Sample Category Title

Sunrise Market Commentary

Markets

While upward pressure on oil prices eased throughout the day yesterday, (natural) gas prices kept adding to the recent gains. The Dutch TTF future hit the €50/MWh for the first time in a month, up 25% from their recent lows (which in turn were about a third higher than pre-war levels). That followed reports from key producer Qatar pausing its push to ramp up LNG output over concerns that transit through the Hormuz Strait isn't safe. Gas is an important component in the euro area's energy mix and features the ECB discussions as prominent as oil does. Markets however took comfort from the latter's price developments over the last 24 hours. Core bonds recovered from their Wednesday whammy, dragging German yields up to 6 bps down at the front end. An October ECB hike remains more than fully priced in. Longer maturities ended flat after turning in additional, marginal gains earlier on the day. Gilts outperformed Bunds with UK yields shedding 6.7-9 bps across the curve. The US Treasury yield curve bull steepened as well, correcting lower by 0.8-4.5 bps. A $22bn 30-yr auction yesterday stopped through with demand metrics strong, helping to push bonds higher be it temporarily. Stock markets rebounded, led by tech (Nasdaq +1.3%) and kept the USD slightly in the defensive. DXY finished sub 101. EUR/USD rose a bit higher north of the 1.14 big figure. USD/JPY stabilized around 162+ levels. The yen, however, is taking the lead in Asian dealings this morning. The pair pushes lower towards 161.5. That followed on news that the Japanese government is pursuing measures that would include one of the world's largest pension funds to do substantially greater investments in Japanese financial assets (see below). It's triggering some of the biggest moves overnight (including in JGB's). Other news is limited. The US said that technical talks with Iran are continuing, perhaps easing some concerns for the conflict to re-escalate into a full blown war. It is, however, nothing new. President Trump, after considering the ceasefire to be over for him, kept the door open for talks, leaving it up to the negotiators to do as they see fit. Brent even slightly grinds higher to $76. Today's eco calendar is all but empty. In technical and probably uninspiring trading going into the weekend we do keep an eye at the long end of the curve that appears to be easily triggered into a yield rise but not as much into a decline.

News & Views

Japanese Finance Minister Satsuki Katayama said the government wants the country's pension funds to substantially lift investments in domestic assets. The Fin Min explained this aim as she assessed that the government wants 'to ensure that the public can directly benefit from Japan's economic growth'. From a market point of view, it would be especially relevant for Japanese financial markets if the Government Pension Investment Fund, managing 293.6 trillion yen (about $1.8 tn), would allocate more of its investments into the domestic markets. Japanese markets at least performed constructively this morning with the Nikkei gaining 1.7%. Long-term Japanese bonds rebound after a difficult period of late (10-y JGB -9.6 bps; 30-y JGB -7.3 bps). Even the yen rebounded from the USD/JPY 162.4 area to the USD/JPY 161.5 area. Regarding Japanese data, Japanese June PPI printed 0.4% m/m and 7.1% y/y (from 1.1% and 6.6% in May). The y/y measure was the highest since the spring of 2023. This kind of pass-through of costs also still supports the case for a continuation of policy normalization.

Inflation in Mexico eased for the third consecutive month in June. Headline inflation declined 0.27% m/m, slowing y/y inflation from 3.94% to 3.37%, the lowest figure since early 2021. Core inflation printed at 0.24% m/m and 4.03% y/y (from 4.19%). The central Bank of Mexico has an inflation target of 3% with a tolerance band of 1ppt. It published the minutes of its June 25 decision when it left the policy rate unchanged at 6.5% in a unanimous decision. The unchanged decision came after a 25 bps cut in May. The bank saw appropriate to keep the policy rate at current level and expects that it might stay at that level for some time to come, even as it discussed upside inflation risks especially in the services sector. The recent decline of inflation was seen as having been driven by non-core components. After a sustained rally throughout most of 2025, the peso over the previous months holds rather strong in a relative tight range between USD/MXN 17.1 and 17.7.

Yen Jumps as Markets See Katayama’s Pension Fund Push as Structural Fix for Currency Weakness

Yen strengthened broadly today after Japanese Finance Minister Katayama said Tokyo wants to encourage pension funds, including the Government Pension Investment Fund (GPIF), to increase investment in domestic financial assets. While no formal policy changes were announced, markets interpreted the comments as a potential shift toward addressing one of the Yen's most persistent structural weaknesses: sustained capital outflows into overseas assets.

The reaction extended well beyond the currency market. Japanese government bonds rallied sharply across the curve, with the 20-year yield falling 11.5 basis points to 3.75%, the 10-year yield dropping 10 basis points to 2.775%, and both the 30- and 40-year yields declining by more than 8 basis points.

A Shift From Intervention Toward Capital Flows

The market's response reflects the sheer scale of Japan's institutional investors. GPIF, the world's largest pension fund with approximately JPY 292.6 trillion in assets, has maintained a broadly balanced allocation between domestic and overseas bonds and equities since its landmark portfolio overhaul in 2014.

That shift away from Japan created a decade of structural capital outflows as hundreds of trillions of Yen were converted into foreign currencies to purchase overseas assets. Katayama's comments were therefore interpreted as opening the possibility—however tentative—of partially reversing that process.

Why Markets Reacted So Strongly

Such a shift could support the Yen through two channels:

- First, greater allocation to domestic assets would require converting part of existing foreign-currency holdings back into Yen, creating structural demand for the currency independent of any official intervention.

- Second, stronger demand for Japanese government bonds would provide additional long-term support for the JGB market at a time when investors have become increasingly concerned about rising long-end yields and Japan's fiscal outlook. In that sense, encouraging greater domestic investment could simultaneously strengthen the Yen and ease pressure on government borrowing costs.

More broadly, the proposal fits Japan's search for alternatives to conventional foreign-exchange intervention. With the interest-rate gap between the Federal Reserve and the Bank of Japan still around 250-275 basis points, aggressive BoJ tightening remains unlikely in the near term. Addressing capital flows instead offers policymakers another avenue to moderate structural Yen weakness without relying solely on either rate hikes or spot-market intervention.

A Structural Idea, Not Yet a Policy

Nevertheless, today's market move may prove premature if concrete follow-through fails to materialize. Katayama spoke only of encouraging greater domestic investment rather than announcing any formal portfolio changes. GPIF operates under an independent board with a fiduciary responsibility to maximize long-term returns, and its strategic asset allocation is typically reviewed only during its multi-year planning process rather than in response to ministerial comments.

Markets have seen similar episodes before, including last week's speculation over changes to Japan's intervention strategy, which quickly faded once no policy action followed. Moreover, even a meaningful reallocation by GPIF would not eliminate the large interest-rate differential that continues to underpin global carry trades against the Yen.

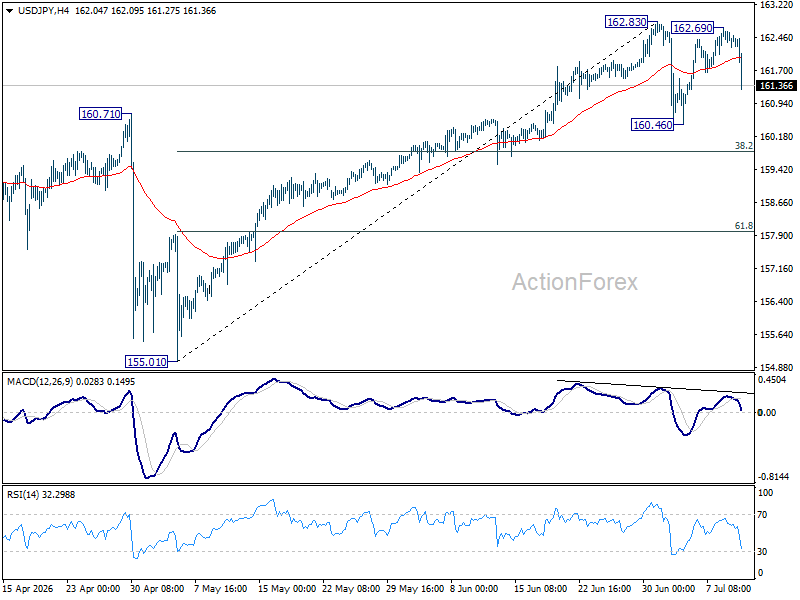

USD/JPY Extending Consolidations

Technically, USD/JPY's sharp decline confirms that the rebound from 160.46 has completed at 162.69 after rejection by the 162.83 high. However, the broader outlook remains unchanged.

The decline from 162.83 is viewed as the third leg of a consolidation pattern within the larger uptrend from 155.01. Deeper pullback could be seen to 160.46 and below. But strong support to emerge at 38.2% retracement of 155.01 to 162.83 at 159.84 to contain downside. The long term up trend is expected to resumed at a later stage, just delayed.

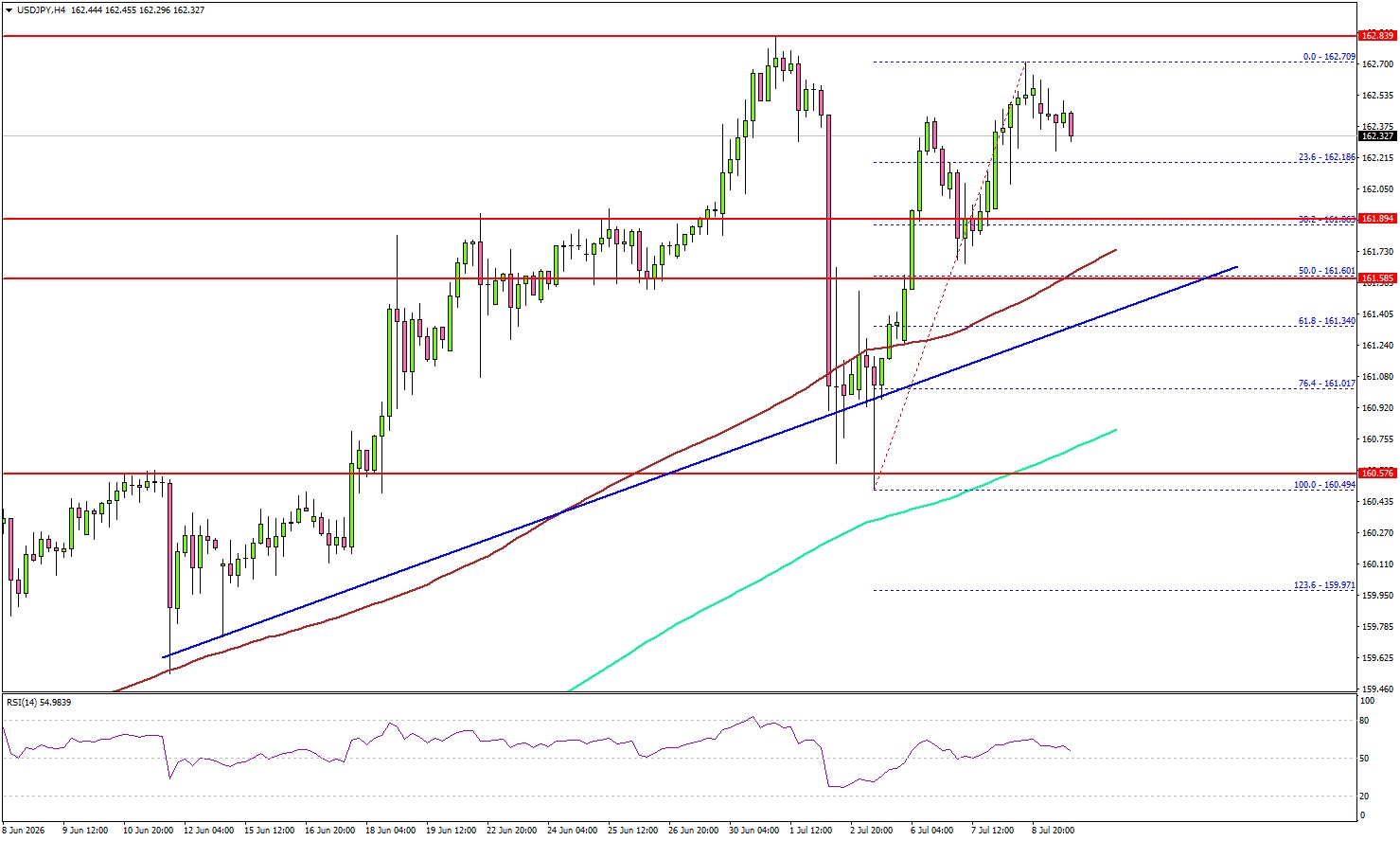

USD/JPY Holds Firm, but Is Another Upswing Ahead?

Key Highlights

- USD/JPY started a fresh increase but struggled near 162.80.

- A major bullish trend line is forming with support at 161.60 on the 4-hour chart.

- Bitcoin could gain bullish momentum if it settles above $65,000.

- WTI Crude Oil prices recovered some losses before the bears appeared near $76.20.

USD/JPY Technical Analysis

The US Dollar gained bullish momentum after it settled above $160.80 against the US Dollar. USD/JPY even climbed above 162.00 before it faced rejection.

Looking at the 4-hour chart, the pair again struggled to surpass the 162.70 and 162.80 levels. It is now correcting some gains and might dip toward the 38.2% Fibonacci retracement level of the upward move from the 160.49 swing low to the 162.70 high.

If there are more losses, the pair might find support near 161.60. Besides, there is a major bullish trend line forming with support at 161.60, the 100 simple moving average (red, 4-hour), and the 50% Fibonacci retracement.

The first major support could be near 160.80 and the 200 simple moving average (green, 4-hour). A downside break and close below 160.80 might send the pair toward 160.00. Any more losses could open the doors for a test of 158.80.

On the upside, the bears might remain active near 162.80. The next major resistance might be 163.40. A close above 163.40 could spark a sharp increase. In the stated case, the bulls could aim for a move to 165.00.

Looking at Bitcoin, the price could start a fresh increase, but a close above $65,000 is important for upside continuation.

Upcoming Key Economic Events:

- USDA WASDE Report.

- Canada’s Net Employment Change for June 2026 – Forecast 10K, versus 87.8K previous.

- Canada’s Unemployment Rate for June 2026 - Forecast 6.6%, versus 6.6% previous.

Japan PPI Hits Fastest Pace Since 2023 as Energy, AI Demand Drive Costs Higher

Japan's producer inflation accelerated more than expected in June, highlighting mounting cost pressures from the Middle East conflict, robust AI-related demand and the persistent weakness of the Yen. Producer Price Index rose 0.4% month-on-month and 7.4% year-on-year, exceeding expectations of 0.3% and 6.8% respectively. Annual producer inflation accelerated from 6.6% in May to its fastest pace since March 2023, suggesting upstream price pressures remain firmly elevated.

The increase was led by a 22.8% surge in fuel prices as higher energy costs continued to feed through supply chains following the conflict in the Middle East. At the same time, non-ferrous metal prices climbed 39.2% from a year earlier, reflecting strong global demand for AI-related raw materials. Together, the data indicate that both geopolitical supply shocks and structural investment trends are continuing to lift production costs across Japanese industry.

A weak Yen added another inflationary pressure. The Yen-based import price index accelerated to a 29.7% year-on-year increase in June from a revised 26.1% in May, underscoring the rising cost of imported raw materials. While producer inflation does not automatically translate into consumer inflation, the latest figures reinforce the Bank of Japan's assessment that price pressures remain elevated and will keep attention on how much of these higher input costs firms are able to pass on to households in the months ahead.

| Indicator | June | May | Expectation |

|---|---|---|---|

| PPI (MoM) | 0.4% | 1.1% | 0.3% |

| PPI (YoY) | 7.4% | 6.6% | 6.8% |

| Fuel Prices (YoY) | 22.8% | — | — |

| Non-Ferrous Metals (YoY) | 39.2% | — | — |

| Import Price Index (JPY basis, YoY) | 29.7% | 26.1% | — |

Loonie Tunes: Playing Second Fiddle to the Greenback

Highlights

- The Loonie has lost substantial ground to the greenback this year, a fate it shares with several other major G10 currencies.

- Wider interest-rate gaps have made U.S. assets more attractive, adding pressure on CAD alongside other advanced-economy currencies.

- The baseline still points to eventual loonie recovery, but that view is vulnerable if U.S. productivity strength keeps rates higher and USD assets more attractive for longer.

The Canadian dollar has weakened materially against the U.S. dollar this year, trading near the bottom of its year-to-date range after falling roughly 3.5% to 4% over the first half of the year. The move has been too broad and too closely tied to the repricing of U.S. assets to be read as a purely Canada-specific story. Instead, CAD weakness looks like one expression of a wider shift back toward U.S. dollar exposure, as markets moved away from earlier expectations that the Fed would be able to ease policy more quickly than other central banks.

That distinction matters for the outlook. If the loonie were simply being marked down on domestic concerns, the path forward would depend mainly on Canadian growth, inflation, and Bank of Canada policy. But if the larger force is renewed demand for U.S. dollar assets, CAD is more exposed to the broader global regime: how investors are pricing U.S. growth, U.S. rates, and the relative appeal of holding dollars versus other currencies. The recent evidence points more strongly to the second interpretation.

Loonie vs. Other Currencies

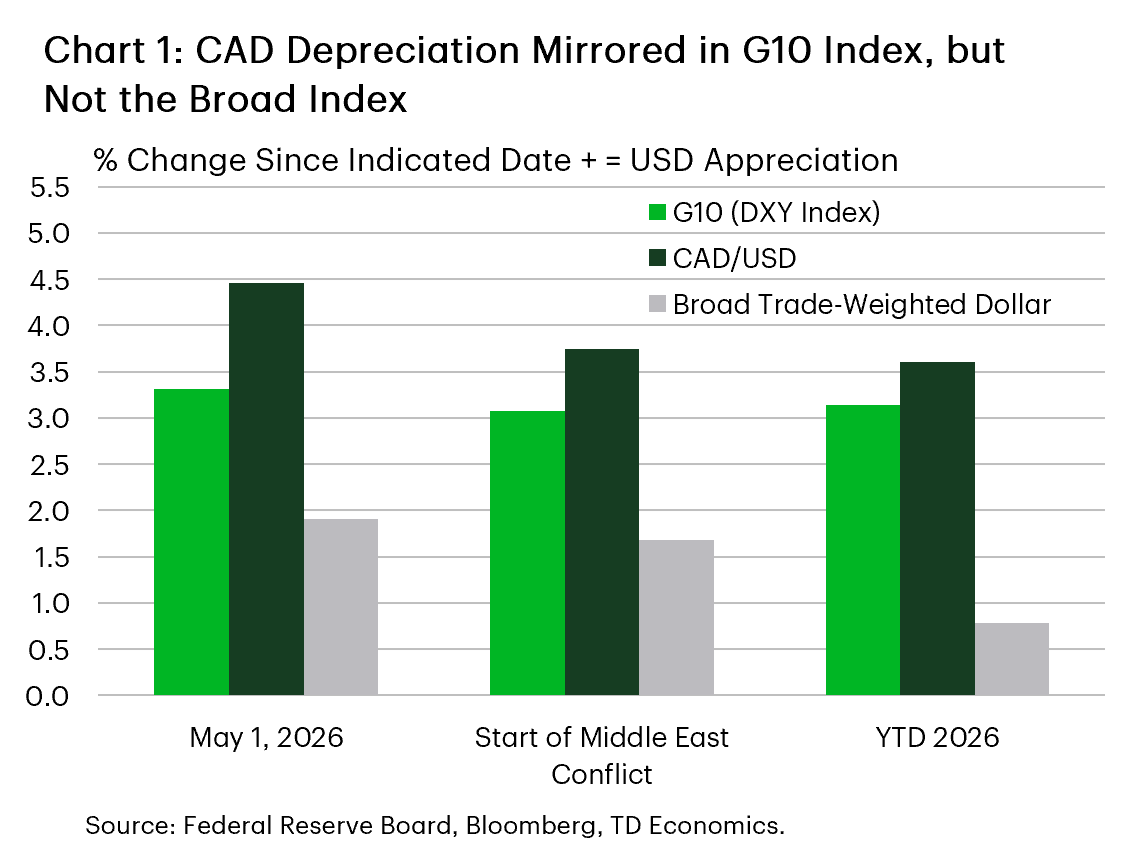

The cross-currency evidence supports this broader framing, but it is important to distinguish between different ways of measuring the U.S. dollar. DXY, the commonly cited "dollar index," tracks the dollar against a small group of major currencies, with the euro carrying by far the largest weight. That makes it useful as a quick read on dollar strength against major advanced-economy currencies, but less representative of how the dollar is moving against the full set of U.S. trading partners. Chart 1 shows that the latest dollar strength has been concentrated most heavily in the currencies that matter most for DXY, while the Federal Reserve's broader dollar index shows a more mixed pattern across the United States' 26 largest trading partners.

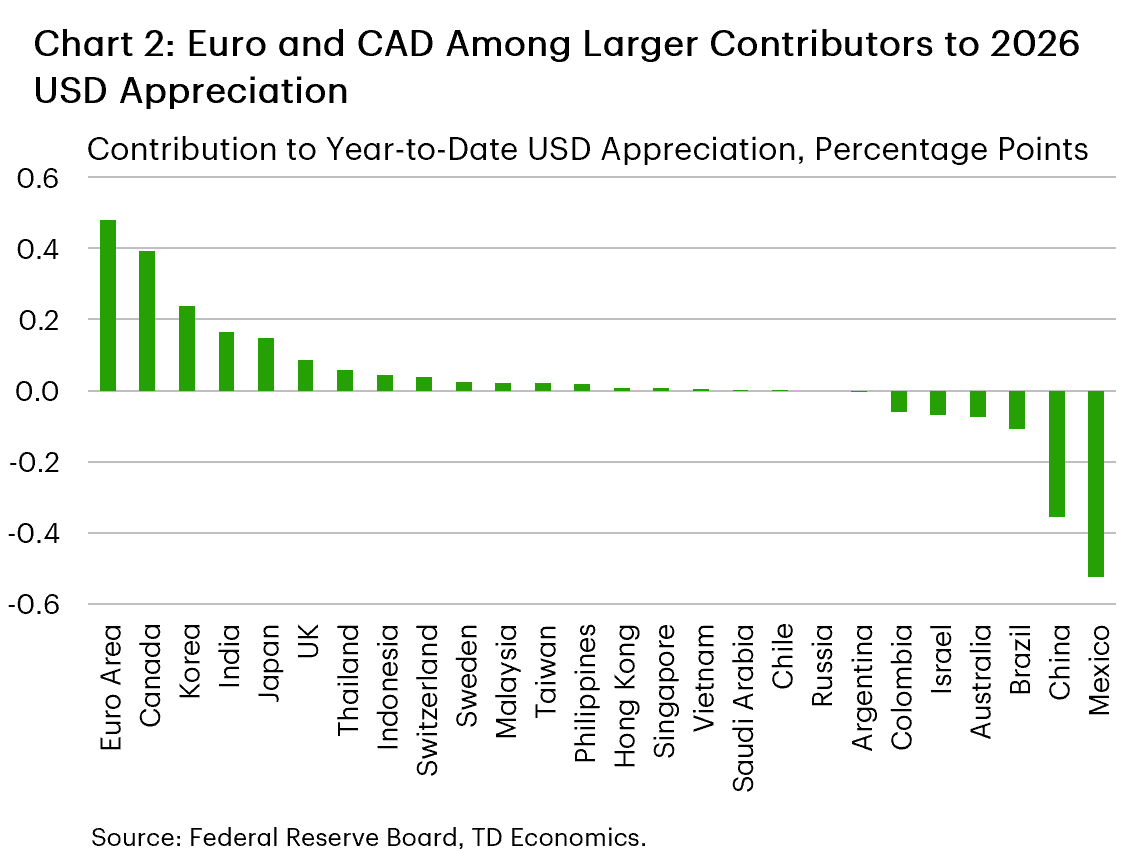

A closer inspection of the currencies in the broad index is offered in Chart 2. There, we can see three groups: the first group contains the currencies that have borne a disproportionate share of the latest dollar move, including the euro, loonie, Korean won, Indian rupee, and the Japanese yen. These are large, liquid currencies that carry meaningful weight in most dollar indexes, so their weakness helps explain why the bilateral CAD move has felt severe even though it is not isolated.

A second group has moved against the broader trend, led by the Mexican peso and Chinese renminbi. The peso is the clearest outlier, supported by high real rates, resilient domestic growth, and optimism around nearshoring, while the renminbi has been steadier than China's soft domestic backdrop would otherwise suggest, helped by policy management and efforts to limit sharp currency moves.

Most remaining currencies sit closer to the middle, moving broadly in line with the aggregate dollar move rather than clearly standing out in either direction.

This split reinforces that CAD has weakened because the dollar backdrop became more supportive, but the intensity of the move also depends on its own mix of growth, rates, policy credibility, and investor positioning. Canada fell into the group where the case for holding local currency became less compelling relative to the U.S. dollar, leaving the loonie more vulnerable once capital began moving back toward USD assets. We consider the usual candidate explanations for this development below.

Signs of Preference for the USD Coming Back

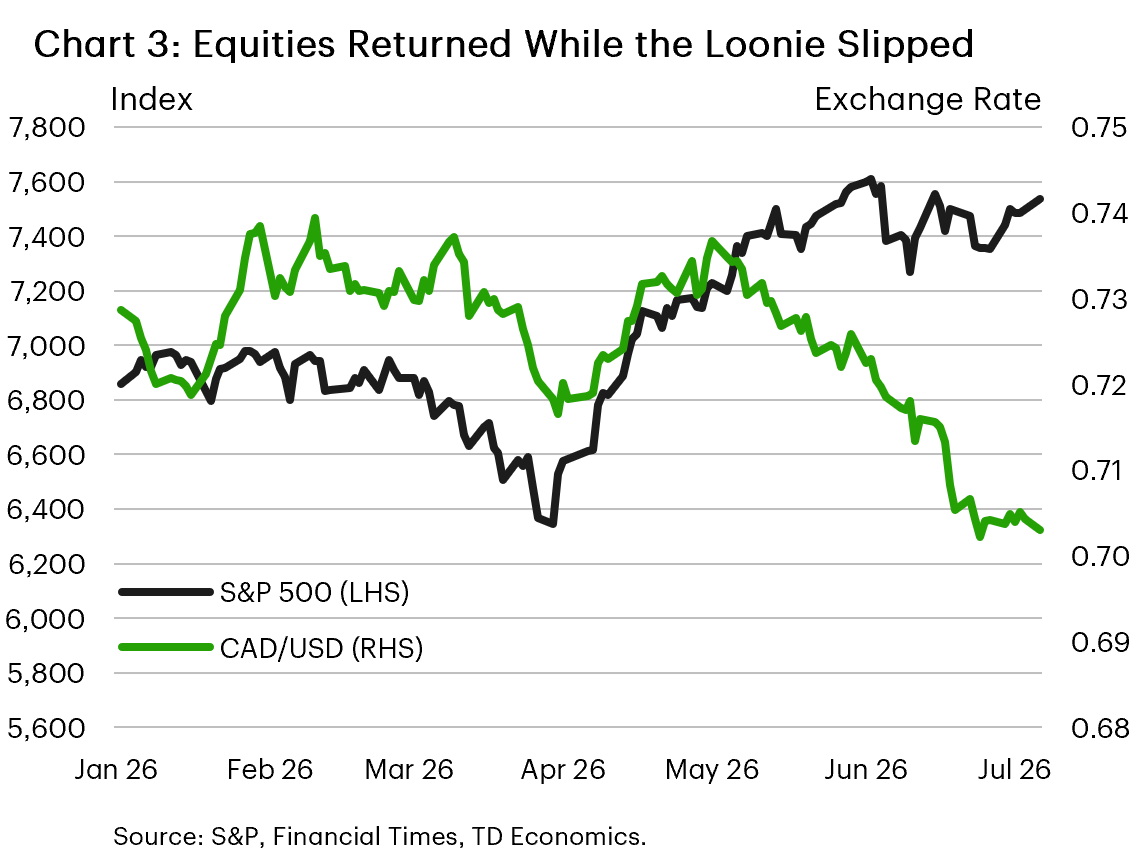

The timing of the move points to renewed preference for U.S. dollar exposure rather than a stand-alone CAD selloff. Chart 3 compares equities with CAD/USD and shows that the loonie started to weaken in May after the U.S. equity markets had recovered. That rebound helped confirm that markets had moved into a more comfortable risk backdrop and capital increasingly gravitated toward the U.S. dollar.

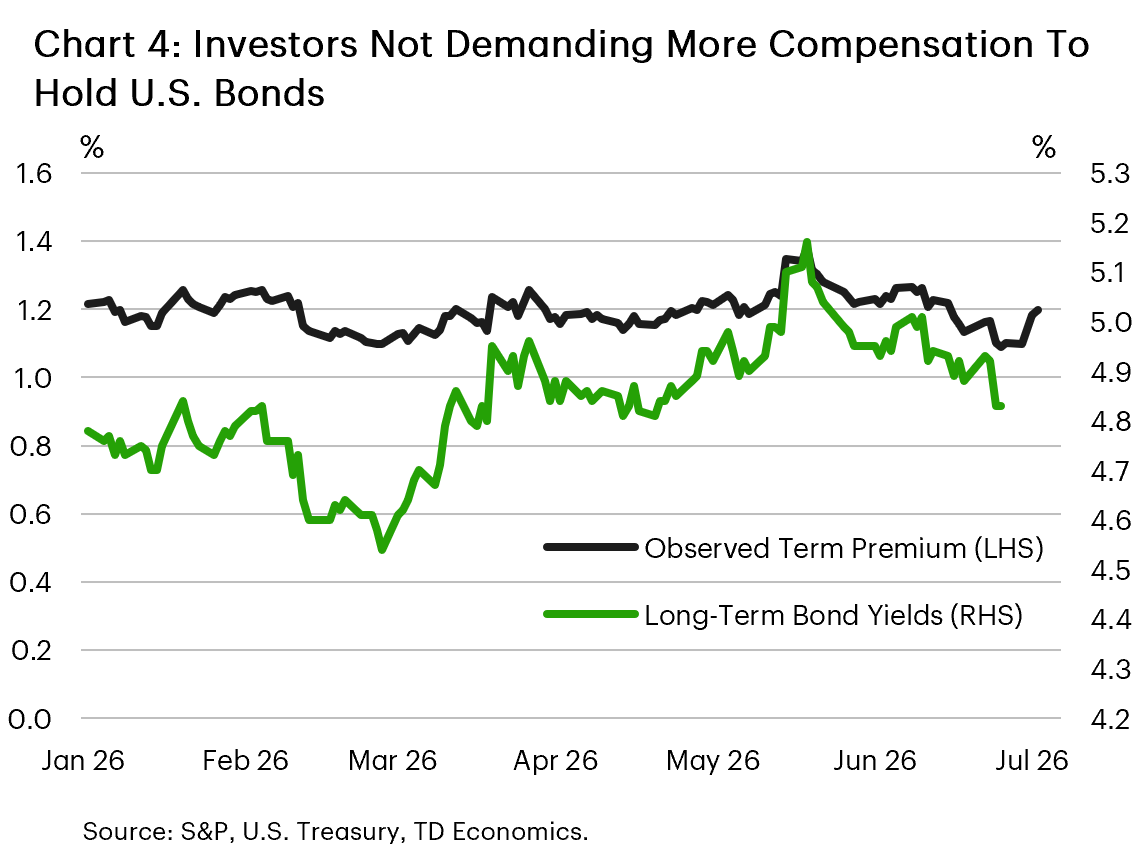

The bond market tells a similar story (Chart 4). Since mid-May, long-term Treasury yields and the observed term premium have moved lower, consistent with renewed demand for U.S. duration and a stronger preference for USD assets. Taken together, the equity and bond signals suggest that the market regime shifted from broad risk repair into a more dollar-centric phase, where investors were willing to take risk but preferred to do so through U.S. assets.

Limited Evidence of a Flight to Safety

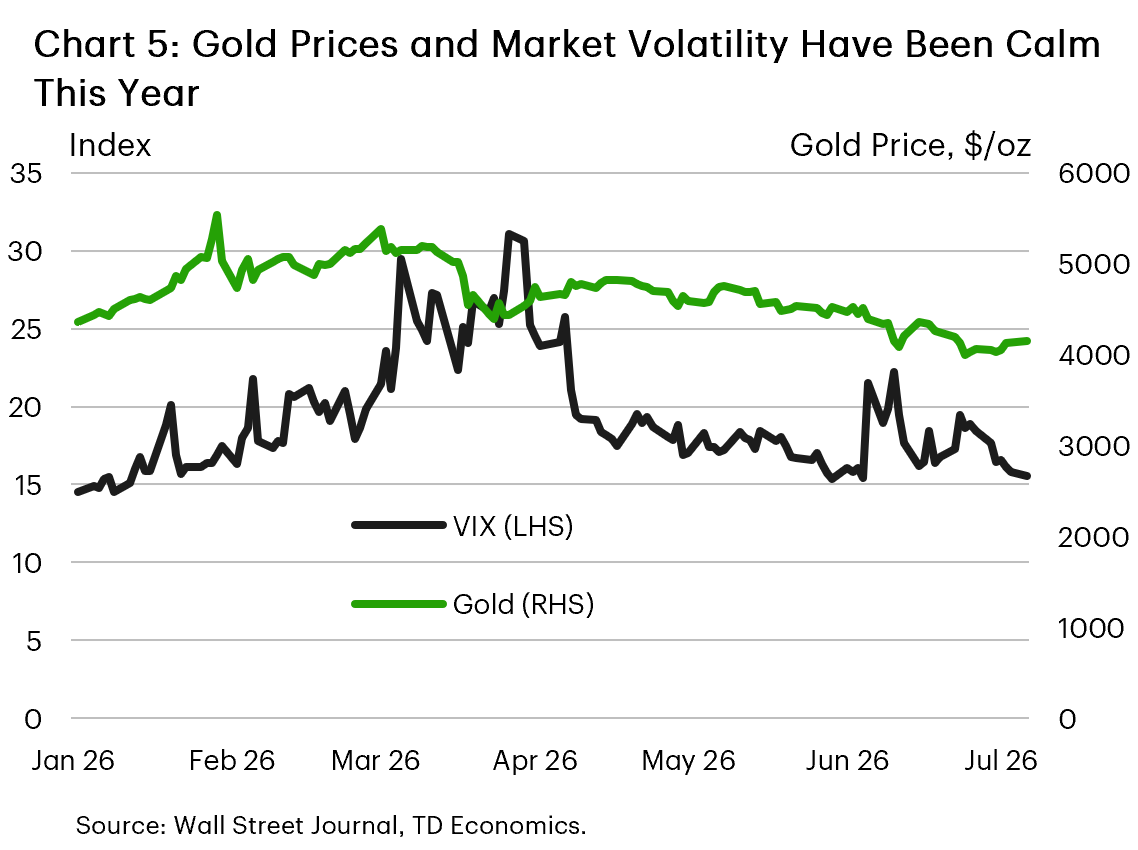

That distinction is important because the evidence for a classic flight-to-safety move is not especially convincing. If investors were simply rushing into safe havens, we would expect to see more persistent stress signals across markets. Instead, as shown in Chart 5, the VIX has retraced its earlier spike and gold prices have fallen over this period, weakening the case that CAD weakness is mainly being driven by generalized risk aversion. Other usual safe-haven currencies such as the euro, Swiss franc, and yen have also depreciated against the U.S. dollar this year. The cleaner interpretation is that investors have not abandoned risk altogether; they have become more selective, with U.S. assets and the dollar standing out as the preferred destination.

That leads naturally to the next driver: interest-rate differentials. The preference for USD assets and widening rate differentials are mutually reinforcing: stronger demand for U.S. exposure helps explain the direction of the move, while the growing U.S. rate advantage has made that preference more durable and intensified the pressure on currencies like the loonie.

Interest Rate Differentials

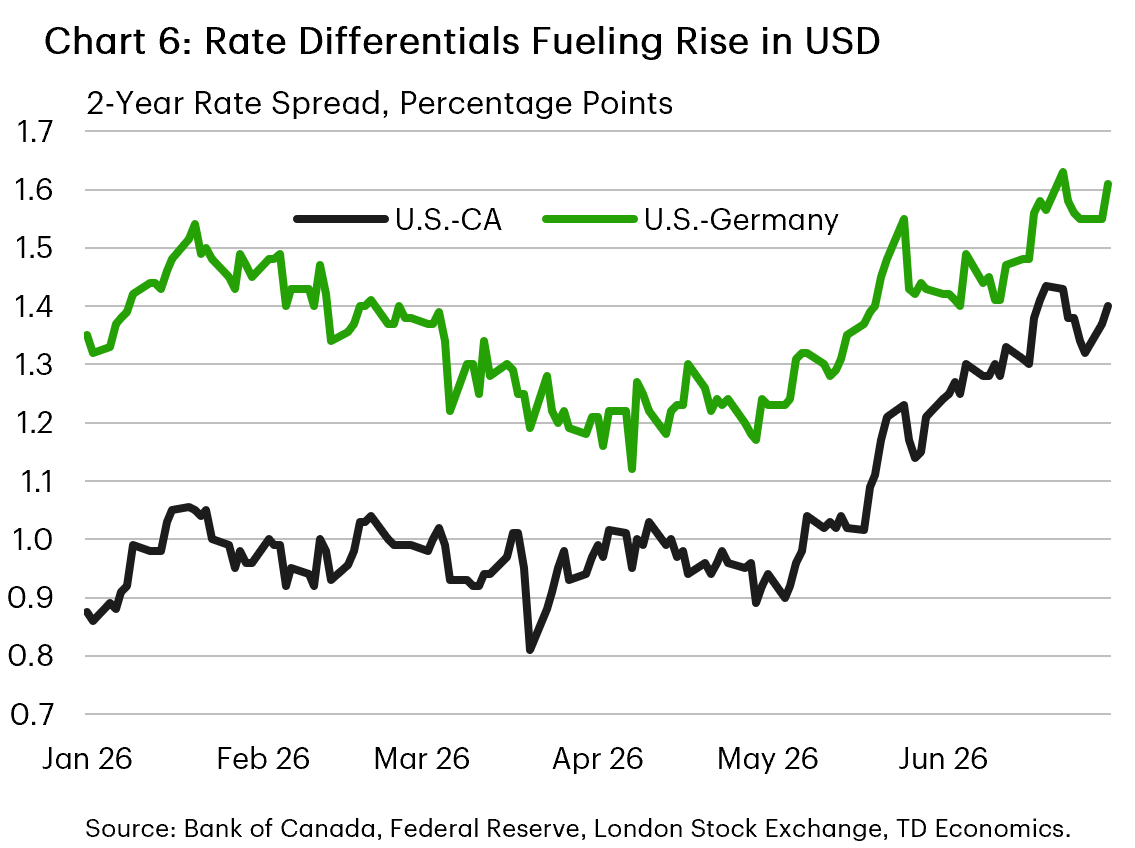

With the start of the war in the Middle East and the push higher on inflation, market expectations for Fed policy changed sharply, pricing in the possibility of Fed rate hikes. This was a sharp reversal from the prevailing sentiment prior to the conflict that the Fed was going to be the lone central bank reducing interest rates in 2026. This means the prior expectation for spreads on borrowing costs between the U.S. and other countries to narrow quickly reversed. The shift is most evident in short-term interest rate spreads between the U.S. and Canada and Germany (Chart 6).

The result of the policy divergence is that spreads vis-à-vis the U.S. on two-year government debt have widened by 25 basis points (bps) and 40 bps for Germany and Canada in the first half of 2026, respectively. The relatively smaller change in Germany is courtesy of a recent hike from the European Central Bank, whereas a dovish Bank of Canada has opted to stay on the sidelines. The widening premium to hold U.S. assets over other countries has helped to lift demand for the dollar, at the expense of other advanced economy currencies like the loonie and euro.

The Path Forward, the Productivity Wildcard and the Loonie

The outlook for the loonie now turns on whether those interest-rate gaps begin to narrow. Our baseline remains that U.S. inflation and growth will moderate in the coming months, allowing the Fed to gradually reduce the fed funds rate to 3.25% in 2027. That would take some pressure off the CAD by lowering the relative return on U.S. dollar assets.

The main risk is that the U.S. economy proves strong enough to keep those rate differentials wider for longer. There are two ways this could happen. The first is a more cyclical scenario, where the energy shock fades but U.S. demand remains firm enough to leave the economy in excess demand. In that case, the Fed would have less room to cut rates without risking renewed inflation pressure.

The second, more structural risk is that the productivity gap between the U.S. and its peers does not narrow back toward historical norms. This matters because stronger productivity growth can allow the U.S. economy to sustain faster growth and higher real rates without generating the same inflation pressure. If that advantage persists, the neutral rate in the U.S. could settle higher than in Canada and other advanced economies.

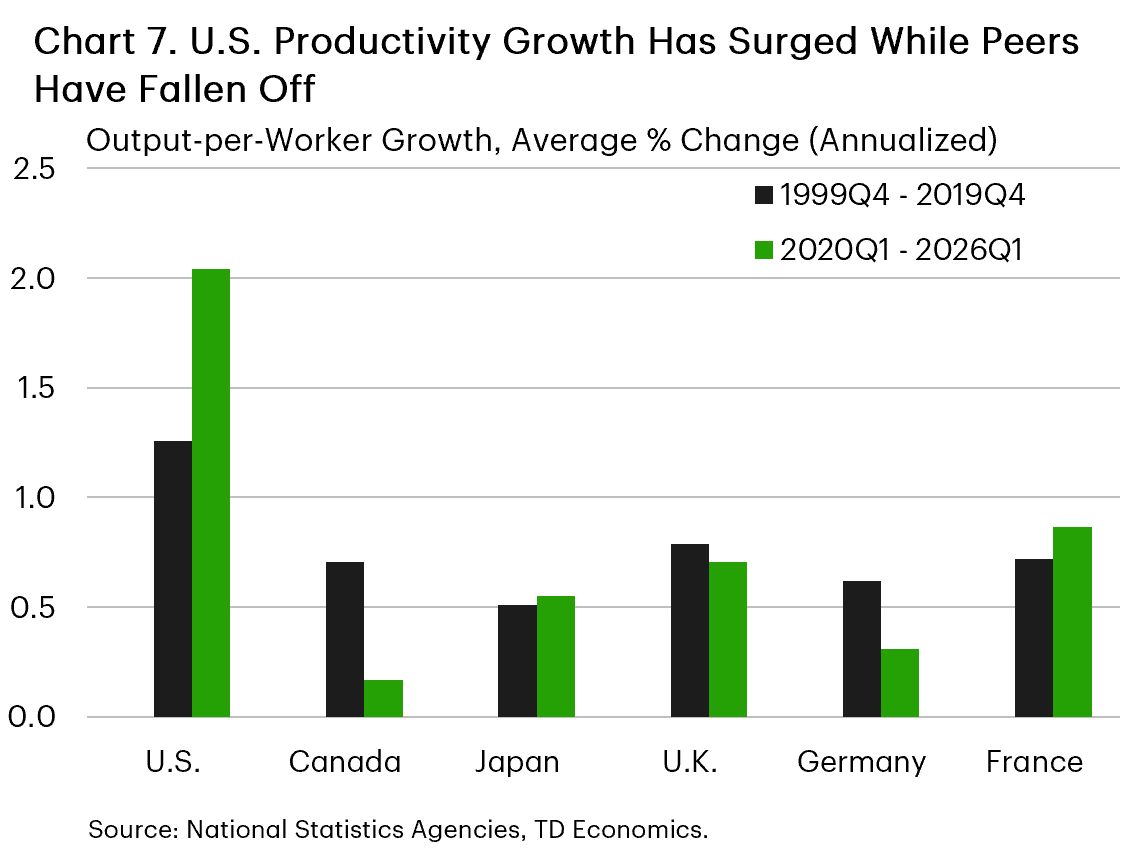

The recent data point in that direction. Since 2020Q1, U.S. output per worker has grown by 2.0% annualized, compared with 1.3% in the 20 years before the pandemic. Canada and other G7 economies have fallen further behind, held back by a mix of weaker capital deepening, softer business investment, and other structural headwinds (Chart 7). Stronger U.S. productivity growth helps explain how the economy has continued to outperform despite materially higher interest rates.

The implication for CAD is straightforward. If stronger U.S. productivity keeps the neutral rate higher, the Fed may not need to deliver as much rate relief as markets currently expect. U.S. short-term rates would remain elevated relative to Canada, preserving the yield advantage that has already helped pull capital toward U.S. assets.

That would leave the loonie vulnerable even if domestic conditions unfold broadly as expected. The baseline still points to some CAD recovery as U.S. rates eventually move lower, but a sustained U.S. productivity advantage would delay that adjustment by keeping rate and growth differentials tilted in favour of the dollar.

Under that scenario, the appreciation expected through the rest of 2026 and into 2027 would likely fail to materialize. Instead, CAD could remain stuck in the 71-72 U.S. cent range into mid-2027, as wider rate and growth differentials continue to make U.S. assets relatively more attractive.

Cliff Notes: Testing Conditions

Key insights from the week that was.

Amid a sparse local data calendar, a speech from RBA Assistant Governor (Economic) Sarah Hunter was scrutinised but had little market impact. The speech focused on supply-side shocks, such as the Middle East conflict, and the conundrum it presents for dual-mandated central banks like the RBA.

Assistant Governor Hunter reiterated the RBA’s perspective that these shocks are harder to ‘look through’ if economic capacity is already tight when the shock occurs, firms can readily pass through costs and/or inflation expectations de-anchor. While the latter is more of a risk than a reality at present, the RBA’s take on recent data suggests concern over capacity and pass-through is warranted, particularly in the construction sector. This is why the Monetary Policy Board telegraphed in its June policy decision that rate hikes remain on the table despite their decision to pause at that meeting following three successive hikes. The future scale and pace of tightening will depend on how the risks around each of these factors evolves in coming months. The upcoming Q2 CPI will prove critical in understanding the best course.

In New Zealand, the RBNZ delivered a 25bp increase at their July meeting, taking the cash rate (OCR) to 2.50%. A key argument for the hike was concern that financial conditions would have eased further if the OCR was left unchanged. The MPC seems to be comfortable with an end-2026 level for the OCR circa 2.75%-3.00% – broadly in line with the May forecasts. Our New Zealand economics team expects follow-up 25bp hikes in September and December and an unchanged sequence of 25bp increases through 2027. That means the peak OCR of 4.00% will now be reached in September 2027 instead of December.

Across in the US, the minutes of the June FOMC meeting showed participants felt a high degree of uncertainty over the outlook and wanted to consider a broad range of incoming information over successive months before determining if policy needs to be adjusted. Remaining on hold and removing previous forward guidance which favoured additional easing from the statement were consensus opinions.

On the balance of risks, the discussion amongst members points to a majority view that price risks had risen and labour market uncertainties receded since April. However, following June’s decision, energy prices jolted lower and nonfarm payrolls growth moderated again. The disconnect between payrolls and household survey employment also continues to grow, the latter in outright decline. Growth in consumer demand is also materially below trend and looks set to remain soft, limiting the ability of firms to pass through cost increases.

Still, price risks remain. Midweek, President Trump stated he believed the ceasefire with Iran was "over" but did not stop negotiators from continuing to engage. This followed strikes on around 80 Iranian military targets by the US in response to 3 ships being hit by projectiles in the Strait. Another 90 sites were hit in a second day of strikes, and Iran retaliated against US military assets in the region on both occasions.

President Trump has made clear he intends to order additional strikes in scale every time Iran threatens shipping on the Omani side of the Strait, which Iran has done to force shipping through the lanes it controls. A renewed blockade of Iranian cargo was also threatened by President Trump, with a view to increasing domestic pressure and restricting Iran’s ability to sell oil into global markets. However, President Trump also felt this escalation would prove short lived. Brent oil rose close to USD81 initially but has since eased back to around USD76. This compares to a low of USD71 early in the week.

Data received in the US and elsewhere in the northern hemisphere this week was secondary in significance and broadly in line with recent trends. Most notable was the ISM services index which reported a deterioration in new orders but also a pairing of input price pressures and improvement in employment, albeit for the latter only to near the 20-year average after three successive contractionary readings.

China's headline and core inflation rates meanwhile stabilised around 1.0%yr in June as producer price inflation edged up to 4.1%yr. Weak domestic demand continues to limit Chinese firms' ability to pass through higher production costs, which have primarily been driven by energy prices. Excess capacity and cautious consumers are likely to restrict consumer inflation in the absence of targeted (and effective) fiscal support.

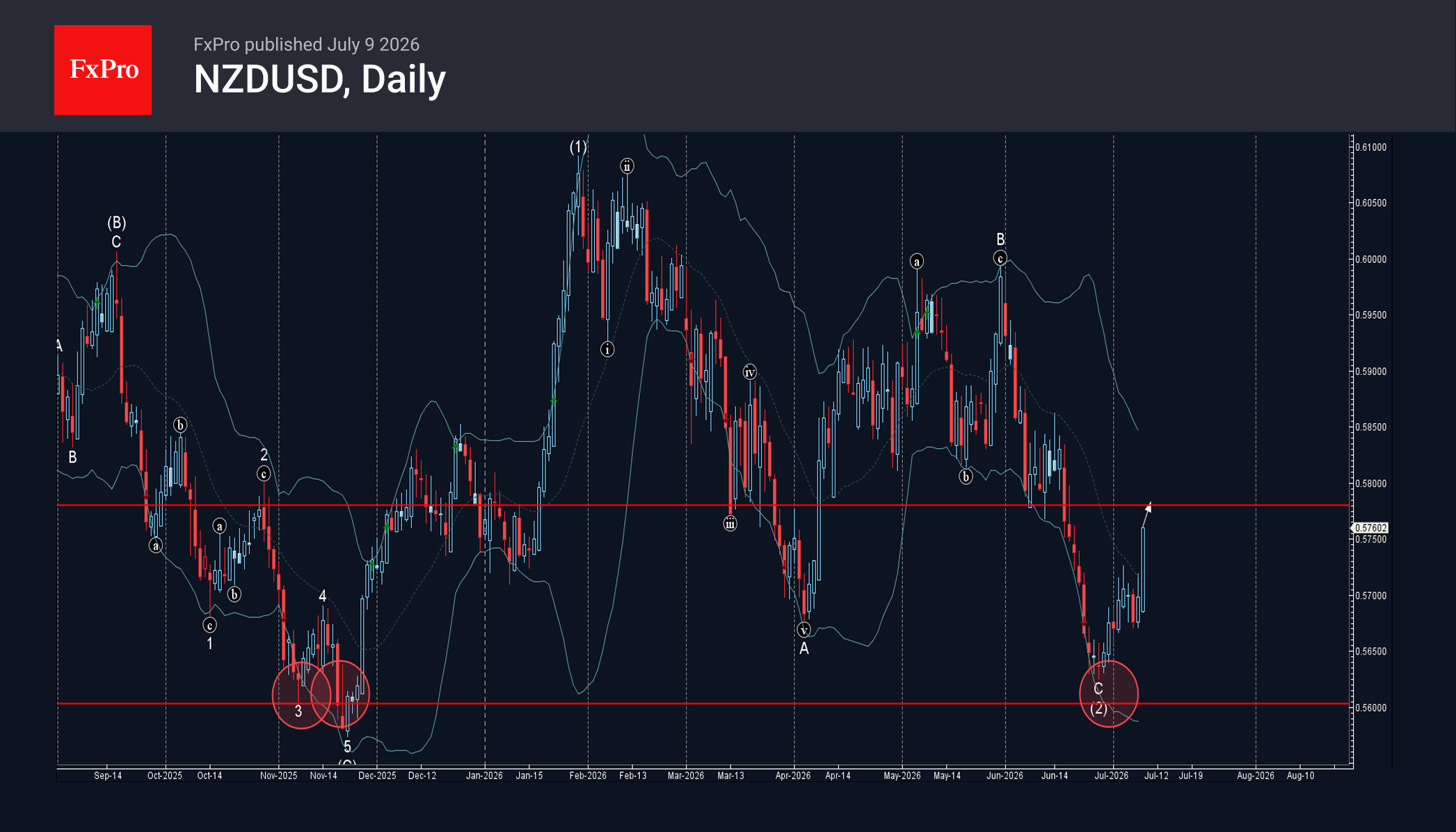

NZDUSD Wave Analysis

NZDUSD: ⬆️ Buy

– NZDUSD reversed from support zone

– Likely to rise to resistance level 0.5780

NZDUSD currency pair recently reversed up from the support zone between the long-term support level 0.5600 (which stopped the strong downtrend d in November) and the lower daily Bollinger Band.

The upward reversal from this support zone started the active medium-term impulse sequence (3).

NZDUSD currency pair can be expected to rise further toward the next resistance level 0.5780 (former support from the start of June).

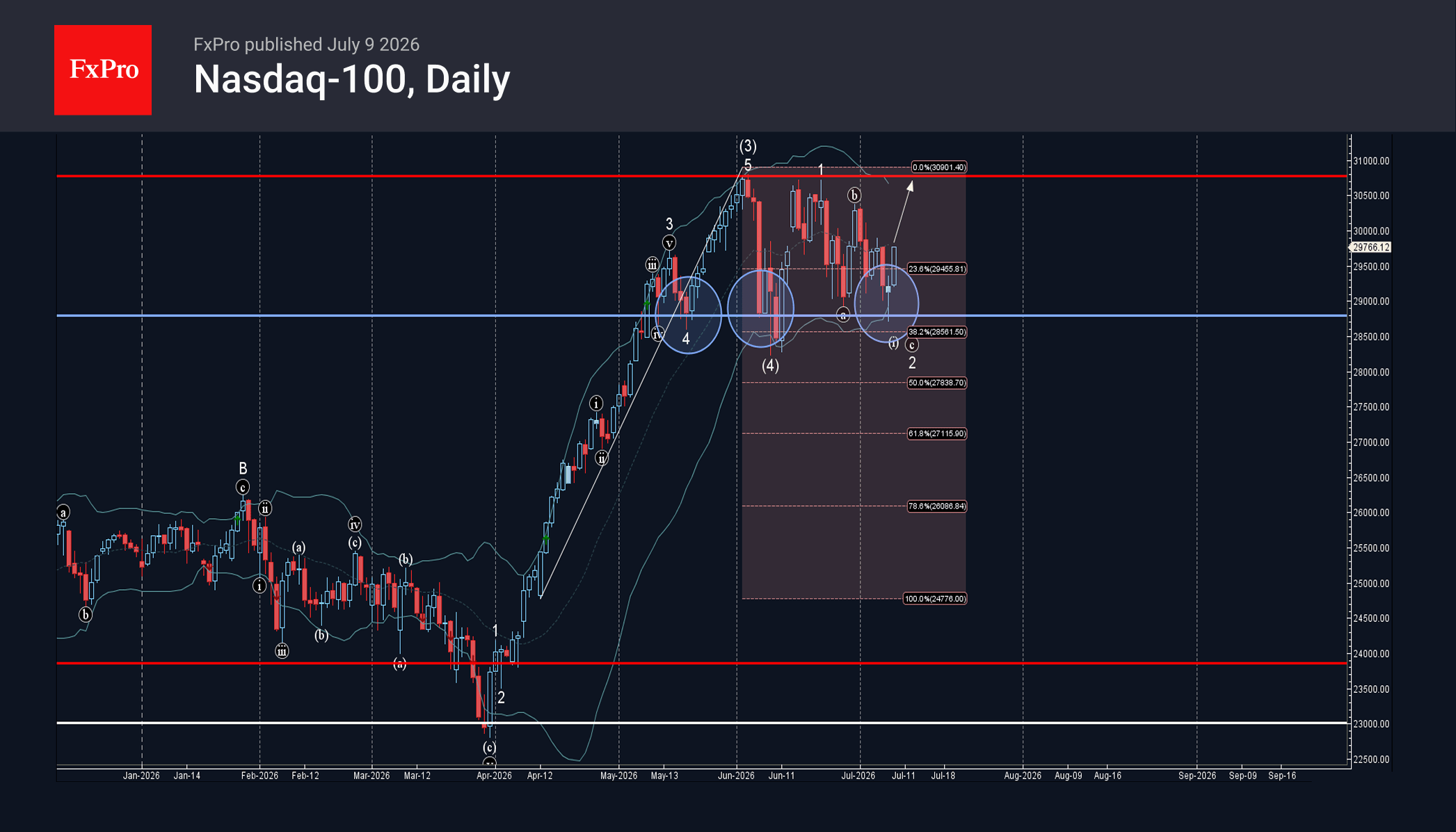

NASDAQ-100 Wave Analysis

Nasdaq-100: ⬆️ Buy

– Nasdaq-100 reversed from support zone

– Likely to rise to resistance level 30770.00

Nasdaq-100 recently reversed up from the support zone between the pivotal support level 28800.00 (which has been reversing the price from May), 38.2% Fibonacci correction of the upward impulse from April and the lower daily Bollinger Band.

The upward reversal from this support zone stopped the previous short-term ABC correction 2.

Given the clear daily uptrend, Nasdaq-100 can be expected to rise further toward the next resistance level 30770.00 (which stopped earlier waves (3) and 1).

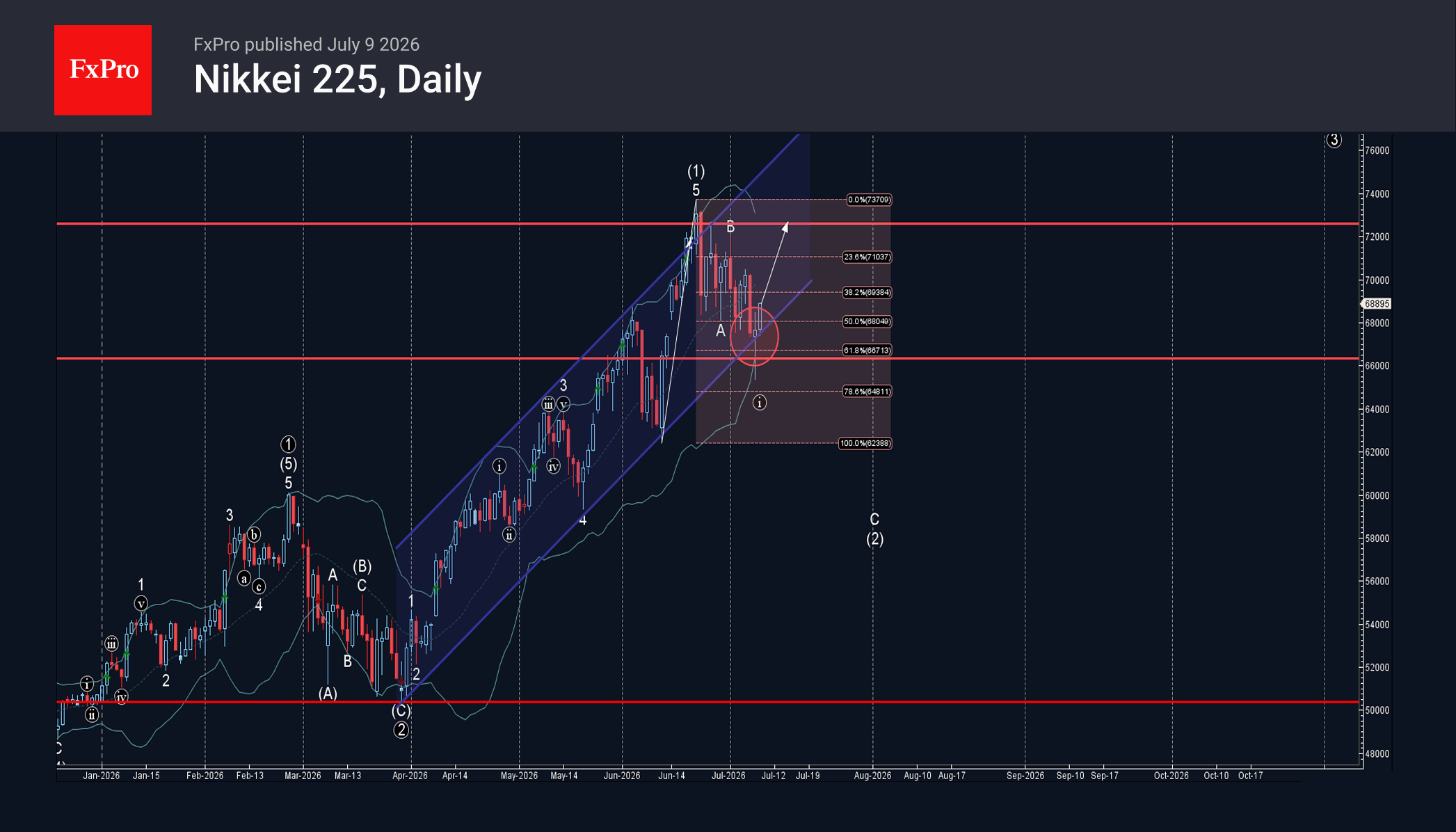

Nikkei 225 Index Wave Analysis

Nikkei 225: ⬆️ Buy

– Nikkei 225 reversed from support zone

– Likely to rise to resistance level 72575.00

Nikkei 225 index recently reversed up from the support zone between the support level 66000.00, lower daily Bollinger Band and the support trendline of the daily up channel from March.

The upward reversal from this support zone created the daily Japanese candlesticks reversal pattern Lon-Legged Doji.

Given the clear daily uptrend, Nikkei 225 index can be expected to rise further toward the next resistance level 72575.00 (which stopped earlier wave (1)).

Eco Data 7/10/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI M/M Jun | 0.40% | 0.30% | 0.90% | 1.10% |

| 23:50 | JPY | PPI Y/Y Jun | 7.10% | 6.80% | 6.30% | 6.60% |

| 06:00 | EUR | Germany CPI M/M Jun F | -0.30% | -0.30% | -0.30% | |

| 06:00 | EUR | Germany CPI Y/Y Jun F | 2.30% | 2.30% | 2.30% | |

| 12:30 | CAD | Net Change in Employment Jun | 18.2K | 10.0K | 87.8K | |

| 12:30 | CAD | Unemployment Rate Jun | 6.50% | 6.60% | 6.60% | |

| 12:30 | CAD | Building Permits M/M May | -1.70% | 1.00% | -7.60% | -6.60% |

| 23:50 | JPY |

| PPI M/M Jun | |

| Actual | 0.40% |

| Consensus | 0.30% |

| Previous | 0.90% |

| Revised | 1.10% |

| 23:50 | JPY |

| PPI Y/Y Jun | |

| Actual | 7.10% |

| Consensus | 6.80% |

| Previous | 6.30% |

| Revised | 6.60% |

| 06:00 | EUR |

| Germany CPI M/M Jun F | |

| Actual | -0.30% |

| Consensus | -0.30% |

| Previous | -0.30% |

| 06:00 | EUR |

| Germany CPI Y/Y Jun F | |

| Actual | 2.30% |

| Consensus | 2.30% |

| Previous | 2.30% |

| 12:30 | CAD |

| Net Change in Employment Jun | |

| Actual | 18.2K |

| Consensus | 10.0K |

| Previous | 87.8K |

| 12:30 | CAD |

| Unemployment Rate Jun | |

| Actual | 6.50% |

| Consensus | 6.60% |

| Previous | 6.60% |

| 12:30 | CAD |

| Building Permits M/M May | |

| Actual | -1.70% |

| Consensus | 1.00% |

| Previous | -7.60% |

| Revised | -6.60% |