Sample Category Title

AUD/USD and NZD/USD Eye Key Upside Break

AUD/USD is moving higher and might rally if it clears 0.6725. NZD/USD is also rising and could extend its increase above the 0.6255 resistance zone.

Important Takeaways for AUD USD and NZD USD Analysis Today

- The Aussie Dollar started a fresh increase above the 0.6680 and 0.6695 levels against the US Dollar.

- There is a key bearish trend line forming with resistance near 0.6715 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is showing positive signs above the 0.6220 support.

- There is a major bearish trend line forming with resistance near 0.6255 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair started a fresh increase from the 0.6650 support. The Aussie Dollar was able to clear the 0.6680 resistance to move into a positive zone against the US Dollar.

The bulls pushed the pair above the 50% Fib retracement level of the downward move from the 0.6725 swing high to the 0.6647 low. There was a close above the 0.6695 resistance and the 50-hour simple moving average.

Finally, the pair spiked above the 76.4% Fib retracement level of the downward move from the 0.6725 swing high to the 0.6647 low. On the upside, the AUD/USD chart indicates that the pair is now facing resistance near a key bearish trend line at 0.6715.

The first major resistance might be 0.6725. An upside break above the 0.6725 resistance might send the pair further higher. The next major resistance is near the 0.6750 level. Any more gains could clear the path for a move toward the 0.6820 resistance zone.

If not, the pair might correct lower below the 50-hour simple moving average at 0.6695. The next support could be 0.6680. If there is a downside break below the 0.6680 support, the pair could extend its decline toward the 0.6650 zone. Any more losses might signal a move toward 0.6600.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair started a steady increase from the 0.6200 level. The New Zealand Dollar broke the 0.6220 resistance to start the recent increase against the US Dollar.

The pair settled above 0.6235 and the 50-hour simple moving average. It tested the 0.6260 zone and is currently consolidating gains above the 23.6% Fib retracement level of the upward wave from the 0.6195 swing low to the 0.6258 high.

The NZD/USD chart suggests that the RSI is still above 50 and signaling more upsides. On the upside, the pair might struggle near 0.6255 and a major bearish trend line.

The next major resistance is near the 0.6280 level. A clear move above the 0.6280 level might even push the pair toward the 0.6320 level. Any more gains might clear the path for a move toward the 0.6400 resistance zone in the coming days.

On the downside, there is a support forming near the 50-hour simple moving average at 0.6235. The next major support is near the 61.8% Fib retracement level of the upward wave from the 0.6195 swing low to the 0.6258 high at 0.6220.

If there is a downside break below the 0.6220 support, the pair might slide toward the 0.6200 support. Any more losses could lead NZD/USD in a bearish zone to 0.6160.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

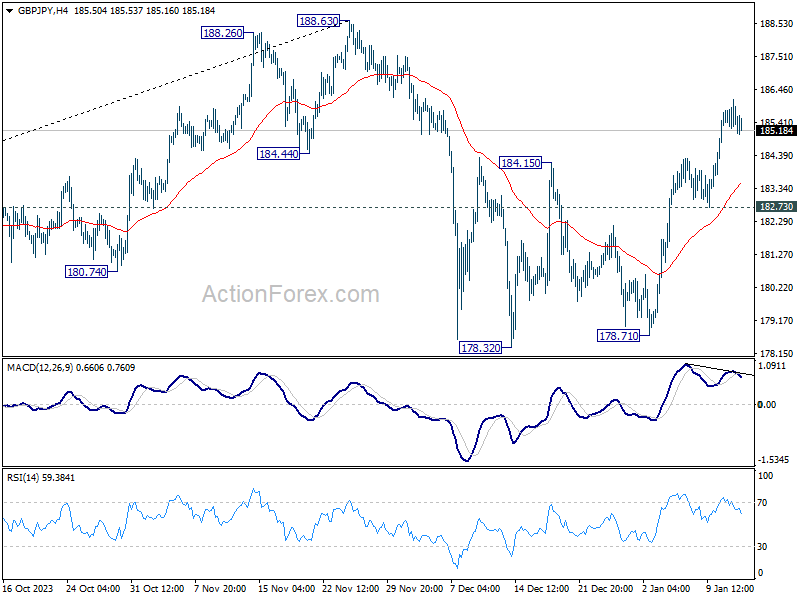

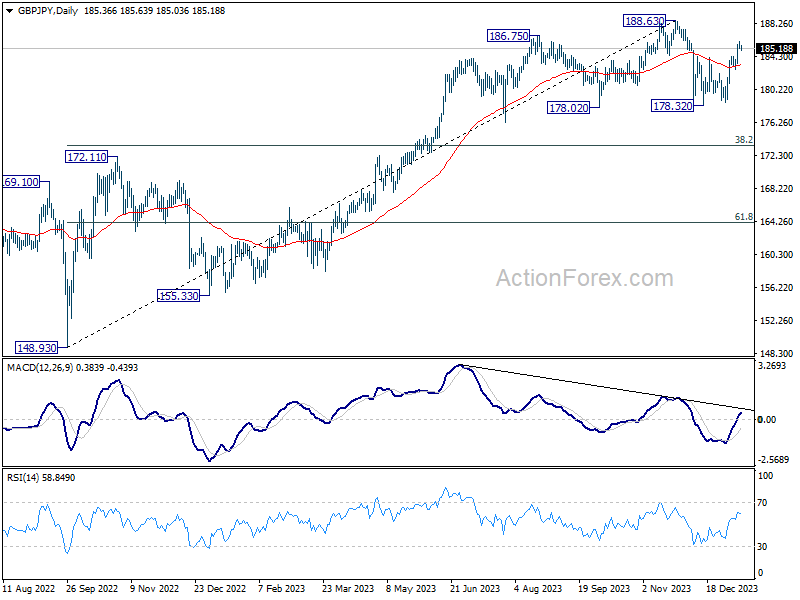

GBP/JPY Daily Outlook

GBP/JPY's rebound 178.32 is in progress and intraday bias stays on the upside. Current rise should target a test on 188.63 high. On the downside, break of 182.73 support is needed to indicate completion of the rebound. Otherwise, further rally will remain in favor in case of retreat.

In the bigger picture, price actions from 188.63 medium term top are seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage.

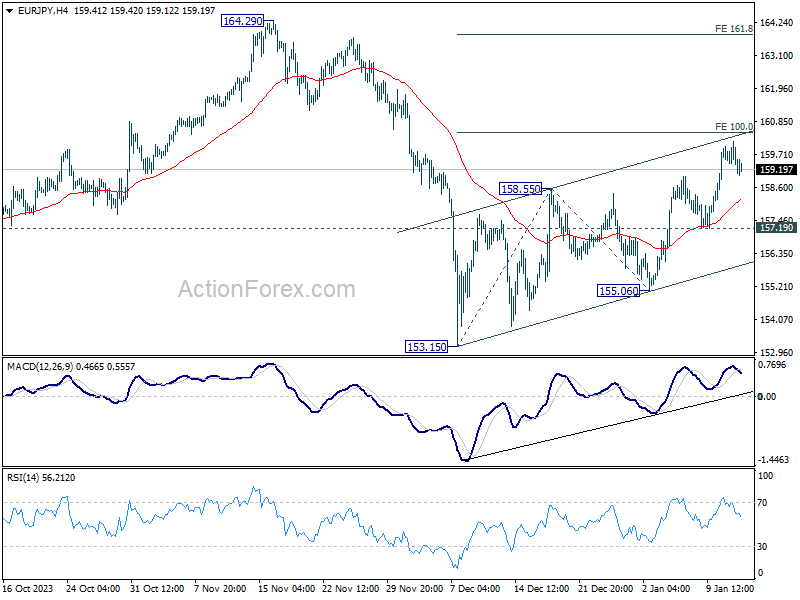

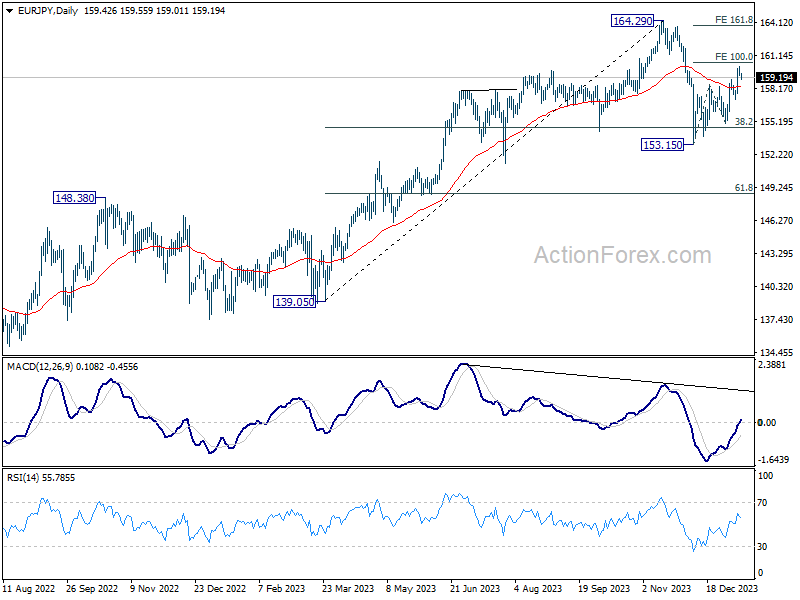

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.15; (P) 159.66; (R1) 159.95; More...

Despite loss of upside momentum, further rally is expected in EUR/JPY for now. Rebound from 153.15 would target 100% projection of 153.15 to 158.55 from 155.06 at 160.46. Firm break there will target 161.8% projection at 163.79. However, break of 157.19 support will argue that the rebound has completed, and turn bias back to the downside.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

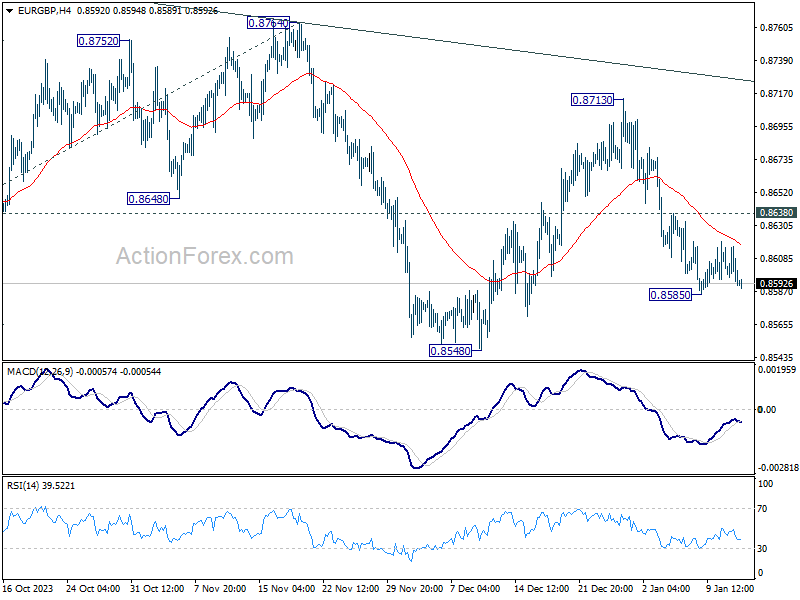

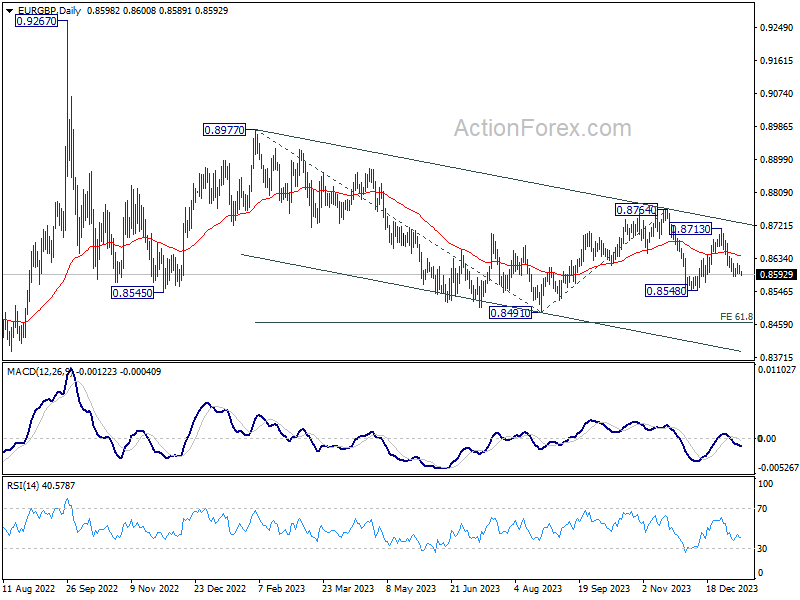

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8589; (P) 0.8603; (R1) 0.8612; More...

EUR/GBP is extending the consolidation from 0.8585 temporary low and intraday bias stays neutral. Further decline is in favor with 0.8638 minor resistance intact. On the downside, break of 0.8585 will resume the fall from 0.8713 to 0.8548 support first. Break there will target 0.8491 low next. However, break of 0.8638 will turn bias to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8764 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

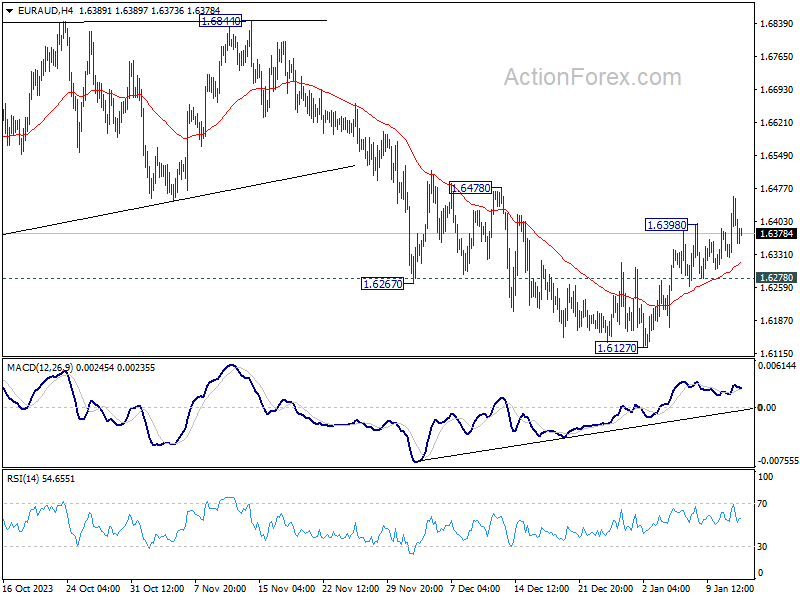

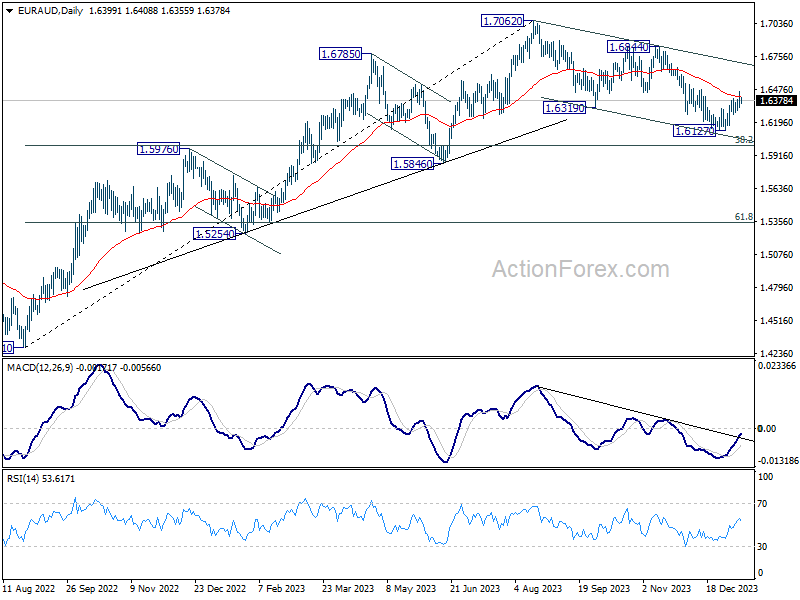

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6337; (P) 1.6398; (R1) 1.6470; More...

EUR/AUD is trying to resume the rebound from 1.6127 by breaking 1.6398. Intraday bias is mildly on the upside for 1.6478 resistance. Firm break there will argue that whole correction from 1.7062 has completed, and target 1.6844 resistance for confirmation. Nevertheless, break of 1.6278 minor support will turn bias back to the downside for retesting 1.6127 low.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 bring rebound. Break of 1.6844 will argue that this up trend is ready to resume through 1.7062 high.

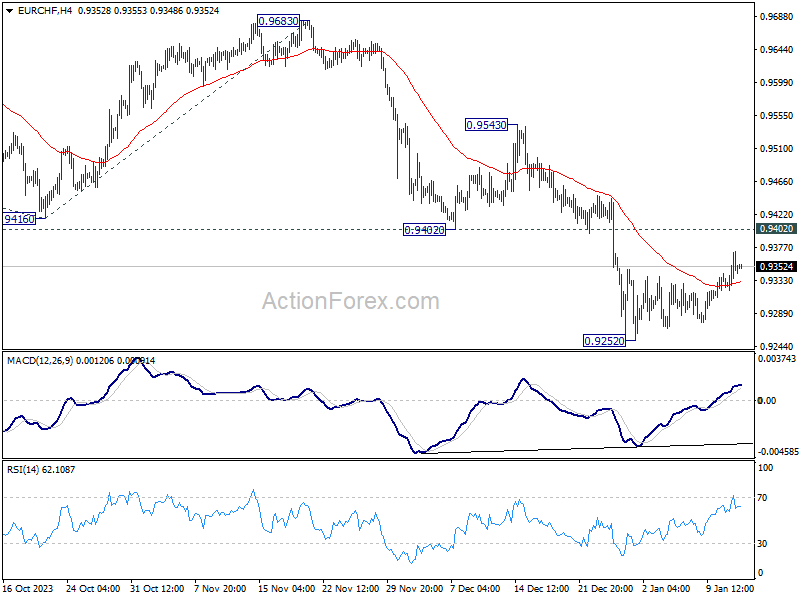

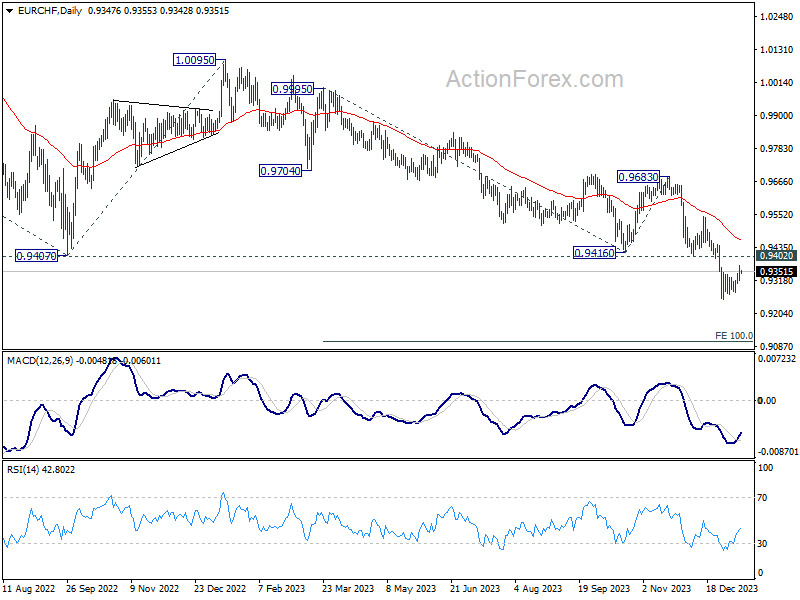

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9321; (P) 0.9348; (R1) 0.9375; More...

EUR/CHF recovered higher today but outlook is unchanged. Intraday bias stays neutral first and outlook remains bearish with 0.9402 support turned resistance intact. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

Dollar a Tad Softer in Uninspired Trading

Markets

Yesterday’s above-consensus US CPI numbers highlight the bumpy nature of the disinflationary process. It was reason enough for the likes of Barkin (Richmond Fed) and Mester (Cleveland Fed) to stay cautious. Both want more evidence with the latter stating that March is probably too soon for a rate cut. Goolsbee (Chicago) bluntly stated that the market was getting ahead of itself. The market reaction itself was muted with a kneejerk move higher in US yields quickly running into resistance. Failing to take out this week’s highs, a technical countermove occurred. Safe haven flows on rumours that the UK together with the US was about to carry out retaliatory missile strikes on Houthi targets extended the downleg. Net daily losses amounted to -3.2 (30-y) to -11.3 bps (2-y). German rate changes varied between -2.3 bps (2-y) and +0.8 bps (30-y). ECB’s Lagarde in an after-market speech said they are winning the inflation battle but joined her US colleagues in wanting confirmation from the data before switching the mindset to rate cuts. The Japanese yen erased previous losses on rising tensions in the Middle East. USD/JPY finished at 145.29 compared to an intraday high of 146.4. EUR/JPY’s adventure above 160 ended soon. EUR/USD experienced some CPI-induced volatility but in the end closed unchanged around 1.097. European stock markets fainted going into the close while Wall Street recovered from a weak open.

Oil prices gap higher this morning in response to the airstrikes. Brent is trading around $79.2/b. Equity markets trade mixed with Japan again outperforming. Stocks in China and South Korea lag. Taiwan is holding its nerves ahead of what are considered pivotal presidential elections this Saturday. The ruling Democratic Progressive Party wants to maintain the status quo vis-à-vis China and strengthen ties with western allies. Opposition candidates however seek to smoothen relations with the Chinese. European equities seem less bothered with geopolitics with futures pointing at a solid open. The dollar is a tad softer in uninspired trading. The economic calendar hasn’t much to offer to change that, unfortunately. Financial companies kick off the Q4 earnings season. US PPI’s are worth mentioning but matter only from an intraday perspective. From a technical point of view, EUR/USD 1.10 looks more prone for a test to the upside than 1.0875 to the downside. Yesterday’s setback has pushed the US 2-y yield back to the December lows of around 4.22%. This level has to hold for the technical picture not to weaken. The 10-y tenor continues to struggle around 4%.

News & Views

Bloomberg reports that Bank of Japan officials are likely to discuss cutting their growth and inflation forecasts when they meet next on January 23. A drop in oil prices could trigger a downward revision of CPI ex fresh food for fiscal year 2024 (starting in April) from 2.8% to 2.5%. In fiscal year 2025, the BoJ will continue to expect inflation below the 2% target. Officials are also likely to discuss a sharper cut in the growth forecast for this fiscal year after weaker-than-expected GDP figures in the third quarter, the sources said. The article strengthens market believe that the BoJ will continue pushing forward its real policy U-turn. Since the start of the year, this triggered new JPY weakness in combination with the rebound in core bond yields. EUR/JPY yesterday tested 62% retracement on the Nov/Dec correction lower at 160.07. USD/JPY made an attempt at 50% retracement on the same correction (146.08). Some safe haven flows related to the above mentioned US/UK strikes prevented a break higher, at least for now.

Chinese exports rose by 2.3% Y/Y in dollar terms in December, helped by favorable comparisons with a year ago when Covid ran through the country. Imports increased by 0.2% M/M, especially thanks to improved ties with Australia (25% increase). For the full-year 2023, Chinese exports dropped by 4.6% compared to record year 2022 marking a first decline since 2016. Full-year imports fell by 5.5% resulting in an $823bn trade surplus for 2023. Chinese inflation data were reported separately. CPI rose for the first time in three months, by 0.1% M/M, but the Y/Y-figure remains mired in negative territory (-0.3%). For 2023 as a whole, CPI inflation averaged only 0.2%. Core CPI held steady at 0.6% Y/Y in December. Factory-gate inflation (PPI) was negative for a fifteenth month running (-2.7% Y/Y), falling by 3% over 2023.

US and UK Launch Airstrikes on Yemen’s Houthis

In focus today

Following the airstrike launched by the US and UK against Houthi rebel target in Yemen overnight (see more below), geopolitics will be on top of the agenda.

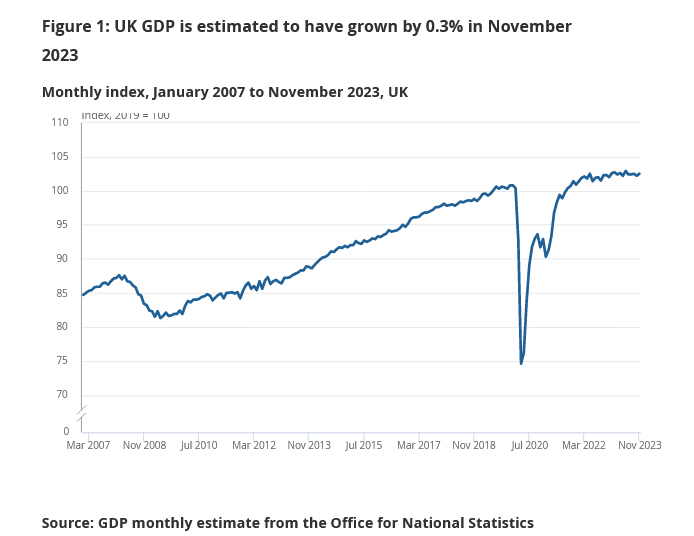

Today, in the UK, we get the monthly GDP estimate for November. It will be interesting to see whether it mirrors the positive momentum indicated by PMIs, which have hovered in expansionary territory the past months.

The US December PPI is also due for release today. Yesterday, both headline and core CPI picked up 0.3% m/m, which markets took as a hawkish signal, but with an overall muted impact.

In Sweden we get housing price statistics (CET 06.00) for December and the Riksbank's Deputy Governor Aino Bunge will attend an event at the Ekonomichefsdagarna conference organised by Kommunalekonomernas förening (KEF) to discuss the economic situation and current monetary policy.

We look to Asia over the weekend, as on Saturday Taiwan will elect a new President as well as parliament. In Taiwan, polls are not allowed 10 days before the election but the most recent surves show a pretty tight margin between DPP's William Lai and KMT's Hou Yu-ih. Lai leads with 36% support vs 31% for Hou. DPP is currently in power and a victory for Lai would mean more of the same with an independence leaning stance whereas a victory by Hou could ease tensions a bit as KMT has generally had a less confrontational stance towards Beijing, although still not being in favour of unification. Also if Lai wins he will have a weaker mandate than current president Tsai Ing-wen who got close to 60% of the votes in 2020 and DPP will likely lose the majority in the Taiwanese parliament.

Finally, early morning European time on Monday, China is expected to lower the policy rate, the Medium Lending Facility 1-year rate, by 10bp from 2.5% to 2.4%.

Economic and market news

What happened overnight: Geopolitics. Oil prices surged overnight, as the US and UK launched airstrikes on the Yemen Houthis, marking a significant escalation in the already tense situation around the Red Sea. The move was a response to the recent Houthi attacks on international shipping in the area, which has so far counted 27 attacks in the past two months, according to US officials. This has vastly reduced the number of containers passing through the Suez Canal, which have instead opted to sail the long way around Africa. As of this morning, Brent was up 1.9% at 78.9 USD/bbl., extending gains from yesterday whe Iran seized an oil tanker off the coast of Oman.

China. Headline CPI dropped again in December by 0.3% y/y, which was a little less than the -0.4% y/y expected by consensus. It was the third month in a row with deflation in headline CPI but again it was mainly driven by a decline in food prices (-3.7%). Core inflation (ex food and energy) was flat at 0.6% y/y so we are still not seeing broad-based deflation. Lower food prices is actually good for consumers as it lowers living costs and thus improves purchasing power. Chinese trade data were also better than expected showing a rise in exports from 0.5% y/y to 2.3% y/y (consensus 1.5% y/y). Since export prices are falling it corresponds to a rise in real terms of around 8%. It highlights that a) the headwind to the Chinese economy from weak exports is fading and b) the global manufacturing recession is easing. Imports rose from -0.6% y/y to 0.2% y/y (consensus -0.5% y/y).

Bank of Japan. Overnight, reports surfaced that the Bank of Japan is said to revise forecasts for inflation and growth down for the fiscal year 2024 (starting in April) at its meeting on 22-23 January. However, we stress that the projections further out are the ones of significance, of which there are no reports of changes. Officials continue to expect inflation to re-accelerate after a brief slowdown. We therefor do not see this as a gamechanger, although it highlights that the BoJ is likely to stay on hold at the January meeting. We expect the BoJ to exit the negative interest rate policy in April 2024.

What happened yesterday:

US CPI: The most anticipated news of the day was the release of the US CPI for December. Both surprised slightly to the upside, with headline printing at 0.3% m/m (cons. 0.2%), and core at 0.31% m/m (cons. 0.3%). Both the dollar and 10Y treasury yields gained on release, as markets tempered expectations of a March rate cut, but the movements more or less reversed over the day, with EUR/USD marginally down and yields flat. We got hawkish signals from Cleveland's Mester, who said that a March cut would be too soon. On balance, markets are still pricing in 6 rate cuts during the course of the year, which we think is too optimistic, and instead expect 4 rate cuts, with the first in March. See also Global Inflation Watch - Diverging Signals in December, 12 January for an overview of global latest inflation trends.

Energy markets: European gas prices declined about 0.5% in yesterday's session. After a mild start to the winter the freezing spell of the past week has been a test for the European gas supply, and it looks to have passed. As of Monday, the EU's gas storage was still 83% full, giving confidence that a lack of gas is unlikely to be a large problem going forward.

Riksbank: Finally, The Riksbank's Per Jansson said in a speech that inflation pressures have come down and that he is convinced that interest rates had peaked. He also signalled that the SEK is still on the Riksbank's radar, with the comment: "But exchange rates can fluctuate rapidly [...] and they can in turn affect inflation prospects".

Equities: Equities held tight on Thursday, although investors had several reasons to sell: Inflation was a little too hot, job data a little too strong and Fed speeches on the hawkish side. However, S&P 500 was down only -0.1% and VIX even dropped slightly. The limited equity impact is interesting and quite positive. Short-term positioning and sentiment is not as stretched long as one could have thought. That being said, investors were not happy. Defensives outperformed and yield sensitive sectors such as utilities and real estate were the losers of the day. Rotation story in the Nordics as well with high multiple stocks like Genmab or EQT selling off and investors piling into defensives like Carlsberg and Coloplast, up +4%. The Japanese rally is continuing this morning after another round of falling inflation figures. European futures are higher this morning and US a notch lower.

FI: The key highlight yesterday, the US CPI figure, yielded a whipsaw market reaction. While initially sending yields higher on a better than expected print, the 2y UST was up by 5bp, however it was quickly reversed. By the end of the day, European yields were virtually unchanged in the 10y point. Following the change of the10y Benchmark bond (Feb 2034), the Italy-Germany spread now stands at 157bp. Curves steepened from the front end, adding 2bp to the rate cut priced for this year to 141bp. Intraday though, markets added slightly more on the back of headlines suggesting that ECB's Vujcic said that once rates cuts starts, 50bp cuts cannot be excluded. Looking at the details though, he said that in his view they move in 25bp steps in an ideal world, which the media headline did not reflect. Yesterday afternoon, Fed's Mester said that a March rate cut is probably too early. Upon announcement of the 4.229% yield of yesterday's 30y 21bn UST supply, 30y yields reacted with a 5bp rally. Tonight, Austria and Sweden are up for a review by DBRS.

FX: Yesterday proved another quiet session in FX markets. The CPI-induced rally in USD was short-lived and EUR/USD remains within the 1.09-1.10 range. SEK traded slightly on the back-foot with EUR/SEK moving above the 11.25-level which contributed to lifting NOK/SEK back closer to parity amid NOK staying little changed. The recent JPY sell-off eased yesterday with USD/JPY now trading just above 145 but still more than 4 figures higher compared to new year.

UK GDP grew 0.3% mom in Nov, but down -0.2% in the three month period

UK GDP grew 0.3% mom in November, above expectation of 0.2% mom. Services output rose 0.4% mom. Production output grew 0.3% mom. Construction sector fell-0.2% mom.

However, in the three months to November, GDP fell -0.2% compared with the prior three months period to August. Services showed no growth, production output fell by -1.5% and construction fell by -0.6% over the same period.

US CPI Bounce Goes Unheard, Focus on Bank Earnings

Yesterday’s US inflation report wasn’t exactly ideal. The headline inflation rose more than expected to 3.4% from 3.1% printed a month earlier. Shelter, electricity, and food prices drove the overall CPI index higher in December. Especially, the shelter costs increased by more than 6%. But if you don’t count food and energy price inflation, core inflation eased to 3.9% during the same month. And well, if you start getting the shelter cost off the calculation, the numbers were quite good. Of course, the metrics that disregard food, energy and shelter prices – like the core and supercore inflation – make little sense to Mr. and Ms. Everyone, as everyone eats, everyone uses energy and everyone needs a shelter. Yet, for the Federal Reserve (Fed), these items have volatile prices, so they prefer looking past these important categories. While doing so, inflation eased. Also, note that a rise in car prices also added to the inflationary pressures last month. But their weight is lower in the calculation of the PCE index. That’s why the Fed’s favourite inflation gauge – the PCE index which will be released by the end of the month - will likely be trending closer to the 2% target.

But all in all, yesterday’s inflation report was less than ideal, and the market reaction was mixed. The US 2 and 10-year first rose then fell, whereas you would expect a swift shift in dovish Fed expectations following a bigger-than-expected jump in US headline inflation. The equities were up and down, and the S&P500 closed the session very slightly in the negative while Nasdaq eked out even a small gain at yesterday’s close.

Disinflation remains the base case scenario for this year, housing costs are expected to fall – at some point – and that could counterweight the rising shipping costs caused by the Red Sea tensions and low water levels in the Panama Canal that also threaten food deflation that we saw last year. Yet some hawkish voices are rising at the Fed, at the start of this year. Fed’s Loretta Mester said that it’s probably too early to cut rates. Mr. Barkin also repeated that he’s looking for more evidence that inflation is headed toward the 2% target.

But it’s obvious that investors are not willing to trade the bad smell for now.

The US dollar index is under pressure after yet a stronger-than-expected inflation report, the EURUSD rebounded lower after hitting the 1.10 mark, as the euro bulls, or the dollar bears found no reasonable conviction to carry the rally above the 1.10 mark, and gold rebounded after hitting the 50-DMA, near $2013 per ounce. Activity on Fed funds futures still gives more than 70% chance for the first Fed rate hike to happen in March. But the Fed won’t find enough evidence that inflation will ease toward the 2% target as early as March. Consequently, there should be a readjustment in market expectations, and we will see the stock and bond prices make a corrective move to the downside.

Earnings season kicks off

Over the next few weeks, attention will be directed toward company earnings, and we will start digesting the earnings starting from the financial sector. The SPDR’s financials closed last year with more than a 20% rally thanks to optimism that the Fed would start cutting the interest rates sooner rather than later. The massive rebound in US long-term papers had a substantial positive impact on their balance sheets. Yet expectations for the US banks are not necessarily positive. First, the banks are expected to announce a 21% decline in their profits compared to the same period last year, as a result of higher costs to attract and maintain deposits in an environment of high inflation and higher Fed rates. Then, credit card delinquencies continue to rise. US consumer spending remained robust yet … people are not buying stuff that they can afford. The bad loans are therefore expected to be on the rise. On the corporate side, investment banking revenues will likely remain weak given that the M&A activity was subdued last year. And well, if the Fed starts cutting the interest rates and the economy slows, the banks will start seeing their net profit margin shrink. Therefore, the FactSet projections indicate that the S&P500’s financial sector could reveal the 4th highest yoy earnings decline among all 11 sectors for Q4, with an estimated downturn of -3.1%. If that’s the case, a correction in the S&P500 financials would only make sense after a more than 20% rally recorded in just two months. Anyway, I stop here and let the bank earnings tell the story.

Same story, different day

In energy, crude oil rebounded 2% yesterday and is better bid this morning on the back of rising tensions in the Red Sea. This time the news that Iran captured an oil tanker off the cost of Oman is pushing prices higher. Yet the Red Sea tensions have so far been insufficient to push the price of a barrel sustainably higher. Therefore, price rallies into and above the $75pb level could be interesting top selling opportunities for those willing to see the price of a barrel fall below the $70pb level.

On the corporate level, consolidation in the US energy sector is now shifting toward the nat gas companies. Chesapeake Energy agreed to merge with Southwestern Energy Company in an all-stock transaction worth $7.4bn. Chesapeake’s price rose 3% while Southwestern Energy lost 2.5%, and efficiencies could support a further correction for Chesapeake.

Nat gas futures have been rising in the US, yet the European TTF futures continue to fall despite snow and harsh winter weather. It is because the European gas storage is so full that some say that winter is already over in the gas market.