Sample Category Title

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 5 and 6 February 2024

Members present

Michele Bullock (Governor and Chair), Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Elana Rubin AM, Carol Schwartz AO, Alison Watkins AM

Others present

Christopher Kent (Assistant Governor, Financial Markets), Marion Kohler (Head, Economic Analysis Department), Tom Rosewall (Deputy Head, Economic Analysis Department)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Sarah Hunter (Assistant Governor, Economic), Penelope Smith (Head, International Department), Carl Schwartz (Acting Head, Domestic Markets Department), Meredith Beechey Osterholm (Future Hub), Sally Cray (Chief Communications Officer)

International economic developments

Members began by observing that global inflation remained high but that there had been encouraging progress in reducing inflation towards central banks' targets. Much of the easing in inflation in advanced economies had been due to movements in energy and goods prices. Members noted that global shipping costs had increased recently, partly related to attacks on vessels in the Red Sea. While this posed some upside risk to tradable goods inflation, the increases in shipping costs had been small relative to those seen during the pandemic.

Compared with goods price inflation, core services price inflation had continued to ease only gradually in most advanced economies. Rent inflation was yet to show clear signs of easing in many economies. On the other hand, inflation for services other than housing had eased from its peaks, consistent with the gradual easing in labour market conditions and an improvement in the balance of demand and supply for services. However, overall services price inflation remained high relative to pre-pandemic rates.

Economic growth had slowed to below-trend rates in many advanced economies in response to restrictive monetary policy settings. This had contributed to progress in returning inflation to target. Members noted that real household disposable income growth was positive in a number of advanced economies, yet consumption growth remained subdued. The United States was the main exception, with relatively firm growth in real incomes and consumption underpinning robust economic growth.

GDP growth in Australia's major trading partners was expected to ease in 2024. Growth in China was expected to slow over 2024 and 2025 as the post-pandemic rebound in consumption of services fades and the property sector remains weak. Weakness in these areas was expected to be partly offset by continued strength in manufacturing investment and further policy support for infrastructure investment. Additional policy measures had supported Chinese steel production and, in turn, the prices of iron ore and coking coal received by Australian exporters.

Domestic economic conditions

Members observed that inflation in Australia had moderated, with both headline and underlying inflation lower in the December quarter 2023 than had been expected three months prior. Core goods price inflation had declined faster than expected, as also seen abroad. Services price inflation, which largely reflects conditions in the domestic economy, had declined to a lesser extent and remained high. Members discussed how much signal to take from the faster-than-expected decline in inflation in the December quarter and whether goods price inflation might fall further given ongoing excess capacity in the Chinese economy. They also considered the implications for inflation if various subsidies that were due to expire were extended.

Members discussed how high inflation, higher taxes and tighter monetary policy had contributed to a noticeable slowing in growth in aggregate demand over 2023. Looking through the volatility in monthly outcomes, retail sales volumes were expected to have been broadly unchanged in the December quarter. Retailers had reported that similar conditions had persisted into the first part of 2024. More broadly, weak household spending growth, particularly in per capita terms, had been only partly offset by strong growth in business investment and public demand. Labour market conditions had remained tight but had continued to ease over preceding months in response to slower economic growth. The unemployment rate and underemployment rate had both increased by around ½ percentage point since mid-2023, albeit from low levels. Overall, conditions in the labour market were assessed to be tight relative to what would be consistent with sustained full employment.

Wages growth had remained robust, although there were signs that it was slowing in some segments of the labour market. Very weak productivity outcomes over the preceding years had contributed to a sharp increase in labour costs per unit of output. Members acknowledged that it is too soon to determine the extent to which a fading of the lingering disruptions from the pandemic and the adoption of artificial intelligence would support a turnaround in productivity growth.

Members also discussed the staff's assessment of spare capacity in the economy. Estimates of potential output, while subject to significant uncertainty, suggested that the level of aggregate demand remained above the economy's supply capacity. This was also consistent with other indicators of spare capacity, such as survey measures of utilisation, metrics from the labour market and the rate of inflation.

Turning to the outlook, members noted that overall demand growth was expected to remain subdued in the near term as high inflation and earlier interest rate increases continue to weigh on household consumption. The near-term outlook for GDP growth had been revised down modestly from the outlook three months prior. This mainly reflected a weaker outlook for consumer spending, reflecting the decline in real incomes over recent years. As inflation moderates and real incomes start to rise from 2024, consumption growth was expected to recover gradually to its pre-pandemic average over 2025. Members considered the risk that consumers might not increase spending as real incomes begin to rise again; this could occur if the effect of the previous fall in real wages outweighs the support from the large stock of additional savings built up in 2020 and 2021 as well as the rise in housing wealth over the previous year. They concluded that the outlook for consumption remains a significant source of uncertainty, with risks to the upside and downside.

Members also discussed the implications of the announced changes to the Stage 3 income tax cuts. They noted that the aggregate reduction in income tax payable was similar to the legislated Stage 3 tax cuts already incorporated in the staff's forecasts. Members were briefed on the potential for the different distribution of income tax reductions across households to affect the forecasts and concluded that the effect would be negligible for plausible assumptions about differences in marginal propensities to consume.

Conditions in the labour market were expected to ease further over the coming year or so, to levels consistent with sustained full employment. Employment was expected to continue to grow moderately, though slower than the working-age population, and the unemployment rate and the broader underutilisation rate were expected to increase further. Nominal wages growth was expected to remain robust in the near term before moderating in response to further easing in the labour market. Members noted that the outlook for wages growth was consistent with the inflation target, on the assumption that productivity growth increases to around its long-run average.

Members observed that inflation was expected to return to the target range of 2–3 per cent in 2025 and to the midpoint in 2026. Inflation was anticipated to decline a little quicker than previously thought, because goods price inflation had declined more than expected and domestic demand was also a little softer than previously anticipated. But services inflation remained high and was still expected to decline only gradually as aggregate demand moderates and growth in labour and non-labour costs eases.

Financial conditions

Members noted that global financial conditions had eased over prior months.

Market participants' expectations for reductions in central banks' policy rates had been brought forward since the previous meeting. This had occurred in response to lower-than-expected inflation and central bank communication that further policy rate increases were less likely. However, members noted that this had reversed in late January after a number of central bank officials stated that policy rate cuts were not imminent because they were looking for more evidence that low inflation would be sustained. Stronger-than-expected US labour market data had also pushed out market expectations for reductions in policy rates in the days prior to the meeting. At the time of the meeting, market pricing implied an expectation that advanced economy central banks would start reducing policy rates from around the middle of the year.

Members noted that fewer reductions in the policy rate were expected in Australia than in many other advanced economies. Market pricing suggested that market participants believed the cash rate had probably reached its peak, with rate cuts of around 50 basis points expected by the end of 2024. This was broadly consistent with the median forecast of market economists. These expectations suggested that the policy rate in Australia would peak at a lower level than in a number of other advanced economies and decline later.

Sovereign bond yields in advanced economies had declined over preceding months in response to the improved inflation outlook and changing expectations for the paths of central bank policy rates. Other measures of financial conditions had also eased. Equity prices had risen to record highs in a number of advanced economies, including Australia, though members noted that the gains in US share prices were narrowly based and valuations there looked stretched. Spreads on corporate bonds had also declined. Nonetheless, the demand for credit generally remained subdued. Corporate bond issuance was below average in the United States and Europe, especially for lower rated corporations, and credit growth in those economies remained low. In discussing these developments, members observed that longer term interest rates were less relevant for financial conditions in Australia than in economies such as the United States. Members also observed that corporate bond issuance was robust in Australia, in contrast to other advanced economies.

In China, financial conditions had eased a little alongside some further policy support to address significant economic headwinds, including considerable stress in the property sector. Overall, the scale of monetary policy easing in China had been moderate, with more substantive support for the economy having been delivered through fiscal policy.

The Australian dollar had appreciated through late 2023. This had occurred against a backdrop of general US dollar weakness that was underpinned by expectations of near-term cuts to the federal funds rate target. The Australian dollar had since depreciated as these expectations were unwound and had been little changed since early November. The trade-weighted Australian dollar was trading near early 2022 levels.

In Australia, financial conditions were considered to be restrictive overall. The tightening of monetary policy had led to a significant rise in household debt payments, which, in combination with other factors, was weighing on disposable incomes and consumption.

Required mortgage payments had risen to a historical high as a share of household disposable income. Members noted this share would rise further as remaining low fixed-rate mortgages expire and roll onto higher rates, and the increase in the cash rate in November continues to flow through to payments. By contrast, a broader measure of total household debt payments (relative to disposable income) remained below its estimated peak, as personal credit had declined significantly since 2008. Extra payments into mortgage offset and redraw accounts had also declined since 2022, though they had increased in the second half of 2023. When viewed alongside weak consumption, this increase suggested that many borrowers might be responding to the incentive from higher interest rates to save more and limit their consumption.

Members noted that the sharp rise in interest rates had also underpinned a large decline in credit growth from its peak in early 2022. Both housing and business credit growth had stabilised at a lower level over the preceding year. Business credit had been growing a little above its post-2008 average, while housing credit growth was below its average over the same period. Even so, new housing lending had picked up over the preceding year, consistent with the rebound in national housing prices.

Considerations for monetary policy

Turning to the policy decision, members noted that there had been further progress towards the Board's objectives but that more progress was required and the outlook remained uncertain.

Inflation in Australia had declined but was still well above target. Members noted that the moderation in inflation had been driven by softer goods price inflation and that any further slowing in this component was likely to be modest. By contrast, services price inflation remained high and had declined only a little. Members observed that while some components of services inflation were unlikely to be responsive to monetary policy in the near term, there was still a large element that reflected excess demand.

Members noted that consumption growth had remained subdued and was a little weaker than previously expected. The slowing in consumer spending reflected the impact on growth in real household disposable income of high inflation and a higher tax and interest burden. Real household disposable income was expected to grow in the period ahead, including because of the anticipated decline in inflation. Despite subdued consumption growth, overall growth in GDP remained modest, supported by a number of other parts of the economy that had been growing strongly. While overall growth had been modest, members agreed that aggregate demand was still high relative to the economy's supply potential, which was generating inflationary pressures.

Members acknowledged the significant uncertainties around the economic outlook. The most material risks were the potential for inflation to be more persistent than anticipated, productivity growth not to recover as assumed and consumption to weaken more markedly than in the staff's central forecast. Members noted that the staff's central forecasts were for inflation to return to the target range of 2–3 per cent in 2025 and to the midpoint in 2026, with the unemployment rate rising modestly as growth in labour supply outpaces growth in employment. This was predicated, however, on inflation expectations remaining anchored around the midpoint of the target range and some assumed recovery in productivity. Members considered the policy implications of a scenario in which inflation expectations instead gradually drift up and another where consumption is materially weaker than in the central forecasts.

Members discussed the extent of the tightness in financial conditions. They noted that financial conditions appeared to be quite restrictive on some measures, but less restrictive on others. Members observed that this is consistent with growth in activity varying quite significantly across parts of the economy.

In light of these observations, members considered whether to raise the cash rate target by a further 25 basis points at this meeting or to leave it unchanged.

The case to raise the cash rate further centred on the observation that it would take some time for inflation to return to target and the labour market to full employment. Inflation was expected to take a further two years or so to return towards the midpoint of the target range under the central forecast. This was consistent with the staff's assessment that aggregate demand remains above the economy's supply potential. Members noted that an increase in the cash rate target at this meeting could slow the growth of demand further and reduce the risk of inflation not returning to target in an acceptable timeframe. Increasing the cash rate target now would not prevent the Board from easing monetary policy if the economy were to weaken more sharply than envisaged.

The case to leave the cash rate target unchanged at this meeting centred on the observation that the risk of inflation not returning to the Board's target within a reasonable timeframe had eased. The moderation in inflation over preceding months had been slightly larger than previously expected, and global inflation outcomes had provided additional confidence that inflation in Australia would moderate further. Data on the labour market and consumer spending had also been weaker than previously expected. Members noted that it was possible that conditions in the labour market were already consistent with full employment, although this was judged to be unlikely.

Members noted that the staff's central forecasts were for inflation to return to target within the timeframe that they had previously concluded was acceptable, and for conditions in the labour market to be broadly consistent with full employment in a year or so. Both of these forecasts were predicated on a technical assumption for the cash rate, derived from market economists' forecasts and market pricing, that include no additional increase in the cash rate. Members observed that the risks around the outlook were broadly balanced; there was a risk that inflation proves more persistent but there was also a risk that consumer spending weakens more sharply than it had to date. Given these observations, it was reasonable to conclude that leaving the cash rate unchanged at this meeting, and continuing to monitor how risks to the outlook evolve, was the most appropriate course of action.

In weighing up these two options, members judged that the case to leave the cash rate target unchanged was the stronger one. They agreed that doing so would best balance the Board's objectives for price stability and full employment. Members noted that the data had evolved in a manner that gave them more confidence that inflation would return to target within a reasonable timeframe while allowing employment to continue to grow.

Members then considered the options for how to communicate the Board's decision in the post-meeting statement. They agreed to communicate that there had been progress towards meeting the Board's inflation objective. At the same time, members noted that it would take some time before they could have sufficient confidence that inflation would return to target within a reasonable timeframe. Uncertainty about the outlook for the economy was high. Members also observed that the costs of inflation not returning to target within the envisaged timeframe were potentially very high. Given this, members agreed that it was appropriate not to rule out a further increase in the cash rate target. They also agreed that it would be important to continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. Members reiterated their resolve to do what is necessary to return inflation to target.

In light of these conclusions, members agreed that it was important for the Board's public statement to make clear that inflation had moderated but was still high, and that it was not yet possible to rule in or out further increases in interest rates. Members also agreed on the importance of highlighting the uncertainty surrounding the economic outlook and the need for monetary policy to be driven by developments in relevant data, the outlook for the economy and the evolving risks.

The decision

The Board decided to leave the cash rate target unchanged at 4.35 per cent, and the interest rate on Exchange Settlement balances unchanged at 4.25 per cent.

How Does a UK Recession Affect the Pound’s Fate?

- BoE maintains more hawkish stance than Fed, ECB

- Despite recession in H2 2023, rate cut bets were not altered

- January data suggests the economy may have turned a corner

- With general elections looming, what’s next for the pound?

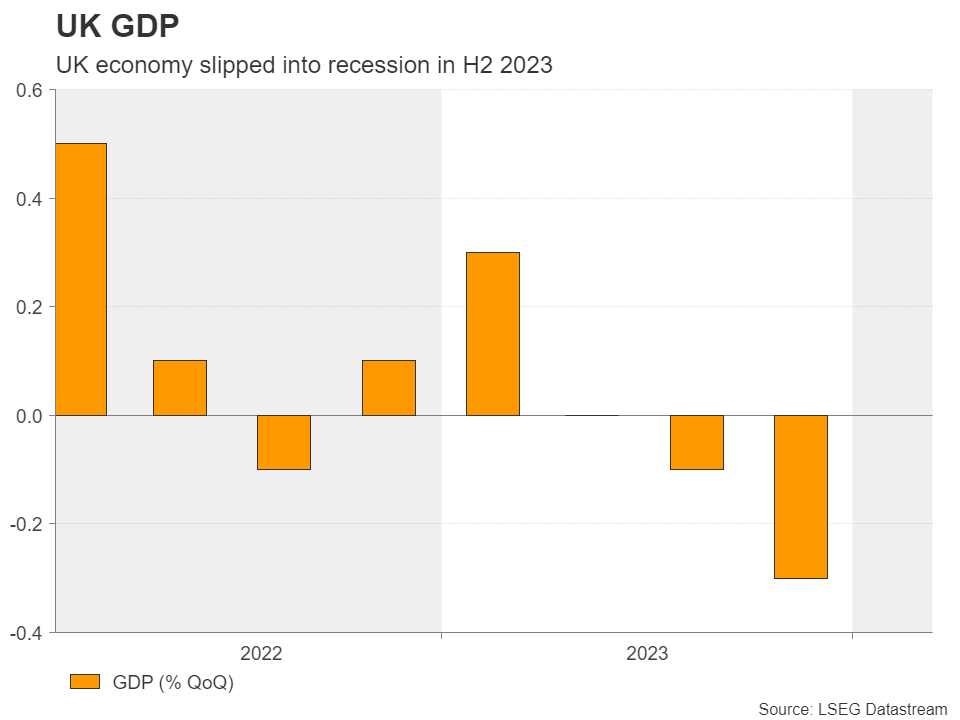

UK enters recession in H2 2023

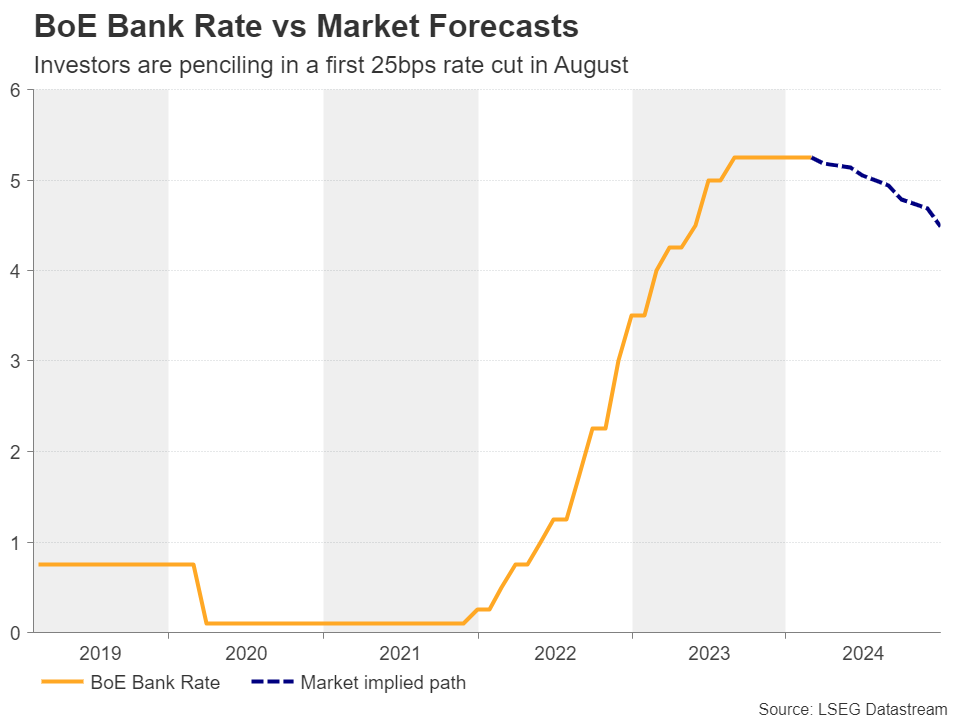

Despite dropping its tightening bias at its February gathering, the Bank of England (BoE) maintained a more hawkish stance than the Fed and the ECB, pushing back against interest rate cuts. At the press conference following the latest decision, Governor Bailey said they are not yet at a point where they can lower borrowing costs, adding that policy needs to stay sufficiently restrictive for sufficiently long.

However, this was before last week’s barrage of economic data, with the highlight being the preliminary GDP numbers for Q4, which revealed that the economy contracted by more than anticipated, officially entering a technical recession. This weighed on the British pound, which had already been hurt the day before, after the CPI figures suggested that inflation held steady in January, confounding expectations of a small acceleration.

However, the market’s BoE implied path was not lowered. In other words, investors did not bring forward their rate cut bets. Currently, they are pricing in around 70bps worth of reductions by the end of the year, with the first quarter-point cut penciled in for August. Even after the notable upward adjustment to its interest rate projections regarding the Fed, the market still holds a more hawkish – or less dovish – view about the BoE.

Has the UK economy turned a corner in 2024?

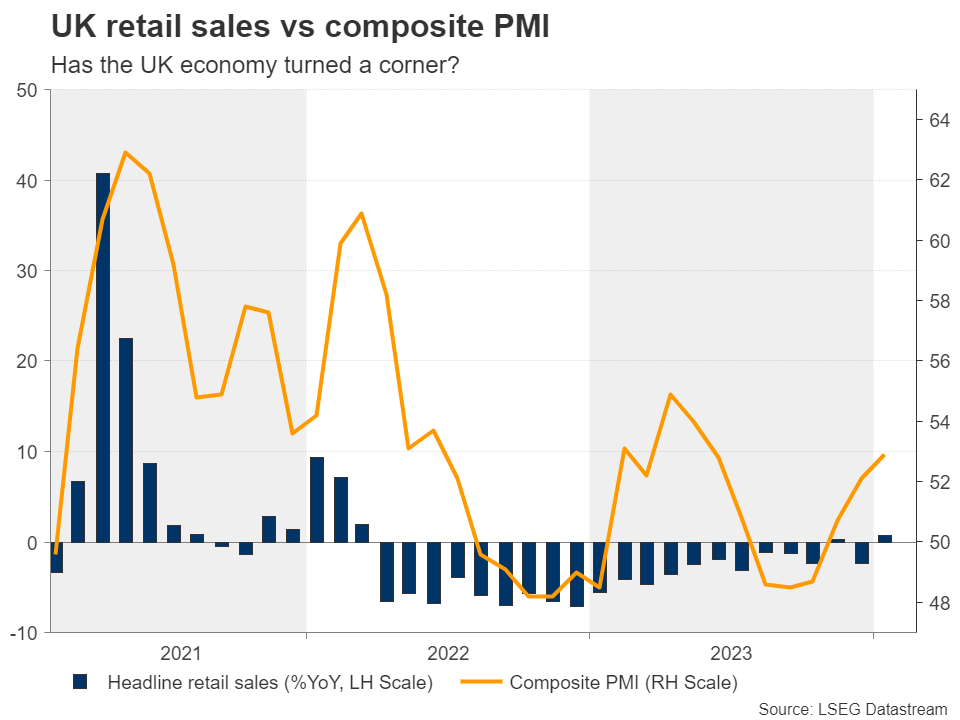

But why is that? One reason may be that, despite the latest slowdown, inflation in the UK remains stickier than other major economies, with the core rate at 5.1%, more than 2.5 times the BoE’s objective of 2%. On top of that, wages have slowed by less than expected, with the rate of average weekly earnings excluding bonuses coming in at 6.2% y/y in December, well above the CPI rates. This still presents some upside risks to the inflation outlook for the months to come. Last but not least, retail sales for January accelerated to their fastest pace in nearly three years, which combined with the improvement in the PMIs for the month, adds to hopes that the economy may have started turning the corner.

The confirmation of a recession in the second half of last year seems to be having more political than economic importance, as it’s a heavy blow to Rishi Sunak’s popularity ahead of an expected general election later this year. Voters appear to have not been convinced that his plan of cutting taxes is working, shifting their trust of the economy to the Labour Party, according to opinion polls.

Just after the GDP data, finance minister Jeremy Hunt said that there were signs the economy is turning a corner and that they must stick to their plan. This means that at least until the election, the fiscal mentality of the government may continue to work against the BoE’s efforts to tackle elevated inflation, thereby prompting the central bank to keep interest rates higher for longer, as officials have been already communicating. Just last Wednesday, BoE Governor Bailey said that he still wanted more evidence that inflation pressures were abating, corroborating the notion that the Bank’s focus remains on price data.

Heading into elections, what’s next for the pound?

With all that in mind, should upcoming data confirm the narrative that the UK economy is growing again, investors are likely to further push back their rate cut bets, which could prove supportive for the pound. Considering also that due to the UK’s twin deficit, the currency has developed a correlation with risk-sentiment, further advances in the equity world could offer an extra help. The opposite may be true if the economy continues to struggle, even with the government abiding by its tax-cut plan.

Having said all that, closer to the elections, which need to be held before January, the uncertainty about the change in fiscal attitude may have a negative impact on sterling. The leading Labour party has been portraying itself as the party of fiscal responsibility and thus, scrapping the Conservative’s agenda may prompt the BoE to start loosening monetary policy sooner.

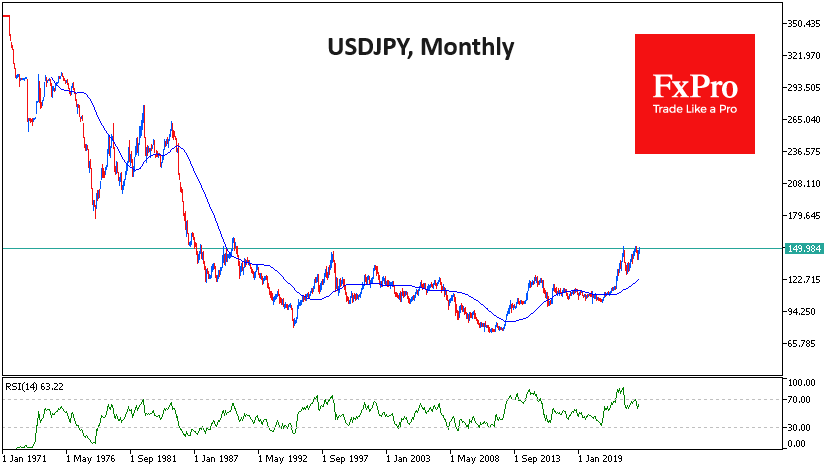

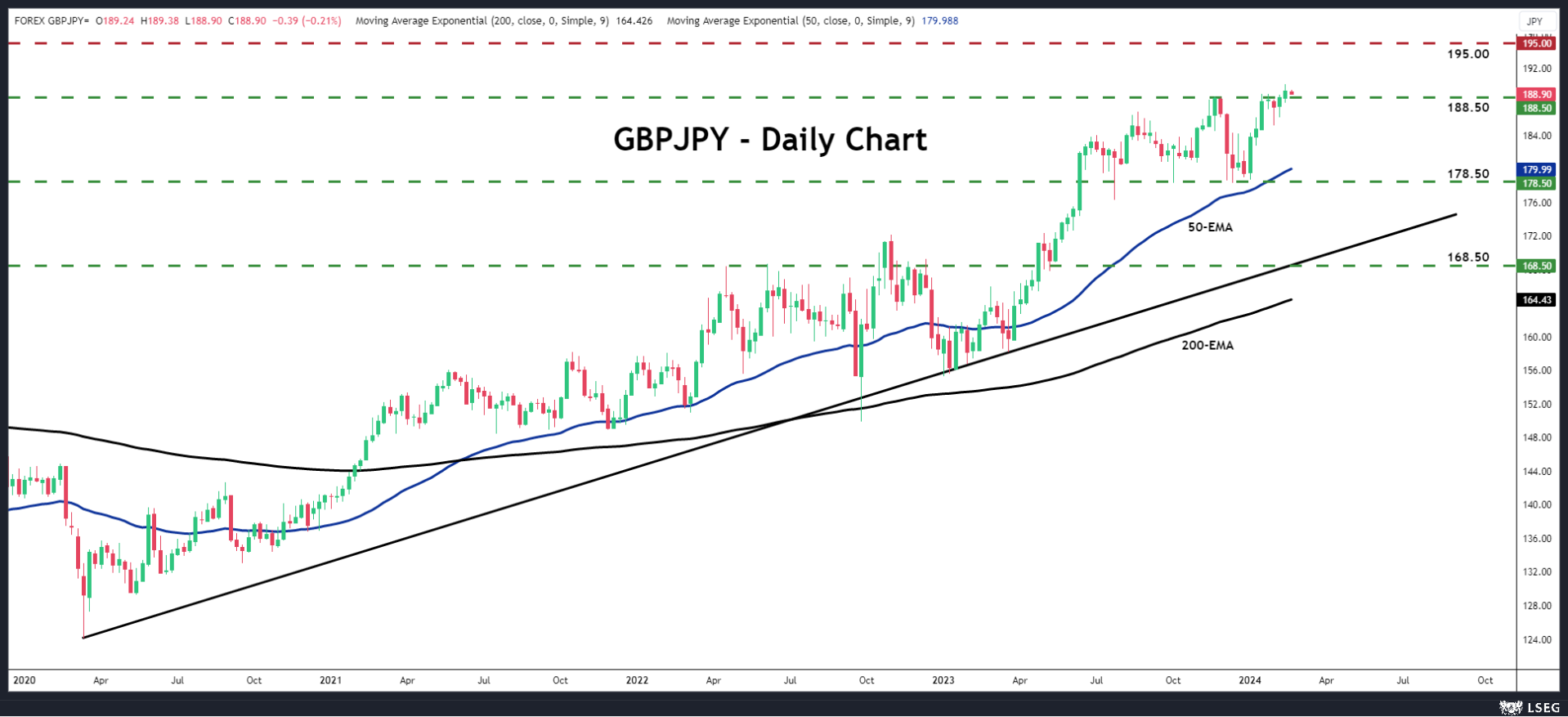

From a technical standpoint, pound/yen has been trading in a steep uptrend since March 2020. Last week, the pair confirmed a higher high, entering territories last tested back in the summer of 2015, suggesting that the bulls may be willing to continue marching north.

The pair may correct lower should the Japanese authorities step in to support the yen, but the retreat may remain limited and short-lived if the BoJ keeps pushing against speculation of a rate hike soon and if data continues to suggest that the UK economy has turned the corner. The next area to consider as a potential resistance may be at around 195.00, near the highs of July and August 2015. For the outlook of this pair to change, a dive all the way below 178.50 may be needed.

AUD: Trade Ideas

Last Tuesday, the Australian dollar experienced its steepest drop of the year, falling by 1.18%, following higher-than-expected US inflation figures, which boosted the US dollar. However, the Aussie has since rebounded and is now trading at a two-week high against the US dollar. Investors are eagerly awaiting the release of the Reserve Bank of Australia's meeting minutes on Tuesday, after the RBA opted to maintain the cash rate at 4.35% in February. Despite speculation about future rate cuts, the RBA has expressed concerns about persistent inflation not reaching the target range of 2%-3% until 2025. With last week's employment report disappointing expectations, attention now turns to Wednesday's wage price index report, which could influence the likelihood of RBA interest rate hikes.

GBPAUD - H4 Timeframe

GBPAUD has recently been rejected off the supply zone on the weekly timeframe, and following this, the price action has created a break of structure to the downside. In light of this, I will be waiting for the price action to complete a retest of the trendline, and then the bearish move can resume. The Fibonacci retracement levels and the trendline resistance are my confirmations for this sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.90905

- Invalidation: 1.95313

EURAUD - D1 Timeframe

EURAUD has just been rejected from the 76% of the Fibonacci retracement level, with the trendline resistance serving as additional confirmation for the bearish direction. I expect to see price drop all the way to 23% as the initial target for this sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.62871

- Invalidation: 1.67623

AUDCHF - D1 Timeframe

AUDCHF on the daily timeframe is currently approaching the 76% Fibonacci retracement level. The notable confluences in this case are the trendline resistance, supply zone, as well as the 200-day moving average resistance. My initial target here is the 23% of the Fibonacci retracement.

Analyst’s Expectations:

- Direction: Bearish

- Target: 0.56816

- Invalidation: 0.58681

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

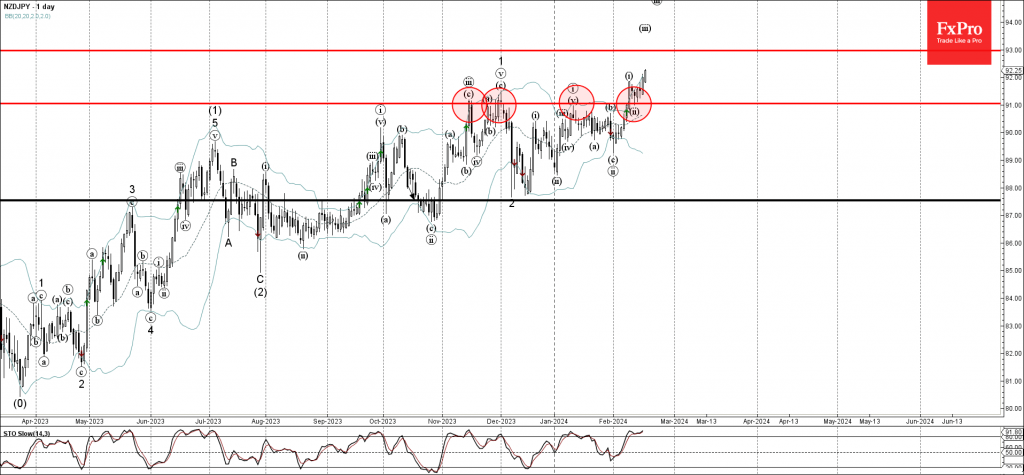

NZDJPY Wave Analysis

- NZDJPY reversed from support level 91.00

- Likely to rise to resistance level 93.00

NZDJPY currency pair recently reversed up from the support level 91.00 (former resistance which has been reversing the price from November).

The upward reversal from the support level 91.00 started the active short-term impulse wave iii of the higher impulse waves 3 and (3).

Given the clear daily uptrend, NZDJPY currency pair can be expected to rise further to the next resistance level 93.00 target price from the completion of the active impulse wave iii.

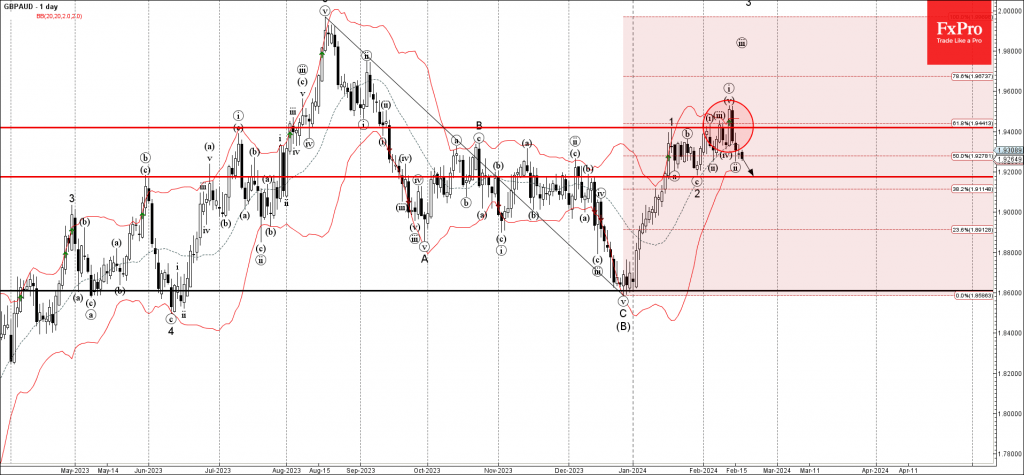

GBPAUD Wave Analysis

- GBPAUD reversed from resistance level 1.9400

- Likely to fall to support level 1.9200

GBPAUD currency pair recently reversed down from the resistance level 1.9400 (which has been repeatedly reversing the pair from the middle of January).

The downward reversal from the resistance level 1.9400 created the 3rd consecutive candlesticks reversal pattern Bearish Engulfing.

Given the continuation of the bearish sterling sentiment seen across the FX markets today, GBPAUD currency pair can be expected to fall further to the next support level 1.9200 (low of the previous correction 2).

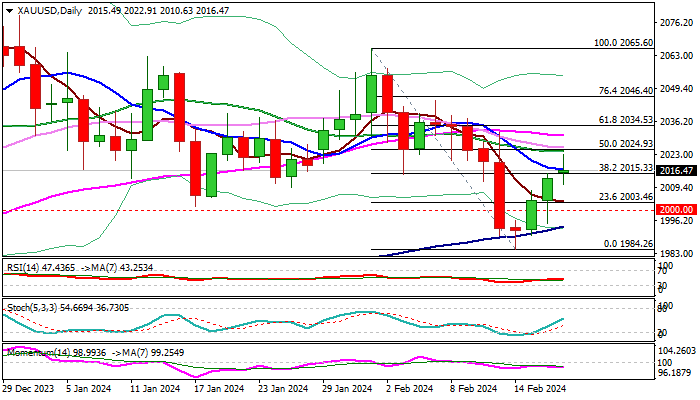

XAU/USD: Gold Extends Recovery Despite Sticky US Inflation

Recovery leg from $1984 (9-week low of Feb 14) extends into third straight day after short-lived probe below psychological $2000 level was contained by 100DMA and Morning Doji Star reversal pattern formed on daily chart.

Although the metal’s price gained pace and established above $2000, caution is still required as 14-d momentum is still in negative territory and a cluster of converged daily moving averages (20/30/55), just above the price (at $2024/30 zone), marks significant obstacle.

Gold price regained ground despite warning of sticky inflation (Friday’s higher than expected PPI numbers further worsened overall picture) and signals of prolonged period of unchanged interest rates, as investors remain optimistic and believe that this is a temporary phenomenon and inflation remains in a steady downward trajectory.

Recovery needs a sustained break above $2030 zone to confirm reversal signal and open way for $2050+ acceleration.

Today’s close above $2015 (cracked Fibo 38.2% of $2065/$1984 bear-leg) to further firm near-term structure, while bulls will be sidelined if the price returns below $2000 level.

Res: 2024; 2030; 2034; 2046.

Sup: 2010; 2000; 1992; 1984.

Sunset Market Commentary

Markets

A quiet weekend, uninspiring overnight Asian dealings, an all but empty economic calendar & US financial markets closed for Presidents’ Day. Those are the poor cards European market were dealt with at the start of the week. It doesn’t come as a surprise, then, to see German yields, the euro and European equities basically flatline. We’ve expanded the New & Views section for the occasion.

News & Views

Headline inflation in Sweden printed at -0.1% M/M and 5.4% Y/Y up from 4.4% (vs 5.0% expected). The preferred measure of the Riksbank, CPIF inflation (fixed interest rate) showed a similar picture (0.3% monthly decline but rebounding from 2.3% Y/Y to 3.3% Y/Y). However, the rise in the Y/Y measure was driven by unfavourable base effects due to a sharp decline in energy prices last year. The Riksbank probably will draw comfort from a further decline in core CPIF inflation excluding energy (-0.5% M/M and 4.4% from 5.3% in December). Monthly details showed a drop in prices for clothing (-8.3%), fuels (-10.8 %), international flights (-23.7%), package holidays (-12.7%) and accommodation services (-4.2%). This was partially counterbalanced by higher electricity prices (5.7% M/M), rents for housing (2.1 %) and interest rate expenses/owner occupied housing costs (1.5%). In its latest monetary policy report (Nov 2023), the RB forecasted CPIF inflation ex energy at 4.5% Y/Y, with the measure expected to return to the low 2% area H2 2024. In the statement after the February decision, the RB indicated that rates could be cut be sooner than initially expected, maybe already in H1. In this respect, the June meeting is/was on the radar. But for that option to materialize, the Fed (and the ECB) probably should be able to start their easing cycle in June (or early) as well. This is less evident after last week’s US data. The Swedish krone gains marginally (EUR/SEK 11.23) but is holding in a ST consolidation pattern between 11.20 and 11.43.

The recent rather sharp weakening of the koruna apparently is becoming a factor of growing importance at least for some members of Czech National Bank MPC. In an interview with Szenamzpravy.cz published on the CNB website, vice Governor Eva Zamrazilova indicated that if the exchange rate remains weaker than the levels expected by the CNB for the medium or longer term, it will have to cut rates at a slower pace. Czech January inflation last week expectedly printed at 1.5% M/M and 2.3% Y/Y (3.0% was expected by the CNB). This sharp slowdown in inflation further raised speculation that the CNB might step up the pace of rate cuts from 50 bps to 75 bps, especially as inflation might drop below the 2.0% target later this year. Last week, governor Michl already argued that while the CNB restored price stability, ongoing high core inflation, a high public deficit and a weaker-than-expected koruna are good arguments for the CNB to lower interest rates only cautiously. In this respect, the bar for 75 bps steps probably remains high. At EUR/CZK 25.45, the koruna is holding near the weakest levels since March 2022.

French Finance Minister Le Maire yesterday brought some bad news regarding the EU’s second-largest economy, lowering this year’s growth forecast to a meagre 1%. Germany’s Bundesbank today issued a similarly depressing message about Europe’s N° 1. Its monthly report projected another economic contraction in the first three months of the year. With the economy having shrunk 0.3% in 2023Q4 it would put Germany in a technical recession. The Bundesbank blamed several factors including uncertainty over fiscal policy since the constitutional court ruling banning the use of off-budget financing vehicles caused a budgetary shockwave reaching in the tens of billions. Economy Minister Habeck last week said this will cripple growth in the updated forecasts (due Wednesday) to just 0.2% this year. The BuBa also highlighted ongoing weak domestic and foreign demand, production hit by train and airport strikes, depleting order books in the industry and construction & dampened investments amid higher borrowing costs. However, the economy should gain traction later this year against the background of a stable labour market and (real) wages rising sharply. The dire message comes ahead of the February PMI’s later this week. These forward looking indicators are projected to still signal an economic contraction (<50) but to improve marginally, extending (manufacturing, from 45.5 to 46) or initiating (47.7 to 48) a bottoming out process, be it an extremely gradual one.

Subdued Trading and Anticipation for RBA Minutes

Activity in the global financial markets are rather muted today, with major European stock indexes reading water within a narrow range. US futures are also showing little change, reflecting the quietness of US market holiday. In the currency sphere, movements are similarly subdued, with Euro and Swiss Franc ranking as the day's weaker currencies followed by Dollar. Kiwi, Aussie, and Yen are having relative strength. Sterling and Swiss Franc find themselves positioned in the middle, presenting mixed performance.

The upcoming Asian trading session, however, promises an uptick in market volatility, with release of RBA minutes highly anticipated. At its February board meeting, RBA maintained official cash rate at 4.35%, aligning with market expectations. Notably, the central bank chose not to abandon its tightening bias. Governor Michele Bullock's stance, that another rate hike remains a possibility but is not definitively on the cards, has sparked keen interest. The forthcoming minutes are expected to shed light on whether an additional hike was seriously considered and the degree of contention surrounding this decision.

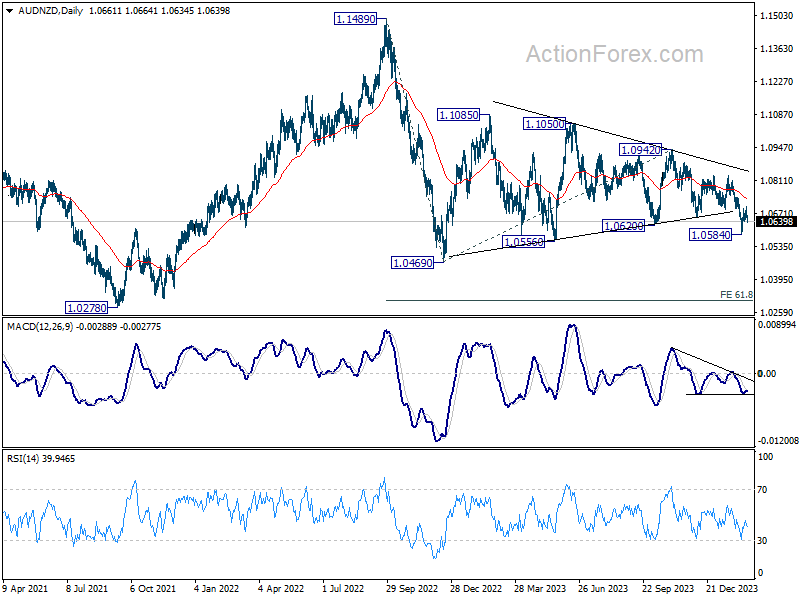

Technically, AUD/NZD recovered after dipping to 1.0584 earlier in the month. But there is no change in the bearish outlook with 55 D EMA (now at 1.0735) intact. Deeper decline is expected and break of 1.0584 will target 1.0469 (2022 low). Firm break there will resume whole down trend from 1.14879 (2022 high).

In Europe, at the time of writing, FTSE is up 0.15%. DAX is down -0.28%. CAC is down -0.19%. UK 10-year yield is down -0.0074 at 4.107. Germany 10-year yield is up 0.009 at 2.417. Earlier in Asia, Nikkei fell -0.04%. Hong Kong HSI fell -1.13%. China Shanghai SSE rose 1.56%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield fell -0.0004 to 0.730.

Bundesbank: Weak German economy but no significant, broad-based and long-lasting decline

In its latest monthly report, Bundesbank acknowledged that the "weak phase" in the German economy since Russian war of aggression against Ukraine would continue.

Despite this, it stops short of predicting a recession, defining it as a "significant, broad-based and long-lasting decline in economic output."

The report further elaborates, indicating "no signs of an impending noticeable deterioration" in the labor market stemming from the current economic slowdown.

On the inflation front, Bundesbank anticipates continued decline in inflation rates in the coming months, with price pressures on food and other goods expected to ease further. Nonetheless, the report signals slower pace of decline in service sector inflation, attributing this trend partly to "continued strong wage growth."

NZ BNZ services rises to 52.1, springs back to growth

New Zealand's BusinessNZ Performance of Services Index rose from 48.8 to 52.1 in January, marking its highest peak since May 2023. This rebound places the sector back into expansion, albeit slightly below long-term average of 53.4.

Components of the PSI showed notable improvements: activity/sales surged to 53.0 from 47.2, employment edged up to 48.1 from 47.2, new orders/business increased to 51.8 from 50.8, and stocks/inventories rose to 53.5 from 51.7. However, a decrease in supplier deliveries to 48.7 from 50.3 hints at logistical challenges.

Reflecting on the sector's performance, BusinessNZ's chief executive, Kirk Hope, remarked on the "seesaw" trend between expansion and contraction observed in recent months. He highlighted that the sector's sustained recovery hinges on "continued momentum" in business activity and new orders, coupled with alleviation in "cost of living" pressures.

BNZ Senior Economist Doug Steel provided an optimistic outlook, suggesting that the combined PMI and PSI activity indicator hints that "annual GDP growth will soon turn positive." Yet Steel cautioned that further progress is essential to mitigate growing spare capacity within the economy.

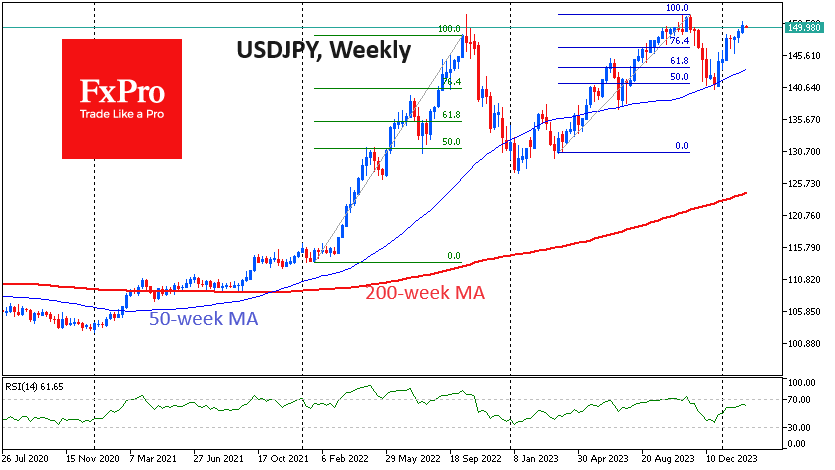

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.81; (P) 150.23; (R1) 150.63; More...

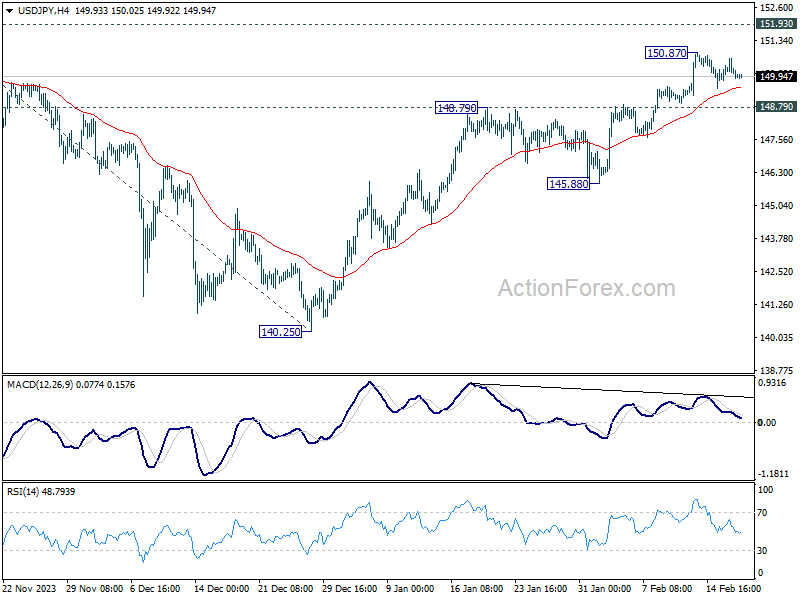

USD/JPY is extending the consolidation from 150.87 and intraday bias remains neutral. Downside of retreat should be contained by 148.79 resistance turned support to bring another rally. Above 150.87 will resume the rise from 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. However, firm break of 148.79 will turn bias to the downside for 145.88 support.

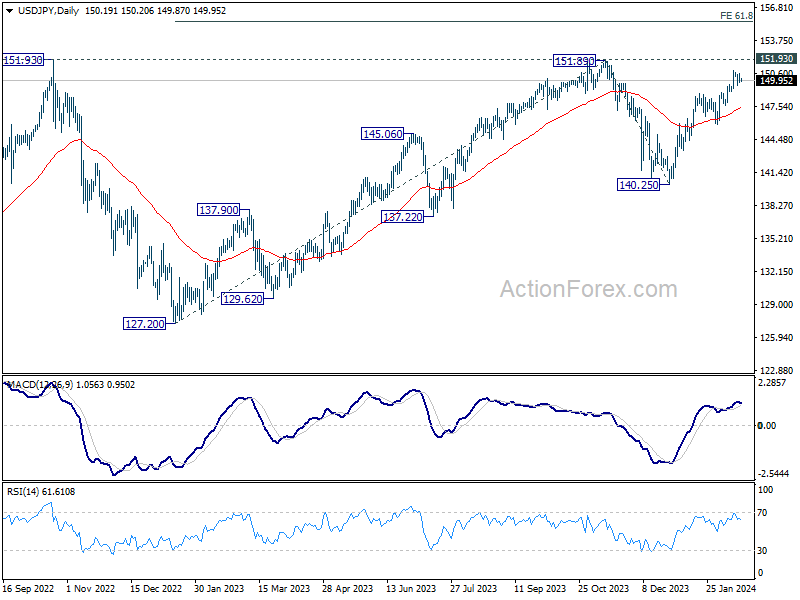

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Jan | 52.1 | 48.8 | ||

| 23:50 | JPY | Machinery Orders M/M Dec | 2.70% | 2.50% | -4.90% | |

| 00:01 | GBP | Rightmove House Price Index M/M Feb | 0.90% | 1.30% | ||

| 11:00 | EUR | German Buba Monthly Report | ||||

| 13:30 | CAD | Industrial Product Price M/M Jan | -0.10% | 0.10% | -1.50% | |

| 13:30 | CAD | Raw Material Price Index Jan | 1.20% | 0.80% | -4.90% |

Yen Bears Have a Good Chance of Reaching Lows Not Seen Since 1990

The Japanese yen is hovering near 150 per dollar, retreating from last week’s four-month highs of 151. The 150-152 area is hazardous for short-term traders, as this is the level from which the Japanese Ministry of Finance intervened in October 2022 and November 2023 to stop the currency from depreciating.

However, it would be too naive to expect a reversal from 151.8, as it has happened several times before. A weaker yen makes Japanese exports more competitive and thus stimulates the economy. In addition, the currency’s weakness fuels imported inflation and puts downward pressure on prices.

By using this tool moderately, the country’s finance ministry and central bank can address their long-term problem of a stagnant economy and deflation. The momentum of the yen’s depreciation in 2022 was excessive, exceeding 30 per cent in seven months. Interventions and the unwinding of long positions in the market have given the yen back about half of this decline.

The second wave of pressure started in March 2023 and lasted about seven months, taking USDJPY back to the peak of the previous cycle. This time, it is harder to say whether we saw intervention or whether the market switched to buying the yen as the outlook for the dollar changed sharply. As with the first wave, the pullback has lost strength, giving back about half of the initial move, or about 7.5%.

The current phase of USDJPY gains began in early January and is taking the yen to extremes before the beginning of March. At the same time, bets on further Yen weakness have risen to their highest levels in over two years. This extreme positioning creates a breeding ground for a downside move, as is the case with such counter-trend strategies.

The yen’s growth impulses have allowed the economy to adjust, so there is no need to defend precisely the 152 level. USDJPY is now 14% higher than a year ago. This is not a critical drop. In our experience, officials start to get worried about exchange rate movements when they approach 20% year-on-year.

In the case of the yen, one should be prepared for neither the Bank of Japan nor the Ministry of Finance to refrain from active action and perhaps even verbal intervention until the 160 yen/$ level, which is the next round level coinciding with the 1990 peak.

Officials may allow the yen to weaken thanks to slower inflation and lower commodity. Japan’s economy has contracted for the past two quarters, suggesting a need for support. Meanwhile, the outperformance of the stock market suggests confidence that the economy is not overly burdened by exchange rate volatility and will soon benefit from more competitive prices for its goods.