 0.6114 has formed. Today, the market might perform a correction to 0.6132. After this correction, the continuation of the growth wave to 0.6075 is expected, with the prospect of further trend development.

Summary

The NZD/USD pair is steadily rising, bolstered by the Reserve Bank of New Zealand's consistent monetary policy. Technical indicators suggest potential corrections and further growth, with close attention to the upcoming US Federal Reserve minutes for additional market direction.

Bitcoin Waits for Ethereum Story to Develop

Market picture

The crypto market cap has stabilised at $2.6 trillion after an impressive surge following the Ethereum rally. Among the top coins over 24 hours, Toncoin is leading the decline, falling 5%, while Dogecoin is leading the way with a 3.4% increase.

Bitcoin is losing 1.9% in 24 hours to just below $70K, having come under pressure after it rallied above $71.3K, as short-term speculators rush to take profits around the all-time highs reached in March. The local highs are just below the peaks in April and March, and now all eyes are on the market’s next move. A break of resistance at $72K has the potential to trigger a real FOMO. A pullback below would force a $60K correction scenario to be considered as the main one.

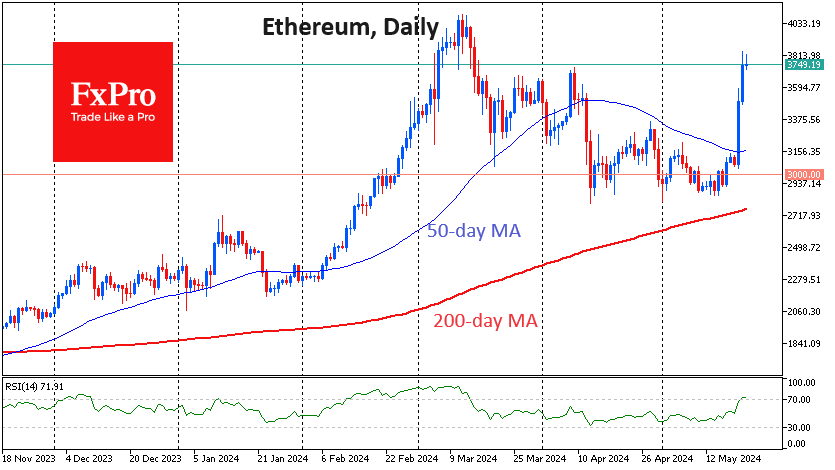

Ethereum has rallied around 22% since Monday evening, surpassing $3800. Technically, we got a signal of a powerful spurt above the 50-day moving average, meaning a return to the bull trend. Short-term, Ethereum has a clear path to $4000, the March peak, after which the bulls can target $4600. Now is the time when Bitcoin’s next move depends on Ethereum.

News background

According to media reports, the US SEC has asked companies to update Form 19b-4 in applications to launch a spot Ethereum-ETF. Bloomberg raised the odds of spot Ethereum-ETF approval from 25% to 75% following the news.

Management company Fidelity removed the steering clause in its updated Form S-1 application for a spot Ethereum-ETF. Galaxy Research believes that staking is the main stumbling block to launching an Ethereum-ETF in the US.

Standard Chartered expects the Ethereum-ETF to be approved as early as this week. The deadline for applications from VanEck and Grayscale is 23 May.

However, the SEC’s action does not mean that spot ETH-ETFs will necessarily be approved in May. Potential issuers need to approve a Form S-1 before launching the instrument.

Telegram’s crypto ‘Wallet’ has opened a P2P auction for the NOT, a token of the Web3 gaming project Notcoin. Users will be able to buy and sell coins in Telegram using more than 290 supported payment methods.