Sample Category Title

Fed’s Barkin endorses patience regarding rate cuts

Richmond Fed President Thomas Barkin has voiced a call for patience concerning interest rate cuts, in the face of prevailing economic uncertainties.

"I am very supportive of being patient to get to where we need to get," Barkin articulated during an event overnight.

Barkin highlighted the ongoing efforts to combat inflation, acknowledging that while progress has been made towards balancing the trade-offs between economic growth and inflation control, "a reasonable amount of uncertainty" remains.

He pointed out that the inflationary challenges are not confined to goods alone but extend to services and rental sectors.

"Declaring victory is very enticing, but you're never going to hear me do that," Barkin asserted.

Fed’s Collins: Sustained, broadening inflation progress needed before methodical policy relaxation

Boston Fed President Susan Collins emphasized the need for "sustained, broadening signs of progress" in inflation reduction before contemplating any "methodical" adjustments to interest rate policy.

"As we gain more confidence in the economy achieving the Committee's goals... I believe it will likely become appropriate to begin easing policy restraint later this year," she stated in a speech overnight.

She advocates for a gradual approach to interest rate adjustments, allowing for "flexibility to manage risks, while promoting stable prices and maximum employment."

Collins also highlighted the resilience of the US economy, as evidenced by recent GDP and labor market data, suggesting that the anticipated slowdown in economic activity "may take some time".

"The path the economy takes toward the Fed's mandated goals may continue to be bumpy and uneven, and we should not overreact to individual data points," she advised.

A critical factor in Collins's assessment is wage dynamics, with a specific interest in wage trends that align with long-term price stability. While acknowledging that not all economic indicators might perfectly converge, "seeing sustained, broadening signs of progress should provide the necessary confidence I would need to begin a methodical adjustment to our policy stance."

Fed’s Kugler highlights inflation risks stemming from consumer behavior, job market, and global tensions

In a speech overnight, Fed Governor Adriana Kugler said she's satisfied with the disinflationary progress, and expects it to "continue". However, she was quick to temper this optimism with a note of caution, emphasizing that Fed's work in combating inflation is far from over. The unpredictability of consumer behavior stands as a reminder of unforeseen developments to "slow progress on inflation."

Kugler also pointed to the recent employment report, which showed unexpected strength. While a strong labor market is generally a positive sign, in the context of Fed's efforts to cool inflation, such robustness could complicate the path to achieving a balanced demand-supply equation in both product and labor markets.

Fed Governor underscored the importance of monitoring geopolitical risks, particularly highlighting how the ongoing conflict in Ukraine and tensions in the Middle East could exacerbate inflationary pressures through "higher commodity prices" and global trade "disruptions", "in turn pushing up goods inflation in the US".

"At some point, the continued cooling of inflation and labor markets may make it appropriate to reduce the target range for the federal funds rate," she noted. Conversely, "if progress on disinflation stalls, it may be appropriate to hold the target range steady at its current level for longer to ensure continued progress on our dual mandate."

GBP/USD – A Bearish Reversal at a Key Fib Level?

- Fed policymakers sticking to the script

- US data continues to point to a strong economy

- Fib rebound may suggest we’ve seen a correction in GBPUSD

It isn’t the busiest week as far as UK and US economic data is concerned but there are still a few pieces worth keeping an eye on. As well as, of course, the scattering of central bank speak.

So far, policymakers appear to remain consistent with the message from the last meeting despite Friday’s surprisingly strong jobs report.

The services PMI on Monday was also far better than expected, further supporting the view that the economy is far from suffering under the weight of high interest rates.

Have we just seen a correction in GBPUSD?

But perhaps it’s the technicals that could prove to be more interesting this week.

GBPUSD Daily

Source – OANDA

On Monday the pair broke below the neckline of a quadruple top formation around 1.26. While it has since pulled back, it could just be a corrective move and the rotation off the 50% Fibonacci retracement level today may support that view.

GBPUSD 4-Hour

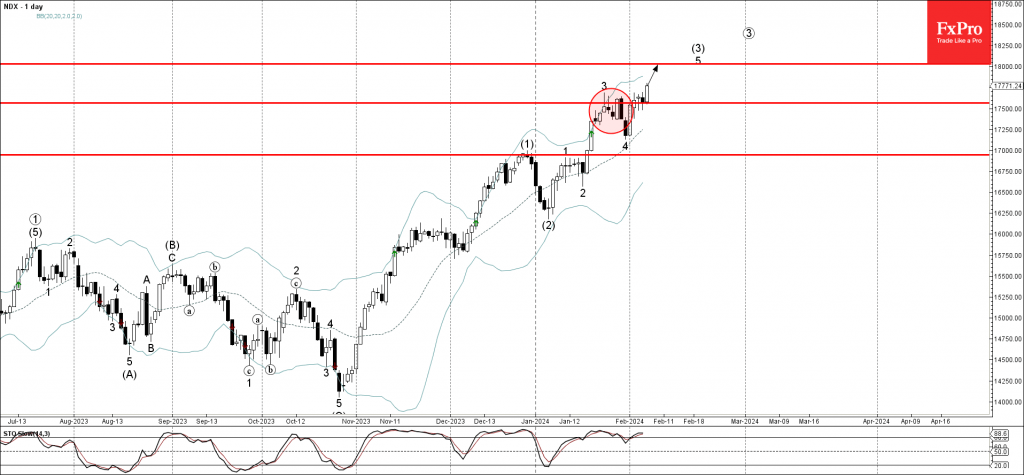

Nasdaq-100 Wave Analysis

- Nasdaq-100 rising inside impulse wave 5

- Likely to rise to resistance level 18000.00

Nasdaq-100 index rising steadily after the price reversed up from the support level 17565.00, former resistance which stopped wave 3 in January.

The upward reversal from the support level 17565.00 continues the active impulse wave 5 of the intermediate impulse sequence (3) from the start of the year.

Given the clear daily uptrend, Nasdaq-100 index can be expected to rise further to the next resistance level 18000.00, target for the completion of the active impulse wave 5.

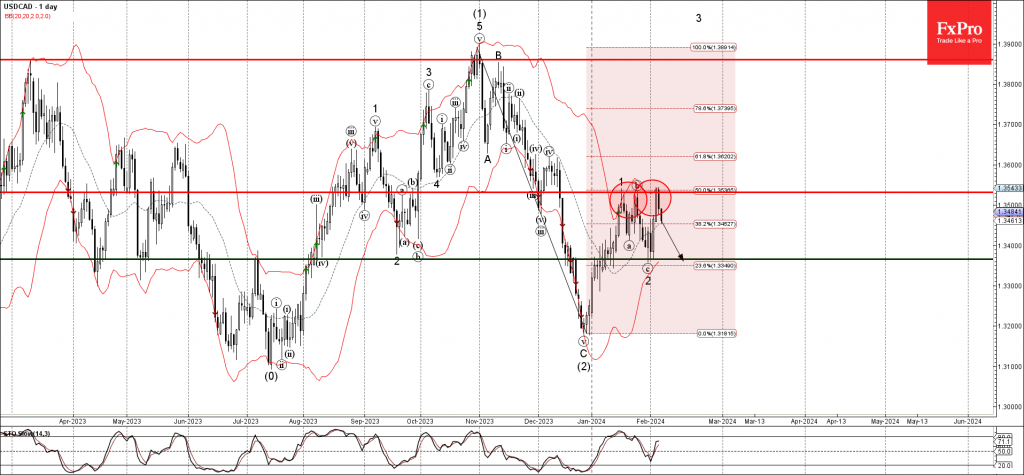

USDCAD Wave Analysis

- USDCAD reversed from resistance level 1.3530

- Likely to fall to support level 1.3365

USDCAD currency pair recently reversed down from the resistance level 1.3530, which stopped waves 1 and (b) in the middle of January.

The resistance level 1.3530 was strengthened by the upper daily Bollinger Band and by the 50% Fibonacci correction of downward ABC correction (2) from October.

Given the strength of the resistance level 1.3530, USDCAD can be expected to fall further to the next support level 1.3365, low of the previous correction 2.

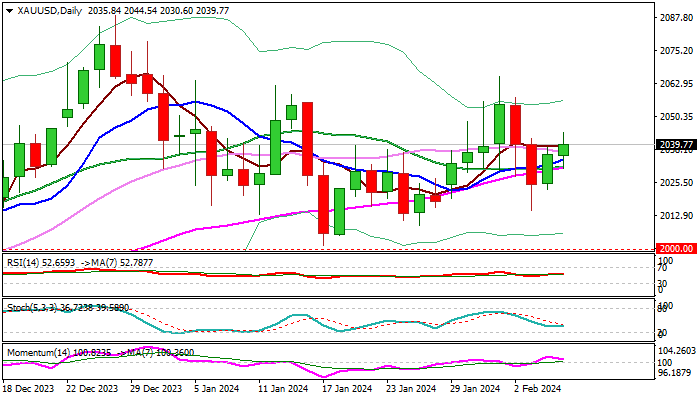

XAU/USD: Gold Remains in Prolonged Consolidation Before Larger Bulls Resume

Short-term action remains in a sideways mode after the metal’s price spiked to new record high ($2141) in early December, holding within $1973/$2088 range, but mainly above psychological $2000 level, which adds to positive bias.

Gold is consolidating after Oct-Dec 2023 18% advance, a part of larger uptrend from $1616 (Nov 2022 higher low) with strong prospects for further gains, as growing global geopolitical tensions, economic uncertainty and signals that the Fed considers interest rates cuts later this year, continue to keep demand for safe-haven bullion steady.

The price is likely to continue to fluctuate within current range, awaiting fresh signals from fundamental side as technical studies on all larger timeframes remain bullishly aligned and contribute to positive outlook.

Gold can rise towards Fibonacci projections at $2206/26, on firm break of $2141 peak, with extension towards $2300 zone expected on stronger acceleration.

Res: 2056; 2065; 2088; 2100

Sup: 2014; 2009; 2000; 1985

Australia & New Zealand: What’s Up For The Down Under Economies?

Summary

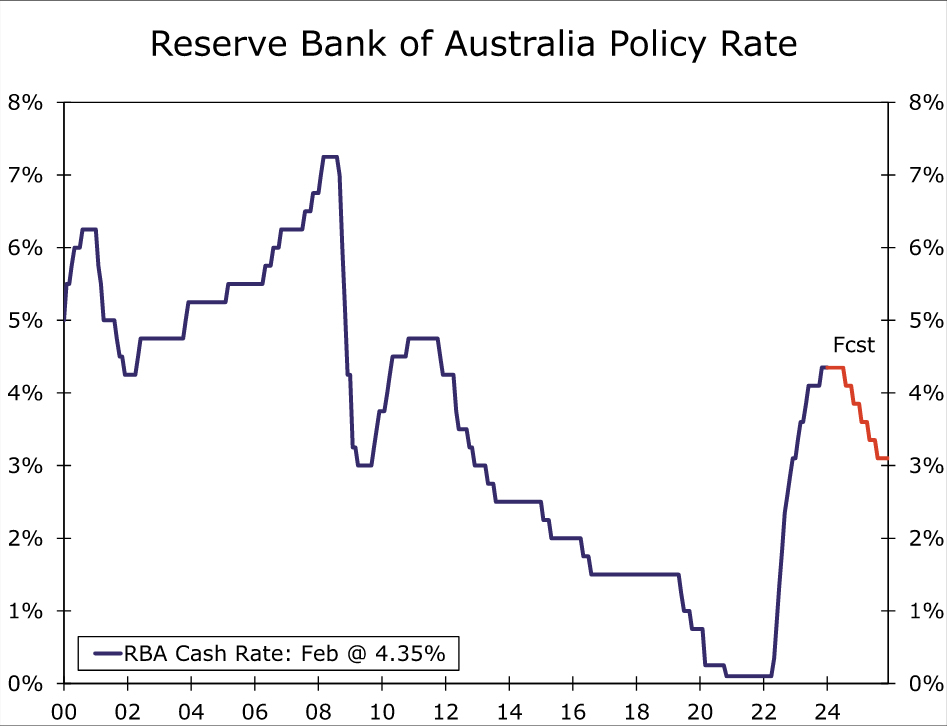

- The Reserve Bank of Australia (RBA) held its policy rate steady at 4.35% this week as expected, and its accompanying announcement was more hawkish than expected. The RBA did not rule out a further increase in interest rates, saying inflation—especially services inflation—is still high.

- We do not expect a further RBA rate increase, but with the central bank forecasting above-target inflation for an extended period, we believe rate cuts are some way off. We anticipate an initial 25 bps rate cut at the August meeting, while also acknowledging the balance of risks as tilted toward a later move.

- In New Zealand, improving sentiment surveys suggest the economy is moving toward recovery after a challenging 2023, while domestically oriented inflation pressures remain elevated. That backdrop is contributing to a continued hawkish stance from the Reserve Bank of New Zealand, which has not ruled out further rate hikes and said there is a way to go before inflation returns to target. We now see RBNZ rate cuts occurring later than previously envisaged, and forecast an initial 25 bps reduction at the August announcement.

- Against a backdrop of a U.S economic slowdown and Fed easing, a more gradual pace of rate cuts from the RBA and RBNZ could offer some support to the Australian and NZ dollars against the greenback over time.

Hawkish Hold From the Reserve Bank of Australia

The Reserve Bank of Australia (RBA) held its policy interest rate at 4.35% at this week's meeting, as widely expected. While acknowledging slower growth and improving inflation trends, the RBA is nonetheless clearly wary of reducing interest rates prematurely. This is reflected in several elements of its announcement:

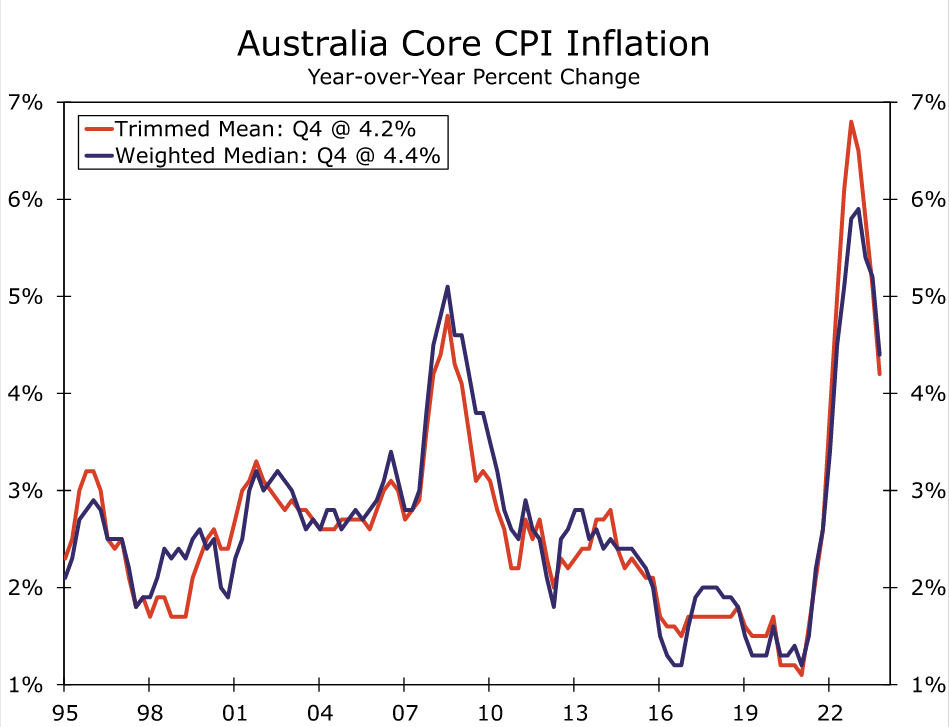

- Inflation remains high at 4.1 per cent. Goods inflation has slowed, but services inflation has declined at a more gradual pace, consistent with continuing excess demand and strong domestic cost pressures.

- The RBA remains highly attentive to inflation risks.

- While conditions in the labor market continue to ease gradually, they remain tighter than is consistent with sustained full employment and inflation at target.

- The RBA expects it will be some time yet before inflation is sustainably in the target range of 2%-3%. The path of interest rates that will best ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks, and a further increase in interest rates cannot be ruled out.

Importantly, therefore, the RBA kept the possibility of a rate increase on the table, even as it lowered both its GDP growth and CPI inflation forecasts. With respect to economic activity, the RBA now forecasts annual average GDP growth of 1.5% for 2024, down from the 1.8% it forecast in November. It also projects a slightly faster rise in the unemployment rate to 4.3% by the end of this year, compared to 4.2% previously. Meanwhile, despite a downside surprise for Australia's CPI in Q4-2023, inflation is expected to remain above the 2%-3% inflation target range for an extended period. Both headline inflation and trimmed mean inflation are not forecast to return to that target range until the end of 2025, and are not forecast to be at the midpoint of that range until mid-2026.

Keep in mind these forecasts are all predicated on the technical assumption of a policy rate path that is broadly consistent with market implied pricing, which sees the policy rate at 4.3% in mid-2024 and 3.9% by end-2024. Even with that technical assumption, however, the RBA projects inflation remaining above the target range for an extended period. In our view, given that RBA continues to highlight that "returning inflation to target within a reasonable timeframe remains the Board’s highest priority", at the very least that suggests rate cuts are unlikely to come before the second half of this year. That is, we view the RBA's announcement and forecasts as consistent with interest rate cuts starting in the second half of this year or later.

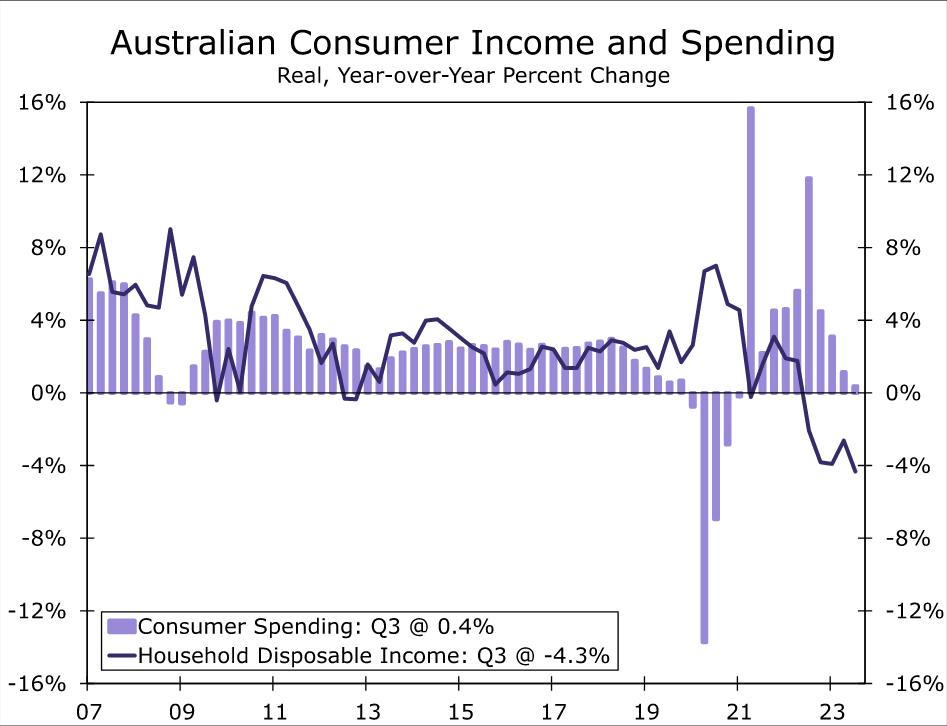

Against this backdrop, we doubt that sluggish economic growth will elicit early easing from Australia's central bank. The RBA has repeatedly highlighted an uncertain outlook for the consumer, uncertainty that is reflected in recent data. Q4 real retail sales rose a modest 0.3% quarter-over-quarter and, while that was better than expected, it was offset by a downward revision to Q3 sales. In fact, the increase in quarterly sales was the first since Q3-2022, and thus, in our view, represents more stabilization than strength in retail activity. In terms of consumer fundamentals, real household disposable incomes fell 4.3% year-over-year in Q3-2023 and the household saving rate dropped to just 1.1% of disposable income, arguing against a quick rebound in consumer spending. Perhaps on a more encouraging note however, tax cuts scheduled for 1 July have been adjusted to provide greater support to lower income earners, which should at least offer some support for consumer spending, and help to limit the extent of any slowdown in the overall economy.

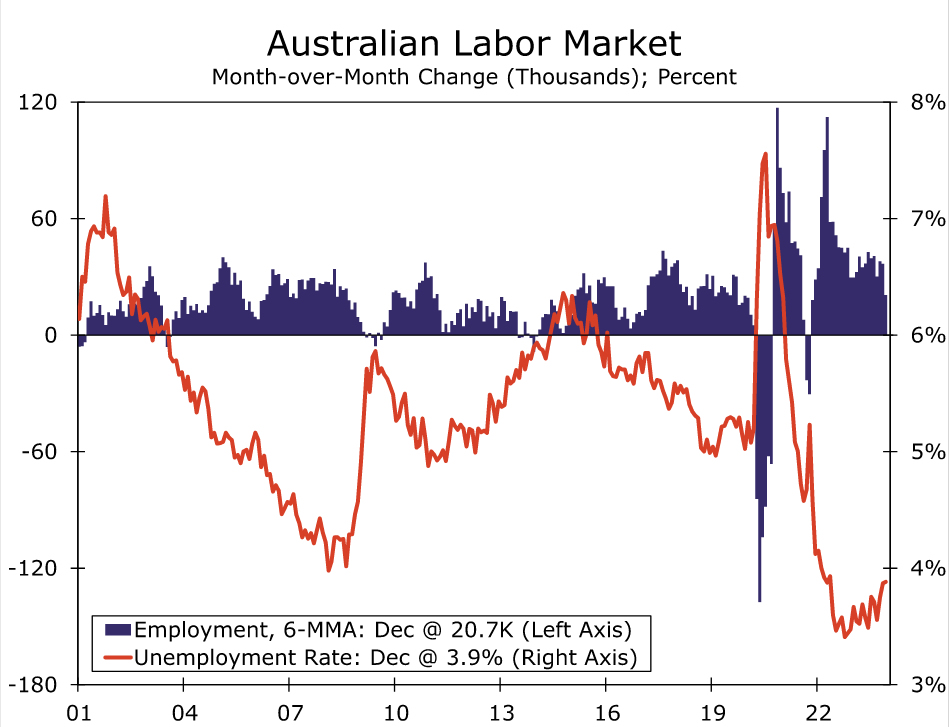

Even amid slow growth, the labor market has remained reasonably resilient so far. Employment has been particularly volatile in recent months, with a large December decline in jobs broadly offsetting a big November increase. Looking through that volatility, the average monthly employment increase slowed during the second half of last year to a still-respectable 20,700 per month. The unemployment rate has also increased to 3.9%, from as low as 3.4% in late 2022. While the labor market has loosened to some extent, we note that a further moderate increase in unemployment and slowing in wage growth (from the current 4.1% year-over-year for the Wage Price Index) would be in line with the RBA's forecast, and could make the central bank more comfortable that inflation is returning sustainably to the target range.

Accordingly, we think an initial RBA rate cut remains some way off. At this time, we remain comfortable with our outlook for an initial 25 bps rate reduction to 4.10% at the August monetary policy announcement, by which time the labor market will likely have softened further, and wage and price pressures will likely have moderated somewhat. We also expect the pace of rate cuts to be quite gradual even after that initial easing, at just 25 bps per quarter, which means the RBA's policy rate would not reach a low of 3.10% until the second half of 2025. While we see risks around this policy rate outlook in both directions, those risks are perhaps tilted toward a later rate cut than an earlier rate cut. Persistence in services or wage inflation could easily see an initial rate cut pushed back to Q4 of this year while, although it is not our base case, an especially sharp slowdown in consumer spending or inflation pressures could still prompt the RBA to move earlier than August.

The pace of monetary easing we forecast for the RBA, at least through the end of 2024, is broadly in line with that implied by market pricing. As mentioned, however, the risks are more heavily tilted toward a later move. Moreover, even our base case for an initial RBA rate cut in August sees Australia's central bank moving noticeably later than the Federal Reserve, where we expect an initial rate cut to occur in May. Overall, a gradual moderation of Australian economic growth and inflation that leads to only a gradual pace of monetary easing from the Reserve Bank of Australia should be supportive of the Australian dollar versus the greenback over time.

High Inflation and Recovering Economy Keeping New Zealand Central Bank Hawkish

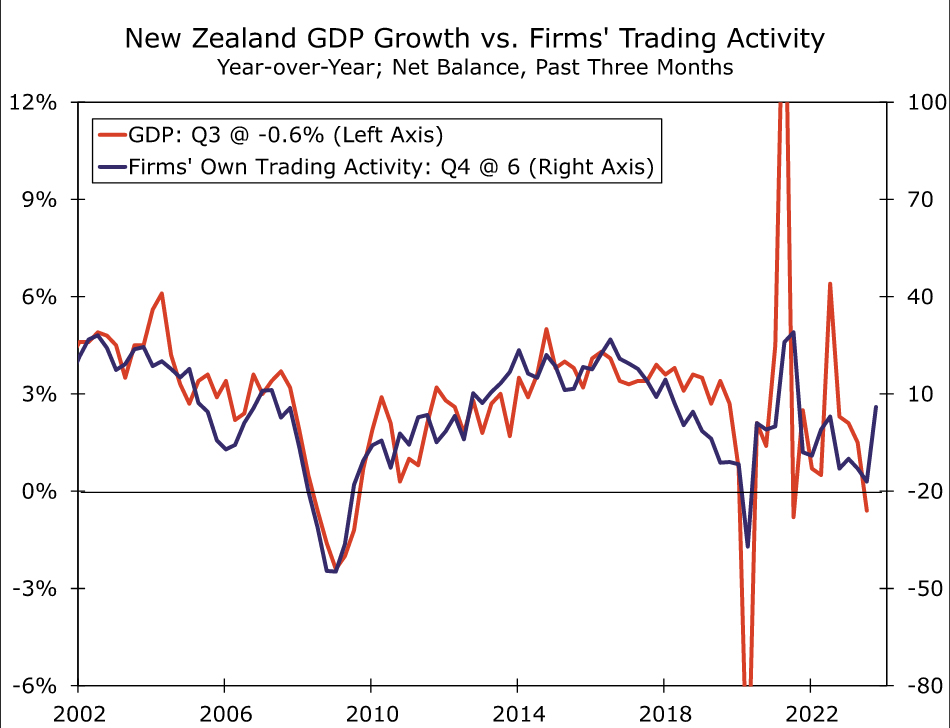

In New Zealand, the economy appears to be moving toward recovery after what was a challenging year through much of 2023. The impact of elevated inflation and the Reserve Bank of New Zealand's (RBNZ) aggressive monetary tightening contributed to GDP reporting sequential declines in three out of four quarters through Q3-2023, according to the latest available figures. Election-related uncertainty may have also provided a temporary restraint to growth late last year. Q3-2023 saw New Zealand's GDP fall 0.3% quarter-over-quarter and 0.6% year-over-year: economic underperformance that occurred even as immigration, and population growth, surged.

Some key economic headwinds facing New Zealand are now starting to abate; inflation has peaked, and we also believe the RBNZ has come to the end of its rate hike cycle. We think that should gradually allow for the economy to transition to a recovery phase, even if these key fundamentals have not turned to significant tailwinds just yet. That appears to be reflected in some available economic indicators for Q4 of last year. Most importantly, the Quarterly Survey of Business Opinion saw businesses become much less downbeat, as just a net 2% of businesses were pessimistic in Q4, compared to the net 52% of businesses who were pessimistic in Q3. Moreover, a net 6% of respondents reported an increase in their own trading activity in Q4, compared to net 17% who reported a decrease in Q3. This latter point is significant as, historically, it is firms' assessment of their own trading activity that has tended to be more closely correlated with overall GDP growth.

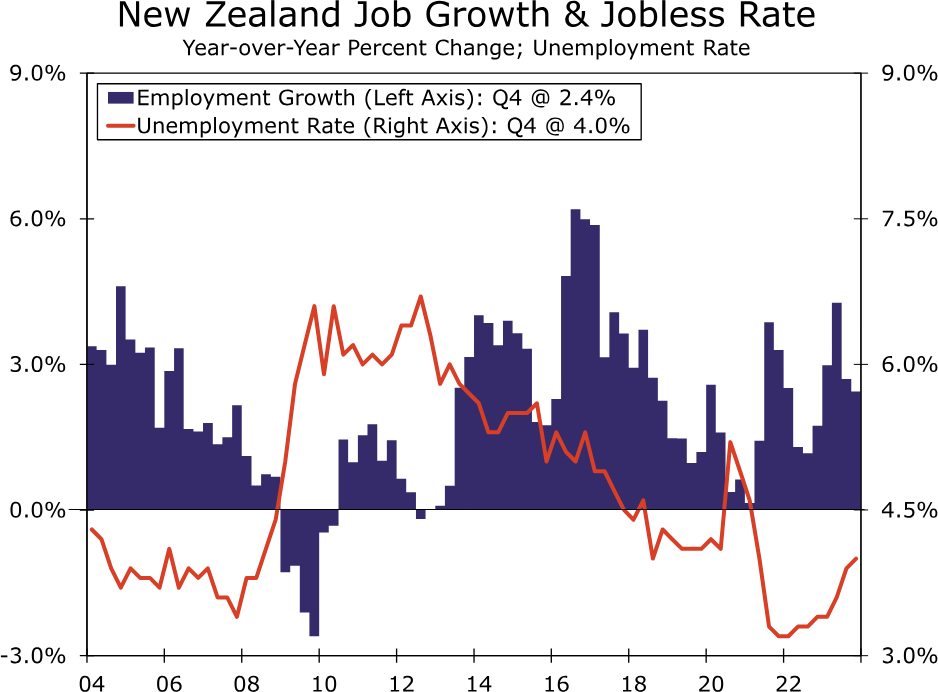

The improvement in sentiment in Q4 suggests that a gradual economic recovery may be upon us, a message that is also reflected in labor market data for the fourth quarter. Q4 employment rose 0.4% quarter-over-quarter, rebounding following a small decline in Q3, while employment was also up 2.4% year-over-year. The unemployment rate did edge higher to 4.0%, though in part, that stems from surging population growth. In fact, if anything, rising unemployment may help to place some restraint on wage pressures. The fourth quarter also saw the Labor Cost Index for the private sector rise to 1.0% quarter-over-quarter and ease to 3.9% year-over-year. Overall, we believe the New Zealand economy can enjoy a moderate recovery this year. We forecast GDP growth of 1.2% for 2024, which would be up from an estimated 0.8% growth in 2023.

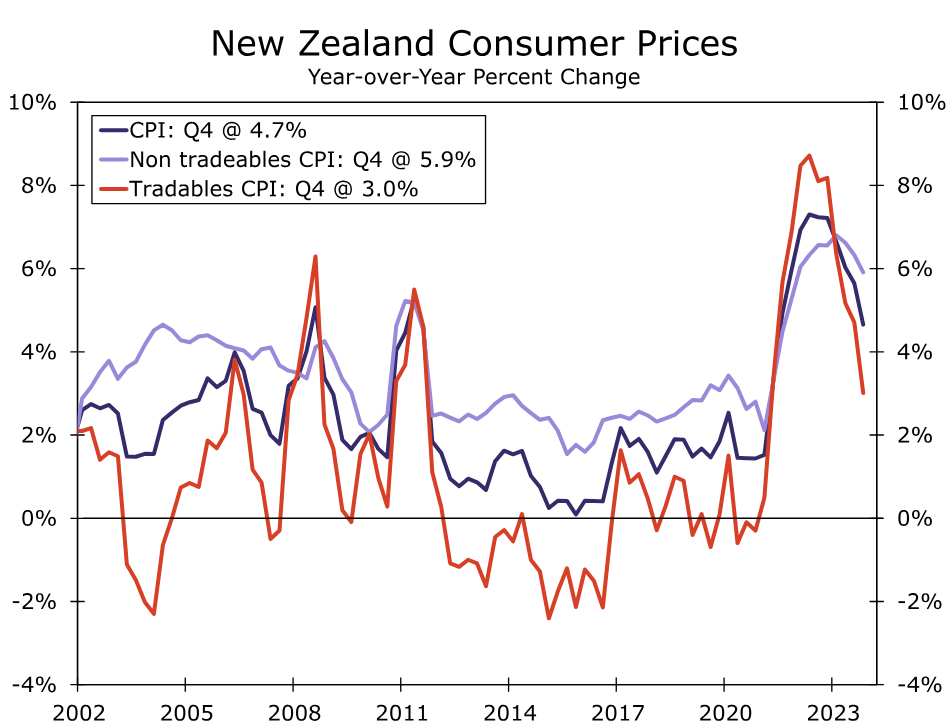

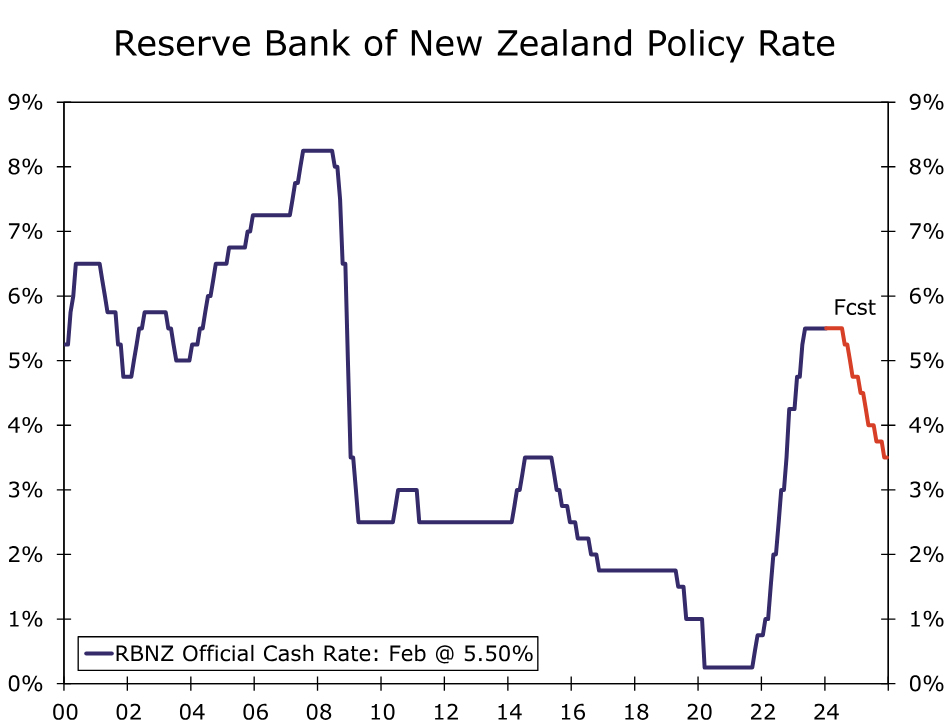

On the inflation front, consumer prices have started to recede, although domestically oriented inflation pressures remain persistent. Q4 CPI inflation slowed to 4.7% year-over-year, matching the consensus forecast. However, although tradeables inflation surprised to the downside and slowed to 3.0%, non-tradeables inflation surprised to the upside, with only a moderate slowing to 5.9%. Both headline inflation and, more particularly, domestically-oriented inflation, remain well above the central bank's 2% inflation target. As a result, the RBNZ has maintained a relatively hawkish monetary policy stance. At its most recent announcement in November, the RBNZ said that despite some decline, inflation remains too high, and policymakers maintain a wariness of inflationary pressures. In fact, the central bank said if inflationary pressures were stronger than expected, the policy rate would likely need to increase further. In more recent comments, RBNZ Chief Economist Conway offered additional hawkish comments. Conway said non-tradeables inflation was higher than expected and a long way from 2%, and that the central bank still has a way to go to get inflation back to target. Given the backdrop of improving sentiment, domestic inflationary pressures and a hawkish central bank, we now see RBNZ policy rate cuts occurring later than previously envisaged. We expect an initial 25 bps rate cut to 5.25% at the August announcement. Beyond that, we see a relatively steady pace of easing, with our forecast for a cumulative 75 bps of rate cuts in 2024, and a further cumulative 125 bps of rate cuts in 2025, which would see the RBNZ's policy rate reach 3.50% by the end of next year. Against a backdrop of a U.S economic slowdown and Fed easing, we believe a moderate rebound in NZ economic growth and gradual RBNZ monetary easing should see the New Zealand dollar enjoy moderate gains against the U.S. dollar over time.

What Impact Will Canada’s Employment Figures Have on Loonie?

- Canada’s economy likely added more jobs in January

- Ivey PMIs rises to its highest level in 9 months

- BoC summary of deliberations gets releasedon Wednesday

- Loonie rises ahead of Friday’s data due at 13:30 GMT

In Canada, a number of data releases are scheduled for this week. On Tuesday, the Ivey Purchasing Managers' Index (PMIs) came out, which will be followed by the summary of deliberations from the most recent Bank of Canada meeting on Wednesday. The report is analogous to the meeting minutes and will provide investors with a comprehensive record of the discussions that took place on January 24. On Friday, the employment data for January will determine if the upward trajectory of the jobless rate persists.

BoC’s Macklem speaks ahead of BoC summary of deliberations

Tiff Macklem, the Governor of the Bank of Canada, is defining the boundaries of monetary policy by cautioning that the central bank cannot address issues like housing affordability through adjustments in interest rates.

In his prepared remarks delivered in Montreal on Tuesday, Macklem asserts that historical evidence demonstrates the considerable efficacy of monetary policy in managing inflation over the medium term. However, the governor acknowledges that the system also has constraints, such as its incapacity to tackle immediate price changes.

As most people expected, the Bank of Canada kept the goal for its overnight rate at 5% for the fourth time in a row in January. This meant that the cost of borrowing money was at its highest level in 22 years. The Governing Council said that it is still worried about the risks to the outlook of inflation, especially the risks to underlying price growth after preferred core inflation gauges unexpectedly rose in December.

This means that tight monetary policy will stay in place. Headline inflation is expected to stay around 3% for the first half of the year, according to the central bank. It will then start to drop to the 2% goal in 2025. Even though tight policy has caused the economy to slow down, interest rates have stayed high. The Bank said that consumers have cut back on spending, business investment has decreased, and job market conditions have become more balanced.

Ivey PMIs hit highest level since April

According to Tuesday's Ivey Purchasing Managers Index (PMI) statistics, economic activity in Canada accelerated in January to its fastest pace in nine months.

The seasonally adjusted index rose from 56.3 in December to 56.5 in January, reaching its highest point since April. The Ivey PMI is a monthly indicator that tracks economic activity as reported by a group of Canadian purchasing managers. An increase in activity is indicated by a value above 50.

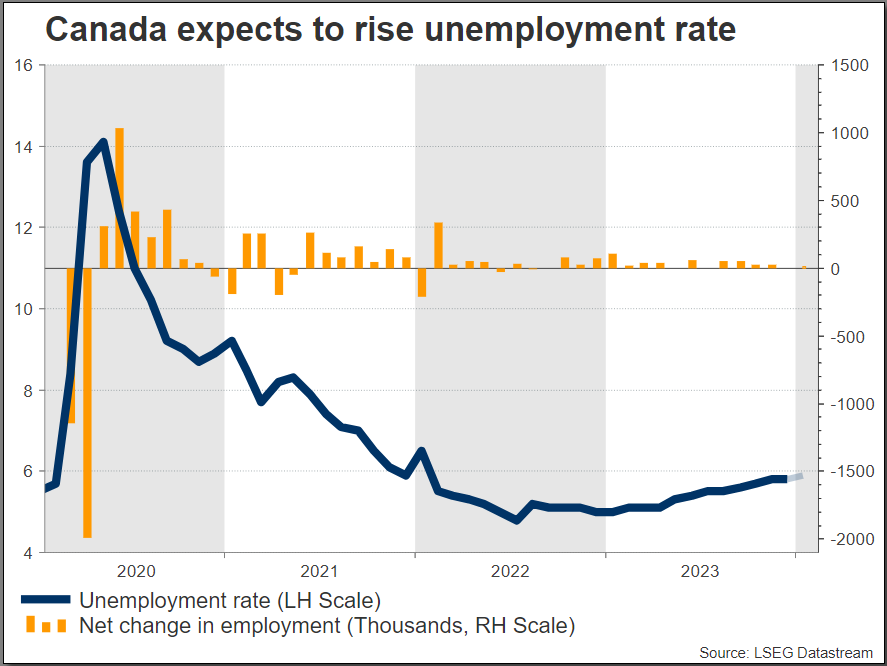

Canada’s unemployment rate expected to tick up

In December 2023, Canada's jobless rate stayed at 5.8%, the same as the 22-month high recorded the previous month. It was a little lower than the forecast of 5.9%, but it's expected to rise to 5.9% in January.

Notably, the indicator has exhibited a gradual upward trend since April, and a continuation in this direction could bolster demands for earlier reductions in borrowing costs.

Canada's employment level went up by 0.1k in December, after going up by 24.9k in November. This was less than the 13.5k growth that was expected. Based on this month's report, it is expected to add 15.0K jobs in January.

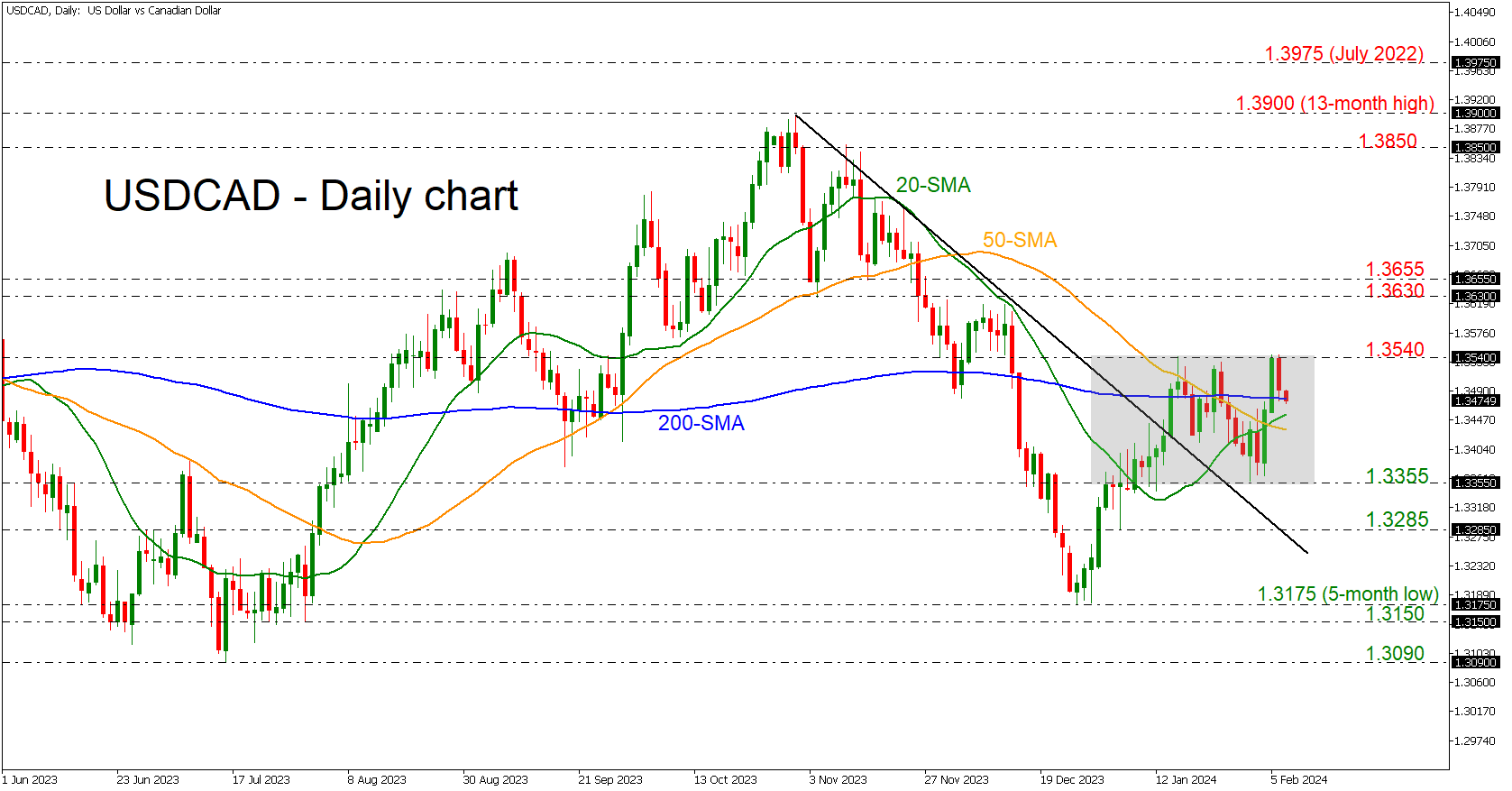

USDCAD loses ground in sideways channel

USDCAD loses ground in sideways channel

If the data indicates a slowdown in the economy, it is possible that USDCAD will stay above its simple moving averages (SMAs), which have been limiting upward movements around the 1.3400 level. More precisely, if the price surpasses the current resistance level of 1.3540, which is currently operating as the upper boundary of a short-term consolidation range between 1.3355 and 1.3540, it might potentially reach the restrictive zone of 1.3630-1.3655.

If the bears manage to push the price below the 1.3355 support level, selling pressure might increase below the 1.3285 area, approaching the five-month low of 1.3175.