Sample Category Title

EUR/USD Remains Vulnerable to the Downside

Markets

More ECB quotes hit the wires yesterday. But hawkish twists from the likes of Kazimir (rate-cut debate now is premature) got less attention. Markets instead singled out heavyweight Villeroy over the weekend effectively turning every meeting into a live one. VP de Guindos said inflation is moving positively and risks are tilted to the downside. Centeno from Portugal later added that the ECB should cut sooner rather than later. German bunds outperformed Treasuries by slipping between 4.4-7.2 bps at the start of the week. US Treasuries followed Bunds higher and even caught up with them later. US yields dropped up to 6.5 bps with the belly of the curve outperforming the wings. US Treasury in late dealings announced a reduction in its quarterly borrowing estimate to $760bn (assuming an end-of-March $750bn cash balance). This compares to the $816bn projected in October. This unexpected cut followed projections of further unspecified “higher net fiscal flows” and a higher beginning of quarter cash balance. Issuance details will be published on Wednesday. ECB talk pressured EUR/USD and brought the 1.0793 support area (50% retracement on the 2023Q4 rally) close by. That did what it’s supposed to do with the abrupt drop in US yields and a constructive risk sentiment (likes of the S&P500 hit new record highs again) providing EUR/USD additional oxygen. The pair eventually closed at 1.0833, down from 1.0858 at the open. Sterling shrugged off Friday’s softish session and closed at the strongest level since August last year against the euro (EUR/GBP 0.852) even as Gilt yields dropped more from an absolute point of view (>8 bps). In commodity markets, oil prices stood out. Brent traded just shy of $85/b at the open as the Middle East/Red Sea conflict is increasingly leaving marks. While gains evaporated later, oil still closed at the highest level since end-November. Tensions in the region are running higher again. The US is mulling a tough enough response to a deadly attack in Jordan by Iran-backed militants over the weekend.

The economic calendar heats up from today on. The US publishes its Conference Board consumer confidence, which is projected to improve to the highest since December 2021. Europe is at the center of attention though. Q4 GDP numbers are published with the European economy seen having contracted 0.1% q/q after shrinking similarly in Q3. The French economy in the meantime as expected stagnated. The first member states publish January inflation figures as well. These include Belgium and Spain ahead of France, Germany and Portugal tomorrow. In the current market mindset we’ll probably get a larger reaction to downside surprises. Euro area money markets do already price in a 25 bps cut at every 2024 meeting from April on, however. First support in the German 10-y yield is located at 2.16%. EUR/USD remains vulnerable to the downside. After 1.0793, 1.0724 (December correction low) and 1.0712 (61.8% retracement) pops up as the next reference.

News & Views

Reserve Bank of New Zealand chief economist Conway pushed back against the global trend of fast and aggressive policy rate cut cycles which also spilled the New Zealand money markets. They currently discount a 25 bps rate cut by July whereas the RBNZ as recently as November suggested to keep policy rates unchanged at 5.5% through 2024. Markets bet that weaker activity data in Q3 and Q4 will be a trigger for the RBNZ to move faster but Conway pointed out recent (downward) GDP revisions don’t necessarily mean that capacity pressures in the economy are much lower than previously assumed. On top, they’re mostly down to weaker government spending. Conway downplayed the recent Q4 headline inflation miss by stressing stickier non-tradeables inflation which is a long way from 2%. To sum up, Conway believes that monetary policy is working, with the economy and inflation falling, but the RBNZ has a way to go to get inflation back to the target midpoint. The kiwi dollar profited with NZD/USD testing first resistance at 0.6149.

British shop prices rose at the slowest annual pace since May 2022 this month (2.9% Y/Y from 4.3% Y/Y in December). Heavier discounting of goods in January sales compared with January 2023 offer part of the explanation. Non-food prices rose by 1.3% Y/Y (least since Feb 2022) while food prices increased by 6.1% Y/Y (lowest since June 2022). Lower wholesale costs are finally allowing supermarkets to cut the price of some goods though consumer demand remains fragile.

S&P 500 Renews Record Ahead of Big Tech Earnings, Fed Decision

It was yet another day, and another record high for the US major stock indices. The S&P500 traded to 4930 for the first time, driven higher by falling US yields after the US Treasury surprisingly cut its quarterly borrowing estimate, on hope that five of 7 Magnificent stocks will surprise positively when they reveal their results this week, and on hope that we might hear something relatively dovish from the Federal Reserve (Fed) meeting this week.

The dovish Fed expectations prevent the US dollar index from making a decisive move above its 200-DMA. Investors expect the Fed to cut the rates from May and the dollar to lose value this year. Yet the Fed’s path to rate cuts may not be as swift as many believe, if inflation numbers start looking bad again. Rents – which are the main responsible of the remaining inflation pressures are expected to ease and be the major driver of inflation to the Fed’s 2% target, yet gasoline prices which fell more than 50% since the summer 2022 peak to the end of last year, and which helped bringing inflation down from a 9% peak, start showing signs of rebounding since the start of the year. For now, the rise is not alarming, but the base effect will likely play against the falling inflation trend in the next few months. It will be interesting to see if the rise in rents fall sufficiently and soon enough to temper the rise that we see today in energy prices. The latter may or may not prevent the Fed from cutting in the H1, but it will help investors to scale back their 150bp cut expectations for this year. And that could help alleviate the US dollar.

Elsewhere, the EURUSD has been benefiting from a limited courage to sell the US dollar, but the pair is extending losses below its 200-DMA on expectation that the European Central Bank (ECB) can’t keep its interest rates at the current levels with the sputtering economies. This morning, the Eurozone countries will start revealing their inflation and growth updates. The euro area’s aggregate GDP for Q4 is due today, and inflation for January is due on Thursday. The lower the growth, and the slower the inflation, the sooner the ECB will cut rates. But if inflation surprises to the upside, we could see a part of the ECB dovishness vanish, even with gloomy growth numbers. We shall see support in the EURUSD into the 1.0793/1.0775 – area that includes the 50% Fibonacci retracement on October to December rebound and the 100-DMA.

In energy, crude oil remains upbeat after last week’s positive price breakout above the $75pb and the rising tensions in the Red Sea region as everyone is now expecting the US response to the latest attacks. US crude saw resistance into the $80pb level yesterday and we could see consolidation between $78/80pb before a potential breakout above the $80pb psychological level. Oil stocks are better bid with the rising oil. Exxon rebounded more than 7% since last week and could well break above September-to-now descending channel if Friday’s results satisfy investors.

And oh, green transition goals are being thrown to a garbage. Yesterday, a hedge fund called Bluebell asked BP to cut spending on clean energy and boost its oil and gas investments instead. They said that ‘BP is preparing to operate in a world that BP should know will not exist’. Anyway, BP and other oil companies will likely see the benefits of rising oil prices. BP looks like an interesting long with a 500p target.

Dovish Tunes from the ECB

In focus today

In the euro area, Q4 GDP is released. The composite PMI indicator was almost unchanged from Q3 to Q4 at 47.2 indicating negative GDP growth, and German GDP fell 0.3% q/q. Hence, we expect the euro area release to show that GDP fell 0.1% q/q in Q4 thereby posting the second consecutive quarter with negative GDP growth. If we are right, we are in a "technical" recession. However, we stress that it is not a real recession as the labour market is still very tight and the unemployment rate was historically low at 6.4% in November. We also look out for Spanish inflation data for January that will give an indication of where we can expect the euro area print to land on Thursday.

From the US, Job Openings and Labor Turnover Survey (JOLTS) will be released for December and Conference Board's consumer confidence survey for January. Markets will keep a close eye especially on the number of job openings, which is a key indicator of labour demand for the Fed.

The US earnings season continues and today and the rest of the week a lot of results will be coming in, today among others, the results from Microsoft and Alphabet.

Overnight we get Chinese official PMIs for January from NBS. Manufacturing PMI has been much weaker than the private version from Caixin lately. We expect the two indices to converge in January and hence look for a rise in NBS PMI manufacturing. Focus will also be on the NBS service PMI which at 50.4 in December is at a low level, partly because it includes construction activity.

In Sweden, the NIER economic tendency survey is published at 09:00 CET. The expected selling prices have started to take off once again in the service sector, which is a concern especially as the Riksbank has been worried about the persistence of service inflation. The survey will also provide us with further indications of the outlook for the labour market, as it includes employers' hiring plans.

Economic and market news

What happened yesterday

ECB commentary. Vice president Luis de Guindos spoke at the Investment Outlook Conference hosted by Citi Private Bank in Madrid. He sounded more dovish than in previous comments, saying that inflation risks in the euro area are tilted to the downside. He also noted that the latest bank lending survey showed stabilization and that he thinks that the disinflation process can continue. ECB's Kazimir said that a rate cut in June is more probable for now, while ECB's Centeno, who typically is more to the dovish side, said that he would prefer to react earlier but more gradually, than later and more forcefully. ECB's Knot said on Sunday said that it is important to wait for wage data, due in May, before deciding on of rate cuts.

The EU threatens to hit Hungary's economy if Viktor Orban vetoes against an ongoing plan to provide financial aid of EUR 50 million to Ukraine. EU officials has said that this does not reflect the status of talks. Victor Orban refused to give in if it comes down to this.

The US Treasury lowered its quarterly estimate for federal borrowing in January through March from USD 816bn to USD 760bn. The US treasury also announced it expects to borrow USD 202bn in the second quarter. As a result, the 10Y US treasury yield dropped to a one-week low following the announcement.

In Sweden the GDP Indicator for December decreased by 0.3% m/m and increased by 0.1% q/q, which showed that Sweden is no longer in a technical recession and provided a first estimate of annual growth for 2023 of -0.3%. This is not nearly as severe as forecasters projected earlier in 2023. Retail sales data for April to November 2023 got heavily revised down making the overall retail sale development in recent months weaker than earlier anticipated.

Equities: Global equities continued their strong run yesterday making the eighth consecutive day of gains. A lower-than-expected estimate from the US treasury department on the Q1 borrowing needs ended up giving a late hour boost to markets. It was no surprise to see cyclical growth benefitting the news with long duration small caps gaining the most. We have been arguing for overweight of equities and small caps because of the markets focus on lower funding cost, and hence this falls well in line with our thinking. In US yesterday, Dow +0.6%, S&P 500 +0.8%, Nasdaq +1.1% and Russell 2000 +1.7%. Normally, the current environment should be very beneficial for Asia and EM stocks in general, but the Chinese domestic challenge keeps dragging EM lower which is again visible this morning with massive underperformance in China as the Evergrande story weighs on sentiment. Futures in Europe are higher this morning while US futures are mixed.

FI: Markets digested the dovish comments from Villeroy during the weekend that said that a rate cut could come at any meeting this year. Centeno was even more dovish and said they should cut sooner rather than later. The 5y point outperformed the rest of the curve. Markets are now fully pricing the first rate cut by ECB in April.

FX: EUR/USD dipped below the 1.0850 mark in a quiet start to a very eventful week, characterised more by EUR weakness than USD strength. EUR/SEK continues to consolidate in the 11.30-40 interval ahead of the Riksbank meeting on Thursday, which we do not expect to rock the boat. Oil prices held steady as the market mulled the potential ramifications of the escalation of geopolitical tensions in the Middle East and the risk US reinstate sanctions on Venezuela after President Maduro back-tracked on this promise of free elections.

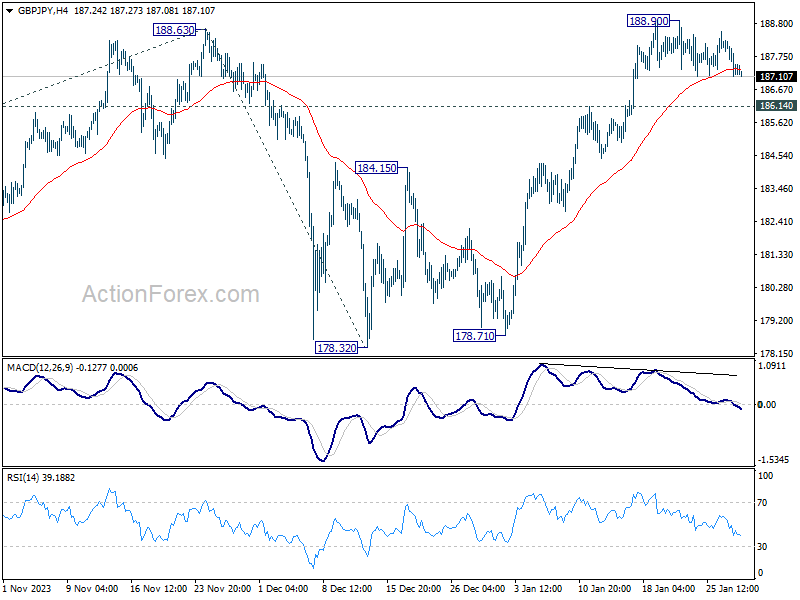

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.95; (P) 187.63; (R1) 188.13; More...

Intraday bias in GBP/JPY remains neutral as consolidation from 188.90 is extending. Further rally is expected as long as 186.14 support holds. Break of 188.90, and sustained trading above 188.63, will confirm up trend resumption. Next target is 38.2% projection of 155.33 to 188.63 from 178.32 at 191.04. However, break of 186.14 will turn bias to the downside for deeper pullback.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

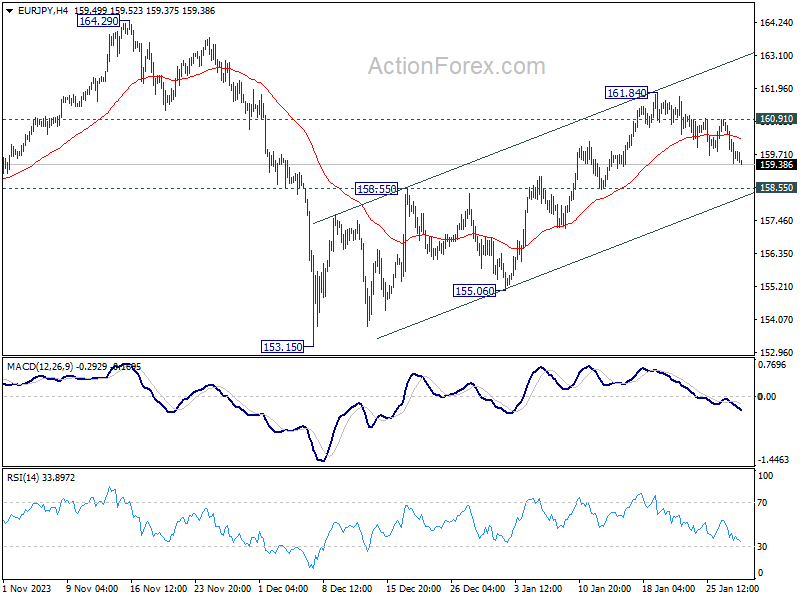

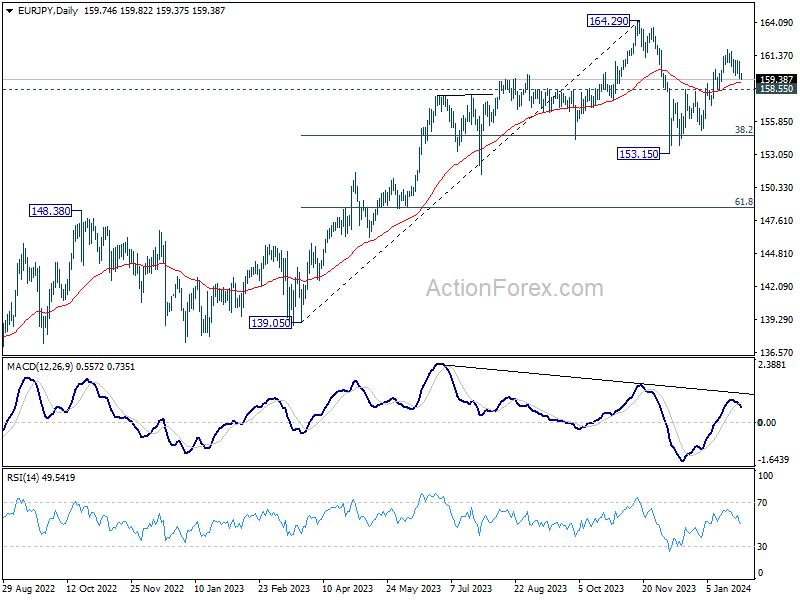

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.19; (P) 160.02; (R1) 160.61; More...

EUR/JPY is extending the consolidation from 161.84 and intraday bias remains neutral. While deeper retreat cannot be ruled out, further rally is expected as long as 158.55 resistance turned support holds. On the upside, break of 160.91 minor resistance will argue that rise from 153.15 is ready to resume through 161.84. Nevertheless, firm break of 158.55 will dampen this view and turn bias back to the downside instead.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

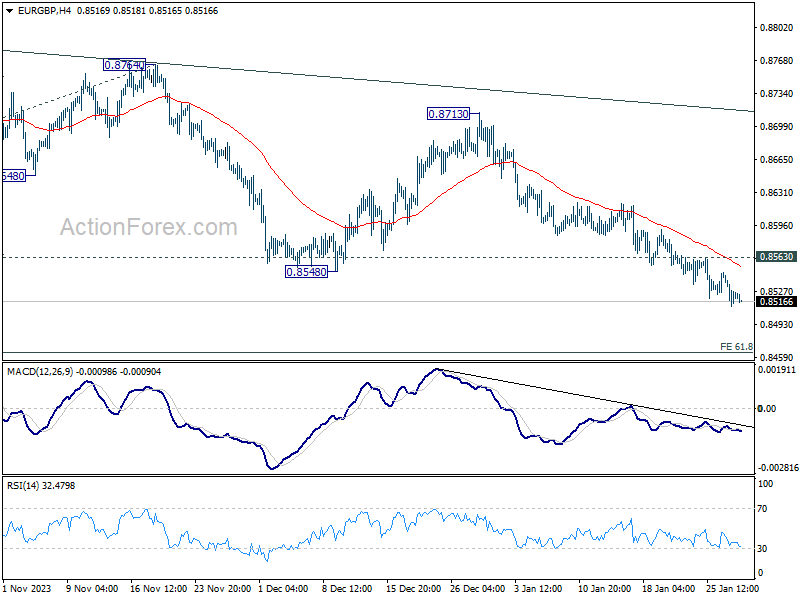

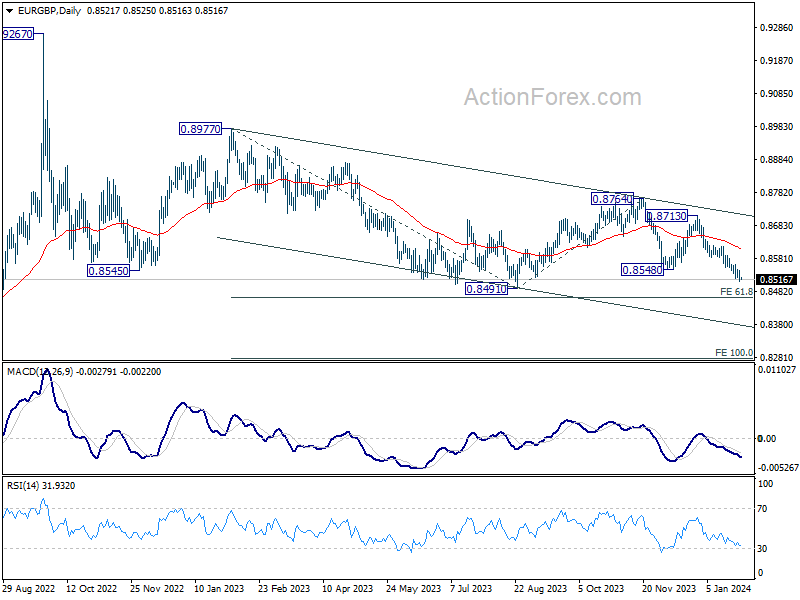

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8510; (P) 0.8527; (R1) 0.8542; More...

Intraday bias in EUR/GBP stays on the downside for 08491 support. Break there will resume larger down trend to 0.8464 projection level. On the upside, above 0.8563 minor resistance will turn intraday bias neutral and bring consolidations again.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

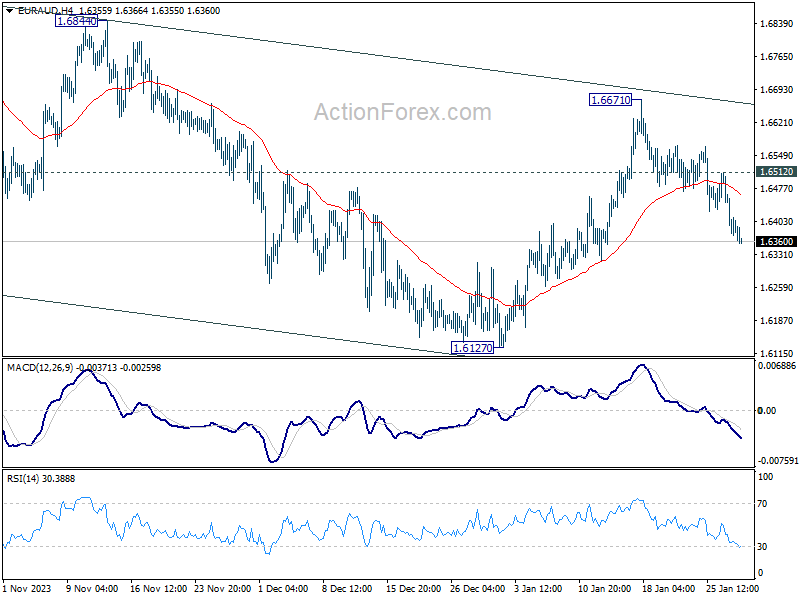

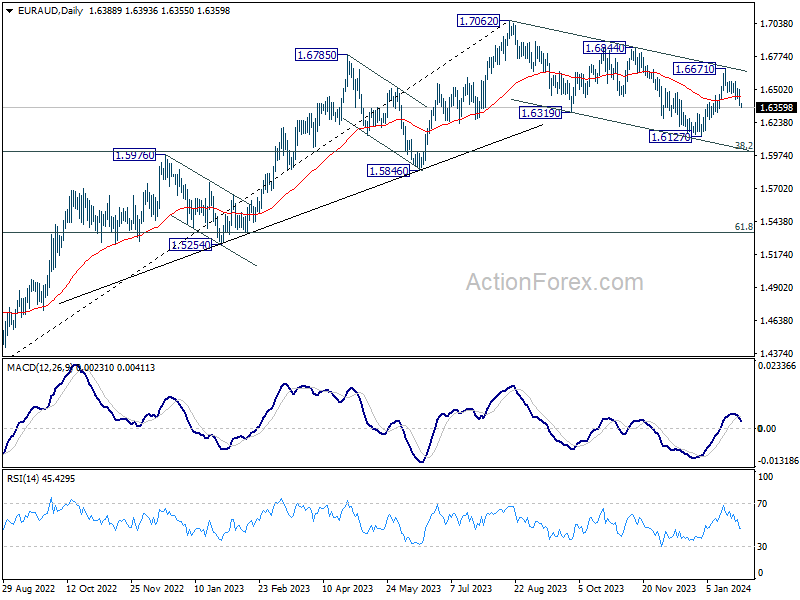

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6340; (P) 1.6423; (R1) 1.6470; More...

Intraday bias in EUR/AUD remains on the downside as fall from 1.6771 is in progress. This decline is seen as part of the larger correction from 1.7062. Next target is 1.6127 and possibly below. On the upside, though, above 1.6512 minor resistance will flip bias back to the upside for 1.6671 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

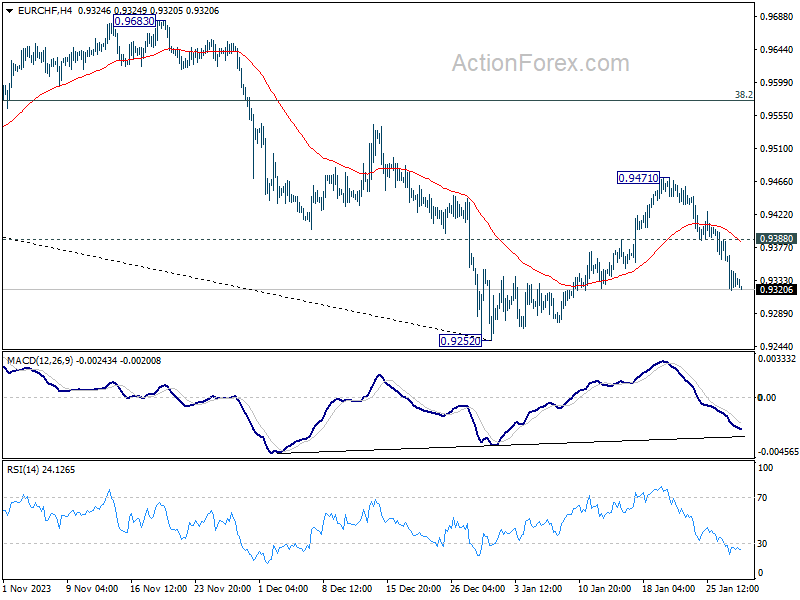

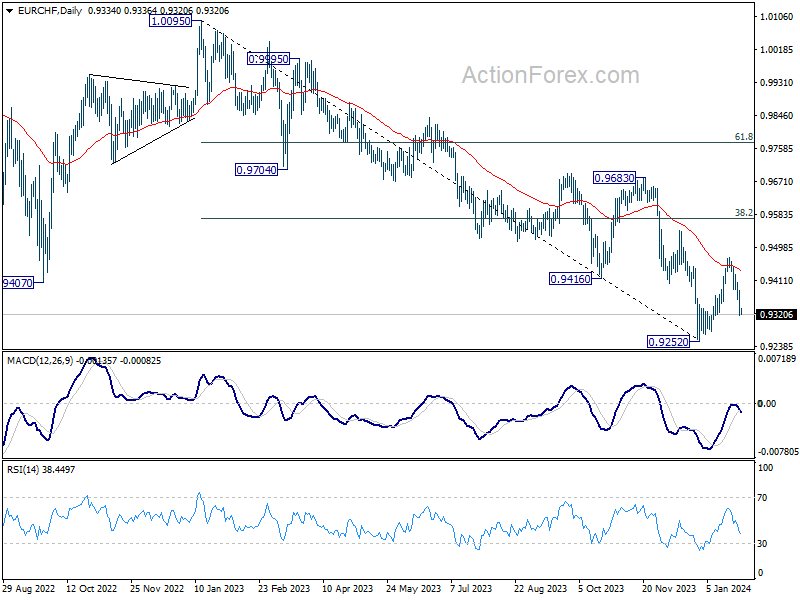

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9305; (P) 0.9348; (R1) 0.9373; More...

EUR/CHF's fall from 0.9471 is still in progress and intraday bias stays on the downside. At this point, strong support is still expected above 0.9252 low to bring rebound. On the upside, above 0.9388 minor resistance will turn bias back to the upside. Further break of 0.9471 will resume the rebound from 0.9252 to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. However, decisive break of 0.9252 will resume whole down rend from 1.0095.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes. However, firm break of 0.9683, and sustained trading above 55 W EMA (now at 0.9638) will argue that EUR/CHF is already in a medium term rally, even as a corrective move.

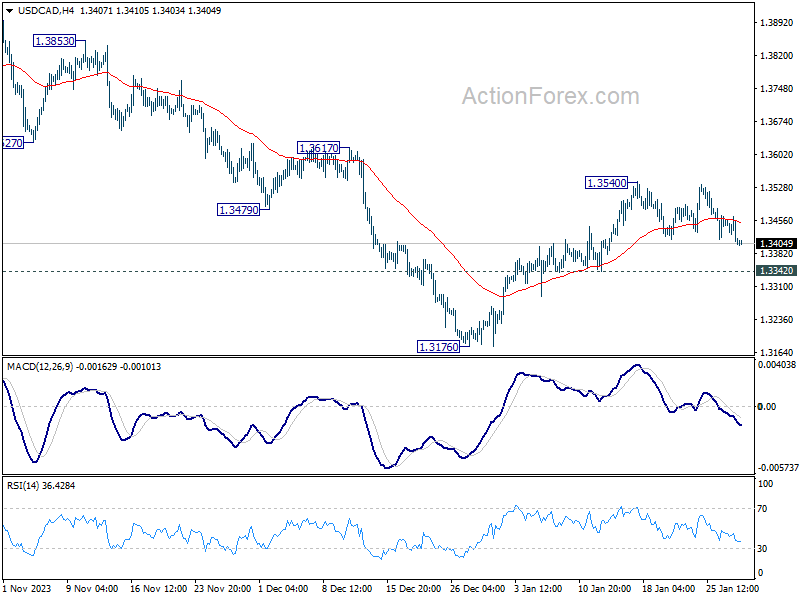

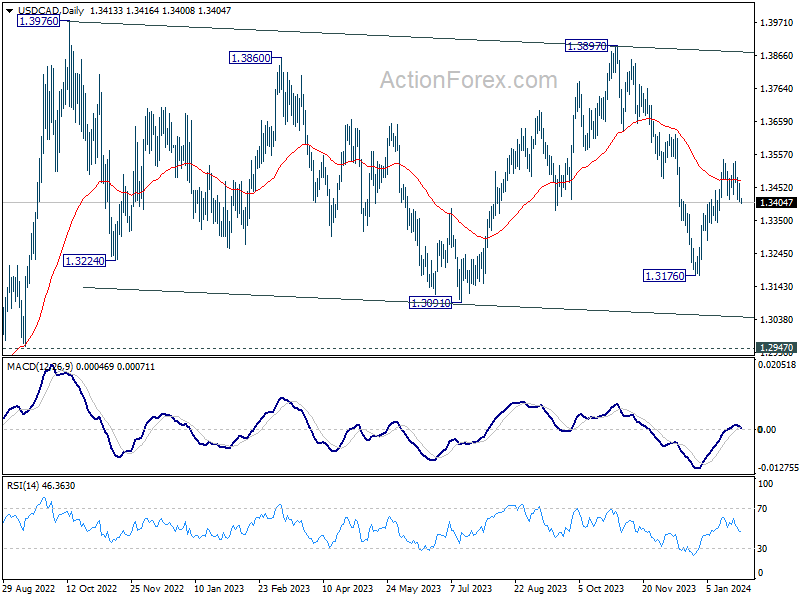

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3395; (P) 1.3430; (R1) 1.3450; More...

USD/CAD's break of 1.3414 minor support dampened the original bullish view. Intraday bias is back on the downside to 1.3342 support first. Firm break there will argue that rebound from 1.3176 has completed at 1.3540, and target this low for resuming whole fall from 1.3897. On the upside, however, break of 1.3540 will resume the rebound from 1.3176 instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

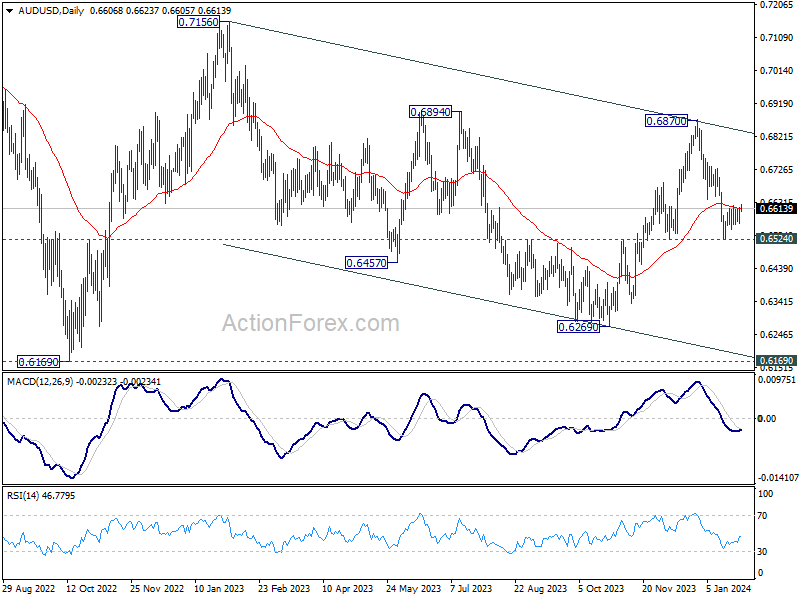

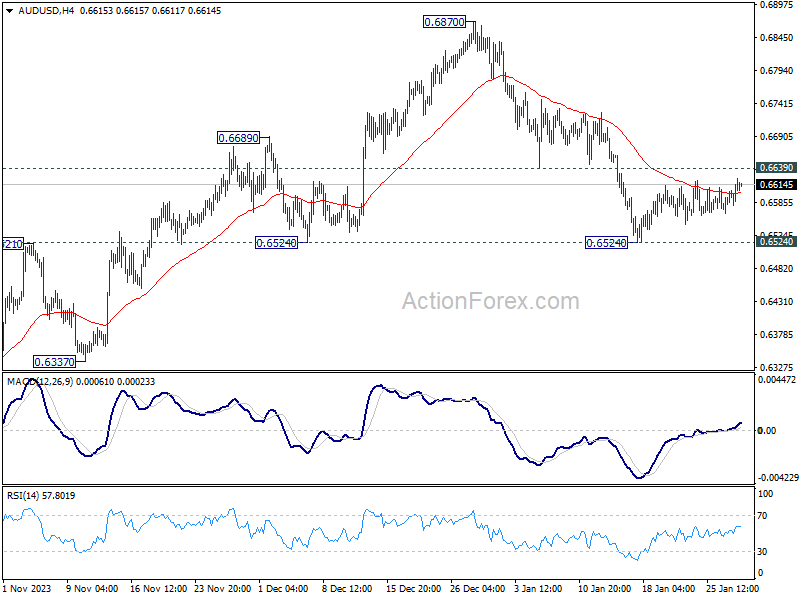

AUD/USD Daily Report

Daily Pivots: (S1) 0.6582; (P) 0.6599; (R1) 0.6628; More...

AUD/USD recovers mildly today but stays in range of 0.6524/6639. Intraday bias remains neutral and further fall is still expected. On the downside, firm break of 0.6524 support will argue that whole rebound from 0.6269 has completed, and bring deeper fall to this support. On the upside, however, firm break of 0.6639 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.