Sample Category Title

Sunset Market Commentary

Markets

The EMU economy came close to stabilizing in March with price pressures easing. The composite PMI recovered slightly more than hoped, from 49.2 to 49.9 (vs 49.7 consensus), matching the best (least bad) outcome since June of last year. Divergence between a weak export-oriented manufacturing sector (45.7 from 46.5) and a recovering domestic services industry (51.1 from 50.2) increased. Ongoing falls in output in France (composite 47.7) and Germany (composite 47.4; mainly manufacturing weakness) offset a gathering upturn in the rest of the EMU, pointing to an even more uneven economic picture. Encouragingly, order books fell at a reduced rate and business confidence about the year ahead improved to a 13-month high. In manufacturing, destocking is close to no longer being a drag on production. Supplier delivery times at goods producers improved, facilitating a further fall in manufacturing input prices. Service sector input cost and selling price inflation rates meanwhile remained elevated due to higher wage costs, though a cooling in the pace of increase in cost burdens was recorded. Today’s PMI’s keep the ECB on schedule to conduct a first 25 bps rate cut in June. Following the release, EUR/USD fell back from 1.0940 to just below 1.09. Early US eco data (consensus-beating Philly Fed Business Outlook, another low number of weekly jobless claims and decent PMI’s; composite 52.2) help the greenback out as well. German yields currently lose up to 3.5 bps at the front end of the curve, but that’s mainly because of lower opening catching up with yesterday’s post-Fed market reaction. Changes on the US yields curve vary between -0.9 bps (30-yr) and +3 bps (2-yr).

The Bank of England kept its policy rate unchanged at 5.25%, but the voting pattern changed. Hawkish members Mann and Haskel no longer advocate a 25 bps rate hike, joining the majority. BoE Dhingra voted for a second consecutive meeting in favor of a 25 bps rate cut and is now the sole dissenter on the 9-headed MPC. Forward guidance at today’s intermediate meeting was left unchanged as well: the BoE keeps under review how long rates should be kept unchanged. Minutes added that monetary policy could remain restrictive even in case of rate cuts. “Things are moving in the right direction”, BoE chair Bailey later added at the press conference stressing encouraging signs that inflation is coming down. CPI inflation is projected to fall to slightly below the 2% target in 2024 Q2, marginally weaker than previously expected owing to the freeze in fuel duty announced in the Budget. UK Gilts outperform today with yields sliding up to 7 bps for the 2-yr tenor as market thinking shifts from the August to the June meeting for a first BoE rate cut. EUR/GBP rises from 0.8540 to 0.8560.

News & Views

The Swiss National Bank cut its policy rate by 25 bps to 1.50% after recently suggesting that the (real) appreciation of the franc had contributed more than enough to slow inflation. It also further eroded (export) demand. The SNB sharply downwardly revised its 2024-26 inflation forecast. At 1.4%, 1.2% and 1.1% respectively, inflation remains easily within the 0%-2% price stability band. In the short term, goods prices in particular continue to ease while inflation is mainly driven by services prices. Longer term, the risk of second-round effects is significantly reduced. With inflation back on track, the SNB can shift its focus back to stimulating economic growth. The SNB expects (moderate) growth of 1% this year and unemployment may rise a bit further. The Swiss franc takes a logical step back from EUR/CHF 0.9675 to 0.9765. The SNB officially has no exchange rate target, but a further depreciation to EUR/CHF 1.00 would probably be welcomed. If this (real) FX correction doesn’t go according to plan, the SNB may further scale back policy tightening in June given low inflation. We don’t see today’s SNB's action as a harbinger of global "frontloading" of monetary easing. Switzerland is in a unique situation.

The Norges Bank kept its policy rate unchanged at 4.5%. Monetary policy is having a tightening effect and economic growth is low. Inflation is slowing but still markedly above target (4.5% Y/Y in February), mainly because of elevated services inflation. Sharply increased business costs, high wage growth and the Norwegian krone’s depreciation through 2023 will contribute to keeping inflation elevated ahead. Compared to the December policy report, growth was nevertheless higher than expected while inflation cooled more. The MPC remains concerned that prematurely lowering its policy rate could keep inflation high and is ready to raise the policy rate again if necessary. The base scenario assumes unchanged rates until autumn though. EUR/NOK is little changed at 11.55.

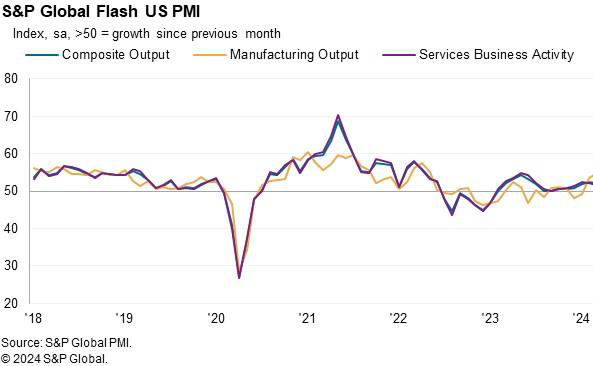

US PMI composite falls to 52.2, unwelcome consumer price pressure in the coming months

US PMI Manufacturing rose from 52.2 to 52.5 in March, a 21-month high. PMI Services fell from 52.3 to 51.7. PMI Composite also fell from 52.5 to 52.2.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

"Further expansions of both manufacturing and service sector output in March helped close off the US economy's strongest quarter since the second quarter of last year. The survey data point to another quarter of robust GDP growth accompanied by sustained hiring as companies continue to report new order growth.

"The brightest news came from the manufacturing sector, where production is now growing at the fastest rate since May 2022. Production gains are linked to improving demand for goods both at home and abroad, driving a further upturn in business confidence in the outlook.

"Service providers meanwhile reported a slower pace of expansion than factories, with the rate of increase also moderating slightly compared to February, linked in part to ongoing cost of living pressures. However, service providers have also become increasingly optimistic about the outlook, with confidence striking a 22-month high in March to suggest the broad-based economic expansion seen in March will persist into the summer.

"A steepening rise in costs, combined with strengthened pricing power amid the recent upturn in demand, meant inflationary pressures gathered pace again in March. Costs have increased on the back of further wage growth and rising fuel prices, pushing overall selling price inflation for goods and services up to its highest for nearly a year. The steep jump in prices from the recent low seen in January hints at unwelcome upward pressure on consumer prices in the coming months."

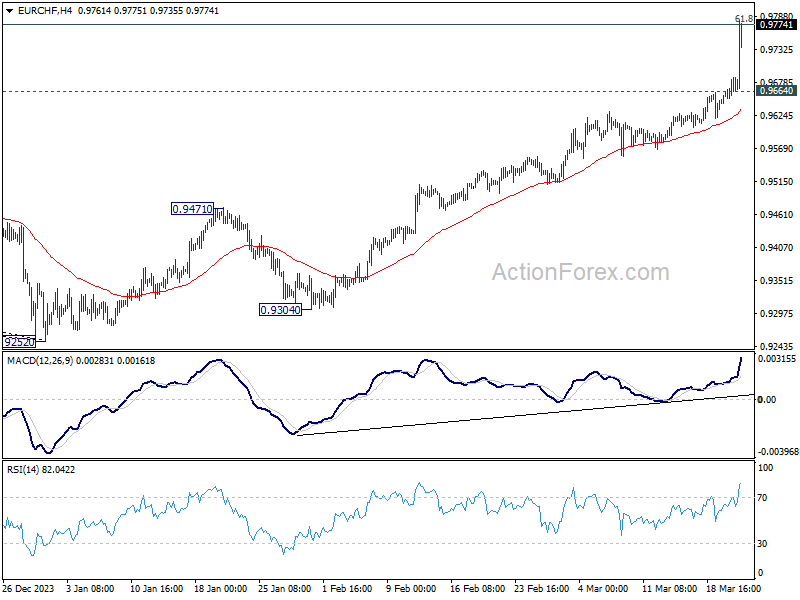

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9656; (P) 0.9672; (R1) 0.9703; More..

EUR/CHF surges to as high as 0.9780 today and met 61.8% retracement of 1.0095 to 0.9252 at 0.9773 already. The strong break of 0.9683 resistance carries larger bullish implications. Intraday bias stays on the upside. Sustained trading above 0.9773 will pave the way to 1.0095 key resistance next. On the downside, below 0.9664 minor support will turn intraday bias neutral and bring consolidations, before staging another rally.

In the bigger picture, the strong break of 0.9683 resistance indicates medium term bottoming at 0.9252 already, on bullish convergence condition in W MACD. Rise from there would now target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303. This will remain the favored case as long as 55 D EMA (now at .9530) holds.

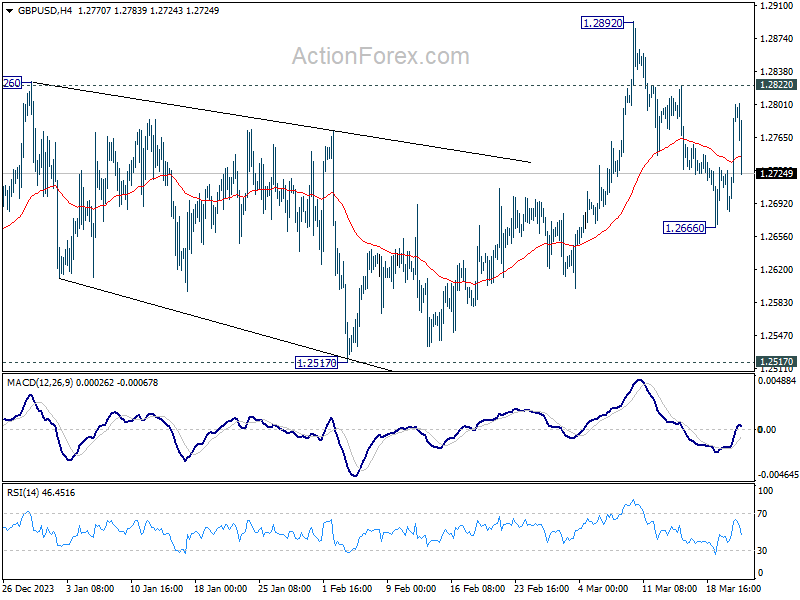

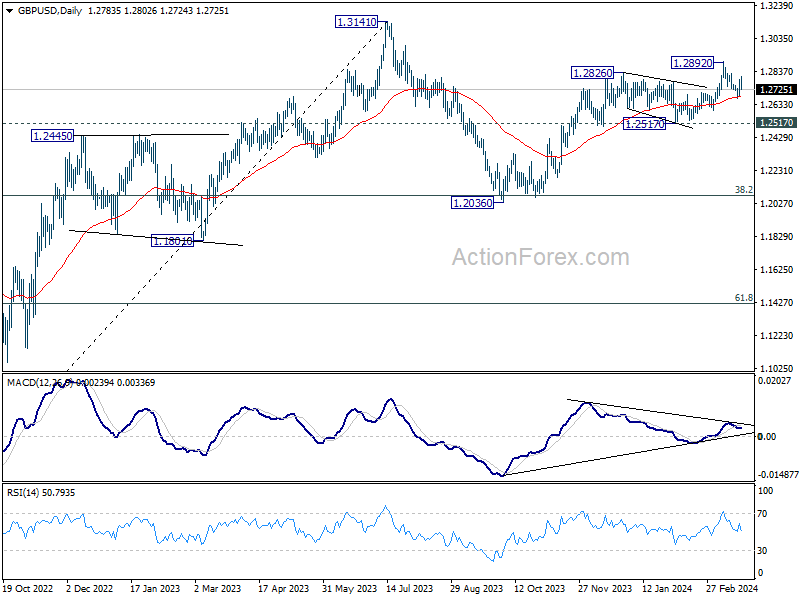

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2718; (P) 1.2753; (R1) 1.2820; More...

Intraday bias in GBP/USD remains neutral at this point. On the downside, break of 1.2666 support and sustained break of 55 D EMA (now at 1.2685) will target 1.2517 structural support next. However, break of 1.2822 will bring further rally to retest 1.2892 instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

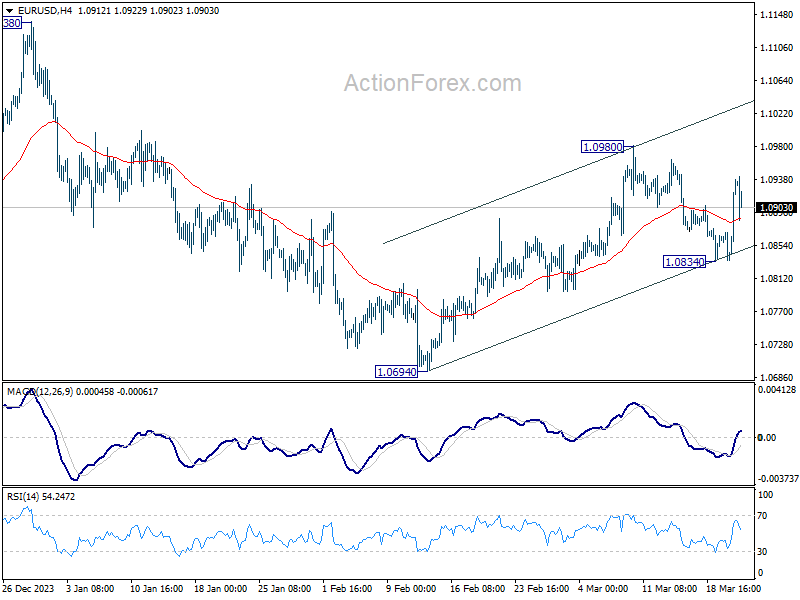

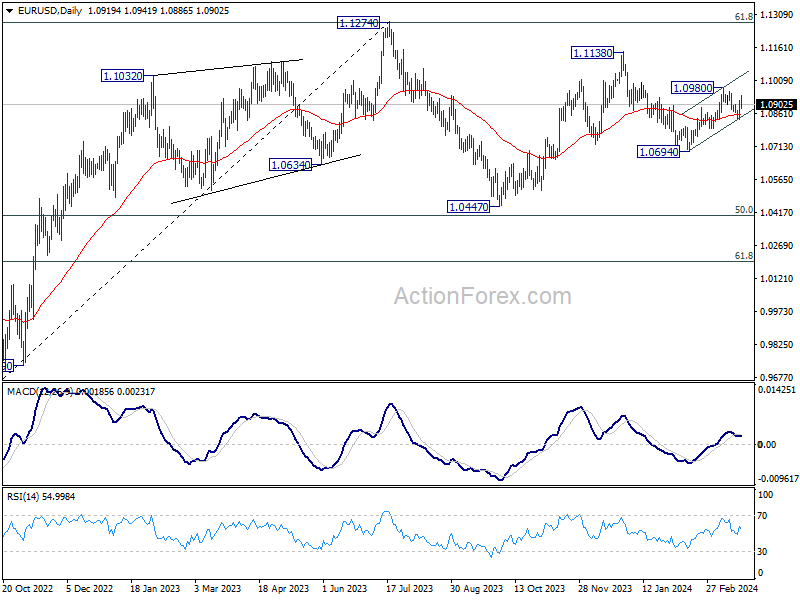

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0864; (P) 1.0894; (R1) 1.0951; More...

Intraday bias in EUR/USD stays mildly on the downside at this point. Pull back from 1.0980 has possibly completed at 1.0834, after drawing support from 55 D EMA. Firm break of 1.0980 resistance will resume the rise from 1.0694. On the downside, sustained trading below 55 D EMA (now at 1.0861) will argue that rebound from 1.0694 has completed and bring retest of this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

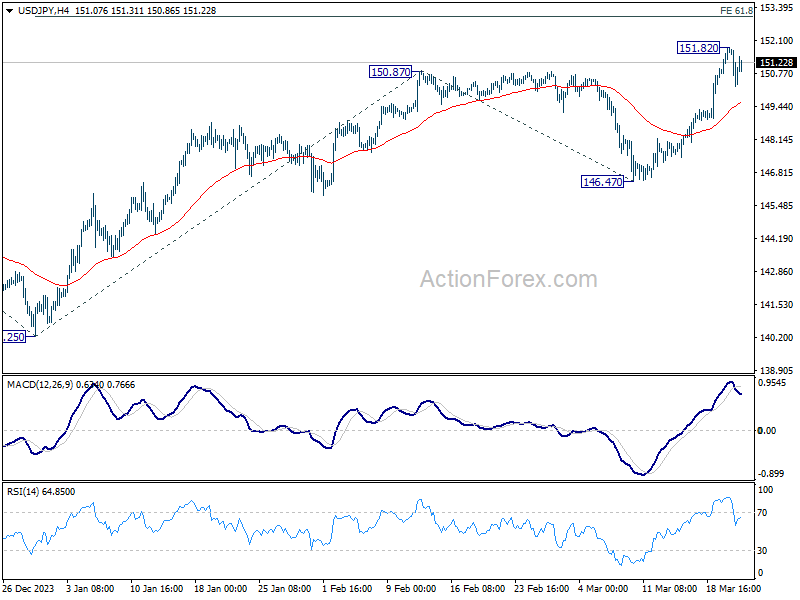

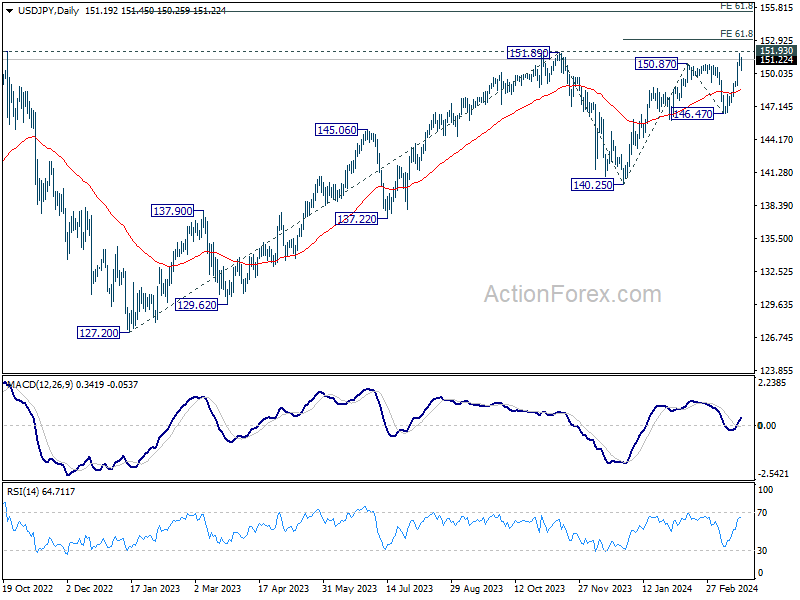

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 150.71; (P) 151.26; (R1) 151.80; More...

Intraday bias in USD/JPY remains neutral as consolidations continue below 151.82 temporary top. Further rise is expected as long as 55 4H EMA (now at 149.63) holds. On the upside, decisive break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03. However, sustained trading below 55 4H EMA will bring deeper fall back to 146.47 support instead.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

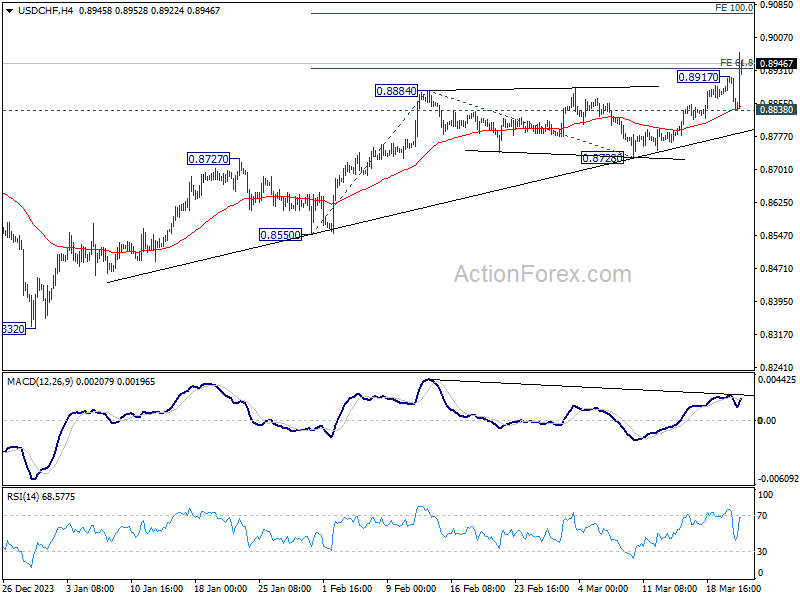

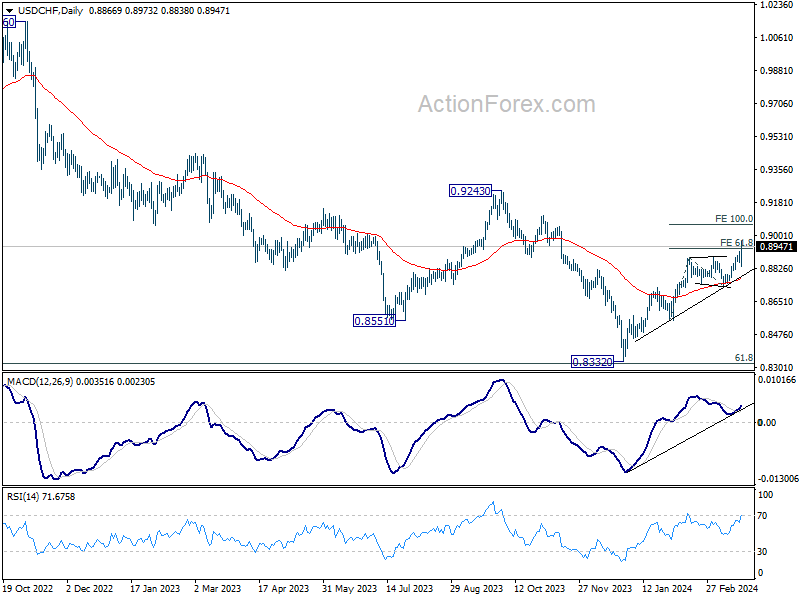

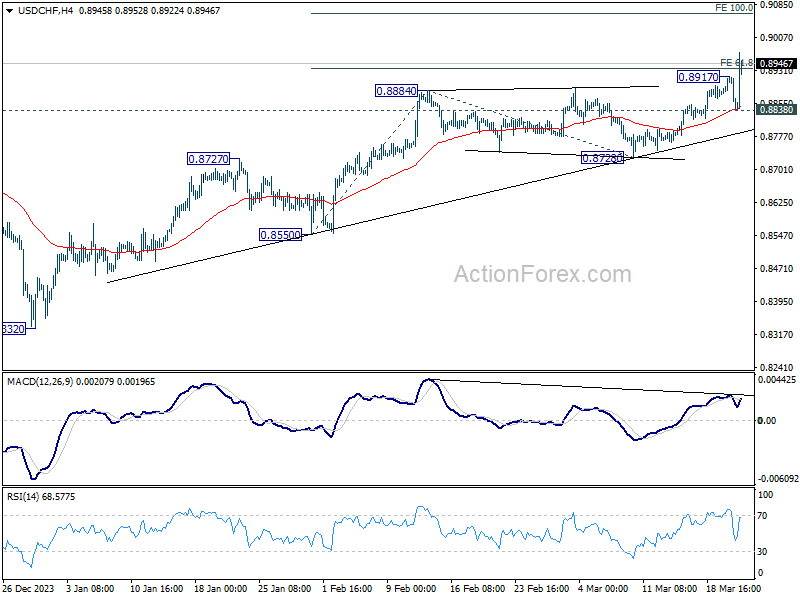

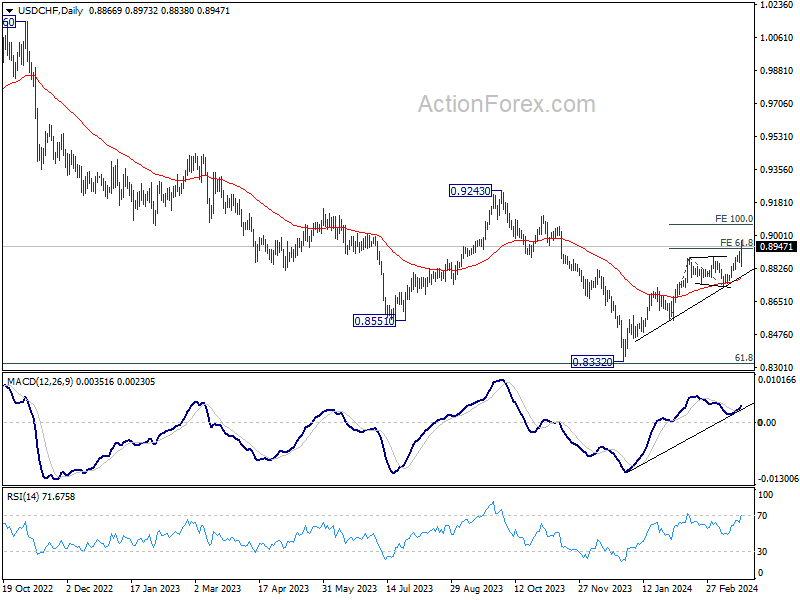

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8846; (P) 0.8882; (R1) 0.8905; More....

USD/CHF's rally resumed after drawing support from 55 4H EMA, and breaks through 0.8917. Intraday bias is back on the upside. Next target is 100% projection projection of 0.8550 to 0.8884 from 0.8728 at 0.9062. On the downside, below 0.88338 minor support will turn intraday bias neutral again. But still, outlook will remain bullish as long as 0.8728 support holds.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

Swiss Franc Tumbles on SNB Cut; Sterling Falters as Hawks Retreat

Swiss Franc is trading as the day's most significant loser in the wake of SNB's surprising decision to cut interest rates. This move, along with a substantial downward revision of inflation forecasts, is seen by some economists as a strategic effort by SNB to alleviate the burden of a high exchange rate on Switzerland's export-driven economy. Speculation is rife among economists about the possibility of another rate reduction in June, particularly if ECB commences its policy easing by then.

British Pound also faced downward pressure as the second worst performer, following BoE decision to maintain its interest rate unchanged. Notably, two previously hawkish members abandoned their stance on calling for a hike. Yet BoE provided no definitive guidance on rate reductions. Despite some progress in reducing inflation, service sector prices continue to be a concern, remaining stubbornly high.

The Australian Dollar stands out as the day's strongest currency, buoyed by impressive employment data and PMI improvements, hinting at less likelihood of an immediate RBA rate cut. Meanwhile, Yen is making a modest recovery from its sharp post-BoJ losses earlier in the week, and Dollar is regaining some ground lost to yesterday's risk-on sentiment. Euro and Canadian Dollar held their ground in the market's middle tier.

Technically, one focus now is whether EUR/GBP could ride on the currency wave of Sterling selloff. Firm break of 0.8577 resistance will be an indication of near term bullish reversal, and target medium term trend line resistance at around 0.8670.

In Europe, at the time of writing, FTSE is up 1.58%. DAX is up 0.39%. CAC is up 0.01%. UK 10-year yield is down -0.0468 at 4.078. Germany 10-year yield is down -0.027 at 2.410. Earlier in Asia, Nikkei rose 2.03% to new record. Hong Kong HSI rose 1.93%. China Shanghai SSE fell -0.08%. Singapore Strait Times rose 1.35%. Japan 10-year JGB yield rose 0.0086 to 0.740.

BoE maintains status quo as hawks relinquish rate hike demands

BoE maintained the Bank Rate at 5.25% as widely expected. The decision was made by an 8-1 vote, with Swati Dhingra singularly advocating for a reduction again. Notably, previous hawks Jonathan Haskel and Catherine Mann adjusted their positions, refraining from advocating for hikes this round.

BoE noted that February's CPI inflation rate of 3.4% was marginally lower than forecasted in the the latest Monetary Policy Report. Despite a decline in services consumer price inflation, it remains significantly high. Nevertheless, most measures of short-term inflation expectations are on a downtrend.

With the government's decision to freeze fuel duty, CPI is projected to dip slightly below 2% mark in the second quarter. However, a slight uptick is anticipated in the latter half of the year.

UK PMI manufacturing hits 20-month high, services ease slightly

UK PMI Manufacturing rose from 47.5 to 49.9 in March, above expectation of 47.9, a 20-month high. PMI Services fell slightly from 53.8 to 53.4, below expectation of 53.8. PMI Composite ticked down from 53.0 to 52.9.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, interprets the data as evidence of UK's recovery from the recession in the latter half of 2023. The aggregate business activity for Q1 suggests 0.25% GDP growth, marking the best quarter since mid-last year

Despite the optimistic growth indicators, inflation remains a pressing issue, particularly in the services sector, where "stubbornly sticky" inflation pressures continue. Moreover, the manufacturing sector saw "renewed inflation".

While the overall inflation rate is expected to decline in the coming months, March's PMI data point to "elevated underlying price pressures," possibly influencing BoE to exercise caution. Williamson, suggests that a decisive shift towards lower interest rates should only occur once there is clear evidence of moderating wage growth.

SNB cuts interest rate, sharply slashes inflation forecasts

In a surprising move, SNB announced a -25bps cut in its policy rate, bringing it down to 1.50%. This decision also introduced a tiered system for the remuneration of banks' sight deposits held at SNB. Deposits up to a specified threshold will earn interest at the policy rate, while those exceeding this limit will attract only 1.0% higher rate. Furthermore, SNB affirmed its readiness to intervene in the foreign exchange market if deemed necessary.

The rationale behind the rate cut, as outlined by the SNB, is the "effective" management of inflation over the past two and a half years, which has allowed inflation rates to settle below the 2% mark for several months. This achievement aligns with the SNB's definition of price stability and sets the stage for a conducive economic environment in the foreseeable future.

The new conditional inflation forecasts are revised sharply lower even with a lower policy rate. SNB project a modest increase in inflation from 1.2% in Q1 to 1.5% in Q2 of this year, followed by a decline to 1.2% in Q1 2025, and a further decrease to 1.1% in the second half of 2026.

Eurozone PMI composite ticks up to 49.9, price development not enough to alter ECB's course

Eurozone PMI Manufacturing from 46.5 to 45.7 in March, below expectation of 47.0. PMI services, on the other hand rose from 50.2 to 51.5, above expectation of 50.5 a 9-month high. PMI Composite ticked up from 49.2 to 49.9, also a 9-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted the "clear weakness" in manufacturing, attributing it largely to Germany's industrial performance. On a brighter note, the further expansion in the services PMI is considered a "positive development."

From a monetary policy perspective, ECB may find some solace in the report's implications on inflationary pressures. Notably, the services sector, which is typically sensitive to wage dynamics, has not seen a further escalation in price pressures.

However, these developments, as de la Rubia notes, are "not enough" to alter the ECB's tentative plan to commence rate cuts in June, rather than an earlier move in April.

Also released, France PMI Manufacturing fell from 47.1 to 45.8. PMI Services fell from 48.4 to 47.8. PMI Composite fell from 48.1 to 47.7.

Germany PMI Manufacturing fell from 42.5 to 41.6. PMI Services rose from 48.3 to 49.8. PMI Composite rose from 46.3 to 47.4.

BoJ's Ueda assures continued accommodative monetary stance following rate hike

Addressing the parliament today, BoJ Governor Kazuo Ueda articulated the rationale behind this week's exit from the long-standing negative interest rate policy and the subsequent rate hike. This move marks a significant shift for Japan's monetary policy, which had been entrenched in a negative interest rate environment for eight years.

Ueda pointed out, "We could have waited until inflation is completely at 2% for a long period of time. But if we did so, it's unclear whether inflation would have stayed at 2%. We might have seen a sharp increase in upside price risks," highlighting the preemptive nature of the BoJ's action.

The decision was influenced by recent trends in service prices and substantial wage increases resulting from annual wage negotiations, indicating a strengthening cycle of wage growth and inflation in Japan.

Despite this historical step, Ueda underscored that Japan's inflation expectations for the medium and long term are "still in the process of accelerating towards 2%". He assured that BoJ remains committed to supporting the economy and prices "by maintaining accommodative monetary conditions for the time being".

He also hinted at future adjustments, stating, "As we exit our massive stimulus program, we will gradually shrink the size of our balance sheet and at some point reduce the size of our government bond buying."

Japan's PMI composite rises to 52.3, strengthening activity and intensifying price pressures

Japan's PMI Manufacturing saw a modest increase from 47.2 to 48.2 in March, while PMI Services surged to from 52.9 to 54.9, its highest level since last May. Composite PMI, which combines both sectors, also climbed from 50.6 to 52.3, reaching its peak since last August.

Usamah Bhatti, Economist at S&P Global Market Intelligence, underscored the private sector's regained momentum at the end of Q1. The expansion was predominantly driven by service providers, while manufacturers experienced a continued, though less severe, contraction.

Alongside this economic revival, Japan is facing a "renewed intensification of price pressures," with the rate of input price inflation hitting a five-month high. This uptick was particularly pronounced among service providers, although manufacturers also reported "stubbornly high input prices". Many firms opted to pass these increased costs onto customers, leading to the highest output charge inflation since last August.

Australia employment surges 116.5k, unemployment rate dives to 3.7%

Australia employment grew strongly by 116.5k in February, well above expectation of 40.2k. Full-time jobs rose 78.2k while part-time jobs rose 38.3k.

Unemployment rate fell sharply from 4.1% to 3.7%, below expectation of 4.0%. Participation rate rose 0.1% to 66.7%. Monthly hours worked also rose 2.8% mom.

Australia PMI composite rises to 11-month, another blow to RBA rate cut expectations

Australia PMI Manufacturing PMI dropped to a 46-month low of 46.8. Conversely, PMI Services climbed to an 11-month peak of 53.5, with the Composite PMI also reaching an 11-month high at 52.4.

Warren Hogan, Chief Economic Advisor at Judo Bank, highlighted that Composite Output Index's increase for the fourth consecutive month signifies the economy's rebound from the cyclical slowdown experienced in 2023. Meanwhile However, inflation remains a concern, with service sector readings indicating persistently high producer and consumer prices.

Hogan noted that the results are "another blow to rate-cut expectations" for RBA. The rebound in economic activity, coupled with inflation exceeding targets, not only diminishes the likelihood of rate reductions, but also raises the possibility of further monetary tightening in 2024. This aligns with recent warnings from RBA.

New Zealand in technical recession as Q4 GDP contracts -0.1% qoq

New Zealand's economy has officially entered technical recession, with GDP contracting by -0.1% qoq in Q4, below expectation of 0.0% qoq. This decline follows -0.3% contraction in Q4, marking two consecutive quarters of negative growth.

GDP per capita declined decline of -0.7% qoq, while real gross national disposable income saw a -1.4% qoq drop.

The contraction was not uniformly felt across all sectors. Of the sixteen industries analyzed, eight experienced growth, notably the rental, hiring, and real estate services sector, alongside public administration, safety, and defense.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8846; (P) 0.8882; (R1) 0.8905; More....

USD/CHF's rally resumed after drawing support from 55 4H EMA, and breaks through 0.8917. Intraday bias is back on the upside. Next target is 100% projection projection of 0.8550 to 0.8884 from 0.8728 at 0.9062. On the downside, below 0.88338 minor support will turn intraday bias neutral again. But still, outlook will remain bullish as long as 0.8728 support holds.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q4 | -0.10% | 0.00% | -0.30% | |

| 22:00 | AUD | Manufacturing PMI Mar P | 46.8 | 47.8 | ||

| 22:00 | AUD | Services PMI Mar P | 53.5 | 53.1 | ||

| 23:50 | JPY | Trade Balance (JPY) Feb | -0.45T | -0.85T | 0.24T | 0.01T |

| 00:30 | JPY | Manufacturing PMI Mar P | 48.2 | 47.5 | 47.2 | |

| 00:30 | AUD | Employment Change Feb | 116.5K | 40.2K | 0.5K | 15.3K |

| 00:30 | AUD | Unemployment Rate Feb | 3.70% | 4.00% | 4.10% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | 7.5B | 5.2B | -17.6B | -17.0B |

| 08:15 | EUR | France Manufacturing PMI Mar P | 45.8 | 47.3 | 47.1 | |

| 08:15 | EUR | France Services PMI Mar P | 47.8 | 48.6 | 48.4 | |

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 41.6 | 43.5 | 42.5 | |

| 08:30 | EUR | Germany Services PMI Mar P | 49.8 | 48.9 | 48.3 | |

| 08:30 | CHF | SNB Interest Rate Decision | 1.50% | 1.75% | 1.75% | |

| 09:00 | CHF | SNB Press Conference | ||||

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 39.4B | 32.3B | 31.9B | |

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 45.7 | 47 | 46.5 | |

| 09:00 | EUR | Eurozone Services PMI Mar P | 51.1 | 50.5 | 50.2 | |

| 09:30 | GBP | Manufacturing PMI Mar P | 49.9 | 47.8 | 47.5 | |

| 09:30 | GBP | Services PMI Mar P | 53.4 | 53.8 | 53.8 | |

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% | 5.25% | |

| 12:00 | GBP | MPC Official Bank Rate Votes | 0--1--8 | 0--1--8 | 2--1--6 | |

| 12:30 | CAD | New Housing Price Index M/M Feb | 0.10% | 0.10% | -0.10% | |

| 12:30 | USD | Initial Jobless Claims (Mar 15) | 210K | 210K | 209K | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Mar | 3.2 | 0.2 | 5.2 | |

| 12:30 | USD | Current Account (USD) Q4 | -195B | -209B | -200B | |

| 13:45 | USD | Manufacturing PMI Mar P | 51.9 | 52.2 | ||

| 13:45 | USD | Services PMI Mar P | 52 | 52.3 | ||

| 14:00 | USD | Existing Home Sales Feb | 3.94M | 4.00M | ||

| 14:30 | USD | EIA Natural Gas Storage Change (Mar 15) | 5B | -9B |

BoE maintains status quo as hawks relinquish rate hike demands

BoE maintained the Bank Rate at 5.25% as widely expected. The decision was made by an 8-1 vote, with Swati Dhingra singularly advocating for a reduction again. Notably, previous hawks Jonathan Haskel and Catherine Mann adjusted their positions, refraining from advocating for hikes this round.

BoE noted that February's CPI inflation rate of 3.4% was marginally lower than forecasted in the the latest Monetary Policy Report. Despite a decline in services consumer price inflation, it remains significantly high. Nevertheless, most measures of short-term inflation expectations are on a downtrend.

With the government's decision to freeze fuel duty, CPI is projected to dip slightly below 2% mark in the second quarter. However, a slight uptick is anticipated in the latter half of the year.

(BOE) Bank rate maintained at 5.25%

Monetary Policy Summary, March 2024

The Bank of England's Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 20 March 2024, the MPC voted by a majority of 8–1 to maintain Bank Rate at 5.25%. One member preferred to reduce Bank Rate by 0.25 percentage points, to 5%.

Since the MPC's previous meeting, market-implied paths for advanced economy policy rates have shifted up. In the United States and the euro area, inflationary pressures have continued to abate, though by slightly less than expected. Material risks remain, notably from developments in the Middle East including disruption to shipping through the Red Sea.

Having declined through the second half of last year, UK GDP and market sector output are expected to start growing again during the first half of this year. Business surveys remain consistent with an improving outlook for activity.

The fiscal measures in Spring Budget 2024 are likely to increase the level of GDP by around ¼% over coming years. As the measures will probably also boost potential supply to some extent, the implications for the output gap, and hence inflationary pressures in the economy, are likely to be smaller.

Reflecting uncertainties around the ONS's Labour Force Survey, the Committee is continuing to consider a wide range of indicators of labour market activity. The labour market has continued to loosen but remains relatively tight by historical standards. Although still elevated, nominal wage growth has moderated across a number of measures. Contacts of the Bank's Agents continue to expect some decline in pay settlements this year and to report greater difficulty in passing on cost increases to prices.

Twelve-month CPI inflation fell to 3.4% in February from 4.0% in January and December, a little below the expectation in the February Monetary Policy Report. Services consumer price inflation has declined but remains elevated, at 6.1% in February. Most indicators of short-term inflation expectations have continued to ease.

CPI inflation is projected to fall to slightly below the 2% target in 2024 Q2, marginally weaker than previously expected owing to the freeze in fuel duty announced in the Budget. In the February Report projection, CPI inflation was expected to increase slightly again in Q3 and Q4, accounted for by the direct energy price contribution to 12-month inflation. Services price inflation is expected to fall back gradually.

The MPC's remit is clear that the inflation target applies at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognises that there will be occasions when inflation will depart from the target as a result of shocks and disturbances. Monetary policy will ensure that CPI inflation returns to the 2% target sustainably in the medium term.

At this meeting, the Committee voted to maintain Bank Rate at 5.25%. Headline CPI inflation has continued to fall back relatively sharply in part owing to base effects and external effects from energy and goods prices. The restrictive stance of monetary policy is weighing on activity in the real economy, is leading to a looser labour market and is bearing down on inflationary pressures. Nonetheless, key indicators of inflation persistence remain elevated.

Monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term in line with the MPC's remit. The Committee has judged since last autumn that monetary policy needs to be restrictive for an extended period of time until the risk of inflation becoming embedded above the 2% target dissipates.

The MPC remains prepared to adjust monetary policy as warranted by economic data to return inflation to the 2% target sustainably. It will therefore continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. On that basis, the Committee will keep under review for how long Bank Rate should be maintained at its current level.

Minutes of the Monetary Policy Committee meeting ending on 20 March 2024

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices.

The international economy

2: UK-weighted global GDP was estimated to have grown by 0.4% in 2023 Q4, in line with the projection in the February Monetary Policy Report. The divergence in growth among advanced economies had continued, with the United States again growing faster than had been expected.

3: Euro-area GDP had been flat in 2023 Q4, in line with the February Report projection. Near-term indicators such as PMIs and industrial production had continued to stabilise, but the recovery was somewhat weaker than had been expected. By contrast, US GDP had grown by 0.8% in the fourth quarter, higher than had been anticipated in the February Report. US growth was expected to slow in 2024 Q1, following a weakening in real private consumption and retail sales growth since the start of the year.

4: In China, GDP had grown by 1.0% in 2023 Q4. Going forward, growth was expected to remain at around that rate and, in early March, the government had set an annual growth target of around 5%. Other emerging market economies had seen mixed GDP growth outturns in the fourth quarter, with India growing particularly strongly. Near-term indicators suggested that some momentum was persisting into 2024.

5: Despite the conflict in the Middle East and continuing disruption to shipping through the Red Sea, there had been limited news in energy prices since the MPC's February meeting. The Brent spot oil price had increased by around 5% to $87 per barrel as OPEC and other aligned oil producers were expected to extend production cuts. European wholesale natural gas spot and near-term futures prices had been broadly flat since the Committee's February meeting, as temperatures had remained mild and storage levels high.

6: Labour markets in advanced economies had continued to loosen but had remained tight overall. The job vacancies rate in particular had continued to decline across countries. The US unemployment rate had increased to 3.9% in February, while non-farm payrolls had grown by 275,000 in the same month. The unemployment rate in the euro area had edged down to 6.4% in January. Wage growth in the euro area and the United States had fallen in 2023 Q4 but data on the outcome of current wage negotiations in the euro area were not yet available. The gap in wage growth between the United Kingdom on the one hand, and the euro area and the United States on the other, had continued to narrow as UK wage growth had declined more quickly recently than wage growth in the other two economies. However, annual pay growth had remained higher in the United Kingdom.

7: Headline and core consumer price inflation had continued to trend down in the euro area and the United States since the start of this year. However, February inflation rates in both regions had been slightly higher than expected by market participants, accounted for by news in core inflation. In the euro area, headline HICP inflation had been 2.6% in February, and core inflation 3.1%. In the United States, headline CPI inflation had been 3.2%, and core inflation 3.8%. Services price inflation had remained elevated in both economies.

8: The Committee discussed some factors that might influence the global long-term real equilibrium interest rate. Factors that had previously been operating, such as demographics, were likely to continue to bear down on the long-term real rate. Increased investment into climate transition technologies or artificial intelligence, driven for example by expectations of higher productivity growth, might be raising the long-term real equilibrium interest rate. Sustained increases in fiscal spending could also have an impact. The Committee would continue to discuss these factors.

Monetary and financial conditions

9: Since the Committee's previous meeting, the market-implied paths for policy rates across major advanced economies had shifted up. Corporate bond spreads had, however, narrowed and equity prices had risen, leaving mixed signals on the direction of the overall change in financial conditions.

10: Following significant falls in market expectations of policy rates in December and January, recent stronger than expected economic data, particularly non-farm payrolls and inflation releases in the United States, had pushed out slightly the expected timing of future reductions in policy rates across major advanced economies. Despite the rise in short-term interest rates, risky asset prices had increased. Market intelligence suggested that the narrowing in corporate credit spreads and rising equity prices had reflected growing confidence that global growth, credit conditions and corporate earnings would improve going forward.

11: In line with market expectations, the Bank of Japan had raised its policy rate to positive territory and had also ended its policy of yield curve control.

12: In the United Kingdom, all respondents to the Bank's latest Market Participants Survey (MaPS) had expected Bank Rate to be left unchanged at this MPC meeting. They had also all continued to expect the next move in Bank Rate to be downward. The median respondent in the latest MaPS had expected a cumulative 75 basis points reduction in Bank Rate this year, starting in August. This was broadly in line with current market pricing but down from 100 basis points in the February MaPS. The median respondent had reported that they perceived the neutral interest rate to be at 3.25%, similar to recent surveys.

13: The Committee discussed the increasing convergence and correlated movements in recent months between market expectations for the UK and US policy rate paths. Market intelligence indicated that, despite differences in recent and projected supply and demand growth, this recent convergence could be attributed to factors such as the similarities in current policy rates and the two economies being in broadly similar stages of the disinflationary process.

14: While quoted mortgage rates had increased somewhat since the Committee's previous meeting, largely reflecting pass-through of increases in risk-free reference rates, they had remained substantially below the levels reached last summer. The availability of secured lending to households had improved slightly in the latest Credit Conditions Survey, and the number of owner-occupied mortgage products advertised was now back at levels recorded before the start of the interest rate tightening cycle. Quoted interest rates on unsecured consumer credit and bank lending to businesses had remained close to their recent peaks.

15: The annual growth rate of aggregate sterling broad money had decreased from -0.3% in December to -1.6% in January, driven by volatility in the holdings of the non-intermediate other financial corporations sector, but had remained slightly above the previous six-month average of -1.8%. Within that, annual growth in household deposits had, however, continued to rise.

Demand and output

16: UK real GDP had fallen by 0.3% in 2023 Q4, weaker than had been expected in the February Monetary Policy Report. This had followed a 0.1% decline in Q3. A Bank staff estimate of market sector output, which was less subject to swings in measured non-market output in health and education, had declined by 0.4% in Q4, after a similar-sized fall in Q3. Within the expenditure components of GDP, domestic household consumption and housing investment had fallen by 0.4% and 1.9% respectively in Q4. Business investment was estimated to have risen by 1.5%.

17: Monthly GDP had risen by 0.2% in January, to its highest level since September 2023. Strength in monthly growth had been concentrated in the construction and government services sectors. Private services output had risen slightly.

18: GDP and market sector output growth were both expected to pick up and be positive over the first half of the year. The flash S&P Global/CIPS UK composite output PMI had been little changed in March at slightly below its long-run historical average, while the future output PMI had eased back slightly from its two-year high in February. There was a similarly positive signal from most other business surveys of current and future market sector activity. Intelligence from the Bank's Agents had also become slightly more optimistic about the outlook. Bank staff continued to expect GDP growth of 0.1% in 2024 Q1 and early indications suggested a small further rise in output growth in Q2.

19: Although consumption had been weaker than expected over 2023, there had been some early signs of a gradual recovery. Retail sales volumes had been volatile but had risen by 3.4% in January following a 3.3% decline in December. Intelligence from the Agents suggested that consumption growth was likely to remain weak in 2024 Q1 but to improve thereafter. GfK consumer confidence had been broadly stable over recent months, with the future personal financial situation sub-balance remaining only slightly below its long-run average. The number of mortgage approvals for house purchases had risen in January to its highest level since October 2022. The UK House Price Index had been broadly flat over recent months, but other timelier indicators of house prices had tended to rise slightly.

20: The Spring Budget 2024 had taken place on 6 March, accompanied by an Economic and fiscal outlook from the Office for Budget Responsibility. The Government had announced a package of fiscal measures, including a further 2p cut in the main rate of employee and self-employed national insurance contributions from April 2024. Bank staff had provisionally estimated that these new measures would increase the level of GDP by around ¼% over coming years. As the measures would probably also boost potential supply to some extent, the implications for the Committee's output gap projection, and hence inflationary pressures in the economy, were likely to be smaller. A full assessment of this news would be conducted as part of the May Report forecast round.

Supply, costs and prices

21: Reflecting uncertainties around the ONS's Labour Force Survey (LFS), the Committee was continuing to consider a wide range of indicators of labour market activity. These collectively pointed to the labour market remaining relatively tight in absolute terms, though continuing to loosen.

22: The ONS had released updated LFS estimates in February but had advised caution in interpreting the results owing to low sample sizes. These estimates also did not reflect the most recent migration and population data. The LFS unemployment rate was estimated to have fallen over the past six months, to 3.9% in the three months to January. Other indicators, such as the claimant count and Agents' intelligence on recruitment difficulties, pointed to a flat or slightly rising profile of unemployment. The vacancies-to-unemployment ratio had remained slightly above its 2019 Q4 levels.

23: The collective steer from a range of measures pointed to modestly positive quarterly employment growth, in line with the February Monetary Policy Report projections. The Committee noted that employment growth had been relatively resilient in an environment of subdued activity, suggesting that companies were potentially retaining their existing employees to meet future increases in demand. This was also consistent with Agents' intelligence. The Committee would monitor whether or not this retention would restrain any tightening in the labour market as GDP growth picked up.

24: Against the backdrop of easing labour market tightness and receding inflation expectations, most indicators of pay growth had declined, although they had remained elevated. Annual private sector regular Average Weekly Earnings (AWE) growth had been 6.1% in the three months to January, 1.1 percentage points lower than in the three months to October and broadly in line with the February Report projection. AWE had moved increasingly into line with other measures such as median private sector pay growth derived from HMRC payrolls data.

25: The Committee discussed the degree of persistence in wage growth. Some shorter-term measures of wage growth had eased, such as an underlying measure based on a range of pay indicators which had been running at a three-month on three-month annualised pace of around 5%, and suggested a moderation in inflationary persistence. On the other hand, adjusting AWE data on a CPI-weighted basis indicated that pay growth could be moderating at a slower pace than the headline data were suggesting. Some forward-looking indicators also pointed to slower moderation. Expectations for future wage growth from the Decision Maker Panel (DMP) Survey had remained flat at 5.2%. The latest intelligence on average pay settlements collected by the Agents had remained close to the levels observed in the Agents' annual survey presented in the February Report. Agents' contacts had generally expected lower pass-through of higher labour costs to prices compared to 2023, however.

26: Twelve-month CPI inflation had fallen to 3.4% in February from 4.0% in January and December, a little below the expectation in the February Report. The latest CPI release had triggered the exchange of open letters between the Governor and the Chancellor of the Exchequer that was being published alongside these minutes. The decline in CPI inflation over recent months could largely be attributed to falls in food and core goods price inflation, as external cost pressures had continued to abate. Services price inflation had declined but remained elevated.

27: Energy prices had continued to drag on annual CPI inflation. Despite the 5% rise in the Ofgem price cap in January, energy was expected to continue to contribute negatively to CPI inflation over the next six months owing to the upcoming reduction in the price cap from April. The freeze in fuel duty announced in the Budget would provide a further marginal drag compared to the February Report projections.

28: Core goods price inflation had fallen to 1.9% in February, slightly lower than expected in the February Report, as cost pressures from previous shocks and global goods price inflation had continued to dissipate. Food and non-alcoholic beverages inflation had also fallen, to 5.0% in February from 6.9% in January. The level of producer input and output prices for both core goods and food had receded significantly from their previous peaks over the past year and had then flattened, while Agents' contacts similarly anticipated falling or flat input costs.

29: Services price inflation had remained higher than CPI inflation, at 6.1% in February, a decrease of 0.4 percentage points from January and in line with February Report expectations. Higher-frequency services price measures that excluded components that were not typically reliable indicators of trends in inflation persistence, such as non-private rents, accommodation and airfares, had risen by around 4½% on a three-month on three-month annualised basis. The moderation of services price inflation in recent months appeared to have been accounted for largely by weakness in non-labour rather than labour costs.

30: Households' median short-term inflation expectations had continued to ease in the February Bank of England Inflation Attitudes Survey, while longer-term expectations had remained steady and close to historical averages. Inflation expectations in the Citi/YouGov survey of households had remained somewhat higher than the Bank measures. The one-year ahead measure had been in decline, though had remained above historical averages, while the longer-term measure had been steadier. Business expectations looking one and three years ahead in the February DMP Survey had eased marginally compared to January but had remained above 2%. In the latest MaPS, median CPI expectations of market participants at the one-year point had fallen a little, while median expectations at the three and five-year horizons had remained unchanged at 2%.

The immediate policy decision

31: The MPC sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

32: In the MPC's February Monetary Policy Report projections, GDP growth had been expected to pick up gradually during the forecast period. CPI inflation had been expected to fall temporarily to the 2% target in 2024 Q2 before increasing again in Q3 and Q4, to around 2¾%. Conditioned on the market-implied path for Bank Rate at the time of the February Report, inflation had then been projected to remain above the 2% target over nearly all of the remainder of the forecast period, owing to persistence in domestic inflationary pressures. The Committee had judged that the risks around the modal inflation projection were skewed to the upside over the first half of the forecast period, stemming from geopolitical factors. Risks from domestic price and wage pressures had been judged to be evenly balanced.

33: Since the MPC's previous meeting, market-implied paths for advanced economy policy rates had shifted up, including in the United Kingdom.

34: Having declined through the second half of last year, UK GDP and market sector output were expected to start growing again during the first half of this year. Business surveys remained consistent with an improving outlook for activity. Reflecting uncertainties around the ONS's Labour Force Survey, the Committee was continuing to consider a wide range of indicators of labour market activity. The labour market had continued to loosen but remained relatively tight by historical standards. To the extent that companies had been retaining their existing employees to meet future increases in demand, employment growth was likely to be weaker relative to output growth in the near term, consistent with a further easing in labour market tightness. Should labour demand prove stronger, there could be less of an easing.

35: Twelve-month CPI inflation had fallen to 3.4% in February from 4.0% in January and December, a little below the expectation in the February Report. Services consumer price inflation had declined but remained elevated, at 6.1% in February. Higher-frequency measures of core services inflation, such as the three-month on three-month annualised rate, had been around 4½%. Most indicators of short-term inflation expectations had continued to ease. Although still elevated, nominal wage growth had moderated across a number of measures. An underlying measure based on a range of pay indicators had been running at a three-month on three-month annualised pace of around 5%. Contacts of the Bank's Agents continued to expect some decline in pay settlements this year and to report greater difficulty in passing on cost increases to prices. CPI inflation was projected to fall to slightly below the 2% target in 2024 Q2, marginally weaker than had previously been expected owing to the freeze in fuel duty announced in the Budget.

36: The MPC's remit was clear that the inflation target applied at all times, reflecting the primacy of price stability in the UK monetary policy framework. The framework recognised that there would be occasions when inflation would depart from the target as a result of shocks and disturbances. Monetary policy would ensure that CPI inflation returned to the 2% target sustainably in the medium term.

37: Monetary policy would need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term in line with the MPC's remit. The Committee had judged since last autumn that monetary policy needed to be restrictive for an extended period of time until the risk of inflation becoming embedded above the 2% target dissipated. The Committee recognised that the stance of monetary policy could remain restrictive even if Bank Rate were to be reduced, given that it was starting from an already restrictive level.

38: Eight members judged that maintaining Bank Rate at 5.25% was warranted at this meeting. Headline CPI inflation had continued to fall back relatively sharply in part owing to base effects and external effects from energy and goods prices. The restrictive stance of monetary policy was weighing on activity in the real economy, was leading to a looser labour market and was bearing down on inflationary pressures. Nonetheless, key indicators of inflation persistence remained elevated.

39: There was a range of views among these members on the extent to which the risks from persistent inflationary pressures had receded. At one end of this range, developments in nominal indicators, including at higher frequencies, suggested that the restrictive stance of policy and the unwinding of second-round effects associated with declining short-term inflation expectations were having a material impact in reducing the more persistent and slower-moving components of inflation. At the other end of this range, wage growth remained too high and was expected to moderate only slowly, as reflected in the Agents' latest intelligence. There were limited signs so far that services price inflation would return to a target-consistent pace sufficiently rapidly, with evidence of diminishing second-round effects still tentative. Some upside risks remained around both the wage and CPI inflation projections.

40: For all of these members, a further accumulation of evidence on inflation persistence would be required to warrant a shift in the monetary policy stance, with members differing on the extent of evidence that was likely to be needed. They would continue to consider the degree of restrictiveness of policy at each meeting.

41: One member preferred a 0.25 percentage point reduction in Bank Rate at this meeting. For this member, waiting for more reassurance before reducing Bank Rate would weigh further on living standards and supply capacity. Bank Rate needed to become less restrictive now to enable a smooth transition in the policy stance and to account for lags in transmission. While this did not preclude the possibility of maintaining Bank Rate if upside risks were to materialise, consumer price inflation was already, and had been for some time, on a firm downward trajectory. Consumption had not recovered to pre-pandemic levels, in sharp contrast to some other advanced economies where it was driving economic growth. The outlook for demand remained weak, with vacancies falling sharply and forward-looking indicators of nominal pay growth easing.

42: The MPC remained prepared to adjust monetary policy as warranted by economic data to return inflation to the 2% target sustainably. It would therefore continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. On that basis, the Committee would keep under review for how long Bank Rate should be maintained at its current level.

43: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 5.25%.

44: Eight members (Andrew Bailey, Sarah Breeden, Ben Broadbent, Megan Greene, Jonathan Haskel, Catherine L Mann, Huw Pill, Dave Ramsden) voted in favour of the proposition. Swati Dhingra voted against the proposition, preferring to reduce Bank Rate by 0.25 percentage points, to 5%.

Operational considerations

45: On 20 March, the total stock of assets held for monetary policy purposes was £729.9 billion, comprising £729.8 billion of UK government bond purchases and £0.1 billion of sterling non‐financial investment‐grade corporate bond purchases.

46: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Ben Broadbent

- Swati Dhingra

- Megan Greene

- Jonathan Haskel

- Catherine L Mann

- Huw Pill

- Dave Ramsden

Sam Beckett was present as the Treasury representative.