Sample Category Title

BoJ’s Ueda assures continued accommodative monetary stance following rate hike

Addressing the parliament today, BoJ Governor Kazuo Ueda articulated the rationale behind this week's exit from the long-standing negative interest rate policy and the subsequent rate hike. This move marks a significant shift for Japan's monetary policy, which had been entrenched in a negative interest rate environment for eight years.

Ueda pointed out, "We could have waited until inflation is completely at 2% for a long period of time. But if we did so, it's unclear whether inflation would have stayed at 2%. We might have seen a sharp increase in upside price risks," highlighting the preemptive nature of the BoJ's action.

The decision was influenced by recent trends in service prices and substantial wage increases resulting from annual wage negotiations, indicating a strengthening cycle of wage growth and inflation in Japan.

Despite this historical step, Ueda underscored that Japan's inflation expectations for the medium and long term are "still in the process of accelerating towards 2%". He assured that BoJ remains committed to supporting the economy and prices "by maintaining accommodative monetary conditions for the time being".

He also hinted at future adjustments, stating, "As we exit our massive stimulus program, we will gradually shrink the size of our balance sheet and at some point reduce the size of our government bond buying."

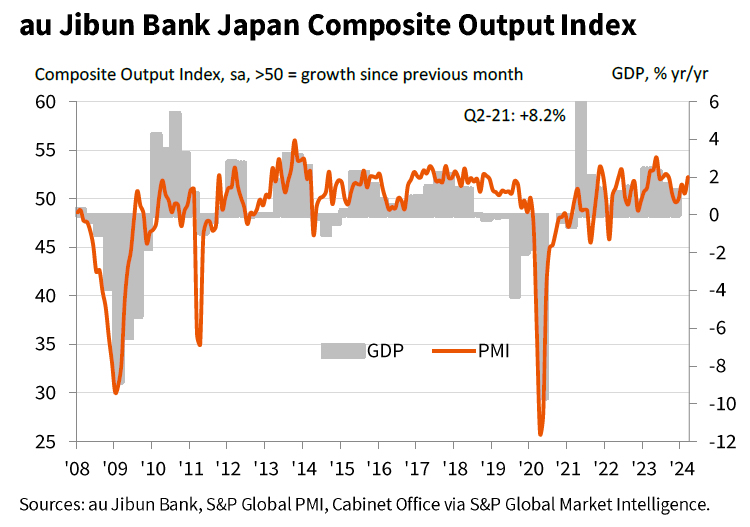

Japan’s PMI composite rises to 52.3, strengthening activity and intensifying price pressures

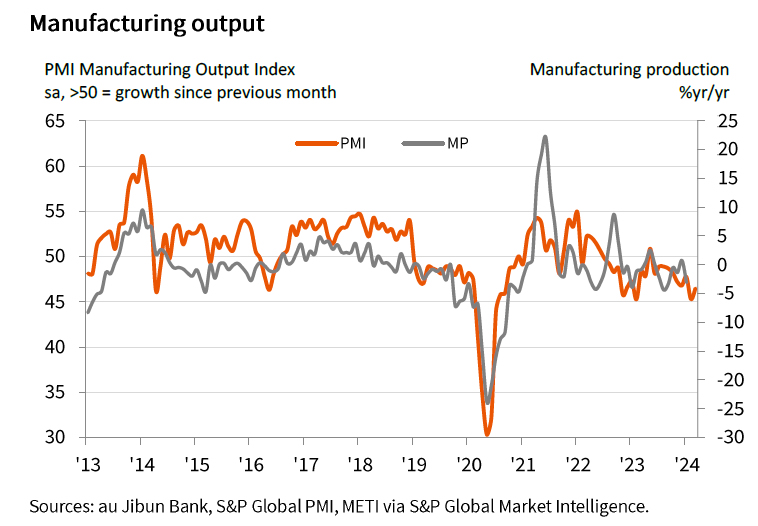

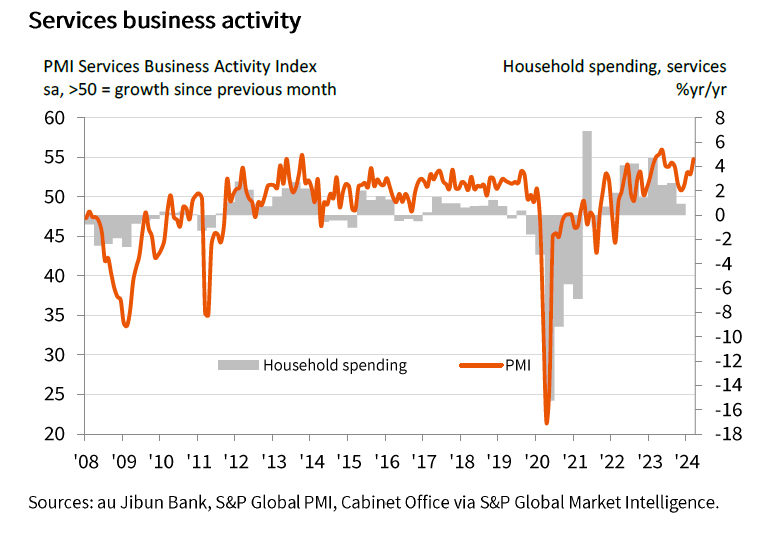

Japan's PMI Manufacturing saw a modest increase from 47.2 to 48.2 in March, while PMI Services surged to from 52.9 to 54.9, its highest level since last May. Composite PMI, which combines both sectors, also climbed from 50.6 to 52.3, reaching its peak since last August.

Usamah Bhatti, Economist at S&P Global Market Intelligence, underscored the private sector's regained momentum at the end of Q1. The expansion was predominantly driven by service providers, while manufacturers experienced a continued, though less severe, contraction.

Alongside this economic revival, Japan is facing a "renewed intensification of price pressures," with the rate of input price inflation hitting a five-month high. This uptick was particularly pronounced among service providers, although manufacturers also reported "stubbornly high input prices". Many firms opted to pass these increased costs onto customers, leading to the highest output charge inflation since last August.

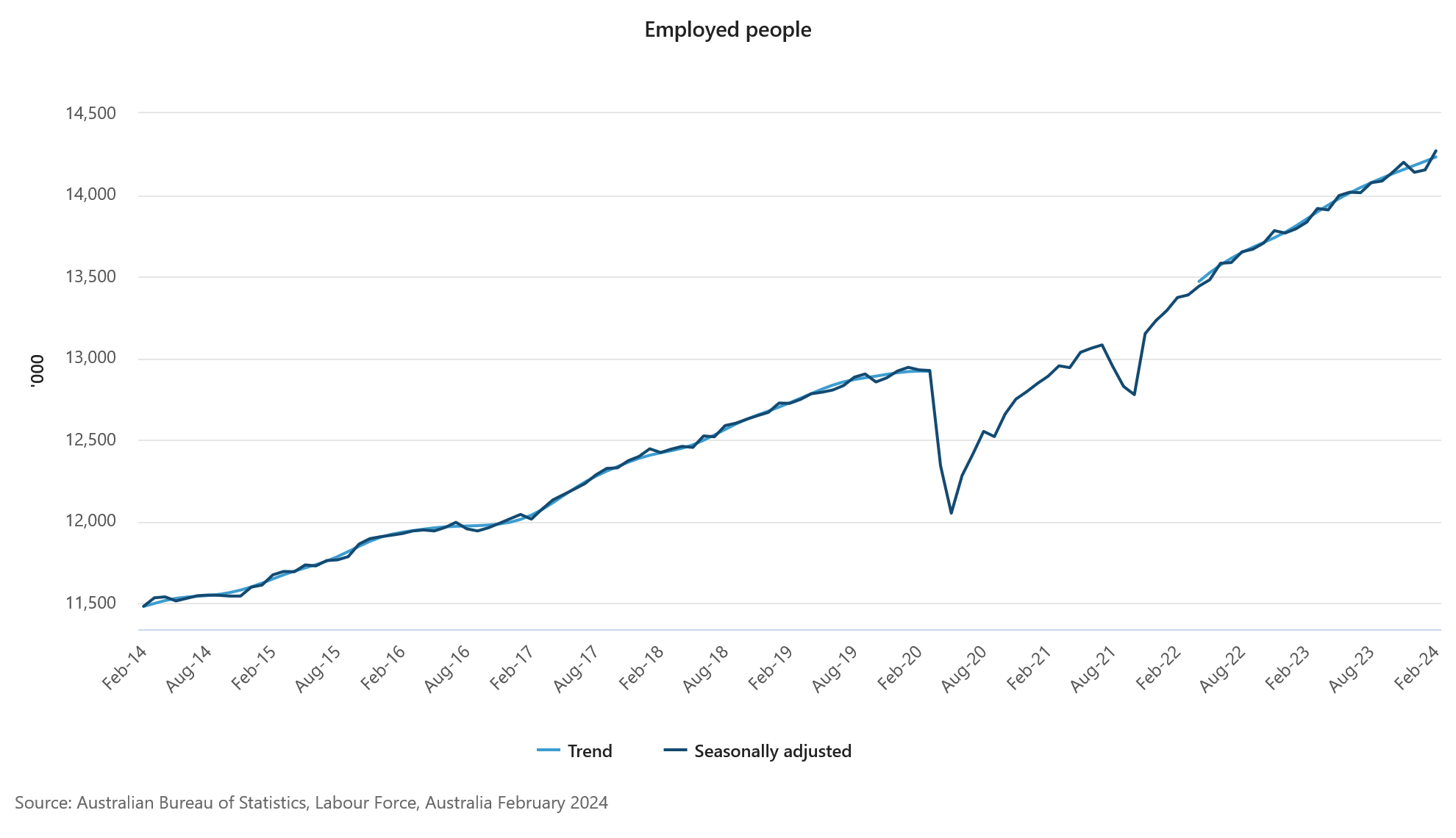

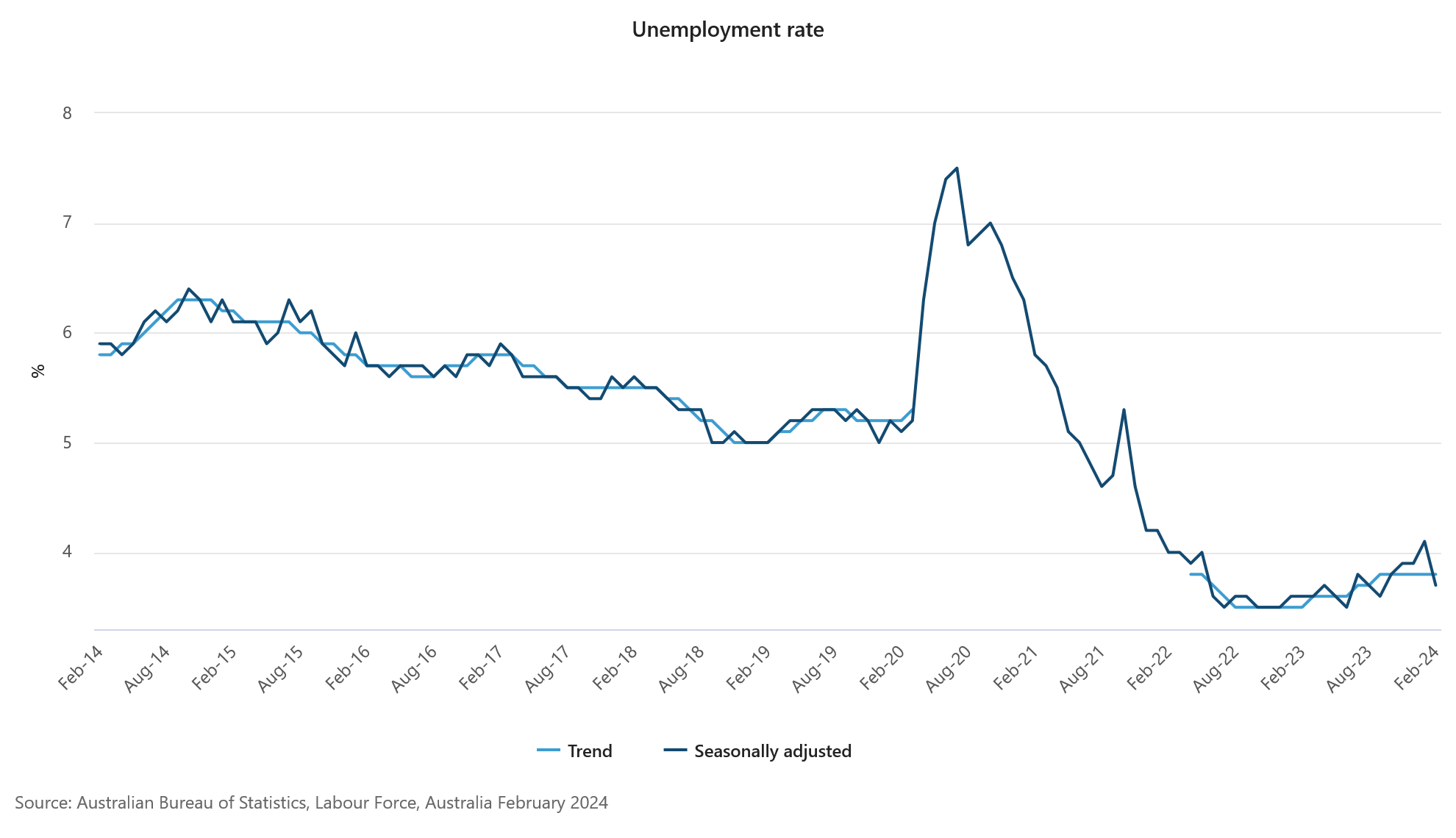

Australia employment surges 116.5k, unemployment rate dives to 3.7%

Australia employment grew strongly by 116.5k in February, well above expectation of 40.2k. Full-time jobs rose 78.2k while part-time jobs rose 38.3k.

Unemployment rate fell sharply from 4.1% to 3.7%, below expectation of 4.0%. Participation rate rose 0.1% to 66.7%. Monthly hours worked also rose 2.8% mom.

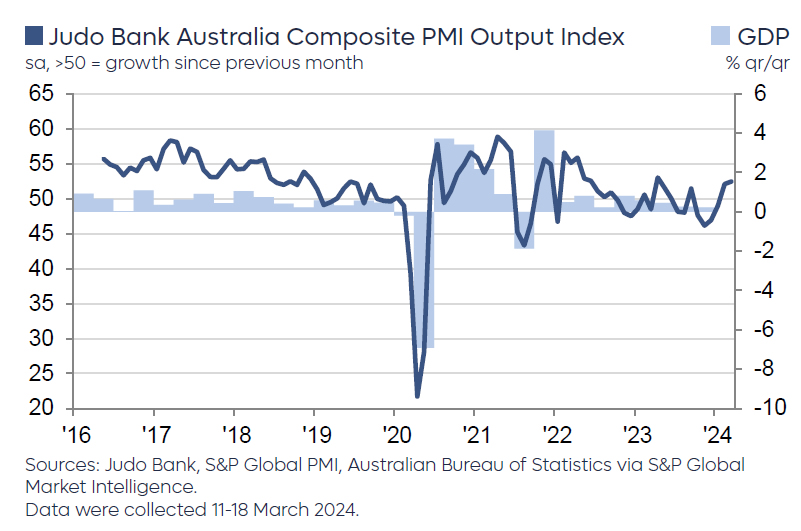

Australia PMI composite rises to 11-month, another blow to RBA rate cut expectations

Australia PMI Manufacturing PMI dropped to a 46-month low of 46.8. Conversely, PMI Services climbed to an 11-month peak of 53.5, with the Composite PMI also reaching an 11-month high at 52.4.

Warren Hogan, Chief Economic Advisor at Judo Bank, highlighted that Composite Output Index's increase for the fourth consecutive month signifies the economy's rebound from the cyclical slowdown experienced in 2023. Meanwhile However, inflation remains a concern, with service sector readings indicating persistently high producer and consumer prices.

Hogan noted that the results are "another blow to rate-cut expectations" for RBA. The rebound in economic activity, coupled with inflation exceeding targets, not only diminishes the likelihood of rate reductions, but also raises the possibility of further monetary tightening in 2024. This aligns with recent warnings from RBA.

New Zealand in technical recession as Q4 GDP contracts -0.1% qoq

New Zealand's economy has officially entered technical recession, with GDP contracting by -0.1% qoq in Q4, below expectation of 0.0% qoq. This decline follows -0.3% contraction in Q4, marking two consecutive quarters of negative growth.

GDP per capita declined decline of -0.7% qoq, while real gross national disposable income saw a -1.4% qoq drop.

The contraction was not uniformly felt across all sectors. Of the sixteen industries analyzed, eight experienced growth, notably the rental, hiring, and real estate services sector, alongside public administration, safety, and defense.

DOW hits new record as Fed holds course on three cuts, despite hawkish undertones

US stocks surged sharply higher overnight, with DOW and S&P 500 closing at new record highs. Market participants expressed relief and optimism as Fed's maintained forecast of three rate cuts for the year. Fed Chair Jerome Powell's remarks during the press conference further buoyed investor sentiment, emphasizing that the recent inflation data "haven't really changed the overall story". He affirmed that inflation is "moving down gradually", albeit via a "somewhat bumpy road."

Despite positive reactions from the stock markets, it's crucial to acknowledge that Fed's has shifted to a slightly more hawkish tone, in particular compared to December meeting. The updated dot plot revealed a narrower margin, with nine out of nineteen members now anticipating just two rate cuts for the year. Moreover, future easing path is envisioned to be more gradual than previously projected. Interest rate is expected to settle at 3.75-4.00% by the end of 2025—a slight increase from December's forecast of 3.50-3.75%. For the end of 2026, the projection was raised to 3.00-3.25%, up from the previous 2.75-3.00%.

Technically, DOW's up trend is now extending to 40k psychological level, and then 138.2% projection of 28660.94 to 34712.28 from 32327.20 at 40690.15. Outlook will stay bullish as long as 38483.25 support holds, in case of pullback.

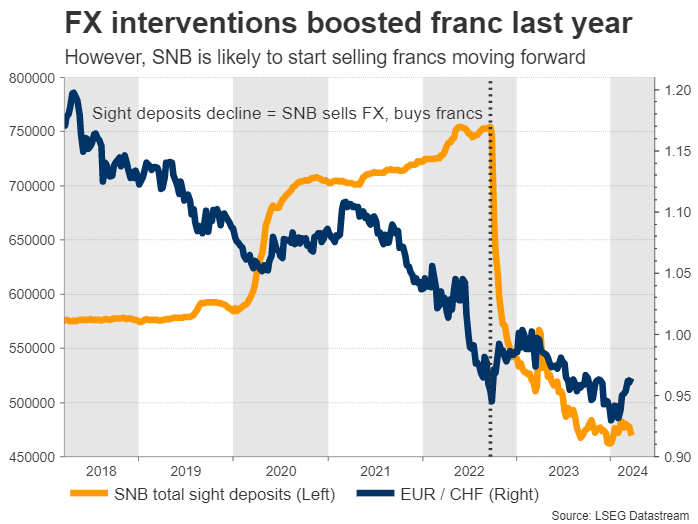

Is Swiss National Bank About to Slash Rates?

- SNB will announce its rate decision on Thursday at 08:30 GMT

- Inflation has cooled, so market is pricing 35% chance of rate cut

- For the Swiss franc, the outlook has started to turn negative

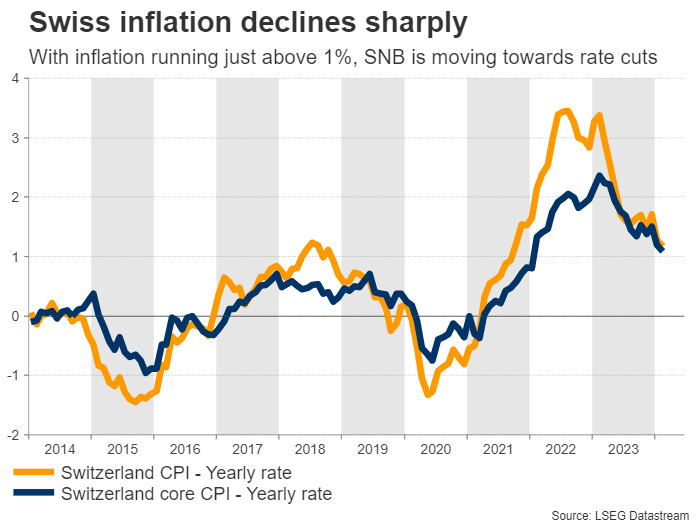

Inflation cools down

The Swiss economy is losing momentum. Economic growth slowed sharply last year, clocking in at just 0.6% in annual terms during the fourth quarter, as domestic consumption moderated while weaker growth trends in the Eurozone and China dampened exports.

Reflecting this slowdown, inflation has declined dramatically, falling to 1.2% in February. Core inflation was even lower at just 1.1% and the government expects even more softness ahead as it recently revised down its inflation forecasts for this year.

In other words, the war against inflation is over. Instead, the new threat on the radar might be a recession if growth remains so fragile. This suggests lower interest rates are coming.

SNB to set the stage for rate cuts

With growth nearly stagnant and inflation running well below its target, the Swiss National Bank certainly has the conditions necessary to begin cutting interest rates. Markets assign a 35% probability that this could happen as early as this week.

More importantly, a rate cut is fully priced in for the June meeting, so investors are saying it is only a matter of time until the SNB takes action to support the economy.

It's a close call, but admittedly, the argument for waiting until June seems stronger. Although the economy has lost steam, it has not fallen off a cliff either, and historically speaking the SNB usually prefers to wait until larger central banks like the ECB make their own moves first.

Hence, this might be the meeting where the SNB simply opens the door for a summer rate cut. Looking at the dollar/franc chart, the levels that could come into play on this decision are 0.8950 on the upside and 0.8870 on the downside.

Franc outlook is increasingly grim

Either way, the outlook for the Swiss franc has started to shift to negative. While the franc was the best-performing currency of 2023, the landscape has changed drastically this year, with several of the factors that bolstered the franc going into reverse.

Chief among those is the SNB's strategy on FX interventions. Last year, the SNB was consistently buying francs on the open market, to help the currency appreciate and dampen imported inflation in the process. But with inflation cooling off, there's no incentive to do that anymore.

Incoming data confirms the SNB has stopped buying the franc, and with inflation running so low, it could shift back to selling francs soon in an attempt to boost imported inflation.

With the central bank also moving towards rate cuts, there isn't much that can help revive the franc, which has already fallen more than 5% against the US dollar this year.

The franc's best chance at a comeback would be an episode of panic in global markets that fuels demand for safe haven assets. Even in this case though, it's doubtful whether any boost would last long in an environment where FX interventions are working against the currency.

First Impressions: NZ GDP, December quarter 2023

GDP contracted by 0.1% in the December quarter, slightly softer than Westpac and RBNZ estimates.

Key results

- Quarterly change: -0.1% (last: -0.3%, Westpac f/c: 0.0%, market f/c: 0.1%, RBNZ 0.0%)

- Annual change: -0.3% (Last -0.6%, Westpac f/c 0.0%, RBNZ 0.0%)

- Annual average change: +0.6% (Last: +1.3%)

The New Zealand economy was broadly flat over the December quarter. The production measure of GDP fell by 0.1%, slightly weaker than the zero growth that we and the Reserve Bank were expecting. Both the expenditure and income measures (the latter being a new addition to today’s release) were flat in inflation-adjusted terms.

Along with some modest revisions to growth in previous quarters – mostly due to recalculating the seasonal factors – output has shrunk by 0.3% over the last year. Again, this was softer than the flat outturn that we and the Reserve Bank had forecast.

The mix of activity was similar to what we expected. Goods-based sectors are tending to do it tougher, with declines in retail, wholesaling, manufacturing and residential construction. This was partly offset by gains in the services sectors, though even here the growth was patchy. Finance, rental services and professional services saw solid gains, but transport and arts and recreational services were down as the recovery in international tourism faltered over the quarter. The biggest lift was in public administration (up 2.8%), though it’s likely that at least some of this related to the October election.

In the context of the very strong population growth that New Zealand is currently seeing, a flat outturn for GDP is quite a soft result. Output was down 0.7% in per capita terms for the December quarter, and has fallen by 3.1% compared to a year ago. That’s a sharp decline compared to history – something that would normally be associated with recession – but in this case it highlights the degree to which the economy had become overheated in the first place.

On balance, today’s report suggests slightly less need to keep monetary policy tight for an extended period. That said, the scale of the surprise for the RBNZ is less than we saw in the September 2023 release, which the RBNZ has tended to downplay. There is also a lot of water still to go under the bridge before the May Monetary Policy Statement, including the next QSBO business survey (early April), the March quarter CPI (mid-April) and the March quarter labour market surveys (early May). There’s also the crucial first Budget for the new coalition Government – while that will be unveiled after the MPS, the RBNZ will no doubt be briefed on the key details.

March FOMC Meeting: Still Building Confidence

Summary

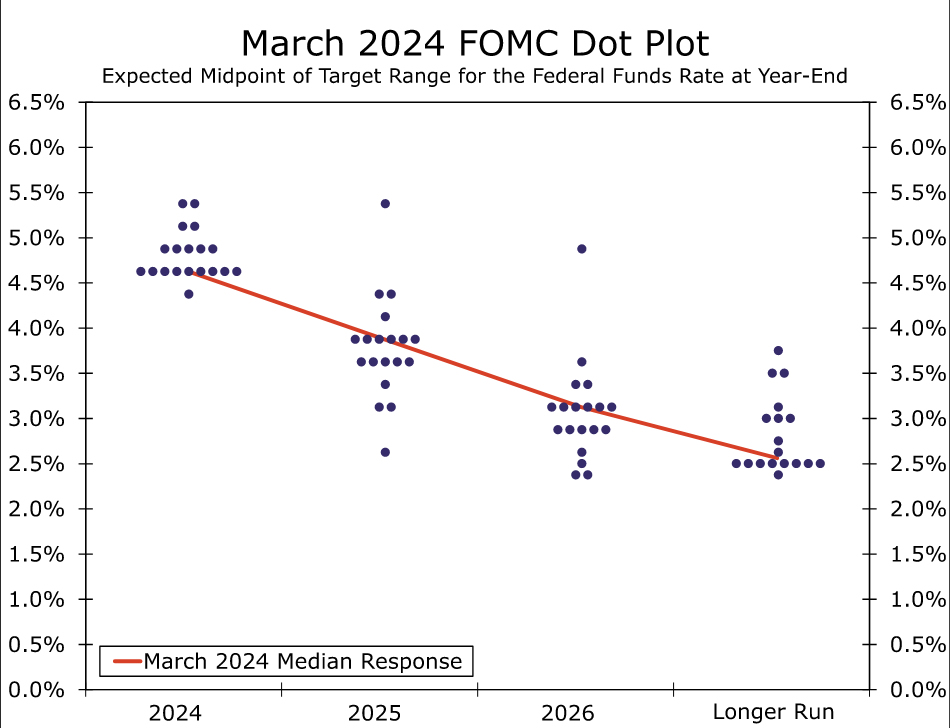

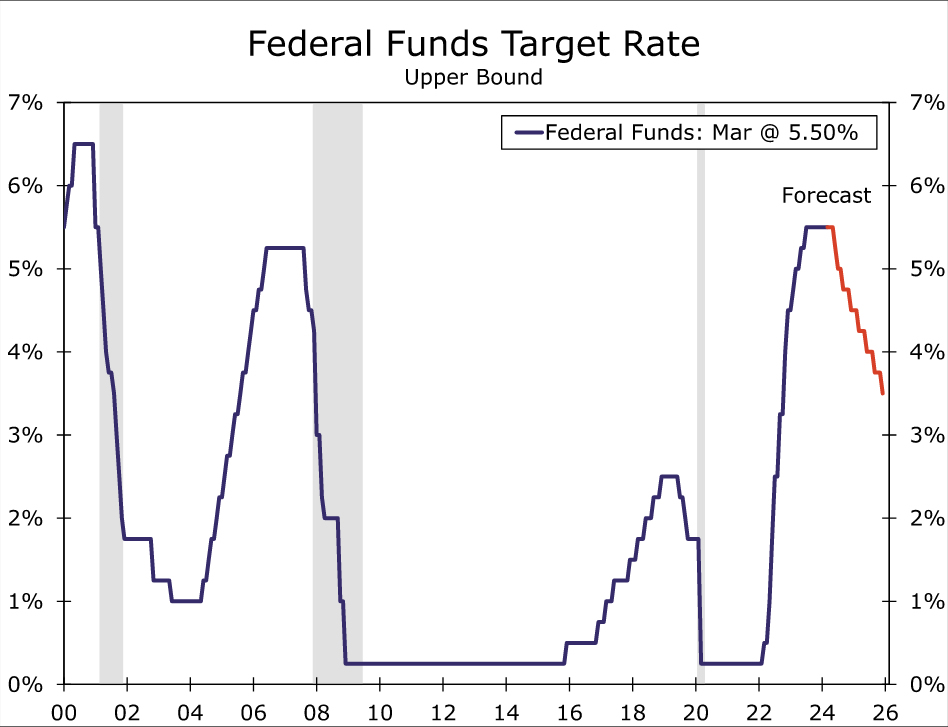

- As was widely expected, the FOMC left the fed funds target range unchanged at 5.25-5.50% at the conclusion of its March meeting.

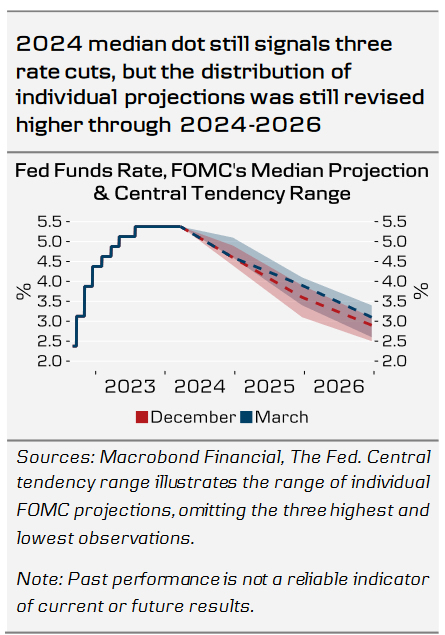

- The Summary of Economic Projections showed that the vast majority of the Committee continues to believe some easing of policy will be appropriate this year. The median projection for the federal funds rate at year-end was unchanged from December's projection at 4.625%. However, the distribution of expectations shifted higher for 2024 and the median dot for 2025 and 2026 moved up 25 bps, implying an incrementally more hawkish outlook.

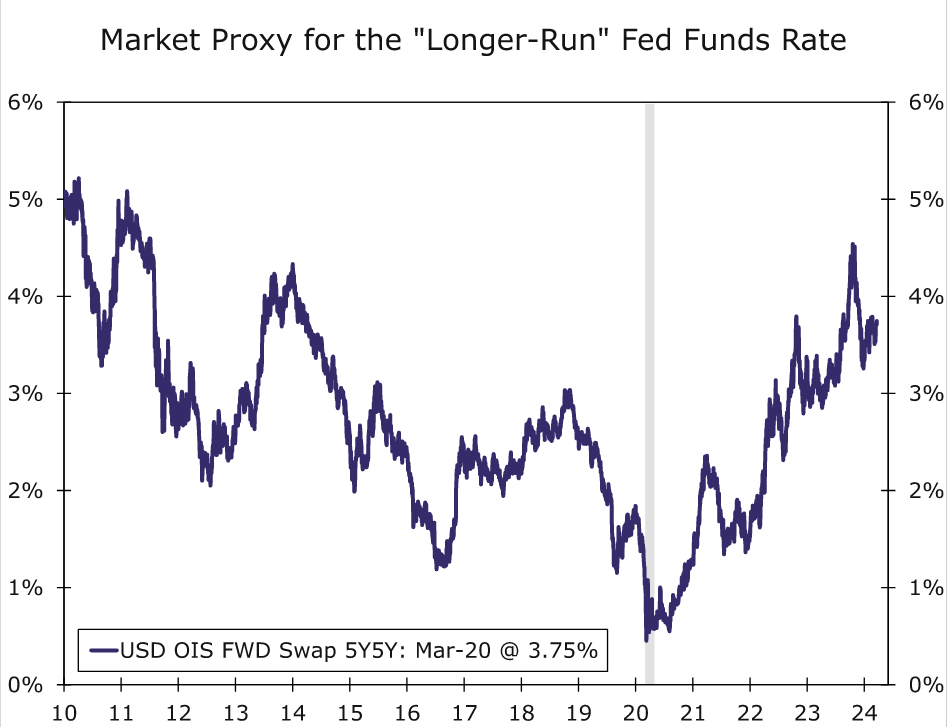

- Notably, the median "longer-run" dot also moved higher. While the increase was small (6 bps), we suspect the longer-run dot will drift higher very slowly to reflect a neutral rate that may have moved somewhat higher relative to the pre-pandemic period.

- The slightly higher fed funds rate outlook comes amid more upbeat projections for economic growth and stickier inflation this year. That said, the Committee's estimates for unemployment and inflation were barely changed for 2025-2026.

- The statement was virtually unchanged, with only a minor tweak to the paragraph on recent economic conditions. The Committee continues to seek "greater confidence that inflation is moving sustainably toward 2%" before reducing the fed funds rate.

- Overall, the updated Summary of Economic Projections suggests that the FOMC believes that inflation is on a path back to its 2% target, but it is likely to be achieved slightly later than previously expected. We continue to look for the FOMC to start reducing the fed funds rate at its June 12 meeting. However, the risks to our outlook are skewed toward the FOMC beginning to ease a little later in the summer or potentially proceeding at a slower pace that leads to less than the 100 bps of easing we project through the end of this year.

- While risks to the FOMC beginning to cut the fed funds rate skew toward later in the year, balance sheet normalization looks likely to occur somewhat earlier. In light of Powell's comments at today's press conference, we think an announcement to slow the pace of quantitative tightening is coming at the May 1 meeting, although we would not be surprised if it slipped to the following meeting on June 12.

FOMC Signals Cuts Coming, Just Not Yet

As widely expected, the FOMC left the target range for the federal funds rate unchanged at 5.25-5.50% at the conclusion of its March meeting. The last rate hike occurred in July 2023, and the Committee has left its policy rate unchanged in the eight months since.

The Summary of Economic Projections (SEP) signaled that all but two of the Committee members expect to start cutting rates this year, with the median participant projecting 75 bps of easing by year-end 2024 (chart). The 2024 median dot was unchanged from the December SEP, although the distribution drifted higher in a sign that policymakers remain on guard against sticky inflation. In that vein, the median dots for 2025 and 2026 rose by 25 bps in each year, consistent with 75 bps of easing in 2025 and another 75 bps of cuts in 2026.

The median "longer-run" dot also moved higher. The longer-run dot represents each participant's view of the level of the federal funds rate that would be most consistent with achieving the Federal Reserve's dual mandate of maximum employment and price stability over the long-run. The increase in the longer-run dot was small, just 6 bps, but it marks the first time the median has been above 2.5% since March 2019. We suspect the longer-run dot will drift higher very slowly to reflect a neutral rate that may have moved somewhat higher relative to the pre-pandemic period. Markets appear to be ahead of the Committee and are priced for short-term interest rates to be between three and four percent over the longer-run (chart).

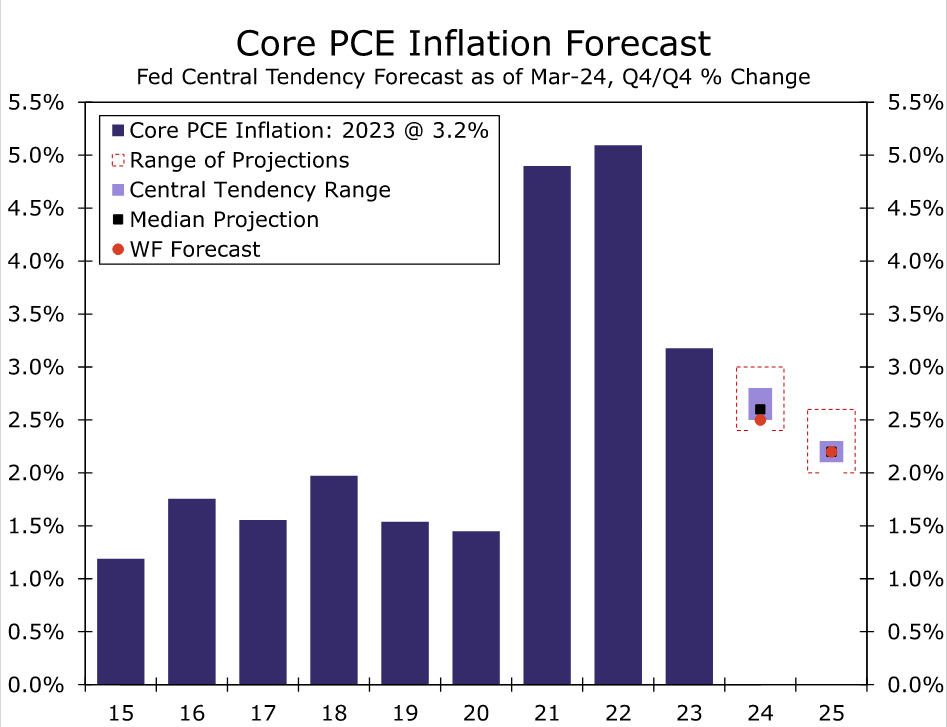

Elsewhere, the Committee's projections for the economy reflected continued resilience in both output and price growth. The median projection for real GDP growth in 2024 is 2.1%—up from 1.4% in the December SEP. Growth projections in 2025 and 2026 were also revised up by two tenths and one tenth of a percentage point, respectively. The Committee's inflation projections also rose modestly, most notably an increase in the median projection for 2024 core PCE inflation from 2.4% to 2.6% (chart). That said, the median forecasts for core inflation in 2025 and 2026 were left unchanged in a sign that the Committee remains confident that inflation progress will continue, just at a slightly slower pace than previously believed.

The post-meeting statement contained virtually no changes to what was released following the January 31 meeting. Job gains were still characterized as "strong," although the phrase that hiring has "moderated since early last year" was stricken with payrolls averaging 265K the past three months. The remainder of the statement contained no changes. Economic activity continues to expand at a "solid" pace, and inflation "remains elevated." Notably, the FOMC continues to seek "greater confidence that inflation is moving sustainably toward 2%" before reducing the fed funds rate.

Source: U.S. Department of Commerce, Federal Reserve Board and Wells Fargo Economics

Source: Federal Reserve Board and Wells Fargo Economics

Overall, the updated Summary of Economic Projections suggests that the FOMC believes that inflation is on a path back to its 2% target, but it is likely to be achieved slightly later than previously expected. We currently expect the Committee to first ease policy at its June 12 meeting, at which time officials will have seen three more months of inflation and employment data, and ultimately reduce the fed funds rate by a total of 100 bps this year (chart). However, with the Committee more upbeat on prospects for economic activity and a bit more worried about inflation, the risks to our outlook are skewed toward the FOMC beginning to ease a little later in the summer (at its July 31 meeting), or potentially proceeding at a slower pace (e.g., every other meeting).

The Committee also reaffirmed its ongoing pace of balance sheet runoff, commonly referred to as quantitative tightening (QT), but Chair Powell's comments in the post-meeting press conference suggested that changes are coming. Powell stated that it is the Committee's view that it would be appropriate to slow the pace of asset runoff "fairly soon." Note that a slower pace of QT would still involve shrinking the Fed's balance sheet, just at a slower pace than what has occurred since QT ramped up in mid-2022. Coming into the meeting, our forecast assumed that the FOMC would announce a plan to slow the pace of QT at its June meeting. In light of Powell's comments today, an announcement at the May meeting seems slightly more likely than a June announcement, although we would not be surprised if it slipped to the June meeting. Either way, we expect the runoff caps for Treasury securities to be reduced to $30 billion while mortgage-backed securities caps are dropped to $20 billion, with this slower pace of runoff continuing until roughly year-end 2024.

Fed Review: Not as High, But for Even Longer?

- The Fed made no changes to its monetary policy in the March meeting, as widely expected. Updated rate projections still signal three rate cuts this year, but 2025, 2026 and longer-term 'dots' we revised slightly higher.

- While Powell did not specify the timing, he suggested that the Fed is soon looking to slow down the pace of QT. That said, we do not believe that completely ending the balance sheet run-off will be on the cards in the near-term.

- Markets reacted dovishly, with end-2024 Fed Funds Rate pricing declining by around 7-8bp and EUR/USD rising above 1.09. 2s10s UST yield curve steepened in line with the signals from the dot plot.

The Fed remains on track towards price stability (and consequently, rate cuts), despite 'bumps' seen in the inflation data in early 2024. Powell chose his wording carefully to avoid sounding too optimistic on inflation, but also made it clear, that as monetary policy remains restrictive and labour supply recovers, further disinflation is still on the radar.

The updated 2024 dots continue to signal three rate cuts, in line with our forecast. There was a slight hawkish adjustment, however, as now only one participant saw the Fed cutting rates more than three times in 2024 (down from 4 in December). In addition, 2025 & 2026 dots were adjusted higher by 25bp, reflecting a more positive outlook for growth. GDP is now seen growing by 2.1% in 2024 (from 1.4%) and 2.0% in 2025-2026 (from 1.8% & 1.9%). Relative to the December projections, participants judged that growth risks had become more balanced (previously tilted to the downside) while risk of higher-than-expected unemployment rate was seen declining. Slightly higher share of participants reported core inflation risks as tilted to the upside.

Interestingly, the longer-term rate projection was revised up to 2.6% (from 2.5%). In the past, we have discussed quick recovery in foreign labour force, faster productivity growth and persistently expansionary fiscal policy as possible drivers of faster potential growth, which could imply that the neutral rate of interest is also higher. We discussed the recent data on labour force in this week's edition of Reading the Markets USD, 19 March.

Powell provided only few details on the near-term plans for QT. He aimed to prepare the market for a slowdown in the pace of run-off in Treasury bond holdings 'fairly soon', but also suggested that completely ending QT will not be in the cards in the near-term. We believe the Fed will continue shrinking its balance sheet at least until the end of this year.

Powell's wording on the near-term rate outlook was mostly unchanged from before. Sudden weakening in labour market conditions could be a potential trigger for an early cut even if for now, Powell saw 'no cracks' in the current conditions. Market pricing for year-end 2024 Fed Funds Rate declined by around 7-8bp and broad USD weakened. We still believe that if incoming hard data begins to show similar signs of weakness as already seen in some of the leading indicators (hiring, ISM), then the Fed could potentially move as early as in the next May meeting. For now, though, we note that it is not a high conviction call, as markets price in only 3-4bp of cuts by May.