Sample Category Title

China’s CPI improved to -0.3%, deflation persists for the 3rd month

China's CPI reflected a modest improvement in December, rising from -0.5% yoy to -0.3% yoy, slightly better than the expected -0.4% yoy. Despite this improvement, December marks the third consecutive month of negative CPI readings, indicating ongoing deflationary pressures in the Chinese economy. The month-on-month CPI also saw a shift, registering 0.1% increase compared to the -0.5% decline in November. Core CPI, which excludes the typically volatile food and energy prices, remained steady at 0.6% yoy, mirroring November's figure.

NBS noted that pork prices continued to be a significant factor influencing the year-on-year CPI, with a decrease of -26.1% yoy , but narrowd from November's -31.8% yoy decline. Services inflation demonstrated a steady rise, with notable increases in tourism and hotel accommodation prices, which surged by 6.8% yoy, and 5.5% yoy, respectively.

PPI also improved from -3.0% yoy to -2.7% yoy, but fell short of the anticipated -2.5%. This marks the 15th consecutive month of decline in the PPI. NBS attributed this continued decline in PPI to several factors, including drop in international oil prices and lack of demand for certain industrial products.

Fed’s Goolsbee: January too soon for committing to future rate cuts

Chicago Fed Austan Goolsbee has highlighted the critical role of ongoing inflation data in shaping Fed's future interest rate decisions. In an interview with Reuters, Goolsbee underlined that it is premature to make definitive decisions about rate adjustments at this juncture.

Goolsbee's said, "I still think that the primary determinant of when and how much rates should be cut will be driven off what's happening to the inflation data, and are we meeting the mandate goals."

He also emphasized the importance of not rushing into policy decisions based on incomplete data sets. "When we have weeks or months of data to come, I don't like tying our hands ... We don't make decisions about March, June, and whatever, in January," he remarked.

Regarding the December CPI reading, Goolsbee noted that it was largely in line with expectations. However, he observed some variations within the data, specifically mentioning that services inflation was cooler than anticipated, while housing inflation was slightly higher.

Fed’s Barkin watching goods-services cost divide

Richmond Fed President Thomas Barkin told reporters after a speech overnight that the December CPI report was "about as expected. He noted a deceleration in the price rise for goods, while shelter and services costs continue to escalate at a more robust pace.

Barkin highlighted the growing disparity between the costs of goods versus shelter and services. He expressed caution about this divide, emphasizing the importance of vigilance in this area.

"This gap between services and shelter and goods is one that I am watching carefully," he stated. His concern is rooted in the potential consequences of a shift from deflationary cycle in goods to a scenario where the economy is predominantly burdened by the rising costs of shelter and services.

"You would not want a goods deflationary cycle to end and find yourself disproportionately bearing the cost of shelter and services," Barkin said.

Fed’s Mester: March too early for rate cut, inflation fight continues

Cleveland Fed President Loretta Mester, in an interview with BloombergTV overnight, emphasized that March might be too soon to consider a rate cut, citing ongoing efforts to combat inflation.

Mester expressed her view that more evidence is needed before considering a reduction in interest rates. "March is probably too early in my estimation for a rate decline because I think we need to see some more evidence," she stated,

The December CPI report released yesterday, according to her, is a clear indication that "there is more work to do," necessitating the maintenance of restrictive monetary policy. Nevertheless, she reassured that the CPI report does not suggest progress in inflation stall out.

Mester also pointed out that the risks associated with monetary policy have become more balanced. The primary focus for this year, as she outlined, is to calibrate policy effectively to maintain healthy labor markets while continuing the process of bringing inflation back to the 2% target.

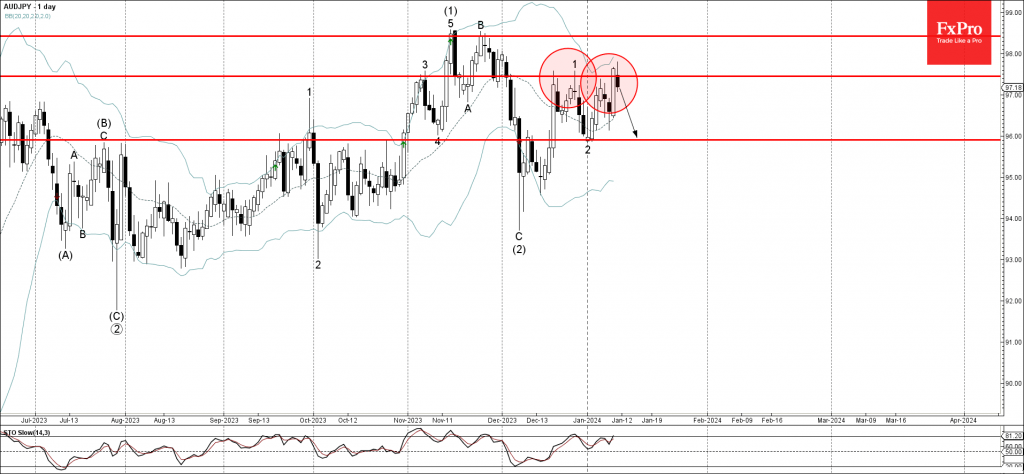

AUDJPY Wave Analysis

- AUDJPY reversed from resistance level 97.45

- Likely to fall to support level 96.00

AUDJPY currency pair recently reversed down from the resistance level 97.45 (which has been reversing the pair from the middle of December).

The resistance level 97.45 was strengthened by the upper daily Bollinger Band.

AUDJPY can be expected to fall further to the next support level 96.00 (low of the previous Morning Star and wave 2 from the end of December).

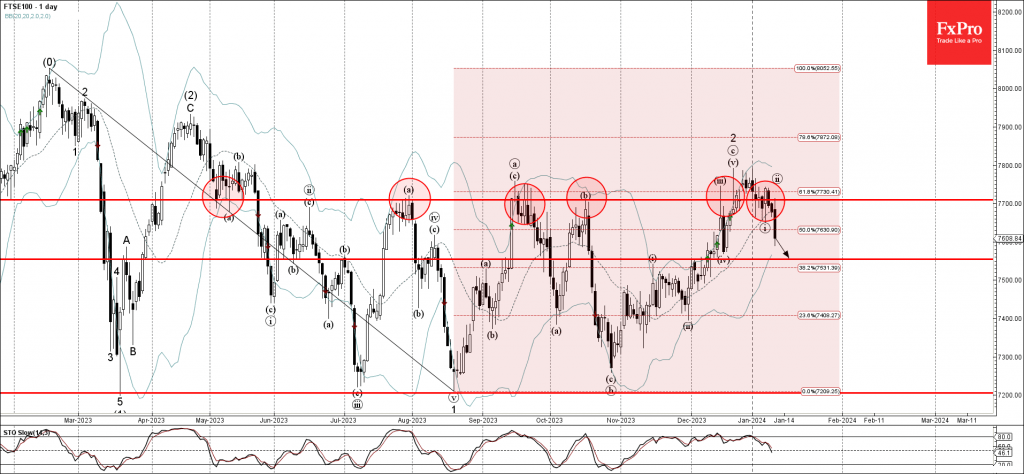

FTSE 100 index Wave Analysis

- FTSE 100 index reversed from resistance level 7700.00

- Likely to fall to support level 7550.00

FTSE 100 index recently reversed down from the multi-month resistance level 7700.00 (which has been reversing the pair from the end of July).

The resistance level 7700.00 was strengthened by the upper daily Bollinger Band and by the 61.8% Fibonacci correction of the downward impulse from April.

FTSE 100 index can be expected to fall further to the next support level 7550.00 (former resistance from November).

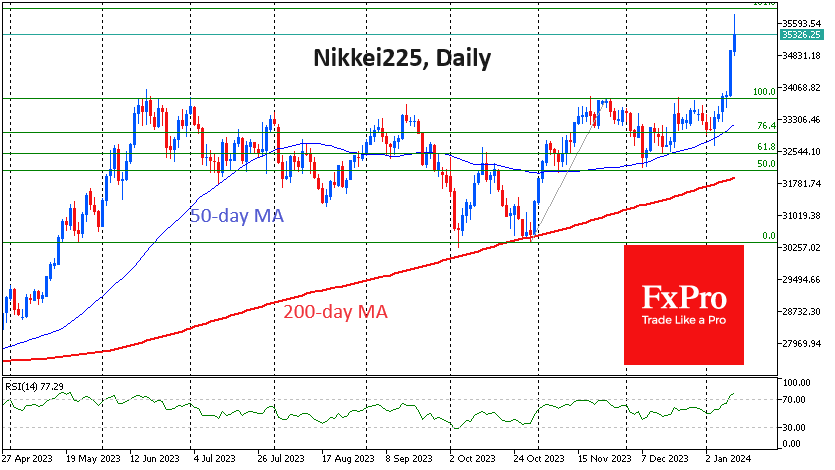

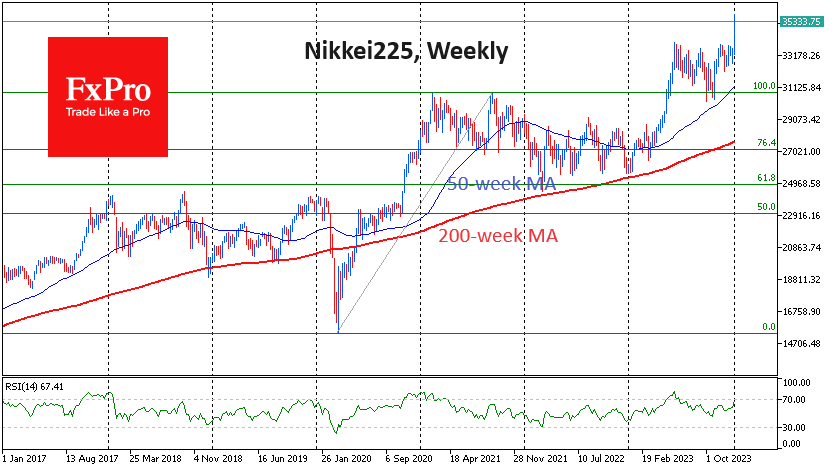

Nikkei225 Needs a Breather But Hardly Done Ascending

Japan’s Nikkei225 index hit new highs since February 1990 on Thursday morning and climbed above 35000. The rise accelerated sharply this week after breaking above the 34000 level, which acted as resistance in the second half of 2023.

The fundamental reason for buying was the dramatic drop in expectations that the Bank of Japan would unwind its ultra-soft monetary policy. The 1 January earthquake and a faster slowdown in consumer inflation have reversed sentiment in the markets.

On the tech analysis side, the Nikkei225 reversed to the upside after touching the 50-day moving average, as it has done repeatedly since November.

However, the move became excessive on Wednesday and Thursday due to likely short covering after breaking important resistance.

In the short term, the index looks overbought, setting up for a local correction in the coming days. However, the big bull cycle in Japanese equities seems to be far from over.

The Nikkei225 doubled from the 2020 lows to the 2021 highs, and the 2022 decline has corrected this rally to a classic 61.8% of the original rise. The buying intensification in 2023 marked a renewal of multi-year highs and a correction to the 2021 peaks.

The development of this pattern opens the door for gains above 40,300 (+14% from current levels) within 12-18 months.

The short-term outlook is less certain as Nikkei225 is overbought to the maximum since May 2022 on RSI on daily charts. Also, the Japanese equity index is close to the 161.8% point of the October-November upside amplitude. This sets up a new wave of profit-taking on the approach to 36000, which is quite close to Thursday’s peaks, forming a not-so-attractive risk/reward ratio.

Sunset Market Commentary

Markets

Trading initially was a long-drawn countdown to today’s US December CPI. Investors tentatively positioned for a rather soft report, with US yields easing 3-4 bps before publication of the data. The report brought a modest upside ‘surprise’. Headline inflation increased 0.3% M/M and 3.4% Y/Y from 3.1% in November (3.2% expected). Core inflation excluding food and energy was close to expectations at 0.3% M/M and 3.9% Y/Y (4.0% in November, 3.8% expected). Looking into the details, food price inflation eased to 0.2% M/M. Energy prices rose 0.4%. Services prices still added 0.5% M/M with shelter an important contributor (0.5% M/M). A 0.3% M/M dynamics for both core and headline measures, suggests that a deceleration to bring inflation sustainably back to the 2.0% target isn’t guaranteed yet. Aside from the higher than expected CPI, weekly jobless claims (202 k) remained at very low levels, suggesting ongoing labour market tightness. Even so, the reaction on US interest rate markets remained modest. Yields briefly jumped into green territory, but the move had no strong momentum. US yields currently are again trading little changed across the curve. Markets still see a >60% chance of a 25 bps Fed rate cut already in March. The US 10-y yield still struggles to hold north the 4.0% barrier (4.03%). Late today, governors Mester and Barkin have a chance to give an instant assessment. The US Treasury will conclude this week’s auctions with the sale of $21 bln 30-y bonds. With few important data scheduled on this side of the Atlantic, German yields are ceding between 4 bps (2-y) and 2.0 bps (30-y). A mild reaction on global bond markets also prevented a sustained decline in major equity indices. The Eurostoxx 50 moved into negative territory post the CPI release, but currently trades little changed. US equites struggle to maintain small opening gains.

On FX, the soft bond market reaction also capped a tentative attempt of the dollar to move higher. The DYX index (102.46) is going nowhere. EUR/USD eased to 1.0950, but first important support at 1.0877 stays out of reach. USD/JPY (146.10) again outperforms; with the pair setting a new YTD top. After a nice rebound of sterling against the euro last week, EUR/GBP today held a tight sideways range, close to, mostly slightly north of the 0.86 big figure.

News & Views

The Czech koruna slipped today. EUR/CZK moved from 24.58 to 24.63 though left intraday highs of around 24.68. CZK weakness followed a big miss in December CPI numbers. The monthly pace dropped from 0.1% in November to -0.4% vs an expected stagnation. This drove the yearly figure down from 7.3% to 6.9%, matching the September 2023 low before inflation accelerated again due to statistical base effects. The CNB was expecting 7%. Core inflation slowed in line with the CNB’s autumn forecast, to 3.6%. The monthly decline was driven by easing prices in domestic fuels (-4.7%), seasonal goods (-2.3%), transport (-1.1%) as well as food (-1.4%). Housing and utility costs inflation decelerated to 0.2%. These carry a big weight in the index. Today’s release brings another CNB rate cut closer in February although the real litmus test will be in January, when companies implement their usual repricing. As the previously mentioned base effects fall out of the equation, however, the CNB expects CPI to drop towards to the upper bound of the 2% +/- 1 ppt target range. Czech swap yields tumble up to 13 bps at the front end of the curve with money markets all but pricing in a 50 bps cut in February. In December last year, the CNB started cautiously with a 25 bps step.

Oil prices jumped towards $78/b (Brent) today. The UK Maritime Trade Operations said an oil tanker was hijacked by people in military-style uniforms before altering course to Iran. It’s a reminder of the tense situation in the broader Middle East region, where frequent attacks by Yemen’s Houthi militants also forced shipping companies to change their usual trajectory via the Red Sea and Suez Canal to go via the much longer route around South Africa. The CEO of a shipping giant responsible for about a fifth of ocean freight said the situation could last for months with implications for global supply. Container freight benchmark rates have risen sharply over the recent weeks. These indicators were closely watched back in the Covid driven supply chain disruption days. While they still trade well below the peak levels back then, freight rates have more than doubled from what were historically more normal levels end 2023.

US: Core Inflation Inches Down to 3.9% in December

The Consumer Price Index (CPI) rose 0.3% month-on-month (m/m) in December, ahead of the consensus forecast calling for a more modest gain of 0.1% m/m. CPI rose 3.4% on a year-over-year basis – up from 3.1% in November.

- After having declined in each of the two months prior, energy prices inched higher by 0.4% m/m in December, due to in uptick in electricity costs (1.3% m/m) and slightly higher prices at the pump (+0.2% m/m). Food prices matched last month's gain of 0.2% m/m, pushing the 12-month change down to 2.7%.

Excluding food & energy, core prices rose 0.3% m/m, in line with the consensus forecast. The twelve-month change fell 0.1 percentage points to 3.9% – the slowest pace of growth since May 2021 – while the three-month annualized rate of change dipped to a softer 3.3%.

Core service prices rose 0.4% m/m – a modest deceleration from November's 0.5% gain. Shelter costs were up a 'soft' 0.5% m/m – unchanged from November – as rent of primary residence (+0.4% m/m) and owners' equivalent rent (+0.5% m/m) both notched sizeable gains. Non-housing services decelerated on a monthly basis, but still grew by a relatively strong 0.4%, while the 12-month change continues to hover at an elevated 3.9%.

Goods prices were flat in December, snapping six consecutive months of declines.

Key Implications

No huge surprises in the December CPI report. While the monthly gain on headline inflation came in a touch above expectations, the more important core measure was bang-on consensus. Importantly, both the three-and-six-month annualized rates of change (at 3.3% and 3.2%, respectively) on core sit well below the twelve-month change, suggesting a further deceleration in the months ahead.

Today's inflation report is unlikely to alter the FOMC's near-term policy stance. Although considerable progress on the inflation front has been made over the past year, imbalances in the labor market remain and if left unchecked, threaten to stall the disinflationary process. As a result, Fed officials will likely need to see more compelling evidence that the labor market is cooling, and that inflation remains on a sustained downward path towards 2% before pulling the trigger on rate cuts. This is unlikely to happen until mid-year.