Sample Category Title

Dollar’s Next Move Hinges on CPI and Warsh’s First Testimony

- US CPI report and Fed Chair Warsh's dual testimonies in the spotlight.

- Headline inflation is expected to ease, but will the deceleration surprise?

- Investors to monitor Warsh's rhetoric for clues about a September rate hike.

- Euro/dollar could revisit recent lows if CPI surprise on the upside and Warsh appears hawkish.

Dollar in demand

The US dollar has been one of the main protagonists of 2026, with the arrival of newcomer Fed Chair Warsh adding to the plethora of bullish catalysts. The dollar index climbed in late June to the highest level since May 2025, when the greenback was trying to recover from the reciprocal tariff announcements.

Busy data calendar – CPI in the spotlight

Next week's calendar will be exceptionally busy with a series of data prints and the first Humphrey-Hawkins testimony from Fed Chair Warsh. Specifically, the last CPI report ahead of the July 29 Fed meeting will be released on Tuesday at 12:30 GMT.

Following the solid May print, given the 20% monthly drop in oil prices in June and despite the World Cup boosting spending, there is a strong probability of the headline CPI decelerating below the 4% level again, largely erasing the May jump. Similarly, core CPI should also follow suit with a smaller drop. Both are expected to remain above the 2% inflation target.

PPI and retail sales data releases will follow on Wednesday and Thursday respectively, while Friday's University of Michigan Consumer Sentiment index will complete the picture. Following the strong PPI report from China, chances of another solid PPI print cannot be underestimated, while both retail sales and UoM survey could climb on the back of the lower energy prices and the World Cup impact, especially as these data releases cover a period when the US soccer team was advancing in the tournament.

Warsh's testimony stands out

Fed Chair Warsh will appear before the House Financial Services Committee on Tuesday and before the Senate Banking Committee on Wednesday. Both have a starting time of 14:00 GMT with the latter usually being less market-moving.

Since taking office, Fed rate hike expectations have jumped, with Warsh's post-FOMC meeting press conference, the panel discussion at the ECB Forum in Sintra, Portugal and the June 17 meeting minutes justifying these hawkish expectations.

Warsh has made it quite clear that he dislikes forward guidance in normal periods and has emphasized the Committee's unease about inflation running well above target, thus highlighting that there is work to be done on price stability. The minutes left little doubt about the hawks holding the upper hand in the FOMC.

Warsh is expected to move along these lines in his dual testimonies, potentially also highlighting the failures of his predecessor to get inflation under control and claiming that the Fed's stance has been distorted by an inflated balance sheet and non-rate measures.

Barring a major hawkish surprise that puts a July rate hike on the table, investors will closely watch for any clues about the expected September rate hike and whether the recent soft labour market data has alarmed Warsh. If Warsh appears confident about the jobs market, expectations of a September hike could strengthen.

Dollar stabilizes after strong gains

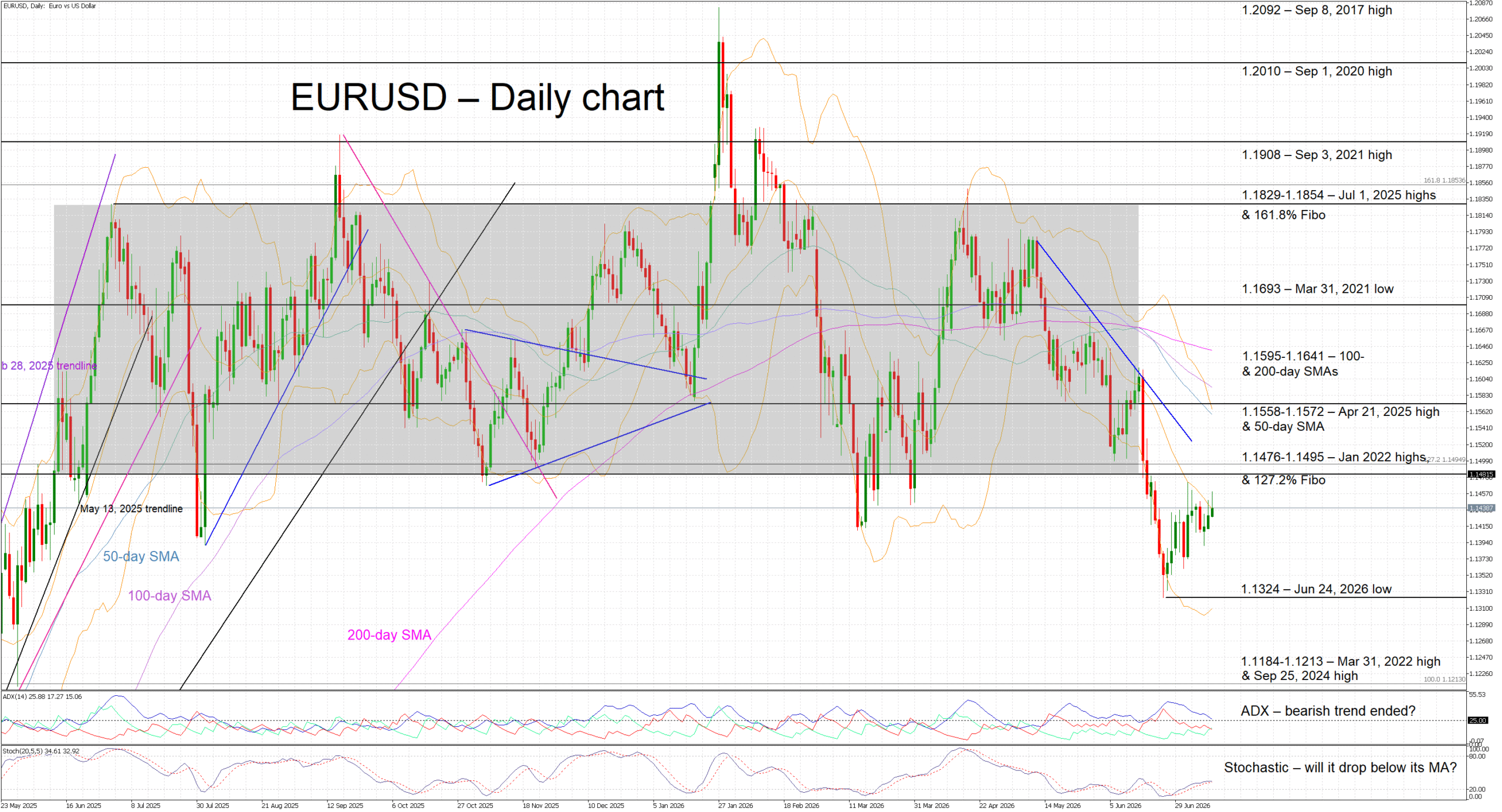

Following the June FOMC meeting, euro/dollar broke the one-year-long wide 1.1470-1.1829 range, dropping to the lowest level since May 30, 2025. With the ECB's hawkish stance exerting little upside influence on this pair and the eurozone economy struggling, the greenback dictates movements.

A softer inflation print on Tuesday and Warsh largely repeating his recent comments could somewhat dent the dollar's appeal. However, expectations for a September hike will most likely remain well supported. A test of the lower boundary of the recent range at 1.1470 could materialize but such a move might prove short-lived.

On the other hand, an inflation report that fails to show significant deceleration and a hawkish Warsh – for example, by repeating the Fed's commitment to price stability while dismissing job market concerns – could push euro/dollar towards the recent trough of 1.1324.

Dow Jones Index Wave Analysis

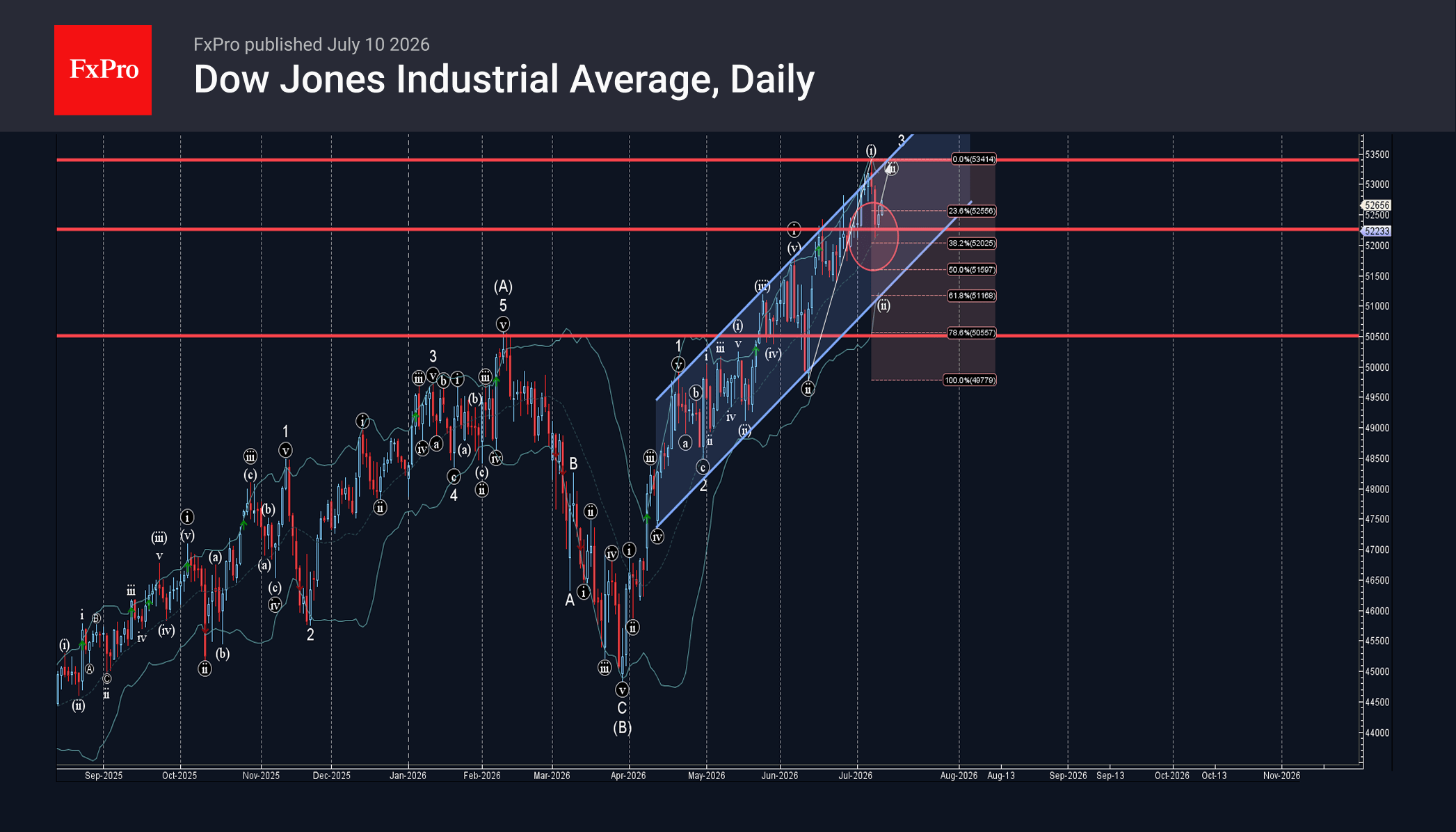

Dow Jones index: ⬆️ Buy

– Dow Jones reversed from support zone

– Likely to rise to resistance level 53500.00

Dow Jones index recently reversed up from the support zone between the support level 52250.00 (former strong resistance from June), 38.2% Fibonacci correction of the upward impulse from June and 20-day moving average.

The upward reversal from this support zone started the active minor impulse wave iii of the intermediate impulse wave (C) from March.

Given the strong daily uptrend, Dow Jones index can be expected to rise further to the next resistance level 53500.00 (which stopped earlier impulse wave i).

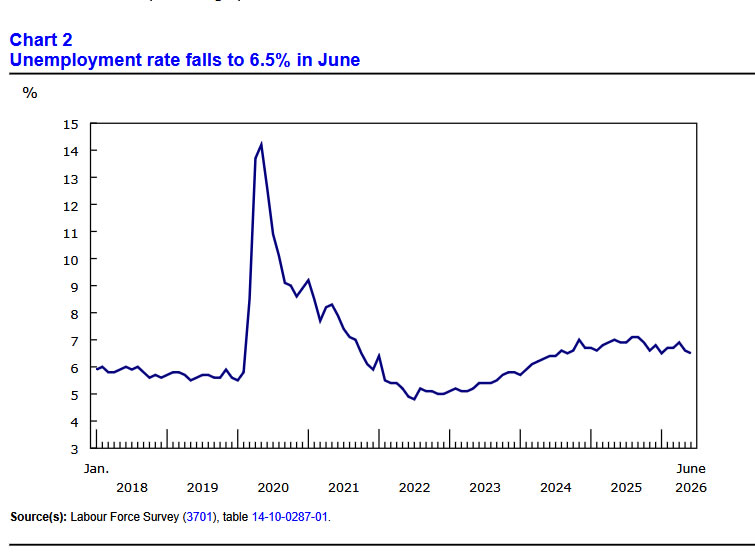

Canada’s Job Market Takes a Small Step in the Right Direction in June

- Canada’s economy added 18k jobs in June (+0.1% m/m), broadly in line with consensus expectations for a 10k gain. Employment gains were concentrated in the private-sector, while public-sector employment declined on the month.

- The unemployment rate eased to 6.5% from 6.6%, as labour supply remained stable, with the labour force participation rate holding at 65%.

- Job gains were led by accommodation and food services (+15k), while manufacturing lost 17k jobs. Manufacturing employment has fallen by 61k since January 2025 (3.2%), when tariff uncertainty began.

- Average hourly wages rose 3.3% year-on-year in June, up from a 3.0% pace in May.

Key Implications

- This report landed broadly in line with market expectations. Following May’s exceptionally strong gain, hiring moderated in June, and the unemployment rate returned to where it began the year. Pulling back the lens, Canada’s labour market has made modest, but positive progress over the past year.

- Manufacturing, where job losses continue to mount, remains a poster child of the uncertainty hanging over the Canadian economy. It is a reminder that the economy continues to operate below capacity, with downside risks concentrated in trade-exposed sectors. This should continue to provide a disinflationary offset. With this backdrop we expect the Bank of Canada to remain on the sidelines and keep its policy rate unchanged at 2.25% at next week's meeting.

Markets Stay in Wait-and-See Mode as Canada, Japan and Oil Offer No Breakthrough

Currency markets is heading to the end of the week on a subdued note as a series of developments across Canada, Japan and the Middle East ultimately reinforced existing narratives rather than triggering a meaningful repricing. Canadian Dollar gained modest support after another resilient employment report, while Yen held onto earlier gains sparked by Japan's pension fund initiative. Yet neither move developed into a sustained trend. Elsewhere, easing tensions between the US and Iran helped keep Brent crude comfortably below the critical USD 80 mark, allowing broader FX trading to settle into consolidation.

Canada Jobs Reinforce BoC Hold

Canadian Dollar firmed modestly in the early US session after June employment data came in slightly stronger than expected. Employment rose by 18.2k against expectations for a 10.0k increase, while the unemployment rate unexpectedly fell to 6.5% from 6.6%. The report was further supported by a steady participation rate and firmer wage growth, presenting a broad picture of a labor market that continues to outperform expectations.

The figures pose a meaningful challenge to any outright dovish Bank of Canada narrative. They reinforce Governor Tiff Macklem's assessment that the domestic economy has remained resilient despite growing uncertainty surrounding Canada's evolving trade relationship with the United States. At the same time, the report falls well short of making a convincing case for renewed tightening. With structural uncertainty surrounding the USMCA review still clouding the medium-term outlook, markets continue to expect the BoC to leave rates unchanged through the remainder of the year. Next week's policy meeting is unlikely to produce a material shift in guidance.

Japan's Structural Idea Needs Time

Yen also remained generally firmer after Finance Minister Katayama suggested encouraging pension funds to increase investment in domestic financial assets. Investors viewed the comments as pointing toward a potential structural solution to one of the Ten's longstanding weaknesses—persistent capital outflows into overseas assets—rather than another round of tactical currency intervention.

However, the initial enthusiasm has begun to fade. The proposal remains an idea rather than a formal policy initiative, and any meaningful portfolio reallocation would require decisions by independent institutional investors such as GPIF. Even if implemented, the process would unfold gradually over years rather than weeks, while the wide interest-rate differential between Japan and the United States continues to underpin carry trades. As a result, today's gains lacked strong follow-through despite the favorable initial market reaction.

Oil Retreat Keeps Broader Markets Calm

Meanwhile, geopolitical concerns also moderated after another round of hostilities between the United States and Iran earlier in the week. While attacks briefly renewed worries about global energy supplies and the security of Strait of Hormuz transit, Brent crude eased back toward USD 76 after failing to sustain gains above USD 80. The pullback suggests markets continue to view the latest flare-up as another episode within an ongoing negotiation process rather than the beginning of a renewed regional conflict.

Reports that both sides have returned to technical discussions further supported that interpretation. As long as Brent remains below the USD 80 threshold, investors appear reluctant to rebuild a significant geopolitical risk premium across broader financial markets.

For the week so far, New Zealand Dollar remains the strongest major currency, followed by Sterling and Canadian Dollar, while Swiss Franc, Yen and Euro lag the performance table.

Yen Jumps as Markets See Katayama's Pension Fund Push as Structural Fix for Currency Weakness

The Yen's latest rally wasn't driven by intervention speculation. Markets instead focused on a potential structural shift in Japan's capital flows after Finance Minister Katayama encouraged greater domestic investment by pension funds. Find out why investors believe this could have a more lasting impact than traditional FX intervention. Read More.

Canada Employment Tops Forecast as Jobless Rate Falls Again

Canada's employment rose by 18.2k in June while the unemployment rate fell to 6.5%, reinforcing labor market resilience ahead of next week's Bank of Canada meeting. Read More.

Japan PPI Hits Fastest Pace Since 2023 as Energy, AI Demand Drive Costs Higher

Japan's wholesale inflation accelerated to its fastest pace since March 2023 as the Middle East energy shock, booming AI-related metals demand and a weaker yen combined to push producer prices higher. Read More.

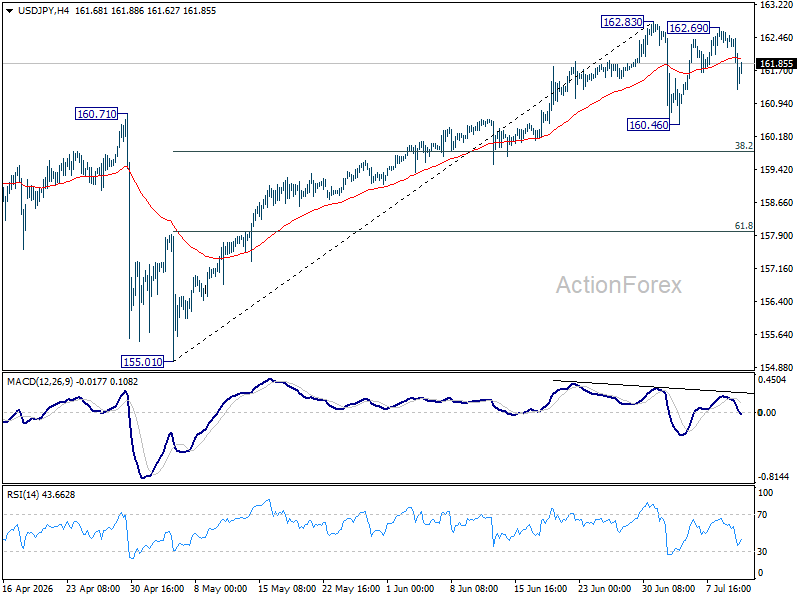

USD/JPY Daily Outlook

USD/JPY falls sharply today but still it's bounded in range below 162.83. Intraday bias remains neutral and more consolidations would be seen. In case of deeper pullback, downside should be contained by 38.2% retracement of 155.01 to 162.83 at 159.84. On the upside, firm break of 162.83 will resume larger up trend.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.

Canada Employment Tops Forecast as Jobless Rate Falls Again

Canada's labor market continued to show resilience in June, with employment rising by 18.2k, comfortably above expectations for a 10.0k increase. While hiring slowed from May's exceptionally strong 87.8k gain, the latest figures point to continued labor market stability rather than the sharp normalization many investors had anticipated. The unemployment rate unexpectedly declined to 6.5% from 6.6%, marking a second consecutive monthly fall and reinforcing the view that labor demand remains firm despite mounting uncertainty surrounding Canada's trade outlook.

The details of the report were broadly encouraging. The employment rate edged up 0.1 percentage point to 60.8%, while the labor force participation rate held steady at 65.0%, indicating that the decline in unemployment was driven by stronger hiring rather than workers leaving the labor force. On a year-over-year basis, employment increased by 99k, or 0.5%, led by a 131k gain in full-time positions. Wage growth also picked up, with average hourly earnings rising 3.3% from a year earlier after a 3.0% increase in May, suggesting income growth remains supportive of household spending.

The figures are unlikely to fundamentally change the Bank of Canada's policy outlook, but they do weaken the case for markets to price a more dovish stance ahead of next week's meeting. Governor Tiff Macklem has emphasized that the larger challenge facing Canada is structural rather than cyclical, with evolving trade relations under the USMCA review process expected to reshape investment and growth over time. One stronger employment report does little to resolve those longer-term uncertainties, but it does suggest the domestic economy is going through that adjustment period in a position of greater strength than many investors had assumed.

| Indicator | June | May | Expectation |

|---|---|---|---|

| Employment Change | +18.2k | +87.8k | +10.0k |

| Unemployment Rate | 6.5% | 6.6% | 6.6% |

| Employment Rate | 60.8% | 60.7% | — |

| Participation Rate | 65.0% | 65.0% | — |

| Average Hourly Wages (YoY) | 3.3% | 3.0% | — |

| Employment (YoY) | +99k (+0.5%) | — | — |

| Full-Time Employment (YoY) | +131k (+0.8%) | — | — |

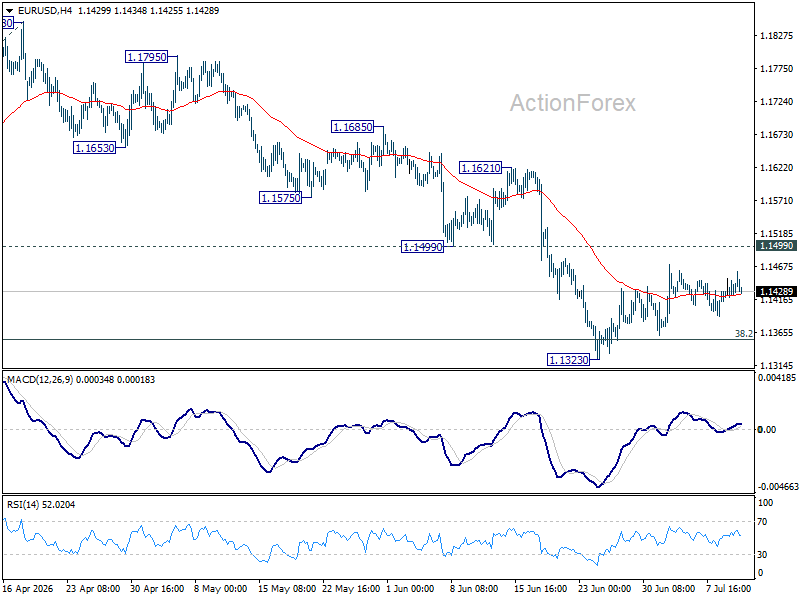

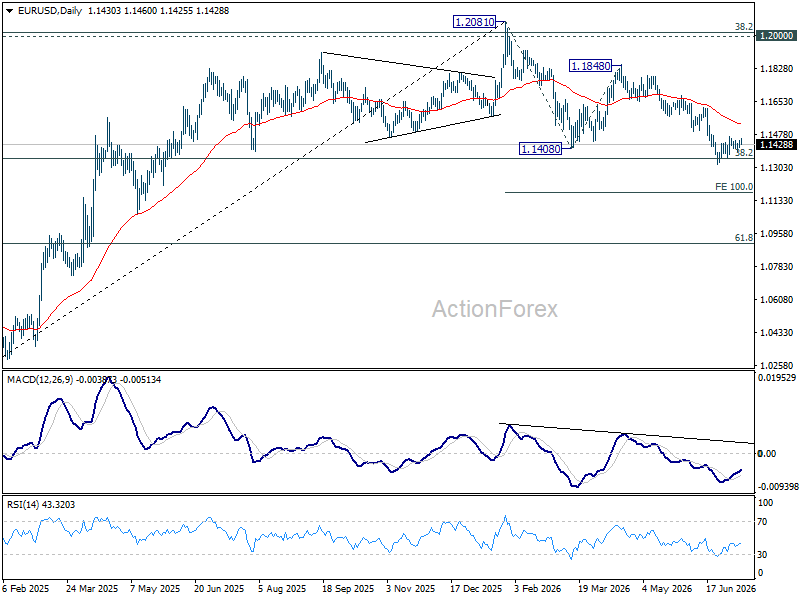

EUR/USD Daily Outlook

EUR/USD is still bounded in consolidations above 1.1323 and intraday bias remains neutral. . With 1.1499 support turned resistance intact, further decline is expected. On the downside, break of 1.1323 will resume the fall from 1.2081 to 100% projection of 1.2081 to 1.1408 from 1.1848 at 1.1175. However, decisive break of 1.1499 will turn bias back to the upside 1.1621 resistance and above.

In the bigger picture, focus is back on 38.2% retracement of 1.0176 to 1.2081 at 1.1353. Decisive break there will revive the case of medium term bearish trend reversal after rejection by 1.2 key cluster resistance level. Further fall should be seen to 61.8% retracement at 1.0904. Nevertheless, strong rebound from 1.1353, followed by break of 1.1621 resistance, will retain medium term bullishness.

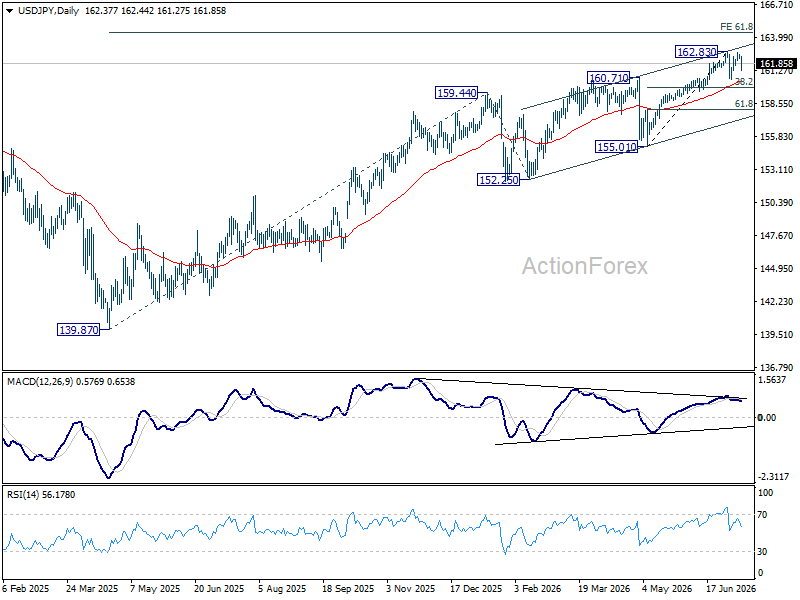

USD/JPY Daily Outlook

USD/JPY falls sharply today but still it's bounded in range below 162.83. Intraday bias remains neutral and more consolidations would be seen. In case of deeper pullback, downside should be contained by 38.2% retracement of 155.01 to 162.83 at 159.84. On the upside, firm break of 162.83 will resume larger up trend.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.

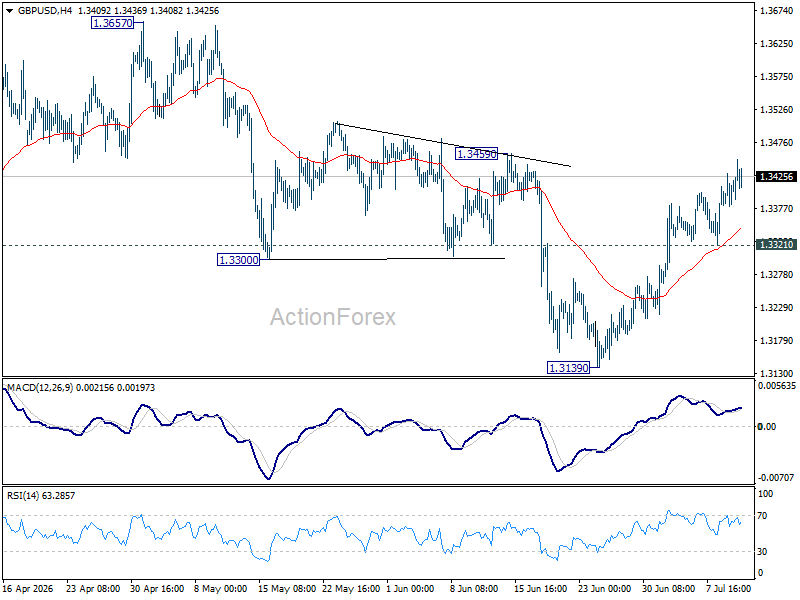

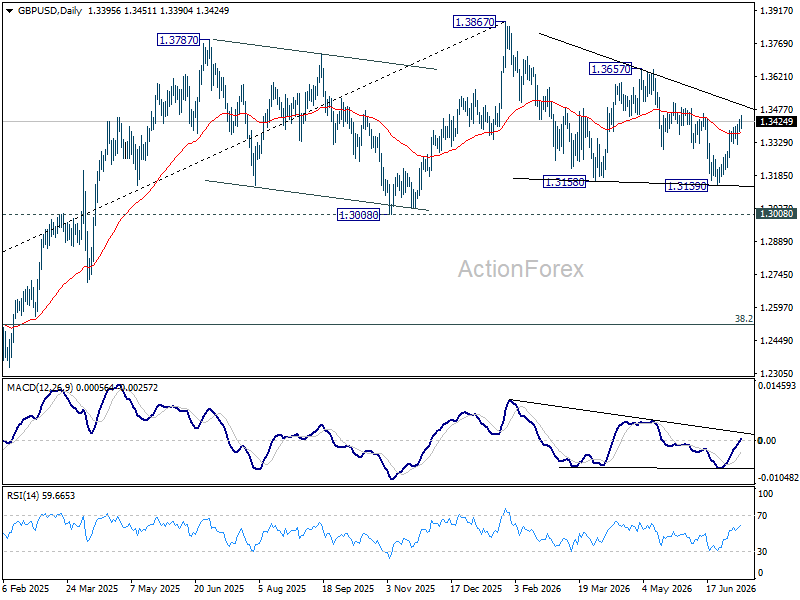

GBP/USD Daily Outlook

Intraday bias in GBP/USD remains on the upside for the moment. Firm break of 1.3459 will argue that whole correction from 1.3867 has completed, and target 1.3657 resistance for confirmation. On the downside, below 1.3321 minor support will bias neutral again first.

In the bigger picture, price actions from 1.3867 are a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

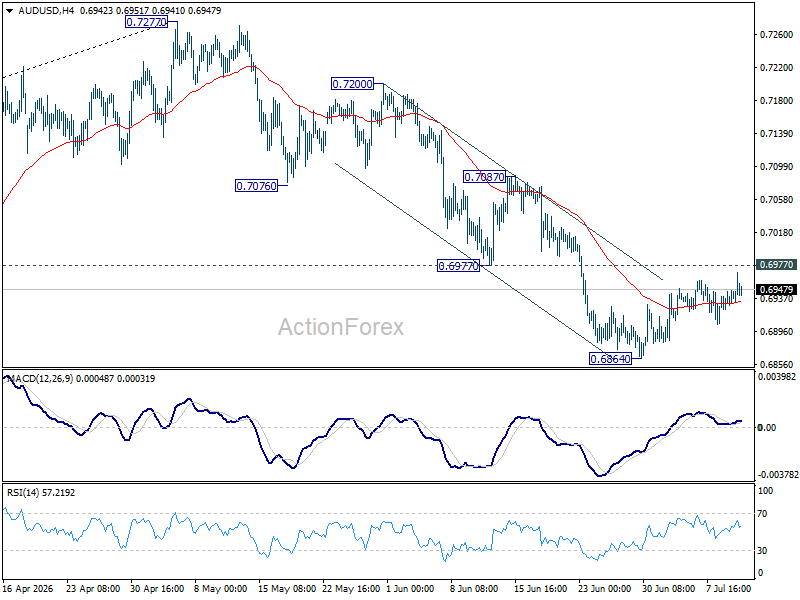

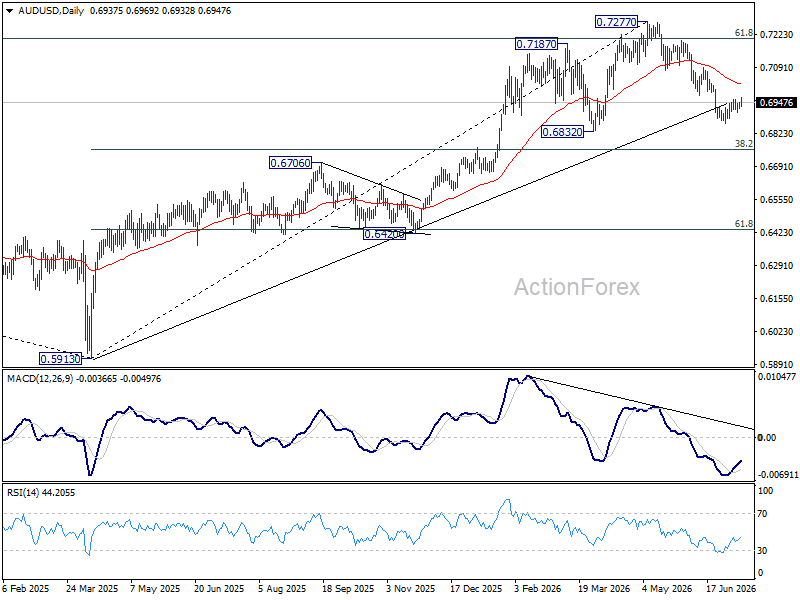

AUD/USD Daily Report

Intraday bias in AUD/USD remains neutral as consolidations continue above 0.6864. Further fall is expected as long as 0.6977 support turned resistance holds. Below 0.6864 will target 0.6832 support. Firm break there will target 0.6756 fibonacci level. However, sustained break of 0.6977 will bring stronger rebound to 0.7087 resistance instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206. Deeper fall could be seen to 38.2% retracement of 0.5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.

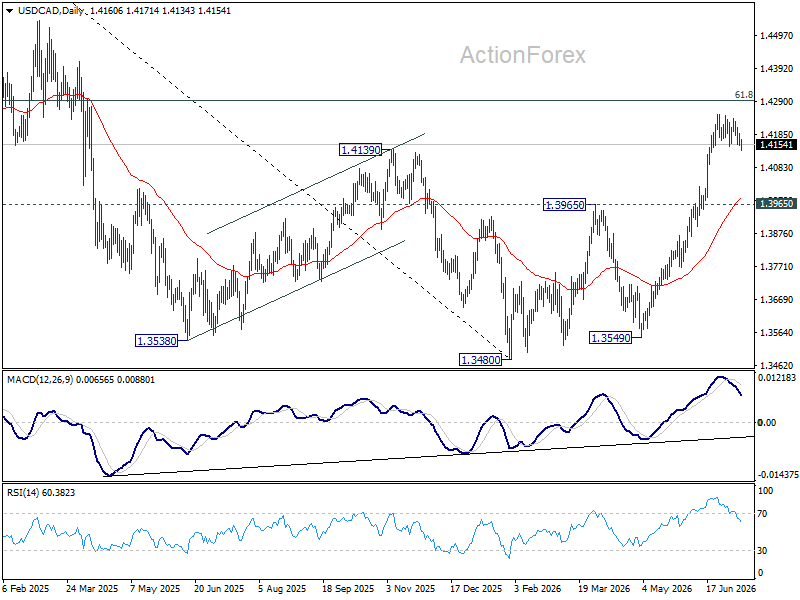

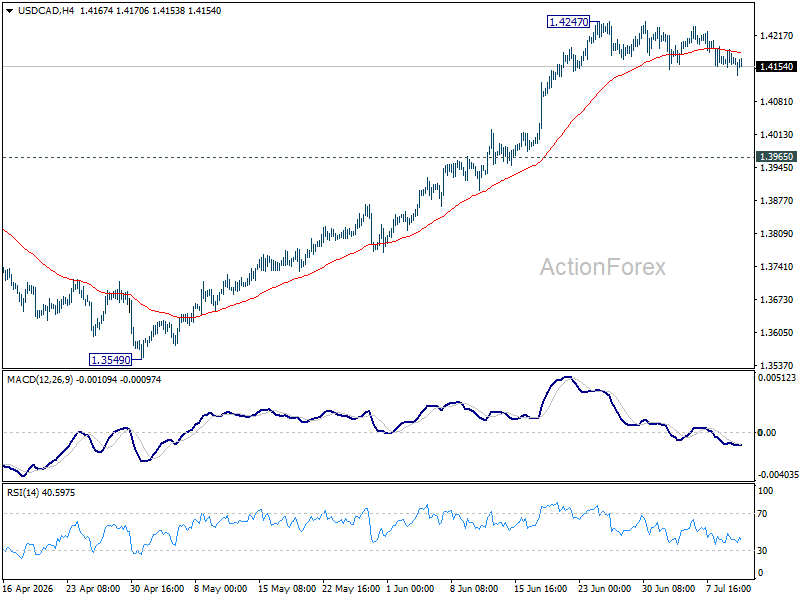

USD/CAD Daily Outlook

USD/CAD is still extending consolidations below 1.4247 and intraday bias remains neutral. Deeper pullback cannot be ruled out. But downside should be contained above 1.3965 resistance turned support. Above 1.4247 will resume the rally from 1.3480 to 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Firm break there will pave the way back to 1.4791 high.

In the bigger picture, current development suggests that fall from 1.4791 has completed as a three wave correction to 1.3480. It's still early to judge if rise from there a corrective bounce, or resumption of the larger up trend from 1.2005 (2021 low). But in either case, retest of 1.4791 high should be seen next.