Sample Category Title

RBNZ holds steady at 5.50% but signals potential hike later in 2024

RBNZ kept Official Cash Rate unchanged at 5.50%, as widely anticipated. However, RBNZ surprised markets by raising its projected rate path, suggesting the possibility of another rate hike later this year. Additionally, the timeline for rate cuts has been pushed further into the latter half of 2025. According to key forecast variables, the OCR is expected to rise from the current 5.5% to 5.7% in Q4 2024 before declining to 5.4% in Q3 2025.

Minutes of the meeting highlighted that members agreed on the "significant upside risk" posed by persistent non-tradable inflation. They noted that the influence of recent inflation outcomes on future inflation expectations is critical for price setting, wage expectations, and the stance of monetary policy. Moreover, slower output growth than currently assumed could reduce the pace at which spending can grow without increasing inflationary pressures.

"Monetary policy may need to tighten and/or remain restrictive for longer if wage and price setters do not align with weaker productivity growth rates," the minutes stated.

(RBNZ) OCR 5.50% – Official Cash Rate remains unchanged

Restrictive monetary policy has reduced capacity pressures in the New Zealand economy and lowered consumer price inflation. Annual consumer price inflation is expected to return to within the Committee's 1 to 3 percent target range by the end of 2024.

The welcome decline in inflation in part reflects lower inflation for goods and services imported into New Zealand. Globally, consumer price inflation has declined from 30-year highs in many advanced economies. However, services inflation is receding slowly, and expected policy interest rate cuts continue to be delayed.

In New Zealand, pressures in the labour market have eased. Businesses are employing more cautiously in line with weak economic activity, while the number of people available to work has increased due to recent high net inward migration. Wage growth and domestic spending are easing to levels more consistent with the Committee's inflation target.

While weaker capacity pressures and an easing labour market are reducing domestic inflation, this decline is tempered by sectors of the economy that are less sensitive to interest rates. These near-term factors include, for example, higher dwelling rents, insurance costs, council rates, and other domestic services price inflation. A slow decline in domestic inflation poses a risk to inflation expectations.

Our economic projections include only officially available information on the Government's fiscal intentions to date, which includes the most recent fiscal update and 'mini budget'. The signalled lower government spending is currently and expected to continue contributing to weaker aggregate demand. Any impact of potential changes in the forthcoming Budget to government spending, or private spending due to tax cuts, remain to be assessed.

Annual consumer price inflation remains above the Committee's 1 to 3 percent target band, and components of domestic services inflation persist. The Committee agreed that monetary policy needs to remain restrictive to ensure inflation returns to target within a reasonable timeframe.

Media contact

James Weir

Senior Adviser External Stakeholders

Phone: +64 4 471 3962 | Mobile: 021 103 1622

Email: James.Weir@rbnz.govt.nz

Summary Record of Meeting – May 2024

The Monetary Policy Committee discussed recent developments in the domestic and global economies and the implications for monetary policy in New Zealand. Restrictive monetary policy is contributing to an easing in capacity pressures. Headline inflation, core inflation, and most measures of inflation expectations are continuing to decline. However, domestic inflation has fallen more slowly than expected and headline Consumers Price Index (CPI) inflation remains above the Committee's target band. Members of the Committee agreed that monetary policy needs to remain restrictive to ensure inflation returns to target within the forecast timeframe.

Aggregate global economic growth was below trend last year and is expected to slow further in 2024. However, the economic outlook varies among New Zealand's trading partners. In the United States, monetary policy has contributed to an easing in capacity pressures and inflation, but economic growth remains stronger than in many other developed economies. In most other advanced economies, domestic demand remains weak. In China, economic activity strengthened in early 2024, although continued weakness in the property sector remains a significant downside risk to growth.

The Committee noted that headline and core inflation have continued to decline in many advanced economies. To date, the decline in headline inflation internationally has been due in large part to lower goods, energy, and food price inflation. Inflation in services has declined, but by less than anticipated at the start of the year. Nevertheless, inflation in New Zealand's trading partners is expected to continue to decline.

In discussing global financial conditions, the Committee noted that persistent inflation in some of New Zealand's key trading partners has led to fewer policy interest rate cuts being priced in by financial markets. Higher long-term wholesale interest rates globally have supported wholesale interest rates in New Zealand. Participants in global financial markets continue to exhibit confidence in the corporate earnings outlook, as reflected in equity prices and credit spreads.

The Committee discussed recent developments in financial conditions in New Zealand. Overall, credit growth remains weak. The average interest rate across the stock of mortgage borrowers continues to increase and is near its projected peak of 6.5 percent. Bank funding costs are expected to increase over the forecast period as funding sources normalise, with a reversion to higher cost wholesale and term deposit funding. Higher funding costs in turn are expected to maintain upward pressure on lending rates over the medium term.

The Committee received an update on the continued sales of New Zealand Government Bonds held in the Large Scale Asset Purchase Programme portfolio. Despite the high level of bond issuance over recent years, measures of secondary market liquidity generally remain in line with historical averages and demand for New Zealand Government Bonds in the primary market remains strong.

The Committee discussed recent domestic economic developments. A prolonged period of restrictive interest rates is reducing household spending and residential and business investment. Capacity pressures in the New Zealand economy have eased significantly over the past year and aggregate demand is now broadly in line with the supply capacity of the economy.

Members noted that labour market pressures are easing and that businesses are reporting it is much easier to find workers. Labour supply has continued to increase, due to strong population growth, and wage growth has continued to decline but remains elevated.

The Committee discussed New Zealand's current low rate of productivity growth and its implications for lower potential output growth and higher capacity pressures. The Committee noted that the revised smaller negative output gap in the published projections is more consistent with recent persistence in domestic inflation pressure.

The Committee discussed possible causes of the current low productivity rate and whether they were temporary or more persistent. For example, some labour hoarding by firms is likely to have occurred in response to the previous acute labour shortages once New Zealand's borders were reopened. This could prove to be temporary.

The Committee noted that the forecast for government expenditure in the projections is based on Treasury's Half Year Economic and Fiscal Update (HYEFU) 2023, adjusted to reflect the December 2023 quarter GDP data. Based on this information, the share of government expenditure in the economy is projected to decline. However, due to weaker potential output growth, government expenditure is higher as a proportion of potential output than projected in the February Statement and hence less disinflationary.

The Committee also discussed the implications of the publicly announced aspects of Budget 2024 for the economic outlook. If the decline in government revenue due to tax cuts is fully offset by lower government expenditure, then the net impact on aggregate spending is broadly neutral over an extended horizon.

However, the Committee discussed how differences in the timing between potential lower government spending and lower tax rates are relevant to monetary policy. The Committee noted that the signalled lower government spending is currently and expected to continue contributing to weaker aggregate demand. However, any likely changes to government spending or private spending due to proposed tax cuts are not in the May Monetary Policy Statement projections. This timing difference poses an upside risk to the forecast of aggregate demand, the relevance of which for monetary policy will be clearer over coming quarters.

The Committee noted that the estimate of the long-run nominal neutral OCR used in the projections has been increased by 25 basis points to 2.75 percent, consistent with the Reserve Bank's indicator suite. The long-run nominal neutral rate affects the central economic projection but has a larger impact in the latter part of the forecast horizon and beyond. Members agreed that the current level of the OCR remains contractionary.

The Committee discussed recent inflation outturns. An easing in capacity pressures in the New Zealand economy and falling inflation expectations over the past 12 months are working to bring domestic inflation down. Annual CPI inflation fell to 4.0 percent in the March 2024 quarter but remains above the Committee's 1 to 3 percent target band.

Both tradable and non-tradables inflation contributed to the decline in headline CPI inflation. However, annual non-tradables inflation declined only slightly to 5.8 percent, which was higher than the 5.3 percent forecast. This upside surprise was broad-based across non-tradables inflation components.

The Committee discussed the outlook for non-tradables inflation. So far, the decline in non-tradables inflation has primarily been due to housing and construction costs, which are typically more sensitive to monetary policy. Further near-term disinflation in non-tradables is likely to be due to falling inflation for some market services, as labour market conditions continue to soften. However, this is expected to be tempered by some relative prices increases, such as for insurance, local authority rates, and dwelling rents.

Members discussed risks to the inflation outlook. The Committee agreed that risks to tradable inflation were balanced but noted that price changes may continue to be volatile. Risks remain to near-term inflation outcomes given ongoing trade disruptions. To date, developments in the Middle East have not resulted in a large increase in oil prices, and goods inflation continues to decline across advanced economies.

Members agreed that persistence in non-tradable inflation remains a significant upside risk. The influence of recent inflation outcomes on setting future inflation expectations is critical to price setting, wage expectations, and the stance of monetary policy. In addition, slower potential output growth than currently assumed would reduce the pace at which spending can grow without putting upward pressure on inflation. Monetary policy may need to tighten and/or remain restrictive for longer if wage and price setters do not align with weaker productivity growth rates.

Members discussed downside risks to the projections. In China, strengthening manufacturing capacity, alongside subdued domestic demand, could lead to a sharper decline in New Zealand import prices than currently assumed. Some members also noted the risk of a decline in global equity prices, particularly in the US. This risk arises from elevated pricing based on expectations of a near-term easing in US monetary policy, ongoing strong earnings growth, and a low-risk premium. Members noted that domestic labour market conditions could deteriorate more quickly than anticipated, particularly if firms reduce their labour force rapidly in response to weak demand.

In the context of persistent domestic inflation, weaker productivity growth, and uncertainty regarding the pace of normalisation in wage and price-setting behaviour, the Committee discussed the possibility of increasing the OCR at this meeting. The Committee assessed that, while the near-term balance of risks around inflation are skewed to the upside, there is more confidence that inflation will decline to within the target range over the medium term. However, the Committee also agreed that interest rates may have to remain at a restrictive level for longer than anticipated in the February Monetary Policy Statement to ensure the inflation target is met.

The Committee discussed the reasons why inflation is outside of the target range and the expected time for inflation to return to target. The Committee noted that the high inflation experienced both domestically and internationally over recent years reflected the significant disruption to global supply, production, and potential output stemming from the pandemic; the impact on demand of the global easing in monetary policy and the rise in fiscal spending during the pandemic; an increase in commodity prices and shipping costs resulting from war and geopolitical tension; severe weather impacts on local food prices; and the persistence of domestic inflation in part reflecting low productivity.

The Committee noted that annual headline CPI inflation was expected to return to the target band in the December quarter of this year. The Committee agreed that in the current circumstances, there is no material trade-off between meeting their inflation objectives and maintaining the stability of the financial system. The Committee noted that borrowers have faced a significant increase in interest costs, but banks are well placed to support their customers through this difficult period. Restrictive monetary policy settings are necessary to reduce demand in the economy, while avoiding unnecessary instability in output, employment, interest rates and the exchange rate.

In discussing the appropriate stance of monetary policy, members agreed they remain confident that monetary policy is restricting demand. A further decline in capacity pressure is expected, supporting a continued decline in inflation. The Committee agreed that interest rates need to remain at a restrictive level for a sustained period to ensure annual headline CPI inflation returns to the 1 to 3 percent target range.

On Wednesday 22 May, the Committee reached a consensus to keep the Official Cash Rate at 5.50 percent.

Attendees:

MPC members: Adrian Orr (Chair), Bob Buckle, Carl Hansen, Caroline Saunders, Christian Hawkesby, Karen Silk, Paul Conway

Treasury Observer: Dominick Stephens

MPC Secretary: Elliot Jones

Japan’s exports rise 8.3% yoy in Apr, imports up 8.3% yoy

In April, Japan's exports increased by 8.3% yoy to JPY 8981B, falling short of expected 11.1% growth. Nonetheless, this marks the fifth consecutive month of export growth and sets a record for April. Key contributors to this growth included hybrid cars, semiconductor-making equipment, and chips.

Imports also rose by 8.3% yoy to JPY 9443B, slightly below expected 9.0% increase, and set a record for the month. The weak Ten continues to inflate import costs for resource-scarce Japan, with crude oil prices jumping 17.7% yoy, compared to a 2.6% yoy increase in Dollar terms. This resulted in a trade balance deficit of JPY -463B.

On a seasonally adjusted basis, exports rose 0.9% mom to JPY 8843B, while imports decreased by -0.5% mom to JPY 9403B, leading to a trade balance deficit of JPY -561B.

BoE’s Bailey signals next move as rate cut amid expected drop in inflation

BoE Governor Andrew Bailey indicated overnight that he anticipates the next move in monetary policy will be a rate cut. He expects a significant decline in April's UK inflation data, but questions remain about how long the current level of monetary policy restriction will need to be maintained.

Bailey addressed the IMF's suggestion to hold a press conference after each rate-setting meeting, rather than just four times a year. He stated, "We will roll that question that the IMF have given to us into our thinking about implementing Ben Bernanke's changes."

ECB’s Nagel: June cut plausible, not on autopilot afterwards

In a newspaper interview, ECB Governing Council member Joachim Nagel expressed optimism about the current economic outlook, noting that "wage growth is expected to moderate as inflation continues to recede." He highlighted that recent developments are "heading in the right direction."

Nagel suggested that a first rate reduction in three weeks is "plausible," provided that incoming data and new projections align with policymakers' expectations. However, he cautioned against rushing into additional monetary easing, emphasizing, "We should not cut rates hastily and jeopardize what we have achieved."

He also underscored the high level of uncertainty, stating, "Even if rates are lowered for the first time in June, that does not mean we will cut rates further" in subsequent meetings. Nagel stressed that ECB's approach is not automatic, saying, "We are not on auto-pilot."

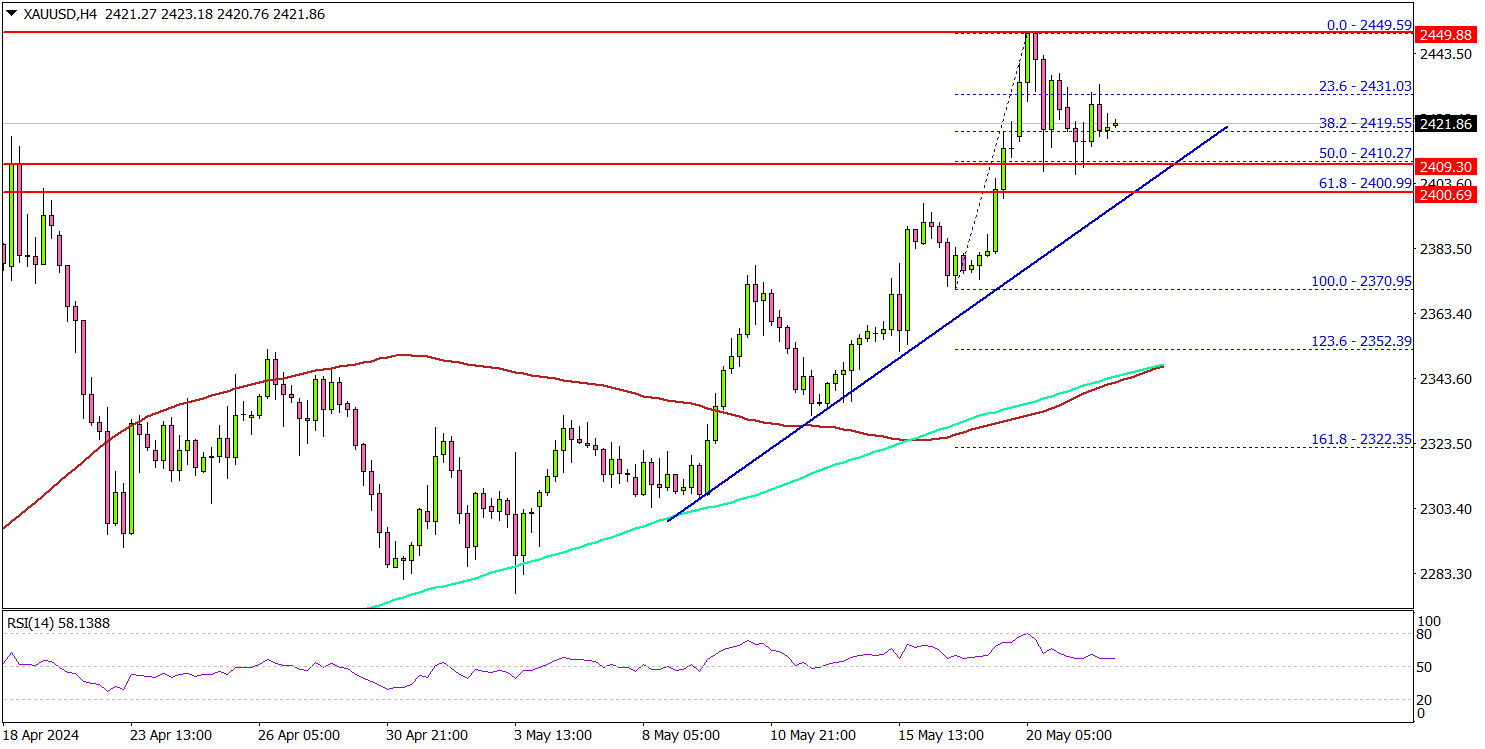

Gold Price Primed To Extend Gains – Here’s Why

Key Highlights

- Gold started a fresh increase above the $2,420 resistance.

- A connecting bullish trend line is forming with support at $2,410 on the 4-hour chart.

- Oil prices are consolidating losses below $80.00.

- EUR/USD could aim for a steady increase above the 1.0885 resistance.

Gold Price Technical Analysis

Gold prices started a fresh increase above the $2,385 resistance against the US Dollar. It traded above the $2,400 zone to move into the green zone.

The 4-hour chart of XAU/USD indicates that the price settled nicely above the $2,400 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours).

It traded as high as $2,449 and recently there was a downside correction. The price dipped below the $2,420 support and tested the 50% Fib retracement level of the upward move from the $2,370 swing low to the $2,449 high.

There is also a major bullish trend line forming with support at $2,410 on the same chart. A downside break below the $2,410 support might call for more downsides. The next major support is near the $2,385 level. Any more losses might send Gold prices toward $2,350.

On the upside, immediate resistance is at $2,435. The first major resistance is now near $2,450, above which the price could accelerate higher toward the $2,462 level.

Looking at Oil, the bears are still in control, and they could aim for another decline unless there is a move above the $81.20 resistance in the near term.

Economic Releases to Watch Today

- UK Consumer Price Index for April 2024 (YoY) – Forecast +2.1%, versus +3.2% previous.

- UK Core Consumer Price Index for April 2024 (YoY) – Forecast +3.6%, versus +4.2% previous.

- US Existing Home Sales for April 2024 (MoM) - Forecast -1.2%, versus -4.3% previous.

NZD/USD Overview Ahead of The Reserve Bank of New Zealand Official Cash Rate

Reserve Bank of New Zealand Consumer Price Index

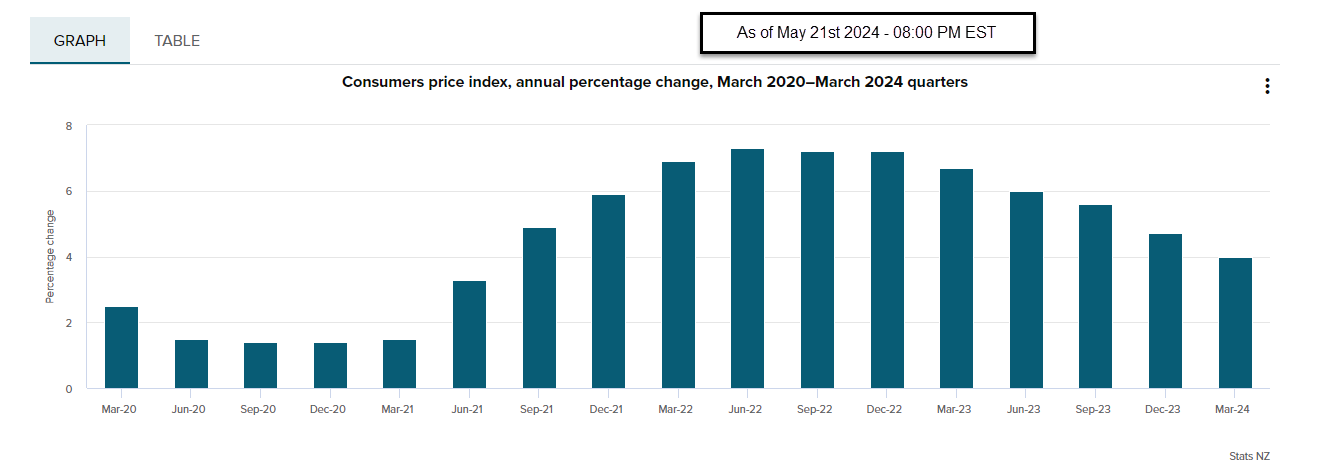

New Zealand Dollar traders eagerly anticipate the Reserve Bank of New Zealand’s Official Cash Rate (OCR), a critical event that can significantly impact the market. Over the past two years, inflation in New Zealand has mirrored global trends. The CPI Y/Y, encompassing all items, has dropped from its 2022 peak of 7.30% and currently rests at 4.00%. Despite this decline, New Zealand’s CPI remains relatively high compared to other global economies, indicating a unique economic landscape. Traders will also pay attention to domestic (non-tradeable) inflation, which measures goods and services that do not face foreign competition. However, the inputs of these goods and services can be influenced by foreign competition.

According to Bloomberg’s World Interest Rate Projection Model, the probability of an RBNZ rate cut for the May 22nd meeting stands at 1%; however, it increases as we approach year-end as more traders anticipate the cuts later in the year. The RBNZ Shadow Board members recommended that RBNZ keep the Official cash rate OCR at 5.5% and cut rates in 2025.

Weekly Chart Technical Analysis

- NZD has been trading within a widening formation as of January 2023, marked by red lines on the weekly chart, and is approaching the upper pattern borderline.

- A confluence of resistance lies within the range of 0.6170 – 0.6260, represented by the upper channel borderline, the standard monthly R2 and R3, and the annual pivot point at 0.6210.

- A potential inverted head and shoulder pattern is currently under formation, and its neckline aligns with the widening pattern of the upper borderline.

- Negative divergence between price action and tick volume; however, volume bars rose for the same duration. Tick volume does not represent real volume; however, it behaves similarly to standard volume indicators in certain cases.

- MACD line crossed above its signal line and aligned with price action.

- Price action broke and closed above multiple short and intermediate moving averages, the EMA9, SMA9, and the SMA20.

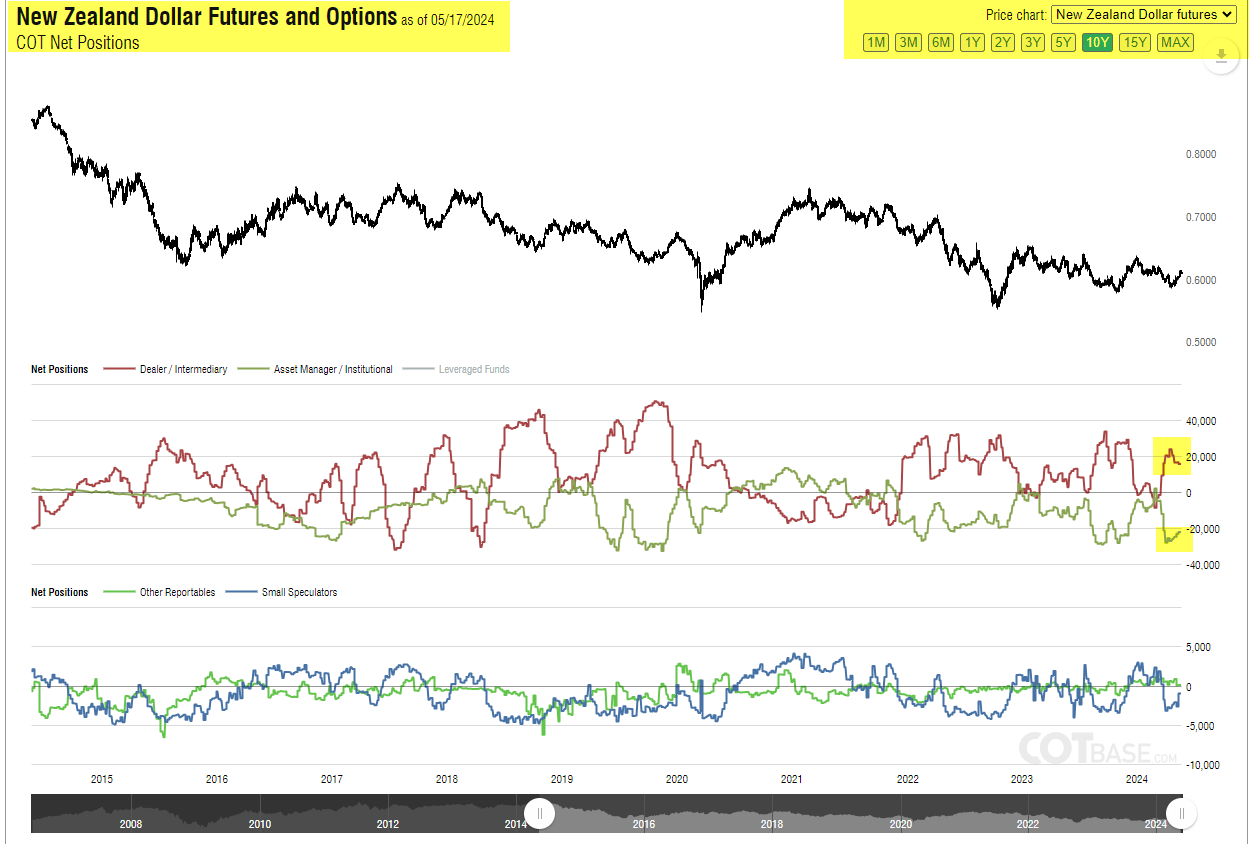

COT Report

- The latest COT report for the week ending on May 17th, 2024 (Includes data up to the end of day Tuesday, May 14th, 2024) shows that Large Speculator and Commercials positioning levels are in line with price action after remaining at their all-time extremes for few weeks, a sharp change in positioning towards long for large speculators and the opposite for commercials.

ETHUSD Heads Towards 2024 Highs on ETF Approval Hopes

- ETHUSD set to notch up a second straight day of sharp gains

- Hopes of spot ether ETF trigger broad-based crypto rally

- But danger that upswing is becoming overstretched

ETHUSD (ether) has charged through its 50-day simple average (SMA) to make a fresh bid for the March peak of 4,093.70, which was a more than two-year high. The surge comes on renewed speculation that an approval by the US Securities and Exchange Commission for a spot ether ETF is imminent.

The momentum indicators point to a strong bullish bias in the near term, but there is a growing risk of a negative correction. Both the RSI and the stochastics have just entered their respective overbought territories.

If ETHUSD extends its rally, the March high of 4093.70 is the first point of call, after which attention would turn to the 4,400.00 zone, which was a frequently tested region from October to December 2021. Breaking above 4,400.00 could pave the way for the all-time high of 4,867.60.

However, should the price go into reverse, there could be some support at the 38.2% Fibonacci retracement of the January-March upleg at 3,356.86. Further down, the 50-day SMA could attempt to halt the decline around 3,161.50. But a more crucial support is the 61.8% Fibonacci of 2,901.64. A breach of this level would shift the risks to the downside.

In brief, there could be some further limited gains for ETHUSD in the short term before the rally pauses for breath. But the price needs to surpass the March top to put the uptrend on a more sustainable footing, whereas a drop below the 61.8% Fibo would invite the bears.

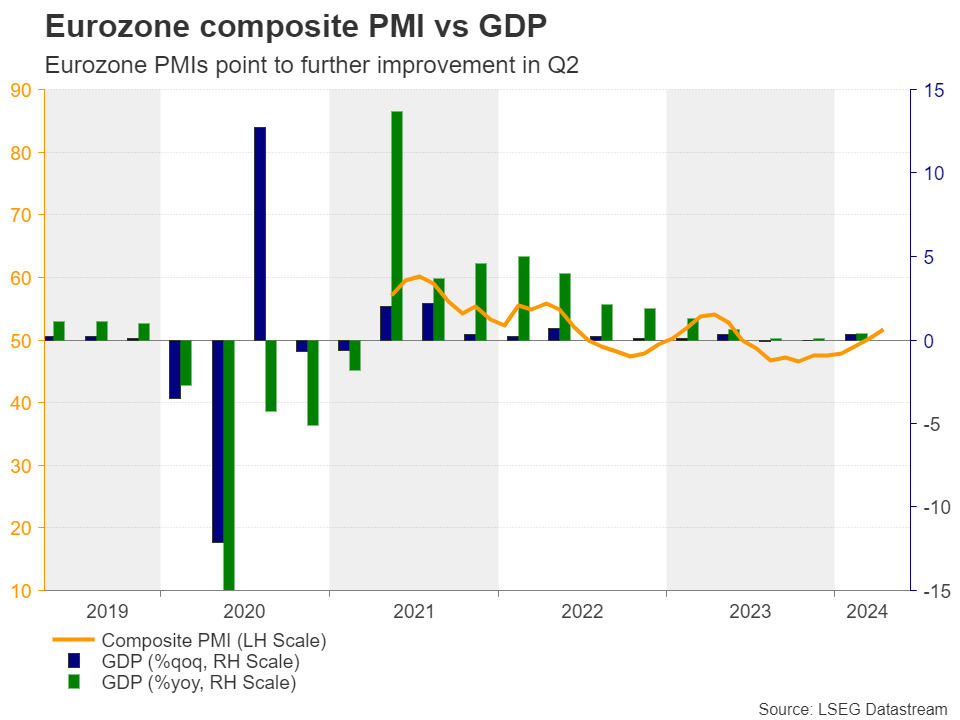

How Will Eurozone PMIs Impact ECB Expectations?

- Eurozone economy has been improving in 2024

- But investors still anticipate an ECB rate cut in June

- The flash PMIs could impact bets beyond that meeting

- The data comes out on Thursday at 08:00 GMT

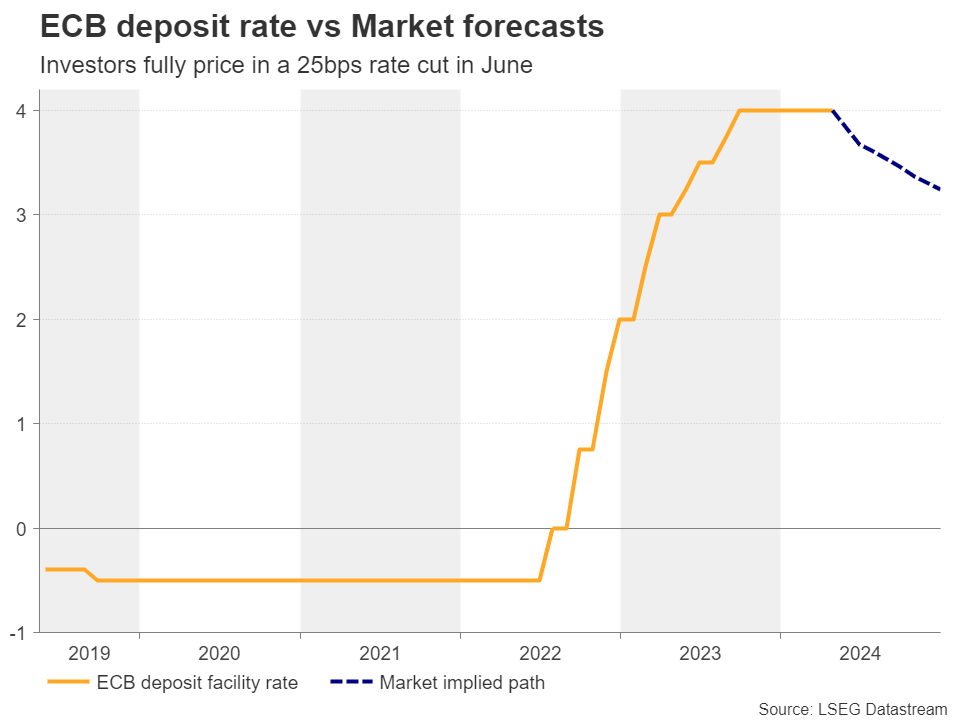

ECB signals confidence in lowering rates

At their latest gathering, ECB officials decided to keep interest rates unchanged as expected but they sent clearer signals that they may start lowering them soon. At the press conference, President Lagarde said that the decline in inflation is comforting and that a few members felt sufficiently confident to cut rates.

Although she did not explicitly refer to a specific timing, a few hours after her speech, a report citing three sources close to the ECB discussion revealed that policymakers were expected to cut interest rates in June.

Economy improves, but June cut a done deal

Since then, the CPI figures for April revealed that the headline rate held steady at 2.4% y/y and the core one slowed by less than anticipated, to 2.7% y/y from 2.9%. On top of that, the GDP data for Q1 pointed to a larger-than-expected rebound in Eurozone economic activity, after the bloc fell into a mild recession during the second half of 2023. According to the PMIs, the improvement continued in April, but investors remained convinced that the ECB will deliver its first quarter-point cut in June. They are pricing 40 more basis points for the rest of the year.

On Thursday, the flash PMI surveys for May are due to be released and the forecasts point to more improvement. That said, with ECB policymakers themselves continuing to signal a strong likelihood for a first rate reduction in June, investors are unlikely to scale back their June cut bets even if there is an upside surprise. They could however take off the table some basis points worth of cuts expected for the rest of the year, which could still prove positive for the euro.

Euro/dollar seeks opportunity to break 1.0885

From a technical standpoint, euro/dollar pulled back after hitting resistance slightly above the 1.0885 zone, which stopped the bulls from drifting north on April 9. However, the pair remains above the downtrend line drawn from the high of December 28 and above the 200-day exponential moving average (EMA), which currently coincides with the 1.0800 key support.

Ergo, a better-than-expected set of PMIs on Thursday may encourage buyers to take the reins again and perhaps push the price above 1.0885. Such a move will confirm a higher high and perhaps pave the way towards the high of March 21 at 1.0930. A break higher could see scope for extensions towards the high of March 8 at 1.0980 or the psychological round figure of 1.1000, which offered resistance back on January 5 and 11.

On the downside, for the outlook to start looking bearish, the pair may need to drop below the key support area of 1.0725 as this will also take the action below the short-term uptrend line drawn from the low of April 16.