Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2666; (P) 1.2688; (R1) 1.2727; More...

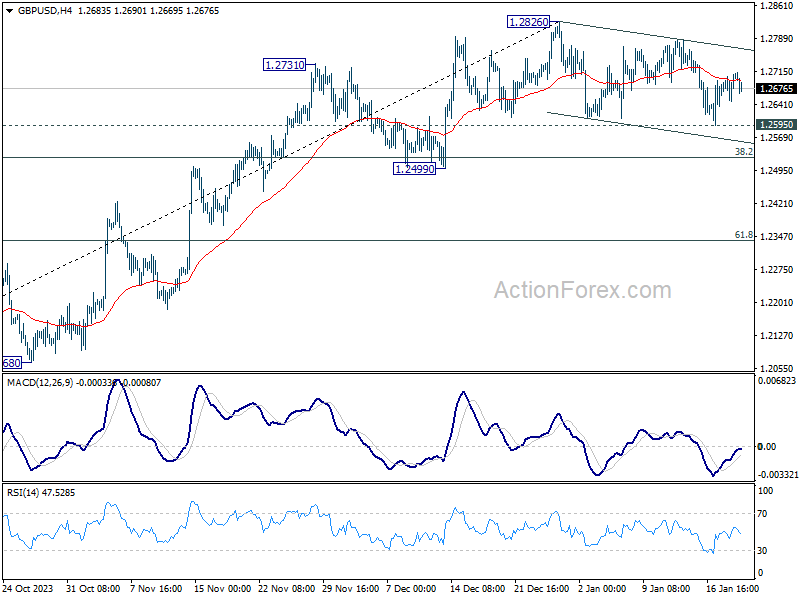

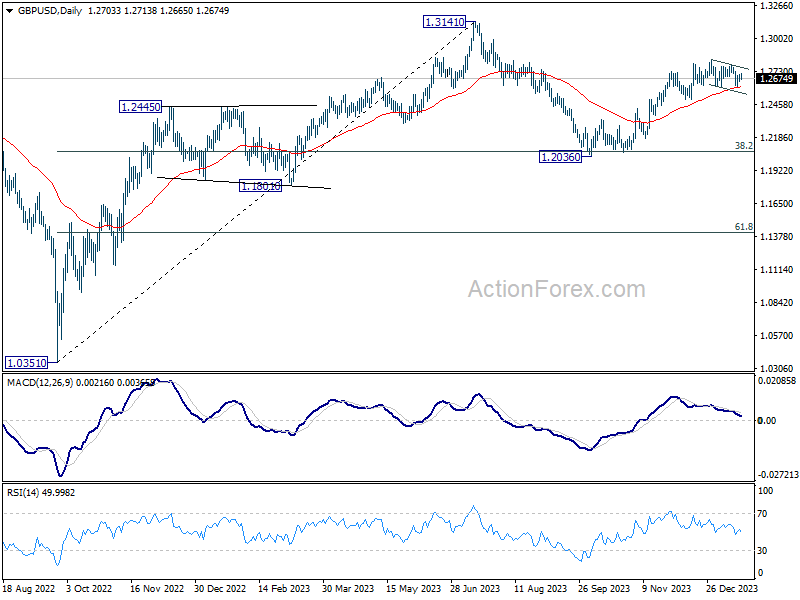

GBP/USD is staying in range above 1.2595 support and intraday bias remains neutral. On the downside, firm break of 1.2595 will resume the decline from 1.2826 to 1.2499 support. Nevertheless, strong rebound from current level will retain near term bullishness. Decisive break of 1.2826 will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Sterling Sees Moderate Decline After Weak Retail Sales, Losses Contained

Sterling fell broadly today following weaker-than-expected retail sales data. Despite this, the British currency's losses have been somewhat contained, indicating a degree of resilience. Concurrently, Japanese Yen and Australian Dollar are showing attempts to recover, but these efforts lack significant follow-through momentum. The day's activities seem more reflective of temporary consolidations rather than indicative of any major shifts in market trends.

As the week draws to a close, Dollar is on track to finish as the strongest performer. Euro and Sterling, which had been contending for the second place, have now given way to Canadian Dollar. However, there is still room for some last-minute adjustments in the rankings. Yen, on the other hand, is poised to be the weakest performer for the week, followed closely by New Zealand Dollar and Swiss Franc. Australian Dollar, which was previously languishing at the bottom, has managed to climb out of the lowest ranks and is set to end the week with mixed performance.

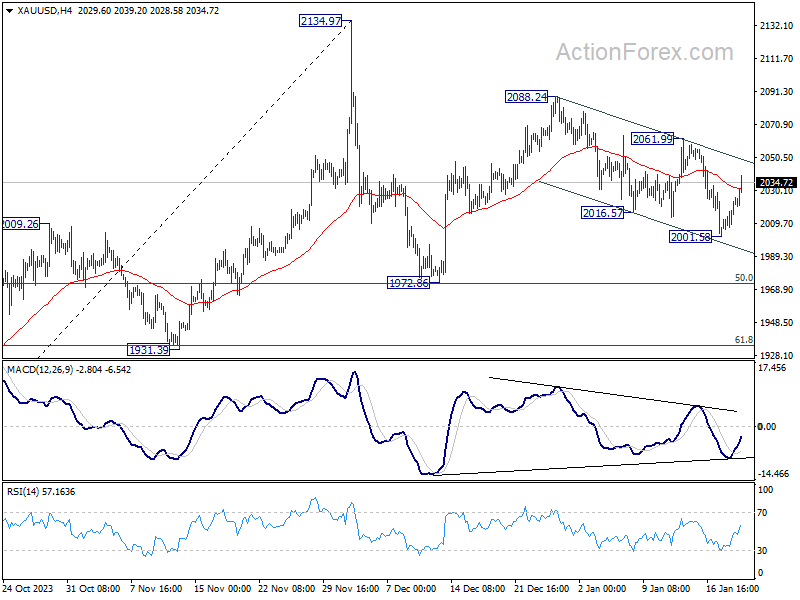

Technically, Gold surprisingly rebounded after defending 2000 handle. But overall outlook is unchanged. Price actions from 2134.97 are viewed as a corrective pattern. Rebound from 1972.86, as the second leg, might not be over yet. Break of 2061.99 will target 2088.24 and above. Nevertheless, another decline and break of 2001.58 will extend the fall from 2088.24 to 1972.86 support instead.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 0.14%. CAC is down -0.08%. UK 10-year yield is down -0.351 at 3.905. Germany 10-year yield is down -0.023 at 2.329. Earlier in Asia, Nikkei rose 1.40%. Hong Kong HSI fell -0.54%. China Shanghai SSE fell -0.47%. Singapore Strait Times rose 0.40%. Japan 10-year JGB yield rose 0.0143 at 0.669.

Canada's retail sales falls -0.2% mom in Nov, ex-auto sales down -0.5% mom

Canada's retail sales fell -0.2% mom to CAD 66.6B in November, worse than expectation of 0.0% mom. Sales declined in four of nine subsectors, led by contraction in food and beverage at -1.4% mom. Excluding autos, sales were down -0.5% mom, much worse than expectation of -0.1% mom.

Advance estimate suggests that sales rose 0.8% mom in December.

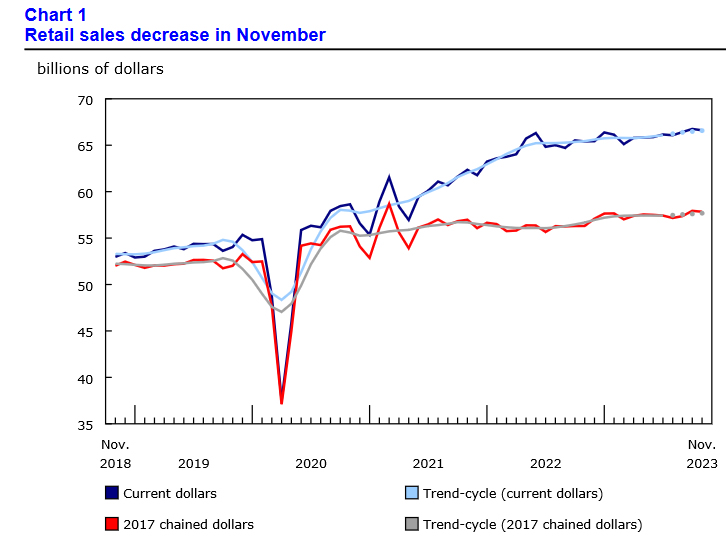

UK retail sales volume down -3.2% mom in Dec, sales value falls -3.6% mom

UK retail sales volume fell -3.2% mom in December, much worse than expectation of -0.5% mom. That's also the largest monthly fall since January 2021. Excluding fuel, sales volume fell -3.3% mom. Automotive fuel sales volumes fell by -1.9% mom. On an annual basis, sales volumes fell by 2.8% in 2023 and were their lowest level since 2018.

In value term, Retail sales value fell -3.6% mom. Ex-fuel sales value fell -3.6% mom.

Japan's CPI core dips to 2.3%, remains above BoJ's target for 21st month

Japan's CPI core, excluding fresh food, decelerated slightly in December, moving from 2.5% yoy to 2.3% yoy, aligning with market expectations. This slowdown brings core inflation rate to its lowest since June 2022, yet it notably remains above BoJ's 2% target for the 21st consecutive month.

Overall headline CPI also showed a slowdown, decreasing from 2.8% yoy to 2.6% yoy. Additionally, CPI core-core, which excludes both food and energy, saw a modest decline, moving from 3.8% yoy to 3.7% yoy.

A notable aspect of CPI data is the stability of services prices, which rose by 2.3% yoy, maintaining the pace from the previous month. This rate marks the fastest increase in services prices in three decades when periods affected by sales tax hikes are excluded.

A significant factor contributing to the slowdown in inflation was the substantial drop in energy prices, which decreased by -11.6% yoy. This decline was driven by reductions in electricity and city gas prices, which fell by -20.5% yoy and -20.6% yoy, respectively, largely due to government subsidies.

NZ BNZ manufacturing falls to 43.1, 10th month of contraction

New Zealand's BusinessNZ Performance of Manufacturing Index fell from 46.5 to 43.1 in December. This latest figure marks a continued contraction in the manufacturing sector, which has now been shrinking for ten consecutive months.

The index components reveal a widespread decline across various manufacturing activities. Production fell from 43.5 to 40.5. Employment decreased from 47.9 to 46.7. New orders dropped from 47.4 to 44.0. Similarly, finished stocks and deliveries both saw declines, from 50.4 to 45.9 and 47.8 to 43.4, respectively.

Manufacturers' feedback further underscored the industry's challenges, with 61% of the comments in December being negative. This is a slight increase from 58.7% in November, though an improvement from 65.1% in October. The predominant concerns revolved around a lack of demand and sales, which have been significant hurdles for many manufacturers.

Stephen Toplis, BNZ's Head of Research, echoed these sentiments in his assessment of the PMI data. "The December PMI reaffirms our view that economic conditions remain very difficult," he stated. Toplis anticipates that while the economy and the manufacturing sector might gain some momentum by the end of 2024, the immediate future appears challenging, particularly with pressures in retail spending and construction activity.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2666; (P) 1.2688; (R1) 1.2727; More...

GBP/USD is staying in range above 1.2595 support and intraday bias remains neutral. On the downside, firm break of 1.2595 will resume the decline from 1.2826 to 1.2499 support. Nevertheless, strong rebound from current level will retain near term bullishness. Decisive break of 1.2826 will resume whole rally from 1.2036.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Dec | 43.1 | 46.7 | 46.5 | |

| 23:30 | JPY | National CPI Y/Y Dec | 2.60% | 2.80% | ||

| 23:30 | JPY | National CPI ex Fresh Food Y/Y Dec | 2.30% | 2.30% | 2.50% | |

| 23:30 | JPY | National CPI ex Food & Energy Y/Y Dec | 3.70% | 3.80% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Nov | -0.70% | 0.20% | -0.80% | -0.20% |

| 07:00 | GBP | Retail Sales M/M Dec | -3.20% | -0.50% | 1.30% | 1.40% |

| 07:00 | EUR | Germany PPI M/M Dec | -1.20% | -0.50% | -0.50% | |

| 07:00 | EUR | Germany PPI Y/Y Dec | -8.60% | -7.90% | -7.90% | |

| 07:30 | CHF | Producer and Import Prices M/M Dec | -0.60% | -0.60% | -0.90% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Dec | -1.10% | -1.30% | ||

| 13:30 | CAD | Retail Sales M/M Nov | -0.20% | 0.00% | 0.70% | 0.50% |

| 13:30 | CAD | Retail Sales ex Autos M/M Nov | -0.50% | -0.10% | 0.60% | 0.40% |

| 15:00 | USD | Existing Home Sales Dec | 3.82M | 3.82M | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan P | 69.6 | 69.7 |

Canada’s retail sales falls -0.2% mom in Nov, ex-auto sales down -0.5% mom

Canada's retail sales fell -0.2% mom to CAD 66.6B in November, worse than expectation of 0.0% mom. Sales declined in four of nine subsectors, led by contraction in food and beverage at -1.4% mom. Excluding autos, sales were down -0.5% mom, much worse than expectation of -0.1% mom.

Advance estimate suggests that sales rose 0.8% mom in December.

Yen Under Pressure, Core CPI Eases

-

- Japan’s Core CPI eases to 2.3%

The Japanese yen has recovered after losing ground earlier in the day. USD/JPY rose as high as 148.80, its highest level in three weeks. The yen has rebounded and is trading in Europe at 148.10, down 0.03%. It has been a rough week for the yen which has fallen 2.1% and is moving closer to the key 150 level.

Japan’s Core CPI falls to 2.3%

Japan’s core inflation slowed for a second consecutive month, easing to 2.3% y/y in December. This matched the market estimate and was down from 2.5% in November. This was the lowest inflation rate since December 2022 and points to weaker inflationary pressure. Core inflation has been above the Bank of Japan’s target for 21 straight months, but the BoJ appears in no rush to tighten policy, arguing that inflation has been driven by cost-push factors and is not sustainable above the 2% level.

Still, the markets expect the BoJ will tighten policy, which would likely send the Japanese yen soaring. Every BoJ meeting has become a must-watch event in case there is a bombshell announcement. The BoJ meets next on Tuesday, with the BoJ likely to maintain current policy settings.

Atlanta Fed President Rafael Bostic has been making the rounds and preaching a message of caution with regard to rate policy. Bostic has said that he doesn’t expect a rate hike until the third-quarter and said caution was essential in order to avoid a scenario where the Fed lowered rates, inflation rose and the Fed had to again raise rates. Bostic’s comments were the latest example of the Fed pushing back against expectations of a rate cut in March. The markets have lowered the odds of a March cut to 54%, compared to 77% just a week ago, according to the CME’s FedWatch tool.

USD/JPY Technical

- USD/JPY pushed past resistance at 148.24 and 148.55 before retreating.

- There is support at 147.67 and 147.36

Canadian Dollar Drifting Ahead of Retail Sales

- Canada’s retail sales expected to fall to zero

The Canadian dollar is showing limited movement for a second straight day. In the European session, USD/CAD is trading at 1.3496, down 0.13%.

Markets brace for stagnant retail sales

Canada releases retail sales for November later today, and the markets are expecting no growth, following a 0.7% gain in October. Retailers tried to entice shoppers with discounts in November such as Black Friday, but unless there is a huge surprise from today’s retail sales, shoppers held the purse strings tight in November.

Canada’s economy contracted in the third quarter and a weak retail sales report will weigh on fourth-quarter GDP, which at best is expected to show minimal growth. The economy has cooled down due to the Bank of Canada’s aggressive tightening which has done a good job of curbing inflation, although December CPI surprised by rising to 3.4%, up from 3.1%.

The BOC has maintained the cash rate at 5.0% for three straight times and barring further acceleration in inflation, the rate-tightening cycle is over. The key question is the timing of a rate cut. The BoC would love to chop rates and kick-start the weak economy, but a rate cut appears unlikely unless inflation moves closer to the 2% target.

The Fed continues to push back against expectations of a March rate cut and the markets have had to sharply lower the odds of a quarter-point cut in March to 54%, down from 77% just one week ago. US economic data remains surprisingly strong, with the latest evidence coming from retail sales on Wednesday. The December report showed a gain of 0.6% m/m, following 0.3% in November and above the market estimate of 0.4%. This was the strongest gain in three months. A day before the retail sales report, Fed Governor Christopher Waller said the strong economy was giving the Fed “the flexibility to move carefully and methodically” on monetary policy.

USD/CAD Technical

- There is resistance at 1.3499 and 1.3554

- 1.3452 is under pressure. Below, there is support at 1.3397

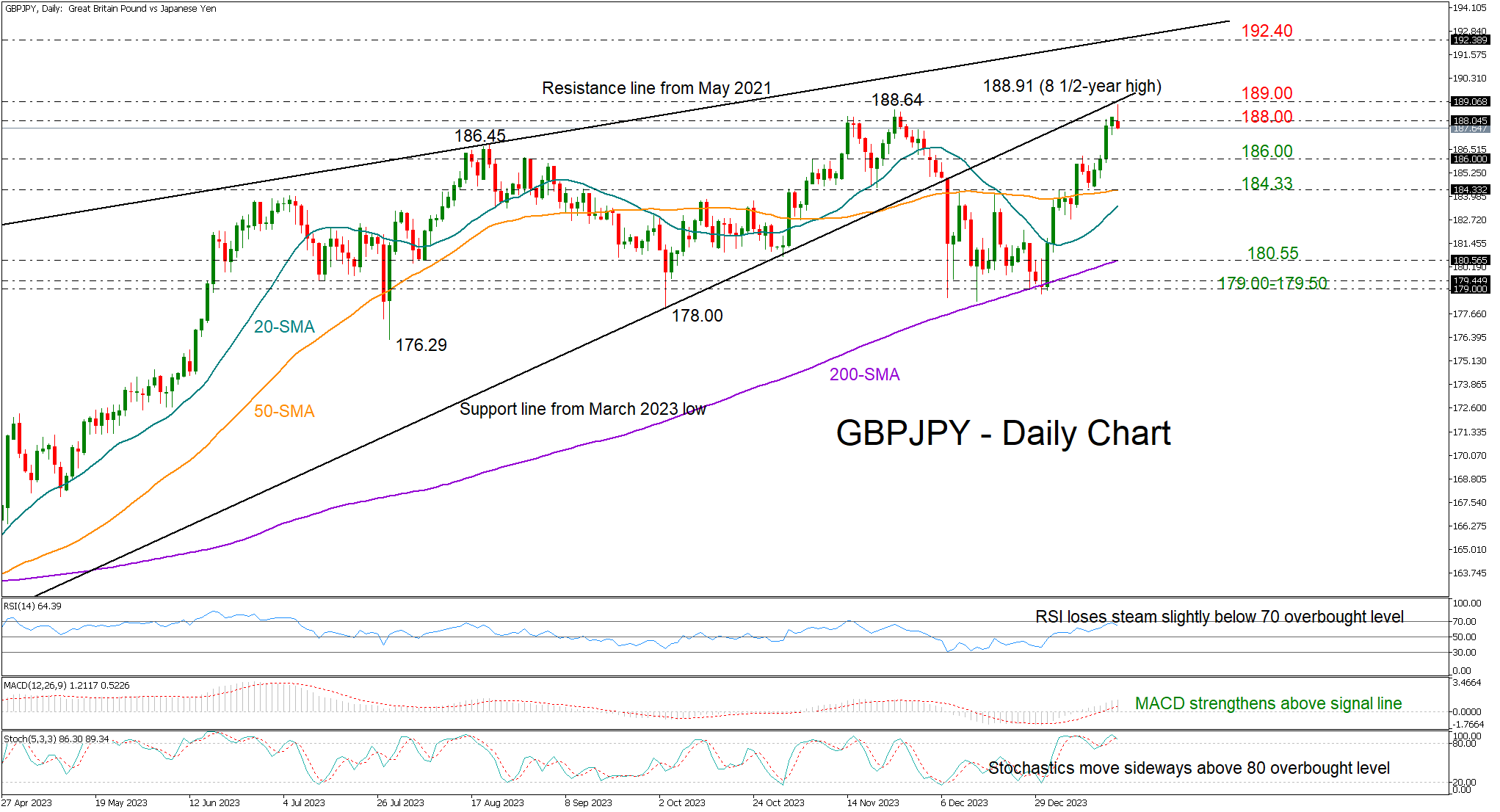

GBPJPY Charts New High But With Caution

- GBPJPY loses momentum after charting new high

- Downside moves likely; resistance within 188.00-189.00 area

GBPJPY ascended almost vertically after touching its 200-day simple moving average (SMA) at the start of January, erasing its latest bearish wave to print a new higher high of 188.90 on Friday—the highest level since August 2015.

The 188.00 round level remains a tough obstacle as the technical indicators detect some skepticism among investors. Specifically, the stochastic oscillator keeps fluctuating sideways within the overbought region and the RSI seems to be losing steam slightly below its 70 overbought level, suggesting room for improvement could be limited.

An extension above the 189.00 mark, where the upward-sloping line from the March 2023 low is placed, could clear the way towards the tough resistance line from May 2021 at 192.40. Additional gains from there could stabilize around the 2015 ceiling of 195.30-195.85.

Should the 188.00 barrier stand firm, the pair could initially seek support near the 186.00 constraining zone and then somewhere between its 50- and 20-day simple moving averages (SMAs) at 184.33 and 183.50, respectively. The 200-day SMA could be the next destination at 180.60, a break of which could immediately bring the 179.00-179.50 floor under examination.

In brief, GBPJPY is facing some difficulty in surpassing November’s wall around the 188.00 number, while the 189.00 mark could be another challenge as overbought signals are present.

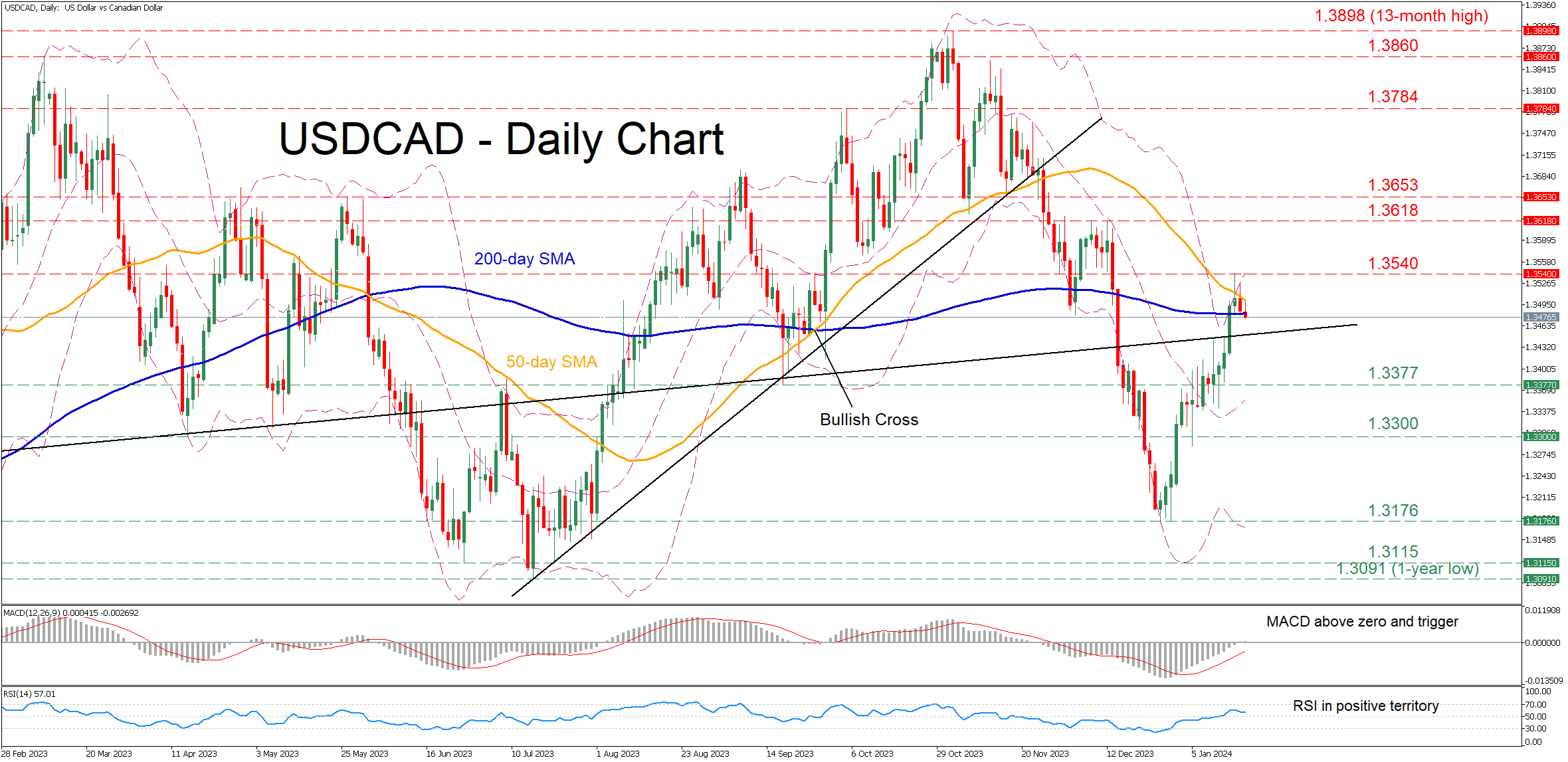

USDCAD Stuck Between Converging SMAs

- USDCAD extends its rebound to a fresh 1-month high

- But does not manage to close above the 50-day SMA

- Momentum indicators turn positive

USDCAD had been staging a solid recovery from its December low of 1.3176, but the 50-day simple moving average (SMA) prevented further gains. Despite the rejection, the 200-day SMA has been acting as a strong floor, thus the price is currently hovering between the converging SMAs.

Considering that the MACD has climbed to its positive zone for the first time since late November, the pair could jump above the 50-day SMA and revisit its one-month peak of 1.3540. Conquering that hurdle, the bulls could attack 1.3618, a region that held strong multiple times in December. Further advances may then cease at the April-May resistance of 1.3653.

Alternatively, should the price slide below its 200-day SMA, the September bottom of 1.3377 could be the first barricade for the price to claim. A violation of that territory could open the door for the April bottom of 1.3300. Failing to halt there, the pair could extend its retreat towards the December low of 1.3176..

In brief, USDCAD has been stuck between the converging 50- and 200-day SMAs, while the wide Bollinger bands might suggest heightened volatility moving forward. Therefore, a decisive break above or below the range defined by the SMAs could lead to a significant move in the same direction.

GBP/USD Dips as Retail Sales Slide

- UK retail sales slide 3.2% in December

- GBP/USD edges lower

The British pound has weakened slightly on Friday. In the European session, GBP/USD is trading at 1.2682, down 0.18%.

UK retail sales take a tumble

The markets were expecting a letdown from December retail sales after a strong November reading, but nobody was expecting a multi-year drop. Yet that’s what happened, as retail sales plunged 3.2% m/m, the lowest level since January 2021. Considering the sharp drop, the British pound’s reaction has been muted.

In November, retail sales jumped a revised 1.4%, as shoppers flocked to department stores to take advantage of Black Friday sales and other discounts. This meant that much of the Christmas shopping took place in November. The massive drop of 3.2% crushed the consensus estimate of -0.5%.

There is more to this story than Black Friday sales. The weak December reading reflected a UK consumer who is pessimistic about the economy and is being relentlessly squeezed by high inflation and elevated borrowing costs. December retail sales were brutal but the struggles faced by consumers are nothing new – retail sales fell by 2.8% in 2023, the lowest level since 2018.

The sharp drop in retail sales will have a negative impact on December GDP, which could mean that GDP for the fourth quarter is negative. If that is the case, the UK will technically be in a recession, with two consecutive quarters of negative growth. Even if the UK manages to avoid a recession, growth will be flat.

The Bank of England has kept rates unchanged for three straight times and meets on February 1. The sharp drop in retail sales supports the BoE considering a rate cut, but December inflation rose unexpectedly from 3.9% to 4.0%, and the BoE will be hesitant to chop rates before inflation is closer to the 2% target.

GBP/USD Technical

- GBP/USD is testing support at 1.2689. Next, there is support at 1.2625

- There is resistance at 1.2738 and 1.2802

UK Retail Sales Plunge in December

UK Retail Sales fell sharply in December as consumers tightened their pursestrings during what is normally a hugely important time of year for retailers.

Any sense of optimism from the jump in sales in November was short-lived, with the decline in sales last month as widespread as it was steep. Everyone from food retailers to department stores saw a sharp reduction in sales as consumers spent less on gifts and, as it turns out, food during the festive season.

While real household incomes are rising once more, the last two years have clearly taken a significant toll and it would appear many are not yet feeling better off as a result of inflation falling below wage growth.

Some of that may be psychological after two years of seeing bills and prices rising so much compared with incomes but there will also be plenty whose incomes are still being squeezed or who have savings buffers that need rebuilding and debt repaying.

Then there's the evidence we're continuing to see in the aftermath of lockdowns that people are more inclined to spend on experiences than they are goods which has perhaps lasted longer than expected.

Either way, the question that Bank of England policymakers will be asking themselves is what this all means for the economy and the inflationary environment. While problematic for retailers, less demand could help the central bank in its mission to get inflation back to 2% and, as a result, cut interest rates sooner than it would currently admit.

Oil consolidating despite Middle East risks

Oil prices are steady today after another choppy but ultimately consolidatory week. While the price of crude remains sensitive to events in the Middle East, as we've seen over the last couple of weeks, the oil market remains well-balanced which is why we're not seeing prices higher. Supply disruptions remain an upside risk but there are downside risks too including the global economy and OPEC+ unity.

Gold holding above $2,000 for now

Gold is trading a little higher at the end of the week after rebounding off $2,000 a day earlier. The yellow metal has been driven lower by slightly softer expectations for rate cuts this year and a lack of data that could turn things back in its favour. The figures we've seen since the turn of the year have been fine but more than that is needed to maintain the enthusiasm markets ended 2023 with.

How big a post-ETF correction are we looking at?

Bitcoin is continuing to struggle in the aftermath of the spot ETF approvals. While we haven't seen a dramatic decline, the price is still more than 15% off its highs and it broke below $42,000 which appeared to be holding quite well over the last month. The key level now could be $40,000, a break of which would be a big psychological blow and perhaps indicate a more intense post-ETF correction is on the cards.

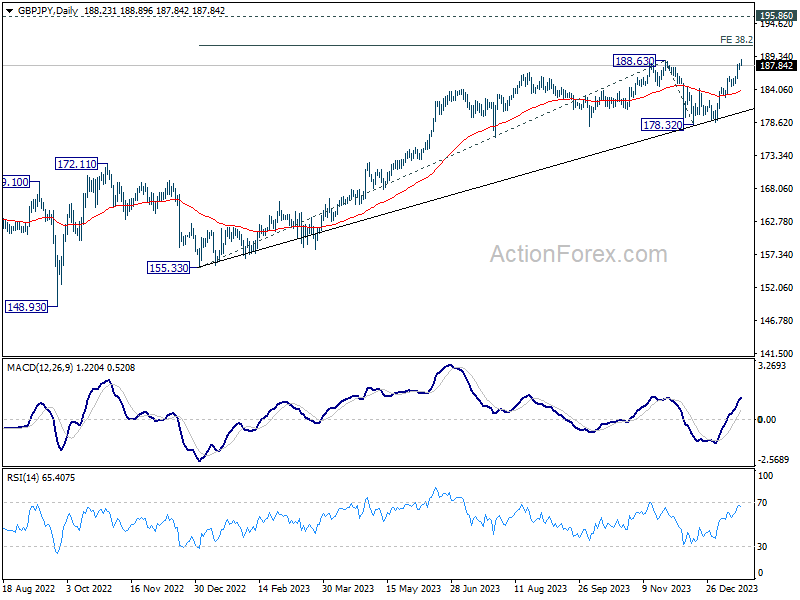

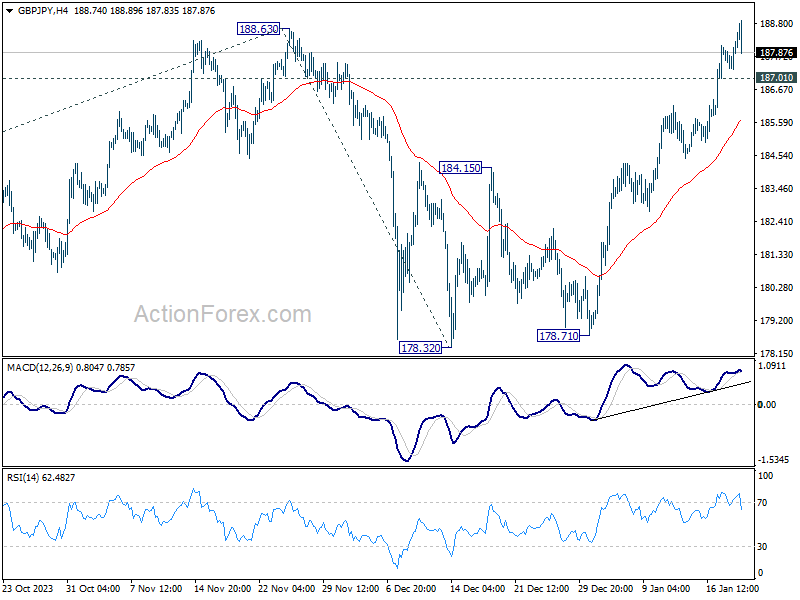

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.63; (P) 187.94; (R1) 188.57; More...

Intraday bias in GBP/JPY stays on the upside for the moment. Sustained break of 188.63 will confirm larger up trend resumption. Next target is 38.2% projection of 155.33 to 188.63 from 178.32 at 191.04. On the downside, below 1187.01 minor support will turn intraday bias neutral and bring consolidations first. But outlook will stay bullish as long as 184.15 resistance turned support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).