Sample Category Title

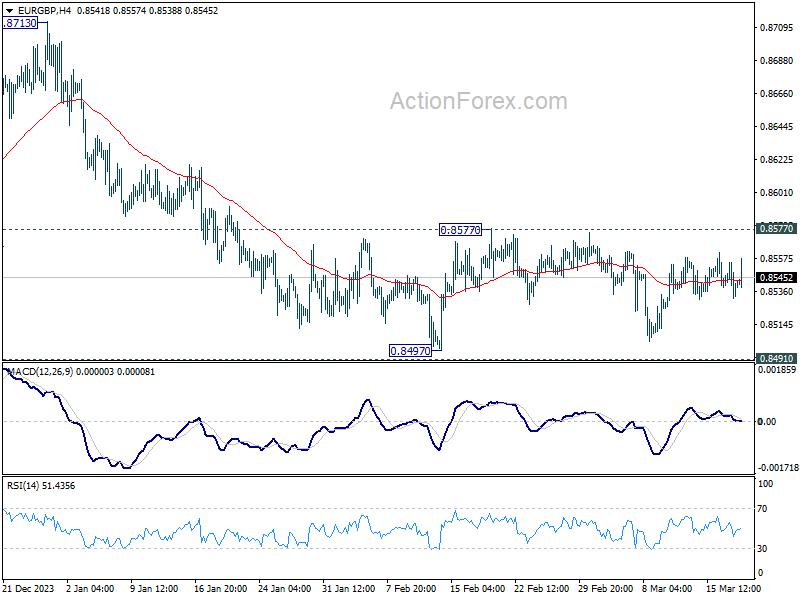

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8531; (P) 0.8543; (R1) 0.8554; More...

EUR/GBP is still bounded in range trading and intraday bias stays neutral. On the downside, decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. However, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

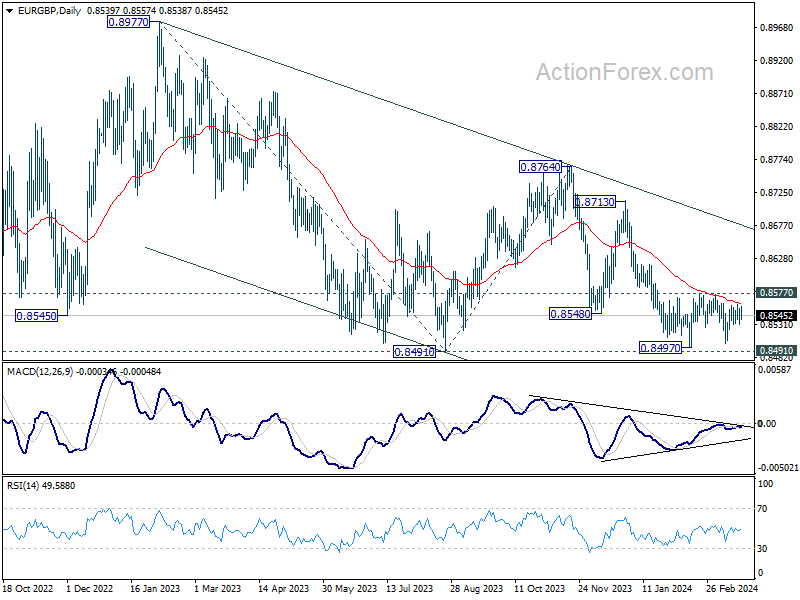

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

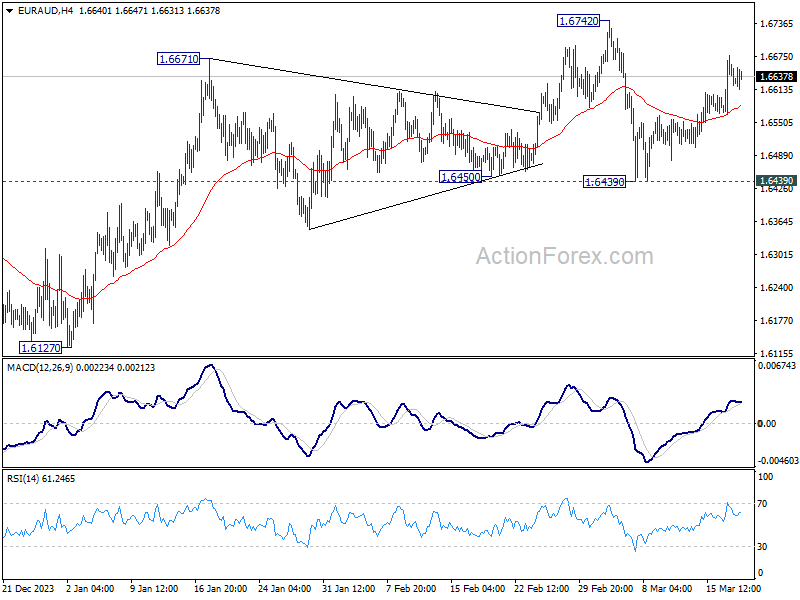

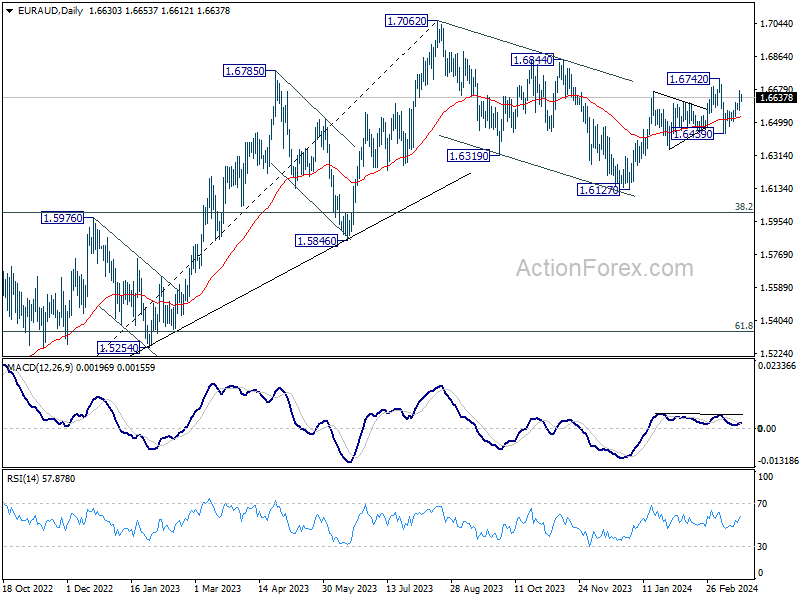

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6572; (P) 1.6626; (R1) 1.6692; More...

Intraday bias in EUR/AUD remains on the upside for retesting 1.6742 resistance first. Decisive break there will resume whole rise from 1.6127 and target 1.6844 resistance next. For now, near term outlook will remain cautiously bullish as long as 1.6439 support holds, in case of retreat.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

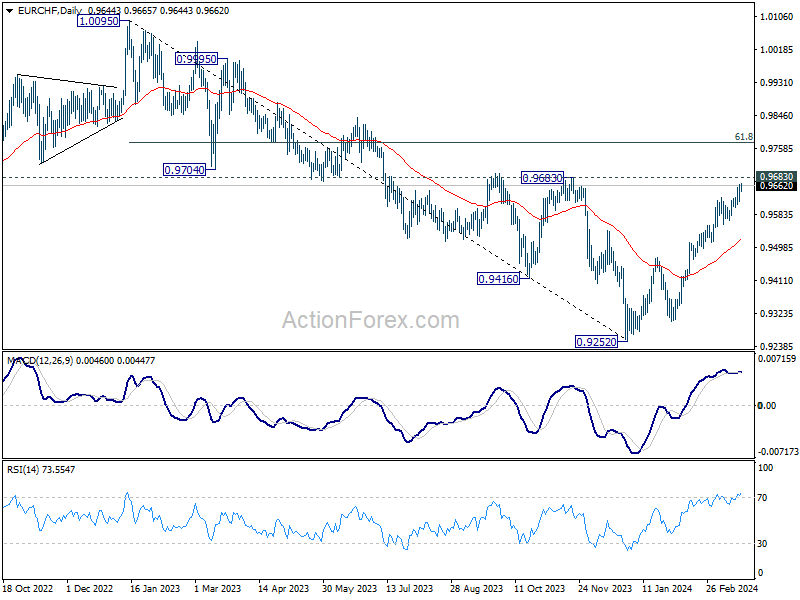

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9626; (P) 0.9645; (R1) 0.9670; More..,

Intraday bias in EUR/CHF stays on the upside for the moment. Current rally from 0.9252 would target 0.9683 key resistance next. Considering bearish divergence condition in 4H MACD, break of 0.9618 support will indicate short term topping. In this case, intraday bias will be back on the downside for 55 D EMA (now at 0.9520).

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

Happy Fed Day

Yesterday’s Bank of Japan (BoJ) decision to exit the negative rates went quite smoothly for equities and bonds, relatively disquieting for the yen. The USDJPY spiked past 151.50 this morning on BoJ’s commitment to keep the policy as accommodative as possible and keep buying Japanese government bonds until it’s sure it hits the 2% target – from the downside. The EURJPY hit a fresh high despite the dovish vibes from the European Central Bank (ECB) and a hawkish move from the BoJ.

Certainly, the BoJ meeting was perhaps the biggest disappointment of the year for the yen bulls, but for the Nikkei bulls and the overseas – especially US bond markets – there is relief that the BoJ normalization will remain soft and slow. The Nikkei index threw itself back above the 40’000 mark and will likely be seeking fresh records. The end of the ETF purchases will do little as the BoJ bought only around 210bn yen worth of assets last year – that’s around $150 mio for a USDJPY rate of 140, and they bought none this year. The Japanese companies earnings are robust, they benefit from the US-China tensions, a cheap yen, ultra-lose monetary conditions and corporate governance reforms. On the other hand, the yield differential between Japan and major counterparts remains high enough to prevent the Japanese investors from bringing their money back home in a hurry. In summary, the yen should still appreciate once the BoJ reaction is over, but the selloff in Japanese bonds will likely remain limited and outlook for the Japanese stocks remains positive.

Fed day

Unlike the expectations of the beginning of the year, the Federal Reserve (Fed) will most probably keep the rates unchanged today, update its dot plot and maybe give a hint on whether they will start slowing QT. Given the recent uptick in inflation, strong economic growth, healthy jobs market and robust earnings, we could see some Fed members plot fewer rate cuts for the year and the latter could tilt the median forecast to 2 rate cuts this year from 3 plotted in December.

But because that expectation is broadly reflected in the market pricing, there is a chance that a hawkish picture from the dot plot sees limited reaction if the Fed gives any hint that it will slow its balance sheet unwinding.

The dollar index is pushing higher into the decision, the 2-year yield is down below 4.70%, the S&P500 flirts with ATH levels, as Nvidia bulls showed back in force despite a disappointing kneejerk reaction to the company’s new Blackwell chip that should improve the performance of AI computations.

FX and commodities

The EURUSD is testing the 100-DMA to the downside before the Fed decision, while Cable is preparing to return to the December-to-March down trending channel following a softer-than-expected inflation report released just this morning in the UK. Both headline and core inflation jumped less than expected on a monthly basis and fell more than expected on a yearly basis. The actual numbers are still sensibly above the Bank of England’s (BoE) 2% policy target, but the trend is encouraging and should give a further boost to the BoE doves before tomorrow’s MPC meeting. The BoE is not expected to make a change to its rate policy tomorrow yet any shift in MPC members preferences could modify the expectation for the timing of the first rate cut – which is not expected to happen before June.

In commodities, strong US dollar and rising US yields pressure gold prices to the downside, while US crude extended gains extended gains past the $83.50pb yesterday after the latest API data showed that the US oil inventories continued to drop on the week to March 15th. Trend and momentum indicators remain positive for a further push toward the $85pb mark, though the overbought conditions and any loss of appetite following the Fed decision could trigger a minor downside correction.

All Eyes on the Fed

In focus today

In the US today's main event will be the FOMC meeting. The Fed is widely expected to maintain monetary policy unchanged. Focus will be on any clues about the timing of the first rate cuts as well as the end-game for QT, which the Fed agreed to discuss in more detail at today's meeting. The Fed will also publish its updated rate and economic projections. For more details, see Fed preview, 15 March.

In the euro area focus turns to consumer confidence. Weak consumer confidence is likely the reason for the low consumer spending in the euro area, hence we follow consumer confidence closely to estimate when private consumption will improve. An uptick in private consumption is expected to be the main growth driver this year.

In the UK, we get inflation data for February at 8:00 CET. Inflation momentum has been easing broadly and we expect further downticks across headline and core inflation. Consensus expects headline to decline to 3.5% (from 4.0%) and core to 4.6% (from 5.1%). While the release is important in a broader context, we do not believe that it will change the outcome of the Bank of England meeting tomorrow in the absence of a sharp surprise in either direction.

In Sweden, Deputy Governor Aino Bunge speaks on the Riksbank's perspectives on cash. Her appearance is the last one before the monetary policy decision and publication of the Monetary Policy Report next week, 27 March. At 10:30 CET Minister of Finance Elisabeth Svantesson presents the Ministry of Finance's latest forecast on the economic situation, where no major news is expected.

Economic and market news

What happened overnight

In China, the one-year loan prime rate and the five-year loan prime rate were kept unchanged at 3.45% and 3.95%, respectively, fully in line with consensus.

What happened yesterday

In the euro area, Germany unveiled a new EUR 500 million military aid package to boost Ukraine's military. The aid package is part of an already announced EUR 8 billion support budget for 2024.

On the macro front, the German ZEW data was better than expected in March, though the economic situation remains very weak. This suggests that the German economy is likely to trail behind its European peers in 2024. GDP growth is expected to settle around -0.1% q/q in Q1 2024, but with still solid labour markets, slowly recovering real incomes and global manufacturing cycle turning higher, a steep recession will still likely be avoided. Moreover, ECB Vice President Luis de Guindos said that the ECB would be ready to discuss a rate cut in June, given that sufficient data would be available by then - though he noted that rapid wage growth and poor productivity might pose challenges to this schedule. De Guindos adds to a growing list of policymakers who have emphasized the June meeting as a potential starting point for policy easing.

In Sweden, Deputy Governor Martin Flodén stated on Tuesday that "it has become increasingly clear that inflation is falling back towards the target. Last week's inflation outcome reinforces this picture. There is still a possible risk of setbacks, but the risk of inflation becoming entrenched at high levels has diminished".

Equities: Global equities were higher yesterday, with the leading index S&P 500 locking in a new record closing high, driven by value, and notably energy stocks (oil prices up 7% in the last five sessions). Yields were lower for a change, also boosting appetite for equities. With macro data surpassing consensus expectations, we had the perfect combination for higher equities. US main indices yesterday saw Dow +0.8%, S&P 500 +0.6%, Nasdaq +0.4%, and Russell 2000 +0.5%.

FI: There was a modest decline in the 2Y and 10Y US Treasury yields yesterday ahead of the FOMC meeting today. There is no trading in Treasuries in Asia this morning as it is a market holiday in Japan.

FX: JPY was the biggest loser yesterday after the BOJ hiked for the first time in 17 years. USD/JPY rallied to around 151 - the highest level since last November. EUR/USD held steady below 1.09 as the market awaits the outcome of the FOMC meeting tonight.

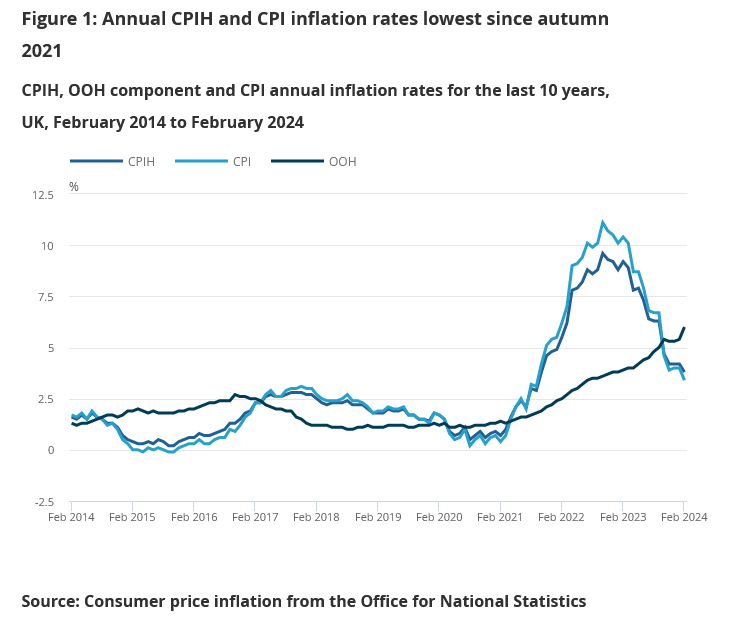

UK CPI slows to 3.4% in Feb, core down to 4.5%

UK CPI slowed from 4.0% yoy to 3.4% yoy in February, below expectation of 3.5% yoy. CPI core (excluding energy, food, alcohol and tobacco) slowed from 5.1% yoy to 4.5% yoy, below expectation of 4.6% yoy.

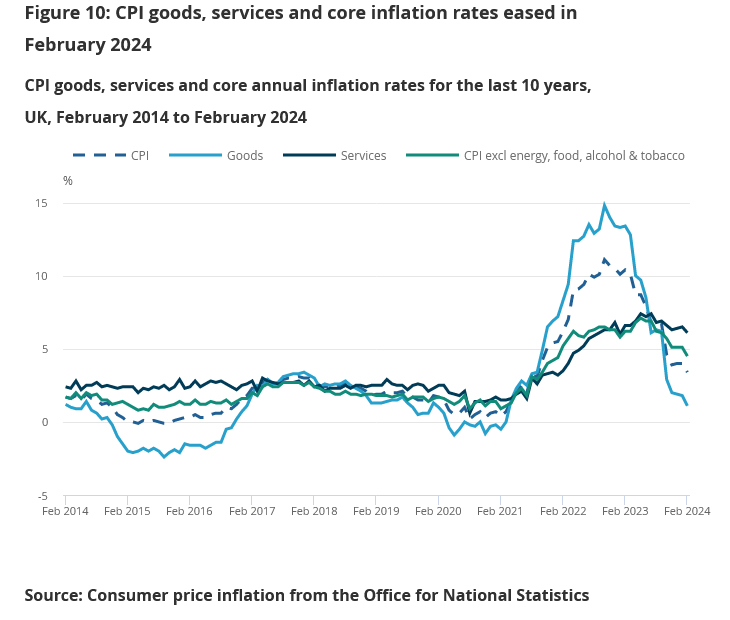

CPI goods annual rate slowed from 1.8% yoy to 1.1% yoy, while CPI services annual rate eased from 6.5% yoy to 6.1% yoy.

On a monthly basis, CPI rose 0.6% mom, below expectation of 0.7% mom.

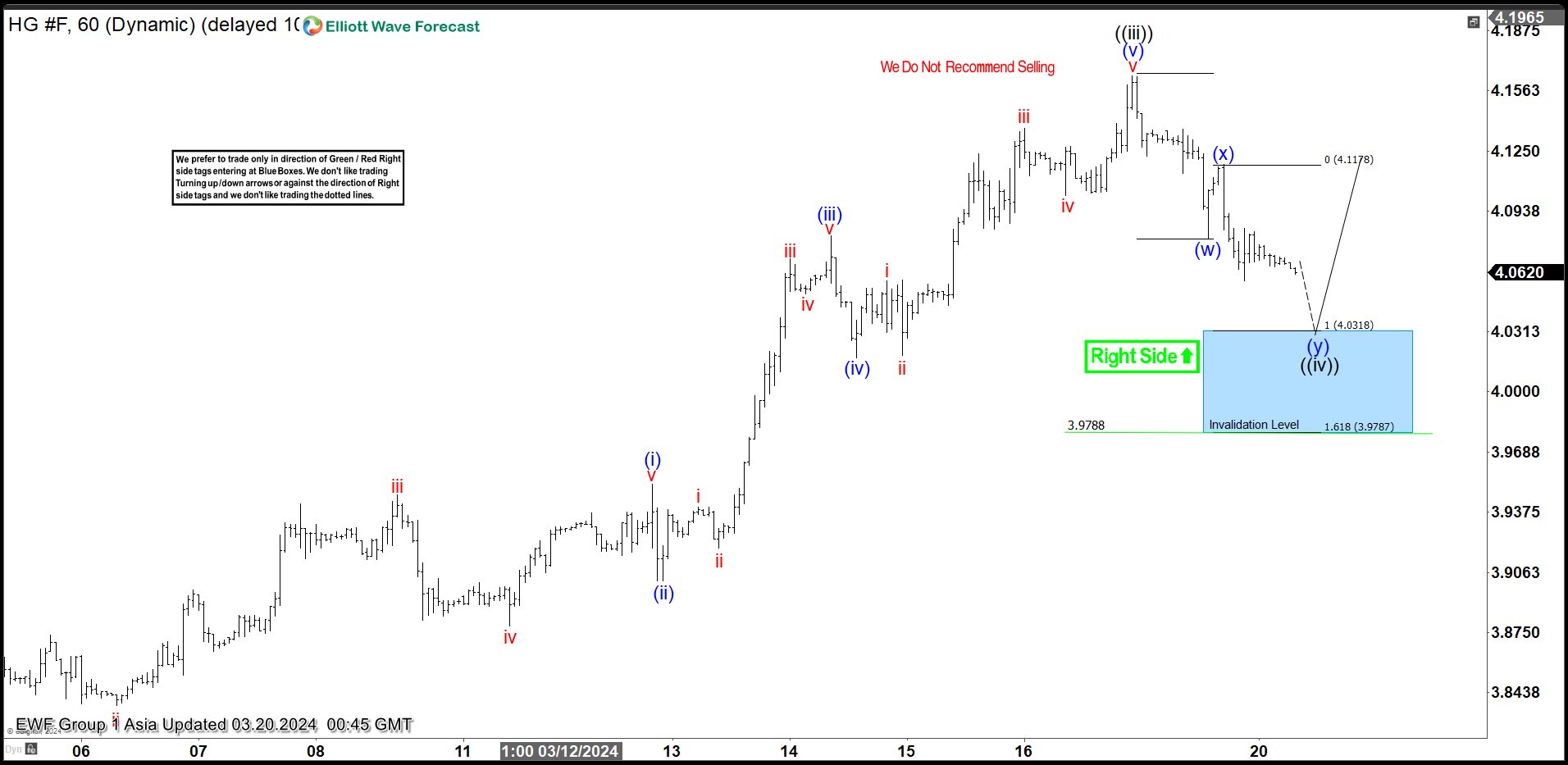

Copper (HG) Short Term Pullback Should Find Buyers

Short Term Elliott Wave view in Copper (HG) shows that the rally from 2.9.2024 low is in progress as a 5 waves impulse. Up from 2.9.2024 low, wave ((i)) ended at 3.9085 and dips in wave ((ii)) ended at 3.8015. The metal extended higher in wave ((iii)) towards 4.164. Subdivision of wave ((iii)) unfolded in another impulsive structure in lesser degree as the 1 hour chart below shows. Up from wave ((ii)), wave (i) ended at 3.952 and dips in wave (ii) ended at 3.902. The metal extended higher in wave (iii) towards 4.081 and pullback in wave (iv) ended at 4.0175. Final leg wave (v) ended at 4.164 which completed wave ((iii)).

Wave ((iv)) pullback is in progress as a double three Elliott Wave structure. Down from wave ((iii)), wave (w) ended at 4.08 and wave (x) ended at 4.118. Wave (y) lower is in progress and target lower is 100% – 161.8% Fibonacci extension of wave (w). The area comes at 3.98 – 4.03 which is shown with a blue box area. From this area, the metal should extend higher or at least bounce in 3 waves. Near term, as far as the pullback stays above 3.978 (1.618 extension), expect the metal to turn higher from the blue box area.

HG 60 Minutes Elliott Wave Chart

Copper (HG) Elliott Wave Video

https://www.youtube.com/watch?v=K1NCTdB77cA

EUR/USD Dips Again, USD/JPY Rallies Above 151

EUR/USD started another decline from the 1.0960 resistance. USD/JPY surged and broke the 151.00 resistance zone.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline below the 1.0900 support zone.

- There is a key bearish trend line forming with resistance at 1.0870 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 150.00 and 151.00 levels.

- There is a connecting bullish trend line forming with support at 150.20 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair struggled to clear the 1.0960 resistance zone. The Euro started a fresh decline and traded below the 1.0900 support zone against the US Dollar.

The pair even declined below 1.0870 and tested the 1.0835 zone. A low was formed near 1.0834 and the pair is now correcting losses. On the upside, the pair is now facing resistance near the 50% Fib retracement level of the recent decline from the 1.0906 swing high to the 1.0834 low at 1.0870.

There is also a key bearish trend line forming with resistance at 1.0870. The next key resistance is near the 76.4% Fib retracement level of the recent decline from the 1.0906 swing high to the 1.0834 low at 1.0890.

The main resistance is 1.0905. A clear move above the 1.0905 level could send the pair toward the 1.0960 resistance. An upside break above 1.0960 could set the pace for another increase. In the stated case, the pair might rise toward 1.1020.

If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.0835. The next key support is at 1.0820. If there is a downside break below 1.0820, the pair could drop toward 1.0785. The next support is near 1.0750, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a strong increase from the 147.60 zone. The US Dollar gained bullish momentum above 148.90 against the Japanese Yen.

It even cleared the 50-hour simple moving average and 150.00. The current price action above the 151.00 level is positive. A high is formed at 151.47 and the pair might continue to rise. Immediate resistance on the USD/JPY chartis near 151.50.

The first major resistance is near 152.00. If there is a close above the 152.00 level and the RSI stays moves 60, the pair could rise toward 152.80. The next major resistance is near 153.50, above which the pair could test 155.00 in the coming days.

On the downside, the first major support is near the 23.6% Fib retracement level of the upward move from the 148.91 swing low to the 151.50 high at 150.85.

The next major support is visible near a connecting bullish trend line at 150.20 or the 50% Fib retracement level of the upward move from the 148.91 swing low to the 151.50 high. If there is a close below 150.20, the pair could decline steadily.

In the stated case, the pair might drop toward the 149.50 support zone. The next stop for the bears may perhaps be near the 147.60 region.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

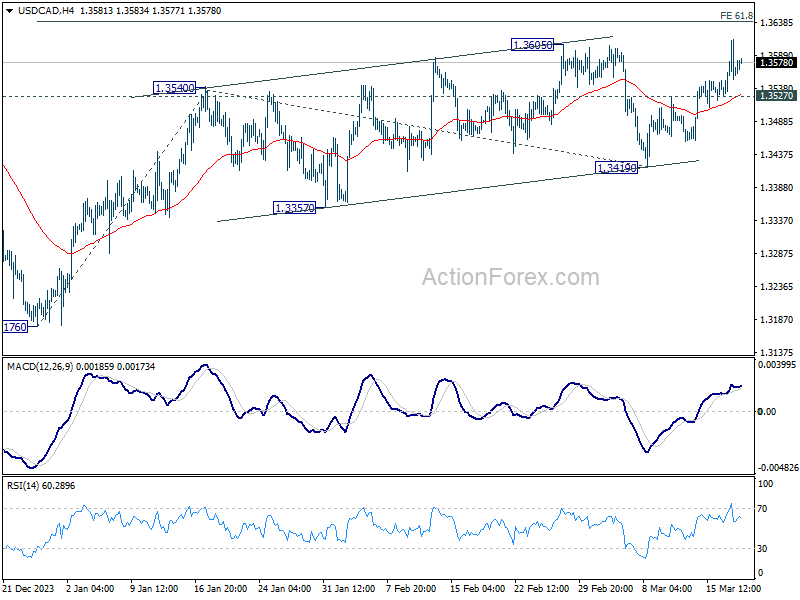

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3525; (P) 1.3570; (R1) 1.3610; More...

Intraday bias in USD/CAD remains on the upside at this point. Current rally from 1.3176 is in progress for 61.8% projection of 1.3176 to 1.3540 from 1.3419 at 1.3644 first. Decisive break there could prompt upside acceleration to 100% projection at 1.3783 next. On the downside, below 1.3527 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 1.3419 support holds.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

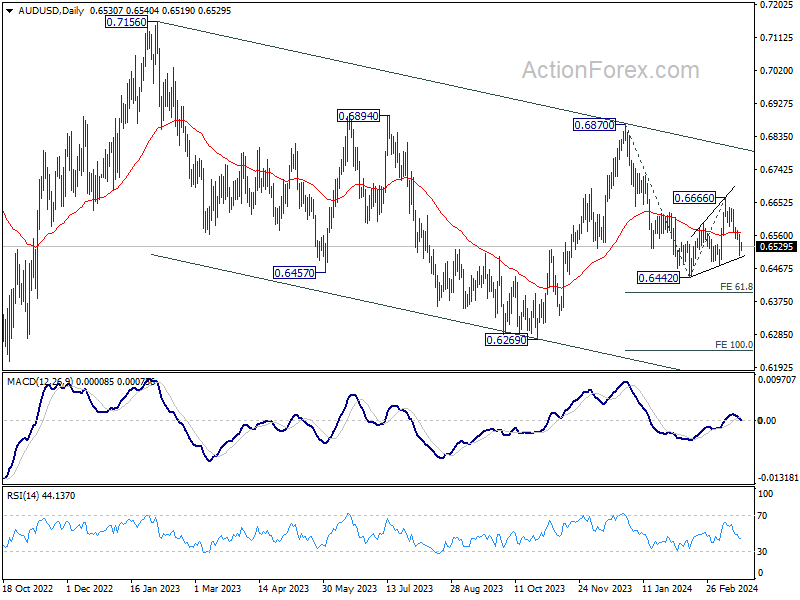

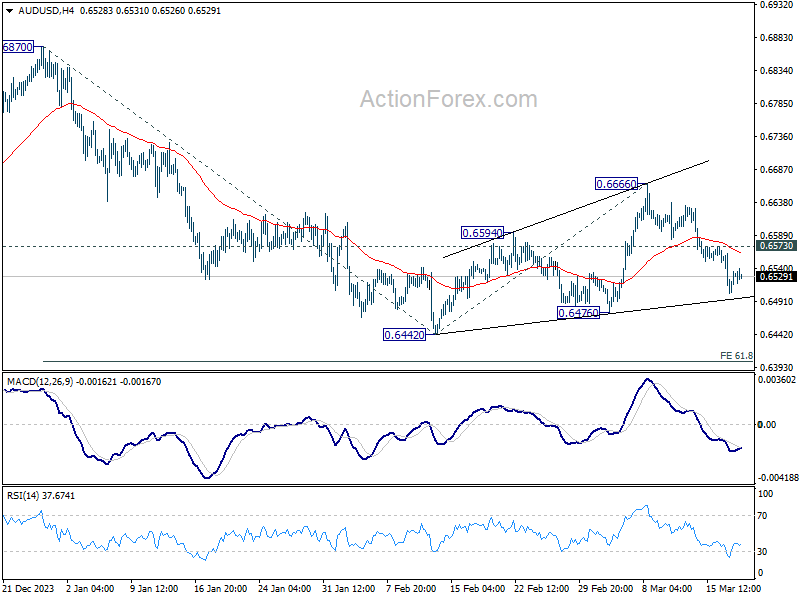

AUD/USD Daily Report

Daily Pivots: (S1) 0.6503; (P) 0.6533; (R1) 0.6563; More...

Intraday bias in AUD/USD remains on the downside for 0.6476 support. Break there will argue that decline from 0.6870 is ready to resume through 0.6442 low. On the upside, break of 0.6583 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.6666 resistance holds.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.