Sample Category Title

Sunrise Market Commentary

Markets

Oil prices yesterday peaked at north of $80 in the wake of renewed attacks between the US and Iran. The recovery from +/- $70 levels seen earlier this month isn't markets betting on full-blown out-of-control war. But at the very least it serves as a reminder that geopolitical risks are far from gone. As things currently stand, the ceasefire is de facto dead. It prompted a hefty repositioning on European bond markets. In terms of the ECB scenarios, markets had perhaps banked too much on the benign one. Along with oil, gas prices have shifted from this milder scenario to the baseline which has two to three rate hikes embedded. German front-end yields rallied 12.4 bps and are nearing the 2026 highs again. Longer maturities added 6.6 bps (30-yr) to 10 bps (10-yr, two-month high). Revived inflationary spirits come at a time when public finances are potentially becoming a hot topic again with euro area member states beginning preparations for next year's budget. UK gilts underperformed. Yields pushed 10.2-15.5 bps higher in a bear flattening move. The 10-yr here is closing in on the 5% mark. US yields built on Tuesday's gains with a 1.7-4.4 bps increase. Short-term rates, e.g. the 2-yr, are testing the recent 1.5 year highs. FOMC meeting minutes of Warsh's first policy meeting in June revealed that a "few" officials saw a case for a June hike already before eventually backing the on-hold decision. The general view was that upside risks to price stability remained elevated while the downside ones for employment had "moderated a bit". It resulted ultimately in a hawkish tilt in the central bank's official stance. Dollar currency pairs yesterday saw little movement. Sterling on the other hand extended its recent bull run to EUR/GBP 0.8527. GBP outperformance started with the technical break below EUR/GBP 0.86 and, together with a political stability premium and beneficial interest rate differentials, clearly more than offsets the fragile risk environment (European stocks down 1.8% yesterday).

In absence of an inspiring economic calendar, it's the geopolitical narrative that sets the tone for trading once again. Oil prices aren't rising any further so far, despite a second day of attacks shortly after yesterday's US closing hours. That's keeping a lid on US yields and is setting the stage for a lower open of German ones too. President Trump has a habit to escalate and then de-escalate but we'd be cautious in assuming a quick return to business as usual, particularly in oil prices and core bonds.

News & Views

Chinese headline CPI at -0.3% m/m and 1% y/y (from -0.1% m/m and 1.2% y/y) in May showed some further easing of end-demand price pressures. Consumer goods prices inflation slowed from 1.6% to 1.1%. Services price inflation held at modest 0.8% y/y. Food prices still held in negative territory (-1.6% y/y from -1.7%) while non-food prices slowed from 1.9% to 1.5%. Core CPI (ex food & energy) also moderated to 1% from 1.1%. The overall picture of consumer price data at least suggests that there still is no meaningful demand-driven push in domestic prices. June producer prices, which were also published this morning, in this respect painted somewhat of a more nuanced picture. The headline PPI figure 'accelerated' from 3.9% Y/Y to 4.1%. However, considering a 0.3% m/m decline, this rise to an important part is due to a strong base effect from last year. In a yearly perspective, prices rise for mining (16.5%), raw materials (8.6%) and manufacturing (3%) rose substantially. Producer prices for consumer goods (-0.9% y/y) declined. It suggests a cost-driven push in producer price inflation, but not all of this probably can be passed on to consumers. The central bank probably will keep an ease policy stance as domestic consumer demand remains modest. USD/CNY this morning eased marginally to 6.796 after a (USD driven) modest rise of late.

In an appearance before parliament, Bank of Korea (BoK) Governor Shin Hyun Song warned that policy rate will have to be raised at an appropriate time. The comments come one week ahead of the July 16 BoK policy decision. The BoK governor in this respect argued that a tighter policy is needed as inflation remains above target in a context of improving economic growth and at the same time rising risks of financial stability. The BoK has its policy rate at 2.5% since cutting it to that level end May 2025. June CPI inflation in Korea last week was reported at 0.1% m/m and 3.2% y/y. Even as the won recently regained some ground (currently USD/KRW 1504.25, compared to levels near 1560 in June/early this month) the weak level of the currency still includes an inflationary risk.

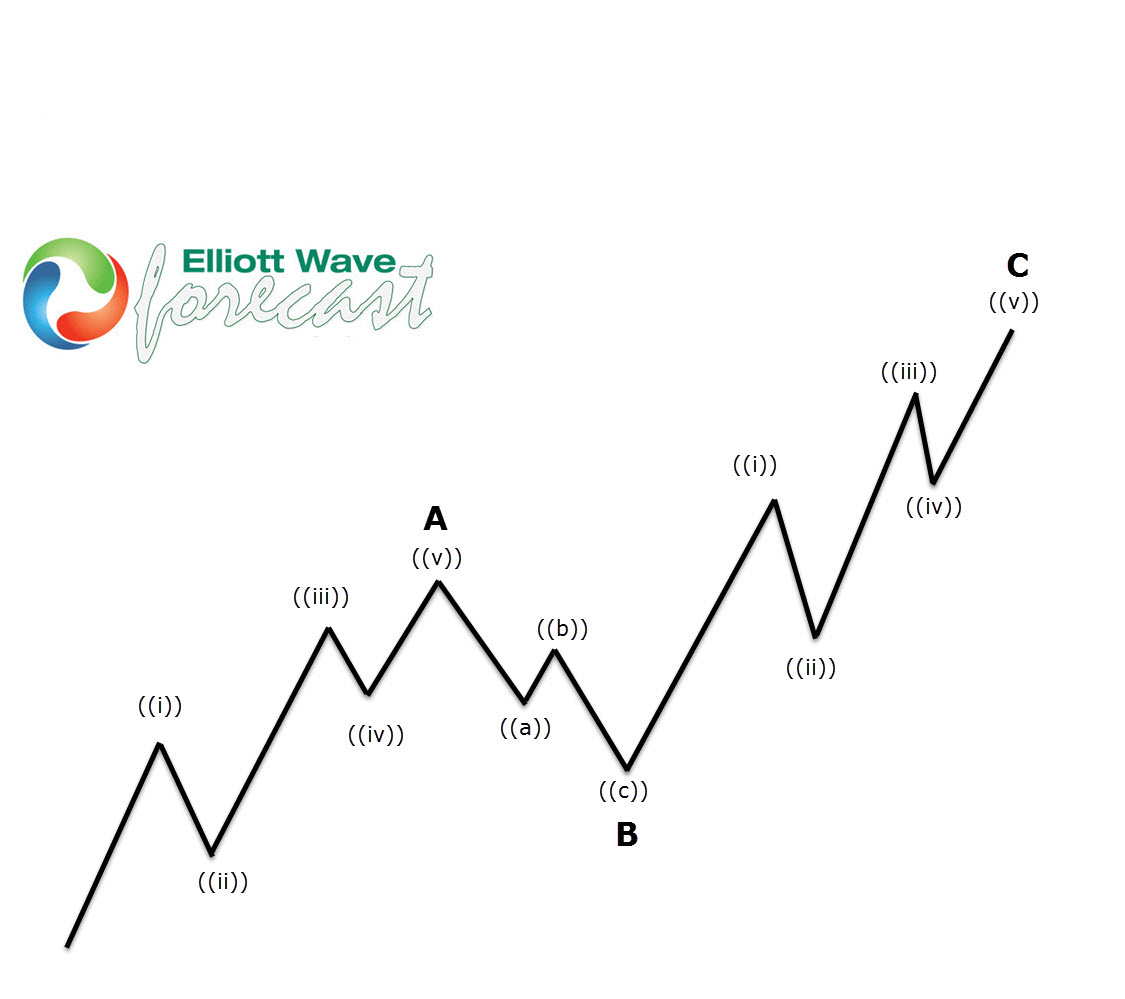

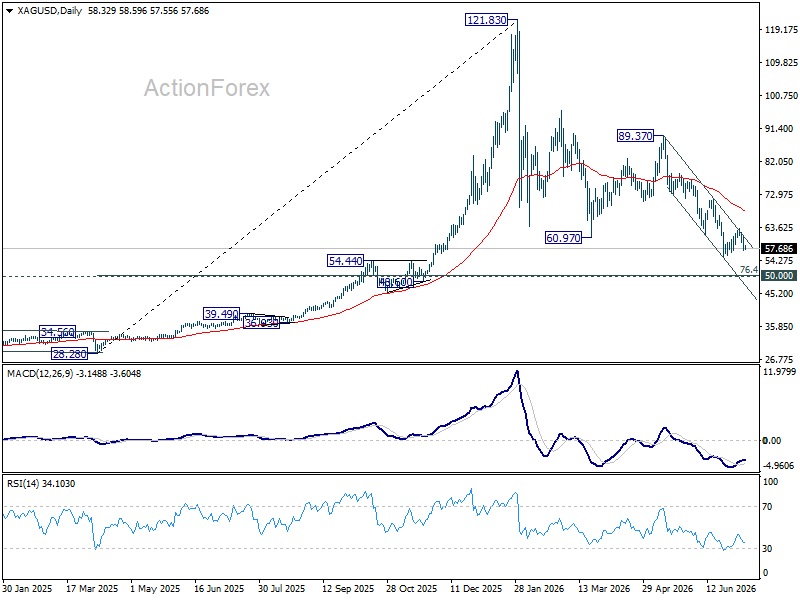

Silver XAGUSD Elliott Wave Calling for a Decline After Zig Zag Pattern

Hello fellow traders. In this technical article we’re going to take a quick look at the Elliott Wave charts of Silver Commodity XAGUSD . As our members know, both Silver and Gold are showing incomplete bearish sequences in the daily cycles. Recently SILVER made short term recovery that unfolded as Wave Zig Zag Pattern. In the further text we are going to explain the Elliott Wave Pattern and the Forecast.

Before we take a look at the real market example, let’s explain Elliott Wave Zigzag pattern.

Elliott Wave Zigzag is the most popular corrective pattern in Elliott Wave theory . It’s made of 3 swings which have 5-3-5 inner structure. Inner swings are labeled as A,B,C where A =5 waves, B=3 waves and C=5 waves. That means A and C can be either impulsive waves or diagonals. (Leading Diagonal in case of wave A or Ending in case of wave C) . Waves A and C must meet all conditions of being 5 wave structure, such as: having RSI divergency between wave subdivisions, ideal Fibonacci extensions and ideal retracements.

SILVER Elliott Wave 1 Hour Chart 07.03.2026

The current view suggests that SILVER is forming a recovery against the 71.598 peak. The price action is unfolding as an Elliott Wave Zig Zag pattern. We can count five waves within the first leg of the correction, labeled as ((a)).

The current structure suggests that another short-term high could still develop to complete the correction as a 5-3-5 pattern. The commodity can reach the 61.90–64.78 area, which represents a potential sellers’ zone, before the next leg lower begins. As usual, this zone was identified by measuring the equal legs of ((a)) against ((b)) using the Fibonacci extension tool. As long as the price remains below 64.78, the proposed bearish view remains valid.

Did you know ? 90% of traders fail because they don’t understand market patterns. Are you in the top 10%? Test yourself with this advanced Elliott Wave Test

Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

SILVER Elliott Wave 1 Hour Chart 07.09.2026

The commodity has made another leg higher and completed five waves within the ((c)) leg, as expected. The correction was completed within the proposed zone at 63.29, and we have seen a very decent reaction from this area. Now, we would like to see further downside extension and a break below the red A low to confirm the proposed bearish view.

Keep in mind that the market is dynamic, and the proposed view may have changed in the meantime. Our member chat rooms are open 24/7 and provide ongoing expert guidance on market trends and Elliott Wave analysis. Members are encouraged to ask questions about market structure and technical setups at any time

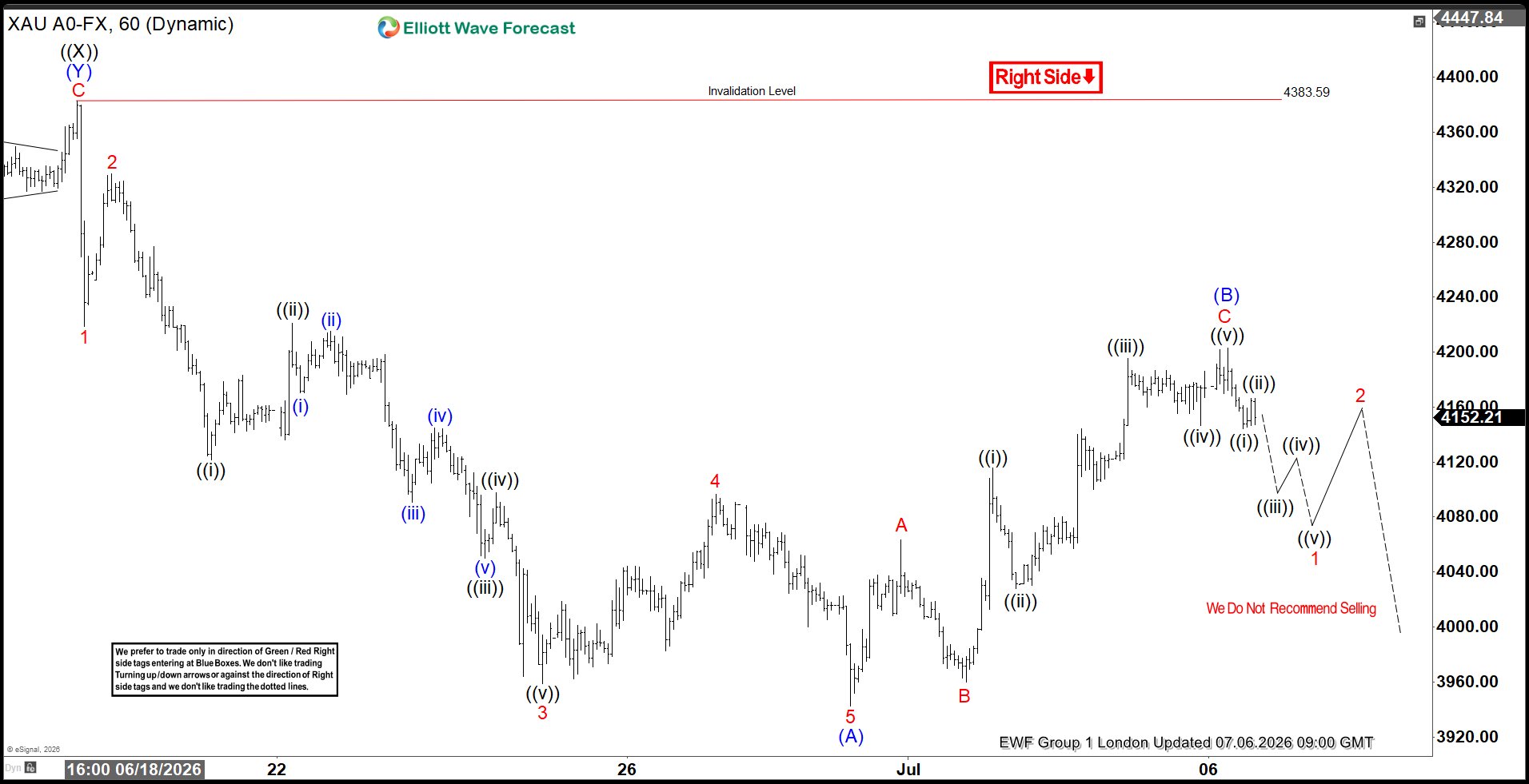

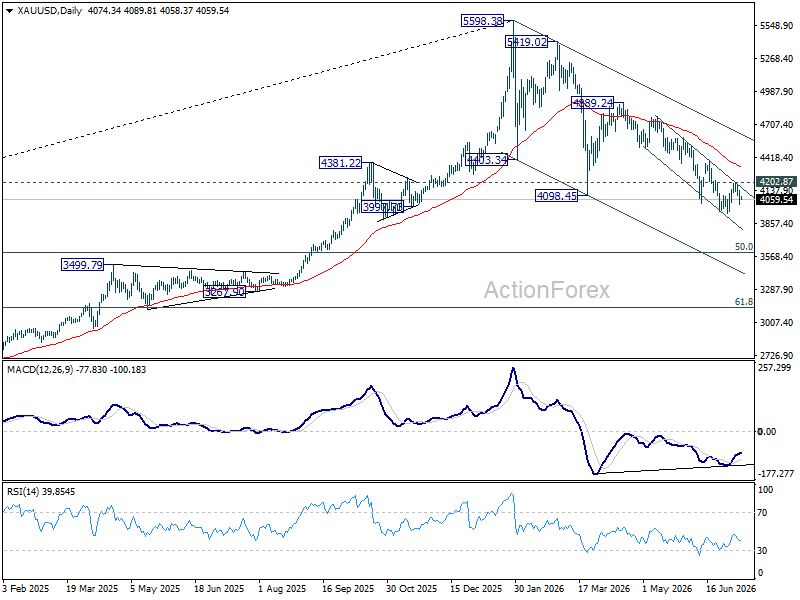

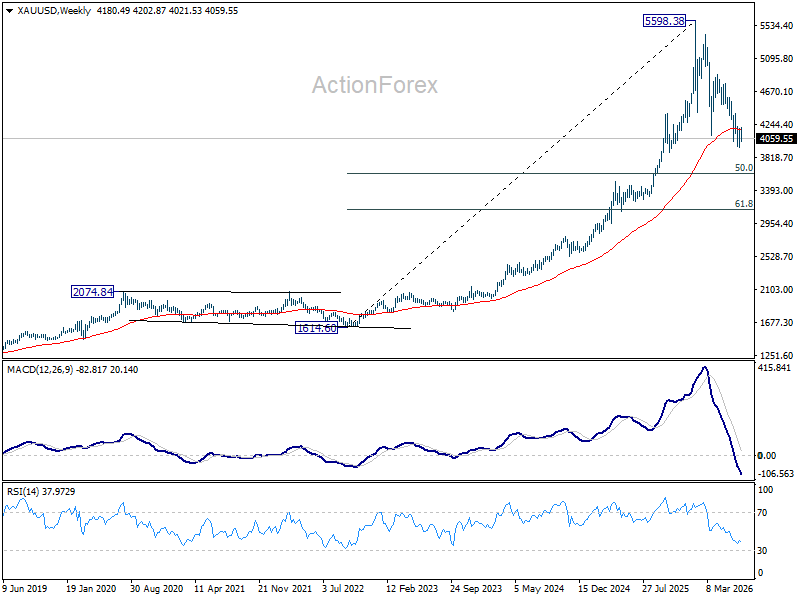

Gold XAUUSD Turns Lower After Completing Correction

Hello traders. In this technical article we’re going to look at the Elliott Wave charts of GOLD commodity published in members area of the website. As our members know, GOLD is shoing incomplete bearish sequences in the daily cycle and we have been calling for a decline in the commodity. As expected, the correction unfolded in a clear three-wave structure before sellers stepped back in. In this discussion, we will break down the Elliott Wave forecast.

GOLD Elliott Wave 1 Hour Chart 07.03.2026

The current view suggests that GOLD is forming a recovery against the 4385.35 peak. The price structure indicates that another short-term high could still develop to complete the correction before the next leg lower begins.

The 4385.35 level remains the key pivot, and as long as the price stays below this area, the proposed bearish view remains valid.

Did you know ? 90% of traders fail because they don’t understand market patterns. Are you in the top 10%? Test yourself with this advanced Elliott Wave Test

Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

GOLD Elliott Wave 1 Hour Chart 07.03.2026

The commodity has reached another short-term high and completed the wave (B) recovery at the 4201 peak. From there, the price has started to show signs of weakness. As long as the commodity remains below this key resistance level, we expect the downside pressure to persist and would like to see further weakness before a larger recovery can take place.

A break below the wave (B) blue low would provide additional confirmation that the bearish sequence is unfolding and that the next leg lower is underway.

Keep in mind that the market is dynamic, and the proposed view may have changed in the meantime. Our member chat rooms are open 24/7 and provide ongoing expert guidance on market trends and Elliott Wave analysis. Members are encouraged to ask questions about market structure and technical setups at any time

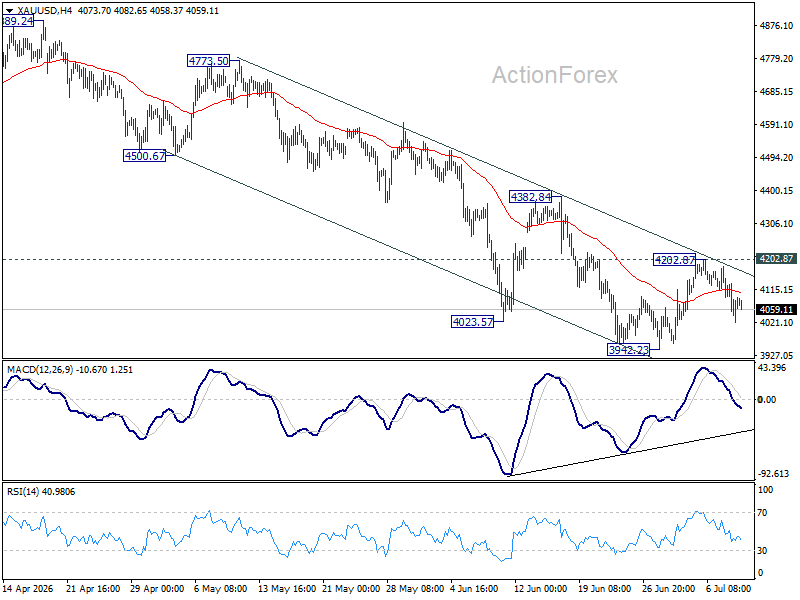

Gold and Silver Bears Need One More Trigger: Brent Above $80

Gold and silver have lost the momentum generated by their recent rebounds, but sellers have yet to secure the decisive breakdown they are looking for. Gold's recovery stalled at 4202.87, while silver turned lower after reaching 63.25. The next move now appears to hinge on a market far removed from precious metals themselves: Brent crude. If oil establishes itself above $80, the inflation narrative that has dominated markets for months could quickly return to centre stage.

Events in the Middle East are moving in that direction. Fresh US strikes against Iranian targets followed attacks on commercial shipping in and around the Strait of Hormuz, while President Donald Trump declared the ceasefire effectively "over" and questioned whether further negotiations were worthwhile. The rhetoric was accompanied by concrete policy action after Washington withdrew the waiver allowing Iran to continue exporting oil. Tehran responded by branding the strikes a treaty violation and signalling it was prepared to respond to further military action. Taken together, the latest developments look less like another temporary dispute within a ceasefire framework and more like the first meaningful signs that the agreement itself may be starting to unravel.

For metals markets, however, the crucial issue is not whether tensions remain elevated, but whether they push oil high enough to change the inflation outlook. A sustained break above Brent's $80 psychological level, reinforced by a move through 38.2% retracement of 98.99 to 70.14 at 81.16, would suggest investors are rebuilding a meaningful geopolitical premium into energy prices. That would increase the risk that the Federal Reserve will move closer towards rate hikes, strengthening the Dollar and maintaining upward pressure on real yields. In that environment, a decisive break below Gold's $4000 area and a renewed slide in Silver towards $50 would become considerably more likely.

The charts continue to favor that bearish outcome. Gold remains comfortably inside its descending channel, with 4,202.87 marking the key resistance that bulls must overcome. Until then, a break below 3,942.23 remains the preferred scenario. Firm break of 3,942.23 will resume the larger down trend. Next target will be 50% retracement of 1,614.60 (2022 low) to 5,598.38 (2026 high) at 3,606.49.

Silver is following the same script. The failure at 63.25 reinforces the integrity of the near-term falling channel, while 55.59 remains the key support to watch. A decisive break there would confirm the broader downtrend has resumed and expose the next major downside objective 76.4% retracement of 28.28 to 121.83 at 50.26.

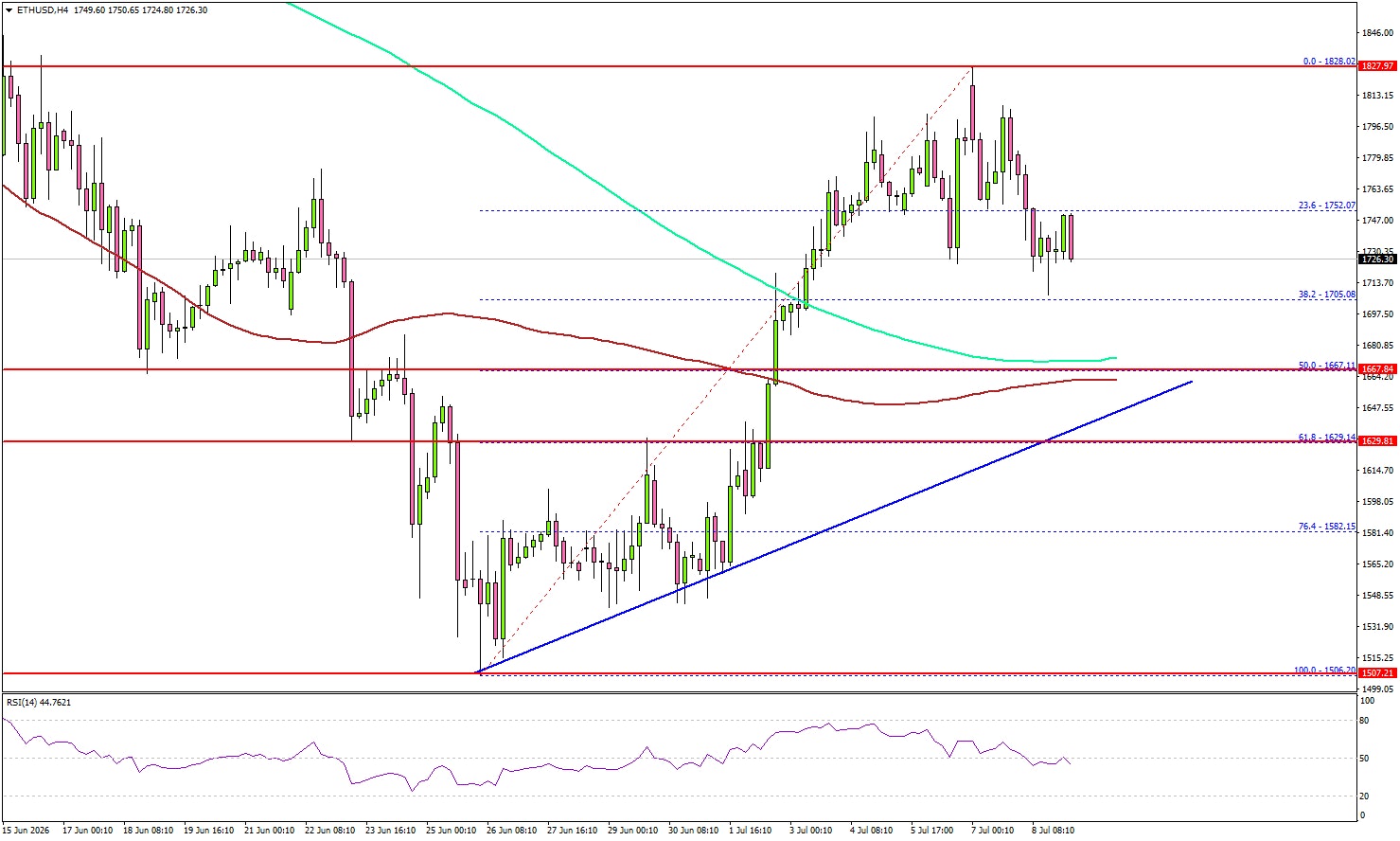

Ethereum Recovery Faces a Reality Check with Support Waiting Below

Key Highlights

- Ethereum failed to clear the $1,825 resistance and trimmed gains.

- A bullish trend line is forming with support at $1,665 on the 4-hour chart of ETH/USD.

- Bitcoin price also struggled above $64,000 and dipped again.

- XRP seems to be facing hurdles near $1.1650 and $1.180.

Ethereum Technical Analysis

Ethereum started a recovery wave above $1,650 against the US Dollar. ETH/USD climbed above $1,750 before the bears appeared.

Looking at the 4-hour chart, the price failed to stay above $1,800 but settled well above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). A high was formed at $1,828 before the price dipped.

There was a move below the 23.6% Fib retracement level of the recovery wave from the $1,506 swing low to the $1,828 high. On the downside, the bulls might be active near $1,650 and $1,620.

There is also a bullish trend line forming with support at $1,665 and the 50% Fib retracement. Any more losses might call for a move toward $1,550. The main support could be $1,500.

On the upside, the bears might remain active near $1,800. The first key resistance could be near the $1,825 level. The main hurdle for bulls sits near $1,880. A close above the $1,880 level could open doors for a larger upward movement. In the stated case, ETH could rise toward $2,000.

Looking at Bitcoin, the price failed to continue higher, trimmed gains, and is now struggling below the $63,500 support zone.

Economic Releases

- US Initial Jobless Claims - Forecast 218K, versus 215K previous.

- US Existing Home Sales for June 2026 (MoM) - Forecast +0.1%, versus +3.2% previous.

- Fed's Williams speech.

China Inflation Cools Further as Consumer Prices Ease, Producer Inflation Hits Three-Year High

China's consumer inflation eased further in June, highlighting subdued domestic price pressures even as producer inflation climbed to its highest level in nearly three years. Consumer prices fell -0.3% mom, steeper than the expected -0.2% decline, while annual CPI slowed from 1.2% yoy to 1.0%, undershooting expectations of 1.1%. Core CPI also edged down from 1.1% to 1.0%, its slowest pace since January, suggesting underlying inflation remained contained despite steady economic activity.

The moderation in consumer inflation reflected softer price increases for industrial consumer goods, particularly gold jewellery and gasoline, according to the National Bureau of Statistics. The decline in energy-related prices followed the sharp fall in global crude oil prices after the US and Iran reached a ceasefire in June, helping ease imported inflation pressures. The data indicate that weaker energy costs are beginning to offset broader price pressures facing households.

In contrast, producer prices continued to strengthen. PPI accelerated from 3.9% to 4.1% yoy, matching market expectations and marking a fourth consecutive monthly increase, with annual producer inflation reaching its highest level since July 2022. The NBS attributed the gains to higher prices in coal mining, electrical machinery, electronics and ferrous metals. However, producer prices fell -0.3% month-on-month after June's collapse in global oil prices, suggesting upstream inflation may moderate further in coming months if energy prices remain contained.

| Indicator | June | May | Expectation |

|---|---|---|---|

| CPI (MoM) | -0.3% | -0.1% | -0.2% |

| CPI (YoY) | 1.0% | 1.2% | 1.1% |

| Core CPI (YoY) | 1.0% | 1.1% | — |

| PPI (MoM) | -0.3% | — | — |

| PPI (YoY) | 4.1% | 3.9% | 4.1% |

New Zealand Manufacturing PMI Surges to Strongest Since 2021 as Orders Soar

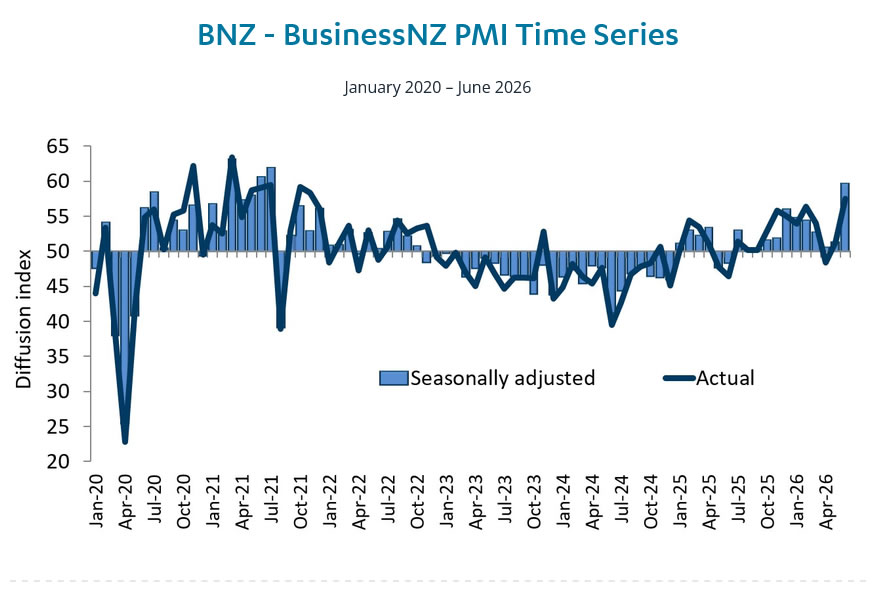

New Zealand's manufacturing sector posted a powerful recovery in June, with the BusinessNZ Performance of Manufacturing Index (PMI) jumping from 51.3 to 59.7, well above its long-run average of 52.5. The reading marked the strongest expansion since July 2021, highlighting a broad improvement in activity after the sector spent much of the past two years struggling with weak demand and heightened uncertainty.

The rebound was broad-based, with every major sub-index firmly in expansion territory. New orders led the way, surging from 53.2 to 64.1, pointing to a strengthening pipeline of future work. Production also accelerated sharply, rising from 50.6 to 59.4, while employment climbed from 51.4 to 55.8, suggesting manufacturers have become more confident about hiring. Deliveries improved from 52.9 to 57.3 and finished stocks increased from 54.3 to 56.9, reinforcing the view that the recovery is gaining traction across the supply chain rather than being driven by a single component.

BusinessNZ Director of Advocacy Catherine Beard described the result as "hugely encouraging," noting it was accompanied by the first clear shift toward positive business sentiment in recent months. While respondents continued to cite Middle East tensions, elevated fuel prices and cost-of-living pressures as challenges, these concerns were outweighed by reports of stronger sales, fuller order books and renewed confidence. BNZ Head of Research Stephen Toplis said he was "staggered" by the strength of the rebound, noting that outside of the post-pandemic recovery in 2021, the latest reading was the strongest since May 2017. The sharp improvement suggests New Zealand's manufacturing sector has entered the second half of the year with considerably stronger momentum than many had anticipated.

| Indicator | June | May | Prior/Notes |

|---|---|---|---|

| PMI | 59.7 | 51.3 | Highest since July 2021; long-run average 52.5 |

| Production | 59.4 | 50.6 | Strong acceleration |

| New Orders | 64.1 | 53.2 | Strongest sub-index |

| Employment | 55.8 | 51.4 | Hiring strengthened |

| Deliveries | 57.3 | 52.9 | Faster supplier deliveries |

| Finished Stocks | 56.9 | 54.3 | Continued expansion |

FOMC Minutes Show Some Officials Were Ready to Hike in June

The minutes of the Federal Reserve's June 16-17 meeting revealed that the unanimous decision to leave interest rates unchanged masked a noticeably more hawkish debate beneath the surface. While all policymakers ultimately supported keeping the federal funds target range at 3.50%-3.75%, "a few participants commented that... there was a case for raising the target range" at that meeting before deciding to wait for additional evidence. The discussion took place nearly two weeks before June's weaker-than-expected payroll report, meaning it reflects the Committee's thinking before labor market concerns re-emerged.

Inflation, rather than employment, dominated the discussion. Participants agreed that inflation "had increased further and remained well above the Committee's 2 percent longer-run objective," with risks "still tilted to the upside." Policymakers cited tariffs, lingering supply disruptions linked to the Strait of Hormuz, and robust AI-related investment as key drivers of persistent price pressures. Several participants warned that strong demand for AI infrastructure would continue supporting prices for technology products and electricity, while most judged that economic growth exceeding potential output could keep inflation elevated. By contrast, many participants said the labor market "was not currently a source of inflationary pressures," with wage growth broadly consistent with inflation eventually returning to target.

The minutes also offered the first clear confirmation that Chair Kevin Warsh's communication strategy enjoys broad Committee support. A majority of participants favored shortening the post-meeting statement, while most agreed that language implying an easing bias should be removed. Those discussions reinforce Warsh's preference for reducing reliance on forward guidance and allowing incoming data to shape policy decisions. The minutes also highlighted a genuine divide over the appropriate policy path. While many participants judged rates should end the year within or slightly below the current range, many others believed the appropriate policy rate would be above today's level by year-end, underscoring that another rate hike remained a live possibility before softer June payroll data shifted market expectations.

(FED) Minutes of the Federal Open Market Committee

June 16–17, 2026

A joint meeting of the Federal Open Market Committee and the Board of Governors of the Federal Reserve System was held in the offices of the Board of Governors on Tuesday, June 16, 2026, at 10:00 a.m. and continued on Wednesday, June 17, 2026, at 9:00 a.m.1

Developments in Financial Markets and Open Market Operations

The manager turned first to an overview of market developments during the intermeeting period. Asset prices were affected by a number of factors, including developments related to the conflict in the Middle East, continued solid real economic data, higher inflation data, and ongoing investment in artificial intelligence (AI). Optimism around a near-term resolution of the conflict in the Middle East and the announcement of a memorandum of understanding between the U.S. and Iran pushed the oil futures curve and near-term inflation compensation materially lower relative to levels from the time of the April FOMC meeting. Expected policy rates, Treasury yields, the U.S. dollar, and domestic equity prices all rose.

Regarding monetary policy expectations, the manager observed that market participants and respondents to the Open Market Desk Survey of Market Expectations (Desk survey) generally expected no change in the target range of the federal funds rate at the June FOMC meeting. Market- and survey-based measures of expected policy rates moved higher over the intermeeting period. In the Desk survey, the median of the modal paths of the federal funds rate implied no changes in the target range through the beginning of 2027 and one rate cut in the second quarter of next year. Market pricing suggested that one rate hike was priced for mid-2027, but the manager noted that these measures were likely boosted, in part, by term premiums.

The manager then discussed inflation expectations. He noted that optimism around the Iran conflict pushed market-based measures of expected inflation significantly lower over the period, leaving near-term inflation expectations only moderately higher than they were before the onset of the conflict. Longer-term inflation expectations remained well anchored near the Committee's 2 percent longer-run inflation objective.

Turning to Treasury markets, the manager noted that the nominal 10-year Treasury yield had increased around 20 basis points since the April FOMC meeting and about 50 basis points since the start of the conflict in the Middle East. The manager commented that the ownership composition of Treasury securities has shifted somewhat over the past several years from relatively price-insensitive official-sector holders to more price-sensitive private investors, which could have implications for the term premium component of yields.

The manager next described developments in equity markets. The S&P 500 index increased by nearly 6 percent over the intermeeting period, led by the technology sector. Higher earnings expectations accounted for a large portion of the overall increase, particularly in the technology sector. Initial public offering activity in the U.S. appeared set to accelerate this year, with the proceeds expected to help fund ongoing investments in AI infrastructure.

In discussing credit markets, the manager noted that private credit markets continued to receive attention over the intermeeting period. Gross inflows to business development companies slowed notably in the second quarter, and available data suggested that net inflows were likely to become more negative amid an acceleration in investor redemption requests.

With regard to international developments, the manager noted that over the intermeeting period the increase in the two-year Treasury yield was larger than increases in sovereign yields of similar maturity in other advanced economies, as market-based expectations for the path of the domestic policy rate moved upward. The increases in two-year sovereign yields since the start of the conflict in the Middle East were now similar across many advanced foreign economies (AFEs). Consistent with the widening interest rate gap over the intermeeting period, the foreign exchange value of the U.S. dollar had modestly appreciated.

The manager observed that money market conditions were generally stable, although conditions softened notably early in the intermeeting period before they partially rebounded. In particular, repurchase agreement (repo) rates dropped to 15 basis points below the interest rate on reserve balances in mid-May. Consistent with that drop, the effective federal funds rate declined 2 basis points, the first such change since November. There was modest take-up of the Federal Reserve's overnight reverse repurchase agreement operations on days when repo rates were especially low, confirming that those operations were effective in firming the floor under money market rates. Regarding the decline in repo rates early in the period, the manager noted several likely driving factors: Reserves increased following the seasonal low around the April tax date as the Treasury General Account dropped, reserve management purchases added reserves and reduced the bill supply available to the public, U.S. global systemically important banks likely increased intermediation capacity in response to regulatory changes earlier in the year, the demand for repo financing on the part of levered investors declined, and seasonal increases in cash investments of government-sponsored enterprises coincided with the lowest rates seen over the intermeeting period. The manager noted that, these developments notwithstanding, the level of reserves in the system appeared to remain within a range consistent with an ample supply.

By unanimous vote, the Committee ratified the Desk's domestic transactions over the intermeeting period. There were no intervention operations in foreign currencies for the System's account during the intermeeting period.

Staff Review of the Economic Situation

The information available at the time of the meeting indicated that inflation remained elevated and had moved higher, partly reflecting the effects of energy and other supply shocks. Labor market conditions remained stable, and real gross domestic product (GDP) continued to expand at a solid pace.

Total consumer price inflation—as measured by the 12-month change in the price index for personal consumption expenditures (PCE)—was 3.8 percent in April. Core PCE price inflation, which excludes changes in consumer energy prices and many consumer food prices, was 3.3 percent. Both total and core inflation were higher than their levels a year earlier, a development that the staff attributed to a variety of factors, including the pass-through of past tariff increases, higher energy and input costs stemming from the conflict in the Middle East, and the surge in demand related to the AI buildout. Core goods price inflation had risen relative to a year earlier, which the staff judged as largely reflecting the effects of tariffs and AI-related price pressures. Core services price inflation had been relatively stable over that period, as a gradual decline in the housing services component was about offset by a modest step-up in the core nonhousing services component. Based on data from the consumer and producer price indexes, the staff estimated that total PCE price inflation rose to 4.1 percent in May, boosted by an increase in consumer energy prices, and core PCE price inflation was estimated to be 3.4 percent.

The unemployment rate was 4.3 percent in May and had changed little, on balance, since the middle of the previous year. Nonfarm payroll employment rose at a solid pace in the three months through May. The 12-month change in the employment cost index for private-sector workers was 3.4 percent through March, the same as its year-earlier pace. Average hourly earnings increased 3.4 percent over the 12 months ending in May, 0.5 percentage point lower than a year earlier.

Available indicators suggested that real GDP growth continued at a solid pace in the second quarter. Real private domestic final purchases—which comprises PCE and private fixed investment and which often provides a better signal of underlying economic momentum than does real GDP—appeared to have picked up in the second quarter and was rising faster than GDP. Real consumer spending had been solid, and the AI buildout continued to boost real investment spending on data centers, high-tech equipment, and software. Data for April showed continued strength in both imports and exports of high-tech goods and a jump in energy exports.

Economic growth abroad stepped down in the first quarter of 2026, with weakness in Canada, the euro area, and Mexico. By contrast, output growth in several high-income Asian economies remained robust, as their exports of high-tech goods continued to surge, driven by the AI buildout. Recent indicators suggested that the conflict in the Middle East was weighing on foreign economic activity because of higher energy costs and weaker consumer and business confidence, particularly in lower-income Asian economies and in Europe.

Foreign headline inflation had increased significantly since the start of the conflict in the Middle East, with a sharp rise in retail energy and producer prices across Europe and much of Asia. Some central banks, including the European Central Bank, responded to higher inflation by raising their policy rates. More broadly, most foreign central banks emphasized the risks of higher inflation leading to second-round effects and the need to mitigate these risks, despite prospects of weaker output growth, and signaled either policy rate hikes or a slower pace of easing going forward.

Staff Review of the Financial Situation

Over the intermeeting period, the market-implied expected path of the federal funds rate and nominal Treasury yields moved higher as stronger-than-expected economic data reinforced expectations that economic activity would remain resilient. The market-implied path of the policy rate over the latter half of this year increased during the intermeeting period, and related measures of uncertainty about the path of policy rose, partly reflecting a higher term premium. The rise in nominal Treasury yields, most notable at shorter maturities, reflected higher real rates. Short-term market-based measures of inflation compensation declined significantly but stayed at a slightly elevated level. Market-based measures of longer-term inflation compensation and survey-based measures of inflation expectations remained well anchored.

Broad equity price indexes increased notably, boosted by robust corporate earnings and further investor optimism surrounding AI implications for corporate profitability, despite the headwind of higher yields. Consistent with improved risk sentiment, the VIX—a forward-looking measure of near-term equity market volatility—declined slightly to below the median of its historical distribution, while corporate bond spreads narrowed somewhat.

Foreign financial market movements were largely driven by news of the increased prospects for a reopening of the Strait of Hormuz and then the announcement near the end of the intermeeting period that an agreement had been reached. Market-based policy expectations and near-term inflation compensation measures declined in most major AFEs. Nonetheless, market pricing still indicated at least one additional policy rate hike both in the euro area and in the U.K. over the remainder of this year. The broad dollar index rose as differentials between short-term interest rates in the U.S. and the AFEs widened. Strong corporate earnings and continued investor optimism related to AI contributed to increases in foreign equity prices.

Conditions in U.S. short-term funding markets remained stable. Aggregate bank reserves moved up following the previous period's tax receipt–driven decline. Money market rates ended the period slightly lower, on net, amid continued low bill supply.

Financing conditions in domestic credit markets remained generally accommodative for larger businesses and municipalities but somewhat restrictive for many small businesses and households. Borrowing costs continued to be elevated, and interest rates increased somewhat over the intermeeting period in some sectors, primarily reflecting increases in Treasury yields.

Credit continued to be generally available to most businesses, households, and municipalities. Bank lending continued to expand, and issuance of corporate bonds remained solid, partly driven by the financing needs of AI-related investments. Issuance in the leveraged loan market had picked up to a robust pace, while signals pointed to a continued slowdown in the private credit market. By contrast, credit conditions remained somewhat tight for small businesses and household borrowers with lower credit scores. Issuance of municipal bonds remained strong.

Staff Economic Outlook

The staff's inflation forecast for this year and the next was higher than the one prepared for the April meeting, reflecting incoming data, higher energy prices and other input costs due to the conflict in the Middle East, and the effects of the AI buildout on consumer prices. Total inflation was projected to slow over the second half of this year from its recent pace, as retail gasoline prices were expected to decline, although core inflation was forecast to change little over the rest of the year. Inflation was projected to step down next year, as some of the factors lifting inflation this year—such as tariffs—were expected to wane, and then move down further to about 2 percent in 2028.

The staff's outlook for real GDP growth was a bit lower than the one prepared for the previous meeting, mostly reflecting incoming data. Real GDP was forecast to expand at about the same pace as potential this year and to slightly outpace potential over the next two years, buttressed by persistently strong productivity growth, continued gains in AI-related capital spending, and supportive financial conditions. The unemployment rate was expected to remain close to the staff's estimate of its longer-run rate this year and next before edging slightly below it in 2028.

The staff continued to view the uncertainty around their forecast as elevated, importantly because of uncertainty about the conflict in the Middle East and about the potential economic effects of AI investment and adoption. On balance, risks to the forecasts for employment and real GDP growth were seen as tilted somewhat to the downside. Risks to the inflation projection were seen as more skewed to the upside. With inflation having run significantly above 2 percent over the past five years and in light of some emergent price pressures that appeared unrelated to tariffs or energy prices, the staff continued to view the possibility that inflation would be more persistent than projected as a salient risk.

Participants' Views on Current Conditions and the Economic Outlook

In conjunction with this FOMC meeting, almost all participants submitted their projections of the most likely outcomes for real GDP growth, the unemployment rate, and inflation for each year from 2026 through 2028 and over the longer run. The projections were based on participants' individual assessments of appropriate monetary policy, including their projections of the federal funds rate. Almost all participants also provided their individual assessments of the level of uncertainty and the balance of risks associated with their projections. The Summary of Economic Projections was released to the public following the conclusion of the meeting.

Participants generally noted that inflation had increased further and remained well above the Committee's 2 percent longer-run objective. They observed that both core and total inflation had moved higher and generally attributed these increases to the lingering effects of tariffs, supply chain disruptions related to the closure of the Strait of Hormuz, and strength in demand for some goods and services stemming from robust AI-related investment. Several participants commented that price pressures had become more broad based, with a large share of goods and services—including transportation, airfares, petrochemical products, and agricultural inputs—experiencing substantial increases. Several participants remarked that services price inflation excluding housing had declined little and remained high.

The majority of participants commented that most measures of medium- and longer-term inflation expectations remained at levels consistent with the Committee's 2 percent objective. Participants noted the importance of stable longer-term inflation expectations and emphasized the Committee's role in keeping those expectations anchored at levels consistent with 2 percent inflation.

Participants anticipated that inflation would remain elevated in the near term and then begin to decline as the effects of tariffs and energy price increases wane and other supply disruptions related to the closure of the Strait of Hormuz diminish. Participants judged that the risks to the inflation outlook were still tilted to the upside. Many participants noted that elevated commodity prices and supply disruptions could persist longer than currently anticipated. Several participants reported that their business contacts were facing notable cost pressures. Some participants observed that the sharp rise in input costs reported in business surveys raised concerns about the potential for higher energy and commodity costs to pass through more broadly to final goods prices. Several participants noted, however, that firms in their Districts reported that they had been cautious about increasing prices, citing concerns that higher prices could reduce demand or their market shares. Many participants noted that ongoing strong demand for AI infrastructure would likely sustain upward pressure on prices for technology products and electricity. Most participants remarked that growth in economic activity that exceeded that of potential output, owing in part to strong AI business investment, could contribute to more persistent inflationary pressures. Some participants remarked that productivity gains associated with AI adoption would eventually reduce production costs and increase aggregate supply, which should put downward pressure on inflation, though they noted this effect would likely take time to materialize. Several participants noted that the deceleration in housing services prices was likely to continue to be a source of disinflationary pressure. The majority of participants highlighted the possibility that, after several years of inflation above 2 percent, continued elevated inflation rates could begin to affect inflation expectations and wage- and price-setting decisions. Participants emphasized that considerable uncertainty surrounded their inflation outlook and stressed the importance of closely monitoring inflation developments and inflation expectations.

With regard to the labor market, participants generally observed that the unemployment rate had remained relatively stable over the past year at a level near participants' estimates of its longer-run level. Participants generally remarked that payroll employment gains had strengthened this year and appeared roughly consistent with underlying labor force growth. Several participants observed that other labor market indicators, such as job openings, initial unemployment insurance claims, and layoffs had remained stable in recent months and that such data pointed to a balanced labor market. Several participants noted, however, that declines in the job-finding rate and certain survey measures of job availability reflected a labor market with relatively low dynamism. Many participants remarked that the labor market was not currently a source of inflationary pressures, or that nominal wage growth remained consistent with inflation moving toward 2 percent.

Participants generally expected labor market conditions to remain stable in the near term, with the unemployment rate staying close to current levels. Some participants remarked that their concerns earlier this year about labor market deterioration had eased with recent data, and several participants noted that the solid payroll employment data in recent months could signal increased labor market momentum. Several participants cited, however, the possibility that uncertainty related to geopolitical developments or the broader economic outlook could lead firms to reduce hiring or begin implementing layoffs. Some participants commented on the possibility that AI could, over time, affect employment prospects for some classes of workers.

Participants generally observed that economic activity had continued to expand at a solid pace, despite elevated uncertainty, supported by strong business investment and resilient consumer spending. Participants generally noted that the strength in business investment remained concentrated in AI-related expenditures, which showed no signs of slowing, as companies continued to announce capital expenditure plans that exceeded earlier expectations. Some participants suggested that those investments would likely increase the growth of productivity and of potential output in the coming years. These participants remarked, however, that considerable uncertainty remained regarding both the timing and magnitude of potential productivity gains, which were expected to lag the ongoing boost of AI adoption on demand. Some participants noted that broad financial conditions were supporting demand. These participants pointed specifically to high equity prices and noted that those prices had been driven by strong corporate earnings and optimism about AI. With respect to household spending, most participants observed that stock market gains and federal income tax refunds sent earlier this year had provided support to consumer spending, particularly among higher-income households. They noted, however, that lower-income households were increasingly relying on credit to maintain spending and continued to face disproportionate pressures from elevated gasoline and grocery prices.

Participants generally expected solid real GDP growth to continue throughout the remainder of the year and pointed to several factors likely to support continued expansion, including ongoing AI-related investment, household spending, and fiscal policy. Participants generally acknowledged that while the economy had demonstrated resilience to date, uncertainty surrounding the economic outlook remained elevated, partly due to the conflict in the Middle East.

In their consideration of monetary policy at this meeting, all participants supported maintaining the current target range for the federal funds rate. Participants generally noted that recent indicators suggested that economic activity had been expanding at a solid pace and that labor market conditions had appeared stable. Participants observed that inflation was elevated relative to the Committee's 2 percent longer-run objective, in part reflecting price increases from supply shocks in certain sectors, including energy. Participants generally assessed that information received over the intermeeting period suggested that upside risks to price stability remained elevated while downside risks to achieving maximum employment had moderated a bit. A few participants commented that, in light of these developments, there was a case for raising the target range for the federal funds rate, but those participants indicated that they supported maintaining the current target range at this meeting. Several participants remarked that they did not see the current policy stance as restrictive, while a few other participants commented that they saw the current policy stance as slightly restrictive.

With regard to the outlook for monetary policy, amid high assessed uncertainty, various participants discussed a range of scenarios for the evolution of the economy and for future monetary policy actions. Most participants remarked on scenarios in which inflationary pressures would dissipate and inflation would soon begin to return to 2 percent. In such scenarios, almost all of these participants noted that it would likely be appropriate to maintain or eventually lower the target range for the federal funds rate. Most participants, however, also pointed to scenarios in which, in the context of stable labor market conditions, inflation would remain elevated due to strong AI-related demand, the conflict in the Middle East, or the effects of tariffs. In such scenarios, almost all of these participants indicated that some policy firming would likely be warranted to return inflation to 2 percent. Regarding participants' individual assessments of appropriate monetary policy under what each participant judged to be the most likely scenario for the economy, many participants indicated that the appropriate level of the federal funds rate would be within or slightly below the current target range at the end of this year. Many other participants, however, assessed that the appropriate level of the federal funds rate would be above the current target range at the end of this year. Participants noted that their future policy actions would depend on incoming information.

A number of participants noted that it was an opportune time to consider significant changes to the FOMC's postmeeting statement. A majority of participants remarked that they saw advantages in shortening the statement. Most participants emphasized that they preferred not to repeat the language in the previous postmeeting statement that had suggested an easing bias regarding the likely direction of the Committee's future interest rate decisions. Various participants discussed how the public could perceive the changes to the postmeeting statement. Some participants commented that they welcomed the opportunity to review the Committee's communications tools and practices.

The Chairman described plans to establish five independent task forces to examine issues related to the broad conduct of monetary policy.

Committee Policy Actions

In support of the Committee's dual-mandate goals, all members agreed to maintain the target range for the federal funds rate at 3-1/2 to 3-3/4 percent and to reaffirm the FOMC's policy of maintaining ample reserves in the banking system. Members also agreed that the statement would not repeat the language that had suggested an easing bias regarding the likely direction of the Committee's future interest rate decisions. Members noted that there had been little change in the unemployment rate and solid growth in economic activity, but that inflation remained elevated relative to the Committee's 2 percent goal. Against this backdrop, members concurred that the postmeeting statement would convey the Committee's commitment to achieving its dual-mandate goals and emphasize that the Committee will deliver price stability.

At the conclusion of the discussion, the Committee voted to direct the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the System Open Market Account (SOMA) in accordance with the following domestic policy directive, for release at 2:00 p.m.:

"Effective June 18, 2026, the Federal Open Market Committee directs the Desk to:

- Undertake open market operations as necessary to maintain the federal funds rate in a target range of 3-1/2 to 3-3/4 percent.

- Conduct standing overnight repurchase agreement operations at a rate of 3.75 percent.

- Conduct standing overnight reverse repurchase agreement operations at an offering rate of 3.5 percent and with a per-counterparty limit of $160 billion per day.

- When appropriate, increase the SOMA holdings of securities through purchases of Treasury bills and, if needed, other Treasury securities with remaining maturities of 3 years or less to maintain an ample level of reserves.

- Roll over at auction all principal payments from the Federal Reserve's holdings of Treasury securities. Reinvest all principal payments from the Federal Reserve's holdings of agency securities into Treasury bills."

The vote also encompassed approval of the statement below for release at 2:00 p.m.:

"The Federal Open Market Committee approved the following statement for release by a 12 – 0 vote:

The Committee decided to maintain the target range for the federal funds rate at 3-1/2 to 3-3/4 percent, in support of the Federal Reserve's dual mandate. The Committee reaffirmed its policy of maintaining ample reserves in the banking system.

Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.

Inflation remains elevated relative to the Committee's 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability."

Voting for this action: Kevin Warsh, John C. Williams, Michael S. Barr, Michelle W. Bowman, Lisa D. Cook, Beth M. Hammack, Philip N. Jefferson, Neel Kashkari, Lorie K. Logan, Anna Paulson, Jerome H. Powell, and Christopher J. Waller.

Voting against this action: None.

Consistent with the Committee's decision to leave the target range for the federal funds rate unchanged, the Board of Governors of the Federal Reserve System voted unanimously to maintain the interest rate paid on reserve balances at 3.65 percent, effective June 18, 2026. The Board of Governors of the Federal Reserve System voted unanimously to approve the establishment of the primary credit rate at the existing level of 3.75 percent.

It was agreed that the next meeting of the Committee would be held on Tuesday–Wednesday, July 28–29, 2026. The meeting adjourned at 10:30 a.m. on June 17, 2026.

Notation Vote

By notation vote completed on May 19, 2026, the Committee unanimously approved the minutes of the Committee meeting held on April 28–29, 2026.

Attendance

Kevin Warsh, Chairman

John C. Williams, Vice Chair

Michael S. Barr

Michelle W. Bowman

Lisa D. Cook

Beth M. Hammack

Philip N. Jefferson

Neel Kashkari

Lorie K. Logan

Anna Paulson

Jerome H. Powell

Christopher J. Waller

Thomas I. Barkin, Mary C. Daly, Austan D. Goolsbee, Sushmita Shukla, and Cheryl L. Venable, Alternate Members of the Committee

Susan M. Collins, Alberto G. Musalem, and Jeffrey R. Schmid, Presidents of the Federal Reserve Banks of Boston, St. Louis, and Kansas City, respectively

Joshua Gallin, Secretary

Matthew M. Luecke, Deputy Secretary

Michelle A. Smith, Assistant Secretary

Mark E. Van Der Weide, General Counsel

Richard Ostrander, Deputy General Counsel

Trevor A. Reeve, Economist

Stacey Tevlin, Economist

Beth Anne Wilson, Economist

Stephanie R. Aaronson, Shaghil Ahmed, Brian M. Doyle, Eric M. Engen, Michael T. Kiley, Elizabeth Klee, Edward S. Knotek II, Karel Mertens, Andrea Raffo, and Donald Keith Sill, Associate Economists

Roberto Perli, Manager, System Open Market Account

Julie Ann Remache, Deputy Manager, System Open Market Account

Jose Acosta, Senior System Engineer II, Division of Information Technology, Board

Isaiah C. Ahn, Information Management Analyst, Division of Monetary Affairs, Board

Alyssa Arute,2 Assistant Director, Division of Reserve Bank Operations and Payment Systems, Board

Gadi Barlevy, Executive Vice President, Federal Reserve Bank of Chicago

William F. Bassett, Senior Associate Director, Division of Financial Stability, Board

Kimberly N. Bayard, Section Chief, Division of Research and Statistics, Board

Michele Cavallo, Special Adviser to the Board, Division of Board Members, Board

Lisa Chung,2 Head of Domestic and International Markets, Federal Reserve Bank of New York

Andrew Cohen,3 Special Adviser to the Board, Division of Board Members, Board

Francisco Covas, Deputy Director, Division of Supervision and Regulation, Board

Ryan A. Decker, Special Adviser to the Board, Division of Board Members, Board

Cynthia L. Doniger,4 Principal Economist, Division of Monetary Affairs, Board

Burcu Duygan-Bump, Deputy Director, Division of Research and Statistics, Board

Eric C. Engstrom, Special Adviser to the Chairman, Division of Board Members, Board

Giovanni Favara, Associate Director, Division of Monetary Affairs, Board

Laura J. Feiveson,4 Special Adviser to the Board, Division of Board Members, Board

Andrew Figura, Senior Associate Director, Division of Research and Statistics, Board

Jenn Gallagher, Assistant to the Board, Division of Board Members, Board

Carlos Garriga, Senior Vice President, Federal Reserve Bank of St. Louis

Joseph W. Gruber, Executive Vice President, Federal Reserve Bank of Kansas City

Daniel L. Heil, Assistant to the Chairman (Special Projects), Division of Board Members, Board

Erik Heitfield, Deputy Associate Director, Division of Research and Statistics, Board

Valerie S. Hinojosa, Assistant Director, Division of Monetary Affairs, Board

Jane E. Ihrig, Special Adviser to the Board, Division of Board Members, Board

Margaret M. Jacobson, Senior Economist, Division of Monetary Affairs, Board

Benjamin K. Johannsen, Deputy Associate Director, Division of Monetary Affairs, Board

Anna R. Kovner, Executive Vice President, Federal Reserve Bank of Richmond

Spencer D. Krane, Senior Vice President, Federal Reserve Bank of Chicago

Sylvain Leduc, Executive Vice President and Director of Economic Research, Federal Reserve Bank of San Francisco

Andreas Lehnert, Director, Division of Financial Stability, Board

Paul Lengermann, Deputy Associate Director, Division of Research and Statistics, Board

Eric LeSueur,2 Policy and Market Analysis Advisor, Federal Reserve Bank of New York

Logan T. Lewis, Assistant Director, Division of International Finance, Board

Laura Lipscomb, Special Adviser to the Board, Division of Board Members, Board

Francesca Loria, Principal Economist, Division of Monetary Affairs, Board

Byron Lutz, Deputy Associate Director, Division of Research and Statistics, Board

Jonathan P. McCarthy, Economic Research Advisor, Federal Reserve Bank of New York

John P. McConnell, Assistant to the Chairman (Speechwriting), Division of Board Members, Board

Benjamin W. McDonough, Secretary of the Board, Office of the Secretary, Board

David Newville, Director, Division of Consumer and Community Affairs, Board

Anna Nordstrom, Head of Markets, Federal Reserve Bank of New York

Alyssa T. O'Connor, Special Adviser to the Board, Division of Board Members, Board

Karen A. Pennell, First Vice President, Federal Reserve Bank of Boston

Eugenio P. Pinto, Special Adviser to the Board, Division of Board Members, Board

Odelle Quisumbing,2 Assistant to the Secretary, Office of the Secretary, Board

Nellisha D. Ramdass, Deputy Director, Division of Monetary Affairs, Board

Romina D. Ruprecht, Senior Economist, Division of Monetary Affairs, Board

Zeynep Senyuz, Special Adviser to the Board, Division of Board Members, Board

Hiroatsu Tanaka, Principal Economist, Division of Monetary Affairs, Board

Mary H. Tian, Group Manager, Division of Monetary Affairs, Board

Jeffrey D. Walker,2 Senior Associate Director, Division of Reserve Bank Operations and Payment Systems, Board

Jonathan Willis, Vice President, Federal Reserve Bank of Atlanta

Paul Winfree, Assistant to the Chairman (Special Projects), Division of Board Members, Board

Emre Yoldas, Deputy Associate Director, Division of International Finance, Board

Egon Zakrajšek, Executive Vice President, Federal Reserve Bank of Boston

_______________________

Joshua Gallin

Secretary

1. The Federal Open Market Committee is referenced as the "FOMC" and the "Committee" in these minutes; the Board of Governors of the Federal Reserve System is referenced as the "Board" in these minutes. Return to text

2. Attended through the discussion of developments in financial markets and open market operations. Return to text

3. Attended Wednesday's session only. Return to text

4. Attended Tuesday's session only. Return to text

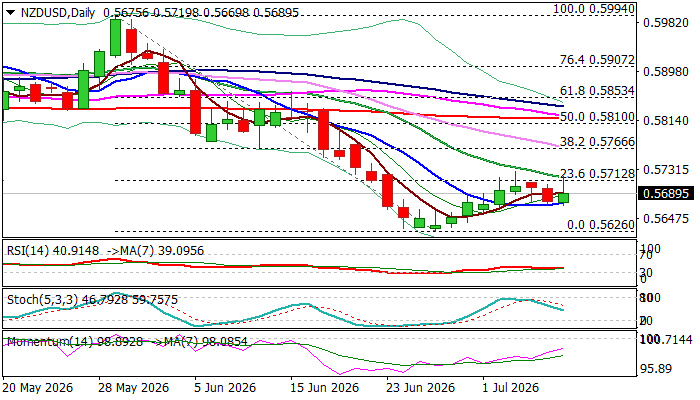

NZD Jumps on RBNZ Hawkish Hike but Struggles to Hold Gains

The New Zealand dollar rose 0.75% in immediate reaction to (expected) action of the RBNZ to raise interest rates by 25 basis points to 2.5%, earlier today.

This was the first rate hike in almost three years, with comments from the policymakers pointing to potential further tightening (although without timing for the future action), as some policymakers see increased inflationary risk, while others describe the outlook as balanced for now.

Overall, markets saw today’s decision as hawkish hike, with about 60% bets for another hike in September’s policy meeting.

The Kiwi dollar reversed a part of today’s post-rate gain, unable (again) to sustain break above initial barriers at 0.5712/16 (Fibo 23.6% of 0.5994/0.5626 / falling 20DMA) and capitalize from relatively strong bullish signals from the central bank’s decision.

Daily studies remain in predominantly bearish configuration that continues to produce headwinds to recovery leg from 0.5626 (new 2026 low posted on June 26), after two failures here have been already registered recently.

The downside is likely to remain vulnerable as long as price action holds below 0.5712/16 pivots, while firm break higher would signal bullish continuation and open way for further recovery towards next significant barrier at 0.5766 (Fibo 38.2% / falling 30DMA).

Res: 0.5716; 0.5766; 0.5810; 0.5840

Sup: 0.5672; 0.5626; 0.5600; 0.5565