Sample Category Title

Silver Recovers But Picture Still Cautiously Negative

- Silver prices bounce back after seven-week decline

- Momentum oscillators around their neutral levels

- Break either above 24.60 or below 21.90 would signal direction

Silver prices have risen over the last week, breaking above a downtrend line to recover a small chunk of the losses from the selloff that started in early December. That said, the structure of lower highs and lower lows is still in force and the market is also trading below its key moving averages, which suggests that the outlook remains cautiously negative.

Momentum oscillators are near their neutral levels, providing no indications about what comes next. The RSI has flattened close to its 50 line, and while the MACD is above its red trigger line, it’s still in negative territory.

If buyers remain in control and pierce above the 23.25 level, an even bigger battle would probably wait for them slightly higher at 23.55, which is roughly where the 50- and 200-day simple moving averages (SMAs) have converged. Another successful break could open the door towards the 24.60 zone, defined by the top in late December.

On the downside, sellers would need to penetrate below the 22.50 region, and even more importantly below the latest low of 21.90, to signal a resumption of the recent downtrend.

All told, the recovery in silver prices is unconvincing so far. A new high above 24.60 could change that, while in contrast, a clean break below 21.90 would signal further losses.

British Pound Edges Lower as Shop Inflation Drops

The British pound is lower on Tuesday. In the European session, GBP/USD is trading at 1.2680, down 0.23%.

UK shop inflation decelerates sharply

Inflation in UK shops rose 2.9% y/y in January, compared to 4.3% in December. This was the lowest pace since May 2022. This was an encouraging sign after consumer price inflation surprised by ticking higher to 4.0% in December, up from 3.9% a month earlier. Retailers are enticing shoppers with discounts, which has helped to lower inflation. Still, The Christmas shopping season was weak as consumers are holding back on spending due to the cost-of-living crisis.

The Bank of England meets next on Thursday and is likely to maintain the benchmark rate of 5.25% for a fourth straight time. The rate-hiking cycle is likely over, although the BoE is likely to continue its “higher for longer stance” and keep rates in restrictive territory until inflation falls closer to the 2% target. Services inflation and wage growth are both above 6% and the Bailey & Co. will want to see these numbers drop before cutting rates.

The markets were exuberant in December about rate cuts, pricing in six cuts in 2024, starting in May. The markets have since tempered expectations and have priced in four cuts this year, with the odds of a May cut around 50%, but more likely in August. The central bank hasn’t sent out any signals about rate cuts, but at the Thursday meeting, Governor Bailey might choose to soften the pushback against rate cuts expectations without endorsing rate cuts.

The US will release employment and consumer confidence data later in the day, with mixed readings expected. JOLTS Job Openings is expected to drop to 8.75 million, down from 8.79 million, while CB Consumer Confidence is projected to rise to 115 in January, up from 110.7 in December.

GBP/USD Technical

- GBP/USD is testing resistance at 1.2740. Next, there is resistance at 1.2772

- There is support at 1.2711 and 1.2679

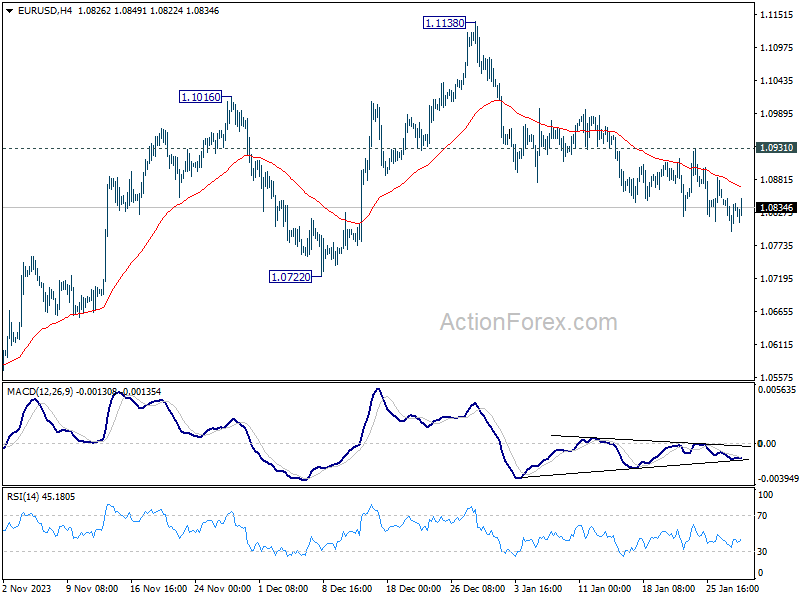

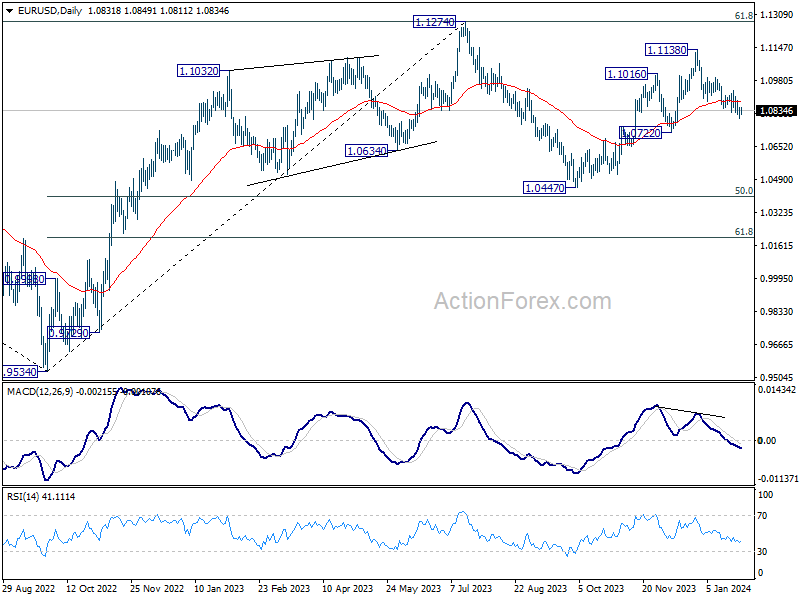

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0803; (P) 1.0827; (R1) 1.0858; More...

No change in EUR/USD's outlook. Further decline is expected with 1.0931 resistance intact. Fall from 1.1138 should target 1.0722 support next. Decisive break there will argue that whole rise from 1.0447 has completed, and target this low. However, on the upside, break of 1.0931 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

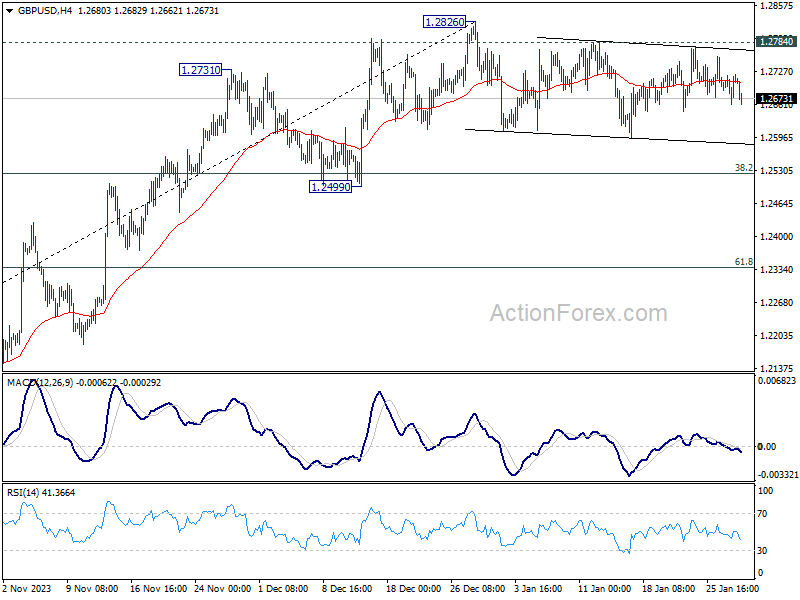

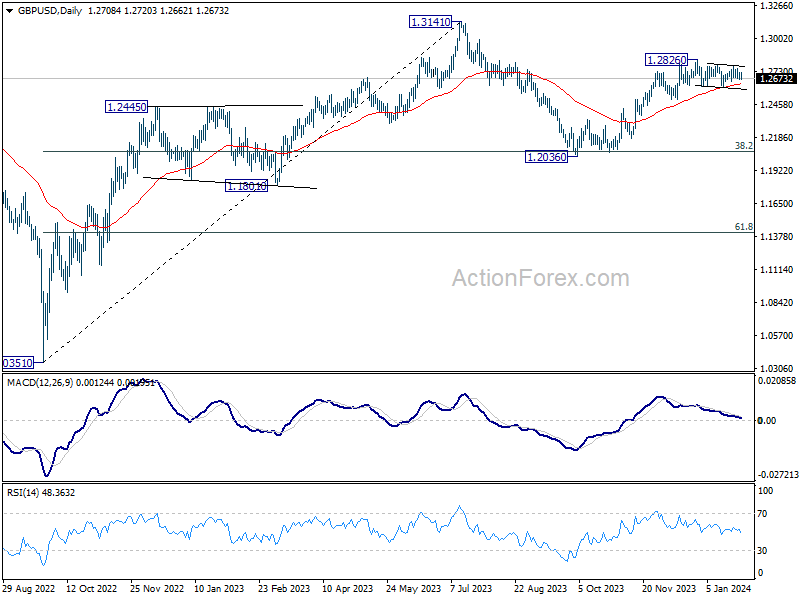

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2674; (P) 1.2697; (R1) 1.2731; More...

GBP/USD is still bounded in range trading and intraday bias stays neutral at this point. Another fall cannot be ruled out, but downside should be contained above 1.2499 support to bring rebound. On the upside, firm break of 1.2784 resistance will suggest that consolidation pattern has completed. Further rise should be seen through 1.2826 to resume the rally from 1.2036. Next target will be 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

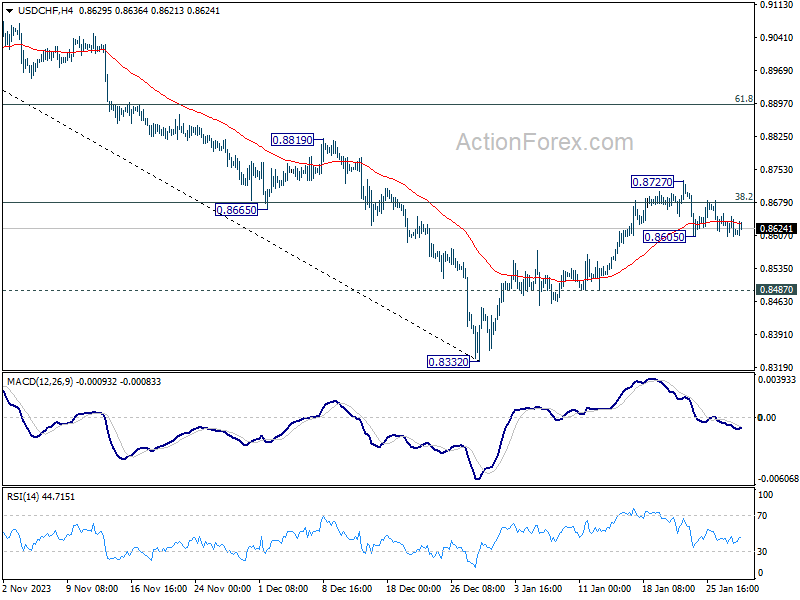

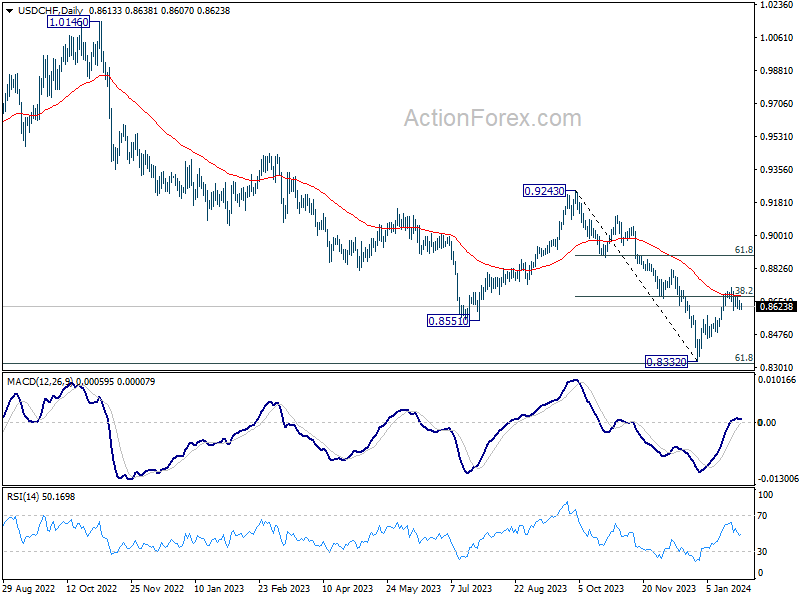

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8594; (P) 0.8626; (R1) 0.8645; More....

Outlook in USD/CHF remains unchanged as range trading continues. Intraday bias stays neutral at this point. On the downside, below 0.8605 will resume the pull back from 0.8727 to 0.8487 support. Break there will argue that rebound from 0.8332 has completed, and bring retest of this low. On the upside, firm break of 0.8727 will resume the rebound to 61.8% retracement of 0.9243 to 0.8332 at 0.8995 instead.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

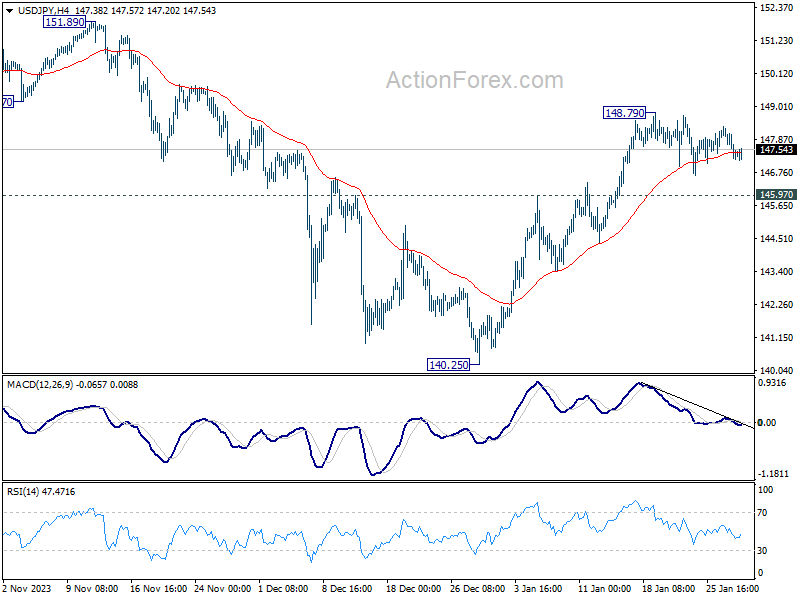

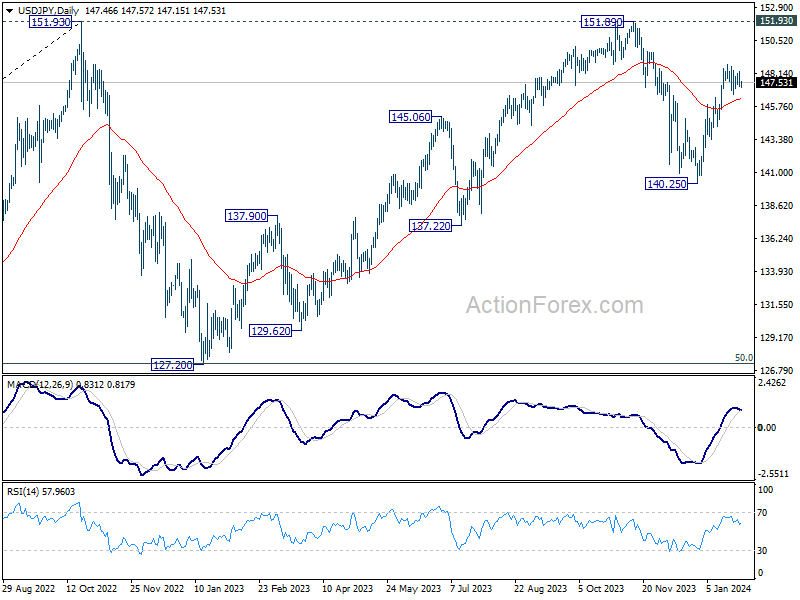

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.05; (P) 147.70; (R1) 148.14; More...

USD/JPY is still bounded in consolidation from 148.79 and intraday bias remains neutral. With 145.97 resistance turned support intact, further rally is in favor. As noted before, corrective fall from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 142.33) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

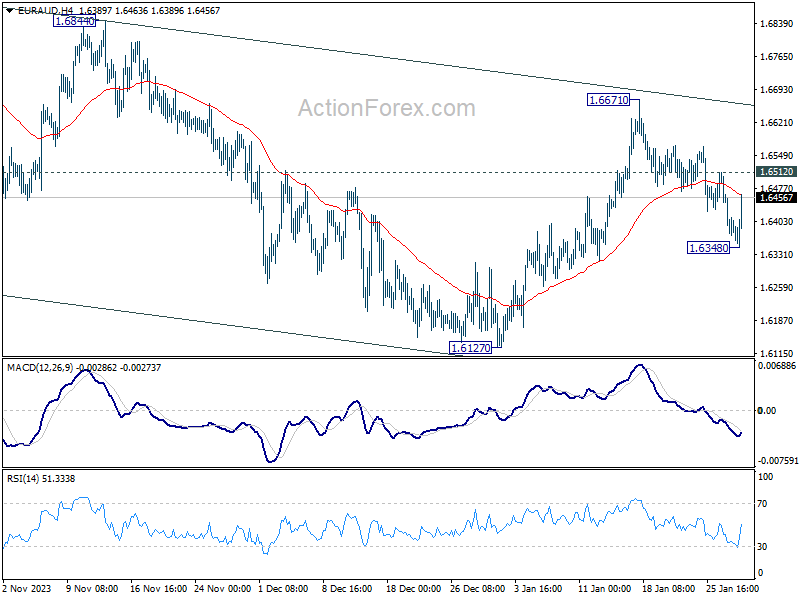

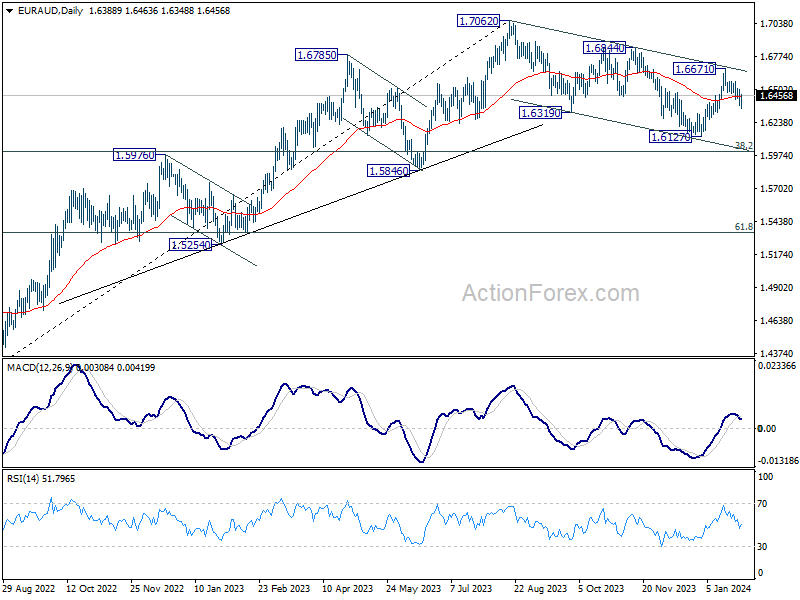

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.6340; (P) 1.6423; (R1) 1.6470; More...

Intraday bias in EUR/AUD is turned neutral first with today's strong recovery. On the upside, break of 1.6512 minor resistance will argue that pull back from 1.6671 has completed, and revive near term bullishness. Intraday bias will be back on the upside for 1.6671 resistance. On the downside, break of 1.6348 will resume the fall to 1.6127 support.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

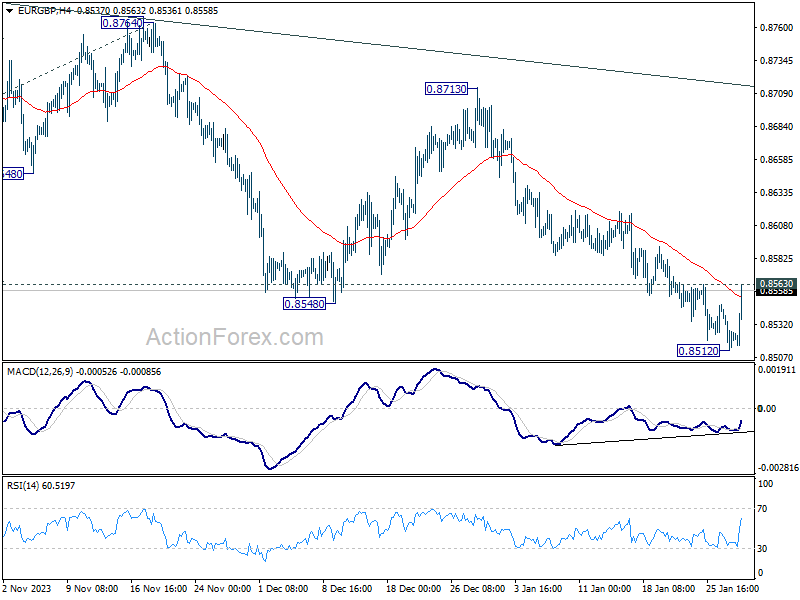

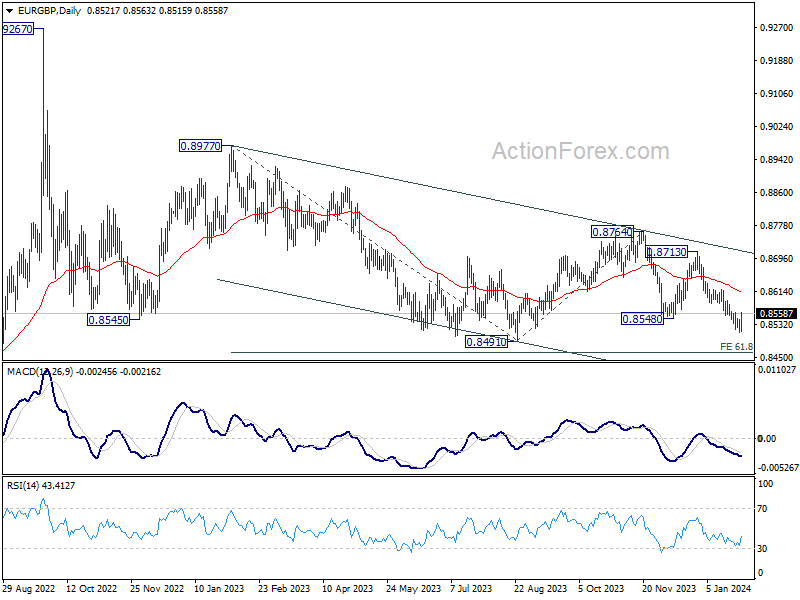

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8510; (P) 0.8527; (R1) 0.8542; More...

Intraday bias in EUR/GBP is turned neutral first with today's strong recovery. Immediate focus is now on 0.8563 minor resistance. Firm break there will suggest short term bottoming, on bullish convergence condition in 4H MACD. Intraday bias will be turned to the upside for stronger rebound to 55 D EMA (now at 0.8613). On the downside, break of 0.8512 will resume the fall from 0.8764 to retest 0.8491 support instead.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

Euro Recovers as Recession Dodged in Eurozone, Aussie Softens ahead of CPI

Euro recovers broadly today, as lifted by GDP data that indicated the Eurozone economy has narrowly averted a technical recession. This positive development has also led to a notable rebound in Germany's benchmark treasury yields. Meanwhile selling pressure has shifted Sterling and Swiss Franc, both of which are ceding some of their recent gains against Euro. The upcoming CPI flash release on Thursday is now set to the next focal point for the common currency.

In contrast, Australian Dollar faces notable weakness today amid the steep pullback in the stock markets of China and Hong Kong. The initial optimism surrounding rescue package by the Chinese government for the markets seems to be waning, with analysts suggesting that more action is needed to restore confidence. Additionally, Aussie traders are also adopting a cautious stance ahead of the upcoming release of quarterly CPI data and PMI reports from China.

In other currency market developments, Japanese Yen and Dollar are following Euro as the second and third strongest currencies of the day so far, respectively. Swiss Franc and Sterling find themselves on the weaker end, with Canadian and New Zealand Dollar showing mixed performances.

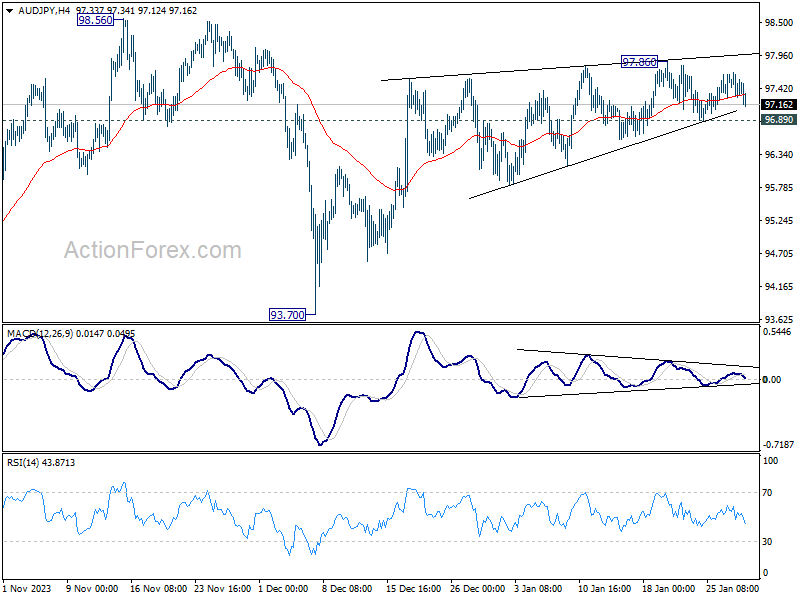

Technically, AUD/JPY demands attention in the upcoming Asian session. Rebound from 93.70 continued to lose momentum as seen in 4H MACD. Such rebound is seen as the second leg of the pattern from 98.56. While another rise cannot be ruled out, upside should be limited by 98.56. Decisive break of 96.89 support will argue that the third leg has already started, back towards 93.70 support.

In Europe, at the time of writing, FTSE is up 0.57%. DAX is up 0.09%. CAC is up 0.33%. UK 10-year yield is up 0.009 at 3.884. Germany 10-year yield is up 0.026 at 2.265. Earlier in Asia, Nikkei rose 0.11%. Hong Kong HSI fell -2.32%. China Shanghai SSE fell -1.83%. Singapore Strait Times rose 0.31%. Japan 10-year yield fell -0.0139 to 0.712.

In Europe, at the time of writing, FTSE is up 0.57%. DAX is up 0.09%. CAC is up 0.33%. UK 10-year yield is up 0.009 at 3.884. Germany 10-year yield is up 0.026 at 2.265. Earlier in Asia, Nikkei rose 0.11%. Hong Kong HSI fell -2.32%. China Shanghai SSE fell -1.83%. Singapore Strait Times rose 0.31%. Japan 10-year yield fell -0.0139 to 0.712.

ECB's Vujcic emphasizes gradual transition in monetary policy, downplays recession risks

ECB Governing Council member Boris Vujcic emphasizing that a "smooth transition" in monetary policy is more important then the timing of the first rate cut. Also, he'd prefer to move in smaller steps.

"April or June doesn't really make much of a difference for the economy," he stated, "I think it's more important that we achieve a kind of smooth transition."

Vujcic also expressed a preference for gradual rate adjustments, favoring 25 basis point moves as opposed to larger steps. Additionally, there would be some "pauses" in between every rate move.

Regarding the economy, Vujcic said, "the risk of a recession in the euro zone is getting smaller and smaller", projecting an upcoming phase characterized by modest economic growth coupled with further disinflation.

Eurozone GDP stable in Q4, avoids contraction

Eurozone GDP was stable in Q4, better than expectation of -0.1% qoq contraction. Compared with the same quarter of the previous year, GDP increased by 0.1% yoy. EU GDP was also stable in Q4, and increased 0.2% yoy.

Among the Member States for which data are available, Portugal (+0.8%) recorded the highest increase compared to the previous quarter, followed by Spain (+0.6%), Belgium and Latvia (both +0.4%). Declines were recorded in Ireland (-0.7%), Germany and Lithuania (both -0.3%). The year on year growth rates were positive for six countries and negative for five.

Ifo: German economy to contract -0.2% in Q1, restrictive monetary policy taking full effect

Germany's economy is bracing for a challenging first quarter, with ifo Institute projecting a contraction in GDP by -0.2%. Timo Wollmershäuser, Head of Forecasts at ifo, indicated that this decline would "tip the German economy into recession."

Wollmershäuser explained, "Companies in almost all sectors of the economy are complaining about falling demand". In the manufacturing and construction sectors, where once robust order backlogs have significantly "melted away". A concerning trend of decreasing incoming orders has been observed for several months, with residential construction experiencing a notable surge in cancellations.

"It appears that restrictive monetary policy in Europe and North America, with its aim of stabilizing prices through sharp rises in key interest rates, is now taking full effect," Wollmershäuser added

Unique factors further aggravate the situation. Wollmershäuser notes, "High illness levels, rail strikes at Deutsche Bahn, and an unusually cold and snowy January," are additional burdens on the economy. Despite these factors, he finds a silver lining in private consumption, which shows some positive trends.

Swiss KOF rises to 101.5, signaling imminent economic recovery

Swiss KOF Economic Barometer rose from 98.0 to 101.5 in January, above expectation of 98.2. That was the third consecutive month of increase, and the first instance since March of the previous year that the barometer has exceeded its medium-term average. This development is being interpreted as "increasing signs that the Swiss economy will soon recover".

The improvement is particularly noticeable in the accommodation industry and other service sectors. The combined indicators for manufacturing, construction, and foreign demand are also "develop slightly positive". Consumer demand, however, is "virtually unchanged". The only sector that appears to be facing challenges is the financial and insurance activities, where the outlook has deteriorated.

RBNZ's Conway: We still have a way to go on inflation

RBNZ Chief Economist Paul Conway struck a hawkish tone in a speech today, tempering market expectations for imminent policy easing. Conway acknowledged the effectiveness of current monetary policy in slowing the economy and reducing inflation. But he emphasized noted that the journey to achieving the target midpoint is far from over. His remarks also indicated that recent weaker GDP data would not automatically lead to a dovish shift in RBNZ's approach.

Conway stated, "Monetary policy is working, with the economy slowing and inflation falling. But we still have a way to go to get inflation back to the target midpoint." He added that the upcoming February Statement would offer more insights, grounded in comprehensive data analysis.

Furthermore, Conway pointed out recent GDP revisions don't necessarily imply a significant reduction in the economy's capacity pressures. He highlighted that private demand, which is more responsive to interest rate changes, has seen upward revisions, particularly in consumption and business investment.

Conway also pointed out that annual non-tradable inflation at 5.9% was higher than RBNZ's forecasts, even though headline CPI slowed to 4.7% in Q4 while core inflation have also fallen.

Australia's retail sales falls -2.7% mom, spending remains subdued

Australia retail sales turnover fell -2.7% mom to AUD 35.19B in December, worst than expectation of -1.9% mom. Annually, sales fell -0.8% yoy.

Ben Dorber, ABS head of retail statistics, said: "The large fall in retail turnover in December was caused by a fall in discretionary spending. Consumers brought forward some of their usual December spending to November to take advantage of Black Friday sales.

"While there was a large seasonally adjusted fall in December, retail turnover rose 0.1 per cent in trend terms. This shows that underlying retail spending remains subdued when we look through the volatile movements over recent months in the lead up to Christmas."

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8510; (P) 0.8527; (R1) 0.8542; More...

Intraday bias in EUR/GBP is turned neutral first with today's strong recovery. Immediate focus is now on 0.8563 minor resistance. Firm break there will suggest short term bottoming, on bullish convergence condition in 4H MACD. Intraday bias will be turned to the upside for stronger rebound to 55 D EMA (now at 0.8613). On the downside, break of 0.8512 will resume the fall from 0.8764 to retest 0.8491 support instead.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Dec | 2.40% | 2.50% | 2.50% | |

| 00:30 | AUD | Retail Sales M/M Dec | -2.70% | -1.90% | 2.00% | 1.60% |

| 06:30 | EUR | France Consumer Spending M/M Dec | 0.30% | 0.00% | 0.70% | 0.60% |

| 06:30 | EUR | France GDP Q/Q Q4 P | 0.00% | 0.00% | -0.10% | |

| 07:00 | CHF | Trade Balance (CHF) Dec | 1.25B | 2.55B | 3.71B | 3.83B |

| 08:00 | CHF | KOF Leading Indicator Jan | 101.5 | 98.2 | 97.8 | 98.0 |

| 09:00 | EUR | Italy GDP Q/Q Q4 P | 0.20% | 0.00% | 0.10% | |

| 09:00 | EUR | Germany GDP Q/Q Q4 P | -0.30% | -0.30% | -0.10% | |

| 09:30 | GBP | M4 Money Supply M/M Dec | 0.50% | 0.20% | -0.10% | |

| 09:30 | GBP | Mortgage Approvals Dec | 50K | 53K | 50K | |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.00% | -0.10% | -0.10% | |

| 10:00 | EUR | Eurozone Economic Sentiment Jan | 96.2 | 96.2 | 96.4 | |

| 10:00 | EUR | Eurozone Industrial Confidence Jan | -9.4 | -9.0 | -9.2 | -9.6 |

| 10:00 | EUR | Eurozone Services Confidence Jan | 8.8 | 8.0 | 8.4 | |

| 10:00 | EUR | Eurozone Consumer Confidence Jan F | -16.1 | -16.1 | -16.1 | |

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Nov | 4.80% | 4.90% | ||

| 14:00 | USD | Housing Price Index M/M Nov | 0.20% | 0.30% | ||

| 15:00 | USD | Consumer Confidence Jan | 113.2 | 110.7 |

ECB’s Vujcic emphasizes gradual transition in monetary policy, downplays recession risks

ECB Governing Council member Boris Vujcic emphasizing that a "smooth transition" in monetary policy is more important then the timing of the first rate cut. Also, he'd prefer to move in smaller steps.

"April or June doesn't really make much of a difference for the economy," he stated, "I think it's more important that we achieve a kind of smooth transition."

Vujcic also expressed a preference for gradual rate adjustments, favoring 25 basis point moves as opposed to larger steps. Additionally, there would be some "pauses" in between every rate move.

Regarding the economy, Vujcic said, "the risk of a recession in the euro zone is getting smaller and smaller", projecting an upcoming phase characterized by modest economic growth coupled with further disinflation.