Sample Category Title

FOMC Remain Data Dependent, But on Track for June

The FOMC are sanguine on the growth and inflation outlook, and view the risks as coming into balance.

March’s FOMC meeting communications and forecasts were largely as expected, highlighting policymakers’ confidence in the fight against inflation and achieving a soft landing. The FOMC is on track to begin cutting in June, assuming progress continues to be made with inflation. The bigger risk is the degree of persistence in price pressures into the medium-term, and consequently the end point for this cutting cycle.

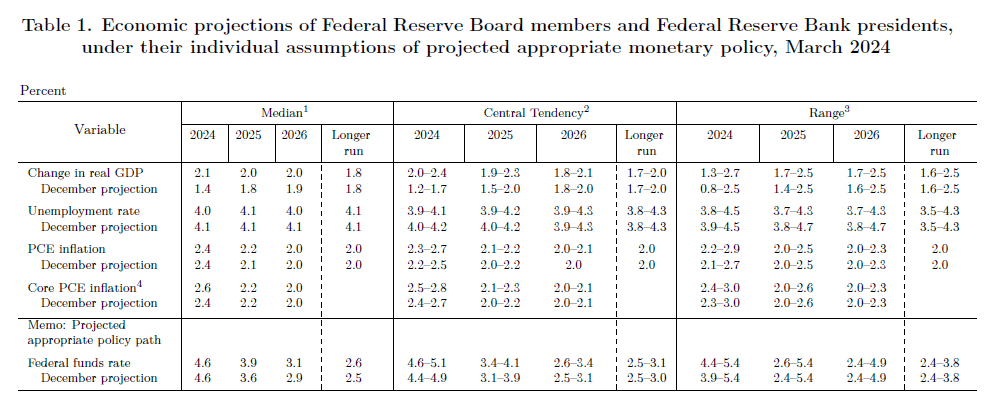

The revisions to Committee members’ forecasts were marginal in scale but of significance, signalling greater belief in the durability of activity growth and labour market strength but, at the same time, confidence in returning inflation to target. The Committee now expects growth to remain above potential (1.8%) through the entire forecast period, at 2.1% in 2024 and 2.0% in 2025 and 2026 (previously 1.4%, 1.8% and 1.9%). Little-to-no further deterioration is anticipated for the labour market, with the unemployment rate expected to plateau around 4.0% in 2024-26 from 3.9% currently.

These forecasts recognise the strength of GDP and nonfarm payrolls to end-2023, but give little weight to the downside risks recently evident in the business surveys, measures of labour utilisation (such as hours worked and the number of jobs per worker) and retail sales – spending was marginally lower over January and February combined after a strong 2023. In our view, these risks are nascent but material.

Even with their benign view on activity, the FOMC are confident inflation is on track to swiftly and sustainably return to target. Core PCE is forecast to be higher in 2024 (2.6% versus 2.4% in December) but the projections are unchanged for 2025, 2026 and the longer run – respectively 2.2%, 2.0% and 2.0% (note the longer run figure is for headline). In the press conference, Chair Powell made clear that the upward revision was a response to recent data (a higher starting point) not a change in the perceived current or future composition of inflation pressures. There was also no change regarding the risks to inflation. Housing rent was the only component discussed at length during the press conference. While slow to come through, a material deceleration in shelter is still anticipated over the year ahead. This is critical to the outlook because, in recent months, shelter has made up more than half of total inflation month-on-month.

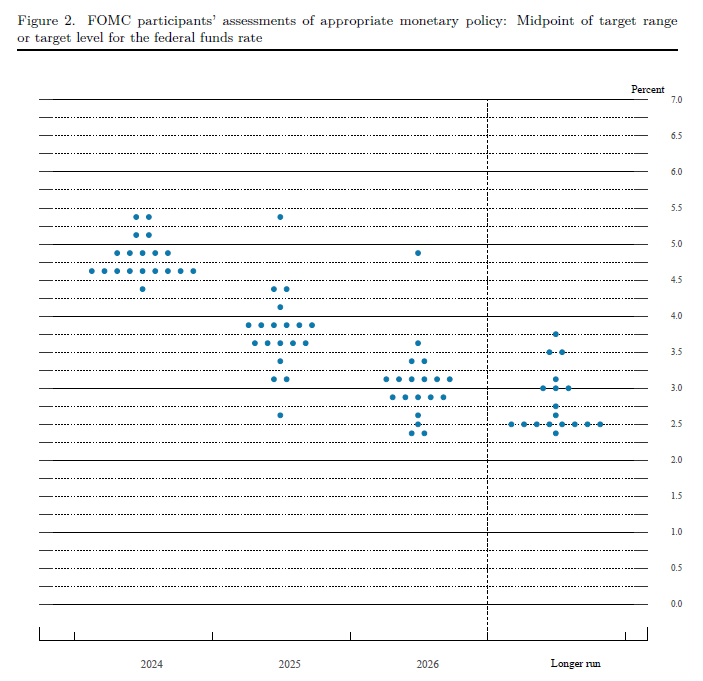

Where the Committee has grown a little more cautious is with respect to the medium-term risks for inflation. This is evident in the minor revisions to the fed funds rate projection. Three cuts are still anticipated for 2024, but the median number of cuts for 2025 is now only three (previously four). Another three cuts are projected for 2026, as was the case in December, and two more are seen into the long run to 2.6%. While only 10bps above the prior longer run rate estimate of 2.5%, this revision signals some risk of persistent or recurring inflation risks.

While we continue to anticipate an additional cut in both 2024 and 2025 compared to the FOMC’s view (a cumulative 200bps of cuts versus the FOMC’s 150bps), we believe it is more probable that the FOMC will halt the cutting cycle at 3.375% in late-2025, when our forecast horizon currently ends, than continue down to 3.1% in 2026 and 2.6% in the longer run. This is not based on a materially different view of neutral through the cycle, but rather because we anticipate recurring supply-side inflation pressures stemming from tight capacity across housing and infrastructure and due to the US’ decision to reshore production away from Asia, building in a higher cost of production for some goods. We expect US inflation to average closer to 2.5% than 2.0% in 2025, requiring a modestly contractionary stance of policy be maintained to manage both the risks and expectations.

In our view, the implications of such an outturn would be a period of below-trend GDP growth and consequently a degree of persistent slack in the labour market, the unemployment rate holding around 4.5% through at least 2025. These are not terrible outcomes by any means, but do justify a continued downtrend in the US dollar and growing uncertainty over the US fiscal position.

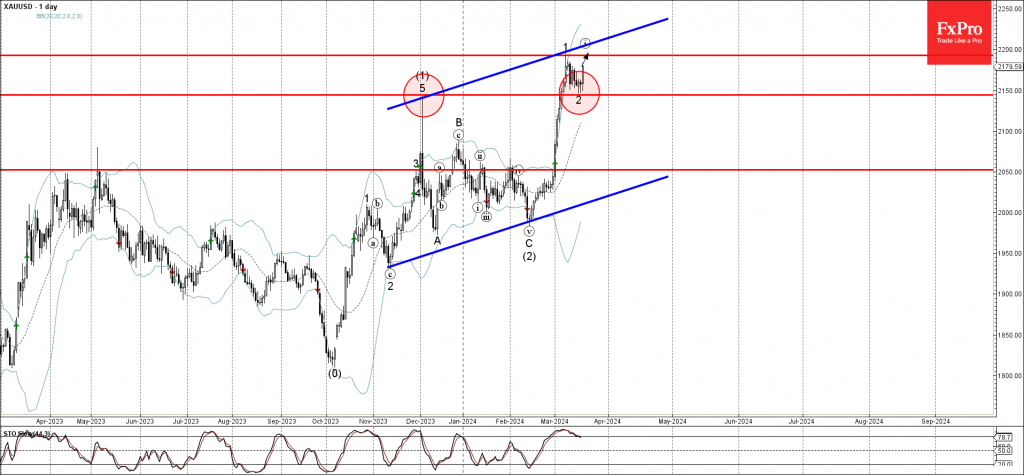

Gold Wave Analysis

- Gold reversed from key support level 2150.00

- Likely to rise to resistance level 2197.00

Gold earlier reversed up from the key support level 2150.00 (former strong resistance, which stopped the earlier upward impulse wave (1) in December).

The upward reversal from the support level 2150.00 started the active impulse wave 3, which belongs to the intermediate impulse wave (3) from February.

Given the clear daily uptrend, Gold can be expected to rise further toward the next resistance level 2197.00, top of the previous impulse wave 1.

Fed still sees three cuts this year, but slower easing thereafter

Fed left interest rate unchanged at 5.25-5.50% as widely expected. The new economic projections and dot plots are clearly more hawkish than December's. Yet, Dollar dips initially after the announcement, perhaps because they're not as hawkish as feared.

In the new median economic projections interest rate is still seen at 4.625% by the end of 2024. But federal funds are are now projection to decline slower to 3.875% by the end of 2025 (vs prior 3.625%), and then 3.125% by the end of 2026 (vs prior 2.875%). The long run federal funds rate is seen slightly higher from 2.5% to 2.6%.

Looking at the details of the dot plot for end of 2024, nine members see interest rate above 4.75%, and 10 below that level. That is one member has shifted the stance (the split was 8-11 in December). Also, only one member expects interest rate to be below 4.50%. That is, Fed isn't likely to cut more than three times this year, with higher risk of cutting less.

Other forecasts see:-

GDP growth:

- 2024 GDP growth at 2.1% (upgraded from 1.4%).

- 2025 GDP growth at 2.0% (upgraded from 1.8%).

- 2026 GDP growth at 2.0% (upgraded from 1.9%).

Headline PCE:

- 2024 PCE inflation at 2.4% (unchanged).

- 2025 PCE inflation at 2.2% (raised from 2.1%).

- 2026 PCE inflation at 2.0% (unchanged).

Core PCE:

- 2024 core PCE inflation at 2.6% (raised from 2.4).

- 2025 core PCE inflation at 2.2% (unchanged).

- 2026 core PCE inflation at 2.0% (unchanged).

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Philip N. Jefferson; Adriana D. Kugler; Loretta J. Mester; and Christopher J. Waller.

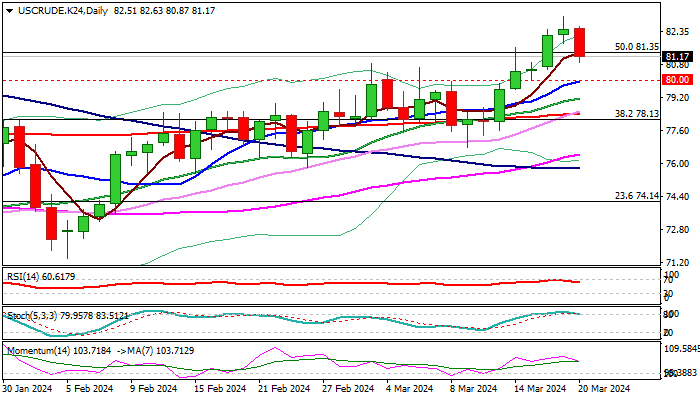

WTI Oil Price Falls on Profit Taking from New Multi-Month High

WTI oil price pulls back from new 4 ½ month high ($83.10), down 1.6% for the day so far, as traders collected profits ahead of Fed policy announcement.

The oil price accelerated higher recently on fresh concerns about oil supply, following attacks on Russian refining installations and persisting threats of stronger disruptions.

Stronger than expected drop in crude inventories (API report) and lower build in crude stocks compared to the previous week (EIA report) contributes to signals of a healthy demand, with improving economic data from the world’s largest oil importer China, adding to supportive factors.

From the technical point of view, oil price continues to move within a larger uptrend from $67.70 (Dec 2023 low), with daily studies being firmly bullish, but overbought, which sparked the latest sell-off.

Pullback is likely to be a shallow and ideally to be contained by psychological $80.00 support, reinforced by rising 10DMA, though deeper drop cannot be ruled out, with extended dips to find ground above $78.63/43 (Fibo 38.2% of $71.40/$83.10 / 200DMA respectively) to mark a healthy correction and keep larger bulls in play.

Res: 82.63; 83.10; 83.58; 84.57

Sup: 80.34; 80.00; 79.15; 78.63

Japanese Yen (USD/JPY) Hits Four-Month Low

The USD/JPY pair surged to a four-month high as investors recalibrated their expectations for the Bank of Japan's future actions. The consensus is now that the BoJ's monetary policy will remain accommodative, even with the shift away from negative interest rates.

On Tuesday, the Bank of Japan announced its first interest rate hike in 17 years, indicating its expectation to observe favorable fiscal conditions for some time. However, the yen remains under pressure due to the significant interest rate differential between Japan and the United States.

Japan's negative interest rate period extended over eight years. The recent decision marks a historic move following a prolonged phase of quantitative monetary easing.

The market generally believes that the Bank of Japan's transition to a stable monetary policy is far from complete. This perspective is supported by the BoJ's "soft" statements and the subsequent reaction of the JPY.

The yen plunged by 1% against the US dollar immediately following the BoJ's decision and continues to weaken. The upward trend in the USD/JPY pair began in early January 2024 and has remained strong.

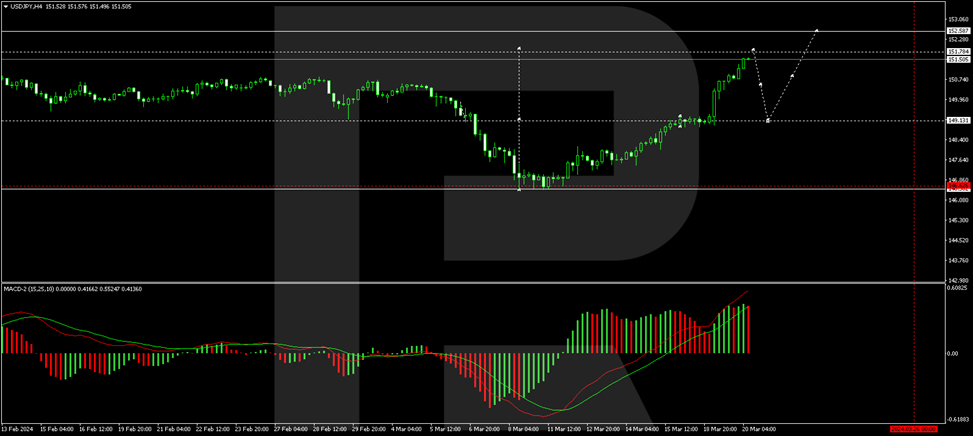

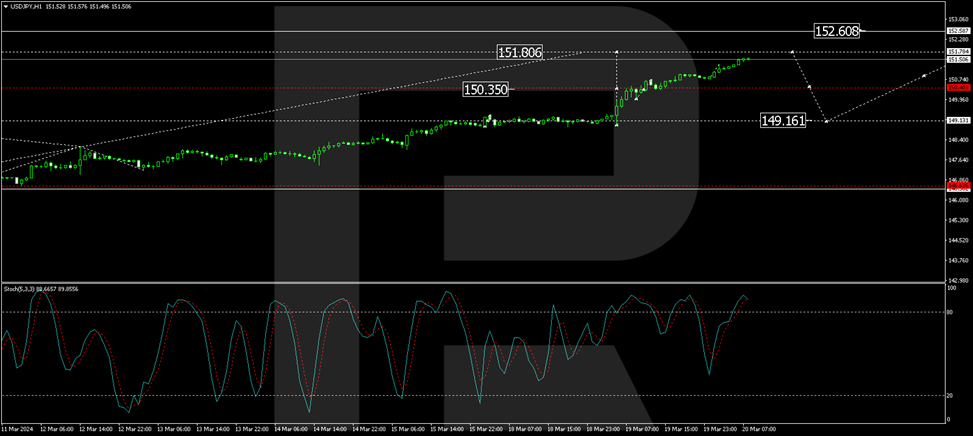

USD/JPY technical analysis

The H4 USD/JPY chart shows a consolidation range formed around the 149.13 level. With an upward breakout, the pair continues to develop a growth wave towards 151.77. A correction phase to 150.00 could follow, then a rise to 152.60. The MACD oscillator supports this scenario, with its signal line strictly pointing upwards and aiming for new highs.

On the H1 USD/JPY chart, a narrow consolidation range has developed around the 150.40 level. Exiting upwards from this range, the growth wave continues towards 151.78. After reaching this level, a potential correction back to 150.40 (testing from above) is considered, followed by a new growth structure towards 152.60. The Stochastic oscillator corroborates this scenario, with its signal line above the 80 mark and preparing to drop to 50.

Sunset Market Commentary

Markets

The ECB and its Watchers XXIV conference and UK February CPI data provided a welcome interlude counting down to tonight’s Fed decision. ECB Lagarde basically held to the recent communication line. Moving into the dial back phase requires wage growth to slow further, a continued decline in inflation towards 2% and a confirmation in new internal projections. This suggests that the June meeting is the preferred time to start the easing cycle. ”Our decisions will have to remain data dependent and meeting-by-meeting, responding to new information as it comes in”. In this framework, the ECB isn’t able to pre-commit to a particular rate path, even after the first rate cut. Executive Board member Schnabel elaborated on a potential higher neutral rate due to structural factors including the climate transition, the digital transformation and changes in the geopolitical context. The comments had no lasting impact on European interest rate markets. In German yields trade between flat (2-y) and -2.5 bps (30-y).

UK February inflation data were close to expectations. Headline inflation eased to 0.6% M/M and 3.4% Y/Y from 4% (vs 3.5% expected). Core inflation also declined slightly more than expected to 4.5% from 5.1%. However, services inflation remains stubbornly hight at 6.1%. UK gilts are marginally outperforming US Treasuries and Bunds, declining between 1.5 bps (2-y) and 3 bps (5 & 10-y). Question remains whether these data are sufficient for the BoE to become more specific in its timing of rate cuts when they announce their policy decision tomorrow. Recall the MPC was highly divided in February. 6 members voted to leave the policy rate unchanged. Two members still considered it necessary to raise the policy rate (25 bps) as inflation remains too long above the target. On the other hand, one member already vote to cut rates. Money markets still see a first BoE rate cut at the August meeting. Looking at sterling, today’s inflation data didn’t inspire markets to prepare for a dovish twist. EUR/GBP briefly ‘jumped’ to the 0.8855 area immediately after the release, but EUR/GBP currently even trades marginally lower at 0.854.

US interest rate markets are almost paralyzed in the run-up to the Fed decision, with yield changes less than one bp across the curve. The dollar succeeds some follow through gains (DXY 104.1, EUR/USD 1.085). USD/JPY (151.75) is only a whisker away from the 2023 top. Equites, both in Europe and the US are little changed. With respect to the Fed meeting, markets look out whether/to what extent stubbornly high inflation will force Powell and co to upwardly revise their inflation forecasts and whether 3 rate cuts (25 bps) this year is still the mainstream scenario. We see no reason for the Fed to inspire markets to front-run on its easing cycle. On the contrary.

News & Views

Belgian consumer confidence held steady at -5 in March after wiping out an uptick towards the end of last year over the past two months. In the National Bank of Belgium’s survey, households displayed more pessimism in March about the outlook for the labour market over the next twelve months. Fears of a rise in unemployment popped up again even if there was little change in the expectations for the general economic situation. On a personal level, while their expectations for their own future financial situation remained virtually unchanged, households have raised their savings intentions, which had dipped last month. It’s this latter component that compensated for a worsening labour market outlook, resulting in the unchanged -5 headline figure.

Leo Varadkar unexpectedly announced his resignation as both Irish Prime Minister and leader of the governing Fine Gael party. Varadkar said there was no “real reason” behind his departure but it does come after the government suffered twin defeats in Irish referenda, for which the outgoing premier took responsibility. His party is also sliding in the polls to the benefit of Sinn Fein over Ireland’s acute housing crisis and concerns over immigration. Varadkar’s resignation doesn’t necessarily trigger general elections, which are scheduled for March 2025. He asked for a new leader of the party to be chosen on April 6 with the new prime minister then to be elected after parliament’s Easter break.

Will JP 225 Index Continue Its Record Rally?

- JP 225 index flirts with all-time highs

- Short-term technical signals remain encouraging

Japan’s 225 stock index (cash) is on the rise again, aiming to revive its five-month-old positive trend above the March record high of 40,564 after finding support near the 38,310 area.

The technical signals favor the upward move in the price as the RSI is sloping northwards and is still some distance off its 70 overbought mark. The stochastic oscillator continues to trend up, and the MACD is looking to rise above its red signal line, both backing the bullish scenario too.

If the market enters uncharted territory, the bulls could temporarily stop inside the 41,400-42,000 range, which is defined by two upward trendlines. Running higher, the index could gear up to 44,211, where the 261.8% Fibonacci extension of the latest downfall is positioned.

On the downside, the 20-day simple moving average (SMA) could come first into view at 39,432 ahead of the ascending trendline at 38,884. A break below the latter could lose steam somewhere between the 23.6% Fibonacci retracement of the five-month-old upleg at 38,160 and the 50-day SMA at 37,826. If the bears win the battle there, the door could open for the 37,000 round level and the 38.2% Fibonacci of 36,674.

Summing up, the uptrend in Japan’s 225 stock index may have more legs to continue higher in the coming sessions, with the confirmation signal expected to come above 40,564.

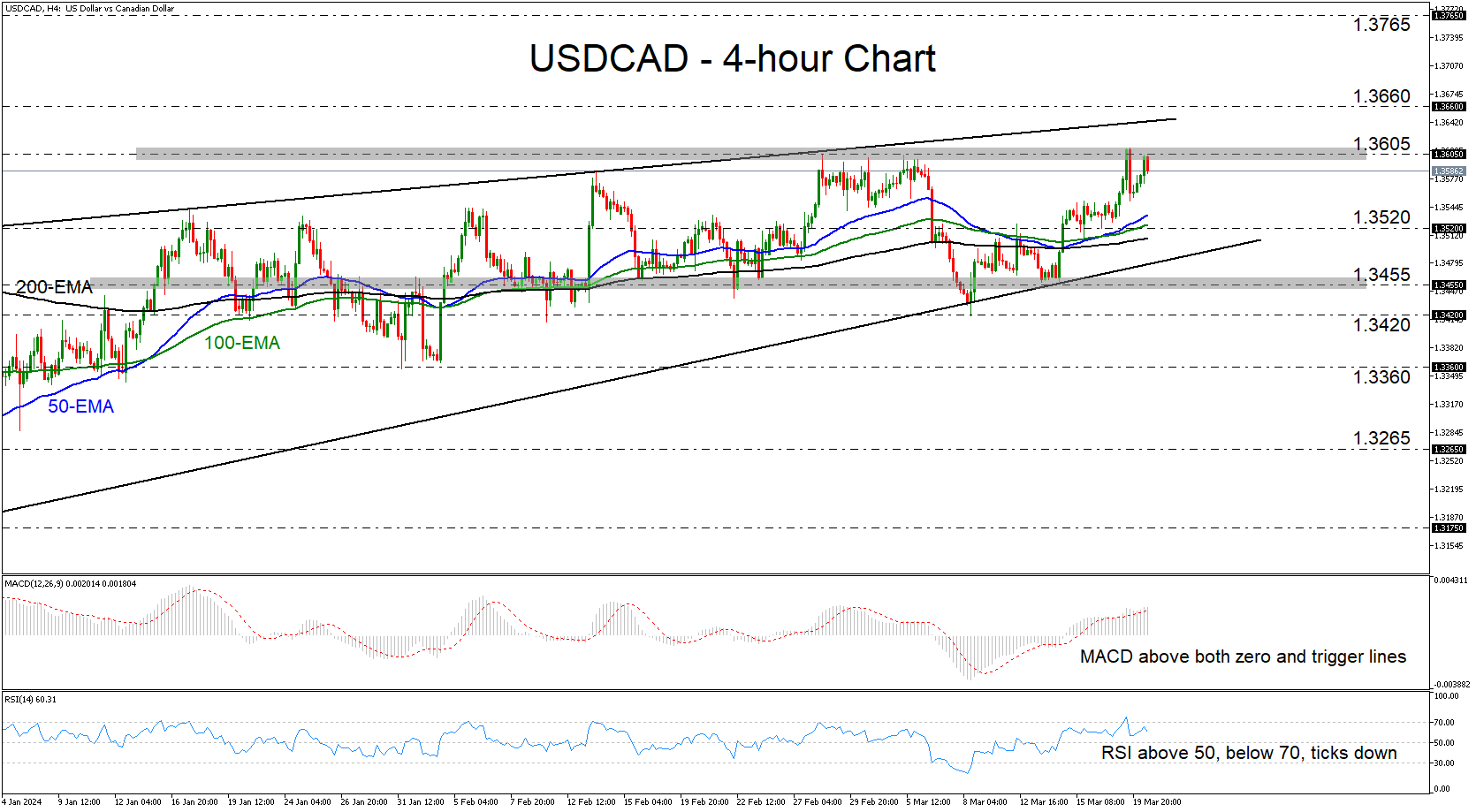

Time for USDCAD to Go for a Higher High?

- USDCAD rises after cooler than expected Canadian inflation

- A break above 1.3605 could signal uptrend continuation

- For the outlook to turn bearish, a dip below 1.3455 may be needed

USDCAD rose yesterday after the Canadian CPI numbers came in lower than expected. However, the pair found resistance near the key barrier of 1.3605 that’s been preventing the price from moving higher since February 28, and then it pulled back. Today, the bulls retook charge, but they were stopped near the 1.3605 obstacle again.

The MACD is lying above both its zero and trigger lines, detecting positive momentum, but the RSI, although above 50, ticked down from slightly below its 70 line. The RSI corroborates the notion that a break above 1.3605 may be needed for the outlook to brighten.

Such a break would confirm a higher high on all time frames and perhaps allow extensions towards the upside resistance line drawn from the high of January 17, or towards the 1.3660 barrier, which was last tested on November 27. If the bulls are not willing to stop there either, then they may climb all the way up to the 1.3765 territory marked by the high of November 22.

For the outlook to darken, the pair may need to slip all the way below the key support area of 1.3455. Such a dip would also confirm the break below the upside support line taken from the low of December 29. The bears may then aim for the 1.3420 barrier, the break of which could carry extensions towards the low of January 31 at around 1.3360.

Recapping, USDCAD moved higher after Canada’s lower than expected inflation numbers, but it is struggling to overcome the key resistance of 1.3605. Only a decisive break above that zone could be considered as a trend continuation signal.